Developing an Audit Program for Legend Corporation Limited Report

VerifiedAdded on 2021/02/21

|14

|3881

|108

Report

AI Summary

This report provides a comprehensive audit program for Legend Corporation Limited, an ASX-listed engineering solutions provider. It begins by identifying key business risks and factors impacting inherent and control risks, followed by analytical procedures of the statement of financial position and performance over the last three years. The report then determines material account balances, including five assets and liabilities, and lists relevant financial report assertions. Subsequently, it designs a comprehensive set of audit work steps for each material account balance, incorporating a sampling plan. The analysis includes liquidity, leverage, efficiency, and profitability ratios, and the report emphasizes the importance of materiality in audit planning. The report provides an in-depth examination of the company's financial health and provides a framework for conducting a thorough audit.

DEVELOPING AN AUDIT PROGRAM

FOR A SELECTED PUBLICALLY

LISTED COMPANY

FOR A SELECTED PUBLICALLY

LISTED COMPANY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

1. Selecting listed company....................................................................................................3

2. Nature and industry along with identifying key business risks and factors impacting inherent

and control risk.......................................................................................................................3

3. Performing analytical procedures of statement of financial position and financial

performance over last three years with ratios.........................................................................4

4. Discussing that account balances which are considered as material..................................7

5. Selecting different material account balances with five assets and liabilities....................7

6. Listing relevant financial report assertions of material account with reason.....................8

7. Designing comprehensive set of audit work steps for every material account balances..10

8. Including sampling plan with use of every material account balance..............................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

Books and journal.................................................................................................................14

INTRODUCTION...........................................................................................................................3

1. Selecting listed company....................................................................................................3

2. Nature and industry along with identifying key business risks and factors impacting inherent

and control risk.......................................................................................................................3

3. Performing analytical procedures of statement of financial position and financial

performance over last three years with ratios.........................................................................4

4. Discussing that account balances which are considered as material..................................7

5. Selecting different material account balances with five assets and liabilities....................7

6. Listing relevant financial report assertions of material account with reason.....................8

7. Designing comprehensive set of audit work steps for every material account balances..10

8. Including sampling plan with use of every material account balance..............................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

Books and journal.................................................................................................................14

INTRODUCTION

Auditing is referred as detailed examination of financial reports of company and is used

for offering confidence for every stakeholders about accurate accounting reports of organizations.

In simple words, it is known as accumulation and evaluation of evidence to identify and report on

degree of correspondence among reflected information and established criteria. The present report

is analysing ASX listed company Legend corporation Limited with its nature and identify and this

will determine key business risks. There will be consideration of factors which impacts inherent

and control risks along with application of Audit Risk model. It will perform analytical

procedures of statement of financial position and performance over last three years and material

balances will be considered. This report will discuss different material account balances with five

assets and liabilities and designing comprehensive set of audit works for every material account

and addressing assertions for every account. Lastly, this will include sampling plan for every

material account balance to be tested.

1. Selecting listed company

Legend Corporation Limited

2. Nature and industry along with identifying key business risks and factors impacting inherent

and control risk

Legend Corporation Limited is an Australian engineering solutions providers which

operates in information technology, electrical, power utility and semi conductor industries

(Annual report of Legend Corporation Ltd, 2018). It is listed on Australian Securities exchange

since March 2004 as this operates through three segments as Gas and Plumbing Supplies,

Electrical, Power and Infrastructure and Innovative Electrical Solutions.

Key business risk High medium Low

Interest rate risk Medium

Foreign currency risk Low

Liquidity risk Low

Credit risk analysis Low

Interest rate risk: The exposure of this risk increase with financial assets and liabilities

recognised at reporting date where alteration in interest rate impact future cash flows of fair value

of fixed rate financial instruments (Wen, Xiao and Wang, 2018). Its policy is to minimise or

Auditing is referred as detailed examination of financial reports of company and is used

for offering confidence for every stakeholders about accurate accounting reports of organizations.

In simple words, it is known as accumulation and evaluation of evidence to identify and report on

degree of correspondence among reflected information and established criteria. The present report

is analysing ASX listed company Legend corporation Limited with its nature and identify and this

will determine key business risks. There will be consideration of factors which impacts inherent

and control risks along with application of Audit Risk model. It will perform analytical

procedures of statement of financial position and performance over last three years and material

balances will be considered. This report will discuss different material account balances with five

assets and liabilities and designing comprehensive set of audit works for every material account

and addressing assertions for every account. Lastly, this will include sampling plan for every

material account balance to be tested.

1. Selecting listed company

Legend Corporation Limited

2. Nature and industry along with identifying key business risks and factors impacting inherent

and control risk

Legend Corporation Limited is an Australian engineering solutions providers which

operates in information technology, electrical, power utility and semi conductor industries

(Annual report of Legend Corporation Ltd, 2018). It is listed on Australian Securities exchange

since March 2004 as this operates through three segments as Gas and Plumbing Supplies,

Electrical, Power and Infrastructure and Innovative Electrical Solutions.

Key business risk High medium Low

Interest rate risk Medium

Foreign currency risk Low

Liquidity risk Low

Credit risk analysis Low

Interest rate risk: The exposure of this risk increase with financial assets and liabilities

recognised at reporting date where alteration in interest rate impact future cash flows of fair value

of fixed rate financial instruments (Wen, Xiao and Wang, 2018). Its policy is to minimise or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reduce interest rate cash flow risk exposure on funding for long term perspective with use of blend

of floating and fixed interest rate debt which is at medium level.

Foreign currency risk: It is low because organization is having its overseas operations as of sales

and purchases which are denominated in US dollars. The nature of USD is relatively very small

and frequent and formally designate forward contracts as hedging instruments instead of

considering contracts to be part of arrangements of economic hedge.

Liquidity risk: It is very low as debts has been settled along with obligation on basis of

financial liabilities (Kogan, Sudit and Vasarhelyi, 2018). This group has managed risk by

maintaining reputable credit profile and to invest in surplus cash with major financial institutions.

