Kean University Introduction to Derivatives Second Exam

VerifiedAdded on 2022/08/03

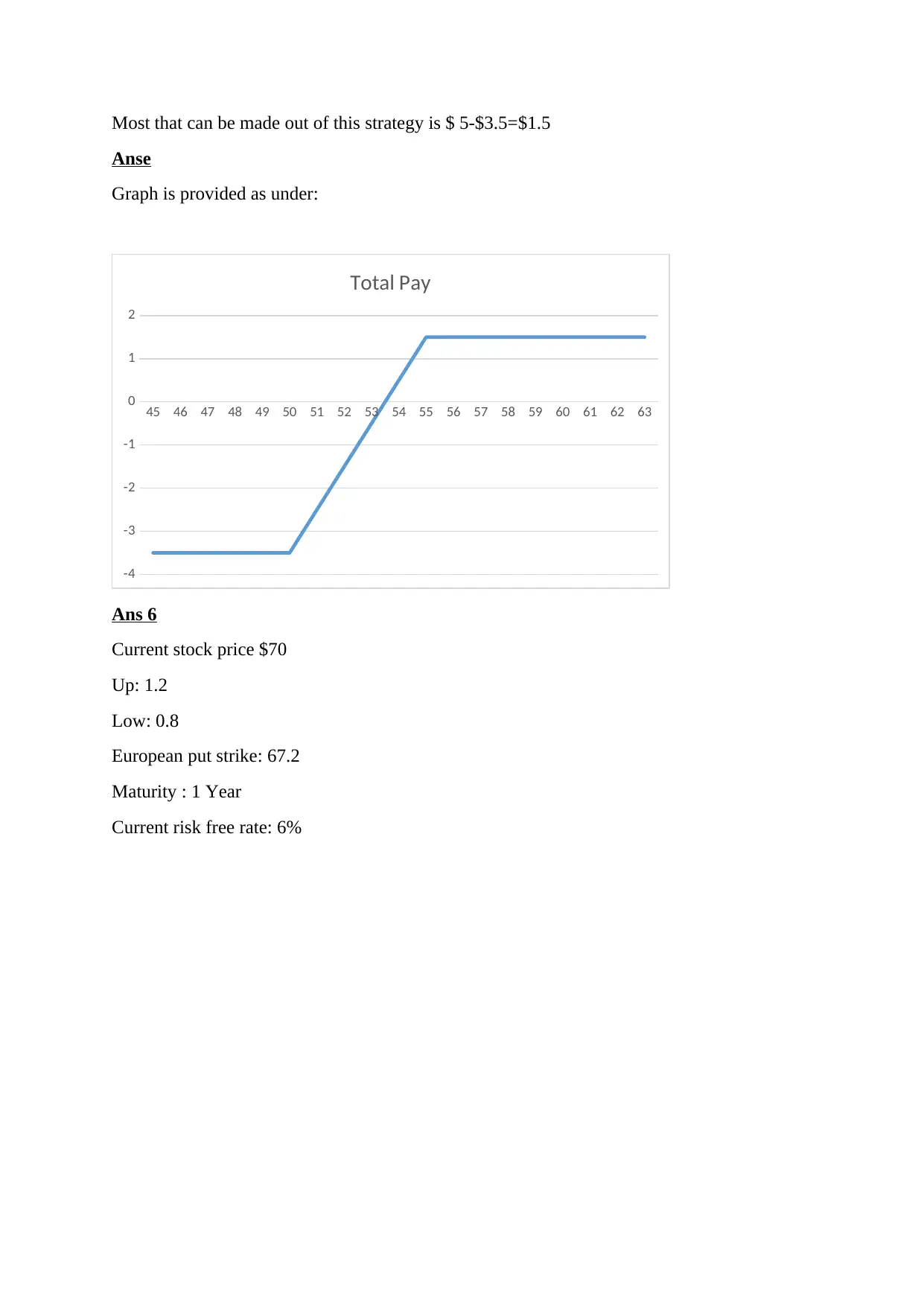

|5

|935

|25

Quiz and Exam

AI Summary

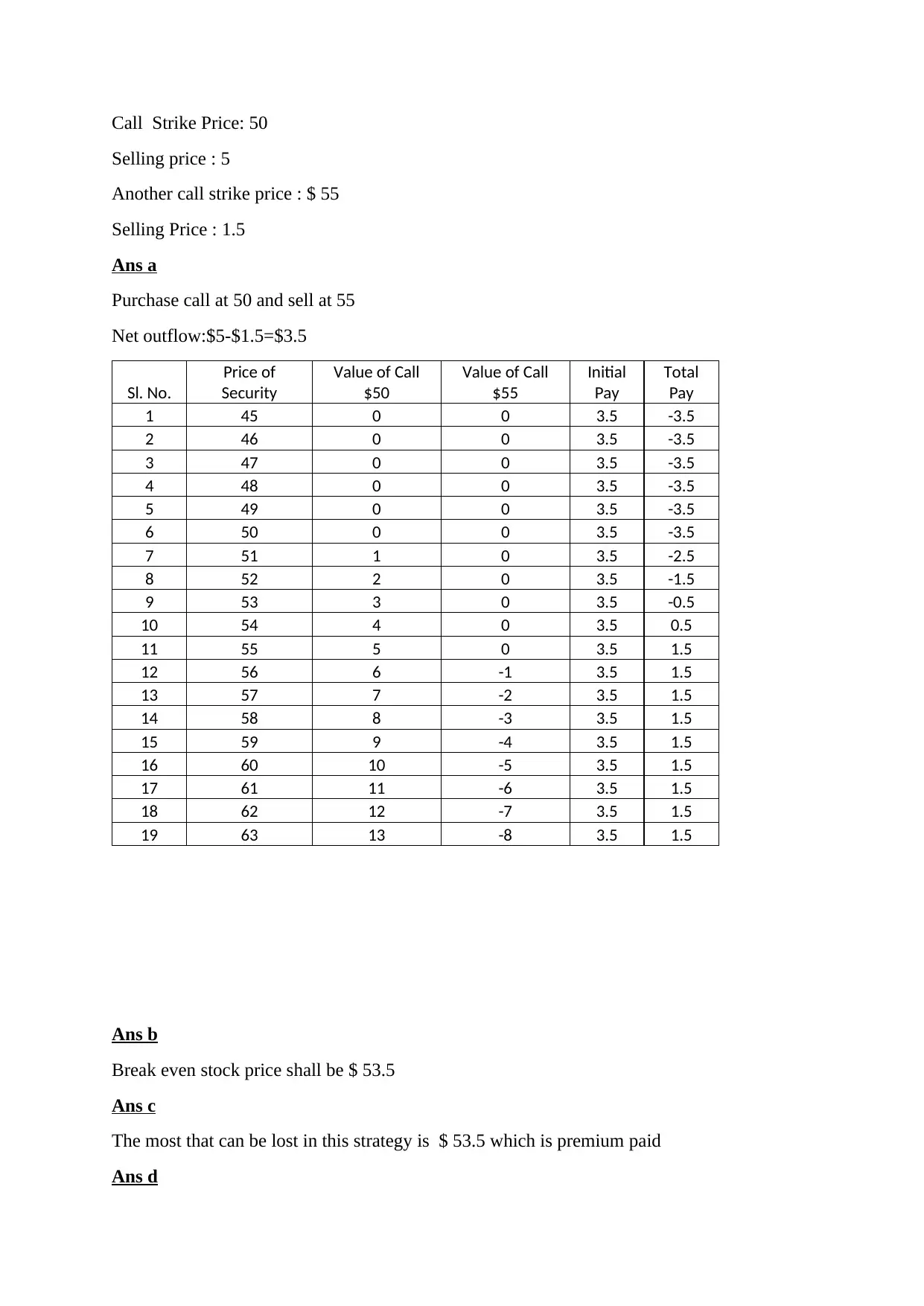

This document presents solutions to a second exam in an Introduction to Derivatives course. The exam covers core concepts such as American and European options, option delta, and bullish market indicators. It includes multiple-choice questions, definitions, and problem-solving scenarios. The solutions address topics like calculating gains and losses on options, break-even points, and the impact of stock dividends. Furthermore, the document explores strategies such as protective puts and covered calls, analyzing potential profits and losses. The document also includes a detailed analysis of option pricing using the Black-Scholes model and binomial trees. The solutions are comprehensive and provide a thorough understanding of the subject matter, making it a valuable resource for students preparing for derivatives exams.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.