Descriptive and Inferential Data Analysis Report - United Health Group

VerifiedAdded on 2023/06/14

|26

|2779

|470

Report

AI Summary

This report presents a data analysis of insurance claims, employing descriptive and inferential statistics. Descriptive statistics highlight an average claim payment of $73457.49, with a 95% probability of claims falling between $68970.58 and $77944.41. The average claimant age is 44.49 years, with a 95% confidence interval between 42.02 and 46.96 years. Hypothesis testing reveals that the average paid claim amount is likely below $77,500, and the proportion of 'MILD' or 'MEDIUM' severity claims is at least 75%. Gender significantly impacts claim severity proportions. Claim amounts are higher when claimants have private attorneys. The proportion of private attorney representation is similar for both 'SEVERE' and 'MEDIUM' claims. Finally, the analysis indicates that the percentage of 'SEVERE' claims does not significantly differ between Orthopaedic surgeons and other specialists, and the average claim amount for 'SEVERE' severity is not higher for Orthopaedic surgeons.

Running head: DATA ANALYSIS

Descriptive and Inferential Analytics

Name of the Student:

Name of the University:

Author’s Note:

Descriptive and Inferential Analytics

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1DATA ANALYSIS

Table of Contents

Introduction:...............................................................................................................................2

1. Descriptive Statistics:.............................................................................................................2

2. Estimation:.........................................................................................................................2

2.a)......................................................................................................................................2

2. b)....................................................................................................................................3

Answer 3................................................................................................................................3

3.a)......................................................................................................................................3

3. b)....................................................................................................................................3

3.c)......................................................................................................................................4

3.d).....................................................................................................................................4

3. e).....................................................................................................................................4

Answer 4................................................................................................................................5

4. a).....................................................................................................................................5

4.b).....................................................................................................................................5

Conclusion:................................................................................................................................6

References:.................................................................................................................................7

Appendix:...................................................................................................................................8

Table of Contents

Introduction:...............................................................................................................................2

1. Descriptive Statistics:.............................................................................................................2

2. Estimation:.........................................................................................................................2

2.a)......................................................................................................................................2

2. b)....................................................................................................................................3

Answer 3................................................................................................................................3

3.a)......................................................................................................................................3

3. b)....................................................................................................................................3

3.c)......................................................................................................................................4

3.d).....................................................................................................................................4

3. e).....................................................................................................................................4

Answer 4................................................................................................................................5

4. a).....................................................................................................................................5

4.b).....................................................................................................................................5

Conclusion:................................................................................................................................6

References:.................................................................................................................................7

Appendix:...................................................................................................................................8

2DATA ANALYSIS

Table of Tables

Table 1......................................................................................................................................12

Table 2......................................................................................................................................12

Table 3......................................................................................................................................12

Table 4......................................................................................................................................13

Table 5......................................................................................................................................14

Table 6......................................................................................................................................15

Table 7.1...................................................................................................................................17

Table 7.2……………………………………………………………………………………...18

Table 8......................................................................................................................................20

Table 9......................................................................................................................................22

Table 10.1.................................................................................................................................23

Table 10.2……………………………………………………………………………………24

Table of Figures

Figure 1....................................................................................................................................13

Figure 2....................................................................................................................................14

Figure 3....................................................................................................................................15

Figure 4....................................................................................................................................16

Figure 5....................................................................................................................................19

Figure 6....................................................................................................................................21

Figure 7....................................................................................................................................24

Figure 8....................................................................................................................................26

Table of Tables

Table 1......................................................................................................................................12

Table 2......................................................................................................................................12

Table 3......................................................................................................................................12

Table 4......................................................................................................................................13

Table 5......................................................................................................................................14

Table 6......................................................................................................................................15

Table 7.1...................................................................................................................................17

Table 7.2……………………………………………………………………………………...18

Table 8......................................................................................................................................20

Table 9......................................................................................................................................22

Table 10.1.................................................................................................................................23

Table 10.2……………………………………………………………………………………24

Table of Figures

Figure 1....................................................................................................................................13

Figure 2....................................................................................................................................14

Figure 3....................................................................................................................................15

Figure 4....................................................................................................................................16

Figure 5....................................................................................................................................19

Figure 6....................................................................................................................................21

Figure 7....................................................................................................................................24

Figure 8....................................................................................................................................26

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3DATA ANALYSIS

To: You

From: Edmond Kendrick

Subject: Analysis of Claims

As per earlier discussion, I have cleaned and simplified the undertaken dataset to eight

variables for your convenience. The cleaned dataset contains information about 200 randomly

selected claims promised this year.