3. Performing analytical procedures of statement of financial position and financial performance

over last three years with ratios

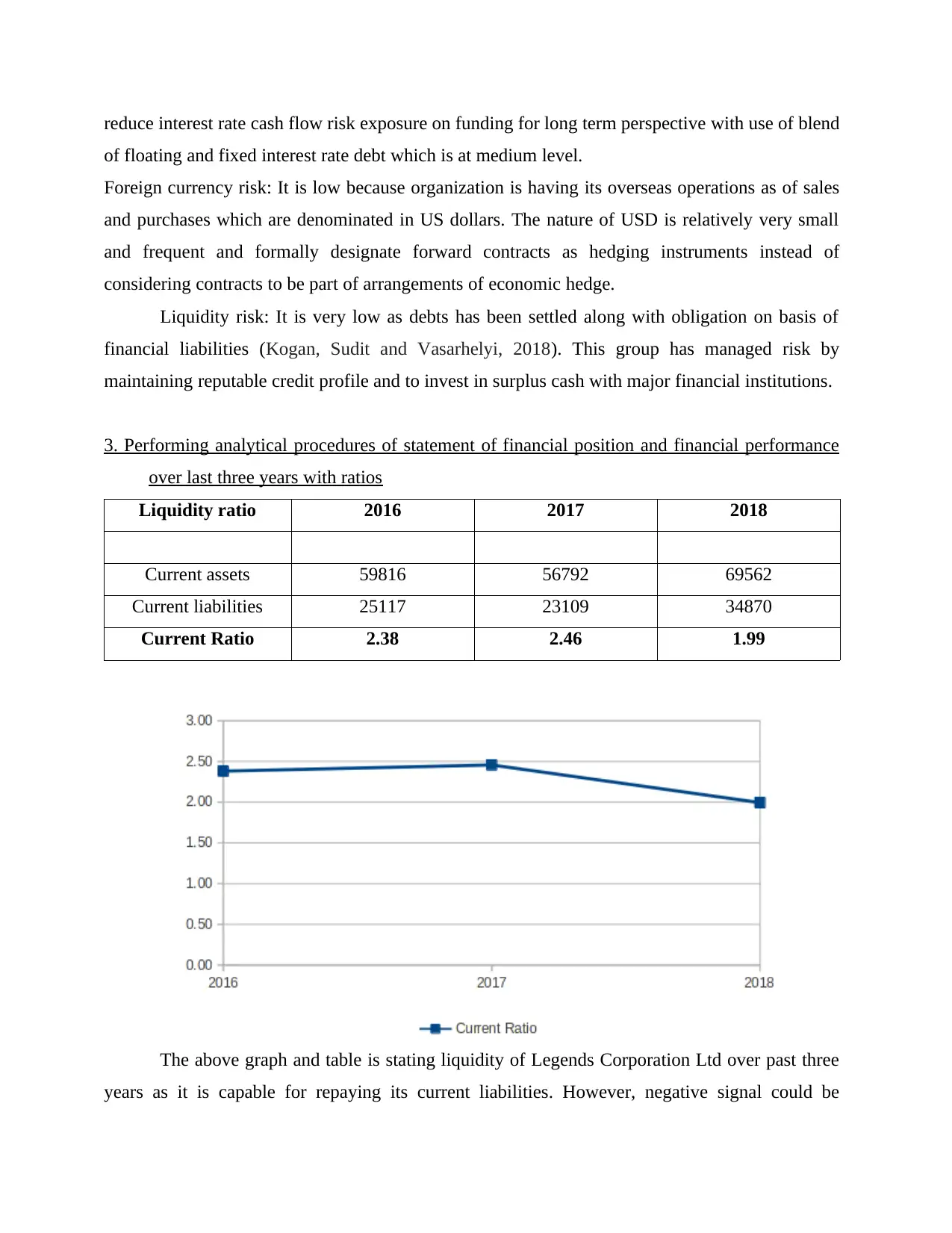

Liquidity ratio 2016 2017 2018

Current assets 59816 56792 69562

Current liabilities 25117 23109 34870

Current Ratio 2.38 2.46 1.99

The above graph and table is stating liquidity of Legends Corporation Ltd over past three

years as it is capable for repaying its current liabilities. However, negative signal could be

of floating and fixed interest rate debt which is at medium level.

Foreign currency risk: It is low because organization is having its overseas operations as of sales

and purchases which are denominated in US dollars. The nature of USD is relatively very small

and frequent and formally designate forward contracts as hedging instruments instead of

considering contracts to be part of arrangements of economic hedge.

Liquidity risk: It is very low as debts has been settled along with obligation on basis of

financial liabilities (Kogan, Sudit and Vasarhelyi, 2018). This group has managed risk by

maintaining reputable credit profile and to invest in surplus cash with major financial institutions.

3. Performing analytical procedures of statement of financial position and financial performance

over last three years with ratios

Liquidity ratio 2016 2017 2018

Current assets 59816 56792 69562

Current liabilities 25117 23109 34870

Current Ratio 2.38 2.46 1.99

The above graph and table is stating liquidity of Legends Corporation Ltd over past three

years as it is capable for repaying its current liabilities. However, negative signal could be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

observed as it is decreasing in 2018 so it should imply the implications for improving or

maintaining it.

