Report on Functions of Management Accounting Systems

VerifiedAdded on 2024/06/03

|15

|3891

|74

Report

AI Summary

This report provides a comprehensive overview of the functions of management accounting systems within an organization. It begins by distinguishing management accounting from financial accounting, highlighting the importance of management accounting information as a decision-making tool for department managers. The report discusses cost accounting systems, including actual, normal, and standard costing, as well as inventory management and job costing systems. Furthermore, it presents different types of managerial accounting reports and emphasizes the importance of understandable financial information. Practical application is demonstrated through an income statement analysis using both absorption and marginal costing methods. Finally, the report explores the use of budgeting for planning and control purposes, including a discussion of the advantages and disadvantages of budgets in organizational management. This assignment solution is available for students on Desklib, offering valuable insights and study tools.

FUNCTIONS OF MANAGEMENT ACCOUNTING SYSTEMS

NAME OF THE STUDENT

NAME OF THE UNIVERSITY

STUDENT’S ID

NAME OF THE STUDENT

NAME OF THE UNIVERSITY

STUDENT’S ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................5

Task 2...............................................................................................................................................7

TASK 3............................................................................................................................................9

TASK 4..........................................................................................................................................12

Conclusion.....................................................................................................................................14

Reference list.................................................................................................................................15

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................5

Task 2...............................................................................................................................................7

TASK 3............................................................................................................................................9

TASK 4..........................................................................................................................................12

Conclusion.....................................................................................................................................14

Reference list.................................................................................................................................15

Introduction

In this assignment we are going to formulate a well-researched report on the Functions of

management Accounting Systems.

A management process basically consists of four steps which are performed by different

department managers and these four basic functions of management are:

Planning

Organizing

Controlling

Decision-making

Management Accounting Systems have a very important role to play in all of the above four

mentioned managerial functions performed by different department managers. Management

Accounting can be described as the process of making management reports and accounts which

help an organization in providing clear and timely financial and statistical information to the

department managers which helps the managers in making long-term and short-term decisions.

Management Accounting helps an organization in achieving its goals and objectives.

Management Accounting is completely different from Financial Accounting. Management

Accounting is mostly used to help the different managers within an organization to help them in

the process of decision-making (Johnstone, 2018). Financial Accounting is used to provide

useful information to the people within the organization and also to the people outside the

organization.

These are the roles of Management Accounting Systems in an organization:

Forecasting the future

To help in Make-or-buy decisions

Forecast of Cash Flows

Understanding performance variance

Scrutinize the rate of return

In this assignment we are going to formulate a well-researched report on the Functions of

management Accounting Systems.

A management process basically consists of four steps which are performed by different

department managers and these four basic functions of management are:

Planning

Organizing

Controlling

Decision-making

Management Accounting Systems have a very important role to play in all of the above four

mentioned managerial functions performed by different department managers. Management

Accounting can be described as the process of making management reports and accounts which

help an organization in providing clear and timely financial and statistical information to the

department managers which helps the managers in making long-term and short-term decisions.

Management Accounting helps an organization in achieving its goals and objectives.

Management Accounting is completely different from Financial Accounting. Management

Accounting is mostly used to help the different managers within an organization to help them in

the process of decision-making (Johnstone, 2018). Financial Accounting is used to provide

useful information to the people within the organization and also to the people outside the

organization.

These are the roles of Management Accounting Systems in an organization:

Forecasting the future

To help in Make-or-buy decisions

Forecast of Cash Flows

Understanding performance variance

Scrutinize the rate of return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

a) Explanation of management accounting and the essential requirements of management

accounting system which entails:

i. Distinguishing management accounting from financial accounting.

Management Accounting can be defined as the process of making management reports

and accounts which help an organization in providing clear and timely financial and

statistical information to the department managers which helps the managers in making

long-term and short-term decisions. Management Accounting is also known as

Managerial Accounting.

Financial Accounting can be defined as an accounting system that is used to prepare

financial statements for external parties like creditors, shareholder, investors, suppliers,

lenders, customers, etc (Pratheepkanth, 2018). Financial Accounting can be called the

purest type of bookkeeping and keeps a legitimate record and report of money related

information to give the data required by the clients.

ii. The importance of management accounting information as a decision making tool

for department managers.

