Capital Structure Determinants: Manufacturing Companies in Sri Lanka

VerifiedAdded on 2022/05/18

|13

|3659

|26

Report

AI Summary

This report presents the methodology used to analyze the determinants of capital structure in listed manufacturing companies on the Colombo Stock Exchange (CSE) in Sri Lanka. The study focuses on the period from 2014 to 2018, examining the impact of factors like profitability, capital intensity, tangibility of assets, non-debt tax shield, and firm size on capital structure, specifically debt-to-equity ratio, long-term leverage, and total leverage. The research employs a quantitative approach, utilizing secondary data from annual reports and CSE publications. The methodology includes descriptive statistics (mean, mode, median), correlation analysis, and multiple regression analysis using the E-views software package to test the formulated hypotheses. The report outlines the population (manufacturing sector with 41 companies), the sample (20 companies), and the data collection process. The analysis aims to identify the significant relationships and impacts between the independent variables (determinants) and the dependent variables (capital structure measures), providing insights into the financial decision-making processes of these companies. The study sets the upper level of statistical significance for hypothesis testing at 5% (0.05).

CHAPTER 03

METHODOLOGY

“DETERMINANTS OF CAPITAL STRUCTURE: SPECIAL

REFERENCE TO LISTED MANUFACTURING

COMPANIES OF COLOMBO STOCK

EXCHANGE(CSE),SRI LANKA”

S.MADHUSHIKA SENEVIRATHNE

2015/BAD/202

METHODOLOGY

“DETERMINANTS OF CAPITAL STRUCTURE: SPECIAL

REFERENCE TO LISTED MANUFACTURING

COMPANIES OF COLOMBO STOCK

EXCHANGE(CSE),SRI LANKA”

S.MADHUSHIKA SENEVIRATHNE

2015/BAD/202

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CHAPTER 03

METHODOLOGY

3.1 Introduction

This chapter clearly describes as how to collect data from where and in which way. It also tells

about samples, dependent variable and independent variables how to evaluate and described. And

also this is explains the data collection procedure, research method and measurement,

operationalization and hypotheses.

This chapter deals with the conceptualization and methodology used in collection of sufficient data

and information from the data sources, and the steps and procedures involved in transferring from

into managerial information to drive findings and take decisions.

This chapter is most important to this study because the techniques discussed in this chapter guided

the researcher in the collection and analysis of the actual data. Further, this chapter presents an

output of the previous chapters; introduction, literature review and input to the next chapter on

data presentation and analysis.

3.2 Geographical and Demographical Profile

The Democratic Socialist Republic of Sri Lanka is an island in the Indian Ocean, which lies off

the south-eastern tip of the Indian subcontinent and consists of a total area of 65610 sq km (25,332

square miles). Sri Lanka is divided into 9 provinces and 25 districts. Among them Jaffna district

is located in the far north of Sri Lanka in Northern Province and occupies most of the Jaffna

peninsula. It has an area of 1025 square kilometres (395.8 sq Miles).

Sri Lanka had a population of 21.052 million in 2018 (August). Among them 10.39 million

(49.3%) were male and 10.66 million (50.7%) were female. The population destiny in Sri Lanka

is 334 per Km2 (865 people per mi2). Population growth rate was 0.8 dependency ratio was 51.23.

(Department of Census & statistics, 2018).

CHAPTER 03

METHODOLOGY

3.1 Introduction

This chapter clearly describes as how to collect data from where and in which way. It also tells

about samples, dependent variable and independent variables how to evaluate and described. And

also this is explains the data collection procedure, research method and measurement,

operationalization and hypotheses.

This chapter deals with the conceptualization and methodology used in collection of sufficient data

and information from the data sources, and the steps and procedures involved in transferring from

into managerial information to drive findings and take decisions.

This chapter is most important to this study because the techniques discussed in this chapter guided

the researcher in the collection and analysis of the actual data. Further, this chapter presents an

output of the previous chapters; introduction, literature review and input to the next chapter on

data presentation and analysis.

3.2 Geographical and Demographical Profile

The Democratic Socialist Republic of Sri Lanka is an island in the Indian Ocean, which lies off

the south-eastern tip of the Indian subcontinent and consists of a total area of 65610 sq km (25,332

square miles). Sri Lanka is divided into 9 provinces and 25 districts. Among them Jaffna district

is located in the far north of Sri Lanka in Northern Province and occupies most of the Jaffna

peninsula. It has an area of 1025 square kilometres (395.8 sq Miles).

Sri Lanka had a population of 21.052 million in 2018 (August). Among them 10.39 million

(49.3%) were male and 10.66 million (50.7%) were female. The population destiny in Sri Lanka

is 334 per Km2 (865 people per mi2). Population growth rate was 0.8 dependency ratio was 51.23.

(Department of Census & statistics, 2018).

2

3.3 Organizational Profile

Colombo Stock Exchange (CSE) has 297 companies representing 20 business sectors as at 31st

December 2018, with market capitalization of Rs. 2,839.45 Bn. Public companies incorporated

under the Companies Act No. 7 of 2007 or any other statutory corporation, incorporated or

established under the laws of Sri Lanka or established under the laws of any other state (subject to

Exchange Control approval) are eligible to seek a listing on the Colombo Stock Exchange to raise

debt or equity. Companies desiring to be admitted to the official list of the Exchange and to secure

a listing of their securities will be required to comply with the relevant provisions of the above act

and the Securities and Exchange Commission Act No.36 of 1987 (as amended) and the Listed

Rules of the Exchange.

