Analysis of Property, Plant, and Equipment Derecognition - Finance

VerifiedAdded on 2020/05/28

|4

|677

|70

Report

AI Summary

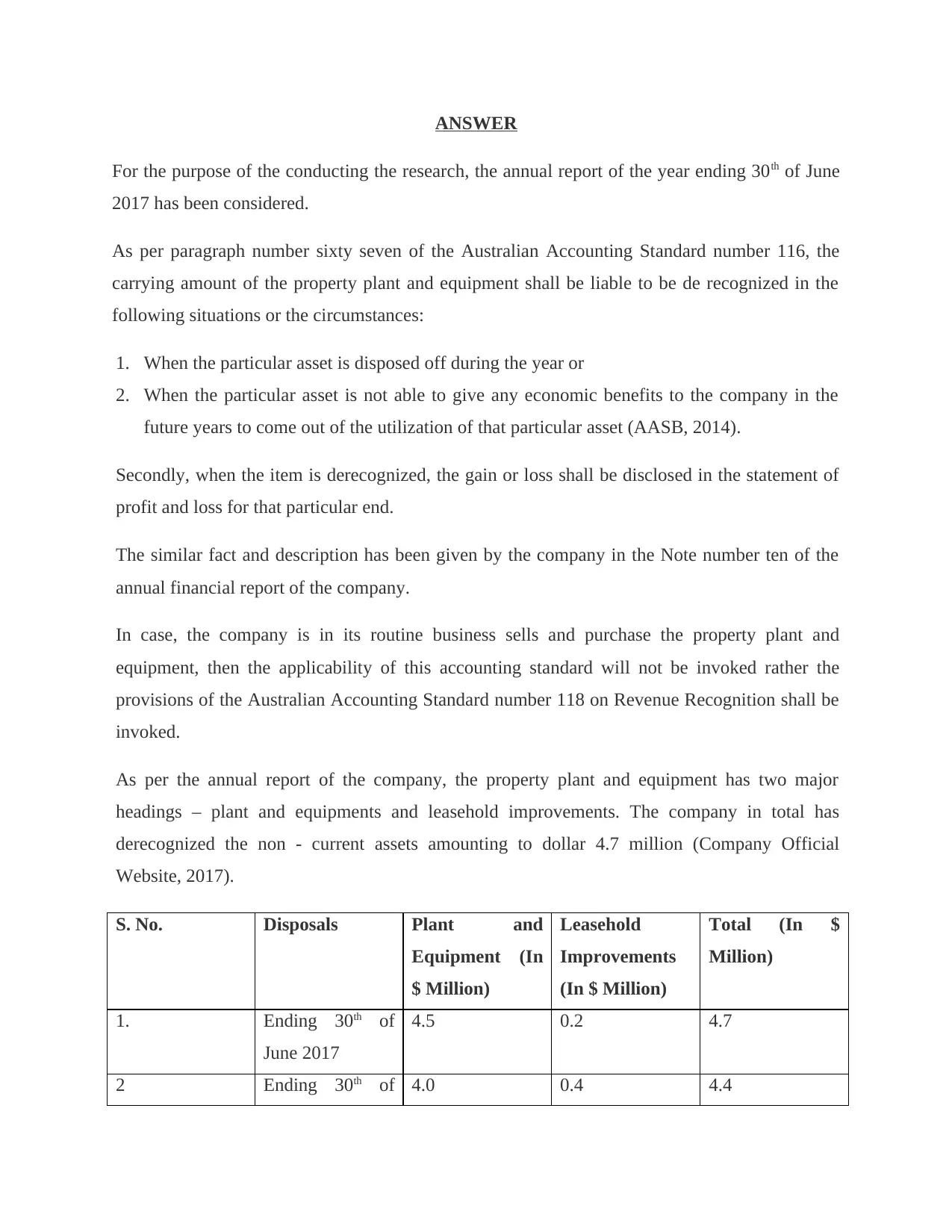

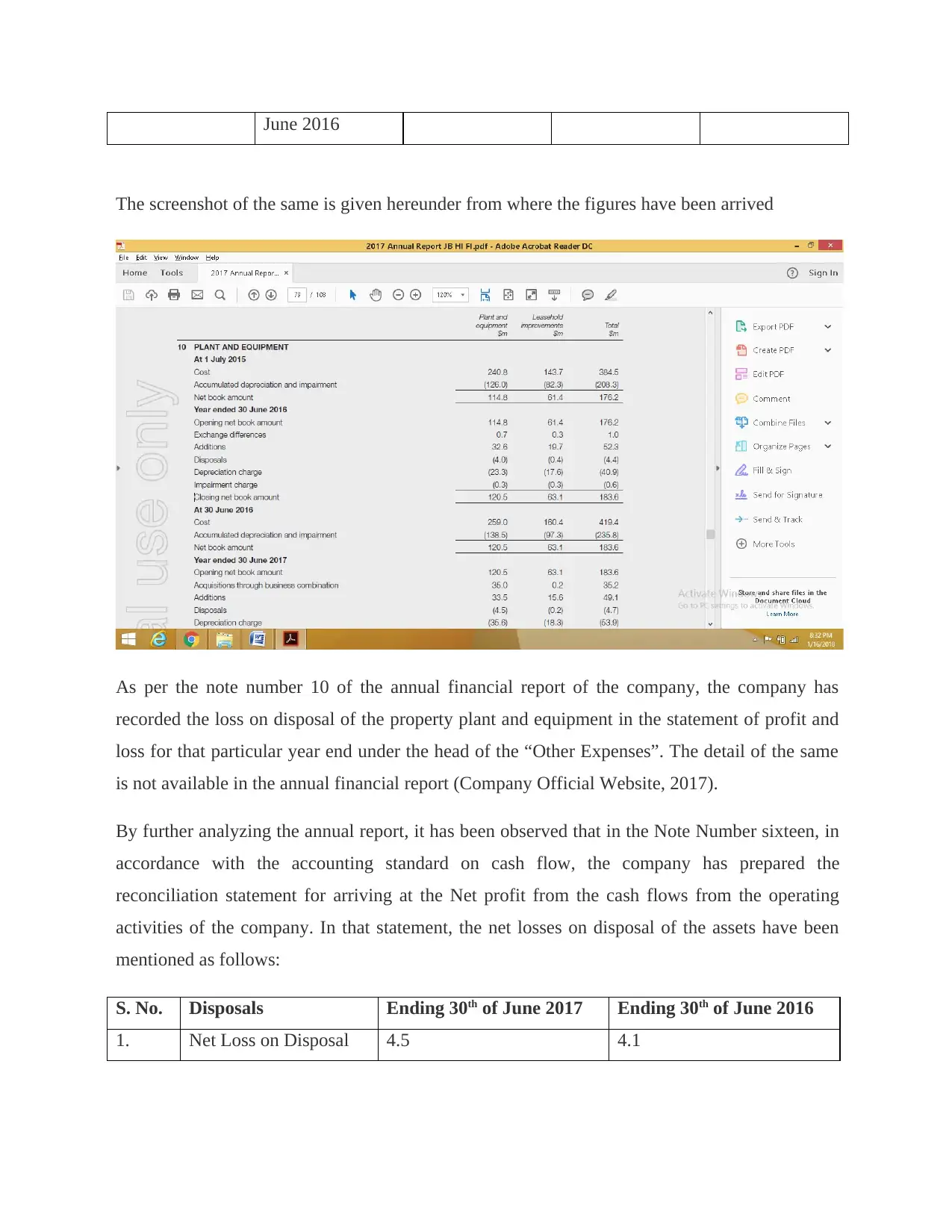

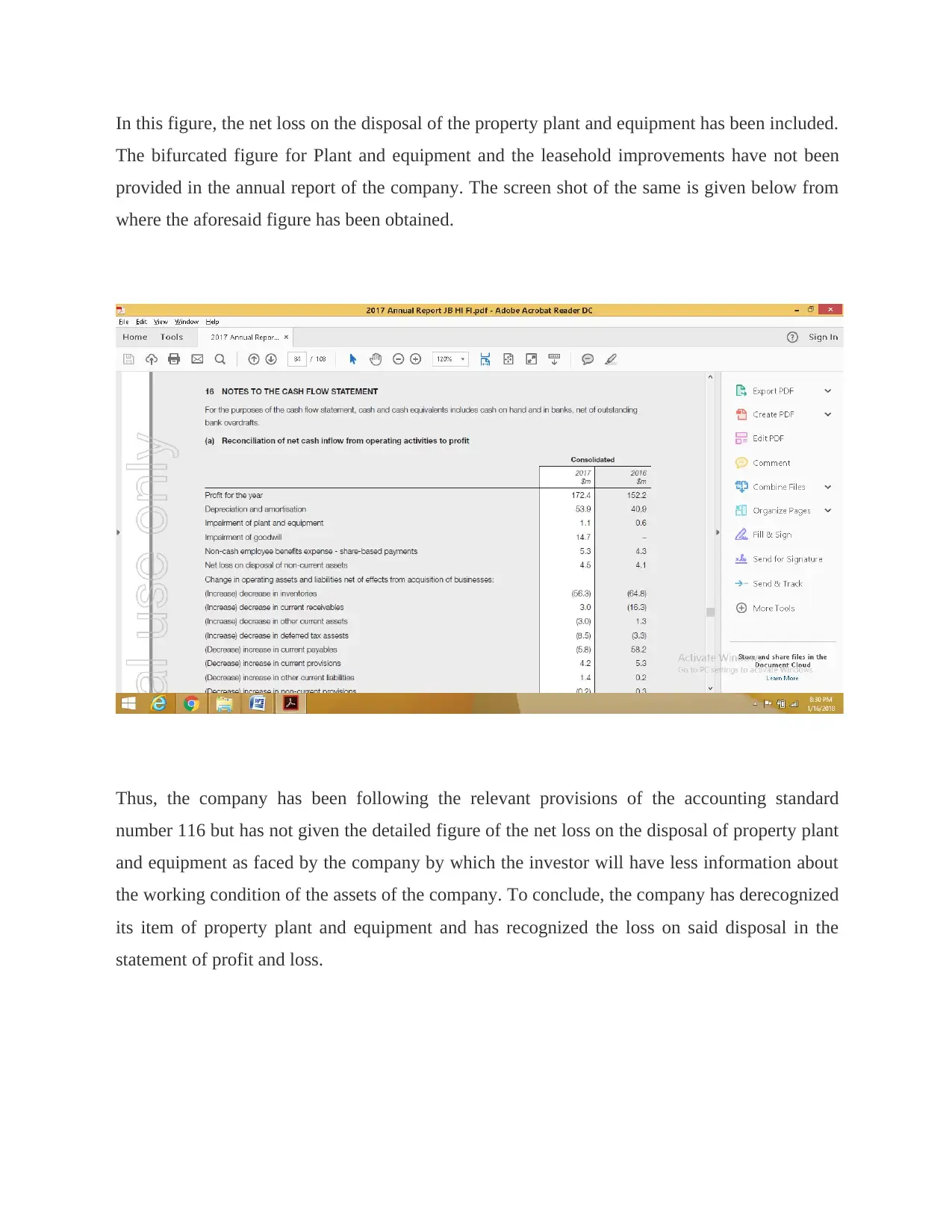

This report analyzes the derecognition of property, plant, and equipment (PPE) based on the annual report of a company ending June 30, 2017, referencing Australian Accounting Standard 116. The analysis covers the circumstances under which PPE is derecognized, including disposal and lack of future economic benefits. The report examines the company's treatment of PPE, including plant and equipment, and leasehold improvements. It highlights the total derecognition of non-current assets and the recorded losses on disposal in the statement of profit and loss. The analysis also references the reconciliation statement for cash flows from operating activities, noting the inclusion of net losses on disposal. The report concludes that while the company follows relevant accounting standards, it could improve transparency by providing more detailed figures on losses, potentially benefiting investors. The references include the AASB guidelines and the company's official website for financial data.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.