Audit Program Development for Bega Cheese Limited Project

VerifiedAdded on 2023/01/07

|22

|4227

|48

Project

AI Summary

This project report presents a comprehensive audit program designed for Bega Cheese Limited, a publicly listed Australian company. It begins with an executive summary and an introduction outlining the report's objectives. The main body includes an analysis of the industry's nature and key risks faced by Bega Cheese, followed by a detailed examination of the company's financial performance over three years using ratio analysis. The report identifies and discusses ten material account balances, their relevant financial report assertions, and the preparation of audit work, including sampling plans for each material account. The analysis considers inherent and control risks, and incorporates the audit risk model to assess potential misstatements. The report concludes with a summary of findings and a list of references, providing a practical guide to audit program development for similar companies. This report is available on Desklib, offering valuable insights for students and professionals in finance and accounting.

Developing an Audit

Program for a

selected publically

listed Company

Program for a

selected publically

listed Company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

A project report has been prepared taking into account one of Australia's publicly

traded firms. It reflects on how an organization is planning for the audit program. It

requires recognition of the test of controls and the implementation of suitable test on

separate transactions and account balances. It indicates that the auditor will adapt the

practical protocols to the particular risks evaluated. It also lists multiple value of assets

and liabilities of balance sheet and refers to their related assertions. The key aim of this

project is to figure out how to be select the most reliable and successful mix of audit

rules to assure that the audit goal is attained. Finally, a sample plan for each of the

material accounts to be checked has also been incorporated. The above descriptions

were expressed in a table format so as to allow for easy interpretation and contrast.

A project report has been prepared taking into account one of Australia's publicly

traded firms. It reflects on how an organization is planning for the audit program. It

requires recognition of the test of controls and the implementation of suitable test on

separate transactions and account balances. It indicates that the auditor will adapt the

practical protocols to the particular risks evaluated. It also lists multiple value of assets

and liabilities of balance sheet and refers to their related assertions. The key aim of this

project is to figure out how to be select the most reliable and successful mix of audit

rules to assure that the audit goal is attained. Finally, a sample plan for each of the

material accounts to be checked has also been incorporated. The above descriptions

were expressed in a table format so as to allow for easy interpretation and contrast.

Contents

EXECUTIVE SUMMARY.........................................................................................................................2

INTRODUCTION......................................................................................................................................4

MAIN BODY..............................................................................................................................................4

1. Analysis of nature of industry and key risks..............................................................................4

2. Analysis of financial performance of above company for three years...................................8

3. Discussion of account balances which are consider Material...............................................13

4. Ten different material account balances..................................................................................14

5. Relevant financial report assertions.........................................................................................14

6. Preparation of set of audit work................................................................................................17

7. Sampling plan for each material account.................................................................................19

CONCLUSION........................................................................................................................................20

REFERENCES........................................................................................................................................21

EXECUTIVE SUMMARY.........................................................................................................................2

INTRODUCTION......................................................................................................................................4

MAIN BODY..............................................................................................................................................4

1. Analysis of nature of industry and key risks..............................................................................4

2. Analysis of financial performance of above company for three years...................................8

3. Discussion of account balances which are consider Material...............................................13

4. Ten different material account balances..................................................................................14

5. Relevant financial report assertions.........................................................................................14

6. Preparation of set of audit work................................................................................................17

7. Sampling plan for each material account.................................................................................19

CONCLUSION........................................................................................................................................20

REFERENCES........................................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

It is important for business entities to apply a suitable and effective audit program

so that financial statements can be prepared in more transparent and accurate manner

(Eulerich, Georgi and Schmidt, 2019). In the aspect of project report an audit program

has been prepared for a publically listed company registered in Australian stock

exchange. The name of company is Bega Cheese limited that is involved in sector of

consumer staples. This company was founded in year 1899, headquartered in Bega,

Australia. This company is Australia’s diversified food company which has its

manufacturing sites at different locations like new south wales, Queensland and

Victoria. The company was formed as a public limited company in year 2011 ( About

Bega cheese limited, 2020). The project report contains information about key risks

faced by chosen company, financial performance and an appropriate audit program in

accordance of ten selected material accounts.

