Holmes Institute HA3032: Developing an Audit Program for Vmoto Ltd

VerifiedAdded on 2021/02/22

|11

|3615

|93

Report

AI Summary

This report presents a comprehensive audit program developed for Vmoto Ltd, a leading electric vehicle company. It begins with an overview of Vmoto Ltd, its key business risks, and an analysis of four key financial ratios, including gross margin and return on equity. The report then identifies and explains material account balances from the company's financial statements, such as cash, receivables, and inventory, along with relevant assertions like accuracy and completeness. Detailed audit work steps are provided for each material account balance, including a sampling plan. The report also discusses the differences between tests of controls, substantive tests of transactions, and substantive tests of balances, and the conditions under which an auditor undertakes substantive audit procedures. Finally, it explores the relationship of assertions to account balances and the selection of the most effective combination of audit procedures, providing a practical framework for auditing Vmoto Ltd's financial statements.

Developing an Audit

Program

1

Program

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...............................................................................................................1

TASK 1...............................................................................................................................1

Overview of company.....................................................................................................1

Key business risks.........................................................................................................2

Four key ratios and brief explanation.............................................................................2

Material Accounts...........................................................................................................3

Ten different material account balances........................................................................4

Explanation of selected assertion relevant to material account balance.......................5

Comprehensive set of audit work steps for each material account balance.................7

Sampling plan for each material account.......................................................................7

CONCLUSION...................................................................................................................7

REFERENCES..................................................................................................................8

2

INTRODUCTION...............................................................................................................1

TASK 1...............................................................................................................................1

Overview of company.....................................................................................................1

Key business risks.........................................................................................................2

Four key ratios and brief explanation.............................................................................2

Material Accounts...........................................................................................................3

Ten different material account balances........................................................................4

Explanation of selected assertion relevant to material account balance.......................5

Comprehensive set of audit work steps for each material account balance.................7

Sampling plan for each material account.......................................................................7

CONCLUSION...................................................................................................................7

REFERENCES..................................................................................................................8

2

INTRODUCTION

In the present era, the concept of auditing is increasing as each and every firm

wants to detect the error and frauds at the right time lowering their impact on the overall

performance of business (Austin and Carpenter, Cantore, 2017). This help an

organisation to get more advance loan from bank because the audited statement is

more faithful and reliable. In order to conduct an audit program there is need of proper

and accurate plan which gives detailed information regarding conducting an audit and it

guide the auditor to maintain an ethics within company. The audit program might be

determined as the plan of action of the auditor specifying the tasks to be performed, the

audit tests to be performed and the processes to be accompanied, the persons

responsible for performing the work as well as the time under which the work to be

performed. In this assignment Vmoto Ltd has been selected that support to better

understand the concept of audit program.

In this report, difference between tests of controls, substantive tests of

transactions and substantive tests of balances, condition for auditor to undertake

substantive audit procedures, relation of assertions to accounts balance, selection of

most accurate and effective combination of audit procedure is discussed.

TASK 1

Overview of company.

The company Vmoto Ltd is one of the leading electric vehicle manufacturing and

distributing company all over the world. The company was established in 29 October

2001 and have its operation in Australia, America and New Zealand and the middle east

(About Vmoto Limited, 2019). The company have a mission to become the largest

electric vehicle product distributor and also to deliver EV solution to its user at

international level. Vmoto Limited manufactures, markets and distributes motorcycles,

scooters and all-terrain vehicles. The company is dealing in consumer discretionary

sector within leisure product industry and recreational vehicles sub industry. The

company have a strategy to sell the high value and margin two wheeler electric product

such as delivery scooter, police vehicle, food motorcycle etc. at international level which

support them to gain the well positioned and become a global topmost two-wheel

electrical vehicle provider and electric vehicle solution supplier. In recent financial year

2018 the company sell around 10875 as a whole in which 10081 of electric vehicles are

sold in international market.

Key business risks.