Introduction:

The case study of United Health Group that is the America’s most vibrant provider of health

insurance displays that medical malpractice is developing in USA health-centres. The

previous research on a huge amount of data refers that almost 2.4% of annual health-care

spending is being wasted due to medical malpractices. Another study indicated that in the

time span 1991 to 2005, 7.4% of the licensed physicians were claiming malpractice in USA.

Such type of trend is a major concern for common people and patients.

The data under consideration in this research report justifies the ground situation of medical

malpractices. The analysis may display the numbers of successful malpractice claims that is

recently contributing the high premiums for medical insurance due to malpractice.

1. Descriptive Statistics:

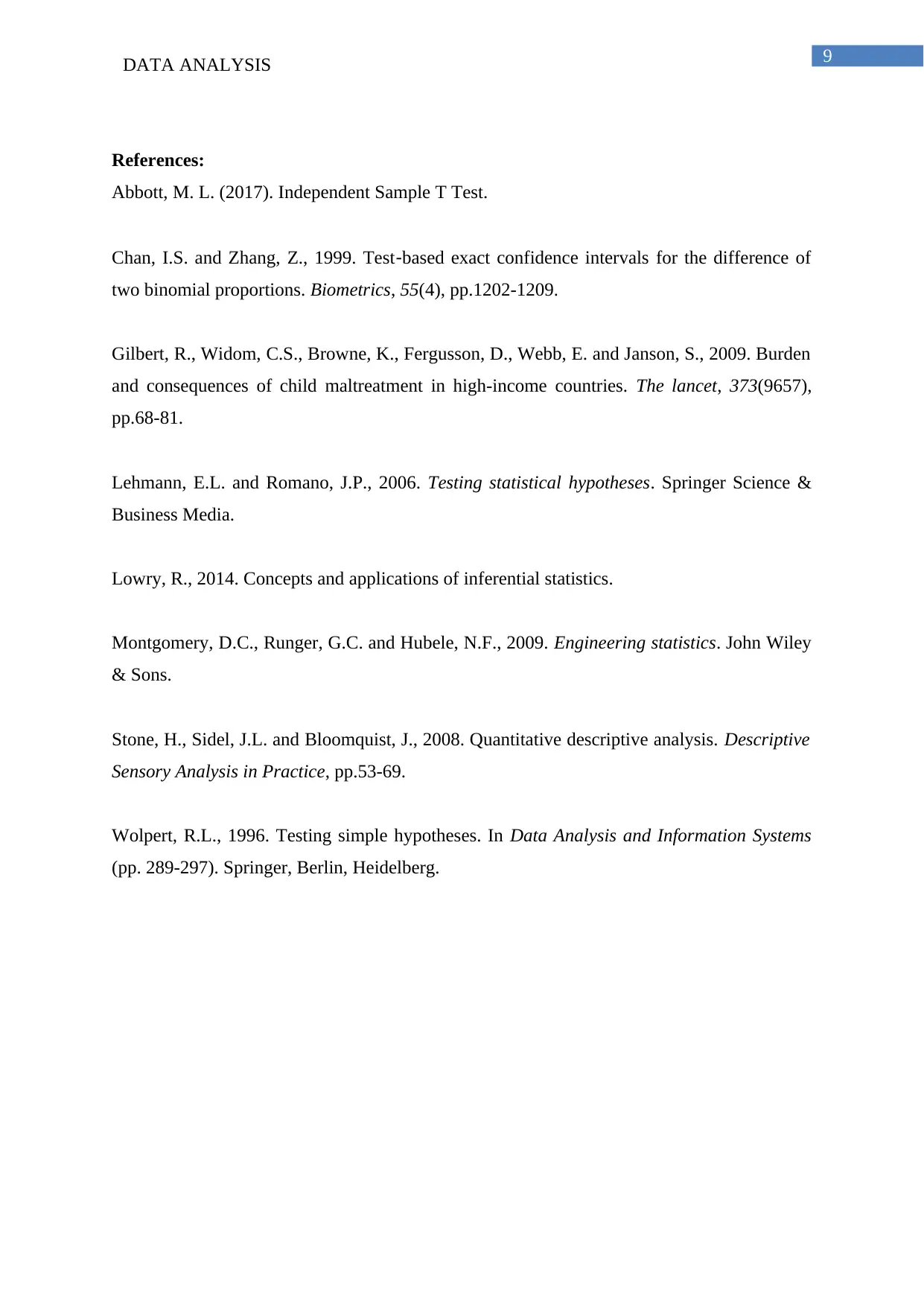

The descriptive or summary statistics of Claim payment amount of 200 samples refers that

the average amount of the claim payment is $73457.49. The lowest amount of claim payment

is $1547and the highest amount of claim payment is $228724.8 with the range of amount of

claim payment $227177.8. There is 95% probability where an observation of claiming

amount lies in the interval of $(73457.49±4486.92) or ($77944.41, $68970.58) (Stone, Sidel

and Bloomquist 2008).