MAIN BODY

1. Analysis of nature of industry and key risks.

Bega cheese limited is an Australian based company which is listed in Australian

stock exchange. The company is known for its cheese as they provide quality

cheese products since 40 years and they dominate the market. Company sells

around 1 million packs of cheese on a daily basis. In year 2017, company

increased their product portfolio by including some other products such as

vegemite, peanut butter, ZoOSh. The company’s products are chosen on priority

in different supermarkets as they produce organic cheese items (About Bega

cheese limited, 2020). The rationale behind maintaining higher quality in food

products is that they buy raw material for production of cheese products directly

from farmers and different farms. This company also follows different types of

regulations such as they try to make limited noise so that neighborhoods cannot

be disturbed along with assurance of proper management of wastage of water is

It is important for business entities to apply a suitable and effective audit program

so that financial statements can be prepared in more transparent and accurate manner

(Eulerich, Georgi and Schmidt, 2019). In the aspect of project report an audit program

has been prepared for a publically listed company registered in Australian stock

exchange. The name of company is Bega Cheese limited that is involved in sector of

consumer staples. This company was founded in year 1899, headquartered in Bega,

Australia. This company is Australia’s diversified food company which has its

manufacturing sites at different locations like new south wales, Queensland and

Victoria. The company was formed as a public limited company in year 2011 ( About

Bega cheese limited, 2020). The project report contains information about key risks

faced by chosen company, financial performance and an appropriate audit program in

accordance of ten selected material accounts.

MAIN BODY

1. Analysis of nature of industry and key risks.

Bega cheese limited is an Australian based company which is listed in Australian

stock exchange. The company is known for its cheese as they provide quality

cheese products since 40 years and they dominate the market. Company sells

around 1 million packs of cheese on a daily basis. In year 2017, company

increased their product portfolio by including some other products such as

vegemite, peanut butter, ZoOSh. The company’s products are chosen on priority

in different supermarkets as they produce organic cheese items (About Bega

cheese limited, 2020). The rationale behind maintaining higher quality in food

products is that they buy raw material for production of cheese products directly

from farmers and different farms. This company also follows different types of

regulations such as they try to make limited noise so that neighborhoods cannot

be disturbed along with assurance of proper management of wastage of water is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

also considered. So as per this discussion, it can be stated that company is

based in the sector of food manufacturing and they have monopoly in various

cheese products in Australia. Though, there are some competitors too but no one

is able to maintain similar quality in products as Bega cheese limited.

Main business risks- Each business faces number of risks in which some risks

can be controlled and some can’t be. The risks which are under control of a

business, arise due to internal inefficiency. On the other hands, those risks which

are not in control of a company, occur due to any external environment factor.

Underneath some types of risks are mentioned below in such manner:

Competitive risk- It can be characterized as form of risk which occurs in

businesses due to number of competitive companies are available in

market (Zhaokai and Moffitt, 2019). This types of risk cannot be controlled

by business entities. For instance, the above Bega cheese limited has

number of other competitors such as Nu farm, Sun Rice, Costa group etc.

These all companies may trouble to revenues and existence of above

mentioned company by offering number of substitute products.

Credit risk- This is defined as a type of risk that occurs in companies due

to inefficiency of debtors in order to pay debt amount. Eventually, big

companies offer credit facility to different clients and if these clients fail to

make payment which they owed than company may face huge loss. Such

as Bega cheese limited can face this risk if their customers do not make

payment for the goods which are sold on credit.

Liquidity risk- It can be understood as a form of risk that occurs because

of lack of financial resources in order to make payment of short term

debts. In the context of above Bega cheese limited, they may face this risk

if they fail to make projection of financial resources.

Risk of material misstatement- This is known as a type of risk that can occur in

business entities because of intentionally or without intentionally by accountants

in financial statements (Al-Bawab, 2019). In regards to a company, there are

based in the sector of food manufacturing and they have monopoly in various

cheese products in Australia. Though, there are some competitors too but no one

is able to maintain similar quality in products as Bega cheese limited.

Main business risks- Each business faces number of risks in which some risks

can be controlled and some can’t be. The risks which are under control of a

business, arise due to internal inefficiency. On the other hands, those risks which

are not in control of a company, occur due to any external environment factor.

Underneath some types of risks are mentioned below in such manner:

Competitive risk- It can be characterized as form of risk which occurs in

businesses due to number of competitive companies are available in

market (Zhaokai and Moffitt, 2019). This types of risk cannot be controlled

by business entities. For instance, the above Bega cheese limited has

number of other competitors such as Nu farm, Sun Rice, Costa group etc.

These all companies may trouble to revenues and existence of above

mentioned company by offering number of substitute products.

Credit risk- This is defined as a type of risk that occurs in companies due

to inefficiency of debtors in order to pay debt amount. Eventually, big

companies offer credit facility to different clients and if these clients fail to

make payment which they owed than company may face huge loss. Such

as Bega cheese limited can face this risk if their customers do not make

payment for the goods which are sold on credit.

Liquidity risk- It can be understood as a form of risk that occurs because

of lack of financial resources in order to make payment of short term

debts. In the context of above Bega cheese limited, they may face this risk

if they fail to make projection of financial resources.

Risk of material misstatement- This is known as a type of risk that can occur in

business entities because of intentionally or without intentionally by accountants

in financial statements (Al-Bawab, 2019). In regards to a company, there are

different kinds of accounts in that risk of material misstatement may occur. In

Bega cheese limited, this type of error may happen in annual report including

current, non-current assets and liabilities.