In the present there can be number of business risk that can be faced by the

electric vehicle manufacture company such as the introduction of rapidly developing

digital technologies, increased regulatory stress and worldwide financial instability are

important considerations. It is observed that the key business risk to Vmoto Ltd is

related with cost because battery innovation is costly and the use of batteries in electric

vehicles must be sufficient to enable them to carry the vehicles practical for most driver,

they must be constructed using costly equipment, most of which are difficult to procure.

Audit risk

3

In the present era, the concept of auditing is increasing as each and every firm

wants to detect the error and frauds at the right time lowering their impact on the overall

performance of business (Austin and Carpenter, Cantore, 2017). This help an

organisation to get more advance loan from bank because the audited statement is

more faithful and reliable. In order to conduct an audit program there is need of proper

and accurate plan which gives detailed information regarding conducting an audit and it

guide the auditor to maintain an ethics within company. The audit program might be

determined as the plan of action of the auditor specifying the tasks to be performed, the

audit tests to be performed and the processes to be accompanied, the persons

responsible for performing the work as well as the time under which the work to be

performed. In this assignment Vmoto Ltd has been selected that support to better

understand the concept of audit program.

In this report, difference between tests of controls, substantive tests of

transactions and substantive tests of balances, condition for auditor to undertake

substantive audit procedures, relation of assertions to accounts balance, selection of

most accurate and effective combination of audit procedure is discussed.

TASK 1

Overview of company.

The company Vmoto Ltd is one of the leading electric vehicle manufacturing and

distributing company all over the world. The company was established in 29 October

2001 and have its operation in Australia, America and New Zealand and the middle east

(About Vmoto Limited, 2019). The company have a mission to become the largest

electric vehicle product distributor and also to deliver EV solution to its user at

international level. Vmoto Limited manufactures, markets and distributes motorcycles,

scooters and all-terrain vehicles. The company is dealing in consumer discretionary

sector within leisure product industry and recreational vehicles sub industry. The

company have a strategy to sell the high value and margin two wheeler electric product

such as delivery scooter, police vehicle, food motorcycle etc. at international level which

support them to gain the well positioned and become a global topmost two-wheel

electrical vehicle provider and electric vehicle solution supplier. In recent financial year

2018 the company sell around 10875 as a whole in which 10081 of electric vehicles are

sold in international market.

Key business risks.

In the present there can be number of business risk that can be faced by the

electric vehicle manufacture company such as the introduction of rapidly developing

digital technologies, increased regulatory stress and worldwide financial instability are

important considerations. It is observed that the key business risk to Vmoto Ltd is

related with cost because battery innovation is costly and the use of batteries in electric

vehicles must be sufficient to enable them to carry the vehicles practical for most driver,

they must be constructed using costly equipment, most of which are difficult to procure.

