Consumer Demographics, Household Income & Expenditure in Wollongong

VerifiedAdded on 2021/05/31

|12

|2155

|24

Report

AI Summary

This report provides a detailed demographic analysis of Wollongong City, NSW, Australia, focusing on population characteristics, household structure, income distribution, and expenditure patterns. It highlights that the estimated resident population is 213,841, with a significant portion being couples with children. The report examines dwelling types, noting a mix of medium and high-density housing, and analyzes household income distribution, revealing income inequality through the Gini coefficient. It also explores household expenditure on mortgage and rent, comparing Wollongong to regional NSW, and concludes with a summary of household net worth based on tenure, landlord type and life cycle groups. Desklib offers a platform for students to access this and other solved assignments for study purposes.

Running head: CONSUMER DEMOGRAPHICS

CONSUMER DEMOGRAPHICS

Name of the Student:

Name of the University:

Authors Note:

CONSUMER DEMOGRAPHICS

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONSUMER DEMOGRAPHICS

Demographic Profiles:

Wollongong City is in the Illawarra area of New South Wales. This region is almost 80

kilometer south of Sydney. The city community profiles helps in providing a demographic

analysis of Wollongong and its suburb regions. The population of the region as per the Estimated

Resident Population (ERP) is 213,841and the nearby land area is around 68,384 (Pang, Lin and

Jiang 2015). The population destiny for the area is around 3.13 people per hectare. The city

offers magnificent natural environment that ranges from untouched rainforest to dramatic sea

cliffs and sandy beaches. All age group of people are found in the country. Large percentage of

the area in the city includes outlying towns, rural localities and suburbs.

The people in the area are mostly of average age of about 35 to 40 years. Population of

Aboriginals and Torres Strait Islander includes 2.6% of total population. 30% of population in

the region is couples with children. Older couples without children include 11% of the total

population (Wilkins 2015). Almost 20% of the people in the region are qualified and holds a

degree in University. Average household income of the people on a weekly basis is around $

1,335. The mortgage weekly repayment on the average basis includes $ 449 (Finlay and Price

2015). Unemployment rate is usually low at Wollongong and participation of labor forces is

high. Couples with children are more of the dominant population of Wollongong. Male

population is higher than female population in the area. Majority of population in the area speaks

languages other than English at their homes.

Demographic Profiles:

Wollongong City is in the Illawarra area of New South Wales. This region is almost 80

kilometer south of Sydney. The city community profiles helps in providing a demographic

analysis of Wollongong and its suburb regions. The population of the region as per the Estimated

Resident Population (ERP) is 213,841and the nearby land area is around 68,384 (Pang, Lin and

Jiang 2015). The population destiny for the area is around 3.13 people per hectare. The city

offers magnificent natural environment that ranges from untouched rainforest to dramatic sea

cliffs and sandy beaches. All age group of people are found in the country. Large percentage of

the area in the city includes outlying towns, rural localities and suburbs.

The people in the area are mostly of average age of about 35 to 40 years. Population of

Aboriginals and Torres Strait Islander includes 2.6% of total population. 30% of population in

the region is couples with children. Older couples without children include 11% of the total

population (Wilkins 2015). Almost 20% of the people in the region are qualified and holds a

degree in University. Average household income of the people on a weekly basis is around $

1,335. The mortgage weekly repayment on the average basis includes $ 449 (Finlay and Price

2015). Unemployment rate is usually low at Wollongong and participation of labor forces is

high. Couples with children are more of the dominant population of Wollongong. Male

population is higher than female population in the area. Majority of population in the area speaks

languages other than English at their homes.