The CSE is a company limited by guarantee, established under the Companies Act No.17 of 1982

and is licensed by the Securities and Exchange Commission of Sri Lanka (SEC). The CSE in a

mutual exchange and has 15 full members and 15 trading members licensed to trade both equity

and debt securities, while six members are licensed to trade debt securities only. All members are

licensed by the SEC to operate as stockbrokers. All members are corporate entities and some are

subsidiaries of large financial institutions. (www.cse.lk)

One of the major sectors is manufacturing sector. That includes 41 companies. GDP from

manufacturing Sri Lanka decreased to 348,130 LKR Million in the fourth quarter of 2018 from

389,558 LKR Million in the third quarter of 2018. So the manufacturing products provide higher

contribution to the Sri Lankan Gross Domestic Products. (www.tradingeconomics.com, Sri-

Lanka)

3.4 Research Design

This research tried to outline the determinants of capital structure in listed manufacturing

companies in Sri Lanka. This was a broad study which collected data from manufacturing sector.

Data on determinants of capital structure were collected from secondary sources an Annual

Reports of Manufacturing companies and Colombo Stock Exchange Publications for the periods

2014 to 2018.

3.3 Organizational Profile

Colombo Stock Exchange (CSE) has 297 companies representing 20 business sectors as at 31st

December 2018, with market capitalization of Rs. 2,839.45 Bn. Public companies incorporated

under the Companies Act No. 7 of 2007 or any other statutory corporation, incorporated or

established under the laws of Sri Lanka or established under the laws of any other state (subject to

Exchange Control approval) are eligible to seek a listing on the Colombo Stock Exchange to raise

debt or equity. Companies desiring to be admitted to the official list of the Exchange and to secure

a listing of their securities will be required to comply with the relevant provisions of the above act

and the Securities and Exchange Commission Act No.36 of 1987 (as amended) and the Listed

Rules of the Exchange.

The CSE is a company limited by guarantee, established under the Companies Act No.17 of 1982

and is licensed by the Securities and Exchange Commission of Sri Lanka (SEC). The CSE in a

mutual exchange and has 15 full members and 15 trading members licensed to trade both equity

and debt securities, while six members are licensed to trade debt securities only. All members are

licensed by the SEC to operate as stockbrokers. All members are corporate entities and some are

subsidiaries of large financial institutions. (www.cse.lk)

One of the major sectors is manufacturing sector. That includes 41 companies. GDP from

manufacturing Sri Lanka decreased to 348,130 LKR Million in the fourth quarter of 2018 from

389,558 LKR Million in the third quarter of 2018. So the manufacturing products provide higher

contribution to the Sri Lankan Gross Domestic Products. (www.tradingeconomics.com, Sri-

Lanka)

3.4 Research Design

This research tried to outline the determinants of capital structure in listed manufacturing

companies in Sri Lanka. This was a broad study which collected data from manufacturing sector.

Data on determinants of capital structure were collected from secondary sources an Annual

Reports of Manufacturing companies and Colombo Stock Exchange Publications for the periods

2014 to 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Independent variable of this study is determinants such as profitability, capital intensity, tangibility

of assets, Non debt tax shield, firm size and dependent variable is debt to equity, long term leverage

and total leverage was used to identify the impact and relationship between determinants of capital

structure of listed manufacturing companies of Colombo Stock Exchange.

The data for this analysis used the cross sectional and time series data (Balanced panel data) for

41 companies during the period from 2014 to 2018.

3.5 Population

The Colombo Stock Exchange has 297 companies representing 20 business sectors as at 31st

December 2018. Among all of those sectors only manufacturing sector was selected as the

population for the study purpose. And there are 41 companies listed under manufacturing sector

on the Colombo Stock Exchange.

3.6 Sample

As mentioned above the target population of this study includes 41 listed manufacturing

companies. Then as per the data availability, 20 manufacturing companies have been selected as

the sample.

3.7 Data collection

The source of secondary data was adopted for the sampled data collection of this research study.

Necessary data was collected from 20 listed manufacturing companies ‟ annual reports (based on

availability of data) over 5 years ( 2014, 2015, 2016, 2017 & 2018).

In this study, the data was collected by using the secondary sources, such as:

Annual reports of the sample listed manufacturing companies.

Journals of the listed manufacturing companies in Sri Lanka.

Hand book of the listed companies in Sri Lanka published by Colombo Stock Exchange.

Websites of the listed manufacturing companies and Colombo Stock exchange.

Secondary data for the study were drawn from audited accounts (i.e. income statements and

balance sheets) of the concerned companies as fairly accurate and reliable. Therefore these data

may be considered reliable for the study.

Independent variable of this study is determinants such as profitability, capital intensity, tangibility

of assets, Non debt tax shield, firm size and dependent variable is debt to equity, long term leverage

and total leverage was used to identify the impact and relationship between determinants of capital

structure of listed manufacturing companies of Colombo Stock Exchange.

The data for this analysis used the cross sectional and time series data (Balanced panel data) for

41 companies during the period from 2014 to 2018.

