Holmes Institute HA3032: Developing Audit Program for Public Company

VerifiedAdded on 2023/02/01

|21

|1804

|61

Report

AI Summary

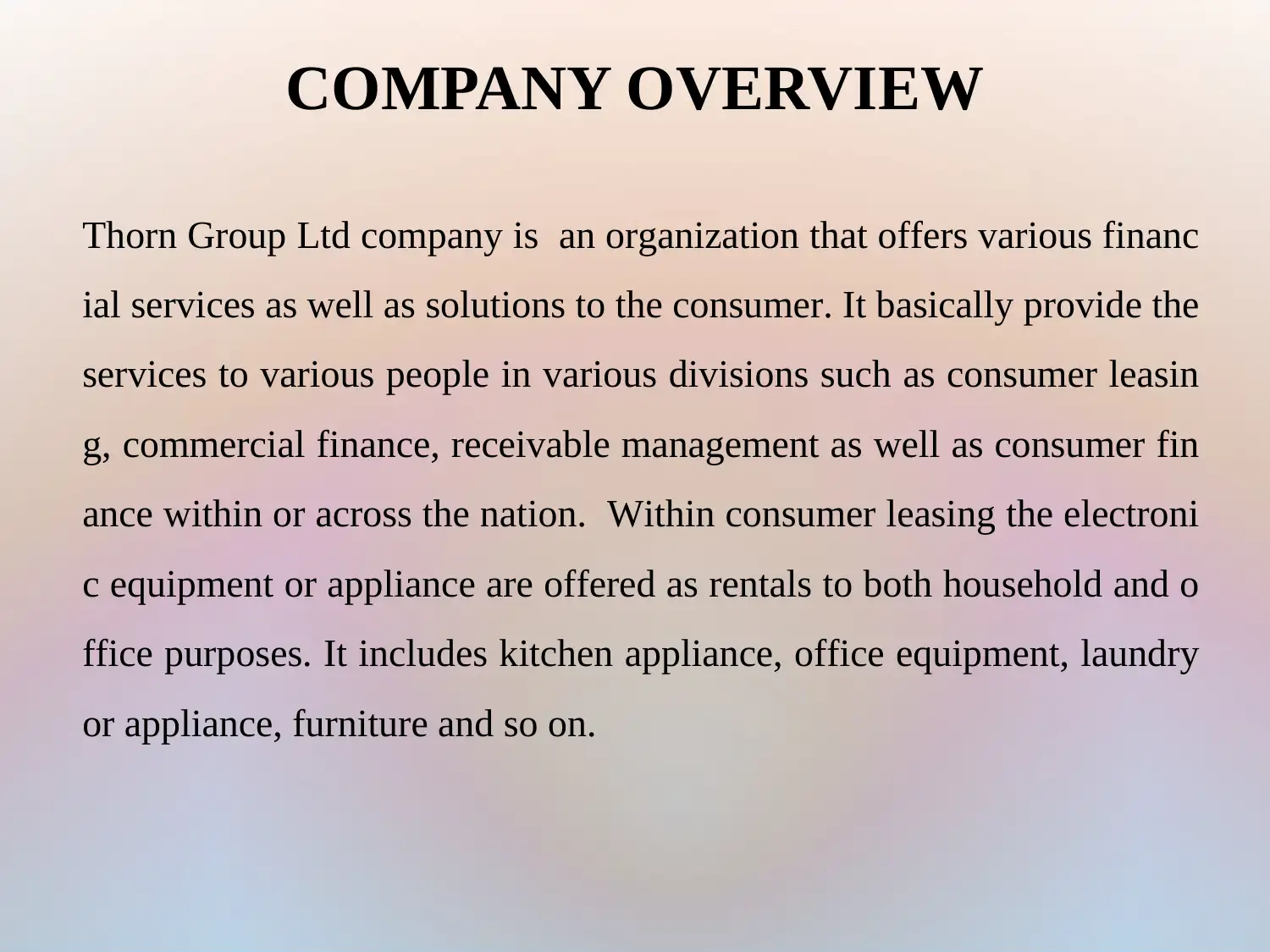

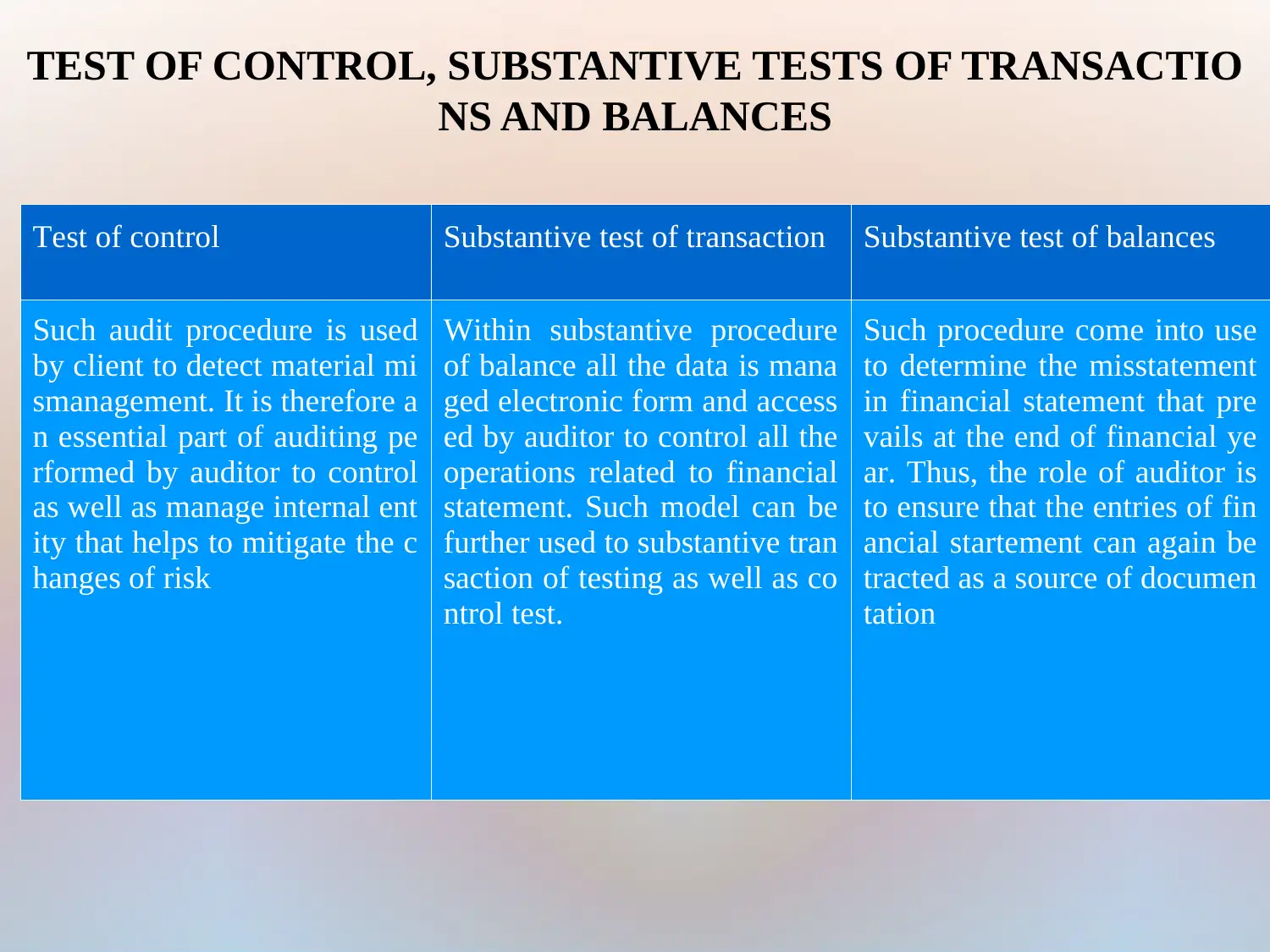

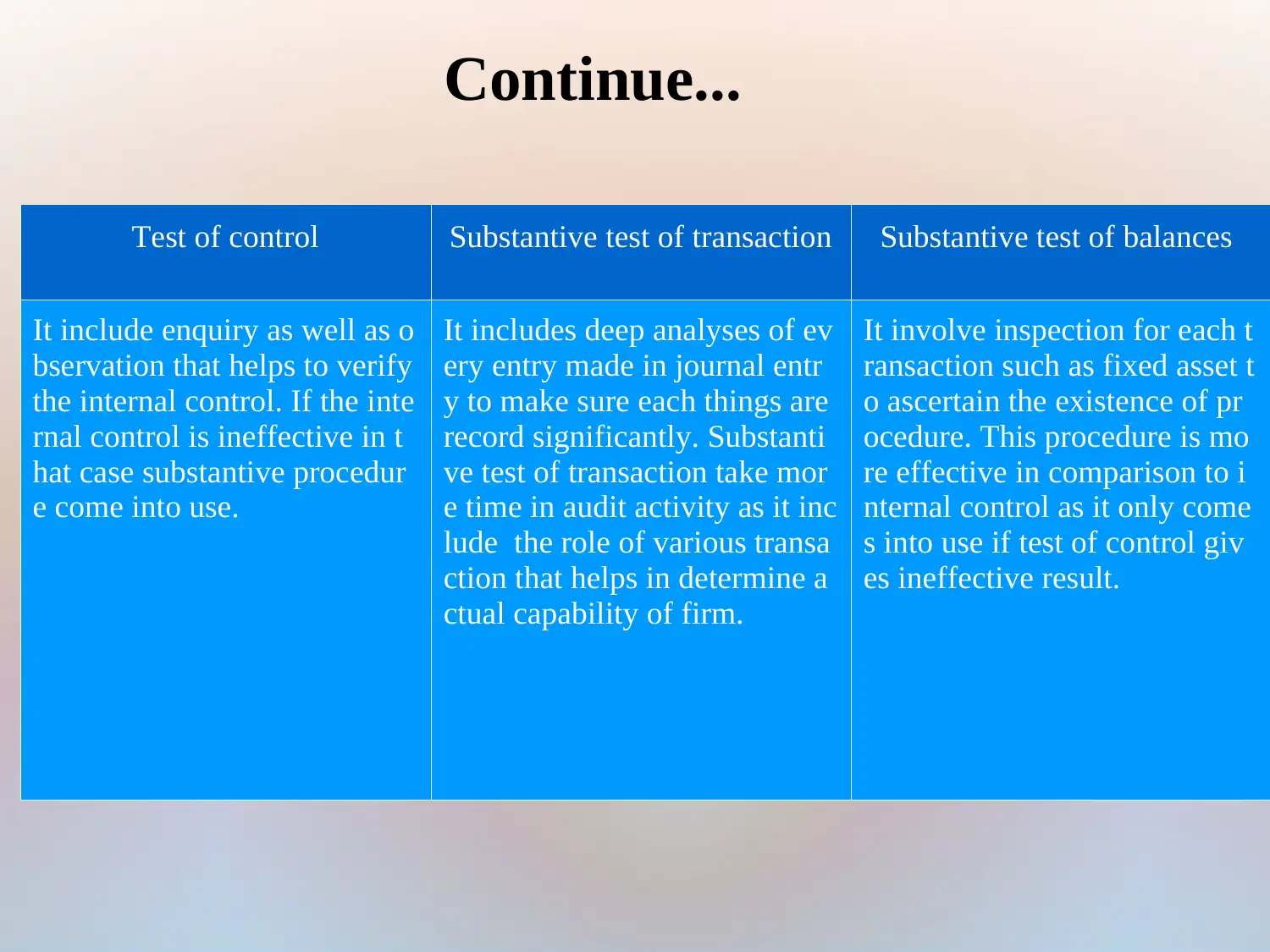

This report presents a comprehensive audit program developed for Thorn Group Ltd., an ASX-listed company. The report begins with an executive summary and an introduction to audit programs, emphasizing their role in validating compliance and risk management. It provides a company overview, followed by an analysis of tests of control, substantive tests of transactions and balances, and key business risks. The report details substantive audit procedures, including the application of an Audit Risk Model, and explores the relationship between assertions and account balances. It identifies material account balances like inventory and account receivable. The report also outlines an audit program for Thorn Group Limited, including a sampling plan. The conclusion summarizes the importance of auditors in business management and references used in the report.

1 out of 21

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.