2. Estimation:

2.a)

Firstly, to find the average age of claimants, we observe that-

To: You

From: Edmond Kendrick

Subject: Analysis of Claims

As per earlier discussion, I have cleaned and simplified the undertaken dataset to eight

variables for your convenience. The cleaned dataset contains information about 200 randomly

selected claims promised this year.

Introduction:

The case study of United Health Group that is the America’s most vibrant provider of health

insurance displays that medical malpractice is developing in USA health-centres. The

previous research on a huge amount of data refers that almost 2.4% of annual health-care

spending is being wasted due to medical malpractices. Another study indicated that in the

time span 1991 to 2005, 7.4% of the licensed physicians were claiming malpractice in USA.

Such type of trend is a major concern for common people and patients.

The data under consideration in this research report justifies the ground situation of medical

malpractices. The analysis may display the numbers of successful malpractice claims that is

recently contributing the high premiums for medical insurance due to malpractice.

1. Descriptive Statistics:

The descriptive or summary statistics of Claim payment amount of 200 samples refers that

the average amount of the claim payment is $73457.49. The lowest amount of claim payment

is $1547and the highest amount of claim payment is $228724.8 with the range of amount of

claim payment $227177.8. There is 95% probability where an observation of claiming

amount lies in the interval of $(73457.49±4486.92) or ($77944.41, $68970.58) (Stone, Sidel

and Bloomquist 2008).

2. Estimation:

2.a)

Firstly, to find the average age of claimants, we observe that-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4DATA ANALYSIS

