Assignment Solution: MAF 308 - Derivatives and Fixed Income Securities

VerifiedAdded on 2020/07/23

|13

|2862

|32

Homework Assignment

AI Summary

This document presents a comprehensive solution to an assignment on derivatives and fixed income securities, likely for a course like MAF 308. The solution encompasses multiple parts, starting with bond valuation, including calculations of bond value, yield to maturity (YTM), and duration. It then moves on to futures contracts, exploring their use in hedging and speculation, the rationale behind these strategies, and the criticality of maturity mismatch. The assignment also delves into option pricing, examining the relationship between option price, strike price, and duration. The document includes tables, calculations, and explanations to illustrate the concepts and provide a thorough understanding of the topics covered. The assignment covers important concepts in financial derivatives, and fixed income securities providing a complete overview of the subject.

MAF 308 - DERIVATIVES AND FIXED

INCOME SECURITIES

INCOME SECURITIES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Question A1 Bond valuation.......................................................................................................1

Question A2 Construction of chart of bond price and YTM.......................................................2

Question A3 Duration of bond....................................................................................................3

PART B...........................................................................................................................................4

Question B2.1 Justification on hedging and speculation.............................................................4

Question B2.2 main purpose of hedge using futures...................................................................5

Question B2.3 Criticality of maturity mismatch..........................................................................6

PART C...........................................................................................................................................7

Question C1.................................................................................................................................7

Question C2.................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Question A1 Bond valuation.......................................................................................................1

Question A2 Construction of chart of bond price and YTM.......................................................2

Question A3 Duration of bond....................................................................................................3

PART B...........................................................................................................................................4

Question B2.1 Justification on hedging and speculation.............................................................4

Question B2.2 main purpose of hedge using futures...................................................................5

Question B2.3 Criticality of maturity mismatch..........................................................................6

PART C...........................................................................................................................................7

Question C1.................................................................................................................................7

Question C2.................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Derivative is the one of the important instrument on which firms make heavy investment to hedge their positions. In current

report, bond value and duration is computed. Along with this, relationship between duration yield on bond and value of it is discussed.

In middle part of report, option price and its relevance to duration remaining in expiry as well as gap between strike price as well as

current market price is discussed in detail. At end of report, conclusion section is prepared.