Audit risk

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

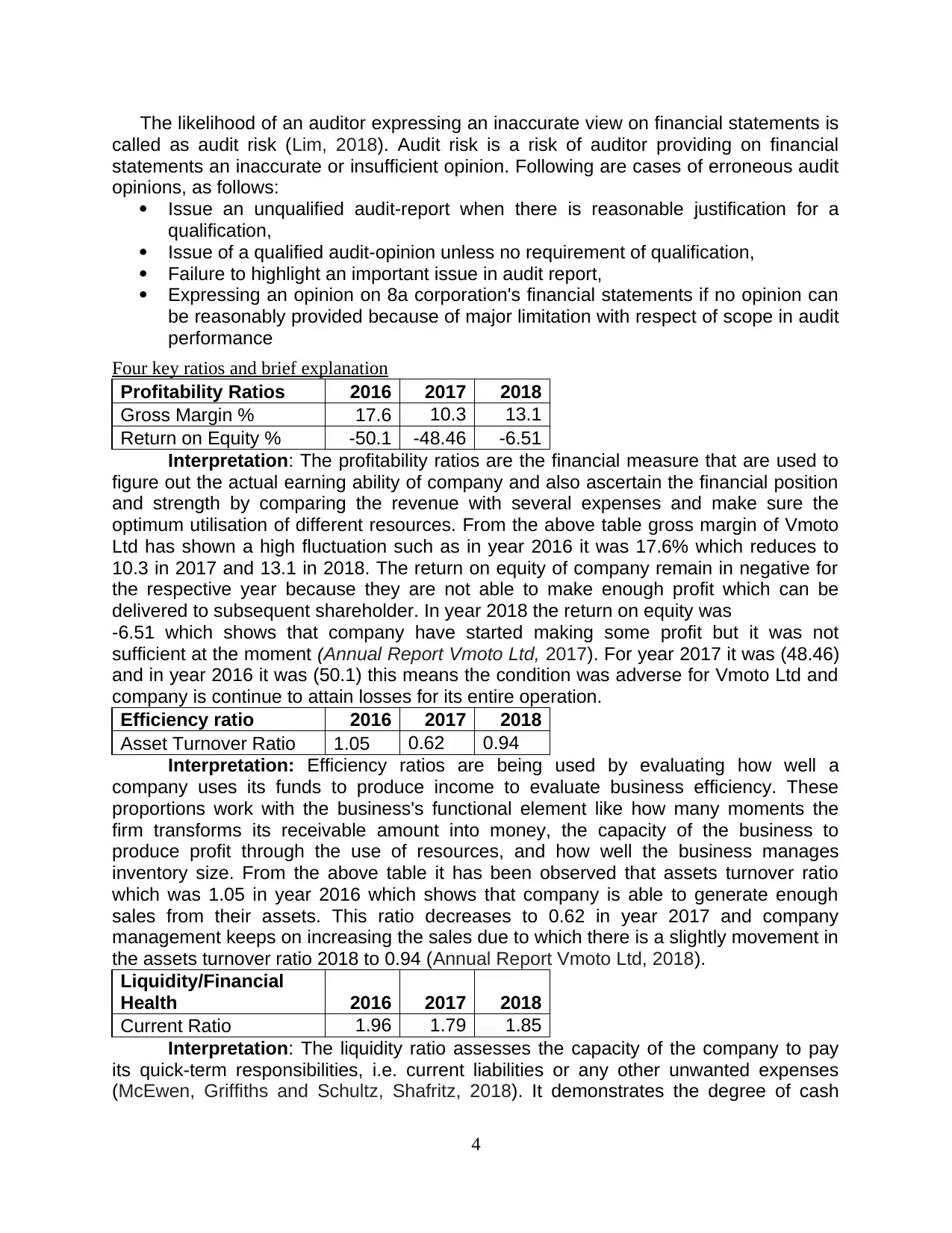

The likelihood of an auditor expressing an inaccurate view on financial statements is

called as audit risk (Lim, 2018). Audit risk is a risk of auditor providing on financial

statements an inaccurate or insufficient opinion. Following are cases of erroneous audit

opinions, as follows:

Issue an unqualified audit-report when there is reasonable justification for a

qualification,

Issue of a qualified audit-opinion unless no requirement of qualification,

Failure to highlight an important issue in audit report,

Expressing an opinion on 8a corporation's financial statements if no opinion can

be reasonably provided because of major limitation with respect of scope in audit

performance

Four key ratios and brief explanation

Profitability Ratios 2016 2017 2018

Gross Margin % 17.6 10.3 13.1

Return on Equity % -50.1 -48.46 -6.51

Interpretation: The profitability ratios are the financial measure that are used to

figure out the actual earning ability of company and also ascertain the financial position

and strength by comparing the revenue with several expenses and make sure the

optimum utilisation of different resources. From the above table gross margin of Vmoto

Ltd has shown a high fluctuation such as in year 2016 it was 17.6% which reduces to

10.3 in 2017 and 13.1 in 2018. The return on equity of company remain in negative for

the respective year because they are not able to make enough profit which can be

delivered to subsequent shareholder. In year 2018 the return on equity was

-6.51 which shows that company have started making some profit but it was not

sufficient at the moment (Annual Report Vmoto Ltd, 2017). For year 2017 it was (48.46)

and in year 2016 it was (50.1) this means the condition was adverse for Vmoto Ltd and

company is continue to attain losses for its entire operation.