Management accounting acts as an important tool in the decision-making process for the

managers. This is why it is also known as Managerial Accounting.

When we talk about small scale business owners and their managers, they have the

responsibility of making uncountable number of decisions every day. With the use of

management accounting their work is made easy. Management accounting makes the use

of information from the organizations operations to prepare a report that provide the

managers with an insight of the organizations business performance like profit margin

and labor utilization (Mueller and Trost, 2018). This provides the managers with the

information along with the data input required for making every day decisions.

iii. Cost accounting systems (actual, normal and standard costing)

The actual cost estimation is distinguished as a cost bookkeeping system that uses the real

cost, current cost rates and genuine utilize capacities utilized as a major aspect of the

creation strategy to decide the cost of specific things. The genuine commonsense

expenses of directors offer back to the wellspring of expenses, for instance, work and

materials.

a) Explanation of management accounting and the essential requirements of management

accounting system which entails:

i. Distinguishing management accounting from financial accounting.

Management Accounting can be defined as the process of making management reports

and accounts which help an organization in providing clear and timely financial and

statistical information to the department managers which helps the managers in making

long-term and short-term decisions. Management Accounting is also known as

Managerial Accounting.

Financial Accounting can be defined as an accounting system that is used to prepare

financial statements for external parties like creditors, shareholder, investors, suppliers,

lenders, customers, etc (Pratheepkanth, 2018). Financial Accounting can be called the

purest type of bookkeeping and keeps a legitimate record and report of money related

information to give the data required by the clients.

ii. The importance of management accounting information as a decision making tool

for department managers.

Management accounting acts as an important tool in the decision-making process for the

managers. This is why it is also known as Managerial Accounting.

When we talk about small scale business owners and their managers, they have the

responsibility of making uncountable number of decisions every day. With the use of

management accounting their work is made easy. Management accounting makes the use

of information from the organizations operations to prepare a report that provide the

managers with an insight of the organizations business performance like profit margin

and labor utilization (Mueller and Trost, 2018). This provides the managers with the

information along with the data input required for making every day decisions.

iii. Cost accounting systems (actual, normal and standard costing)

The actual cost estimation is distinguished as a cost bookkeeping system that uses the real

cost, current cost rates and genuine utilize capacities utilized as a major aspect of the

creation strategy to decide the cost of specific things. The genuine commonsense

expenses of directors offer back to the wellspring of expenses, for instance, work and

materials.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Generally, the estimation of the typical expenses of bookkeeping framework comprises of

the costs used to accomplish the cost of a specific item. It utilizes the genuine cost of

materials, genuine work cost (Qian et al., 2018).

Standard costing is defined as a cost accounting system that some organizations use to

distinguish the contrasts between the genuine expenses of the merchandise created and

the costs that ought to have happened for those products.

iv. Inventory management systems

Inventory management will be characterized as an administration procedure alluding to

the way toward requesting, stockpiling and utilization of an organization stock:

requesting, putting away and utilizing crude materials, segments and completed items.

Stock administration frameworks help track items over the production network or the part

in which business works. This spends everything from age to retail, stockpiling and

transport, and the majority of the advancements on stocks and parts (Bedford and Speklé,

2018). Practically speaking, he comprehends that an organization can see the little parts

that move to its assignments, enabling it to set up better inclinations and hypotheses.

v. Job costing systems

A job costing system incorporates the gathering of data about costs identified with a

specific generation or administration post. This data may have the cost information

furnished to a client as per an assention in which the expenses are paid. The information

is in like manner accommodating in choosing the accuracy of the arrangement of an

affiliation's appraisal, and it should be prepared for saying costs that consolidate sensible

advantage. The data can moreover be used to allot stock costs for gathering things.

Essentially work costing framework needs to gather the accompanying three kinds of

data:

Direct materials

Direct labor

Overhead

b) Presenting financial information

I. Different types of managerial accounting reports.

the costs used to accomplish the cost of a specific item. It utilizes the genuine cost of

materials, genuine work cost (Qian et al., 2018).