2CONSUMER DEMOGRAPHICS

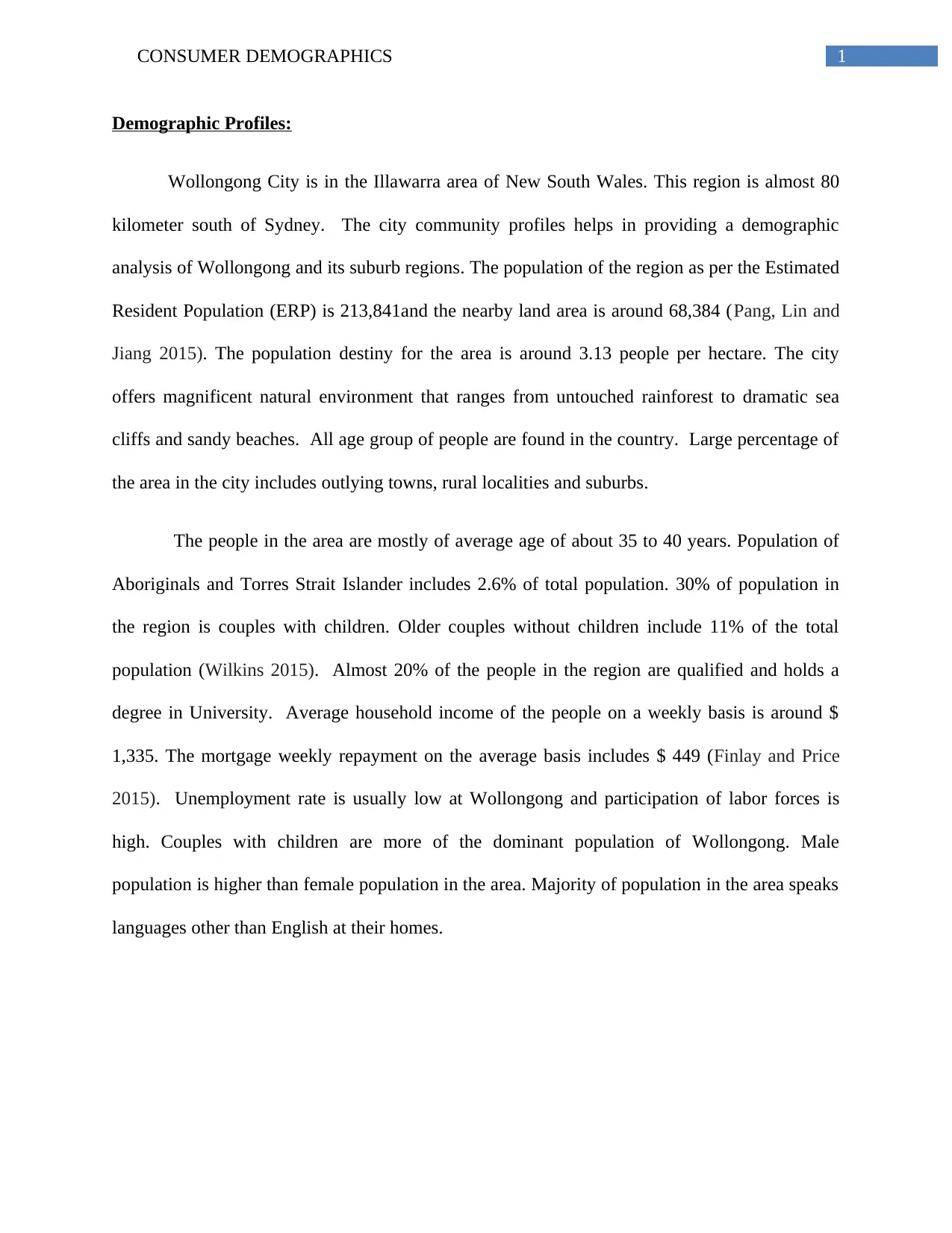

Figure I: Wollongong estimated Population

Source: (Pang, Lin and Jiang 2015)

Household structure and tenure of dwelling related information:

Dwelling type in The Wollongong region is as crucial determinant to know the role and

functions of the residential. Huge concentration related to higher density dwellings is more likely

to attract smaller households and young adults. In Wollongong, almost 31% of the dwelling is of

medium or high density. The dwelling types of the individual are mostly private in form. The

tenure type of dwelling is maximum mortgaged while fully owned is very less. The housing

structure or separate house is more and people dwelling over there often opt for renting.

Separate, larger or detached dwellings are more likely to attract the perspectives families. The

residential built form of the area often showcases the market opportunities as well as its planning

policies. Denser forms of housing are built around the employment centered and public transport

Figure I: Wollongong estimated Population

Source: (Pang, Lin and Jiang 2015)

Household structure and tenure of dwelling related information:

Dwelling type in The Wollongong region is as crucial determinant to know the role and

functions of the residential. Huge concentration related to higher density dwellings is more likely

to attract smaller households and young adults. In Wollongong, almost 31% of the dwelling is of

medium or high density. The dwelling types of the individual are mostly private in form. The

tenure type of dwelling is maximum mortgaged while fully owned is very less. The housing

structure or separate house is more and people dwelling over there often opt for renting.

Separate, larger or detached dwellings are more likely to attract the perspectives families. The

residential built form of the area often showcases the market opportunities as well as its planning

policies. Denser forms of housing are built around the employment centered and public transport

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONSUMER DEMOGRAPHICS

nodes. In the year 2016, separate houses are around 67.3% (Bolton et al. 2018). Medium density

is generally higher than tan the high density type of dwelling. Occupied private dwellings in the

area are maximum. The total number of dwellings in the region is estimated to grow up to 95,149

in the year 2026. The average household size is decreasing from the rate of 2.54 to 2.51 by the

end of 2026. The number of household during this period has increased at an alarming rate and

the average number of individuals. The dwelling occupancy rate has risen up to 95.89%. It is

expected that new dwelling will also increased at a rapid pace for the year 2016.

Household Income Distribution and Inequality:

Household income is one of the main elements to determine the socio-economic status of

a particular region. The people with need of assistance or disability are a vital indicator of the

level of ability so that they can efficiently participate in the economy and society of Australia.

Most of the population in the region has a weekly population of around $650-$799. During the

year 2016, it was ascertained that larger proportion of individuals needs assistance with high

household incomes. Such as people earning income that ranges up to $2, 500 each week and

more. Higher proportion in low income households consisting of earning that is less than $650

each week. In Wollongong City, 10.7% of the overall population earned an overall income of

around $1,750 or more each week for the year 2016 (Rowley et al. 2107). The household

income level of the people are usually not comparable over time and due to influences related to

economic changes like inflation and wage level fluctuations. Through income quartiles the

relative income earning capabilities can be easily compared over time. Through the analysis of

income distribution for the people it is evaluated that a greater proportion of individuals in the

households has highest income quartile. Moreover, greater proportion is seen in the lowest

income quartile. The most vital change in the Wollongong City is seen between the year 20016

nodes. In the year 2016, separate houses are around 67.3% (Bolton et al. 2018). Medium density

is generally higher than tan the high density type of dwelling. Occupied private dwellings in the

area are maximum. The total number of dwellings in the region is estimated to grow up to 95,149

in the year 2026. The average household size is decreasing from the rate of 2.54 to 2.51 by the

end of 2026. The number of household during this period has increased at an alarming rate and

the average number of individuals. The dwelling occupancy rate has risen up to 95.89%. It is

expected that new dwelling will also increased at a rapid pace for the year 2016.

Household Income Distribution and Inequality:

Household income is one of the main elements to determine the socio-economic status of

a particular region. The people with need of assistance or disability are a vital indicator of the

level of ability so that they can efficiently participate in the economy and society of Australia.