3.5 Population

The Colombo Stock Exchange has 297 companies representing 20 business sectors as at 31st

December 2018. Among all of those sectors only manufacturing sector was selected as the

population for the study purpose. And there are 41 companies listed under manufacturing sector

on the Colombo Stock Exchange.

3.6 Sample

As mentioned above the target population of this study includes 41 listed manufacturing

companies. Then as per the data availability, 20 manufacturing companies have been selected as

the sample.

3.7 Data collection

The source of secondary data was adopted for the sampled data collection of this research study.

Necessary data was collected from 20 listed manufacturing companies ‟ annual reports (based on

availability of data) over 5 years ( 2014, 2015, 2016, 2017 & 2018).

In this study, the data was collected by using the secondary sources, such as:

Annual reports of the sample listed manufacturing companies.

Journals of the listed manufacturing companies in Sri Lanka.

Hand book of the listed companies in Sri Lanka published by Colombo Stock Exchange.

Websites of the listed manufacturing companies and Colombo Stock exchange.

Secondary data for the study were drawn from audited accounts (i.e. income statements and

balance sheets) of the concerned companies as fairly accurate and reliable. Therefore these data

may be considered reliable for the study.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

3.8 Methods of Analysis

In this research, use quantitative approach as main analysis tool. Since numerical and secondary

data is used quantitative approach is considered to be a suitable approach for the study. Statistical

analyses are used to describe an account for the observed variability in the data. This involves the

process of analyzing the data that has been collected. Thus the purpose of statistic is to summarize

and answer questions that were obtained in the research.

The collected data was interpreted and simplified to make them eligible for the research purpose.

The data analysis for the proposed research was performed with E-views computer package. The

model shows the relationship between determinants and capital structure as well as impact of

determinants on capital structure. Determinants such as profitability, capital intensity, tangibility

of assets, non debt tax shield and firm size are the independent variables whereas long term

leverage is the dependent variable.

And also for the analysis used both descriptive method (mean, mode & median) and inferential

method (correlation analysis & regression analysis). The upper level of statistical significance for

hypothesis testing was set at 5% (0.05).

3.8.1 Descriptive Statistics

Descriptive statistics are used to describe and summarize the behavior of the variables in a study.

It is include the numbers, tables, and graphs used to describe, organize, summarize, and present

raw data. Descriptive statistics are most often used to examine: Central tendency (location)

measures of data where data tend to fall, as measured by the mean, median, and mode. The mean

may not always be the best measure of central tendency, especially if data are skewed.

Standard deviation is expressed as the positive square root of the variance. It is the average

difference between observed values and the mean. The standard deviation is used when expressing

dispersion in the same units as the original measurements.

3.8.2 Inferential Statistics

Inferential statistics are used to draw conclusions about the reliability and generalizability of the

findings (Kleczyk, 2012). In order to test the research hypotheses; the inferential tests used include

the Pearson’s coefficient of correlation and Regression analysis.

3.8 Methods of Analysis

In this research, use quantitative approach as main analysis tool. Since numerical and secondary

data is used quantitative approach is considered to be a suitable approach for the study. Statistical

analyses are used to describe an account for the observed variability in the data. This involves the

process of analyzing the data that has been collected. Thus the purpose of statistic is to summarize

and answer questions that were obtained in the research.

The collected data was interpreted and simplified to make them eligible for the research purpose.

The data analysis for the proposed research was performed with E-views computer package. The

model shows the relationship between determinants and capital structure as well as impact of

determinants on capital structure. Determinants such as profitability, capital intensity, tangibility

of assets, non debt tax shield and firm size are the independent variables whereas long term

leverage is the dependent variable.

And also for the analysis used both descriptive method (mean, mode & median) and inferential

method (correlation analysis & regression analysis). The upper level of statistical significance for

hypothesis testing was set at 5% (0.05).

3.8.1 Descriptive Statistics

Descriptive statistics are used to describe and summarize the behavior of the variables in a study.

It is include the numbers, tables, and graphs used to describe, organize, summarize, and present

raw data. Descriptive statistics are most often used to examine: Central tendency (location)

measures of data where data tend to fall, as measured by the mean, median, and mode. The mean

may not always be the best measure of central tendency, especially if data are skewed.

Standard deviation is expressed as the positive square root of the variance. It is the average

difference between observed values and the mean. The standard deviation is used when expressing

dispersion in the same units as the original measurements.

3.8.2 Inferential Statistics

Inferential statistics are used to draw conclusions about the reliability and generalizability of the

findings (Kleczyk, 2012). In order to test the research hypotheses; the inferential tests used include

the Pearson’s coefficient of correlation and Regression analysis.

5

3.8.2.1 Correlation Analysis

Correlation analysis is concerned to describe the strength of relationship between two variables.

One of the most fundamental concepts in finding relationships between variables is the concept of

correlations. In this study the correlation analysis is to find out the relationship between capital

structure and the independent factors such as profitability , capital intensity, tangibility of assets,

non debt tax shield and firm size. Normally it represented by symbol “r” it is a number which lies

between -1 and +1. That is -1\< r /> +1.

r = 0 no correlation

r = (0 > +1) positive correlation (variables are simultaneously increased or decreased)

r = (0 <-1) negative correlation (when one variable is increased while other one decreased)

Pearson’s coefficient of correlation was used in research study to identify the relationships between

independent and dependent variable.