Efficiency ratio 2016 2017 2018

Asset Turnover Ratio 1.05 0.62 0.94

Interpretation: Efficiency ratios are being used by evaluating how well a

company uses its funds to produce income to evaluate business efficiency. These

proportions work with the business's functional element like how many moments the

firm transforms its receivable amount into money, the capacity of the business to

produce profit through the use of resources, and how well the business manages

inventory size. From the above table it has been observed that assets turnover ratio

which was 1.05 in year 2016 which shows that company is able to generate enough

sales from their assets. This ratio decreases to 0.62 in year 2017 and company

management keeps on increasing the sales due to which there is a slightly movement in

the assets turnover ratio 2018 to 0.94 (Annual Report Vmoto Ltd, 2018).

Liquidity/Financial

Health 2016 2017 2018

Current Ratio 1.96 1.79 1.85

Interpretation: The liquidity ratio assesses the capacity of the company to pay

its quick-term responsibilities, i.e. current liabilities or any other unwanted expenses

(McEwen, Griffiths and Schultz, Shafritz, 2018). It demonstrates the degree of cash

4

called as audit risk (Lim, 2018). Audit risk is a risk of auditor providing on financial

statements an inaccurate or insufficient opinion. Following are cases of erroneous audit

opinions, as follows:

Issue an unqualified audit-report when there is reasonable justification for a

qualification,

Issue of a qualified audit-opinion unless no requirement of qualification,

Failure to highlight an important issue in audit report,

Expressing an opinion on 8a corporation's financial statements if no opinion can

be reasonably provided because of major limitation with respect of scope in audit

performance

Four key ratios and brief explanation

Profitability Ratios 2016 2017 2018

Gross Margin % 17.6 10.3 13.1

Return on Equity % -50.1 -48.46 -6.51

Interpretation: The profitability ratios are the financial measure that are used to

figure out the actual earning ability of company and also ascertain the financial position

and strength by comparing the revenue with several expenses and make sure the

optimum utilisation of different resources. From the above table gross margin of Vmoto

Ltd has shown a high fluctuation such as in year 2016 it was 17.6% which reduces to

10.3 in 2017 and 13.1 in 2018. The return on equity of company remain in negative for

the respective year because they are not able to make enough profit which can be

delivered to subsequent shareholder. In year 2018 the return on equity was

-6.51 which shows that company have started making some profit but it was not

sufficient at the moment (Annual Report Vmoto Ltd, 2017). For year 2017 it was (48.46)

and in year 2016 it was (50.1) this means the condition was adverse for Vmoto Ltd and

company is continue to attain losses for its entire operation.

Efficiency ratio 2016 2017 2018

Asset Turnover Ratio 1.05 0.62 0.94

Interpretation: Efficiency ratios are being used by evaluating how well a

company uses its funds to produce income to evaluate business efficiency. These

proportions work with the business's functional element like how many moments the

firm transforms its receivable amount into money, the capacity of the business to

produce profit through the use of resources, and how well the business manages

inventory size. From the above table it has been observed that assets turnover ratio

which was 1.05 in year 2016 which shows that company is able to generate enough

sales from their assets. This ratio decreases to 0.62 in year 2017 and company

management keeps on increasing the sales due to which there is a slightly movement in

the assets turnover ratio 2018 to 0.94 (Annual Report Vmoto Ltd, 2018).