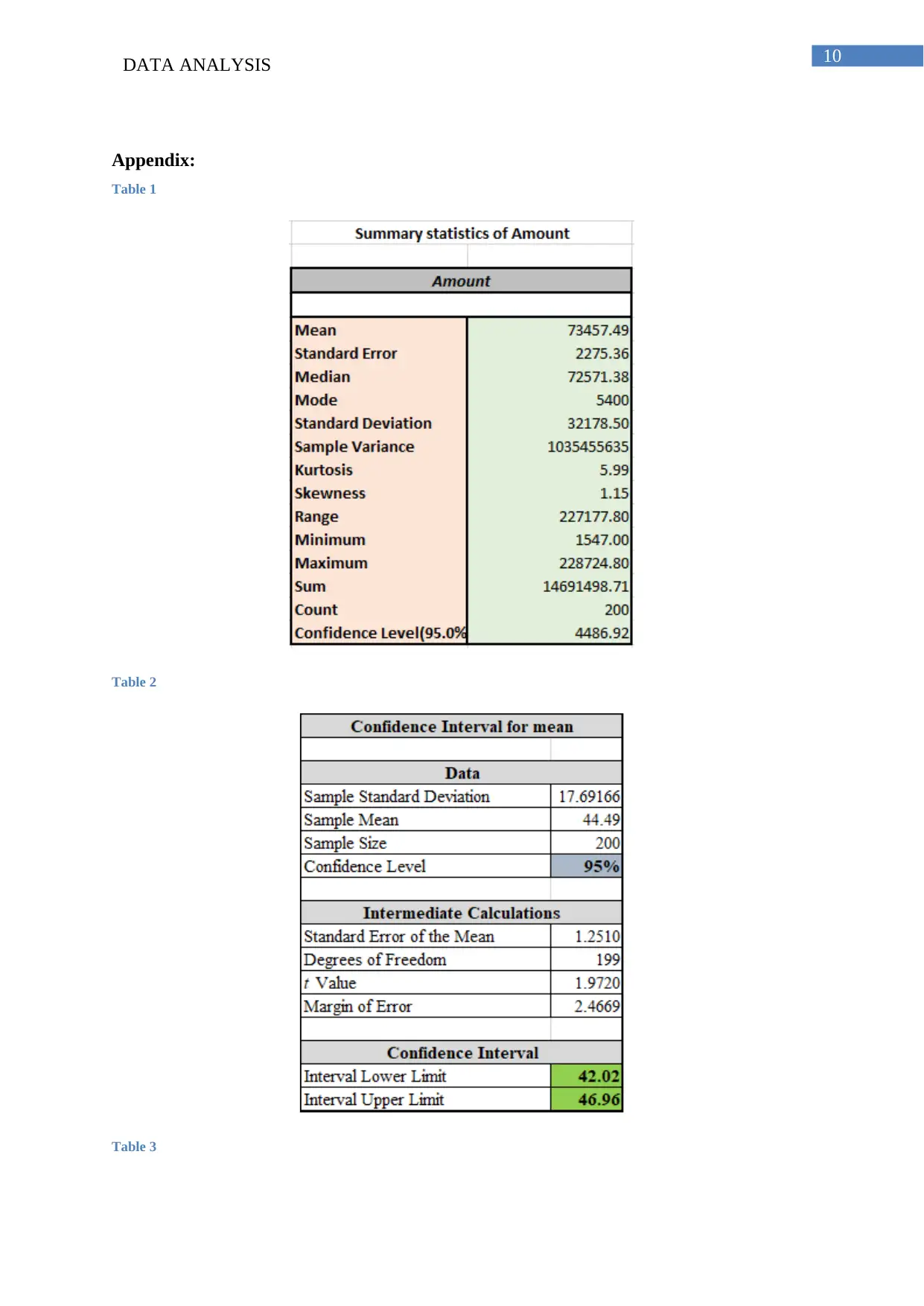

The average age of the insurance claimants is 44.49 years. The interval lower limit of 95%

confidence interval is (44.49-2.4669) years or 42.02 years. The interval upper limit of 95%

confidence interval is (44.49+2.4669) years or 46.96 years. Therefore, it is 95% probable that

the average age of all the claimants lie in the limit of 42.02 years and 46.96 years. That

means 95% of the estimated ages of total claimants lie in the range of 42.02 years and 46.96

years.

2. b)