Most of the population in the region has a weekly population of around $650-$799. During the

year 2016, it was ascertained that larger proportion of individuals needs assistance with high

household incomes. Such as people earning income that ranges up to $2, 500 each week and

more. Higher proportion in low income households consisting of earning that is less than $650

each week. In Wollongong City, 10.7% of the overall population earned an overall income of

around $1,750 or more each week for the year 2016 (Rowley et al. 2107). The household

income level of the people are usually not comparable over time and due to influences related to

economic changes like inflation and wage level fluctuations. Through income quartiles the

relative income earning capabilities can be easily compared over time. Through the analysis of

income distribution for the people it is evaluated that a greater proportion of individuals in the

households has highest income quartile. Moreover, greater proportion is seen in the lowest

income quartile. The most vital change in the Wollongong City is seen between the year 20016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONSUMER DEMOGRAPHICS

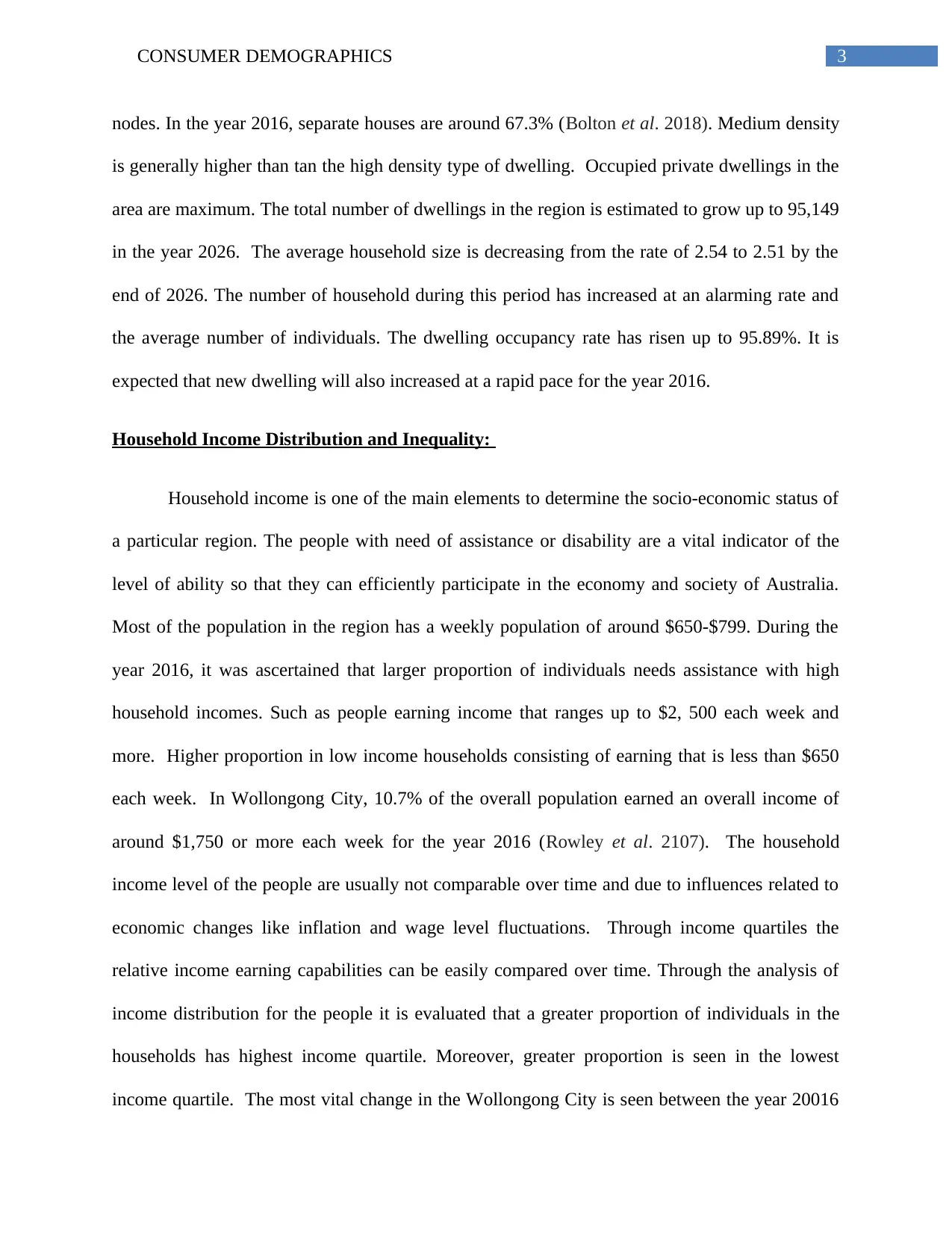

and 2011. People needing assistance that was seen in the medium lowest quartile was increased

by 651 individuals (Milner et al. 2015).