3.8.2.2 Regression Analysis

In statistics, regression analysis is a process for estimating the relationships among variables. It

includes many techniques for modeling and analyzing several variables, when the focus in on the

relationship between a dependent variable and one or more independent variables.

Regression analysis is also used to understand which among the independent variables are related

to the dependent variable, and to explore the forms of these relationships. A statistical measure

that attempts to determine the strength of the relationship between one dependent variable (usually

denoted by Y) and a series of other changing variables (known as independent variables)

In this study multiple regression analysis was performed to investigate the impact of determinants

of capital structure on capital structure which the model used for the study is given below.

Model – I

D/E R i,t = β0+β1PRO i,t +β2 CI i,t + β3 TA i,t + β4 NDT i,t + β5 FSIZE i,t + ε

Model – II

LTDR i,t = β0+β1PRO i,t +β2 CI i,t + β3 TA i,t + β4 NDT i,t + β5 FSIZE i,t + ε

Model – III

TDR i,t = β0+β1PRO i,t +β2 CI i,t + β3 TA i,t + β4 NDT i,t + β5 FSIZE i,t + ε

3.8.2.1 Correlation Analysis

Correlation analysis is concerned to describe the strength of relationship between two variables.

One of the most fundamental concepts in finding relationships between variables is the concept of

correlations. In this study the correlation analysis is to find out the relationship between capital

structure and the independent factors such as profitability , capital intensity, tangibility of assets,

non debt tax shield and firm size. Normally it represented by symbol “r” it is a number which lies

between -1 and +1. That is -1\< r /> +1.

r = 0 no correlation

r = (0 > +1) positive correlation (variables are simultaneously increased or decreased)

r = (0 <-1) negative correlation (when one variable is increased while other one decreased)

Pearson’s coefficient of correlation was used in research study to identify the relationships between

independent and dependent variable.

3.8.2.2 Regression Analysis

In statistics, regression analysis is a process for estimating the relationships among variables. It

includes many techniques for modeling and analyzing several variables, when the focus in on the

relationship between a dependent variable and one or more independent variables.

Regression analysis is also used to understand which among the independent variables are related

to the dependent variable, and to explore the forms of these relationships. A statistical measure

that attempts to determine the strength of the relationship between one dependent variable (usually

denoted by Y) and a series of other changing variables (known as independent variables)

In this study multiple regression analysis was performed to investigate the impact of determinants

of capital structure on capital structure which the model used for the study is given below.

Model – I

D/E R i,t = β0+β1PRO i,t +β2 CI i,t + β3 TA i,t + β4 NDT i,t + β5 FSIZE i,t + ε

Model – II

LTDR i,t = β0+β1PRO i,t +β2 CI i,t + β3 TA i,t + β4 NDT i,t + β5 FSIZE i,t + ε

Model – III

TDR i,t = β0+β1PRO i,t +β2 CI i,t + β3 TA i,t + β4 NDT i,t + β5 FSIZE i,t + ε

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Where,

PRO : Profitability

CI : Capital Intensity

TA : Tangibility of Assets

NDT : Non Debt Tax shield

FSIZE : Firm Size

β0 : constant variable

β1, β2, β3, β4, β5 : Model coefficients of variables

ε : Error term.

i,t : for firm i in period t

3.9 Hypotheses

The possible hypotheses are formulated based on conceptualization of the research problem and

research topic since the objective of this study to investigate the impact of determinants on capital

structure. Finally hypotheses are examined whether it is accepted or not.

If the H0 is rejected then the theory is congruent with practice and there is no gap. But if H0 is

accepted than there is a possibility of knowledge gap between theory and practice regarding the

influence of specific determinants on capital structure.

This research is conducted base on the following hypotheses.

H1: There is a significant relationship between determinants and capital structure.

H1a: There is a significant relationship between profitability and debt equity ratio.

H1b: There is a significant relationship between capital intensity and debt equity ratio.

H1c: There is a significant relationship between tangibility of assets and debt equity ratio.

H1d: There is a significant relationship between non debt tax shield and debt equity ratio.

H1e: There is a significant relationship between firm size and debt equity ratio.

H2: The determinants significantly impact on capital structure

H2a: profitability significantly impact on long term leverage.

H2b: Capital intensity significantly impact on long term leverage.

H2c: Tangibility of assets significantly impact on long term leverage.

H2d: Non debt tax shield significantly impact on long term leverage.

H2e: Firm size significantly impact on long term leverage.

Where,

PRO : Profitability

CI : Capital Intensity

TA : Tangibility of Assets

NDT : Non Debt Tax shield

FSIZE : Firm Size

β0 : constant variable

β1, β2, β3, β4, β5 : Model coefficients of variables

ε : Error term.

i,t : for firm i in period t

3.9 Hypotheses

The possible hypotheses are formulated based on conceptualization of the research problem and

research topic since the objective of this study to investigate the impact of determinants on capital

structure. Finally hypotheses are examined whether it is accepted or not.

If the H0 is rejected then the theory is congruent with practice and there is no gap. But if H0 is

accepted than there is a possibility of knowledge gap between theory and practice regarding the

influence of specific determinants on capital structure.

This research is conducted base on the following hypotheses.

H1: There is a significant relationship between determinants and capital structure.

H1a: There is a significant relationship between profitability and debt equity ratio.