Liquidity/Financial

Health 2016 2017 2018

Current Ratio 1.96 1.79 1.85

Interpretation: The liquidity ratio assesses the capacity of the company to pay

its quick-term responsibilities, i.e. current liabilities or any other unwanted expenses

(McEwen, Griffiths and Schultz, Shafritz, 2018). It demonstrates the degree of cash

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

flow, that is the total quantity of their assets that can be transformed rapidly into money

to pay their commitments when they are actually due. This ratio not only measure the

total of cash the company holds but also determine the actual time current assets can

be transferred into cash. There are different types such as current ratio, quick ratio, acid

test ratio etc. In the Vmoto Ltd the current ratio for the year 2016 was 1.96 which means

company is easily able to convert its assets into cash whenever it is required and there

is good cash flow throughout the year. In year 2017 it was the proportion of current

assets decreases to 1.79 that shows there is some issues within company liquidity.

Then again company start working on its cash flow and make provision so that easily

their current assets are converted into cash because in year 2018 the percentage of

current ratio was 1.85.

Material Accounts

In the accounting world, the material accounts are considering to be important as

in case if the information are missing to these material and it have a greater impact on

the decision making of the user of financial statements. All those items are considered

to be material in case if they have a major influence upon the described profit of

company. For example, raw materials, parts, sub-components and equipment of

manufacturing. In principle, everything absorbed can be categorized as material during

the manufacturing phase.

In the preparing and submission of a financial document, financial accounting

methodologies often address the conception of materiality. While financial reporting

structures can address materiality in distinct ways. According to ISA 320 materiality in

performing and planning an audit programme it helps to Addresses the problem of the

strategy to determining materiality by explaining that materiality relies on the magnitude

and type of an object or on a mixture of both regarded in the context of the specific

conditions in which it occurs. It also establishes advice on the use of appropriate

benchmarks, like classifications of recorded revenue or of totally appropriate

classifications of operations, transactions or disclosures, which should be supported by

the practice of competent judgment in reaching the appropriate level of materiality. For

instance, it tends during the audit that current financial results are going to differ

significantly from the expected financial results that are originally used to assess

materiality for the financial statement itself and the auditor is responsible to review that

materiality.