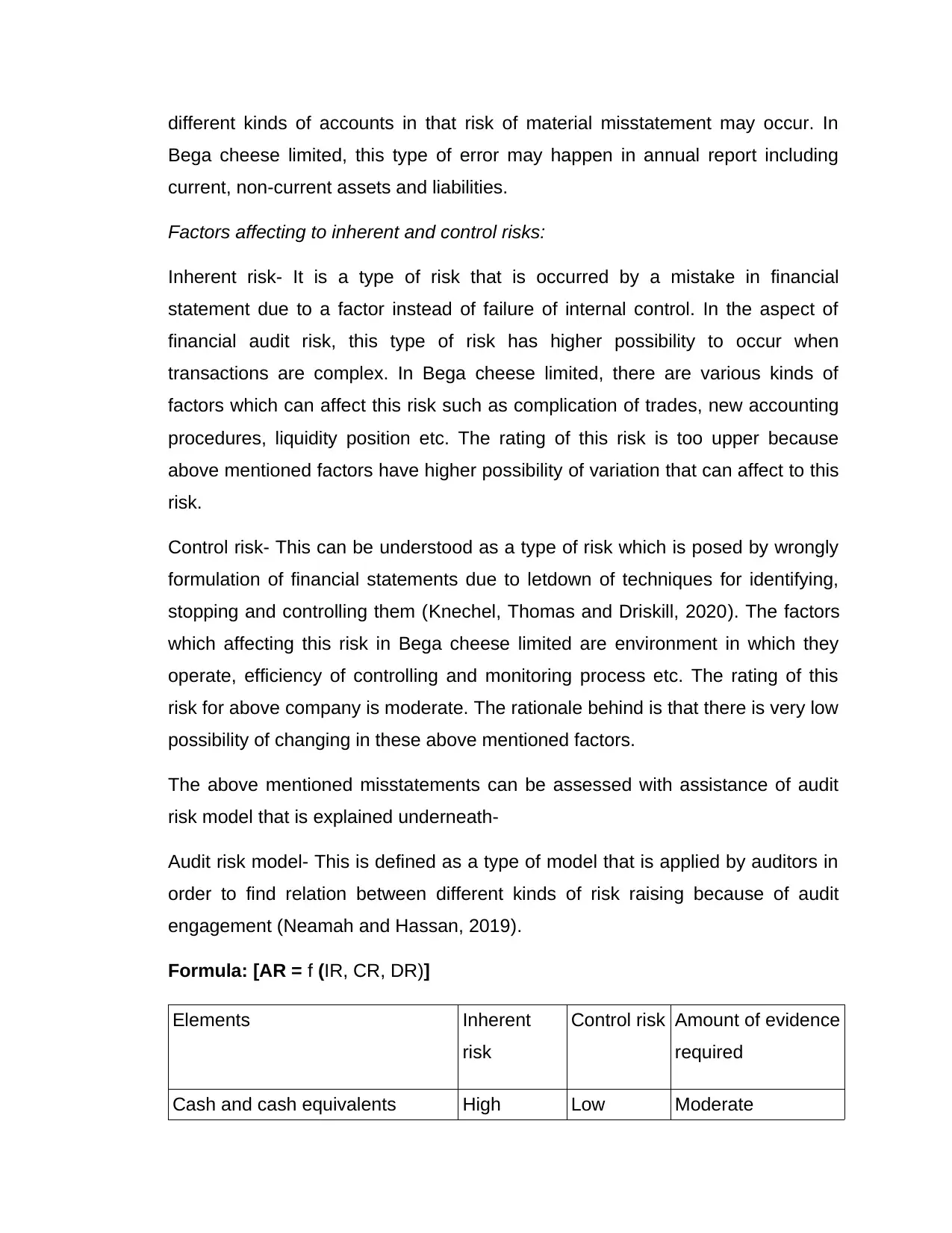

Factors affecting to inherent and control risks:

Inherent risk- It is a type of risk that is occurred by a mistake in financial

statement due to a factor instead of failure of internal control. In the aspect of

financial audit risk, this type of risk has higher possibility to occur when

transactions are complex. In Bega cheese limited, there are various kinds of

factors which can affect this risk such as complication of trades, new accounting

procedures, liquidity position etc. The rating of this risk is too upper because

above mentioned factors have higher possibility of variation that can affect to this

risk.

Control risk- This can be understood as a type of risk which is posed by wrongly

formulation of financial statements due to letdown of techniques for identifying,

stopping and controlling them (Knechel, Thomas and Driskill, 2020). The factors

which affecting this risk in Bega cheese limited are environment in which they

operate, efficiency of controlling and monitoring process etc. The rating of this

risk for above company is moderate. The rationale behind is that there is very low

possibility of changing in these above mentioned factors.