H1b: There is a significant relationship between capital intensity and debt equity ratio.

H1c: There is a significant relationship between tangibility of assets and debt equity ratio.

H1d: There is a significant relationship between non debt tax shield and debt equity ratio.

H1e: There is a significant relationship between firm size and debt equity ratio.

H2: The determinants significantly impact on capital structure

H2a: profitability significantly impact on long term leverage.

H2b: Capital intensity significantly impact on long term leverage.

H2c: Tangibility of assets significantly impact on long term leverage.

H2d: Non debt tax shield significantly impact on long term leverage.

H2e: Firm size significantly impact on long term leverage.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

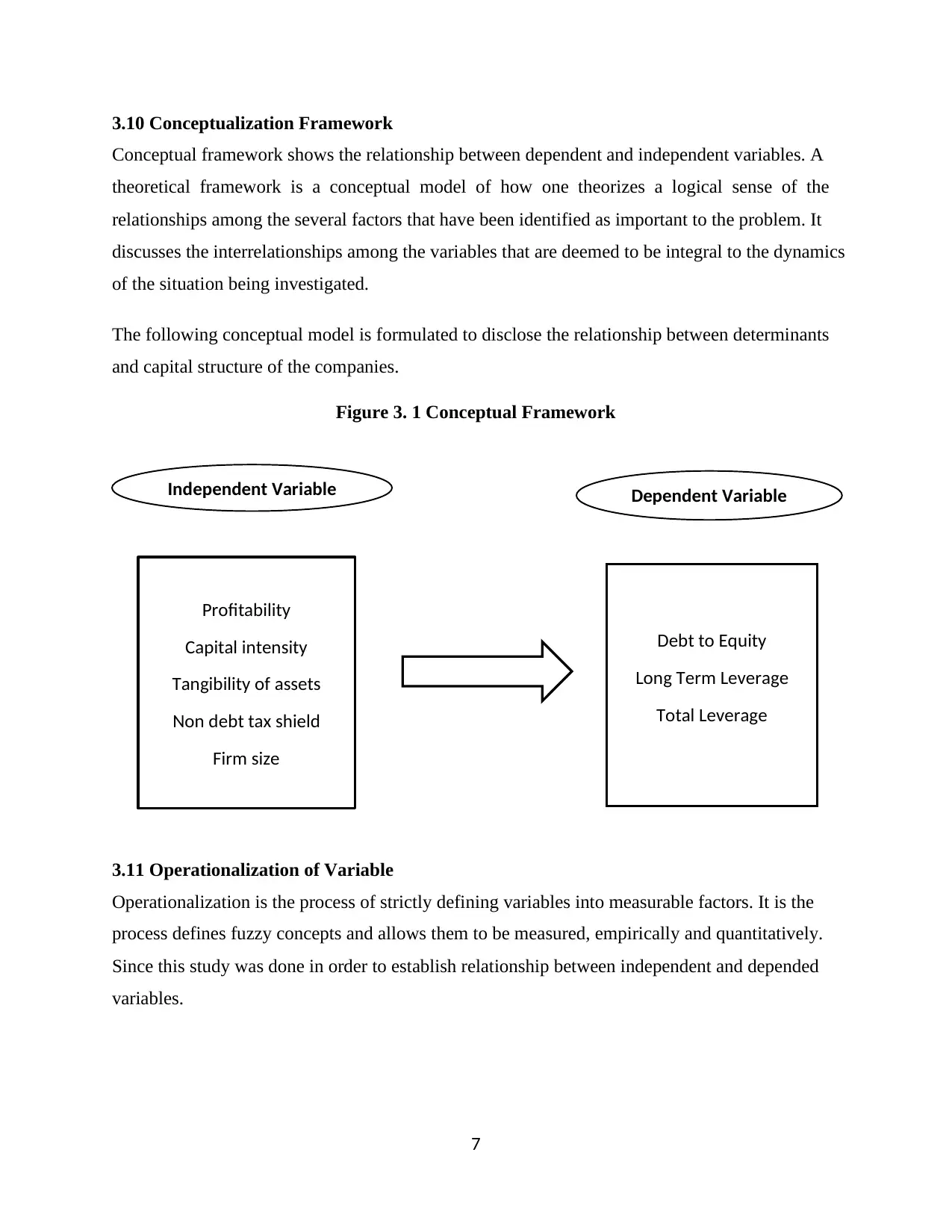

3.10 Conceptualization Framework

Conceptual framework shows the relationship between dependent and independent variables. A

theoretical framework is a conceptual model of how one theorizes a logical sense of the

relationships among the several factors that have been identified as important to the problem. It

discusses the interrelationships among the variables that are deemed to be integral to the dynamics

of the situation being investigated.

The following conceptual model is formulated to disclose the relationship between determinants

and capital structure of the companies.

Figure 3. 1 Conceptual Framework

3.11 Operationalization of Variable

Operationalization is the process of strictly defining variables into measurable factors. It is the

process defines fuzzy concepts and allows them to be measured, empirically and quantitatively.

Since this study was done in order to establish relationship between independent and depended

variables.

