Evaluating Risk Impact & Mitigation in Financial Derivatives Contracts

VerifiedAdded on 2023/06/10

|6

|556

|381

Report

AI Summary

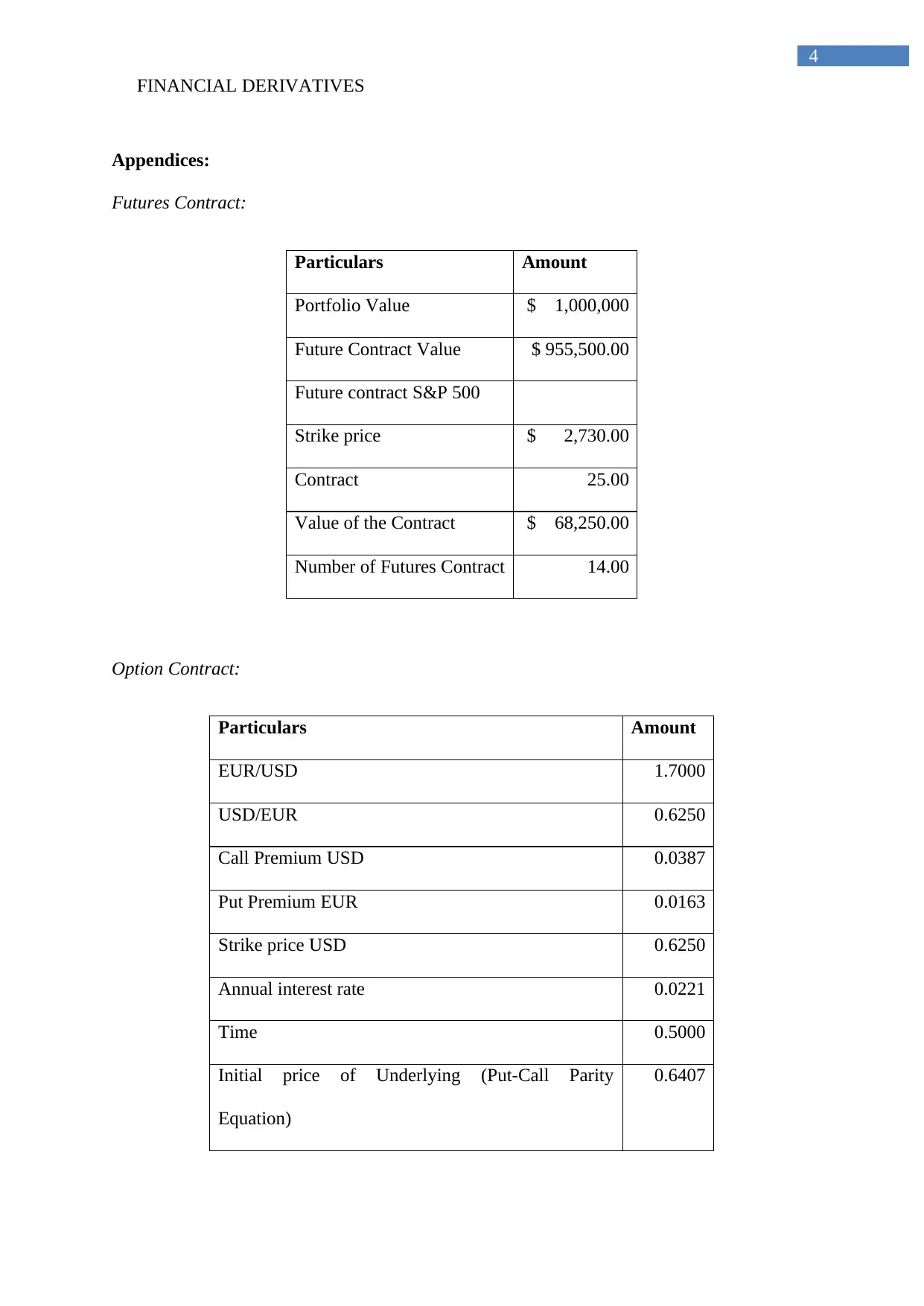

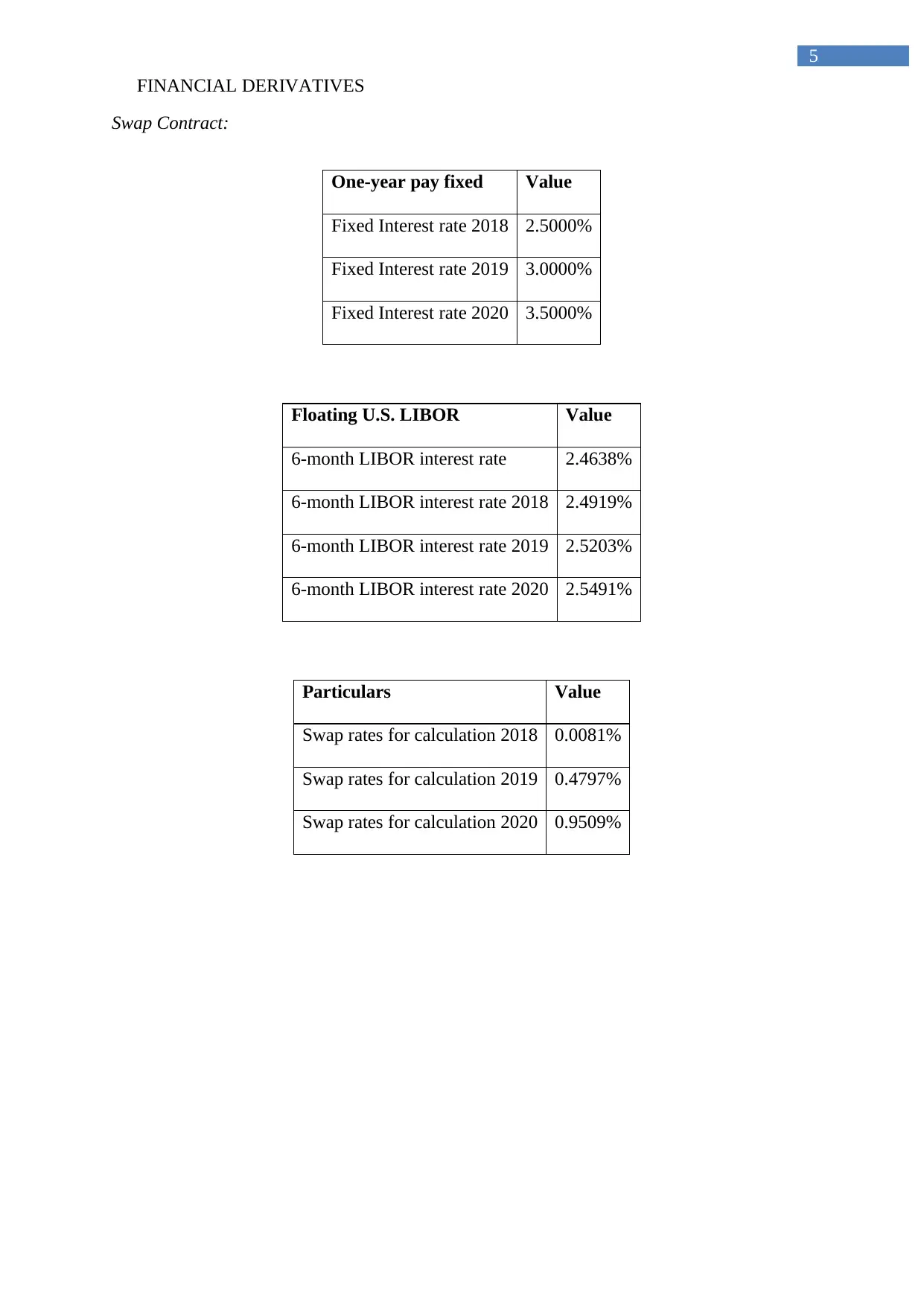

This report examines the use of financial derivatives—specifically futures, options, and swaps—by an investment banker to generate revenue and prevent financial loss. It calculates the potential risk impact of extrinsic and intrinsic factors for mitigating risk values. The analysis focuses on how futures contracts compensate for negative changes in the S&P 500, reducing portfolio risk. Shorting options helps minimize investment risk and control profits. Option contracts manage put-call parity, mitigating currency exchange impacts and maximizing profits. Swap contracts improve investment returns by potentially changing interest rates from LIBOR to fixed rates, minimizing interest payments. Appendices provide detailed calculations for futures, options, and swap contracts, including contract values, premiums, interest rates, and swap rates.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.