The above mentioned misstatements can be assessed with assistance of audit

risk model that is explained underneath-

Audit risk model- This is defined as a type of model that is applied by auditors in

order to find relation between different kinds of risk raising because of audit

engagement (Neamah and Hassan, 2019).

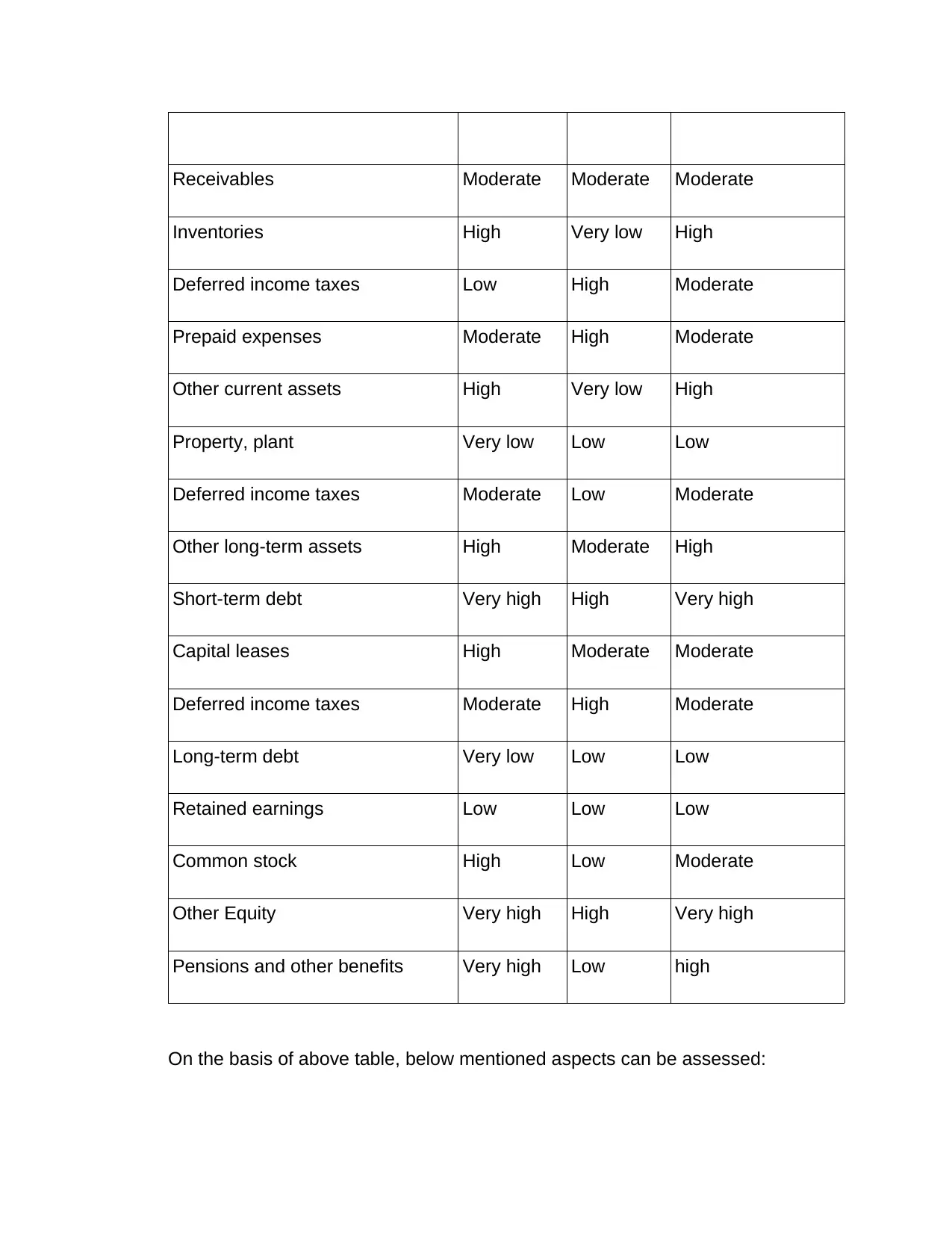

Formula: [AR = f (IR, CR, DR)]

Elements Inherent

risk

Control risk Amount of evidence

required

Cash and cash equivalents High Low Moderate

Bega cheese limited, this type of error may happen in annual report including

current, non-current assets and liabilities.

Factors affecting to inherent and control risks:

Inherent risk- It is a type of risk that is occurred by a mistake in financial

statement due to a factor instead of failure of internal control. In the aspect of

financial audit risk, this type of risk has higher possibility to occur when

transactions are complex. In Bega cheese limited, there are various kinds of

factors which can affect this risk such as complication of trades, new accounting

procedures, liquidity position etc. The rating of this risk is too upper because

above mentioned factors have higher possibility of variation that can affect to this

risk.