Dependent VariableIndependent Variable

Profitability

Capital intensity

Tangibility of assets

Non debt tax shield

Firm size

Debt to Equity

Long Term Leverage

Total Leverage

3.10 Conceptualization Framework

Conceptual framework shows the relationship between dependent and independent variables. A

theoretical framework is a conceptual model of how one theorizes a logical sense of the

relationships among the several factors that have been identified as important to the problem. It

discusses the interrelationships among the variables that are deemed to be integral to the dynamics

of the situation being investigated.

The following conceptual model is formulated to disclose the relationship between determinants

and capital structure of the companies.

Figure 3. 1 Conceptual Framework

3.11 Operationalization of Variable

Operationalization is the process of strictly defining variables into measurable factors. It is the

process defines fuzzy concepts and allows them to be measured, empirically and quantitatively.

Since this study was done in order to establish relationship between independent and depended

variables.

Dependent VariableIndependent Variable

Profitability

Capital intensity

Tangibility of assets

Non debt tax shield

Firm size

Debt to Equity

Long Term Leverage

Total Leverage

8

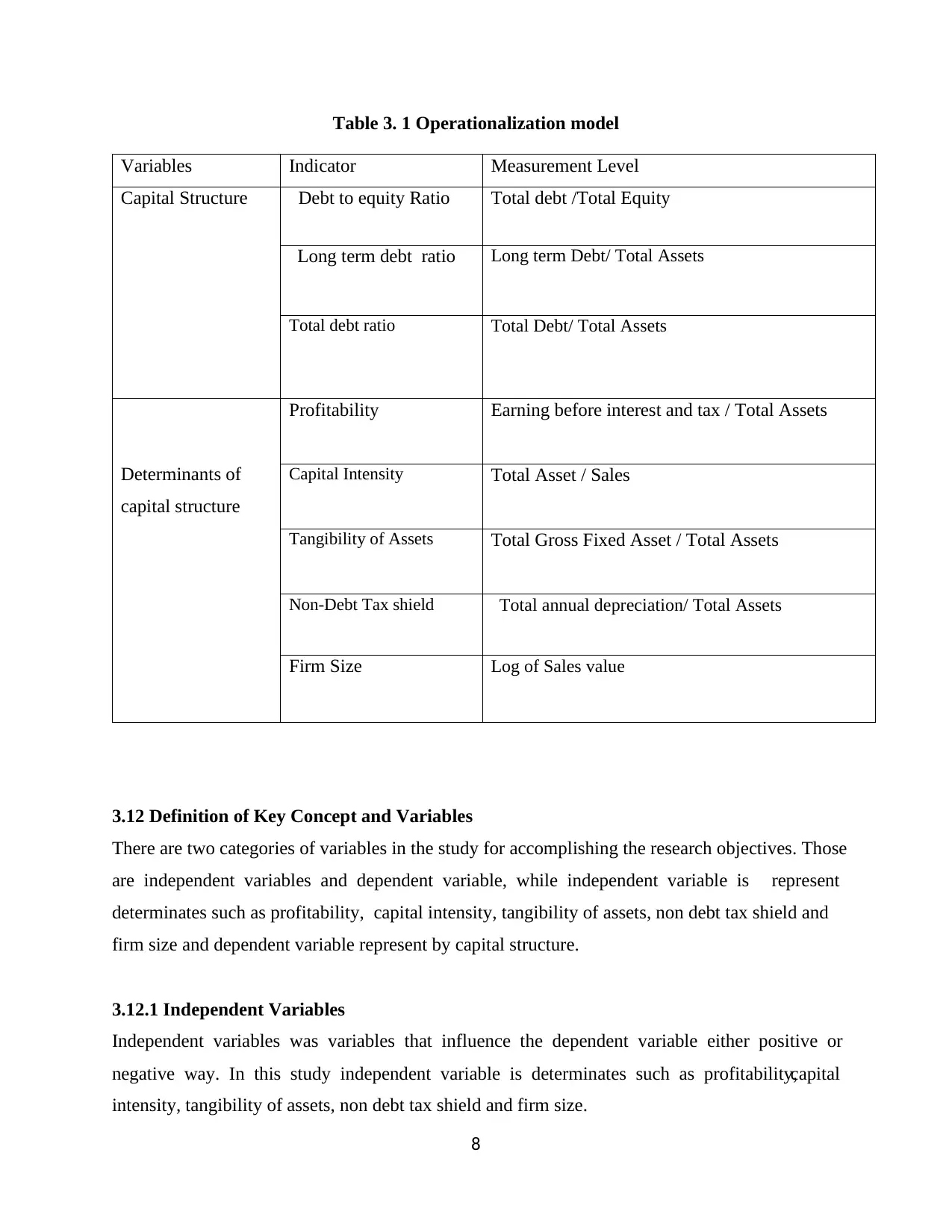

Table 3. 1 Operationalization model

3.12 Definition of Key Concept and Variables

There are two categories of variables in the study for accomplishing the research objectives. Those

are independent variables and dependent variable, while independent variable is represent

determinates such as profitability, capital intensity, tangibility of assets, non debt tax shield and

firm size and dependent variable represent by capital structure.

3.12.1 Independent Variables

Independent variables was variables that influence the dependent variable either positive or

negative way. In this study independent variable is determinates such as profitability,capital

intensity, tangibility of assets, non debt tax shield and firm size.