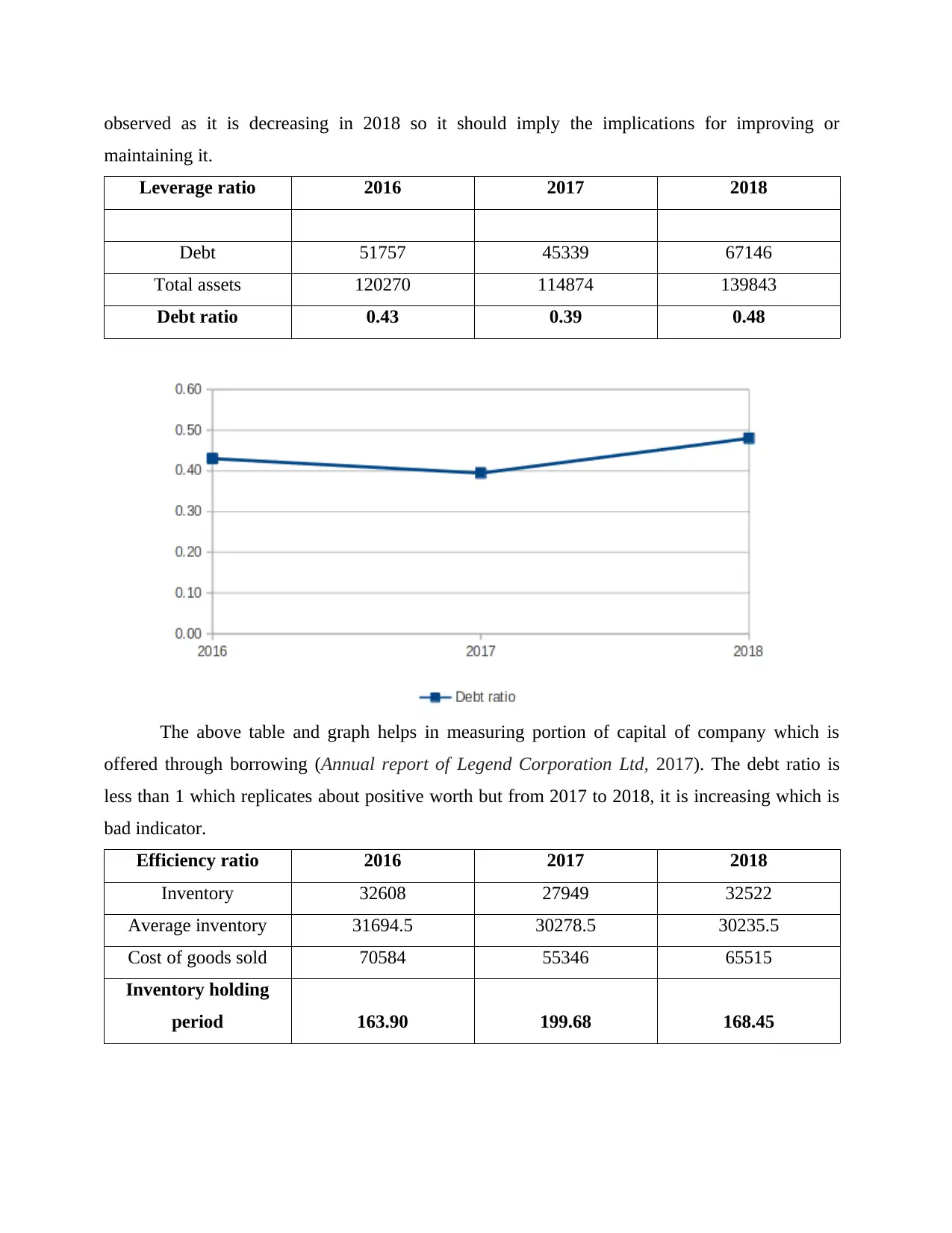

Leverage ratio 2016 2017 2018

Debt 51757 45339 67146

Total assets 120270 114874 139843

Debt ratio 0.43 0.39 0.48

The above table and graph helps in measuring portion of capital of company which is

offered through borrowing (Annual report of Legend Corporation Ltd, 2017). The debt ratio is

less than 1 which replicates about positive worth but from 2017 to 2018, it is increasing which is

bad indicator.

Efficiency ratio 2016 2017 2018

Inventory 32608 27949 32522

Average inventory 31694.5 30278.5 30235.5

Cost of goods sold 70584 55346 65515

Inventory holding

period 163.90 199.68 168.45

maintaining it.

Leverage ratio 2016 2017 2018

Debt 51757 45339 67146

Total assets 120270 114874 139843

Debt ratio 0.43 0.39 0.48

The above table and graph helps in measuring portion of capital of company which is

offered through borrowing (Annual report of Legend Corporation Ltd, 2017). The debt ratio is

less than 1 which replicates about positive worth but from 2017 to 2018, it is increasing which is

bad indicator.

