Developing Audit Program: Huon Aquaculture Group Limited - HA3032

VerifiedAdded on 2022/11/25

|10

|577

|282

Report

AI Summary

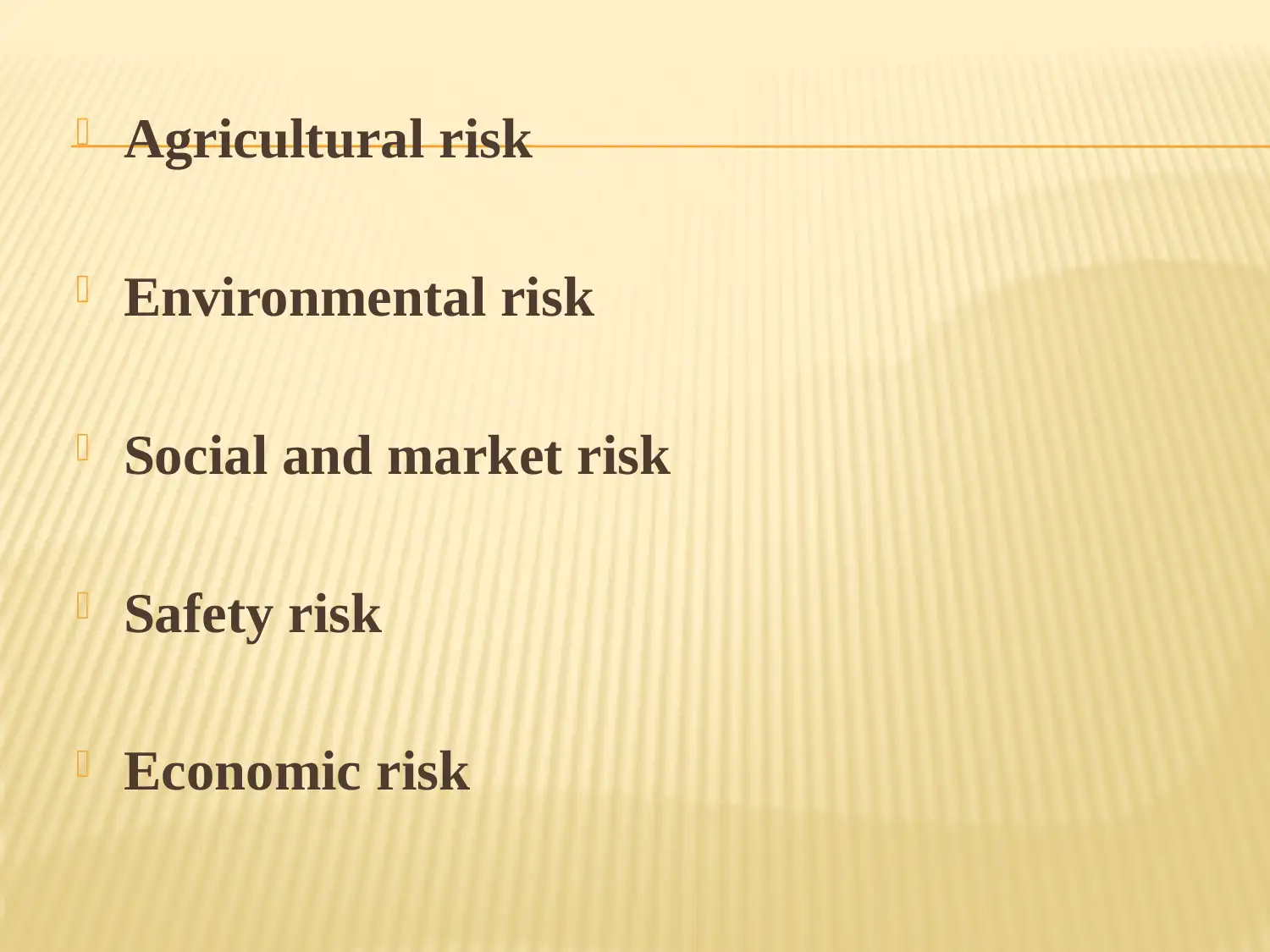

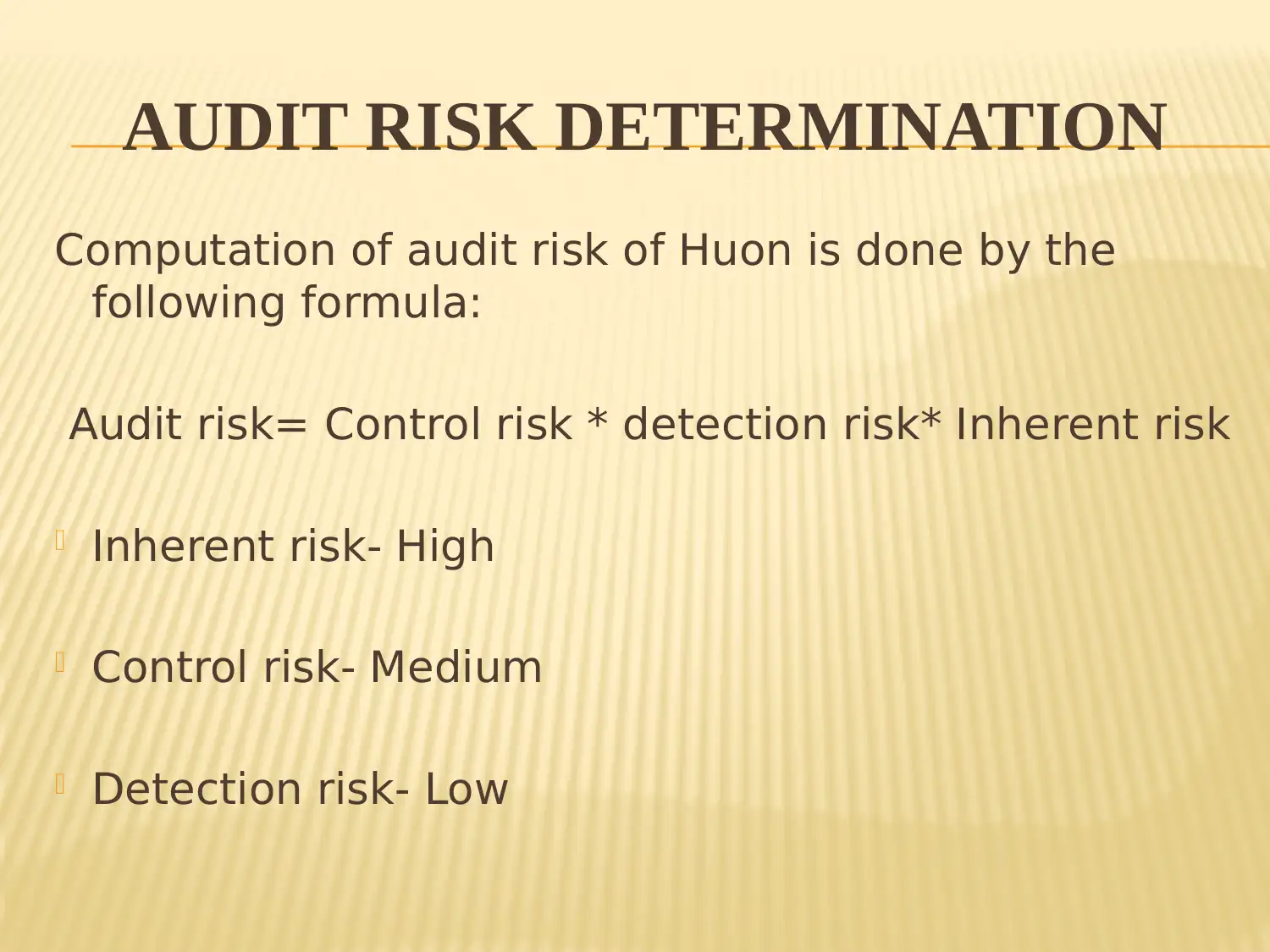

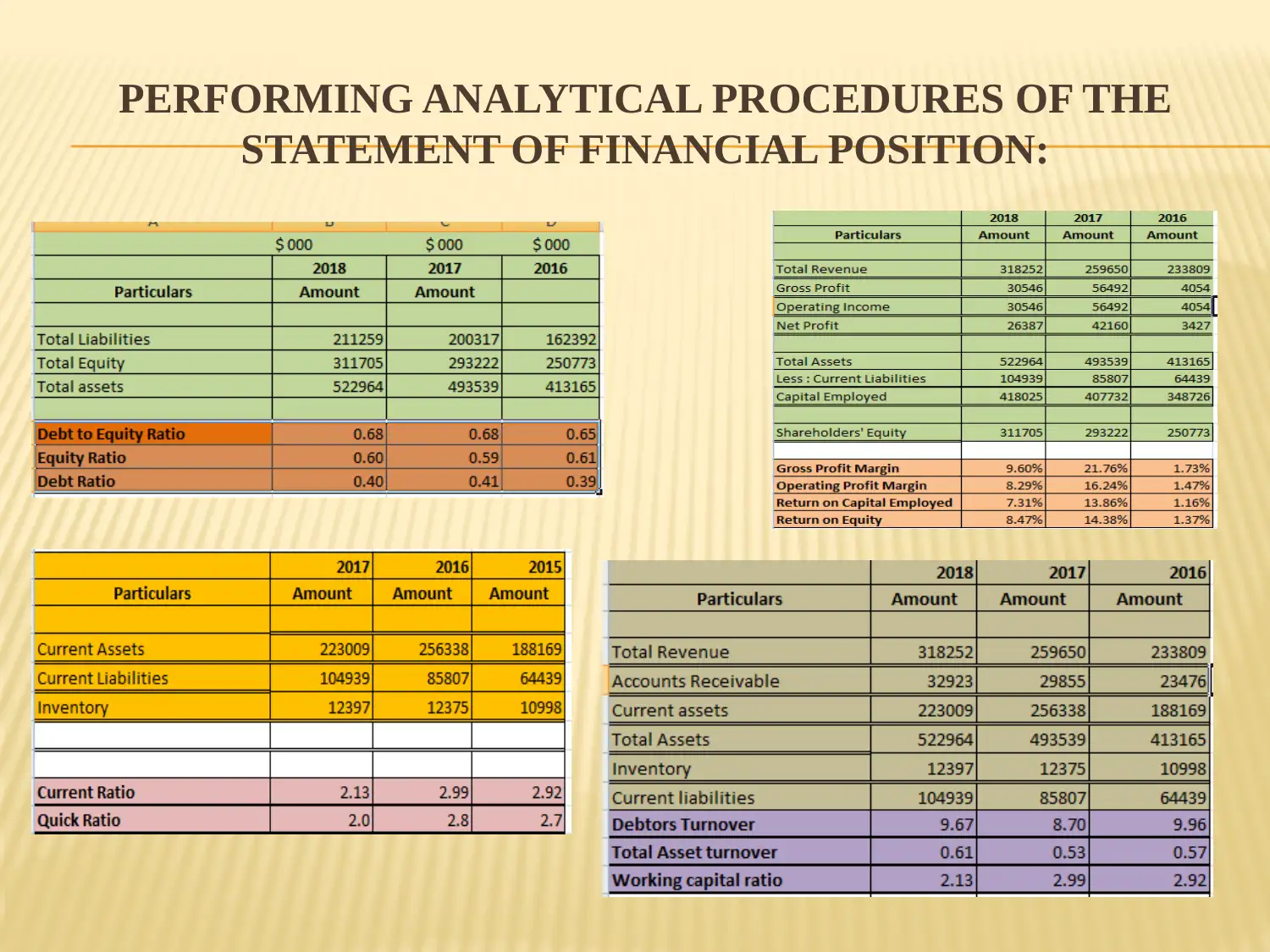

This report provides a comprehensive analysis of an audit program developed for Huon Aquaculture Group Limited, a vertically integrated salmon producer. The assignment focuses on identifying and understanding the business risks faced by the company, including agricultural, environmental, social, market, safety, and economic risks. The audit risk determination is calculated using the formula: Audit risk = Control risk * Detection risk * Inherent risk. The report details the identification of material account balances, the determination of materiality based on the perception of financial statement users and qualitative aspects, and the implementation of analytical procedures. The conclusion highlights the significantly higher level of inherent risk compared to detection and control risks, emphasizing the auditor's professional judgment in assessing account balances and setting accurate thresholds. The total audit risk of Huon Aquaculture Group Limited is determined to be low, supported by references to relevant literature on audit procedures and risk management.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.