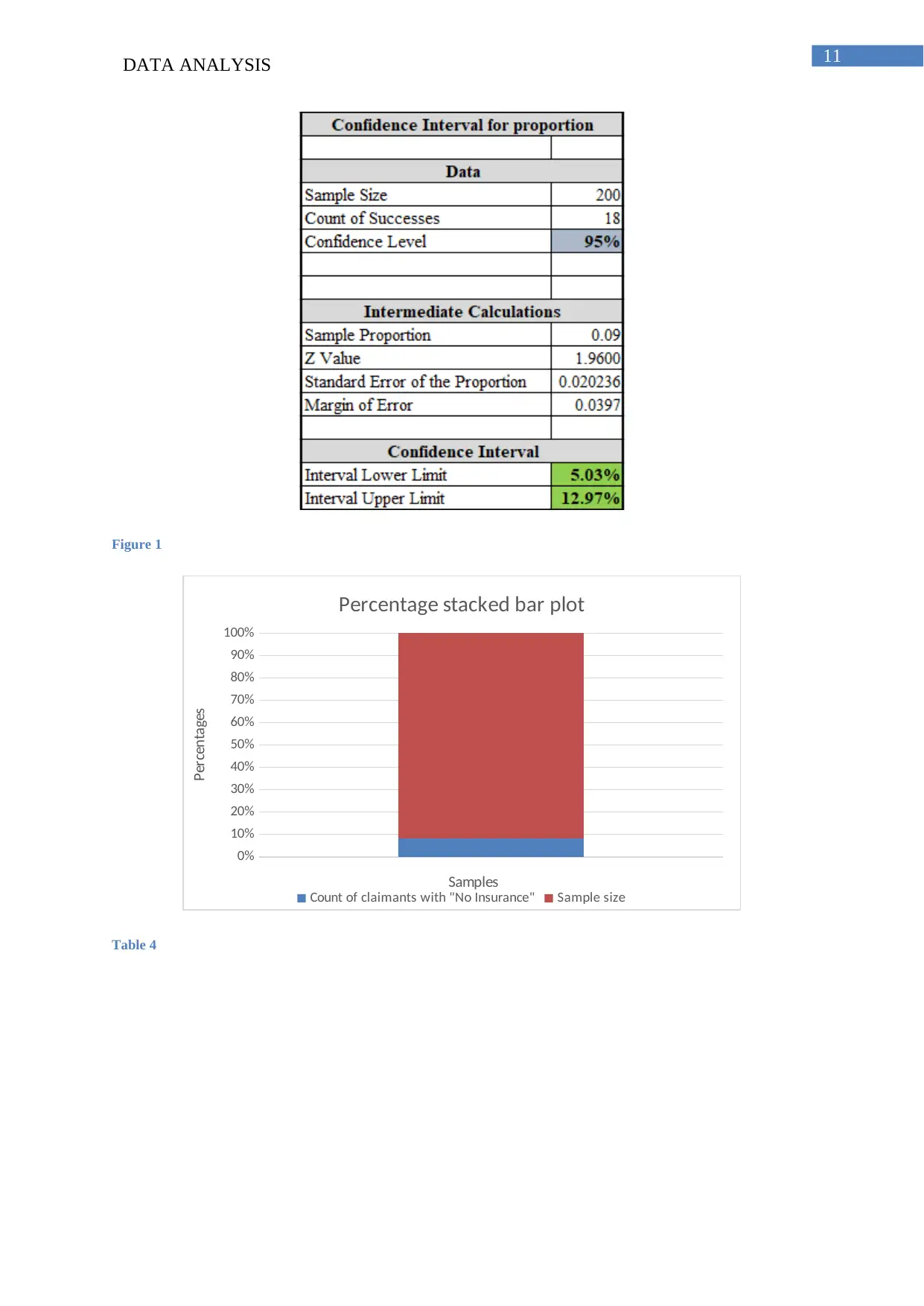

The number of claimants who do not have insurance is 18 among 200 samples. Here number

of samples is 200 and the amount of successes is 18. The proportion of the claimants who do

not have insurance is 0.09.

The upper confidence interval of the proportion of claimants who does not have insurance is

found to be 5.03%. The upper confidence interval of the proportion of claimants who does

not have insurance is found to be 12.97%. Therefore, 95% probability of the estimated

proportion of claimants who do not have insurance lies in the range of 5.03% and 12.97%

(Montgomery, Runger and Hubele 2009).

Answer 3.

3.a)

We construct the basic assertion (H0), where the average paid claim amount is greater than or

equal to $77,500. The alternative assertion (H1), the average of paid claim amount is less than

$77,500.

For the 200 observed claimants, the average of the paid claim amount is $73457.49.

Therefore, with 95% probability, the basic assertion is failed to accept (Lehmann and

Romano 2006). Therefore, it could be interpreted that the mean of paid claiming amount is

below $77,500. At 5% level of significance, there is there is no evidence that the average paid

claim amount is greater than or equal to the proposed amount of industry.

3. b)

A study reported that 3 out of 4 claims (75%) are either “MILD” or “MEDIUM” severity

conditions. Out of 200 people, the number of insurance claimants of “MILD” and

“MEDIUM” severity is 154. The proportion is calculated as 0.77. To find the proportions, the

basic assertion is set that- among every type of severity, the proportion of severity conditions

of “MILD” and “MEDIUM” is less than or equal to 75%. Alternative assertion is assumed as

The average age of the insurance claimants is 44.49 years. The interval lower limit of 95%

confidence interval is (44.49-2.4669) years or 42.02 years. The interval upper limit of 95%

confidence interval is (44.49+2.4669) years or 46.96 years. Therefore, it is 95% probable that

the average age of all the claimants lie in the limit of 42.02 years and 46.96 years. That

means 95% of the estimated ages of total claimants lie in the range of 42.02 years and 46.96

years.

2. b)

The number of claimants who do not have insurance is 18 among 200 samples. Here number

of samples is 200 and the amount of successes is 18. The proportion of the claimants who do

not have insurance is 0.09.

The upper confidence interval of the proportion of claimants who does not have insurance is

found to be 5.03%. The upper confidence interval of the proportion of claimants who does

not have insurance is found to be 12.97%. Therefore, 95% probability of the estimated

proportion of claimants who do not have insurance lies in the range of 5.03% and 12.97%

(Montgomery, Runger and Hubele 2009).

Answer 3.

3.a)

We construct the basic assertion (H0), where the average paid claim amount is greater than or

equal to $77,500. The alternative assertion (H1), the average of paid claim amount is less than

$77,500.

For the 200 observed claimants, the average of the paid claim amount is $73457.49.

Therefore, with 95% probability, the basic assertion is failed to accept (Lehmann and

Romano 2006). Therefore, it could be interpreted that the mean of paid claiming amount is

below $77,500. At 5% level of significance, there is there is no evidence that the average paid

claim amount is greater than or equal to the proposed amount of industry.

3. b)

A study reported that 3 out of 4 claims (75%) are either “MILD” or “MEDIUM” severity

conditions. Out of 200 people, the number of insurance claimants of “MILD” and

“MEDIUM” severity is 154. The proportion is calculated as 0.77. To find the proportions, the

basic assertion is set that- among every type of severity, the proportion of severity conditions

of “MILD” and “MEDIUM” is less than or equal to 75%. Alternative assertion is assumed as

5DATA ANALYSIS

among every type of severity, the proportion of severity conditions of “MILD” and

“MEDIUM” is greater than 75%.

