Evaluation of Depreciation Methods: Recommendation for Burley Designs

VerifiedAdded on 2020/03/04

|4

|866

|22

Report

AI Summary

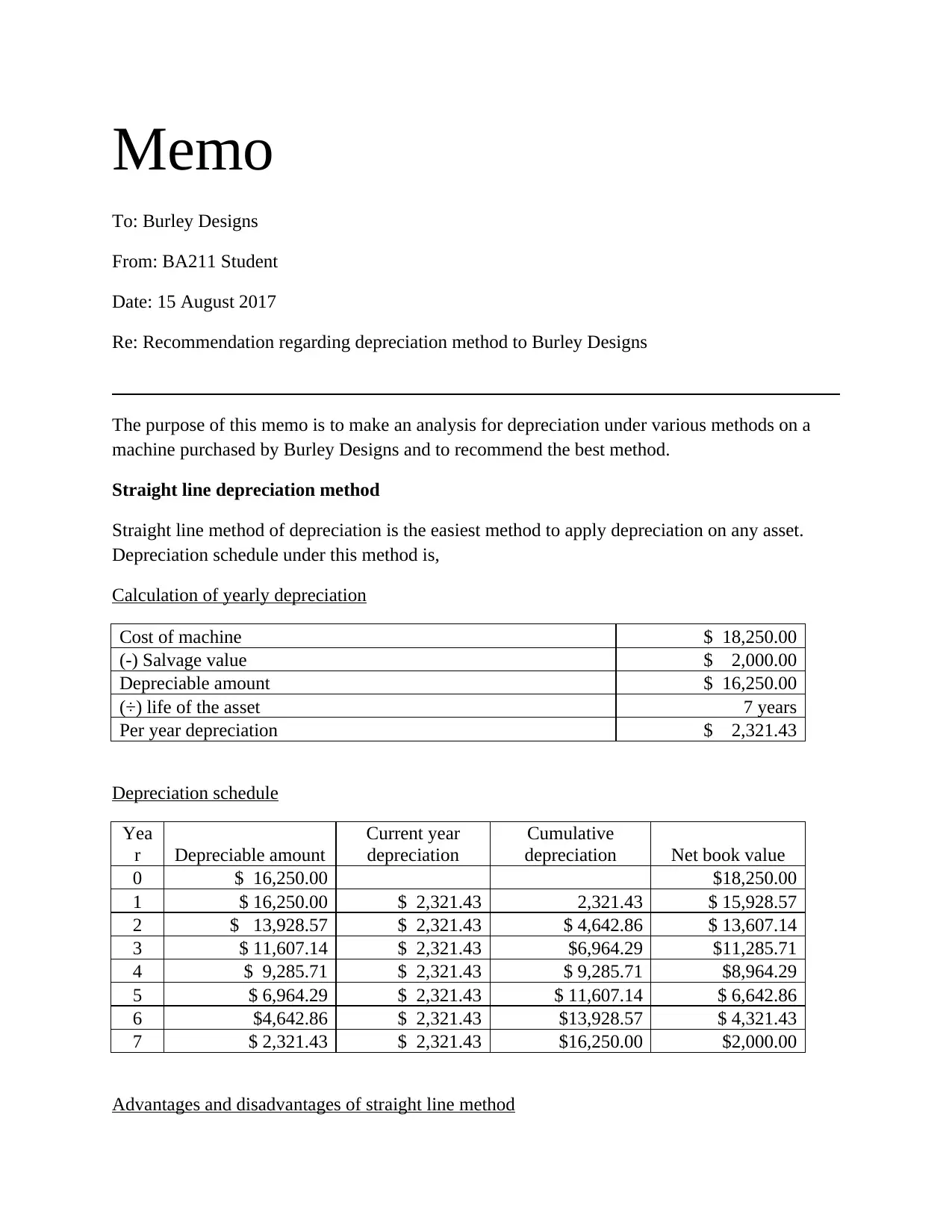

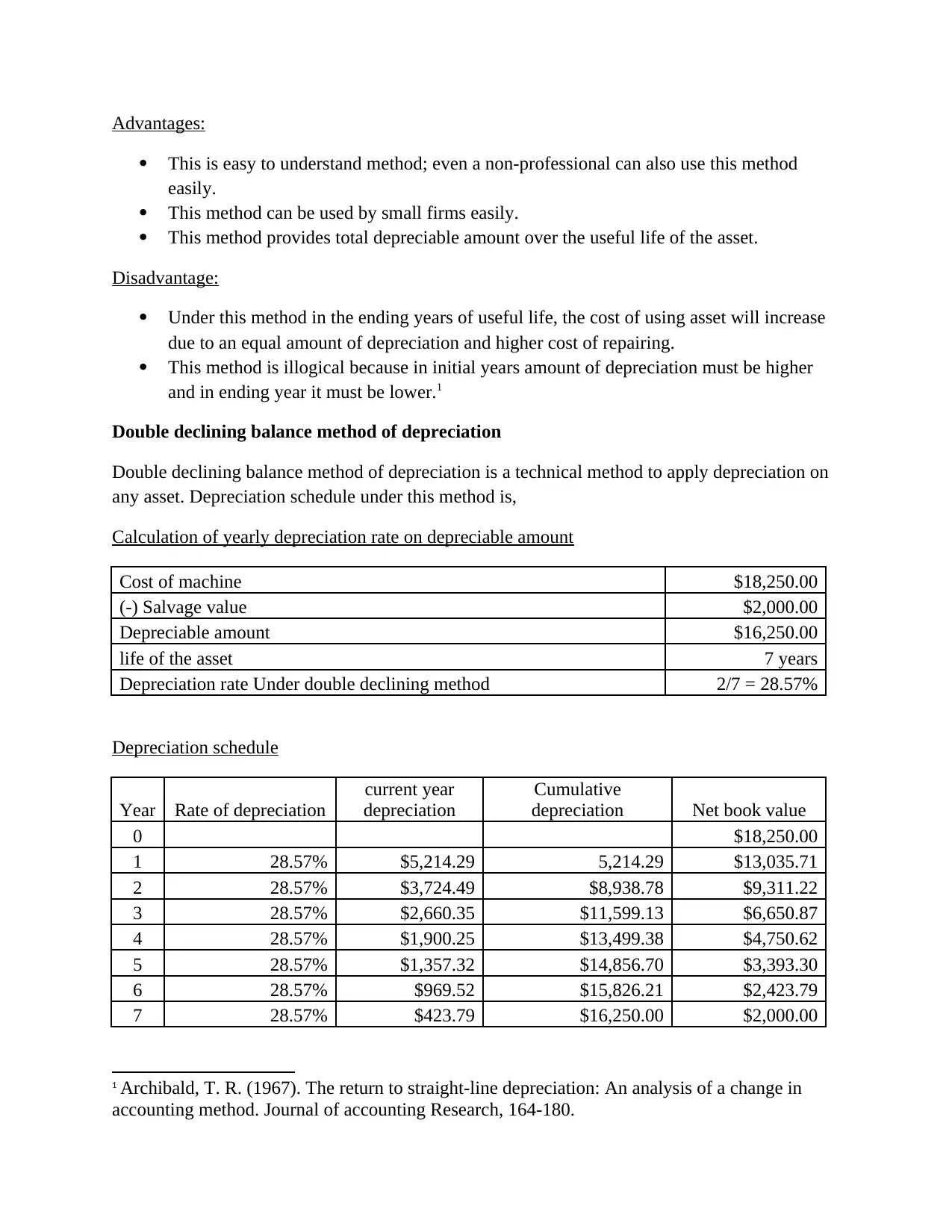

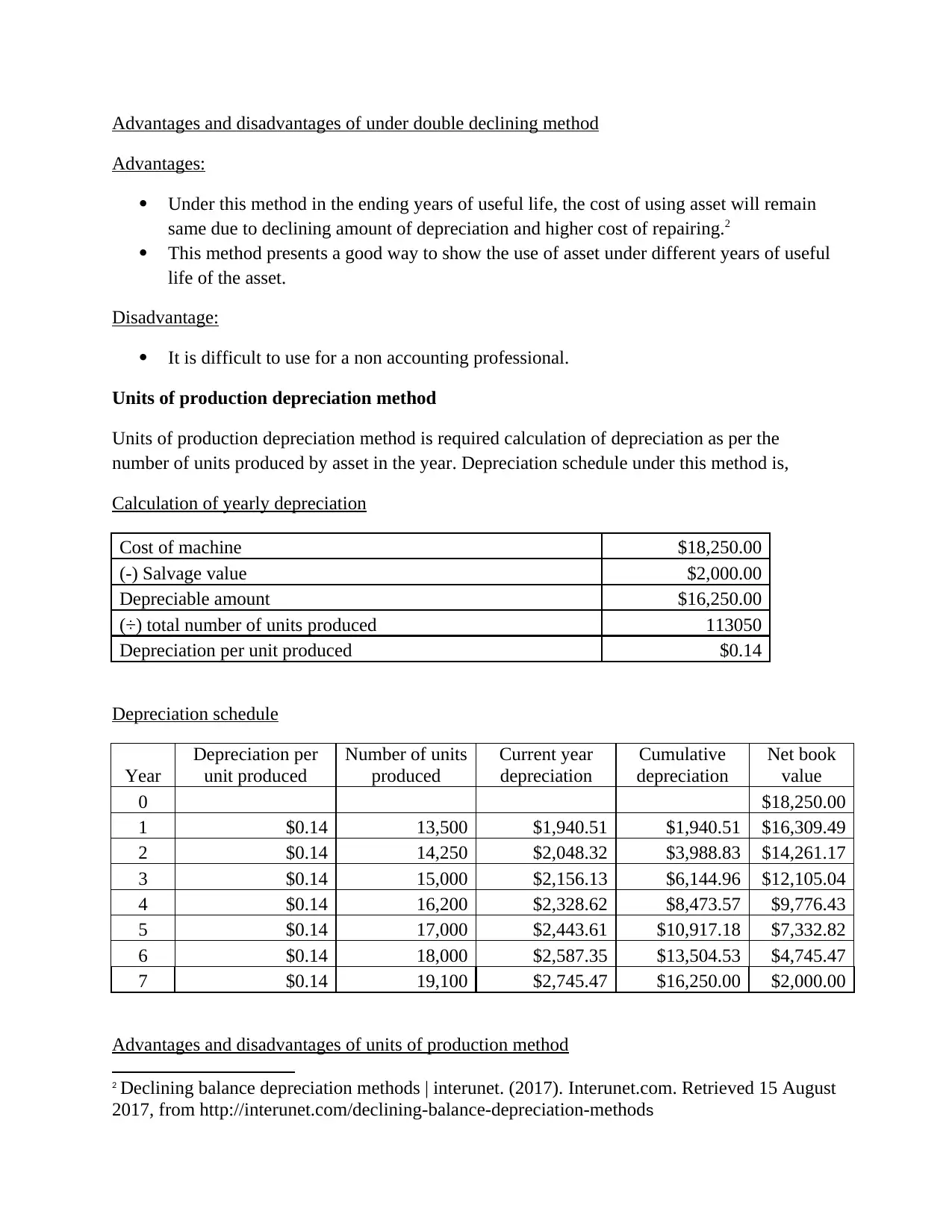

This memo analyzes three depreciation methods—straight-line, double declining balance, and units of production—for a machine purchased by Burley Designs. The straight-line method, though simple, distributes depreciation evenly over the asset's life, potentially misrepresenting the true cost of asset use. The double declining balance method offers a more technically sound approach, reflecting the asset's declining value over time. The units of production method links depreciation to actual asset usage. The analysis includes detailed depreciation schedules, advantages, and disadvantages for each method. The memo concludes that the double declining balance method is the most suitable option for Burley Designs as it provides a more accurate representation of the asset's cost of use and can be applied to all assets. This analysis is presented to provide insights into financial accounting and depreciation methods.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.