Divine Denim: Business Strategy, Costing, and Budget Analysis

VerifiedAdded on 2022/09/16

|12

|1711

|14

Homework Assignment

AI Summary

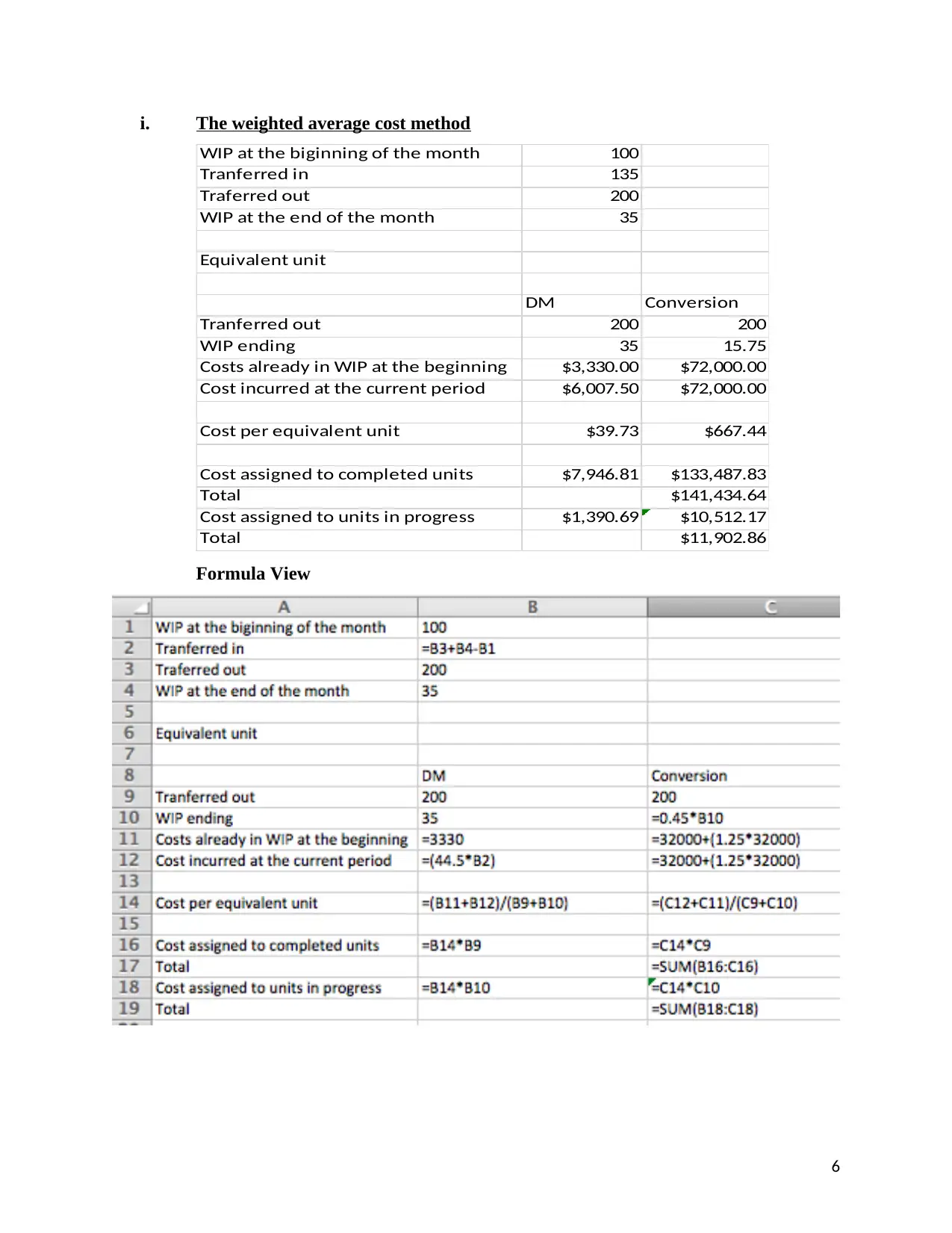