PART A

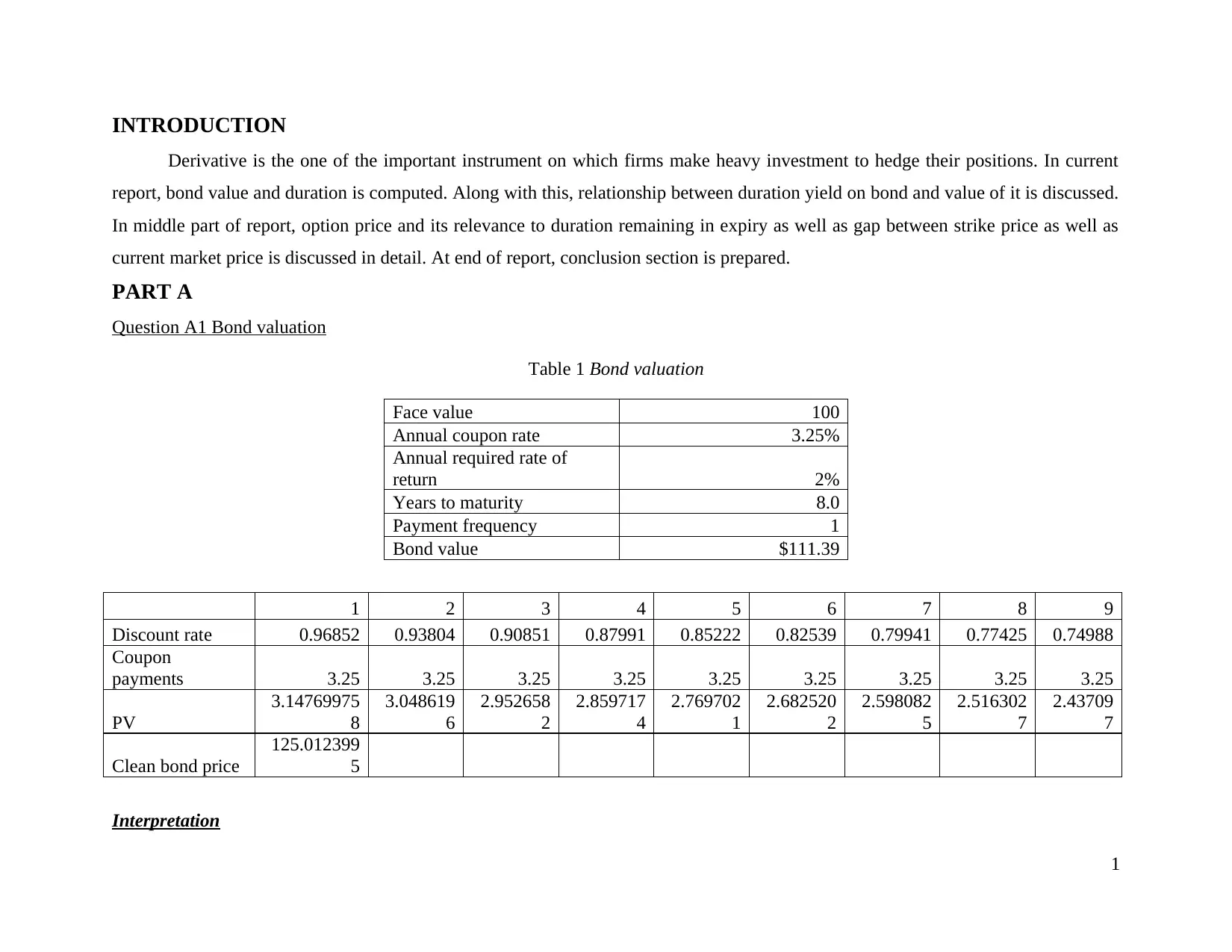

Question A1 Bond valuation

Table 1 Bond valuation

Face value 100

Annual coupon rate 3.25%

Annual required rate of

return 2%

Years to maturity 8.0

Payment frequency 1

Bond value $111.39

1 2 3 4 5 6 7 8 9

Discount rate 0.96852 0.93804 0.90851 0.87991 0.85222 0.82539 0.79941 0.77425 0.74988

Coupon

payments 3.25 3.25 3.25 3.25 3.25 3.25 3.25 3.25 3.25

PV

3.14769975

8

3.048619

6

2.952658

2

2.859717

4

2.769702

1

2.682520

2

2.598082

5

2.516302

7

2.43709

7

Clean bond price

125.012399

5

Interpretation

1

Derivative is the one of the important instrument on which firms make heavy investment to hedge their positions. In current

report, bond value and duration is computed. Along with this, relationship between duration yield on bond and value of it is discussed.

In middle part of report, option price and its relevance to duration remaining in expiry as well as gap between strike price as well as

current market price is discussed in detail. At end of report, conclusion section is prepared.

PART A

Question A1 Bond valuation

Table 1 Bond valuation

Face value 100

Annual coupon rate 3.25%

Annual required rate of

return 2%

Years to maturity 8.0

Payment frequency 1

Bond value $111.39

1 2 3 4 5 6 7 8 9

Discount rate 0.96852 0.93804 0.90851 0.87991 0.85222 0.82539 0.79941 0.77425 0.74988

Coupon

payments 3.25 3.25 3.25 3.25 3.25 3.25 3.25 3.25 3.25

PV

3.14769975

8

3.048619

6

2.952658

2

2.859717

4

2.769702

1

2.682520

2

2.598082

5

2.516302

7

2.43709

7

Clean bond price

125.012399

5

Interpretation

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By considering face value, annual coupon rate and required rate of return bond present value is computed which is $111.39.

This means that in order to purchase bond at relevant date one need to pay mentioned amount. At discount rate discount factor is

computed for 8.9 years. These discount factors are multiplied to coupon payments to compute fair value or present value of future

cash inflows for today period. Face value is added to present value of cash inflows and in this way bond value is computed which is