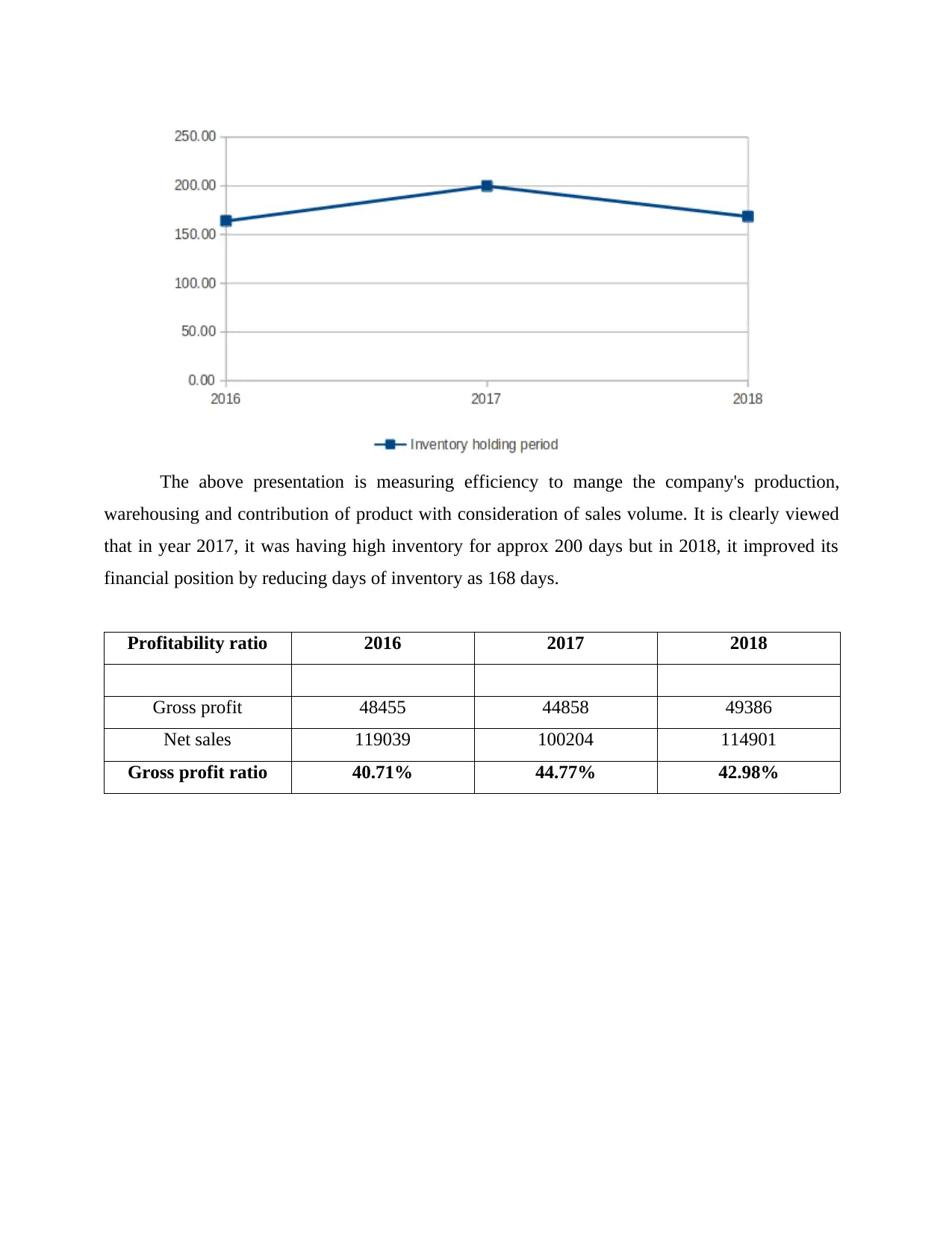

Efficiency ratio 2016 2017 2018

Inventory 32608 27949 32522

Average inventory 31694.5 30278.5 30235.5

Cost of goods sold 70584 55346 65515

Inventory holding

period 163.90 199.68 168.45

The above presentation is measuring efficiency to mange the company's production,

warehousing and contribution of product with consideration of sales volume. It is clearly viewed

that in year 2017, it was having high inventory for approx 200 days but in 2018, it improved its

financial position by reducing days of inventory as 168 days.

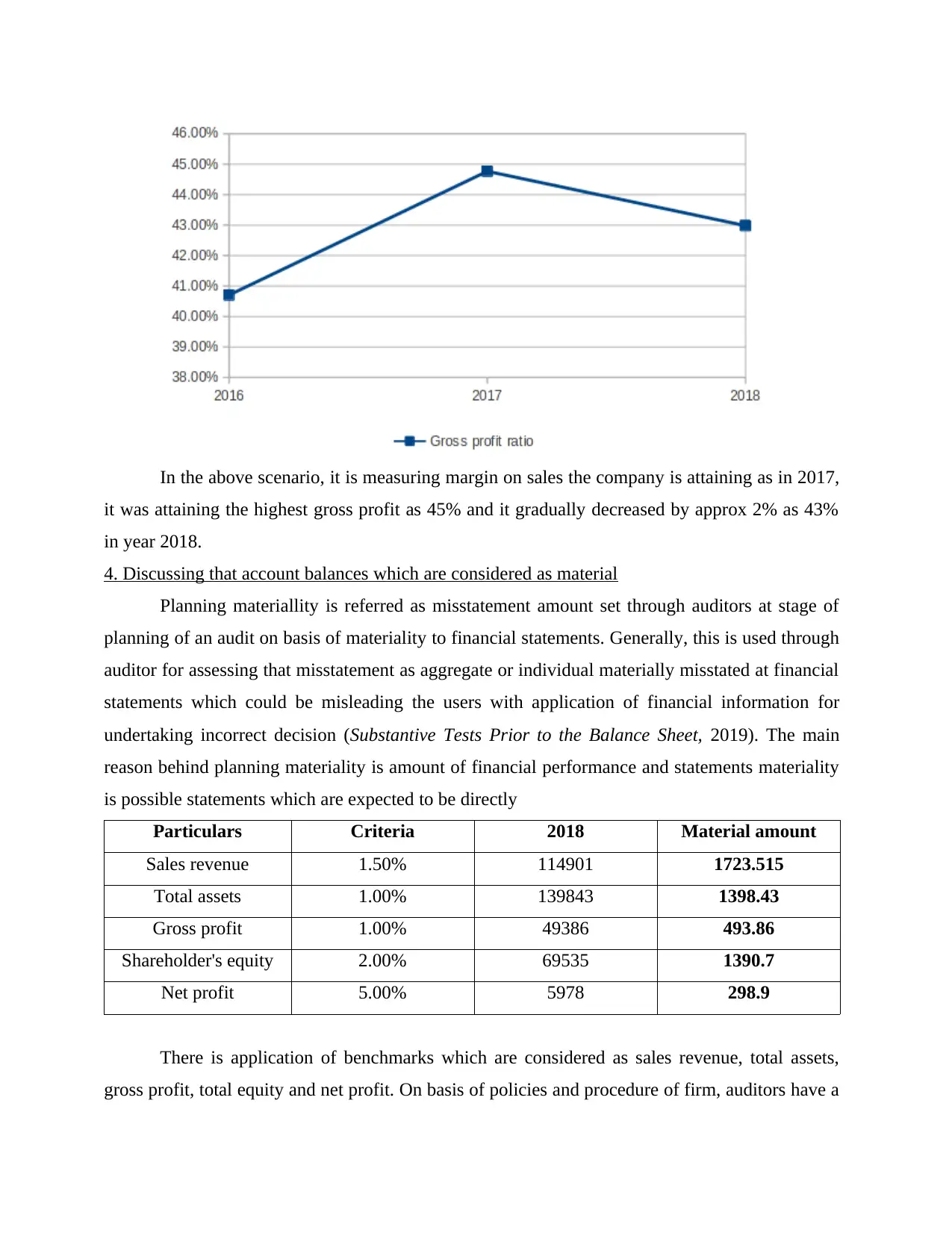

Profitability ratio 2016 2017 2018

Gross profit 48455 44858 49386

Net sales 119039 100204 114901

Gross profit ratio 40.71% 44.77% 42.98%

warehousing and contribution of product with consideration of sales volume. It is clearly viewed