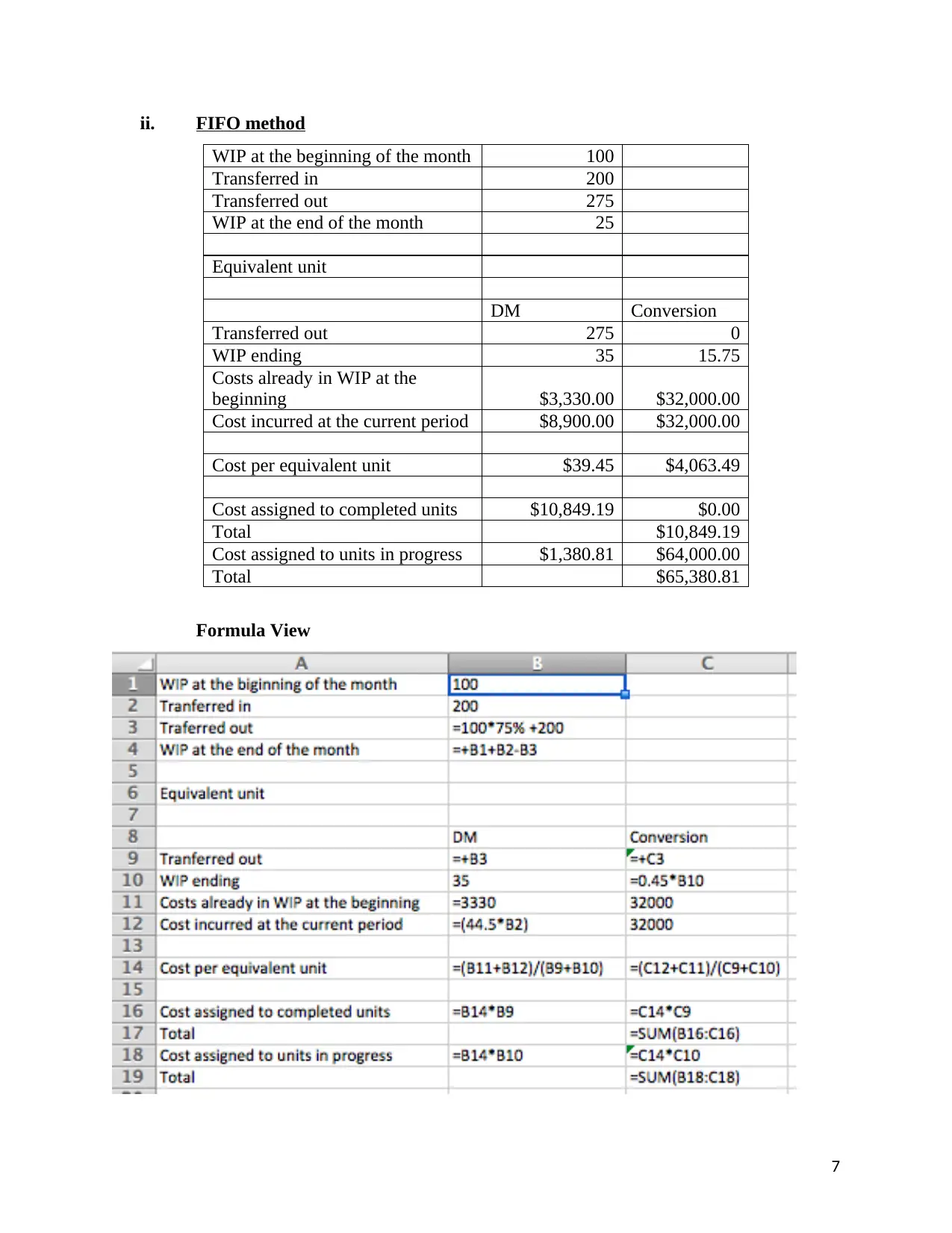

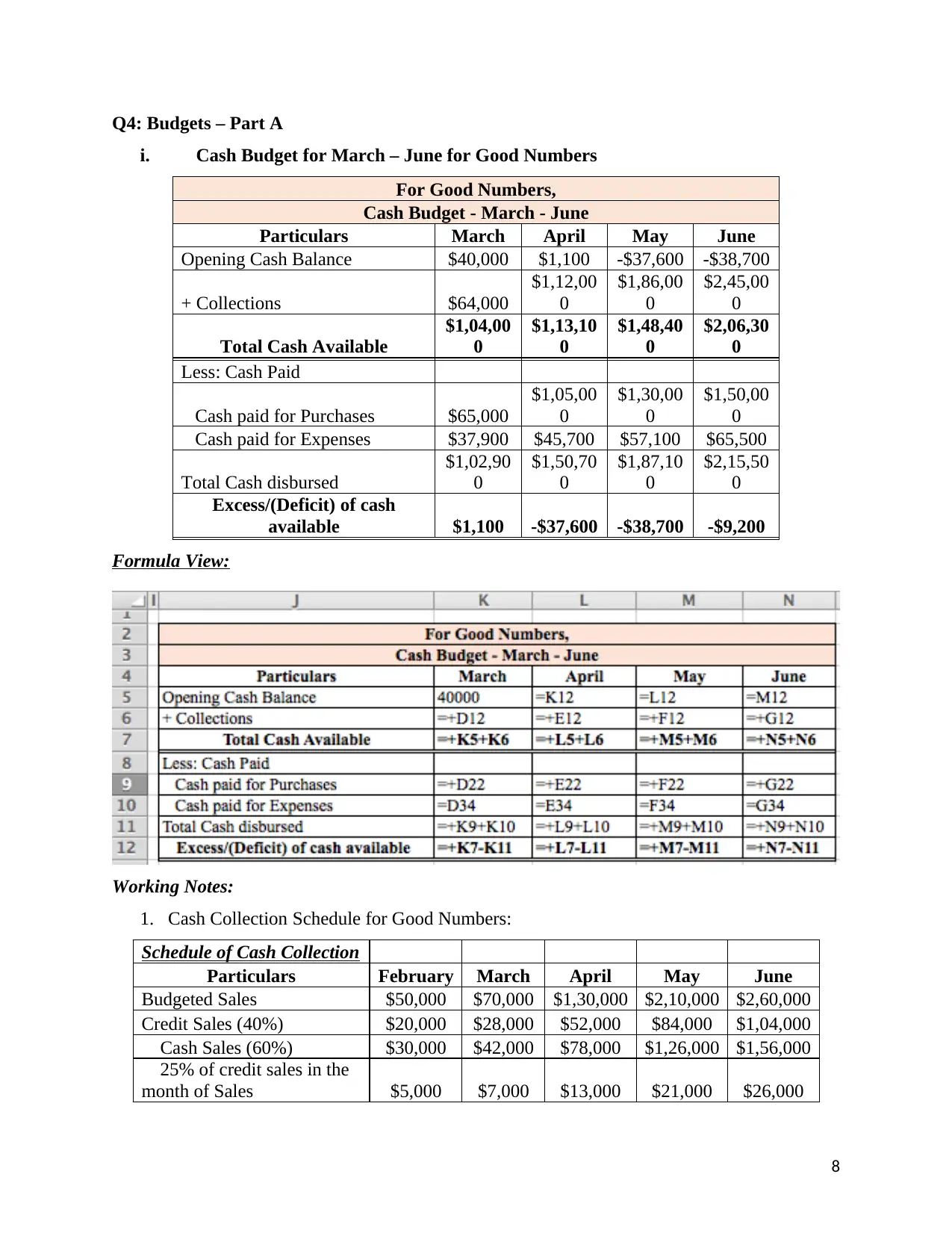

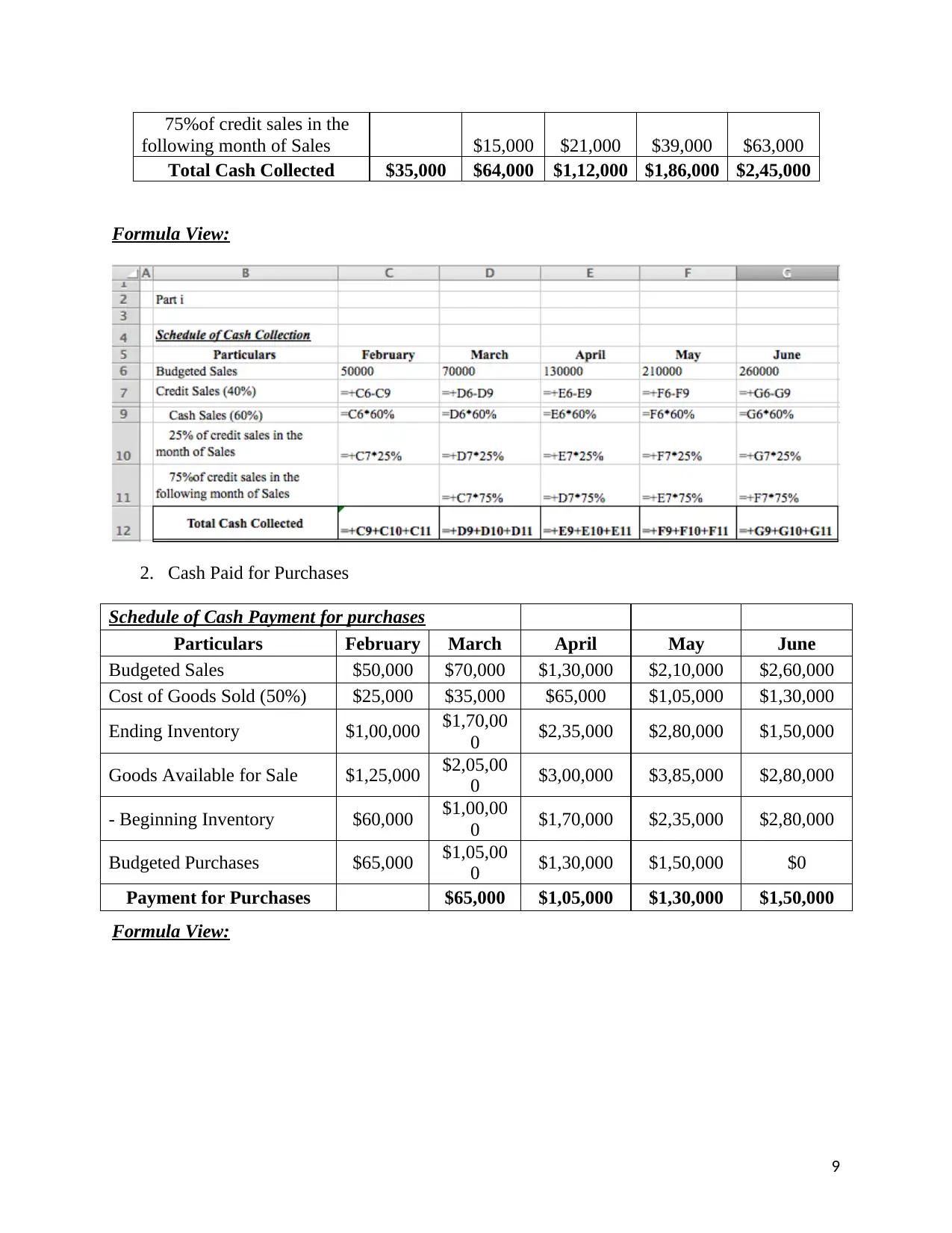

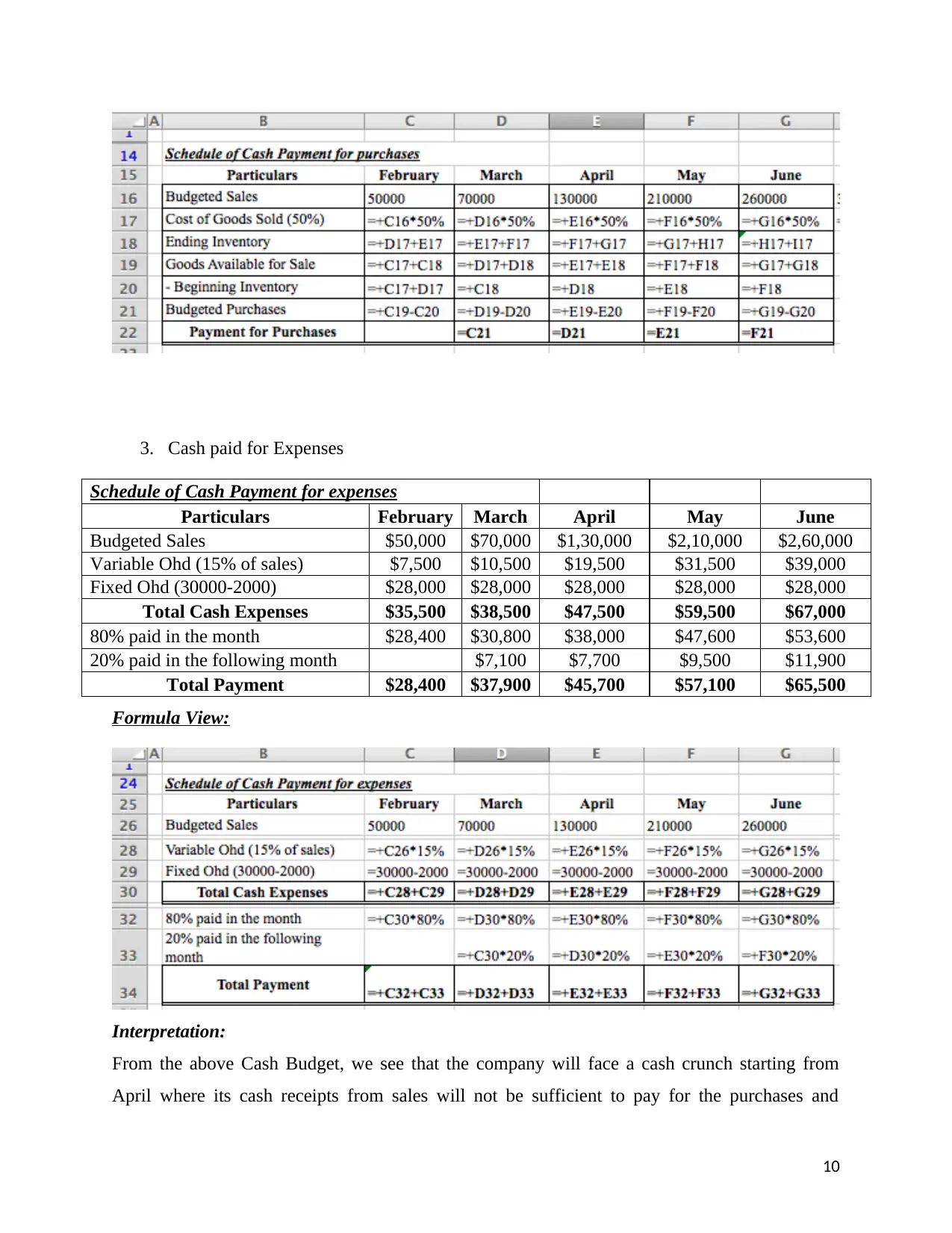

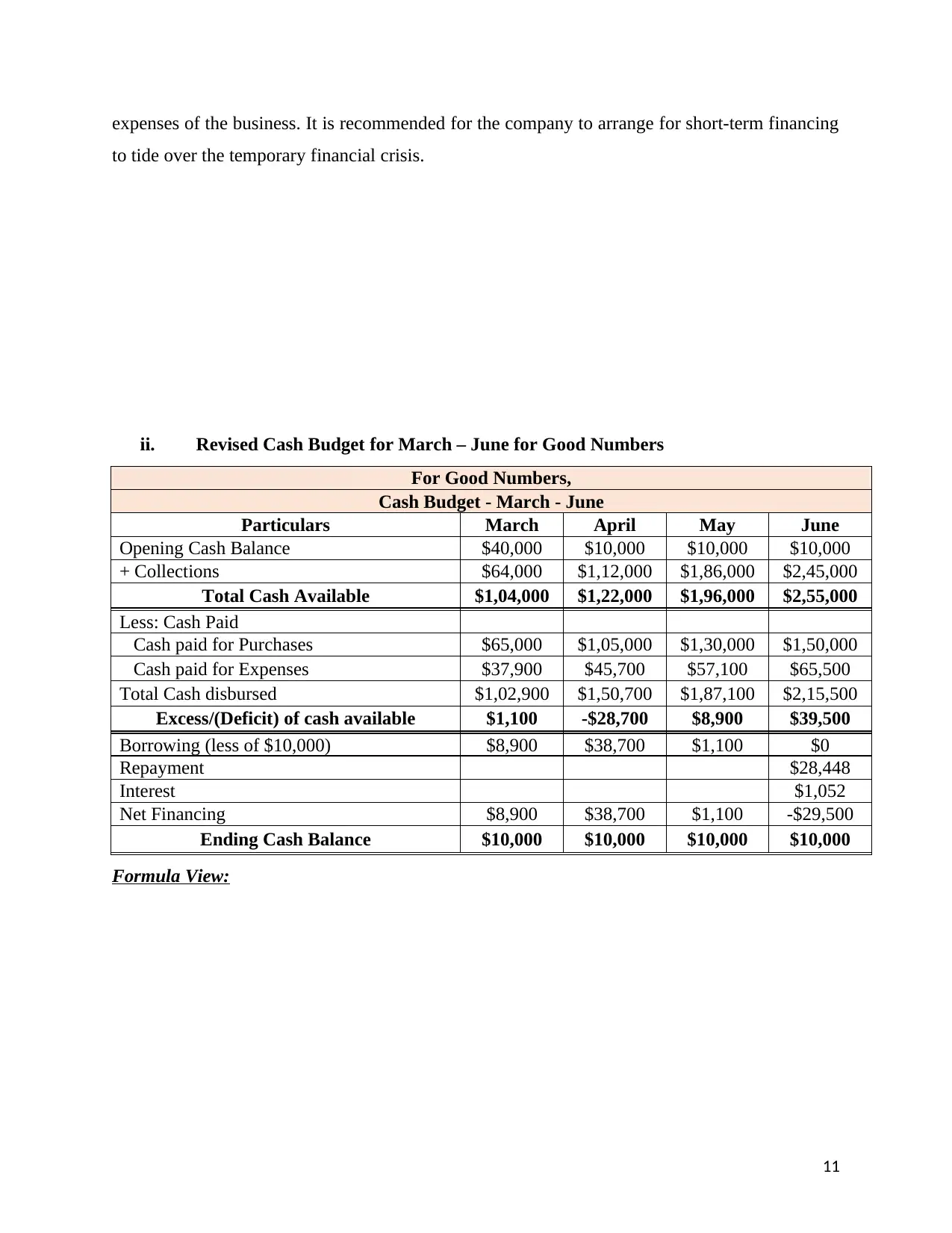