125.01. Thus, it can be said that by using different approaches varied price of bond is computed.

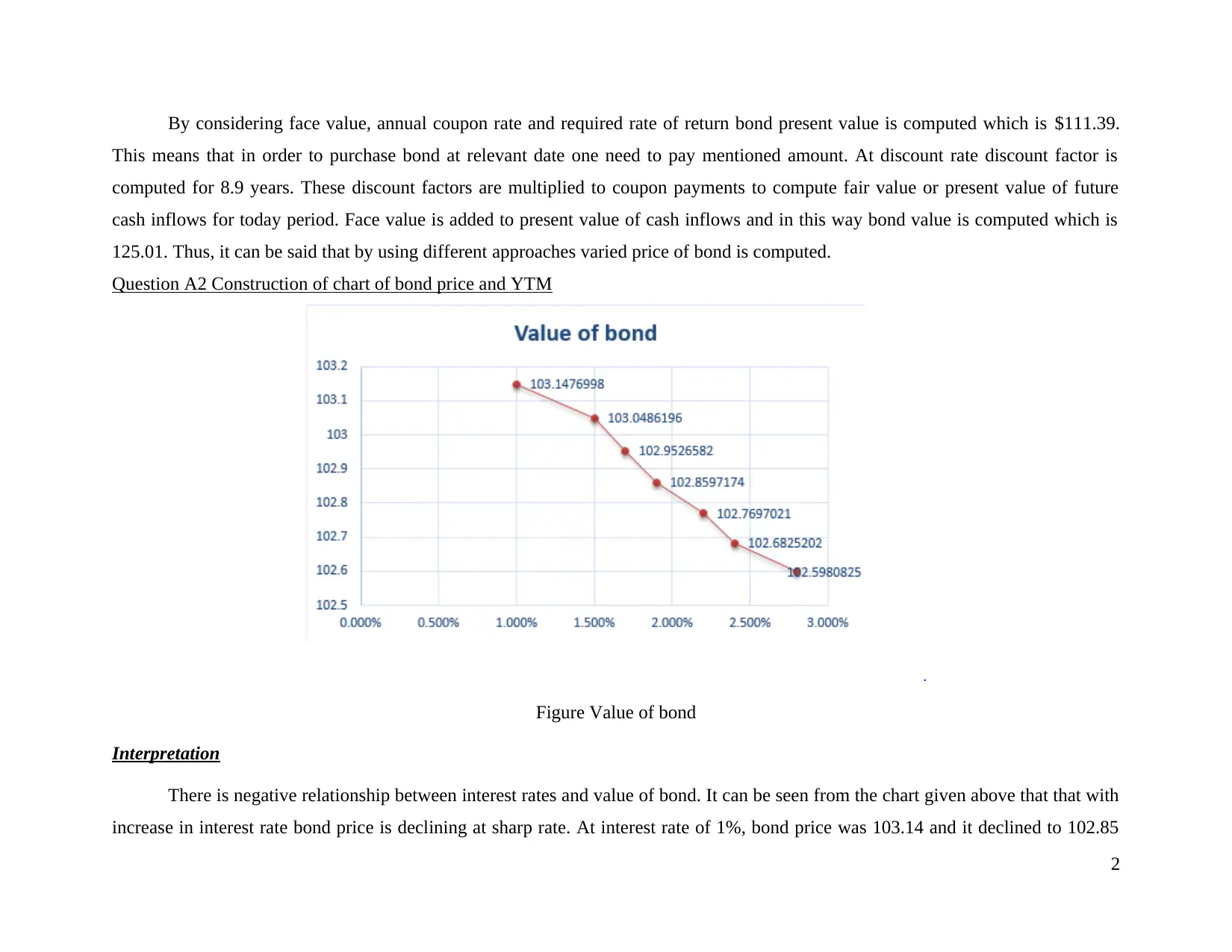

Question A2 Construction of chart of bond price and YTM

Figure Value of bond

Interpretation

There is negative relationship between interest rates and value of bond. It can be seen from the chart given above that that with

increase in interest rate bond price is declining at sharp rate. At interest rate of 1%, bond price was 103.14 and it declined to 102.85

2

This means that in order to purchase bond at relevant date one need to pay mentioned amount. At discount rate discount factor is

computed for 8.9 years. These discount factors are multiplied to coupon payments to compute fair value or present value of future

cash inflows for today period. Face value is added to present value of cash inflows and in this way bond value is computed which is

125.01. Thus, it can be said that by using different approaches varied price of bond is computed.

Question A2 Construction of chart of bond price and YTM

Figure Value of bond

Interpretation

There is negative relationship between interest rates and value of bond. It can be seen from the chart given above that that with

increase in interest rate bond price is declining at sharp rate. At interest rate of 1%, bond price was 103.14 and it declined to 102.85

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

when interest rate increased to 2%. Further, when interest rate hiked to 3% and its price reduced to 102.59. This happened because

coupon payment on bond is certain. On face, value of 100 interest rate is 3.25% and accordingly coupon interest will be 3.25. If bond

price increase to 110 then in that case also coupon will be 3.25, instead those who make investment in bond at this point of time are

earning return of 110*3.25%= 3.57 (Tune, K., 2016). Hence, with increase in bond price bondholders face loss in terms of coupon

amount they receive on yearly basis. Thus, with increase in interest rate bond price reduced.