that in year 2017, it was having high inventory for approx 200 days but in 2018, it improved its

financial position by reducing days of inventory as 168 days.

Profitability ratio 2016 2017 2018

Gross profit 48455 44858 49386

Net sales 119039 100204 114901

Gross profit ratio 40.71% 44.77% 42.98%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the above scenario, it is measuring margin on sales the company is attaining as in 2017,

it was attaining the highest gross profit as 45% and it gradually decreased by approx 2% as 43%

in year 2018.

4. Discussing that account balances which are considered as material

Planning materiallity is referred as misstatement amount set through auditors at stage of

planning of an audit on basis of materiality to financial statements. Generally, this is used through

auditor for assessing that misstatement as aggregate or individual materially misstated at financial

statements which could be misleading the users with application of financial information for

undertaking incorrect decision (Substantive Tests Prior to the Balance Sheet, 2019). The main

reason behind planning materiality is amount of financial performance and statements materiality

is possible statements which are expected to be directly

Particulars Criteria 2018 Material amount

Sales revenue 1.50% 114901 1723.515

Total assets 1.00% 139843 1398.43

Gross profit 1.00% 49386 493.86

Shareholder's equity 2.00% 69535 1390.7

Net profit 5.00% 5978 298.9

There is application of benchmarks which are considered as sales revenue, total assets,

gross profit, total equity and net profit. On basis of policies and procedure of firm, auditors have a

it was attaining the highest gross profit as 45% and it gradually decreased by approx 2% as 43%

in year 2018.

4. Discussing that account balances which are considered as material

Planning materiallity is referred as misstatement amount set through auditors at stage of

planning of an audit on basis of materiality to financial statements. Generally, this is used through

auditor for assessing that misstatement as aggregate or individual materially misstated at financial

statements which could be misleading the users with application of financial information for

undertaking incorrect decision (Substantive Tests Prior to the Balance Sheet, 2019). The main

reason behind planning materiality is amount of financial performance and statements materiality

is possible statements which are expected to be directly

Particulars Criteria 2018 Material amount

Sales revenue 1.50% 114901 1723.515

Total assets 1.00% 139843 1398.43

Gross profit 1.00% 49386 493.86

Shareholder's equity 2.00% 69535 1390.7

Net profit 5.00% 5978 298.9

There is application of benchmarks which are considered as sales revenue, total assets,

gross profit, total equity and net profit. On basis of policies and procedure of firm, auditors have a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

good instinct which are going to impact decisions made through the users of financial statements.

It has been confirmed that materiality must be relate to financial statements being prepared for

particular financial reporting period. On basis of conservative approach and lower percentage of

material misstatements is tended to be implied with context to enterprises that are directly through

high risk industries and faces high risk of fraud which have high accounting risk which have staff

turnover very high and this operates in different locations. The net profit prior to volatile along

with different benchmarks like sales might be very appropriate to imply with 1.5%. With the

operating outcome of organizations are very worse that solvency or liquidity are of real concern

on basis of overall materiality on financial position (Brenninkmeijer and et.al, 2018). The

thresholds directly tend to applied on reported years with cumulative effect misstatements over

years and impact on trends of earnings is also very significant.