With 95% evidence, the basic assertion is accepted. Therefore, it could be inferred that with

respect to all the severity conditions, the proportion of insurance claimants of “MILD” and

“MEDIUM” severity is at least 75%. The conclusion of such inference has enough evidence

about the fact.

3.c)

Now, our investigation is on the basis of finding the significant difference in the proportion of

“MILD” and “MEDIUM” claims according to the gender of the patients. The difference in

proportion of “MILD” or “MEDIUM” claims by female patients compared to the male

patients is calculated.

It is observed that the count of insurance claimants whose severity conditions are either

“MILD” or “MEDIUM” is 154. Among those people, 60 claimants are males and 94

claimants are females. The proportions of males and females in the total claimants are

38.96% and 61.04% respectively. According to the 95% probability, the equality of

proportions of frequencies of males and females is rejected. Therefore, it could be stated that

the difference of proportions is prominent as per inference (Wolpert 1996). It could be

observed that the proportions of “MILD” and “MEDIUM” severity according to the genders

of the insurance claimant are unequal. Therefore, gender has an effect in it.

3.d)

According to the standard of industry, it is hypothecated that the payment amounts of the

samples are associated to private attorney of the claimants represented the claimants.

Particularly, the average claim amount for the private attorney is greater than the average

claim when no private attorney is involved. The average payment amount of the claimants

who has private attorney is $80501.07. The average payment amount of the claimants who has

non-private attorney is $58140.51.

According to the null assertion the difference of the average payment amount of private

attorney and the average payment amount related to non-private attorney is assumed 0. The

among every type of severity, the proportion of severity conditions of “MILD” and

“MEDIUM” is greater than 75%.

With 95% evidence, the basic assertion is accepted. Therefore, it could be inferred that with

respect to all the severity conditions, the proportion of insurance claimants of “MILD” and

“MEDIUM” severity is at least 75%. The conclusion of such inference has enough evidence

about the fact.

3.c)

Now, our investigation is on the basis of finding the significant difference in the proportion of

“MILD” and “MEDIUM” claims according to the gender of the patients. The difference in

proportion of “MILD” or “MEDIUM” claims by female patients compared to the male

patients is calculated.

It is observed that the count of insurance claimants whose severity conditions are either

“MILD” or “MEDIUM” is 154. Among those people, 60 claimants are males and 94

claimants are females. The proportions of males and females in the total claimants are

38.96% and 61.04% respectively. According to the 95% probability, the equality of

proportions of frequencies of males and females is rejected. Therefore, it could be stated that

the difference of proportions is prominent as per inference (Wolpert 1996). It could be

observed that the proportions of “MILD” and “MEDIUM” severity according to the genders

of the insurance claimant are unequal. Therefore, gender has an effect in it.

3.d)

According to the standard of industry, it is hypothecated that the payment amounts of the

samples are associated to private attorney of the claimants represented the claimants.

Particularly, the average claim amount for the private attorney is greater than the average

claim when no private attorney is involved. The average payment amount of the claimants

who has private attorney is $80501.07. The average payment amount of the claimants who has

non-private attorney is $58140.51.

According to the null assertion the difference of the average payment amount of private

attorney and the average payment amount related to non-private attorney is assumed 0. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6DATA ANALYSIS

alternative assertion about the average payment amount of private attorney is unequal to the

average payment amount related to non-private attorney.

The null hypothesis of equality of payment amounts is rejected with 95% possibility (Abbott 2017).

The proposition of the higher average paid claim amount of private attorney with respect to

absence of private attorney is accepted at 5% level of significance. Therefore, there is

sufficient evidence that average payment amount of the claimants who has private attorney is

greater than the payment amount who has non-private attorney. The data completely supports

the proposition.

3. e)

The industry stakeholders consider that private attorney representation is greater in case of

“SEVERE” claims than for claims in case of “MEDIUM” severity. The validity of the

statement is measured with the help of testing of hypothesis. The basic assertion is assumed

as the proportion of private attorney for “SEVERE” severity is equal to the claims with a

“MEDIUM” severity. The alternative assertion is assumed as the difference between

proportion of private attorney for “SEVERE” claims and claims with “MEDIUM” severity is

unequal to 0.

The total number of private attorney is 129. The number of private attorney representation for

“MEDIUM” severity claims is 93. The number of private attorney representation for

“SEVERE” severity claims is 36. According to the private attorney representation, the

proportions of these two severities are 78.26% and 72.66% respectively.