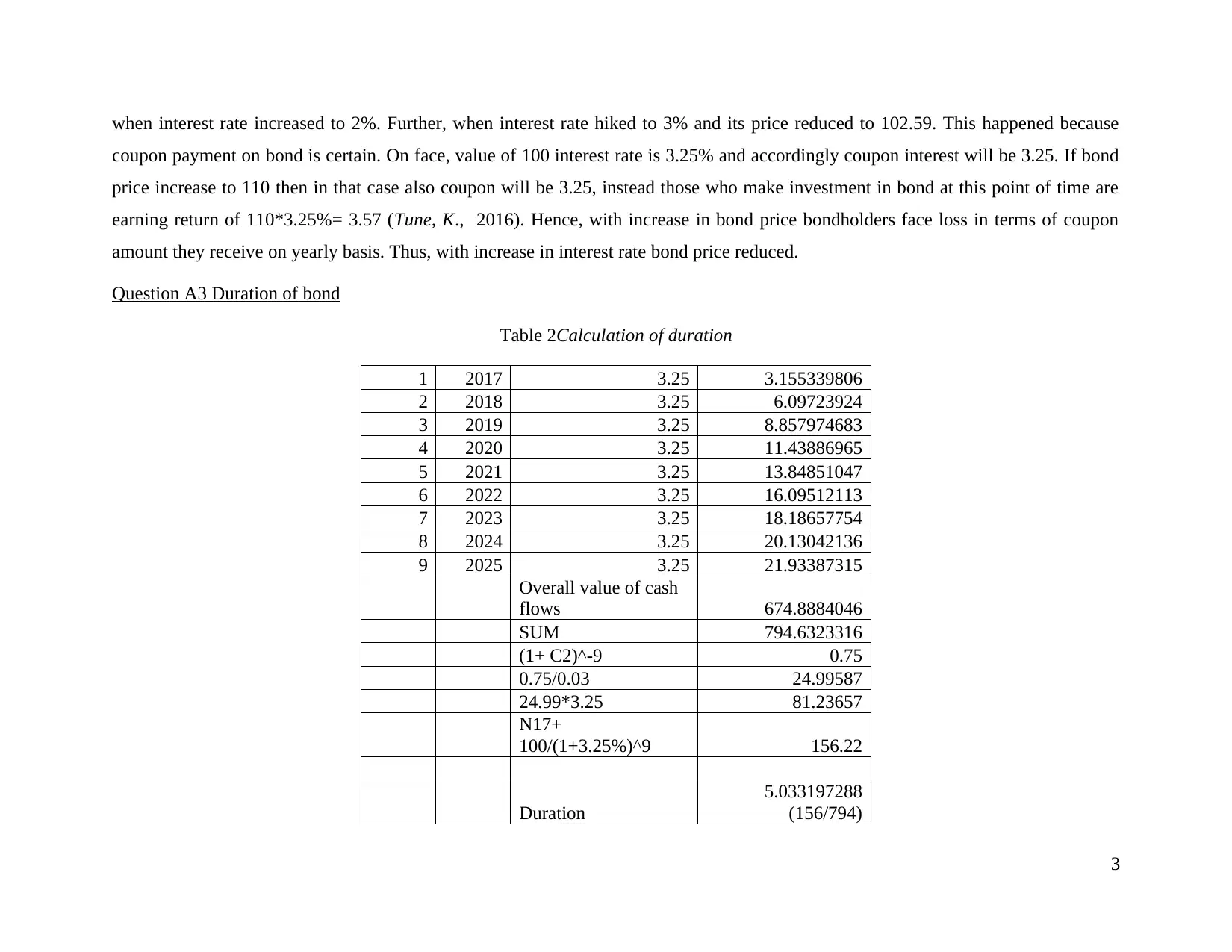

Question A3 Duration of bond

Table 2Calculation of duration

1 2017 3.25 3.155339806

2 2018 3.25 6.09723924

3 2019 3.25 8.857974683

4 2020 3.25 11.43886965

5 2021 3.25 13.84851047

6 2022 3.25 16.09512113

7 2023 3.25 18.18657754

8 2024 3.25 20.13042136

9 2025 3.25 21.93387315

Overall value of cash

flows 674.8884046

SUM 794.6323316

(1+ C2)^-9 0.75

0.75/0.03 24.99587

24.99*3.25 81.23657

N17+

100/(1+3.25%)^9 156.22

Duration

5.033197288

(156/794)

3

coupon payment on bond is certain. On face, value of 100 interest rate is 3.25% and accordingly coupon interest will be 3.25. If bond

price increase to 110 then in that case also coupon will be 3.25, instead those who make investment in bond at this point of time are

earning return of 110*3.25%= 3.57 (Tune, K., 2016). Hence, with increase in bond price bondholders face loss in terms of coupon

amount they receive on yearly basis. Thus, with increase in interest rate bond price reduced.

Question A3 Duration of bond

Table 2Calculation of duration

1 2017 3.25 3.155339806

2 2018 3.25 6.09723924

3 2019 3.25 8.857974683

4 2020 3.25 11.43886965

5 2021 3.25 13.84851047

6 2022 3.25 16.09512113

7 2023 3.25 18.18657754

8 2024 3.25 20.13042136

9 2025 3.25 21.93387315

Overall value of cash

flows 674.8884046

SUM 794.6323316

(1+ C2)^-9 0.75

0.75/0.03 24.99587

24.99*3.25 81.23657

N17+

100/(1+3.25%)^9 156.22

Duration

5.033197288

(156/794)

3

Bond duration is 5 years, which can be considered moderate sensitive in terms of maturity date. Price of bond may change by

5% with 1% change in interest rate or YTM. Bond is sensitive to interest rate change because more is the duration of bond it become

hard task to make prediction of likely changes that may be observed in interest rate (Duration and convexity, 2017). Due to turmoil in

market investors make wrong decisions many times and due to this reason more is the duration of bond security is sensitive to interest

rate change. In short, period one can predict likely changes that may be observed in economic environment and changes that may be

seen in interest rate structure . It is easy to make decisions in respect to bond that are nearby to maturity date. Hence, such kind of

bonds is less sensitive to interest rate change.

PART B

Question B1 Use of Futures to hedge or speculate

Futures are the type of derivative contract that are used to earn profit when securities that are hold in stock market are at risk.

Future contract are simply a promise to make purchase of specific units of instrument at agreed price on specific date irrespective to

price at which shares are traded in the stock exchange. Futures are used to hedge by the business firms. Usually firms, make an

investment in shares in the stock exchange but it are exposed to market risk (Zanotti, Gabbi. and Geranio, 2010). In such kind of

situation, firm main target is to earn profit on future if it faces loss on its open positions so that loss faced on investment can be offset

from profit that is earned on futures. Way in which futures are used to hedge can be understand from simple example suppose 500

units of GlaxoSmithKline are purchased at specific price and market is bullish but it is expected that due to small fluctuations share

price may decline and loss can be faced on investment. In order to maintain profit of determined amount investment can be made in

future contract. Under this, future contract of specific month at specific price can be purchased where deal to purchase

GlaxoSmithKline shares at low price then current market price can be locked. In case down turn happened in the market firm can sell

future contract at current market price and extra profit can be earned. To some extent or completely loss that is faced on open positions

is covered by profit that is gained on futures. Thus, it can be said that futures can be used for hedging purpose.

4

5% with 1% change in interest rate or YTM. Bond is sensitive to interest rate change because more is the duration of bond it become

hard task to make prediction of likely changes that may be observed in interest rate (Duration and convexity, 2017). Due to turmoil in

market investors make wrong decisions many times and due to this reason more is the duration of bond security is sensitive to interest

rate change. In short, period one can predict likely changes that may be observed in economic environment and changes that may be

seen in interest rate structure . It is easy to make decisions in respect to bond that are nearby to maturity date. Hence, such kind of

bonds is less sensitive to interest rate change.

