University Finance: Developing and Managing a Budget Report

VerifiedAdded on 2020/05/04

|19

|1647

|42

Report

AI Summary

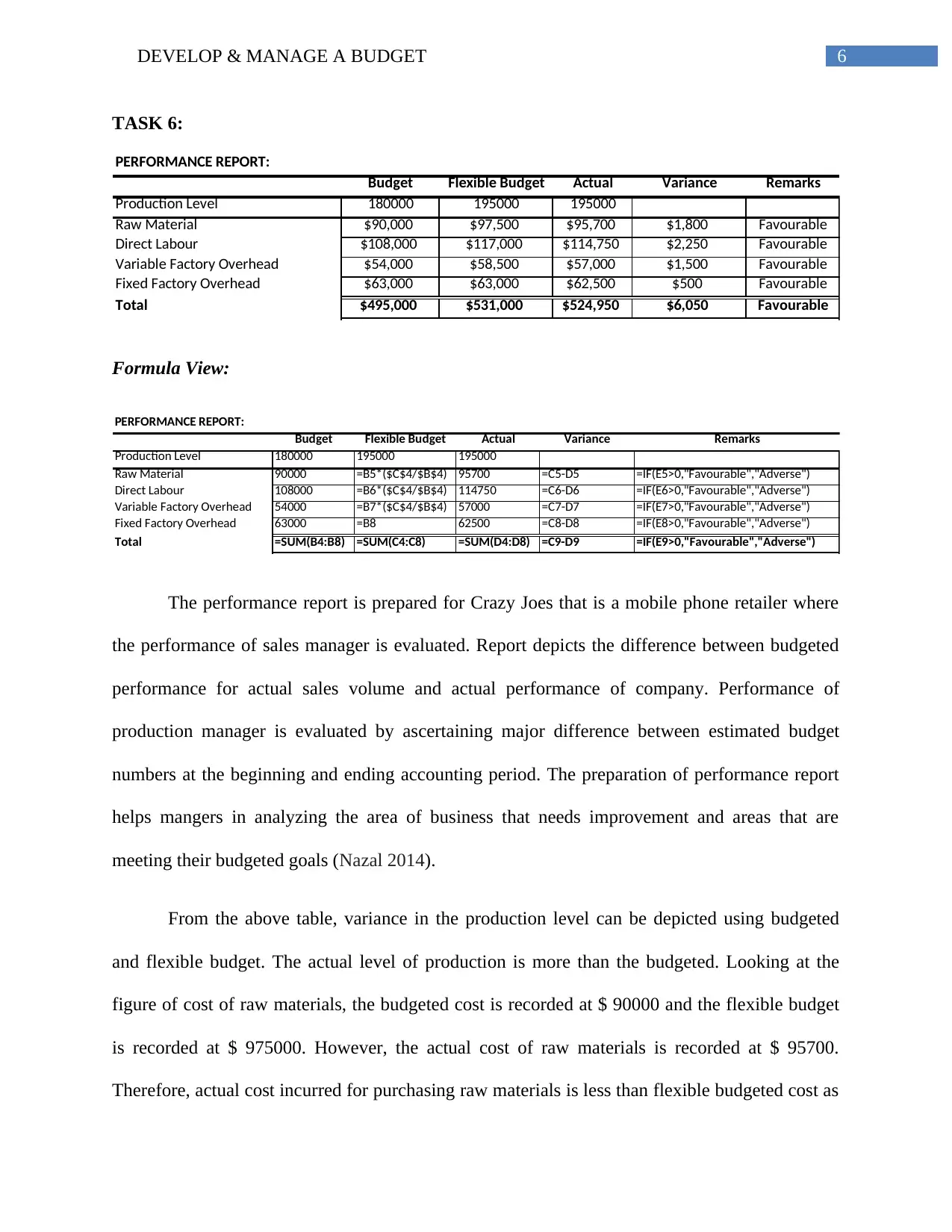

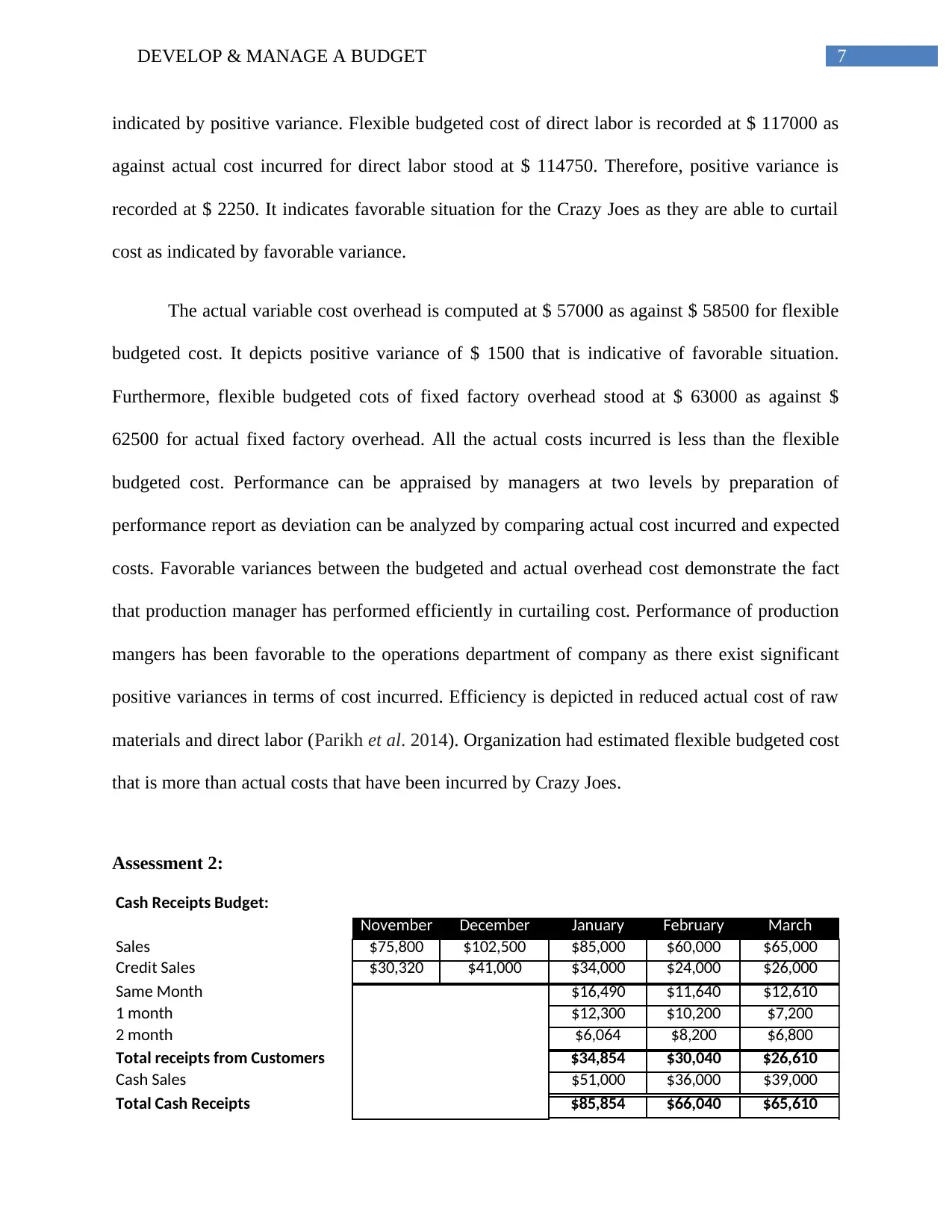

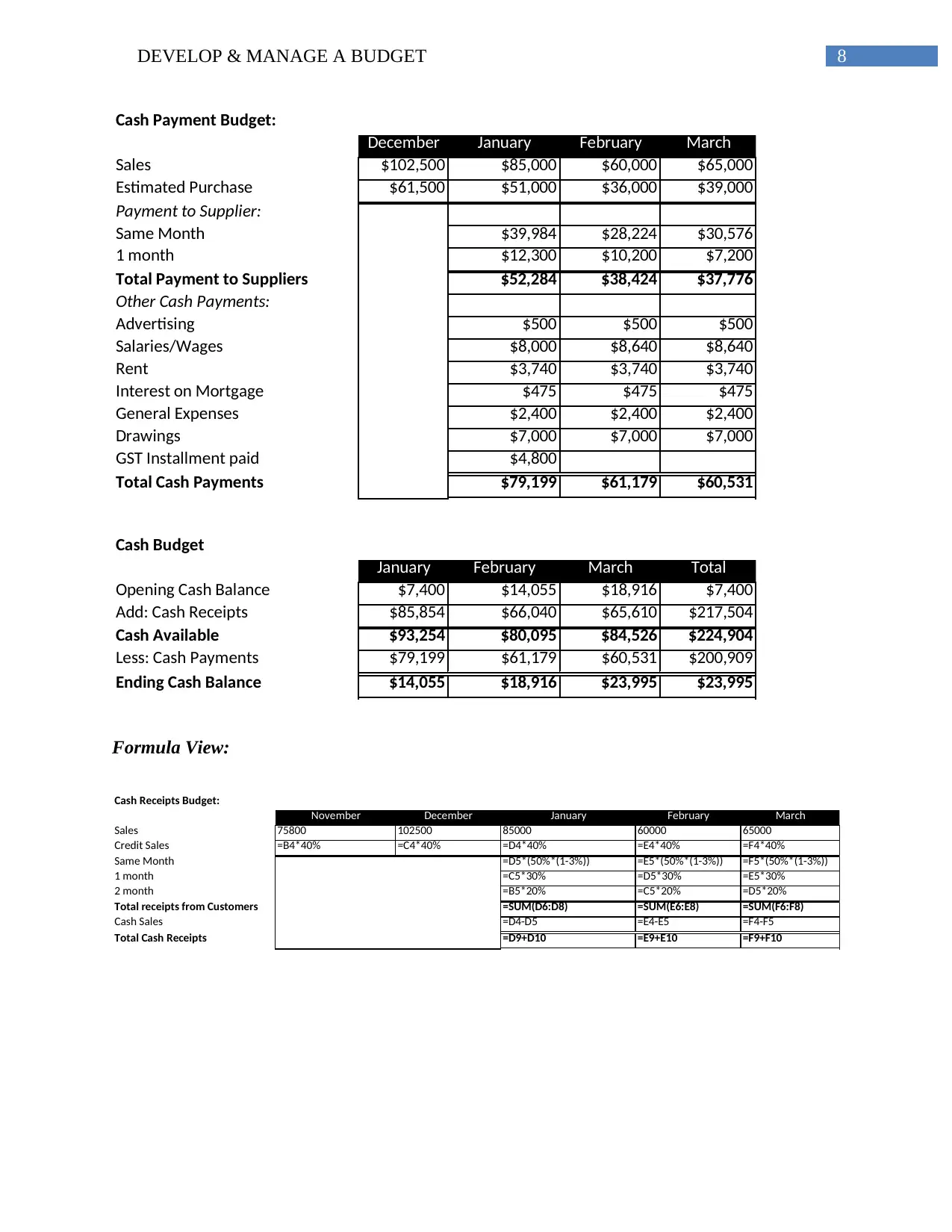

This report provides a comprehensive analysis of budget development and management, focusing on a case study of a mobile phone retailer, Crazy Joes. It details the preparation of performance reports to evaluate sales and production managers, highlighting variance analysis between budgeted and actual figures. The report examines cost control, efficiency, and the impact of flexible budgeting on raw materials, direct labor, and overhead costs. It also explores budgetary control as a management tool, emphasizing its role in coordination, financial scrutiny, resource optimization, and performance assessment. The report discusses the objectives of budgetary control, including enhanced coordination, efficient resource utilization, and the ability to monitor and control financial aspects of the business. It highlights the importance of aligning actual financial results with budgeted figures for effective management and the use of budgetary control in forecasting, planning, and communication. Furthermore, the report addresses the impact of both internal and external factors on budget modifications and the role of management accounting control systems in adapting to changing environmental circumstances, emphasizing cost control and performance evaluation.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.