Control risk- This can be understood as a type of risk which is posed by wrongly

formulation of financial statements due to letdown of techniques for identifying,

stopping and controlling them (Knechel, Thomas and Driskill, 2020). The factors

which affecting this risk in Bega cheese limited are environment in which they

operate, efficiency of controlling and monitoring process etc. The rating of this

risk for above company is moderate. The rationale behind is that there is very low

possibility of changing in these above mentioned factors.

The above mentioned misstatements can be assessed with assistance of audit

risk model that is explained underneath-

Audit risk model- This is defined as a type of model that is applied by auditors in

order to find relation between different kinds of risk raising because of audit

engagement (Neamah and Hassan, 2019).

Formula: [AR = f (IR, CR, DR)]

Elements Inherent

risk

Control risk Amount of evidence

required

Cash and cash equivalents High Low Moderate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Receivables Moderate Moderate Moderate

Inventories High Very low High

Deferred income taxes Low High Moderate

Prepaid expenses Moderate High Moderate

Other current assets High Very low High

Property, plant Very low Low Low

Deferred income taxes Moderate Low Moderate

Other long-term assets High Moderate High

Short-term debt Very high High Very high

Capital leases High Moderate Moderate

Deferred income taxes Moderate High Moderate

Long-term debt Very low Low Low

Retained earnings Low Low Low

Common stock High Low Moderate

Other Equity Very high High Very high

Pensions and other benefits Very high Low high

On the basis of above table, below mentioned aspects can be assessed:

Inventories High Very low High

Deferred income taxes Low High Moderate

Prepaid expenses Moderate High Moderate

Other current assets High Very low High

Property, plant Very low Low Low

Deferred income taxes Moderate Low Moderate

Other long-term assets High Moderate High

Short-term debt Very high High Very high

Capital leases High Moderate Moderate

Deferred income taxes Moderate High Moderate

Long-term debt Very low Low Low

Retained earnings Low Low Low

Common stock High Low Moderate

Other Equity Very high High Very high

Pensions and other benefits Very high Low high

On the basis of above table, below mentioned aspects can be assessed:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Detection risk -It can be described as the possibility of the auditor not finding the

material misstatement in the entity's financial reports. All these irregularities may

be made in Bega cheese Limited’s final accounts due to separate factors, such

as theft or error. In accordance of above table some detection risks are cash and

cash equivalents, receivables, stock, prepaid expenses, pension and other

benefits.

Audit risk- It may be defined as the danger that could arise due to the

inaccuracy of the financial reports and the auditor passes the argument that all

the reports are error-free (Dahanayake, 2020). To mitigate this category of risk,

accountants execute annual basis audit at Bega cheese limited. The above table

states that some of the risks involved with the audit are fixed assets, financial

liabilities, equities etc.

According to the high or lower ranking of inherent and control risk, the estimation

of identification and audit risk may be impaired and if there is a high chance of

them then it will influence auditors to find them and consider the claims wrong.

From the aforementioned table it can be evaluated that cash and cash

equivalents, trade and other receivables, stock, prepaid expenses, pension and

other benefits are the risk which need to be focused by above company.

2. Analysis of financial performance of above company for three years.

This is important for companies to assess their financial position so that effective

decisions can be carried out by managers. In order to analyze financial

performance, there are a range of techniques and ratio analysis is one of them

which is applied for Bega cheese limited in such manner:

Ratio analysis- It can be understood as a form of matrix which is used to

measure financial performance of companies in relation to different aspects

including profitability, investment etc. In the context of above company some key

ratios are calculated and interpreted below in such manner:

material misstatement in the entity's financial reports. All these irregularities may

be made in Bega cheese Limited’s final accounts due to separate factors, such

as theft or error. In accordance of above table some detection risks are cash and

cash equivalents, receivables, stock, prepaid expenses, pension and other

benefits.

Audit risk- It may be defined as the danger that could arise due to the

inaccuracy of the financial reports and the auditor passes the argument that all

the reports are error-free (Dahanayake, 2020). To mitigate this category of risk,

accountants execute annual basis audit at Bega cheese limited. The above table

states that some of the risks involved with the audit are fixed assets, financial

liabilities, equities etc.

According to the high or lower ranking of inherent and control risk, the estimation

of identification and audit risk may be impaired and if there is a high chance of

them then it will influence auditors to find them and consider the claims wrong.

From the aforementioned table it can be evaluated that cash and cash

equivalents, trade and other receivables, stock, prepaid expenses, pension and

other benefits are the risk which need to be focused by above company.