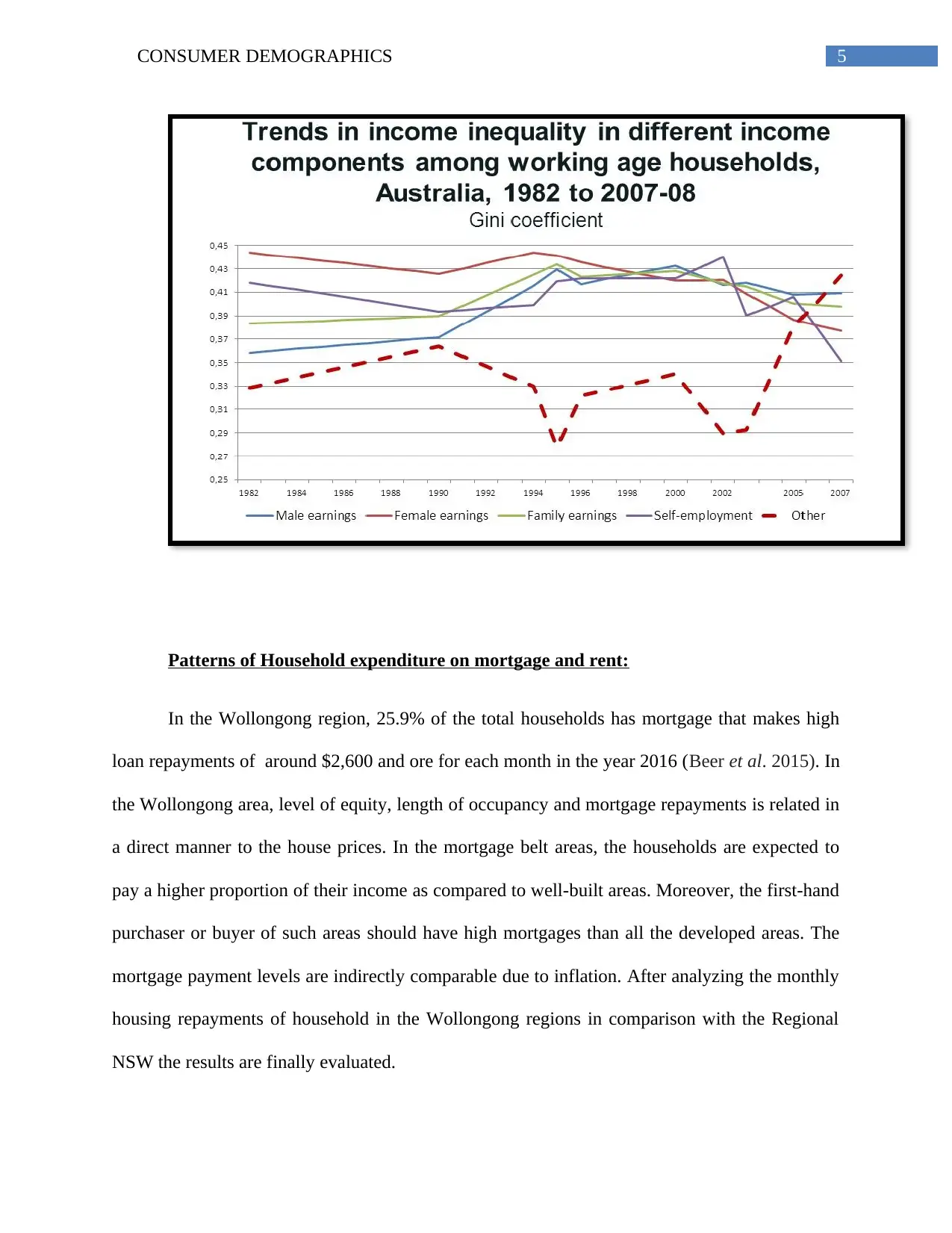

The Gini coefficient is the measure for inequality and is used to calculate the income

distribution of households or individual within an economy. Gini coefficient lies between zero

and unity. The higher is the level of Gini coefficient, more uneven will be the distribution of

income. The Gini coefficient for Wollongong region in Australia is expected to be 0.337.The

Gini coeffiecient is highly sensitive to high values. Since the last twenty years, the income of the

average household has increased by 60%. While the income of the other quintile has also

increased by 74%.

and 2011. People needing assistance that was seen in the medium lowest quartile was increased

by 651 individuals (Milner et al. 2015).

The Gini coefficient is the measure for inequality and is used to calculate the income

distribution of households or individual within an economy. Gini coefficient lies between zero

and unity. The higher is the level of Gini coefficient, more uneven will be the distribution of

income. The Gini coefficient for Wollongong region in Australia is expected to be 0.337.The

Gini coeffiecient is highly sensitive to high values. Since the last twenty years, the income of the

average household has increased by 60%. While the income of the other quintile has also

increased by 74%.

5CONSUMER DEMOGRAPHICS

Patterns of Household expenditure on mortgage and rent:

In the Wollongong region, 25.9% of the total households has mortgage that makes high

loan repayments of around $2,600 and ore for each month in the year 2016 (Beer et al. 2015). In

the Wollongong area, level of equity, length of occupancy and mortgage repayments is related in

a direct manner to the house prices. In the mortgage belt areas, the households are expected to

pay a higher proportion of their income as compared to well-built areas. Moreover, the first-hand

purchaser or buyer of such areas should have high mortgages than all the developed areas. The

mortgage payment levels are indirectly comparable due to inflation. After analyzing the monthly

housing repayments of household in the Wollongong regions in comparison with the Regional

NSW the results are finally evaluated.

Patterns of Household expenditure on mortgage and rent:

In the Wollongong region, 25.9% of the total households has mortgage that makes high

loan repayments of around $2,600 and ore for each month in the year 2016 (Beer et al. 2015). In

the Wollongong area, level of equity, length of occupancy and mortgage repayments is related in

a direct manner to the house prices. In the mortgage belt areas, the households are expected to

pay a higher proportion of their income as compared to well-built areas. Moreover, the first-hand

purchaser or buyer of such areas should have high mortgages than all the developed areas. The

mortgage payment levels are indirectly comparable due to inflation. After analyzing the monthly

housing repayments of household in the Wollongong regions in comparison with the Regional

NSW the results are finally evaluated.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONSUMER DEMOGRAPHICS

Overall, 20% were paying very low repayments whereas 25.9% of households were

giving high mortgage repayments. The major differences between Wollongong NAD Regional

NSW were:

High percentage of people between $ 3,000 to $3,999, which is 11% more as compared to

6.2%.