Standard costing is defined as a cost accounting system that some organizations use to

distinguish the contrasts between the genuine expenses of the merchandise created and

the costs that ought to have happened for those products.

iv. Inventory management systems

Inventory management will be characterized as an administration procedure alluding to

the way toward requesting, stockpiling and utilization of an organization stock:

requesting, putting away and utilizing crude materials, segments and completed items.

Stock administration frameworks help track items over the production network or the part

in which business works. This spends everything from age to retail, stockpiling and

transport, and the majority of the advancements on stocks and parts (Bedford and Speklé,

2018). Practically speaking, he comprehends that an organization can see the little parts

that move to its assignments, enabling it to set up better inclinations and hypotheses.

v. Job costing systems

A job costing system incorporates the gathering of data about costs identified with a

specific generation or administration post. This data may have the cost information

furnished to a client as per an assention in which the expenses are paid. The information

is in like manner accommodating in choosing the accuracy of the arrangement of an

affiliation's appraisal, and it should be prepared for saying costs that consolidate sensible

advantage. The data can moreover be used to allot stock costs for gathering things.

Essentially work costing framework needs to gather the accompanying three kinds of

data:

Direct materials

Direct labor

Overhead

b) Presenting financial information

I. Different types of managerial accounting reports.

Administration bookkeeping reports are utilized to quantify, design, and settle on choices and

measure execution. These administration bookkeeping portrayals are constantly created by the

prerequisites (Hiebl and Richter, 2018). Managerial accounting reports should be made and kept

very carefully by people who are adapted to bookkeeping because many important decisions

depend on the authenticity of these reports. The managerial accounting reports are then analyzed

by the managers to highlight some patterns and convert them into useful information for any

organization.

The different type of managerial accounting reports are the following:

Budget Reports

Account Receivable Aging Reports

Cost Managerial Accounting Reports

Performance Reports

Other Managerial Accounting Reports

II. Why is it important for the information to be presented in manner that must be

understandable?

It is very important for the information to be presented to be understandable because if the

information or the data provided is not clear and not understandable then the management

accounting report that is to be made is affected. It could harm the accounting report as the

financial figures and data may be altered which would create a fluctuating accounting report in

place of the original report that had to be made (Johnstone, 2018). This could affect important

people like the stakeholders of the organization and the organization itself in the long run.

Task 2

The cost card of Tech UK is as follows:

Direct labor £ 5.00

Direct material £ 8.00

Variable production overhead £ 2.00

Fixed production overhead £ 5.00

Standard production cost £ 20.00

measure execution. These administration bookkeeping portrayals are constantly created by the

prerequisites (Hiebl and Richter, 2018). Managerial accounting reports should be made and kept

very carefully by people who are adapted to bookkeeping because many important decisions

depend on the authenticity of these reports. The managerial accounting reports are then analyzed

by the managers to highlight some patterns and convert them into useful information for any

organization.

The different type of managerial accounting reports are the following:

Budget Reports

Account Receivable Aging Reports

Cost Managerial Accounting Reports

Performance Reports

Other Managerial Accounting Reports

II. Why is it important for the information to be presented in manner that must be

understandable?

It is very important for the information to be presented to be understandable because if the

information or the data provided is not clear and not understandable then the management

accounting report that is to be made is affected. It could harm the accounting report as the

financial figures and data may be altered which would create a fluctuating accounting report in

place of the original report that had to be made (Johnstone, 2018). This could affect important

people like the stakeholders of the organization and the organization itself in the long run.

Task 2

The cost card of Tech UK is as follows:

Direct labor £ 5.00

Direct material £ 8.00

Variable production overhead £ 2.00

Fixed production overhead £ 5.00

Standard production cost £ 20.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The figure for fixed costs was ascertained based on an ordinary spending creation of 36,000 units

for every annum. The settled generation roof brought about in September was £ 15,000 every

month.