PART B

Question B1 Use of Futures to hedge or speculate

Futures are the type of derivative contract that are used to earn profit when securities that are hold in stock market are at risk.

Future contract are simply a promise to make purchase of specific units of instrument at agreed price on specific date irrespective to

price at which shares are traded in the stock exchange. Futures are used to hedge by the business firms. Usually firms, make an

investment in shares in the stock exchange but it are exposed to market risk (Zanotti, Gabbi. and Geranio, 2010). In such kind of

situation, firm main target is to earn profit on future if it faces loss on its open positions so that loss faced on investment can be offset

from profit that is earned on futures. Way in which futures are used to hedge can be understand from simple example suppose 500

units of GlaxoSmithKline are purchased at specific price and market is bullish but it is expected that due to small fluctuations share

price may decline and loss can be faced on investment. In order to maintain profit of determined amount investment can be made in

future contract. Under this, future contract of specific month at specific price can be purchased where deal to purchase

GlaxoSmithKline shares at low price then current market price can be locked. In case down turn happened in the market firm can sell

future contract at current market price and extra profit can be earned. To some extent or completely loss that is faced on open positions

is covered by profit that is gained on futures. Thus, it can be said that futures can be used for hedging purpose.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Hedging is also used for speculation purpose because under this if one expect that market will move upward or downward it

can take decisions in respect to purchase or sale of security (Chang, González-Serrano and Jimenez-Martin, 2013). There is little

difference between hedging and speculation, which is that in case of former one with specific objective, and by considering facts one

make investment. Whereas, in latter one by just making estimation investment are made. Hence, future is used for both hedging and

speculation purpose.

Question B2.1 Justification on hedging and speculation

According to the given case scenario, hedging has been performed by MG. It entered into future contracts that it will sell a

certain amount of petroleum every month for next 10 years. In order to mitigate the risk, it entered into another contract stating that it

will get petroleum at a fixed price. It will act as a measure and saviour if petroleum prices shoot up. However, the p[rices went down

leading the company ton land into losses. The investment was made to mitigate risk of first contract but the other contract itself went

to the riskier side. On the contrary, the first future proved to be profitable for the company. Hence, a bit of speculation was also

involved in the given case scenario.

Hedging is the investment made by an individual or a company to mitigate the losses that can take place in the company due to

price movements (Acharya, Lochstoer and Ramadorai, 2013). Swaps, forward, future contracts are considered to be hedging so that

losses can be reduced to the minimum. However, speculation is a trading activity having equal chances of profit and loss and

investment have been made with an intention to earn higher profits. According to the case, investment was made with the view to

mitigate the risk but it went into loses in the end which proves that a bit of speculation was involved in the investment of futures made

by the company.

Hedging is a risky investment strategy and if not proved right it can bring losses to the organization as in the case of MG. The

company made an investment to mitigate the risk of first future contract but the later contract led it to losses. Moreover, speculation is

riskier in comparison to hedge as it has equal chances of gain and loss. The company went for hedging but risk of investment was still

prevailing which shows that there was speculation present in the hedging activity as well.

5

can take decisions in respect to purchase or sale of security (Chang, González-Serrano and Jimenez-Martin, 2013). There is little

difference between hedging and speculation, which is that in case of former one with specific objective, and by considering facts one

make investment. Whereas, in latter one by just making estimation investment are made. Hence, future is used for both hedging and

speculation purpose.

Question B2.1 Justification on hedging and speculation

According to the given case scenario, hedging has been performed by MG. It entered into future contracts that it will sell a

certain amount of petroleum every month for next 10 years. In order to mitigate the risk, it entered into another contract stating that it

will get petroleum at a fixed price. It will act as a measure and saviour if petroleum prices shoot up. However, the p[rices went down

leading the company ton land into losses. The investment was made to mitigate risk of first contract but the other contract itself went

to the riskier side. On the contrary, the first future proved to be profitable for the company. Hence, a bit of speculation was also

involved in the given case scenario.

Hedging is the investment made by an individual or a company to mitigate the losses that can take place in the company due to

price movements (Acharya, Lochstoer and Ramadorai, 2013). Swaps, forward, future contracts are considered to be hedging so that

losses can be reduced to the minimum. However, speculation is a trading activity having equal chances of profit and loss and

investment have been made with an intention to earn higher profits. According to the case, investment was made with the view to

mitigate the risk but it went into loses in the end which proves that a bit of speculation was involved in the investment of futures made

by the company.

Hedging is a risky investment strategy and if not proved right it can bring losses to the organization as in the case of MG. The

company made an investment to mitigate the risk of first future contract but the later contract led it to losses. Moreover, speculation is

riskier in comparison to hedge as it has equal chances of gain and loss. The company went for hedging but risk of investment was still

prevailing which shows that there was speculation present in the hedging activity as well.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question B2.2 main purpose of hedge using futures

A company invest in futures when it is aware that the price of a particular product are going to rise in the near future.

Therefore, in order to mitigate the risk and get the product at present prices, entities or individual;s enter into future contracts. Hence,

hedging through futures helps in assessing the risk and mitigating it. It reduces the risk that a company can go through. There are two

main components that are required to be considered while investing in futures. They are:

Choice of asset underlying in future contracts: It becomes easy if the same product is received in suture contract as well.