High percentage of individuals of $ 2,600 to $2,999, which is 9.5% compared to 6.1%

(Brown and Gray 2015)

In Wollongong area, the medium highest group was the largest quartile and comprises of

at least 29% 0f the overall households with mortgages. Wollongong City’s family structure and

household is a crucial demographic indicator. This helps in revealing the demand level for all

facilities and services that is mostly related to the household types. In Wollongong city, 63.8% of

the total population reported that need for assistance that was fully owned their home. 13.9%

rented privately while the other 16.4% were included in the social housing for the year 2015

(Powdthavee, Lekfuangfu and Wooden 2015).

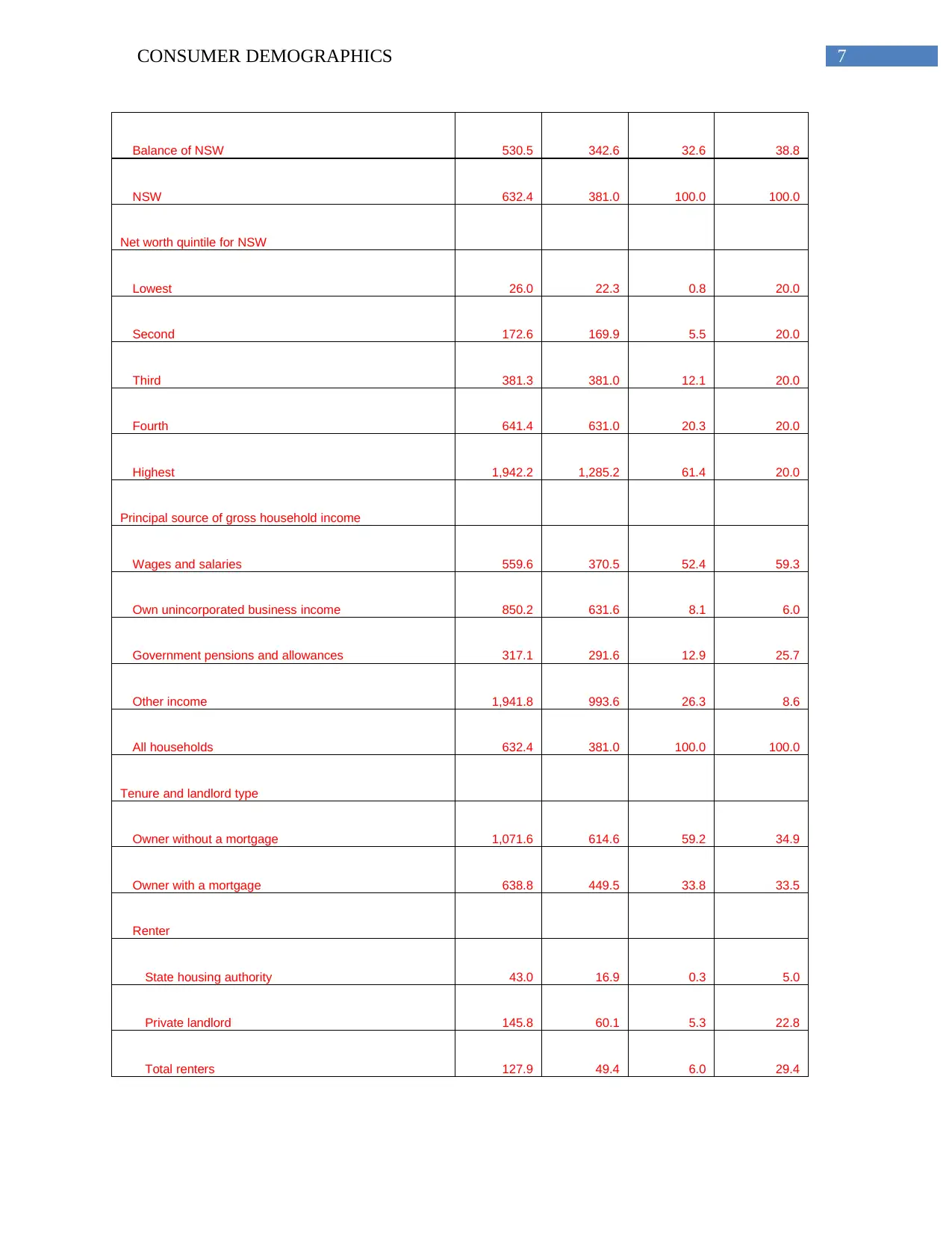

Pattern for Household expenditure for mortgage and rent in NSW, Wollongong:

Mean

household

net worth

Median

household

net worth

Share of

household

wealth

Percentage

of total

households

$'000 $'000 % %

Location

Sydney 697.2 419.0 67.4 61.2

Overall, 20% were paying very low repayments whereas 25.9% of households were

giving high mortgage repayments. The major differences between Wollongong NAD Regional

NSW were:

High percentage of people between $ 3,000 to $3,999, which is 11% more as compared to

6.2%.

High percentage of individuals of $ 2,600 to $2,999, which is 9.5% compared to 6.1%

(Brown and Gray 2015)

In Wollongong area, the medium highest group was the largest quartile and comprises of

at least 29% 0f the overall households with mortgages. Wollongong City’s family structure and

household is a crucial demographic indicator. This helps in revealing the demand level for all

facilities and services that is mostly related to the household types. In Wollongong city, 63.8% of

the total population reported that need for assistance that was fully owned their home. 13.9%

rented privately while the other 16.4% were included in the social housing for the year 2015

(Powdthavee, Lekfuangfu and Wooden 2015).