2. Analysis of financial performance of above company for three years.

This is important for companies to assess their financial position so that effective

decisions can be carried out by managers. In order to analyze financial

performance, there are a range of techniques and ratio analysis is one of them

which is applied for Bega cheese limited in such manner:

Ratio analysis- It can be understood as a form of matrix which is used to

measure financial performance of companies in relation to different aspects

including profitability, investment etc. In the context of above company some key

ratios are calculated and interpreted below in such manner:

Liquidity ratio- This ratio is measured in order to assess liquidity position of a

company so that it can be measured whether there are enough current assets or

not to pay short term debts (Dagilienė and Klovienė, 2019). It includes below

mentioned ratios such as:

Current ratio: Current assets / current liabilities

Data in $ million

except current

ratio

2017 2018 2019

Current assets 818 469 490

Current liabilities 267 278 315

Current ratio 3.06 times 1.69 times 1.55 times

2 0 1 7

2 0 1 8

2 0 1 9

0

0.5

1

1.5

2

2.5

3

3.5

Current rati o

Interpretation: On the basis of above diagram this can be find out that performance

of Bega cheese limited has been reduced year by year in terms of liquidity. As in

year 2017, current ratio was of 3.06 times which reduced by almost 50% and

became of 1.69 times for year 2018. As well as in next year, it became of 1.55 times.

This performance is showing that company failed to meet idea criteria of current ratio

company so that it can be measured whether there are enough current assets or

not to pay short term debts (Dagilienė and Klovienė, 2019). It includes below

mentioned ratios such as:

Current ratio: Current assets / current liabilities

Data in $ million

except current

ratio

2017 2018 2019

Current assets 818 469 490

Current liabilities 267 278 315

Current ratio 3.06 times 1.69 times 1.55 times

2 0 1 7

2 0 1 8

2 0 1 9

0

0.5

1

1.5

2

2.5

3

3.5

Current rati o

Interpretation: On the basis of above diagram this can be find out that performance

of Bega cheese limited has been reduced year by year in terms of liquidity. As in

year 2017, current ratio was of 3.06 times which reduced by almost 50% and

became of 1.69 times for year 2018. As well as in next year, it became of 1.55 times.

This performance is showing that company failed to meet idea criteria of current ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that is of 2:1 times in year 2018 and 2019. The rationale behind this poor

performance is decreased value of current assets in last two years as compared to

year 2017.