There are deals, appropriation and organization costs:

Fixed £10,000 per month

Variable 15 % of the sales value

The selling price per unit is £35 and the number of units produced and sold were:

September (units)

Production 2000

Sales 1500

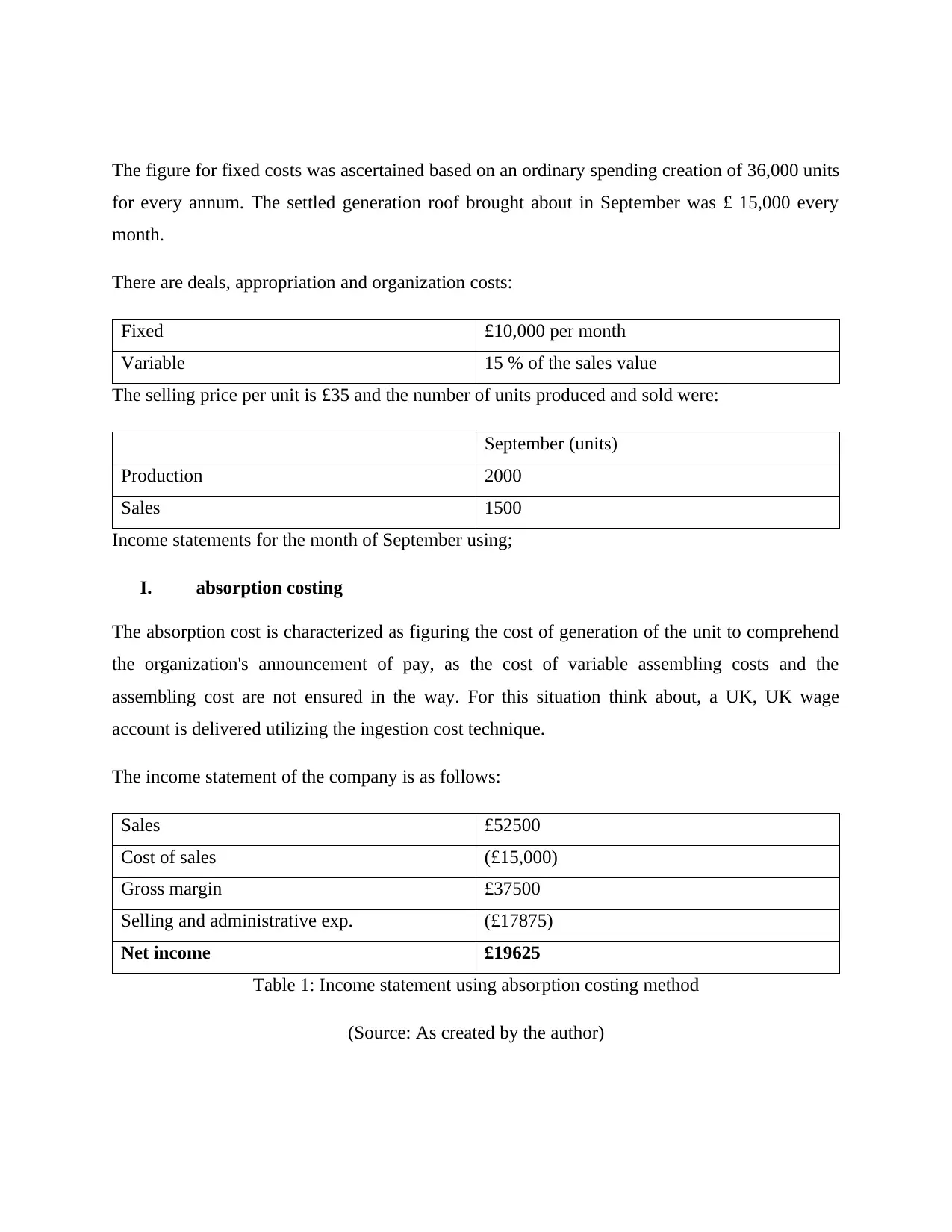

Income statements for the month of September using;

I. absorption costing

The absorption cost is characterized as figuring the cost of generation of the unit to comprehend

the organization's announcement of pay, as the cost of variable assembling costs and the

assembling cost are not ensured in the way. For this situation think about, a UK, UK wage

account is delivered utilizing the ingestion cost technique.

The income statement of the company is as follows:

Sales £52500

Cost of sales (£15,000)

Gross margin £37500

Selling and administrative exp. (£17875)

Net income £19625

Table 1: Income statement using absorption costing method

(Source: As created by the author)

for every annum. The settled generation roof brought about in September was £ 15,000 every

month.