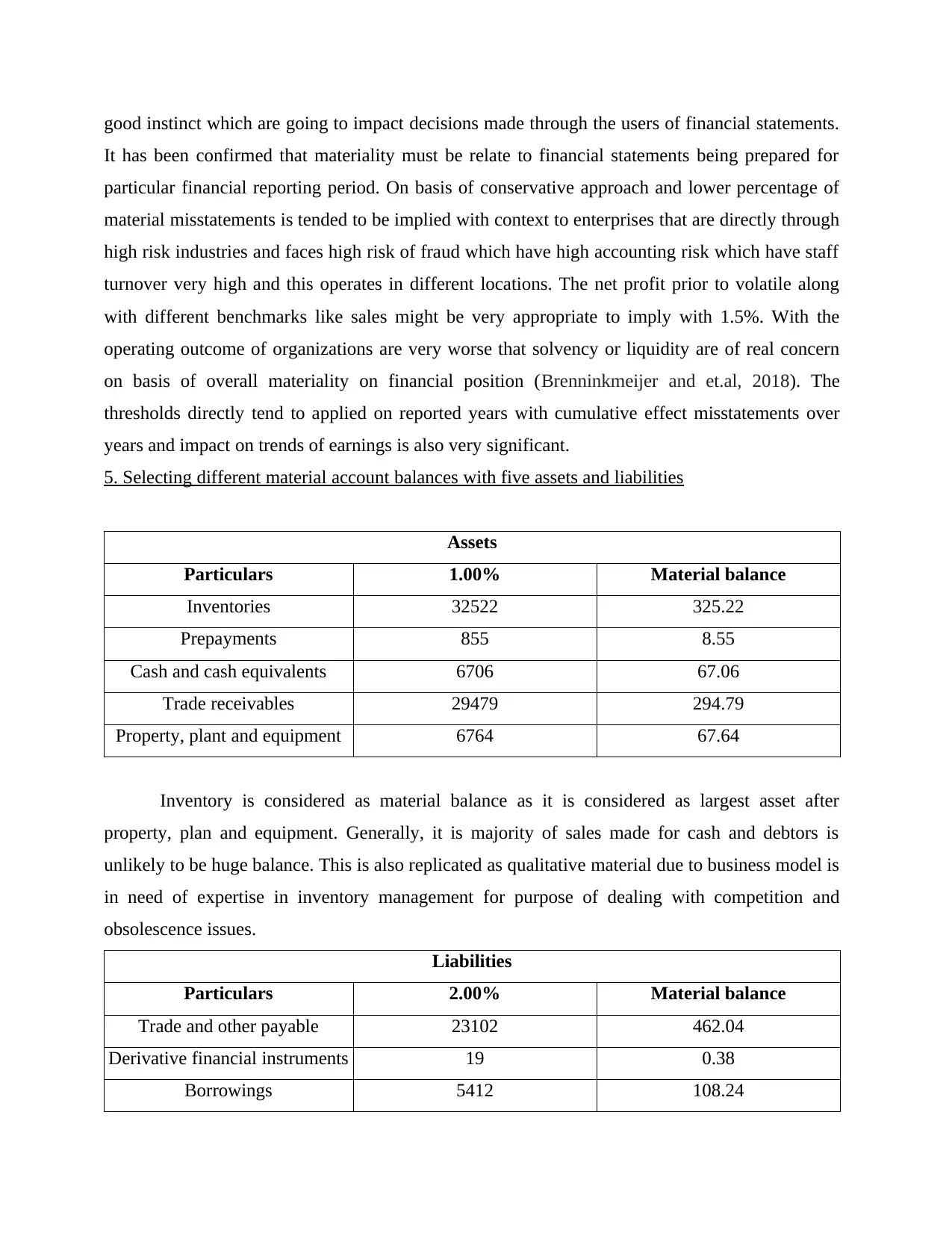

5. Selecting different material account balances with five assets and liabilities

Assets

Particulars 1.00% Material balance

Inventories 32522 325.22

Prepayments 855 8.55

Cash and cash equivalents 6706 67.06

Trade receivables 29479 294.79

Property, plant and equipment 6764 67.64

Inventory is considered as material balance as it is considered as largest asset after

property, plan and equipment. Generally, it is majority of sales made for cash and debtors is

unlikely to be huge balance. This is also replicated as qualitative material due to business model is

in need of expertise in inventory management for purpose of dealing with competition and

obsolescence issues.

Liabilities

Particulars 2.00% Material balance

Trade and other payable 23102 462.04

Derivative financial instruments 19 0.38

Borrowings 5412 108.24

It has been confirmed that materiality must be relate to financial statements being prepared for

particular financial reporting period. On basis of conservative approach and lower percentage of

material misstatements is tended to be implied with context to enterprises that are directly through

high risk industries and faces high risk of fraud which have high accounting risk which have staff

turnover very high and this operates in different locations. The net profit prior to volatile along

with different benchmarks like sales might be very appropriate to imply with 1.5%. With the

operating outcome of organizations are very worse that solvency or liquidity are of real concern

on basis of overall materiality on financial position (Brenninkmeijer and et.al, 2018). The

thresholds directly tend to applied on reported years with cumulative effect misstatements over

years and impact on trends of earnings is also very significant.

5. Selecting different material account balances with five assets and liabilities

Assets

Particulars 1.00% Material balance

Inventories 32522 325.22

Prepayments 855 8.55

Cash and cash equivalents 6706 67.06

Trade receivables 29479 294.79

Property, plant and equipment 6764 67.64

Inventory is considered as material balance as it is considered as largest asset after

property, plan and equipment. Generally, it is majority of sales made for cash and debtors is

unlikely to be huge balance. This is also replicated as qualitative material due to business model is

in need of expertise in inventory management for purpose of dealing with competition and

obsolescence issues.

Liabilities

Particulars 2.00% Material balance

Trade and other payable 23102 462.04

Derivative financial instruments 19 0.38

Borrowings 5412 108.24

Current tax liability 1027 20.54

Short term provisions 5310 106.2

6. Listing relevant financial report assertions of material account with reason

The transactions comprise inventories, prepayments, cash and cash equivalent, trade

receivables, property, plant and equipment as of account balances. Simulatensoulsy, in form of

liability as trade payable, derivative financial instrument, borrowings, current tac liability along

with short term provisions considered in statement of financial position at ending. There is

presence of association among them because test has been performed by auditor with occurrence

of sales as it will also offer some assurance related to existence of receivables. The auditor might

perform different other tests laid emphasis on assurance related to existence. The listed assertions

are stated as below:

The assertions related to classes of events and transactions on basis of disclosure for

duration under audit is about:

Occurrence: The events and transactions that must be traced and all disclosures which

must be considered in financial statements.

Accuracy: The amount and other data on basis of traced transactions and events should be

traced properly and related disclosures should be described and measured appropriately. In

simple terms, amounts of assets, liabilities along with valued equity interests, disclosed

and traced is very proper (Alles and et.al., 2018). The allocation is replicated to different

matters like inclusion of overhead amount for valuing inventory. It could be checked

through vouching cost of assets for buying invoices and checking rate and calculation of

depreciation.

Existence: It signifies that assets and liabilities exists on actual basis and with absence of

overstatement as for instance it comprises trade receivable and inventory in Legend

Corporations and is closely linked to occurrence transactions. It is all about physical

verification of its non current assets such as property, plant and equipment and circulation

of receivables and payables.

Rights and obligations: It signifies that entity has presence of legal title along with control

right to particular asset with presence of obligation for repaying liability. It is related to

Short term provisions 5310 106.2

6. Listing relevant financial report assertions of material account with reason

The transactions comprise inventories, prepayments, cash and cash equivalent, trade

receivables, property, plant and equipment as of account balances. Simulatensoulsy, in form of

liability as trade payable, derivative financial instrument, borrowings, current tac liability along

with short term provisions considered in statement of financial position at ending. There is

presence of association among them because test has been performed by auditor with occurrence

of sales as it will also offer some assurance related to existence of receivables. The auditor might

perform different other tests laid emphasis on assurance related to existence. The listed assertions

are stated as below:

The assertions related to classes of events and transactions on basis of disclosure for

duration under audit is about:

Occurrence: The events and transactions that must be traced and all disclosures which

must be considered in financial statements.