Variables Indicator Measurement Level

Capital Structure Debt to equity Ratio Total debt /Total Equity

Long term debt ratio Long term Debt/ Total Assets

Total debt ratio Total Debt/ Total Assets

Determinants of

capital structure

Profitability Earning before interest and tax / Total Assets

Capital Intensity Total Asset / Sales

Tangibility of Assets Total Gross Fixed Asset / Total Assets

Non-Debt Tax shield Total annual depreciation/ Total Assets

Firm Size Log of Sales value

Table 3. 1 Operationalization model

3.12 Definition of Key Concept and Variables

There are two categories of variables in the study for accomplishing the research objectives. Those

are independent variables and dependent variable, while independent variable is represent

determinates such as profitability, capital intensity, tangibility of assets, non debt tax shield and

firm size and dependent variable represent by capital structure.

3.12.1 Independent Variables

Independent variables was variables that influence the dependent variable either positive or

negative way. In this study independent variable is determinates such as profitability,capital

intensity, tangibility of assets, non debt tax shield and firm size.

Variables Indicator Measurement Level

Capital Structure Debt to equity Ratio Total debt /Total Equity

Long term debt ratio Long term Debt/ Total Assets

Total debt ratio Total Debt/ Total Assets

Determinants of

capital structure

Profitability Earning before interest and tax / Total Assets

Capital Intensity Total Asset / Sales

Tangibility of Assets Total Gross Fixed Asset / Total Assets

Non-Debt Tax shield Total annual depreciation/ Total Assets

Firm Size Log of Sales value

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

3.12.1.1 profitability

According to the tradeoff theory, firms will acquire more debt to prevent managers from wasting

cash free flows gained from profits. Cortez and Susanto (2012) and Bassey et al. (2014) measured

profitability as the corporation’s operating profit divided by its total assets for each year. In

addition, Pratheepan and weerakoon Banda, (2016) used profit after tax divided by total assets,

while Chakraborty, (2013) measured profitability as net annual cash flow divided by total assets.

In this research, the equation for calculating corporate profitability was as follows,

Corporate profitability = Earnings before Interest and Tax

Total Assets

3.12.1.2 Capital intensity

Capital intensity, or the employment of fixed assets, is generally synonymous with the concept of

operating leverage. Thus, increased capital intensity implies increased risk of future earnings

variation. Therefore, top management’s desire to retain control of the firm, and the concern of

creditors to limit risk of default, should result in lower debt levels for firms choosing automation

over labor as the primary factor of production, ceteris paribus (Barton and Gordon, 1988). On the

other hand, the traditional argument is the more capital intensive a firm is, larger will be the need

for long-term debt by the firm due to larger financial requirements and it will also have access to

assets which could be collateralized. So, this study hypothesizes that ceteris paribus, capital

intensity to be negatively related to total debt and short-term debt and positively related to long-

term debt.

Capital intensity can be calculated as following equation:

Capital intensity = Total Assets

Sales

3.12.1.3 Tangibility of assets

Supporting the trade-off theory Rajan and Zingales, (1995) and Titman and Roberto, (1988) stated that

assets tangibility will have a positive relationship with debt ratio because greater collateral may

alleviate the agency costs of the debt itself.

The nature of corporation assets has been represented by asset tangibility by most studies such as

Frank and Goyal (2009), Kayo (2011) measured as tangible or fixed assets over total assets.

3.12.1.1 profitability

According to the tradeoff theory, firms will acquire more debt to prevent managers from wasting

cash free flows gained from profits. Cortez and Susanto (2012) and Bassey et al. (2014) measured

profitability as the corporation’s operating profit divided by its total assets for each year. In

addition, Pratheepan and weerakoon Banda, (2016) used profit after tax divided by total assets,

while Chakraborty, (2013) measured profitability as net annual cash flow divided by total assets.

In this research, the equation for calculating corporate profitability was as follows,

Corporate profitability = Earnings before Interest and Tax

Total Assets

3.12.1.2 Capital intensity

Capital intensity, or the employment of fixed assets, is generally synonymous with the concept of

operating leverage. Thus, increased capital intensity implies increased risk of future earnings

variation. Therefore, top management’s desire to retain control of the firm, and the concern of

creditors to limit risk of default, should result in lower debt levels for firms choosing automation

over labor as the primary factor of production, ceteris paribus (Barton and Gordon, 1988). On the

other hand, the traditional argument is the more capital intensive a firm is, larger will be the need

for long-term debt by the firm due to larger financial requirements and it will also have access to

assets which could be collateralized. So, this study hypothesizes that ceteris paribus, capital

intensity to be negatively related to total debt and short-term debt and positively related to long-

term debt.

Capital intensity can be calculated as following equation:

Capital intensity = Total Assets

Sales

3.12.1.3 Tangibility of assets

Supporting the trade-off theory Rajan and Zingales, (1995) and Titman and Roberto, (1988) stated that

assets tangibility will have a positive relationship with debt ratio because greater collateral may

alleviate the agency costs of the debt itself.

The nature of corporation assets has been represented by asset tangibility by most studies such as

Frank and Goyal (2009), Kayo (2011) measured as tangible or fixed assets over total assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

In this study the assets tangibility is calculating as :

Assets Tangibility = Total gross fixed assets

Total assets

3.12.1.4 Non debt tax shield

In order to reduce the tax bill, firms want to exploit the tax deductibility of interest. If they have

other tax deductible item which they can use as tax shield other than debt then the leverage is low.