Pattern for Household expenditure for mortgage and rent in NSW, Wollongong:

Mean

household

net worth

Median

household

net worth

Share of

household

wealth

Percentage

of total

households

$'000 $'000 % %

Location

Sydney 697.2 419.0 67.4 61.2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONSUMER DEMOGRAPHICS

Balance of NSW 530.5 342.6 32.6 38.8

NSW 632.4 381.0 100.0 100.0

Net worth quintile for NSW

Lowest 26.0 22.3 0.8 20.0

Second 172.6 169.9 5.5 20.0

Third 381.3 381.0 12.1 20.0

Fourth 641.4 631.0 20.3 20.0

Highest 1,942.2 1,285.2 61.4 20.0

Principal source of gross household income

Wages and salaries 559.6 370.5 52.4 59.3

Own unincorporated business income 850.2 631.6 8.1 6.0

Government pensions and allowances 317.1 291.6 12.9 25.7

Other income 1,941.8 993.6 26.3 8.6

All households 632.4 381.0 100.0 100.0

Tenure and landlord type

Owner without a mortgage 1,071.6 614.6 59.2 34.9

Owner with a mortgage 638.8 449.5 33.8 33.5

Renter

State housing authority 43.0 16.9 0.3 5.0

Private landlord 145.8 60.1 5.3 22.8

Total renters 127.9 49.4 6.0 29.4

Balance of NSW 530.5 342.6 32.6 38.8

NSW 632.4 381.0 100.0 100.0

Net worth quintile for NSW

Lowest 26.0 22.3 0.8 20.0

Second 172.6 169.9 5.5 20.0

Third 381.3 381.0 12.1 20.0

Fourth 641.4 631.0 20.3 20.0

Highest 1,942.2 1,285.2 61.4 20.0

Principal source of gross household income

Wages and salaries 559.6 370.5 52.4 59.3

Own unincorporated business income 850.2 631.6 8.1 6.0

Government pensions and allowances 317.1 291.6 12.9 25.7

Other income 1,941.8 993.6 26.3 8.6

All households 632.4 381.0 100.0 100.0

Tenure and landlord type

Owner without a mortgage 1,071.6 614.6 59.2 34.9

Owner with a mortgage 638.8 449.5 33.8 33.5

Renter

State housing authority 43.0 16.9 0.3 5.0

Private landlord 145.8 60.1 5.3 22.8

Total renters 127.9 49.4 6.0 29.4

8CONSUMER DEMOGRAPHICS

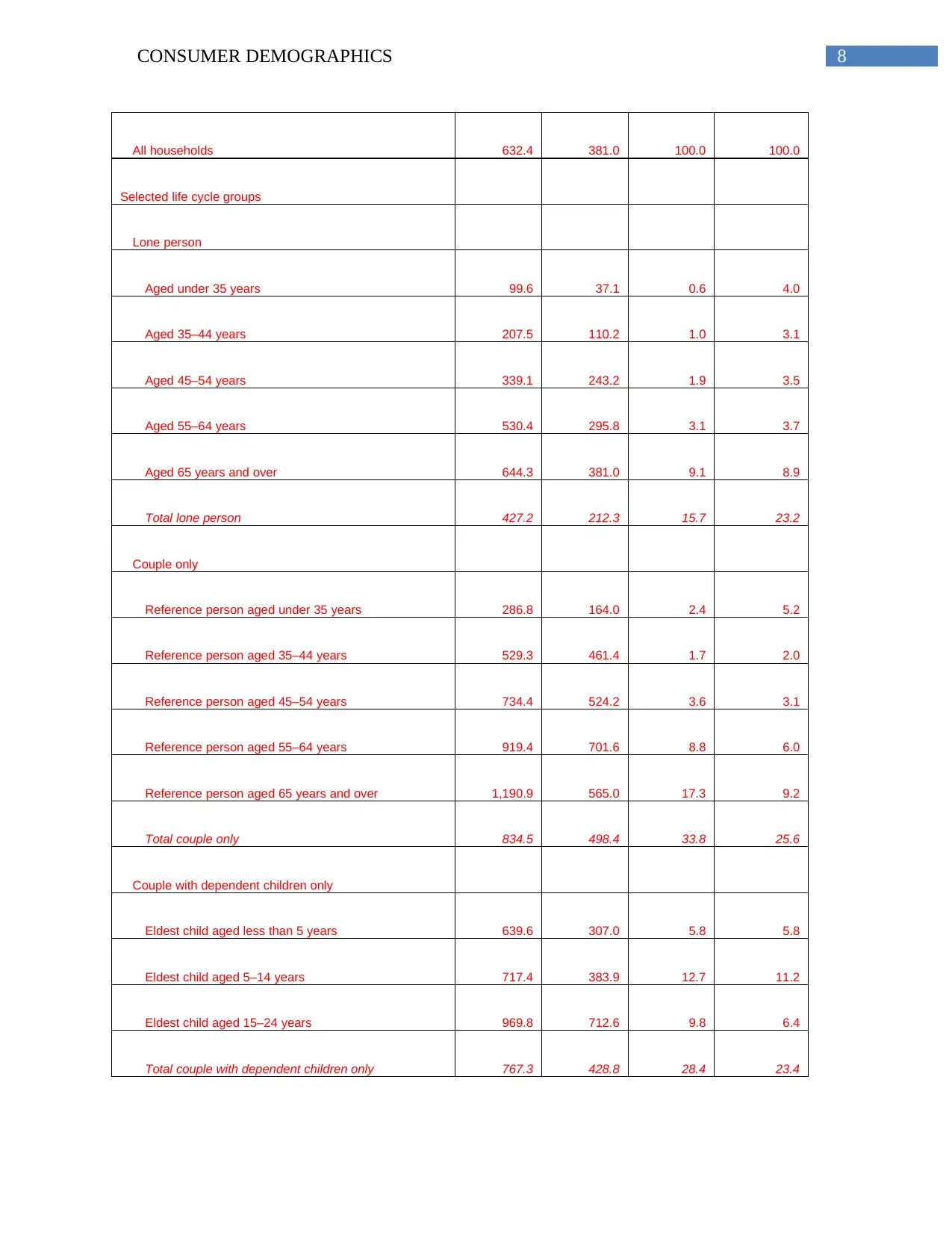

All households 632.4 381.0 100.0 100.0

Selected life cycle groups

Lone person

Aged under 35 years 99.6 37.1 0.6 4.0

Aged 35–44 years 207.5 110.2 1.0 3.1

Aged 45–54 years 339.1 243.2 1.9 3.5

Aged 55–64 years 530.4 295.8 3.1 3.7

Aged 65 years and over 644.3 381.0 9.1 8.9

Total lone person 427.2 212.3 15.7 23.2

Couple only

Reference person aged under 35 years 286.8 164.0 2.4 5.2

Reference person aged 35–44 years 529.3 461.4 1.7 2.0

Reference person aged 45–54 years 734.4 524.2 3.6 3.1

Reference person aged 55–64 years 919.4 701.6 8.8 6.0

Reference person aged 65 years and over 1,190.9 565.0 17.3 9.2

Total couple only 834.5 498.4 33.8 25.6

Couple with dependent children only

Eldest child aged less than 5 years 639.6 307.0 5.8 5.8

Eldest child aged 5–14 years 717.4 383.9 12.7 11.2

Eldest child aged 15–24 years 969.8 712.6 9.8 6.4

Total couple with dependent children only 767.3 428.8 28.4 23.4

All households 632.4 381.0 100.0 100.0

Selected life cycle groups

Lone person

Aged under 35 years 99.6 37.1 0.6 4.0

Aged 35–44 years 207.5 110.2 1.0 3.1

Aged 45–54 years 339.1 243.2 1.9 3.5

Aged 55–64 years 530.4 295.8 3.1 3.7

Aged 65 years and over 644.3 381.0 9.1 8.9

Total lone person 427.2 212.3 15.7 23.2

Couple only

Reference person aged under 35 years 286.8 164.0 2.4 5.2

Reference person aged 35–44 years 529.3 461.4 1.7 2.0

Reference person aged 45–54 years 734.4 524.2 3.6 3.1

Reference person aged 55–64 years 919.4 701.6 8.8 6.0

Reference person aged 65 years and over 1,190.9 565.0 17.3 9.2

Total couple only 834.5 498.4 33.8 25.6

Couple with dependent children only

Eldest child aged less than 5 years 639.6 307.0 5.8 5.8

Eldest child aged 5–14 years 717.4 383.9 12.7 11.2

Eldest child aged 15–24 years 969.8 712.6 9.8 6.4

Total couple with dependent children only 767.3 428.8 28.4 23.4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONSUMER DEMOGRAPHICS