However, in other circumstances, it is important that the entity make rigorous analysis in order to make prudent investment

decision. The alternative product chosen must have the prices that are significantly correlated to the asset being hedged by the

company. It shows if the prices changes of the one product than it will have a significant impact on the other as well that has

been hedged. Hence, appropriate analysis is required to be made by the company in order to find the asset which is closely

linked to the product for which future contract has been made.

Choice of delivery month: It is another important point that is required to be considered while investing in future contract. It

is influenced by various factors. The delivery month is chosen in alignment to the expiration of the hedge fund when delivery

is required to be made. There are chances that the prices of the futures become risky at the time of delivery month. Taking

delivery at the time of hedge may be inconvenient and expensive option for the entity. Hence, it should be a bit later in

comparison to that of the futures.

Moreover, the risk of the contract increases as the time between hedge expiration and delivery is more. Hence, the best option

is to choose the delivery month which is close to the expiration of the hedge but a bit later as well, say, a month or too.

Hence, these are two important aspects that are required to be considered while taking decisions of investment so that the

company do not fee burdened and it can mitigate the losses to serve the purpose for which another contract has been made the

enterprise. Moreover, futures also help in assessing that whether it will prove to be beneficial for the company opt not. Hence,

speculation in the futures are also involved as if the prices went down then the company can lead to losses as well.

6

A company invest in futures when it is aware that the price of a particular product are going to rise in the near future.

Therefore, in order to mitigate the risk and get the product at present prices, entities or individual;s enter into future contracts. Hence,

hedging through futures helps in assessing the risk and mitigating it. It reduces the risk that a company can go through. There are two

main components that are required to be considered while investing in futures. They are:

Choice of asset underlying in future contracts: It becomes easy if the same product is received in suture contract as well.

However, in other circumstances, it is important that the entity make rigorous analysis in order to make prudent investment

decision. The alternative product chosen must have the prices that are significantly correlated to the asset being hedged by the

company. It shows if the prices changes of the one product than it will have a significant impact on the other as well that has

been hedged. Hence, appropriate analysis is required to be made by the company in order to find the asset which is closely

linked to the product for which future contract has been made.

Choice of delivery month: It is another important point that is required to be considered while investing in future contract. It

is influenced by various factors. The delivery month is chosen in alignment to the expiration of the hedge fund when delivery

is required to be made. There are chances that the prices of the futures become risky at the time of delivery month. Taking

delivery at the time of hedge may be inconvenient and expensive option for the entity. Hence, it should be a bit later in

comparison to that of the futures.

Moreover, the risk of the contract increases as the time between hedge expiration and delivery is more. Hence, the best option

is to choose the delivery month which is close to the expiration of the hedge but a bit later as well, say, a month or too.

Hence, these are two important aspects that are required to be considered while taking decisions of investment so that the

company do not fee burdened and it can mitigate the losses to serve the purpose for which another contract has been made the

enterprise. Moreover, futures also help in assessing that whether it will prove to be beneficial for the company opt not. Hence,

speculation in the futures are also involved as if the prices went down then the company can lead to losses as well.

6

Question B2.3 Criticality of maturity mismatch

Maturity mismatch is a condition in the company's balance sheet when the company have higher short term liabilities in

comparison to that of short term assets or vice versa. In case of MG, the company have entered into forward contract where it has

committed to sell certain amount of petroleum at a fixed price for next 10 years. In order to mitigate the risk, it has also entered into

futures so that it position can be hedged. To the contrary, energy prices rose leaving the company into heavy losses due to entering

into futures which was typically for hedging. The maturity of the contract as the short term obligation of the company is more as

compared to that of short term asset.

Moreover, the company have entered into roll over hedging contract which can be continued or stop as per the prevailing

prices of the product. If the company opt for roll-over it may have to analyse the interest rate all over again as per the availability of

the futures. Hence, maturity mismatch is a key factor which is critical and required to be considered while deciding that whether the

company will earn profits through the hedge or it has to incur losses.

Further, another aspect to be analysed is that direct hedges eliminates the risk if they are continued upto the expiration of the

future contracts. Hence, the hedge in which MG have entered is a mismatch because it does not prove to be profitable for the

company. It created short term losses for MG.

7

Maturity mismatch is a condition in the company's balance sheet when the company have higher short term liabilities in

comparison to that of short term assets or vice versa. In case of MG, the company have entered into forward contract where it has

committed to sell certain amount of petroleum at a fixed price for next 10 years. In order to mitigate the risk, it has also entered into

futures so that it position can be hedged. To the contrary, energy prices rose leaving the company into heavy losses due to entering

into futures which was typically for hedging. The maturity of the contract as the short term obligation of the company is more as

compared to that of short term asset.

Moreover, the company have entered into roll over hedging contract which can be continued or stop as per the prevailing

prices of the product. If the company opt for roll-over it may have to analyse the interest rate all over again as per the availability of

the futures. Hence, maturity mismatch is a key factor which is critical and required to be considered while deciding that whether the

company will earn profits through the hedge or it has to incur losses.