There are deals, appropriation and organization costs:

Fixed £10,000 per month

Variable 15 % of the sales value

The selling price per unit is £35 and the number of units produced and sold were:

September (units)

Production 2000

Sales 1500

Income statements for the month of September using;

I. absorption costing

The absorption cost is characterized as figuring the cost of generation of the unit to comprehend

the organization's announcement of pay, as the cost of variable assembling costs and the

assembling cost are not ensured in the way. For this situation think about, a UK, UK wage

account is delivered utilizing the ingestion cost technique.

The income statement of the company is as follows:

Sales £52500

Cost of sales (£15,000)

Gross margin £37500

Selling and administrative exp. (£17875)

Net income £19625

Table 1: Income statement using absorption costing method

(Source: As created by the author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the past income statement utilizing the absorption cost strategy, it can be pronounced that

the organization gets a net pay of £ 19625 in September, assessing the information given by the

organization.

II. marginal costing methods

The marginal costing strategy utilizes the minimal cost certain in the article fundamentally the

variable cost. The minimal cost delivered by the thing included is immediate work cost,

coordinate cost, aberrant circuitous cost of generation and cost of direct expenses (assuming

any). Along these lines, with the expansion in deals and volume of volume, a variable increment

is considered at the variable cost.

Then again, the settled expenses are the expenses of non-change things inside a specific

timeframe, paying little heed to deals and generation. The fringe creation cost is the unit cost of

unprotected unit generation if these units are not being delivered or can be expanded to in excess

of one unit (Hiebl and Richter, 2018).

Presently we can expel the meaning of the negligible cost strategy (as utilized as a part of

administration bookkeeping):

A bookkeeping framework in which the settled expenses for the timeframe are completely

analyzed against the commitment in total and the variable expenses can be changed in taken a

toll units. The marginal cost figuring can be considered as a key strategy for ascertaining the

costs utilized when choices are made. The activity of the fringe cost strategy utilizes the principle

factor in which the consideration of the organization ought to be coordinated to consider the

adjustments in basic leadership.

TASK 3

The use of budget for planning and control purpose

The report is based on the review account management and studies the role of controlling budget

in management process. Budget contributes a major role in the growth and survival of an

organization with the growing competition of the market. Budgets are mainly planned to

highlight the organization financial management and gives a structure to achieve these plans with

appropriate means of controlling the end result respect to the flow of the market. It helps the firm

the organization gets a net pay of £ 19625 in September, assessing the information given by the

organization.

II. marginal costing methods

The marginal costing strategy utilizes the minimal cost certain in the article fundamentally the

variable cost. The minimal cost delivered by the thing included is immediate work cost,

coordinate cost, aberrant circuitous cost of generation and cost of direct expenses (assuming

any). Along these lines, with the expansion in deals and volume of volume, a variable increment

is considered at the variable cost.

Then again, the settled expenses are the expenses of non-change things inside a specific

timeframe, paying little heed to deals and generation. The fringe creation cost is the unit cost of

unprotected unit generation if these units are not being delivered or can be expanded to in excess

of one unit (Hiebl and Richter, 2018).

Presently we can expel the meaning of the negligible cost strategy (as utilized as a part of

administration bookkeeping):

A bookkeeping framework in which the settled expenses for the timeframe are completely

analyzed against the commitment in total and the variable expenses can be changed in taken a

toll units. The marginal cost figuring can be considered as a key strategy for ascertaining the

costs utilized when choices are made. The activity of the fringe cost strategy utilizes the principle

factor in which the consideration of the organization ought to be coordinated to consider the

adjustments in basic leadership.

TASK 3

The use of budget for planning and control purpose

The report is based on the review account management and studies the role of controlling budget

in management process. Budget contributes a major role in the growth and survival of an

organization with the growing competition of the market. Budgets are mainly planned to

highlight the organization financial management and gives a structure to achieve these plans with

appropriate means of controlling the end result respect to the flow of the market. It helps the firm

to obtain proper armor to provide resistance to the challenges and meet the future requirements.