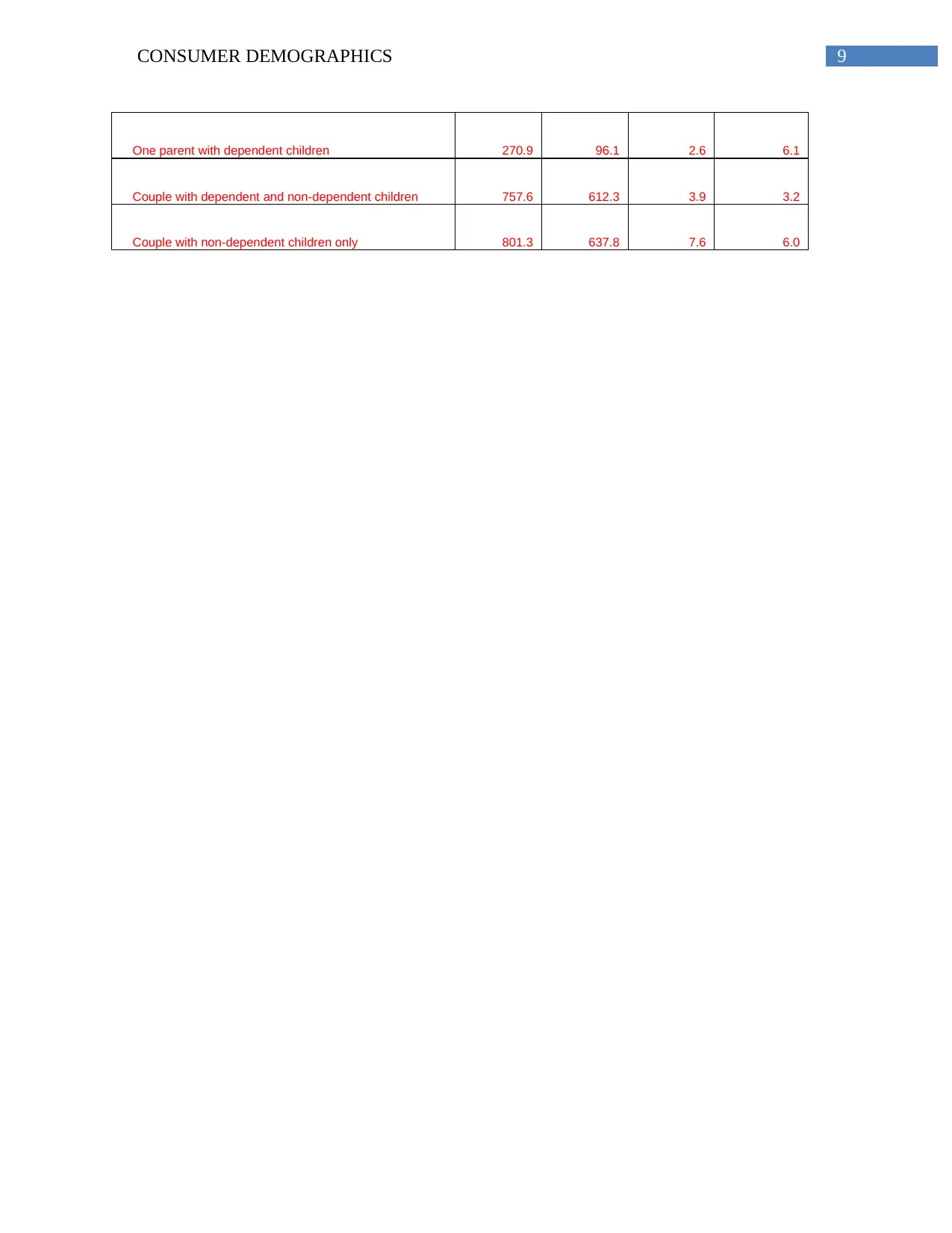

One parent with dependent children 270.9 96.1 2.6 6.1

Couple with dependent and non-dependent children 757.6 612.3 3.9 3.2

Couple with non-dependent children only 801.3 637.8 7.6 6.0

One parent with dependent children 270.9 96.1 2.6 6.1

Couple with dependent and non-dependent children 757.6 612.3 3.9 3.2

Couple with non-dependent children only 801.3 637.8 7.6 6.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONSUMER DEMOGRAPHICS

References:

Beer, A., Bentley, R., Baker, E., Mason, K., Mallett, S., Kavanagh, A. and LaMontagne, T.,

2016. Neoliberalism, economic restructuring and policy change: Precarious housing and

precarious employment in Australia. Urban studies, 53(8), pp.1542-1558.

Bolton, P.E., Rollins, L.A., Brazill-Boast, J., Maute, K.L., Legge, S., Austin, J.J. and Griffith,

S.C., 2018. Genetic diversity through time and space: diversity and demographic history from

natural history specimens and serially sampled contemporary populations of the threatened

Gouldian finch (Erythrura gouldiae). Conservation Genetics, pp.1-18.

Brown, S. and Gray, D., 2016. Household finances and well-being in Australia: An empirical

analysis of comparison effects. Journal of Economic Psychology, 53, pp.17-36.

Da Luz, F.Q., Sainsbury, A., Mannan, H., Touyz, S., Mitchison, D. and Hay, P., 2017.

Prevalence of obesity and comorbid eating disorder behaviors in South Australia from 1995 to

2015. International Journal of Obesity, 41(7), p.1148.

Finlay, R. and Price, F., 2015. Household saving in Australia. The BE Journal of

Macroeconomics, 15(2), pp.677-704.

Milner, A., Niedhammer, I., Chastang, J.F., Spittal, M.J. and LaMontagne, A.D., 2016. Validity

of a job-exposure matrix for psychosocial job stressors: results from the Household Income and

Labour Dynamics in Australia Survey. PloS one, 11(4), p.e0152980.

Pang, Z., Lin, B. and Jiang, J., 2015. The papers listed below have been accepted for publication

in future issues of Australian & New Zealand Journal of Statistics. Aust. NZJ Stat, 57(1), p.167.

References:

Beer, A., Bentley, R., Baker, E., Mason, K., Mallett, S., Kavanagh, A. and LaMontagne, T.,

2016. Neoliberalism, economic restructuring and policy change: Precarious housing and

precarious employment in Australia. Urban studies, 53(8), pp.1542-1558.

Bolton, P.E., Rollins, L.A., Brazill-Boast, J., Maute, K.L., Legge, S., Austin, J.J. and Griffith,