Accuracy: The amount and other data on basis of traced transactions and events should be

traced properly and related disclosures should be described and measured appropriately. In

simple terms, amounts of assets, liabilities along with valued equity interests, disclosed

and traced is very proper (Alles and et.al., 2018). The allocation is replicated to different

matters like inclusion of overhead amount for valuing inventory. It could be checked

through vouching cost of assets for buying invoices and checking rate and calculation of

depreciation.

Existence: It signifies that assets and liabilities exists on actual basis and with absence of

overstatement as for instance it comprises trade receivable and inventory in Legend

Corporations and is closely linked to occurrence transactions. It is all about physical

verification of its non current assets such as property, plant and equipment and circulation

of receivables and payables.

Rights and obligations: It signifies that entity has presence of legal title along with control

right to particular asset with presence of obligation for repaying liability. It is related to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

property as title or deeds could be reviewed as current assets are agreed to buy invoices

which is initially used for confirming cost. The long term liabilities like borrowing could

be agreed for particular agreement of debt.

Completeness: there is absence of omissions along with assets and liabilities which must

be traced and disclosed. In simple words, there is absence of understatement of liabilities

or assets. Further, review of expenditure and review account could help in determining

items which have been capitalised and eliminated through non-current assets. Moreover,

reconciliation of payables ledger balances to statement of supplier is designed at beginning

for confirming completeness and it also provides assurance related to existence.

Classification: It signifies that liabilities, assets and equity interests are traced in

appropriate accounts (Tracking materiality, 2018). The relevant test is with context of

transactions of checking postings of purchase invoice with proper accounts in general

ledger would be relevant.

Presentation: it signifies that disclosure and descriptions of liabilities and assets are

relevant and easy for understanding perspective. The above points are related to

disaggregation and aggregation of transaction with application of assets, liabilities and

equity interests. However, auditors often imply disclosures checklists for ensuring that

financial statement presentation compiles with specific legislation and accounting

standards. Usually, it will recoup above items as transactions, assets, liabilities and equity

interests and would comprise foe confirming about disclosure on basis of non current

assets as property, plant and equipments.

7. Designing comprehensive set of audit work steps for every material account balances

The substantive analytical procedure is on basis of expectations that relationship within

data exist and continues without known conditions on contrary. The presence of relationships

offers evidence of audit as accuracy, completeness and occurrence of numerous transactions. The

main reason behind the nature, substantive analytical procedure could give evidence of numerous

assertions, determining issues related to audit and might be not apparent for detailed work and

direct the attentions of auditor to areas in need of more investigation. Moreover, auditor might

determine risks along with deficiencies in internal control which were not identified in past and

even might cause auditor for re evaluating the planned audit approach. The auditor is in need for

obtaining high assurance through other substantive testing as compared to planned originally.

which is initially used for confirming cost. The long term liabilities like borrowing could

be agreed for particular agreement of debt.

Completeness: there is absence of omissions along with assets and liabilities which must

be traced and disclosed. In simple words, there is absence of understatement of liabilities

or assets. Further, review of expenditure and review account could help in determining

items which have been capitalised and eliminated through non-current assets. Moreover,

reconciliation of payables ledger balances to statement of supplier is designed at beginning

for confirming completeness and it also provides assurance related to existence.

Classification: It signifies that liabilities, assets and equity interests are traced in

appropriate accounts (Tracking materiality, 2018). The relevant test is with context of

transactions of checking postings of purchase invoice with proper accounts in general

ledger would be relevant.

Presentation: it signifies that disclosure and descriptions of liabilities and assets are

relevant and easy for understanding perspective. The above points are related to

disaggregation and aggregation of transaction with application of assets, liabilities and

equity interests. However, auditors often imply disclosures checklists for ensuring that

financial statement presentation compiles with specific legislation and accounting

standards. Usually, it will recoup above items as transactions, assets, liabilities and equity

interests and would comprise foe confirming about disclosure on basis of non current

assets as property, plant and equipments.

7. Designing comprehensive set of audit work steps for every material account balances

The substantive analytical procedure is on basis of expectations that relationship within

data exist and continues without known conditions on contrary. The presence of relationships

offers evidence of audit as accuracy, completeness and occurrence of numerous transactions. The

main reason behind the nature, substantive analytical procedure could give evidence of numerous

assertions, determining issues related to audit and might be not apparent for detailed work and

direct the attentions of auditor to areas in need of more investigation. Moreover, auditor might

determine risks along with deficiencies in internal control which were not identified in past and

even might cause auditor for re evaluating the planned audit approach. The auditor is in need for

obtaining high assurance through other substantive testing as compared to planned originally.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

On basis of deriving the most advantage through substantive analytical procedure so in

this context, there is requirement of adopting substantive analytical procedures and often affected

the extent and nature of testing in detail aspect. However, substantive analytical procedure may

direct attention to areas of raised risk along with assurance gained through effective substantive

analytical procedure would decrease amount of assurance required through other tests. In this

context, there are majorly four elements which consist of different steps which are inherent in

procedure to imply substantive analytical procedures for every material account balances such as:

Developing independent expectation

Defining significant difference or threshold

Computing difference

Investigating significant differences and drawing conclusions

Developing independent expectation: The development of a properly precise, objective

expectations is very significant step in effective application of substantive analytical procedure.

The expectation is a forecast of recorded amount or particular ratio. The forecast could be specific

number, percentage a direction or approximate and depends on desired precision. The auditor

must have presence of independent expectation of application of substantive analytical procedure

and expectations must be developed through determining plausible relationships which are

reasonable expected to exist on basis of knowledge of business, trends of industry along with

other accounts.