So, there exists a negative relationship between non debt tax shield and leverage. DeAngelo and

Masulis (1980) say that non-debt tax shields can be substitutes for the tax benefits of debt financing

and a firm with larger non-debt tax shields is expected to use less debt. Past empirical studies also

show mixed results about the relationship of non-debt tax shield and leverage. Gardner and Trcinka

(1992) find a positive relationship between non-debt tax shield while Shenoy and Koch (1996)

find a negative relation. This study expects a negative relationship between non – debt tax shield and

leverage.

It can be calculated as following equation:

Non debt tax shield = Total annual depreciations

Total Assets

3.12.1.5 Firm size

As discussed in Rajan and Zingales (1995), the theoretical prediction for the effect of size on

leverage is ambiguous. It is argued that larger firms tend to be more diversified and have more

tangible assets, stable cash flows and better reputations. The trade-off theory therefore postulates

that compared to smaller ones, ceteris paribus, larger firms are expected to have a higher debt

capacity due to a lower risk of bankruptcy (bankruptcy cost).

In contrast, the pecking-order theory suggests that, bigger firms are more likely to use less debt

due to lower asymmetric information problems between insiders and outside investors (i.e. larger

firms provide more information to lenders than smaller firms, so the cost of issuing new equity is

lower than the debt issuing cost).

3.12.2 Dependent Variable

Dependent variables were variables depend on other variables for its success and existence. In this

study dependent variable is capital structure.

In this study the assets tangibility is calculating as :

Assets Tangibility = Total gross fixed assets

Total assets

3.12.1.4 Non debt tax shield

In order to reduce the tax bill, firms want to exploit the tax deductibility of interest. If they have

other tax deductible item which they can use as tax shield other than debt then the leverage is low.

So, there exists a negative relationship between non debt tax shield and leverage. DeAngelo and

Masulis (1980) say that non-debt tax shields can be substitutes for the tax benefits of debt financing

and a firm with larger non-debt tax shields is expected to use less debt. Past empirical studies also

show mixed results about the relationship of non-debt tax shield and leverage. Gardner and Trcinka

(1992) find a positive relationship between non-debt tax shield while Shenoy and Koch (1996)

find a negative relation. This study expects a negative relationship between non – debt tax shield and

leverage.

It can be calculated as following equation:

Non debt tax shield = Total annual depreciations

Total Assets

3.12.1.5 Firm size

As discussed in Rajan and Zingales (1995), the theoretical prediction for the effect of size on

leverage is ambiguous. It is argued that larger firms tend to be more diversified and have more

tangible assets, stable cash flows and better reputations. The trade-off theory therefore postulates

that compared to smaller ones, ceteris paribus, larger firms are expected to have a higher debt

capacity due to a lower risk of bankruptcy (bankruptcy cost).

In contrast, the pecking-order theory suggests that, bigger firms are more likely to use less debt

due to lower asymmetric information problems between insiders and outside investors (i.e. larger

firms provide more information to lenders than smaller firms, so the cost of issuing new equity is

lower than the debt issuing cost).

3.12.2 Dependent Variable

Dependent variables were variables depend on other variables for its success and existence. In this

study dependent variable is capital structure.

11

3.12.2.1 Debt to equity Ratio

A debt ratio used to measure a company’s financial leverage, calculated by dividing a company’s

total liabilities by it’s shareholders equity. The D/E ratio indicates how much debt a company is

using to finance its assets relative to the amount of value represented in shareholder’s equity.

D/E ratio = Total Debt

Total Equity

3.12.2.2 Long term debt ratio

A measurement representing the percentage of a corporation’s assets that are financed with loan

and financial obligations lasting more than one year. The ratio provides a general measure of the

financial position of a company, including its ability to meet financial requirements for outstanding

loans.

This ratio can be calculated by this formula:

Long term debt ratio = Long term debt

Total assets

3.12.2.3 Total debt ratio

The debt ratio indicates the percentage of the total assets amounts that is owned by creditors.

The larger debt ratio the greater is the company’s financial leverage. The appropriate debt ratio

depends on the industry and factors that are unique to the company.

The debt ratio also known as the debt to total assets ratio. Hence, the formula for the debt ratio is

as follows.

Debt ratio = Total debt

Total assets

3.12.2.1 Debt to equity Ratio

A debt ratio used to measure a company’s financial leverage, calculated by dividing a company’s

total liabilities by it’s shareholders equity. The D/E ratio indicates how much debt a company is

using to finance its assets relative to the amount of value represented in shareholder’s equity.

D/E ratio = Total Debt

Total Equity

3.12.2.2 Long term debt ratio

A measurement representing the percentage of a corporation’s assets that are financed with loan

and financial obligations lasting more than one year. The ratio provides a general measure of the

financial position of a company, including its ability to meet financial requirements for outstanding

loans.

This ratio can be calculated by this formula:

Long term debt ratio = Long term debt

Total assets

3.12.2.3 Total debt ratio

The debt ratio indicates the percentage of the total assets amounts that is owned by creditors.

The larger debt ratio the greater is the company’s financial leverage. The appropriate debt ratio

depends on the industry and factors that are unique to the company.

The debt ratio also known as the debt to total assets ratio. Hence, the formula for the debt ratio is

as follows.

Debt ratio = Total debt

Total assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.