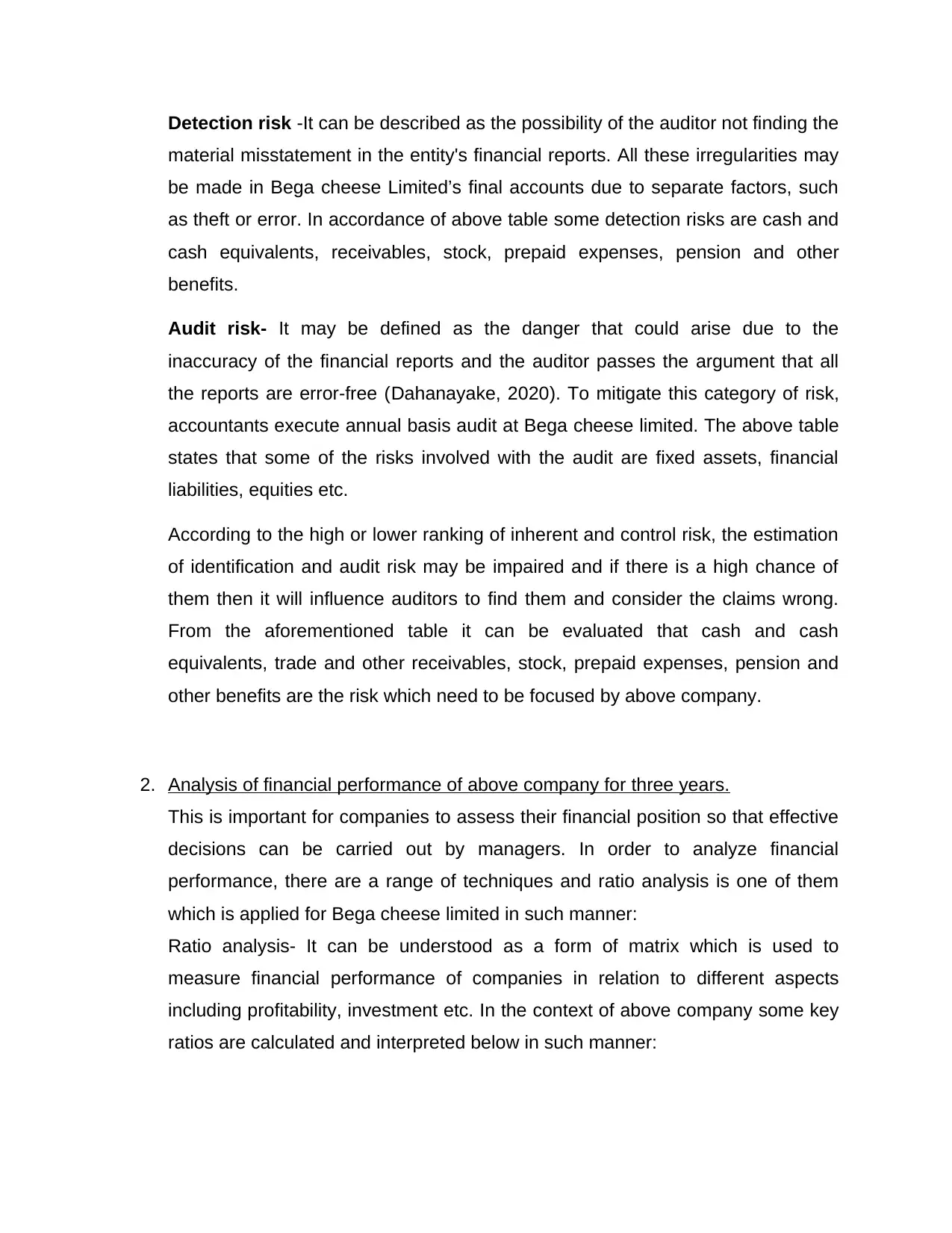

Quick ratio: Quick assets / current liabilities

Data in $ million

except quick ratio

2017 2018 2019

Quick assets 645 219 197

Current liabilities 267 278 315

Quick ratio 2.41 times 0.79 times 0.62 times

2 0 1 7

2 0 1 8

2 0 1 9

0

0.5

1

1.5

2

2.5

Quick rati o

Interpretation: Similar to above current ratio, the quick ratio of company is also has

been reduced in last two years as compared to year 2017. As in year 2017, current

ratio was of 2.41 times which reduced by almost 60% and became of 0.79 times for

year 2018. As well as in next year, it became of 0.62 times. This performance is

showing that company failed to meet idea criteria of quick ratio that is of 1.5:1 times

performance is decreased value of current assets in last two years as compared to

year 2017.

Quick ratio: Quick assets / current liabilities

Data in $ million

except quick ratio

2017 2018 2019

Quick assets 645 219 197

Current liabilities 267 278 315

Quick ratio 2.41 times 0.79 times 0.62 times

2 0 1 7

2 0 1 8

2 0 1 9

0

0.5

1

1.5

2

2.5

Quick rati o

Interpretation: Similar to above current ratio, the quick ratio of company is also has

been reduced in last two years as compared to year 2017. As in year 2017, current

ratio was of 2.41 times which reduced by almost 60% and became of 0.79 times for

year 2018. As well as in next year, it became of 0.62 times. This performance is

showing that company failed to meet idea criteria of quick ratio that is of 1.5:1 times

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in year 2018 and 2019. The rationale behind this poor performance is decreased

value of quick assets in last two years as compared to year 2017.