The structural plan which calculates the data of expenses needed to run the organization and

predicted revenue is called budgeting (Malina, 2018). It can also be defined as the procedure to

prepare a detail statement of financial management considering the input with respect to a given

time. In other words, budgeting can also be defined as a document which basically carries out the

health check for smooth operation of the business in an organization. It includes various

activities establishing various developing project and implementing such report into action.

Budgeting for every organization running from small business to large scale setup helps to figure

out imminent issue within the system and prepare necessary solution to eliminates any such

resistance. The controlling function also figure out any deviation in business proving negatively

and the root cause of such indiscriminate deviation (Ahmetshina et al., 2018). There is various

phase of budgeting for example a startup company basically follows Zero Base budgeting

whereas a large firm operates on Kaizen budgeting. Various arguments arise which result in

advantages and disadvantages of budget.

a.) Advantages and disadvantages of the budgets are:

Advantages of budgeting are-

i. Budgeting compel with appropriate planning and hence making proper

communication of future prediction of the organization which could result in

positive way.

ii. Budgets enhances the basic principle of co-ordination such as communication

between sales and operation team with added customer service team resulting in

smooth operation of the system.

iii. Budgets acts as a motivating factor of performance. It sets a threshold parameter

of performance and optimizing the goal for achievement (Busco and Quattrone,

2018).

iv. Budgets are successful procedures to achieve targets and track defects which

could be further helpful for future guidance and training.

v. Budgets contribute an important factor in saving capital keeping the firm fit to

perform and compete and also influence the decision-making quality of an

organization.

The structural plan which calculates the data of expenses needed to run the organization and

predicted revenue is called budgeting (Malina, 2018). It can also be defined as the procedure to

prepare a detail statement of financial management considering the input with respect to a given

time. In other words, budgeting can also be defined as a document which basically carries out the

health check for smooth operation of the business in an organization. It includes various

activities establishing various developing project and implementing such report into action.

Budgeting for every organization running from small business to large scale setup helps to figure

out imminent issue within the system and prepare necessary solution to eliminates any such

resistance. The controlling function also figure out any deviation in business proving negatively

and the root cause of such indiscriminate deviation (Ahmetshina et al., 2018). There is various

phase of budgeting for example a startup company basically follows Zero Base budgeting

whereas a large firm operates on Kaizen budgeting. Various arguments arise which result in

advantages and disadvantages of budget.

a.) Advantages and disadvantages of the budgets are:

Advantages of budgeting are-

i. Budgeting compel with appropriate planning and hence making proper

communication of future prediction of the organization which could result in

positive way.

ii. Budgets enhances the basic principle of co-ordination such as communication

between sales and operation team with added customer service team resulting in

smooth operation of the system.

iii. Budgets acts as a motivating factor of performance. It sets a threshold parameter

of performance and optimizing the goal for achievement (Busco and Quattrone,

2018).

iv. Budgets are successful procedures to achieve targets and track defects which

could be further helpful for future guidance and training.

v. Budgets contribute an important factor in saving capital keeping the firm fit to

perform and compete and also influence the decision-making quality of an

organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantages of the budgets are-

i. The budgetary system of an organization is selected by the group of managers so

the innovation faces a boundary challenges and thus can be termed as

bureaucratic.

ii. It consumes time even when an organization has its activity defined process while

most of the people rely on bank balance which makes unnecessary time

consumption of budgeting.

iii. Budget are exposed to various threats which are not related to the organization

operation which fails to eliminate the loophole in the quick analyzation of

appropriate decision (Giovannoni, 2018).

b.) Budget preparation process including determination of pricing and different costing

systems that can be used.

The objectives of the organization make the structural skeleton of budget for that organization.

This process includes various parameter from selection of raw materials to delivering products

with added service. The basic structure followed by most of the firm are comparison which helps

them to evaluate actual outcome of the budget. The preparation process includes several steps.