The basic assertion is accepted at 5% level of significance. It could be concluded that the

proportions of claims in case of private attorney in “SEVERE” condition is equal to the

proportions of claims in case of non-private attorney in “MEDIUM” condition. The

proposition is found to be absolutely valid. Hence, the assertion that the number of private

attorney is higher for “SEVERE” claims than for claims with “MEDIUM” severity is invalid.

Answer 4.

alternative assertion about the average payment amount of private attorney is unequal to the

average payment amount related to non-private attorney.

The null hypothesis of equality of payment amounts is rejected with 95% possibility (Abbott 2017).

The proposition of the higher average paid claim amount of private attorney with respect to

absence of private attorney is accepted at 5% level of significance. Therefore, there is

sufficient evidence that average payment amount of the claimants who has private attorney is

greater than the payment amount who has non-private attorney. The data completely supports

the proposition.

3. e)

The industry stakeholders consider that private attorney representation is greater in case of

“SEVERE” claims than for claims in case of “MEDIUM” severity. The validity of the

statement is measured with the help of testing of hypothesis. The basic assertion is assumed

as the proportion of private attorney for “SEVERE” severity is equal to the claims with a

“MEDIUM” severity. The alternative assertion is assumed as the difference between

proportion of private attorney for “SEVERE” claims and claims with “MEDIUM” severity is

unequal to 0.

The total number of private attorney is 129. The number of private attorney representation for

“MEDIUM” severity claims is 93. The number of private attorney representation for

“SEVERE” severity claims is 36. According to the private attorney representation, the

proportions of these two severities are 78.26% and 72.66% respectively.

The basic assertion is accepted at 5% level of significance. It could be concluded that the

proportions of claims in case of private attorney in “SEVERE” condition is equal to the

proportions of claims in case of non-private attorney in “MEDIUM” condition. The

proposition is found to be absolutely valid. Hence, the assertion that the number of private

attorney is higher for “SEVERE” claims than for claims with “MEDIUM” severity is invalid.

Answer 4.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7DATA ANALYSIS

4. a)

You were also interested to find the relationship between the speciality of physician involved,

severity of the claim and the average amount of insurance claim. You regard that the

percentage of claims in “SEVERE” severity is greater for Orthopaedic surgeon and lesser

than other specialists.

The basic assertion assumed that the difference between the percentage of Orthopaedic

surgeon and the other specialists in the “SEVERE” severity is 0. The alternative assertion

assumed that the percentage of Orthopaedic surgeon is lower than other specialists in the

“SEVERE” severity.

It is observed that the 46 patients claim “SEVERE” severity. Among them, 8 patients get

treatment from Orthopaedic surgeons and 38 patients get treatment from other types of

specialists. The proportions are calculated as 17.39% and 82.61% respectively.

Here the basic assertion is rejected at 5% level of significance. Therefore, the assertion of the equal

percentages of “SEVERE” severity that claims insurance under treatment of an Orthopaedic

surgeon and other specialists is accepted. The alternative hypothesis of claims of insurance

from the claimants under Orthopaedic surgeon is lower than the claims about other types of

specialists is accepted.

4.b)

You also consider that the average claim amount for “SEVERE” severity is higher when an

Orthopaedic surgeon is taken under consideration rather than other specialists.

The basic assertion is that the differences of average claim amount for “SEVERE” condition

for Orthopaedic surgeon and the average claim amount for “SEVERE” condition for the other

specialists is 0. The alternative assertion is that the difference of average claim amount for

“SEVERE” condition for Orthopaedic surgeon and the average claim amount for “SEVERE”

condition for the other specialists is unequal to 0.

The number of claimants in “SEVERE” severity is 46. Out of them, 8 claimants were under

supervision of Orthopaedic surgeon and 38 patients were under supervision of other types of

specialists. The average claiming amount of 8 patients is $118944.27. The average claiming

amount of 38 patients is $108466.41.

4. a)

You were also interested to find the relationship between the speciality of physician involved,

severity of the claim and the average amount of insurance claim. You regard that the

percentage of claims in “SEVERE” severity is greater for Orthopaedic surgeon and lesser

than other specialists.

The basic assertion assumed that the difference between the percentage of Orthopaedic

surgeon and the other specialists in the “SEVERE” severity is 0. The alternative assertion

assumed that the percentage of Orthopaedic surgeon is lower than other specialists in the

“SEVERE” severity.

It is observed that the 46 patients claim “SEVERE” severity. Among them, 8 patients get

treatment from Orthopaedic surgeons and 38 patients get treatment from other types of

specialists. The proportions are calculated as 17.39% and 82.61% respectively.