Defining significant difference or threshold: On basis of performing and designing

substantive analytical procedures the auditor must consider amount of variation through

expectation that could be directly accepted with absence of further investigation. The maximum

acceptable variation is commonly referred as threshold. It might be elaborated as numerical values

or percentages of items is being tested (Byrnes and et.al., 2018). Moreover, establishment of

proper threshold is particularly censorious to effective application of substantive analytical

procedures. The prevention of bias in judgement, auditor must identifies threshold for planning

substantive analytical procedure prior to step 3, in which variation among expectation and traced

amount are directly computed.

The threshold is referred as amount of potential misstatement and must not exceed

planning materiality and could be sufficiently small and capable the auditor to determine

this context, there is requirement of adopting substantive analytical procedures and often affected

the extent and nature of testing in detail aspect. However, substantive analytical procedure may

direct attention to areas of raised risk along with assurance gained through effective substantive

analytical procedure would decrease amount of assurance required through other tests. In this

context, there are majorly four elements which consist of different steps which are inherent in

procedure to imply substantive analytical procedures for every material account balances such as:

Developing independent expectation

Defining significant difference or threshold

Computing difference

Investigating significant differences and drawing conclusions

Developing independent expectation: The development of a properly precise, objective

expectations is very significant step in effective application of substantive analytical procedure.

The expectation is a forecast of recorded amount or particular ratio. The forecast could be specific

number, percentage a direction or approximate and depends on desired precision. The auditor

must have presence of independent expectation of application of substantive analytical procedure

and expectations must be developed through determining plausible relationships which are

reasonable expected to exist on basis of knowledge of business, trends of industry along with

other accounts.

Defining significant difference or threshold: On basis of performing and designing

substantive analytical procedures the auditor must consider amount of variation through

expectation that could be directly accepted with absence of further investigation. The maximum

acceptable variation is commonly referred as threshold. It might be elaborated as numerical values

or percentages of items is being tested (Byrnes and et.al., 2018). Moreover, establishment of

proper threshold is particularly censorious to effective application of substantive analytical

procedures. The prevention of bias in judgement, auditor must identifies threshold for planning

substantive analytical procedure prior to step 3, in which variation among expectation and traced

amount are directly computed.

The threshold is referred as amount of potential misstatement and must not exceed

planning materiality and could be sufficiently small and capable the auditor to determine

misstatements which could be material either individually. The aggregated misstaments in other

disaggregated portions of account balance or in other account balances.

Computing difference: This is the third step is comparison of the expected value with the

traced amounts and determination of significant variations. It must be simply replicated as

mechanical calculation. This is very significant for noting computation of variation must be done

after consideration of threshold and expectation. With application of substantive analytical

procedures it is not appropriate for extracting differences through prior period balances and let

outcome impacts expected difference and threshold accepted.

Investigating significant differences and drawing conclusions: Similarly, fourth step is

related to investigation of variations and forming conclusions. The variations indicate a raised

likelihood of misstatements, high degree of precision, greater the likelihood that difference is a

misstatement. Furthermore, explanation shall be sought of full amount of variation not just

exceeding part of threshold part. There is probability that unexplained variations must reflect risk

of material misstatement. The auditor must enable for considering that differences caused through

past factors overlooked for developing expectation in 1st phase like unexpected alterations in

business and alterations in accounting treatments.

In case differences is caused through previously overlooked factors, it is very significant

for verifying the new data to reflect impact would have on original expectations as data had been

considered at beginning place. The understanding of auditing or accounting ramifications of the

innovative data.

8. Including sampling plan with use of every material account balance

Audit sampling is referred as application of procedure of audit to less than 100% of items

within account balance of class of transactions with objective to evaluate some features of

balancing or class. The auditor must be aware about account balances and transactions that might

be likely which consist of misstatements. There is consideration of planning procedures which

comprises audit sampling, The auditor will have absence of special knowledge in planning

procedures which comprises audit sampling. However, auditor will have absence of special

knowledge related to account balances and transaction in judgement would be testes with

objective of fulfilling audit objectives. In the present scenario, there are different methods which

are considered for audit sampling for material misstatements are stated below:

random selection

disaggregated portions of account balance or in other account balances.

Computing difference: This is the third step is comparison of the expected value with the

traced amounts and determination of significant variations. It must be simply replicated as

mechanical calculation. This is very significant for noting computation of variation must be done

after consideration of threshold and expectation. With application of substantive analytical

procedures it is not appropriate for extracting differences through prior period balances and let

outcome impacts expected difference and threshold accepted.

Investigating significant differences and drawing conclusions: Similarly, fourth step is

related to investigation of variations and forming conclusions. The variations indicate a raised

likelihood of misstatements, high degree of precision, greater the likelihood that difference is a

misstatement. Furthermore, explanation shall be sought of full amount of variation not just

exceeding part of threshold part. There is probability that unexplained variations must reflect risk

of material misstatement. The auditor must enable for considering that differences caused through

past factors overlooked for developing expectation in 1st phase like unexpected alterations in

business and alterations in accounting treatments.

In case differences is caused through previously overlooked factors, it is very significant

for verifying the new data to reflect impact would have on original expectations as data had been

considered at beginning place. The understanding of auditing or accounting ramifications of the

innovative data.

8. Including sampling plan with use of every material account balance

Audit sampling is referred as application of procedure of audit to less than 100% of items

within account balance of class of transactions with objective to evaluate some features of

balancing or class. The auditor must be aware about account balances and transactions that might

be likely which consist of misstatements. There is consideration of planning procedures which

comprises audit sampling, The auditor will have absence of special knowledge in planning

procedures which comprises audit sampling. However, auditor will have absence of special

knowledge related to account balances and transaction in judgement would be testes with

objective of fulfilling audit objectives. In the present scenario, there are different methods which

are considered for audit sampling for material misstatements are stated below:

random selection

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.