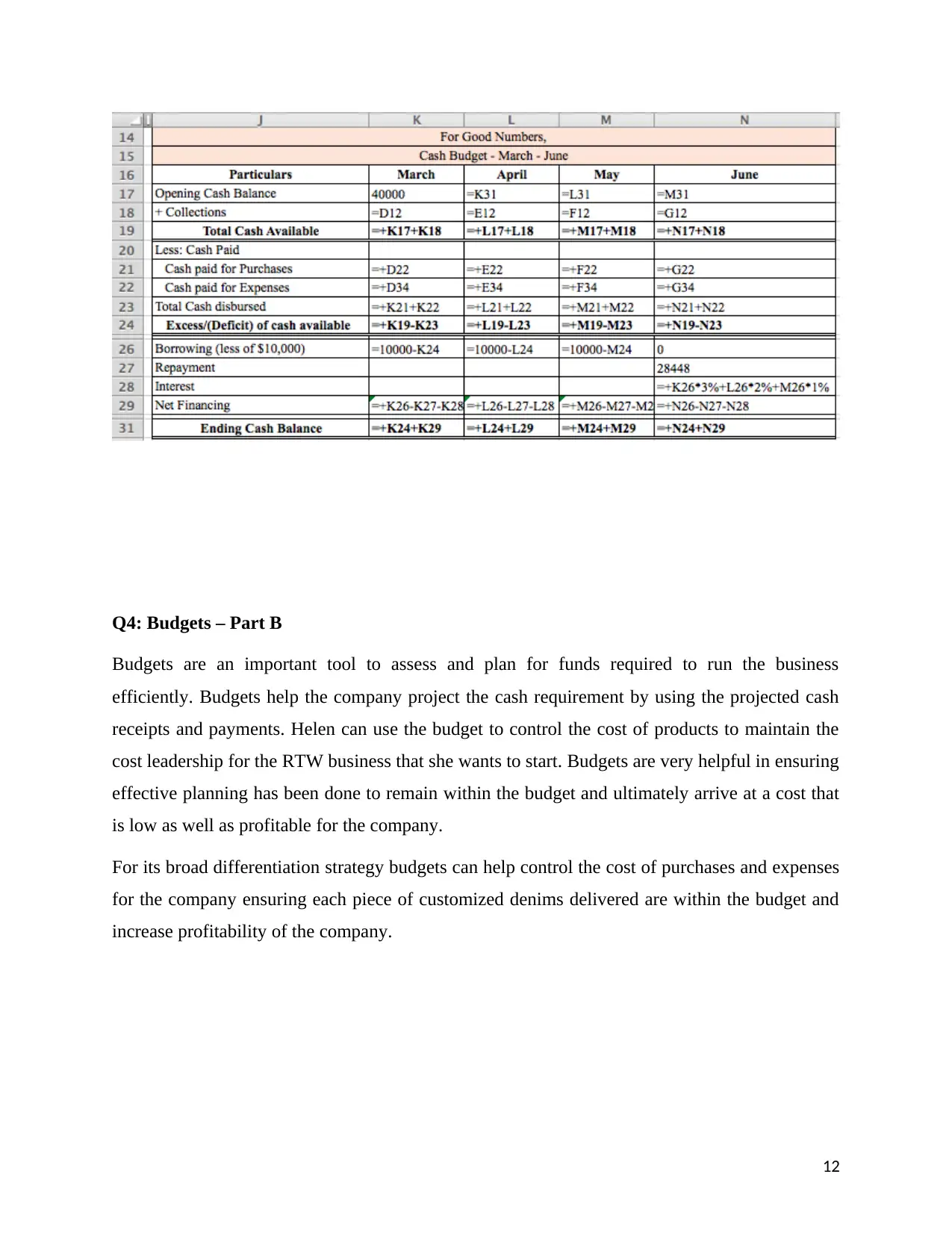

This assignment analyzes Divine Denim, a company specializing in custom and ready-to-wear denim products. It begins with a Porter's Five Forces analysis to assess the competitive landscape for both the made-to-measure and ready-to-wear businesses, highlighting the strategic implications of each. The assignment then delves into cost allocation, presenting direct and step-down methods, alongside a reciprocal method solution. Process costing is examined using weighted average and FIFO methods. Finally, the assignment includes cash budgeting for the company, presenting a cash budget, schedule of cash collections, and cash paid for purchases and expenses, followed by an interpretation and revised cash budget to address the company's cash flow challenges. The analysis emphasizes the importance of budgeting for strategic planning and cost control.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.