Here the basic assertion is rejected at 5% level of significance. Therefore, the assertion of the equal

percentages of “SEVERE” severity that claims insurance under treatment of an Orthopaedic

surgeon and other specialists is accepted. The alternative hypothesis of claims of insurance

from the claimants under Orthopaedic surgeon is lower than the claims about other types of

specialists is accepted.

4.b)

You also consider that the average claim amount for “SEVERE” severity is higher when an

Orthopaedic surgeon is taken under consideration rather than other specialists.

The basic assertion is that the differences of average claim amount for “SEVERE” condition

for Orthopaedic surgeon and the average claim amount for “SEVERE” condition for the other

specialists is 0. The alternative assertion is that the difference of average claim amount for

“SEVERE” condition for Orthopaedic surgeon and the average claim amount for “SEVERE”

condition for the other specialists is unequal to 0.

The number of claimants in “SEVERE” severity is 46. Out of them, 8 claimants were under

supervision of Orthopaedic surgeon and 38 patients were under supervision of other types of

specialists. The average claiming amount of 8 patients is $118944.27. The average claiming

amount of 38 patients is $108466.41.

8DATA ANALYSIS

The basic assertion is accepted here. Hence, the hypothesis of the average claim amount for

“SEVERE” claims is equal for the speciality criterion of both Orthopaedic surgeon and other

specialisations with 95% possibility. Hence, the average claim amount for “SEVERE” severity

is not higher for the involvement of Orthopaedic surgeon than other specialisations.

I look forward to your response.

Sincerely,

Edmond Kendrick

Chief Data Scientist – United Health Group.

The basic assertion is accepted here. Hence, the hypothesis of the average claim amount for

“SEVERE” claims is equal for the speciality criterion of both Orthopaedic surgeon and other

specialisations with 95% possibility. Hence, the average claim amount for “SEVERE” severity

is not higher for the involvement of Orthopaedic surgeon than other specialisations.

I look forward to your response.

Sincerely,

Edmond Kendrick

Chief Data Scientist – United Health Group.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9DATA ANALYSIS

References:

Abbott, M. L. (2017). Independent Sample T Test.

Chan, I.S. and Zhang, Z., 1999. Test‐based exact confidence intervals for the difference of

two binomial proportions. Biometrics, 55(4), pp.1202-1209.

Gilbert, R., Widom, C.S., Browne, K., Fergusson, D., Webb, E. and Janson, S., 2009. Burden

and consequences of child maltreatment in high-income countries. The lancet, 373(9657),

pp.68-81.

Lehmann, E.L. and Romano, J.P., 2006. Testing statistical hypotheses. Springer Science &

Business Media.

Lowry, R., 2014. Concepts and applications of inferential statistics.

Montgomery, D.C., Runger, G.C. and Hubele, N.F., 2009. Engineering statistics. John Wiley

& Sons.

Stone, H., Sidel, J.L. and Bloomquist, J., 2008. Quantitative descriptive analysis. Descriptive

Sensory Analysis in Practice, pp.53-69.

Wolpert, R.L., 1996. Testing simple hypotheses. In Data Analysis and Information Systems

(pp. 289-297). Springer, Berlin, Heidelberg.

References:

Abbott, M. L. (2017). Independent Sample T Test.

Chan, I.S. and Zhang, Z., 1999. Test‐based exact confidence intervals for the difference of

two binomial proportions. Biometrics, 55(4), pp.1202-1209.

Gilbert, R., Widom, C.S., Browne, K., Fergusson, D., Webb, E. and Janson, S., 2009. Burden

and consequences of child maltreatment in high-income countries. The lancet, 373(9657),

pp.68-81.

Lehmann, E.L. and Romano, J.P., 2006. Testing statistical hypotheses. Springer Science &

Business Media.

Lowry, R., 2014. Concepts and applications of inferential statistics.

Montgomery, D.C., Runger, G.C. and Hubele, N.F., 2009. Engineering statistics. John Wiley

& Sons.

Stone, H., Sidel, J.L. and Bloomquist, J., 2008. Quantitative descriptive analysis. Descriptive

Sensory Analysis in Practice, pp.53-69.

Wolpert, R.L., 1996. Testing simple hypotheses. In Data Analysis and Information Systems

(pp. 289-297). Springer, Berlin, Heidelberg.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10DATA ANALYSIS

Appendix:

Table 1

Table 2

Table 3

Appendix:

Table 1

Table 2

Table 3

11DATA ANALYSIS

Figure 1

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Percentage stacked bar plot

Count of claimants with "No Insurance" Sample size

Samples

Percentages

Table 4

Figure 1

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Percentage stacked bar plot

Count of claimants with "No Insurance" Sample size

Samples

Percentages

Table 4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.