S.C., 2018. Genetic diversity through time and space: diversity and demographic history from

natural history specimens and serially sampled contemporary populations of the threatened

Gouldian finch (Erythrura gouldiae). Conservation Genetics, pp.1-18.

Brown, S. and Gray, D., 2016. Household finances and well-being in Australia: An empirical

analysis of comparison effects. Journal of Economic Psychology, 53, pp.17-36.

Da Luz, F.Q., Sainsbury, A., Mannan, H., Touyz, S., Mitchison, D. and Hay, P., 2017.

Prevalence of obesity and comorbid eating disorder behaviors in South Australia from 1995 to

2015. International Journal of Obesity, 41(7), p.1148.

Finlay, R. and Price, F., 2015. Household saving in Australia. The BE Journal of

Macroeconomics, 15(2), pp.677-704.

Milner, A., Niedhammer, I., Chastang, J.F., Spittal, M.J. and LaMontagne, A.D., 2016. Validity

of a job-exposure matrix for psychosocial job stressors: results from the Household Income and

Labour Dynamics in Australia Survey. PloS one, 11(4), p.e0152980.

Pang, Z., Lin, B. and Jiang, J., 2015. The papers listed below have been accepted for publication

in future issues of Australian & New Zealand Journal of Statistics. Aust. NZJ Stat, 57(1), p.167.

11CONSUMER DEMOGRAPHICS

Powdthavee, N., Lekfuangfu, W.N. and Wooden, M., 2015. What's the good of education on our

overall quality of life? A simultaneous equation model of education and life satisfaction for

Australia. Journal of behavioral and experimental economics, 54, pp.10-21.

Rowley, S., Leishman, C., Baker, E., Bentley, R. and Lester, L., 2017. Modelling housing need

in Australia to 2025 (No. 287). AHURI Final Report.

Wilkins, R., 2015. Measuring income inequality in Australia. Australian Economic

Review, 48(1), pp.93-102.

Powdthavee, N., Lekfuangfu, W.N. and Wooden, M., 2015. What's the good of education on our

overall quality of life? A simultaneous equation model of education and life satisfaction for

Australia. Journal of behavioral and experimental economics, 54, pp.10-21.

Rowley, S., Leishman, C., Baker, E., Bentley, R. and Lester, L., 2017. Modelling housing need

in Australia to 2025 (No. 287). AHURI Final Report.

Wilkins, R., 2015. Measuring income inequality in Australia. Australian Economic

Review, 48(1), pp.93-102.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.