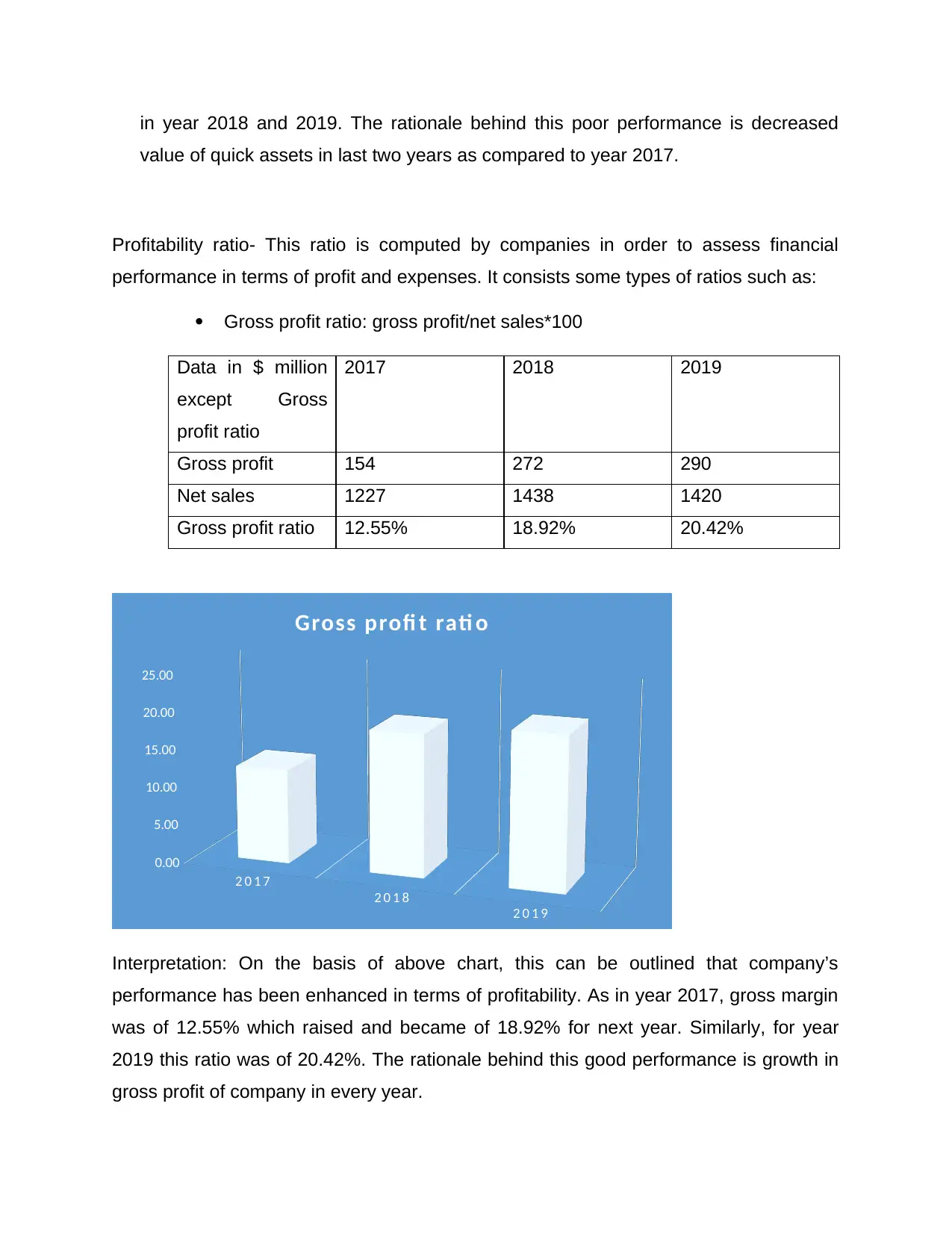

Profitability ratio- This ratio is computed by companies in order to assess financial

performance in terms of profit and expenses. It consists some types of ratios such as:

Gross profit ratio: gross profit/net sales*100

Data in $ million

except Gross

profit ratio

2017 2018 2019

Gross profit 154 272 290

Net sales 1227 1438 1420

Gross profit ratio 12.55% 18.92% 20.42%

2 0 1 7

2 0 1 8

2 0 1 9

0.00

5.00

10.00

15.00

20.00

25.00

Gross profi t rati o

Interpretation: On the basis of above chart, this can be outlined that company’s

performance has been enhanced in terms of profitability. As in year 2017, gross margin

was of 12.55% which raised and became of 18.92% for next year. Similarly, for year

2019 this ratio was of 20.42%. The rationale behind this good performance is growth in

gross profit of company in every year.

value of quick assets in last two years as compared to year 2017.

Profitability ratio- This ratio is computed by companies in order to assess financial

performance in terms of profit and expenses. It consists some types of ratios such as:

Gross profit ratio: gross profit/net sales*100

Data in $ million

except Gross

profit ratio

2017 2018 2019

Gross profit 154 272 290

Net sales 1227 1438 1420

Gross profit ratio 12.55% 18.92% 20.42%

2 0 1 7

2 0 1 8

2 0 1 9

0.00

5.00

10.00

15.00

20.00

25.00

Gross profi t rati o

Interpretation: On the basis of above chart, this can be outlined that company’s

performance has been enhanced in terms of profitability. As in year 2017, gross margin

was of 12.55% which raised and became of 18.92% for next year. Similarly, for year

2019 this ratio was of 20.42%. The rationale behind this good performance is growth in

gross profit of company in every year.

Net profit ratio: net profit/net sales*100

Data in $ million

except net profit

ratio

2017 2018 2019

Net profit 139 29 12

Net sales 1227 1438 1420

Net profit ratio 11.33% 2.02% 0.84%

2 0 1 7

2 0 1 8

2 0 1 9

0

2

4

6

8

10

12

Net profi t rati o

Interpretation: The above mentioned chart is showing that there is dramatically

reduction in net profit ratio of company. In year 2017, net profit margin was of 11.33%

which reduced and became of 2.02% for year 2018. While in year 2019, it was of

0.84%. This is indicating that company is not able to generate higher return on all those

Data in $ million

except net profit

ratio

2017 2018 2019

Net profit 139 29 12

Net sales 1227 1438 1420

Net profit ratio 11.33% 2.02% 0.84%

2 0 1 7

2 0 1 8

2 0 1 9

0

2

4

6

8

10

12

Net profi t rati o

Interpretation: The above mentioned chart is showing that there is dramatically

reduction in net profit ratio of company. In year 2017, net profit margin was of 11.33%

which reduced and became of 2.02% for year 2018. While in year 2019, it was of

0.84%. This is indicating that company is not able to generate higher return on all those

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.