These are-

i. Analyzing the main objective of the company and updating the changes ass per

last budget.

ii. Determine the root cause of obstruction of generating more sales and the process

how it can directly impact the total revenue of the company.

iii. Available funding of the organization gives the skeleton of the budgetary system.

iv. Determination of cost of included step involved in the business activity and

reducing such costing.

v. Creation of a package with could help to analyze the budget comparing with the

expenses sheet of previous year

vi. Investing new models or tools to improve the budgetary system and obtaining cost

cutting techniques which could benefit the firm.

c.) Importance of budget as a tool for planning and control purpose.

i. The budgetary system of an organization is selected by the group of managers so

the innovation faces a boundary challenges and thus can be termed as

bureaucratic.

ii. It consumes time even when an organization has its activity defined process while

most of the people rely on bank balance which makes unnecessary time

consumption of budgeting.

iii. Budget are exposed to various threats which are not related to the organization

operation which fails to eliminate the loophole in the quick analyzation of

appropriate decision (Giovannoni, 2018).

b.) Budget preparation process including determination of pricing and different costing

systems that can be used.

The objectives of the organization make the structural skeleton of budget for that organization.

This process includes various parameter from selection of raw materials to delivering products

with added service. The basic structure followed by most of the firm are comparison which helps

them to evaluate actual outcome of the budget. The preparation process includes several steps.

These are-

i. Analyzing the main objective of the company and updating the changes ass per

last budget.

ii. Determine the root cause of obstruction of generating more sales and the process

how it can directly impact the total revenue of the company.

iii. Available funding of the organization gives the skeleton of the budgetary system.

iv. Determination of cost of included step involved in the business activity and

reducing such costing.

v. Creation of a package with could help to analyze the budget comparing with the

expenses sheet of previous year

vi. Investing new models or tools to improve the budgetary system and obtaining cost

cutting techniques which could benefit the firm.

c.) Importance of budget as a tool for planning and control purpose.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budgeting tools are beneficial in various ways such as it helps in maintaining a proper data

sheet of cost vs expenses and also help in minimizing unnecessary cost to provide maximum

profit with increasing the percentage of growth (Quinn et al., 2018). Budgeting tools can help

in maintaining other aspects such as-

i. It tracks the spending system and alerts when unnecessary spending amount

increases.

ii. It acts as a payment reminder via mails or simple text which alerts any due

pending and can cut the cost of overdues. This can successfully control the

revenue collected annually.

iii. With the increase in technology, it can provide a platform to view budgets from

mobile and thus can compare spending versus expenses in various aspect of the

life.

iv. It gives a time to review before final decision and hence enhances the decision-

making factor.

Different planning tools can be implemented to control the budgeting of an organization such

as implementing of various parameters in the datasheet which can prove to result beneficial

by comparing more crucial parameters. Introduction of reminders or alerts gives time to cut

down over payment fees (ter Bogt and Scapens, 2018). Cloud database inclusion in

budgeting system could help to participate various individuals of the organization leading to

inclusion of more factors and concluding with best possible result.

TASK 4

The use of Balanced score card approach to achieve sustainable success

The management system which is based on the performance metrics and uses various analysis

for improvement of internal functions involved in a business and importance of their outcomes.

This system also provides various feedback and mainly concentrates on the information collected

from various sources of organization by executives to judge the decision-making factor. The

approaches to use balance scorecard initiates an improved behavioral activity by utilizing the

factors such as learning, growth, process and customers. The strategic goals-oriented

performance can track behavioral activities and performance of an employee which can improve

sheet of cost vs expenses and also help in minimizing unnecessary cost to provide maximum

profit with increasing the percentage of growth (Quinn et al., 2018). Budgeting tools can help

in maintaining other aspects such as-

i. It tracks the spending system and alerts when unnecessary spending amount

increases.

ii. It acts as a payment reminder via mails or simple text which alerts any due

pending and can cut the cost of overdues. This can successfully control the

revenue collected annually.

iii. With the increase in technology, it can provide a platform to view budgets from

mobile and thus can compare spending versus expenses in various aspect of the

life.

iv. It gives a time to review before final decision and hence enhances the decision-

making factor.

Different planning tools can be implemented to control the budgeting of an organization such

as implementing of various parameters in the datasheet which can prove to result beneficial

by comparing more crucial parameters. Introduction of reminders or alerts gives time to cut

down over payment fees (ter Bogt and Scapens, 2018). Cloud database inclusion in

budgeting system could help to participate various individuals of the organization leading to

inclusion of more factors and concluding with best possible result.