Further, another aspect to be analysed is that direct hedges eliminates the risk if they are continued upto the expiration of the

future contracts. Hence, the hedge in which MG have entered is a mismatch because it does not prove to be profitable for the

company. It created short term losses for MG.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART C

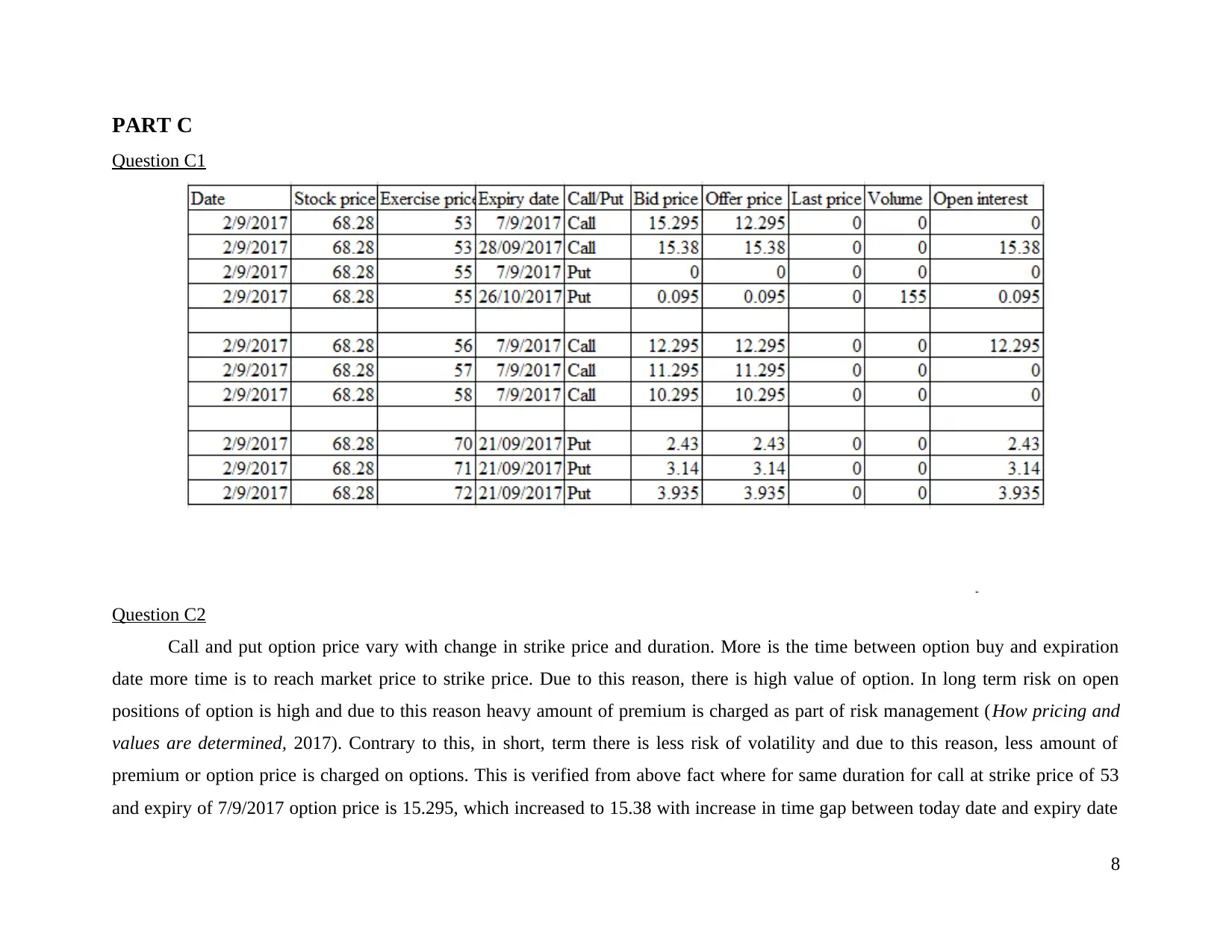

Question C1

Question C2

Call and put option price vary with change in strike price and duration. More is the time between option buy and expiration

date more time is to reach market price to strike price. Due to this reason, there is high value of option. In long term risk on open

positions of option is high and due to this reason heavy amount of premium is charged as part of risk management (How pricing and

values are determined, 2017). Contrary to this, in short, term there is less risk of volatility and due to this reason, less amount of

premium or option price is charged on options. This is verified from above fact where for same duration for call at strike price of 53

and expiry of 7/9/2017 option price is 15.295, which increased to 15.38 with increase in time gap between today date and expiry date

8

Question C1

Question C2

Call and put option price vary with change in strike price and duration. More is the time between option buy and expiration

date more time is to reach market price to strike price. Due to this reason, there is high value of option. In long term risk on open

positions of option is high and due to this reason heavy amount of premium is charged as part of risk management (How pricing and

values are determined, 2017). Contrary to this, in short, term there is less risk of volatility and due to this reason, less amount of

premium or option price is charged on options. This is verified from above fact where for same duration for call at strike price of 53

and expiry of 7/9/2017 option price is 15.295, which increased to 15.38 with increase in time gap between today date and expiry date

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(28/09/2017, call STK price 53). Premium is charged on individuals because in case they do not exercise their right they need to pay

specific amount to other entity. In case duration of expiry is large risk is high and due to heavy loss one can deny from paying

obligatory amount to other entity. In order to prevent this condition as part of risk mitigation high amount of option price is charged on

those contracts whose expiry time is large then those one whose expiry will happened in short duration.

In case of call at low strike price and in case of put at higher strike price heavy option price is charged. This is because if in

case of call gap between call price and current market price increase investor will face heavy risk (Duration and convexity the price

yield relationship, 2017). There is high probability that one may leave its right or not exercise. Again, due to heavy loss one may not

intended to pay obligatory amount to other entity. Hence, to ensure such situation will not occur heavy amount of premium is charged

when call has low and put have high strike price.