TASK 4

The use of Balanced score card approach to achieve sustainable success

The management system which is based on the performance metrics and uses various analysis

for improvement of internal functions involved in a business and importance of their outcomes.

This system also provides various feedback and mainly concentrates on the information collected

from various sources of organization by executives to judge the decision-making factor. The

approaches to use balance scorecard initiates an improved behavioral activity by utilizing the

factors such as learning, growth, process and customers. The strategic goals-oriented

performance can track behavioral activities and performance of an employee which can improve

the efficiency rate of workflow and achieve better solution to reduce the loss suffered by the

company (Ismail et al., 2018). Tech (UK) Limited can figure out the factors which is impacting

on the performance of the company and structure some changes recorded by scorecard. This can

help the organization to map any required changes and develop new innovative objectives

lagging for better improvement of the company. This scorecard can figure out any challenges

facing from internal business perspective to improve the internal operation. The balanced

scorecard approach can also help in finding the laggings if present in customer service and

improve as per requirements. The financial perspective can also improve based on this approach

because metrics of the performance are directly proportional to benefit of the firm hence metrics

resulting in loss of internal operation can induce to eliminate any worker which can result in

benefit.

Other than performance the goal is subjected to achieve on daily basis and this can result in

improving the standards of the organization and plans to meet objective of the organization. The

balanced scorecard approach makes the organization healthy in each aspect and creates a visual

application of decision making based on the performance tracking.

Some organization follows financial accounting approach which relies more in the data sheet

maintenance such as “Travelex”. This is because the data changes with the trends and the main

objective of the firm is to use the latest data in improving the profit percentage. Traveler mainly

depend on the exchange rates and hence the financial accounting helps to quickly give them a

brief trend of the market and provide rates as per their profit (Lasyoud et al., 2018). The financial

approach is very essential because inappropriate knowledge of financial accounting can result

loss and non-maintenance of data sheet can result in giving a huge reduction in collected

revenue. Reports from various resources reveals that balanced scorecard approach is proved to be

working with better efficiency rather than other accounting approach.

Different planning tools involved in balanced scorecard approach helps to control the budgeting

problem of an organization and measures the performance from every individual level.

Implementation of various parameters in the datasheet containing metrics can result beneficial by

comparing more crucial parameters. Introduction of reminders or alerts gives time to cut down

over payment fees (Latan et al., 2018). Cloud database inclusion in balanced scorecard approach

company (Ismail et al., 2018). Tech (UK) Limited can figure out the factors which is impacting

on the performance of the company and structure some changes recorded by scorecard. This can

help the organization to map any required changes and develop new innovative objectives

lagging for better improvement of the company. This scorecard can figure out any challenges

facing from internal business perspective to improve the internal operation. The balanced

scorecard approach can also help in finding the laggings if present in customer service and

improve as per requirements. The financial perspective can also improve based on this approach

because metrics of the performance are directly proportional to benefit of the firm hence metrics

resulting in loss of internal operation can induce to eliminate any worker which can result in

benefit.

Other than performance the goal is subjected to achieve on daily basis and this can result in

improving the standards of the organization and plans to meet objective of the organization. The

balanced scorecard approach makes the organization healthy in each aspect and creates a visual

application of decision making based on the performance tracking.

Some organization follows financial accounting approach which relies more in the data sheet

maintenance such as “Travelex”. This is because the data changes with the trends and the main

objective of the firm is to use the latest data in improving the profit percentage. Traveler mainly

depend on the exchange rates and hence the financial accounting helps to quickly give them a

brief trend of the market and provide rates as per their profit (Lasyoud et al., 2018). The financial

approach is very essential because inappropriate knowledge of financial accounting can result

loss and non-maintenance of data sheet can result in giving a huge reduction in collected

revenue. Reports from various resources reveals that balanced scorecard approach is proved to be

working with better efficiency rather than other accounting approach.

Different planning tools involved in balanced scorecard approach helps to control the budgeting

problem of an organization and measures the performance from every individual level.

Implementation of various parameters in the datasheet containing metrics can result beneficial by

comparing more crucial parameters. Introduction of reminders or alerts gives time to cut down

over payment fees (Latan et al., 2018). Cloud database inclusion in balanced scorecard approach

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.