CONCLUSION

It is concluded that bond value is heavily affected by duration. More is the time remaining in maturity heavy risk will be

associated with bond. With increase in interest rate bond value decline because investor amount less amount of coupon on investment

as interest rate is fixed on fair value. It is also concluded that option price is heavily affected by duration remaining in expiry of

contract and nearness of strike price to current market price. More is duration less premium will be charged and more is gap between

STK price of call and put relative to CMP premium will be high.

9

specific amount to other entity. In case duration of expiry is large risk is high and due to heavy loss one can deny from paying

obligatory amount to other entity. In order to prevent this condition as part of risk mitigation high amount of option price is charged on

those contracts whose expiry time is large then those one whose expiry will happened in short duration.

In case of call at low strike price and in case of put at higher strike price heavy option price is charged. This is because if in

case of call gap between call price and current market price increase investor will face heavy risk (Duration and convexity the price

yield relationship, 2017). There is high probability that one may leave its right or not exercise. Again, due to heavy loss one may not

intended to pay obligatory amount to other entity. Hence, to ensure such situation will not occur heavy amount of premium is charged

when call has low and put have high strike price.

CONCLUSION

It is concluded that bond value is heavily affected by duration. More is the time remaining in maturity heavy risk will be

associated with bond. With increase in interest rate bond value decline because investor amount less amount of coupon on investment

as interest rate is fixed on fair value. It is also concluded that option price is heavily affected by duration remaining in expiry of

contract and nearness of strike price to current market price. More is duration less premium will be charged and more is gap between

STK price of call and put relative to CMP premium will be high.

9

REFERENCES

Books and Journals

Acharya, V. V., Lochstoer, L. A. and Ramadorai, T., 2013. Limits to arbitrage and hedging: Evidence from commodity

markets. Journal of Financial Economics. 109(2). pp.441-465.

Bodie, Z., Kane, A. and Marcus, A. J., 2014. Investments, 10e. McGraw-Hill Education.

Chang, C.L., González-Serrano, L. and Jimenez-Martin, J.A., 2013. Currency hedging strategies using dynamic multivariate

GARCH. Mathematics and Computers in Simulation. 94. pp.164-182.

Hodrick, R., 2014. The empirical evidence on the efficiency of forward and futures foreign exchange markets (Vol. 24). Routledge.

Starrfelt, J. and Kokko, H., 2012. Bet‐hedging—a triple trade‐off between means, variances and correlations. Biological

Reviews. 87(3). pp.742-755.

Van Binsbergen, J. and et.al., 2013. Equity yields. Journal of Financial Economics. 110(3). pp.503-519.

Zanotti, G., Gabbi, G. and Geranio, M., 2010. Hedging with futures: Efficacy of GARCH correlation models to European electricity

markets. Journal of International Financial Markets, Institutions and Money. 20(2). pp.135-148.

Online

Duration and convexity the price yield relationship, 2017. [Online]. Available through:< https://www.raymondjames.com/wealth-

management/advice-products-and-services/investment-solutions/fixed-income/bond-basics/duration-and-convexity>. >.

[Accessed on 2nd September 2017].

Duration and convexity, 2017. [Online]. Available through:< http://thismatter.com/money/bonds/duration-convexity.htm>. [Accessed

on 2nd September 2017].

How pricing and values are determined, 2017.[Online]. Available through :< http://www.investorguide.com/article/11811/options-

how-pricing-and-value-are-determined-igu/>. [Accessed on 2nd September 2017].

10

Books and Journals

Acharya, V. V., Lochstoer, L. A. and Ramadorai, T., 2013. Limits to arbitrage and hedging: Evidence from commodity

markets. Journal of Financial Economics. 109(2). pp.441-465.

Bodie, Z., Kane, A. and Marcus, A. J., 2014. Investments, 10e. McGraw-Hill Education.

Chang, C.L., González-Serrano, L. and Jimenez-Martin, J.A., 2013. Currency hedging strategies using dynamic multivariate

GARCH. Mathematics and Computers in Simulation. 94. pp.164-182.

Hodrick, R., 2014. The empirical evidence on the efficiency of forward and futures foreign exchange markets (Vol. 24). Routledge.

Starrfelt, J. and Kokko, H., 2012. Bet‐hedging—a triple trade‐off between means, variances and correlations. Biological

Reviews. 87(3). pp.742-755.

Van Binsbergen, J. and et.al., 2013. Equity yields. Journal of Financial Economics. 110(3). pp.503-519.

Zanotti, G., Gabbi, G. and Geranio, M., 2010. Hedging with futures: Efficacy of GARCH correlation models to European electricity

markets. Journal of International Financial Markets, Institutions and Money. 20(2). pp.135-148.

Online

Duration and convexity the price yield relationship, 2017. [Online]. Available through:< https://www.raymondjames.com/wealth-

management/advice-products-and-services/investment-solutions/fixed-income/bond-basics/duration-and-convexity>. >.

[Accessed on 2nd September 2017].

Duration and convexity, 2017. [Online]. Available through:< http://thismatter.com/money/bonds/duration-convexity.htm>. [Accessed

on 2nd September 2017].

How pricing and values are determined, 2017.[Online]. Available through :< http://www.investorguide.com/article/11811/options-

how-pricing-and-value-are-determined-igu/>. [Accessed on 2nd September 2017].

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.