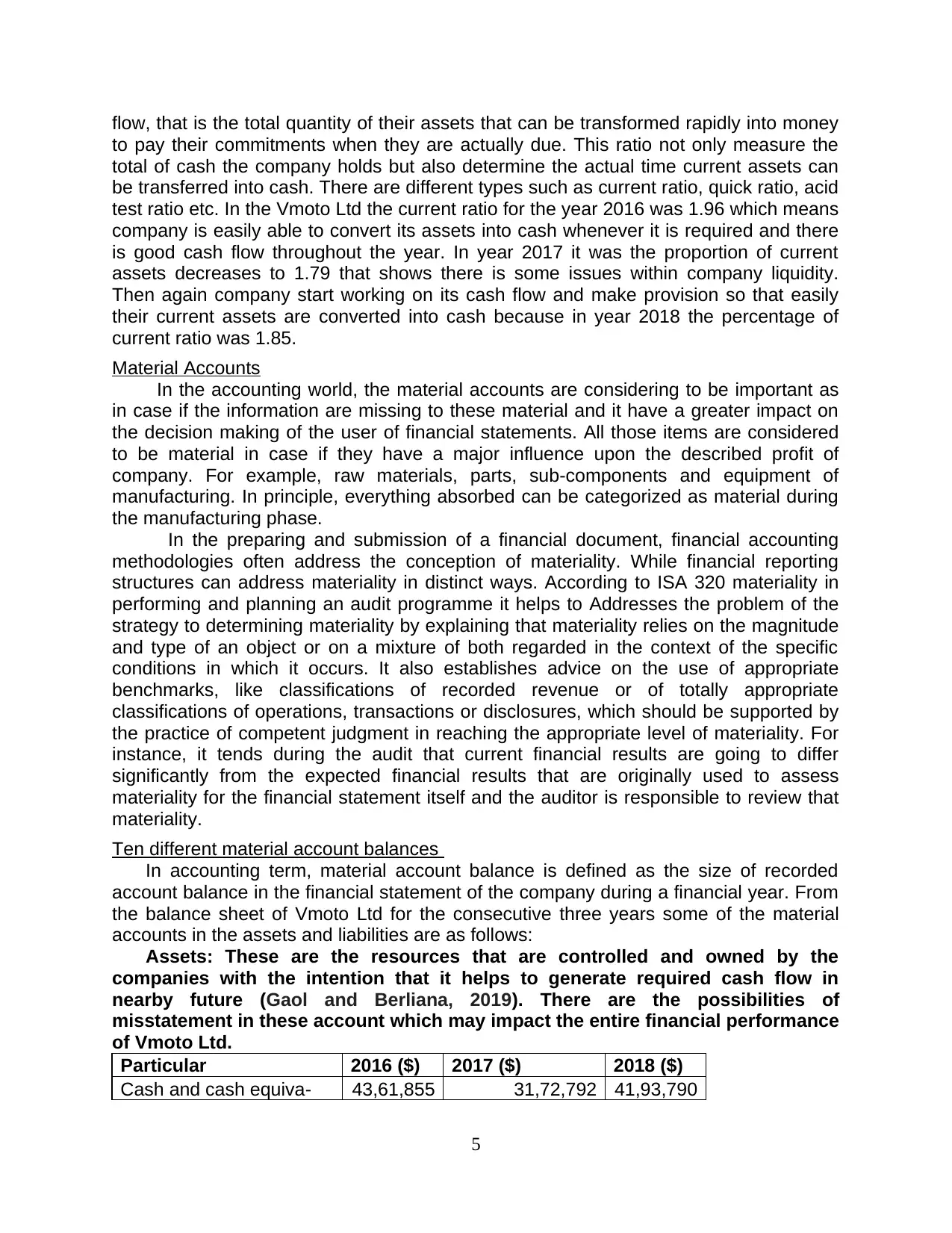

Ten different material account balances

In accounting term, material account balance is defined as the size of recorded

account balance in the financial statement of the company during a financial year. From

the balance sheet of Vmoto Ltd for the consecutive three years some of the material

accounts in the assets and liabilities are as follows:

Assets: These are the resources that are controlled and owned by the

companies with the intention that it helps to generate required cash flow in

nearby future (Gaol and Berliana, 2019). There are the possibilities of

misstatement in these account which may impact the entire financial performance

of Vmoto Ltd.

Particular 2016 ($) 2017 ($) 2018 ($)

Cash and cash equiva- 43,61,855 31,72,792 41,93,790

5

to pay their commitments when they are actually due. This ratio not only measure the

total of cash the company holds but also determine the actual time current assets can

be transferred into cash. There are different types such as current ratio, quick ratio, acid

test ratio etc. In the Vmoto Ltd the current ratio for the year 2016 was 1.96 which means

company is easily able to convert its assets into cash whenever it is required and there

is good cash flow throughout the year. In year 2017 it was the proportion of current

assets decreases to 1.79 that shows there is some issues within company liquidity.

Then again company start working on its cash flow and make provision so that easily

their current assets are converted into cash because in year 2018 the percentage of

current ratio was 1.85.

Material Accounts

In the accounting world, the material accounts are considering to be important as

in case if the information are missing to these material and it have a greater impact on

the decision making of the user of financial statements. All those items are considered

to be material in case if they have a major influence upon the described profit of

company. For example, raw materials, parts, sub-components and equipment of

manufacturing. In principle, everything absorbed can be categorized as material during

the manufacturing phase.

In the preparing and submission of a financial document, financial accounting

methodologies often address the conception of materiality. While financial reporting

structures can address materiality in distinct ways. According to ISA 320 materiality in

performing and planning an audit programme it helps to Addresses the problem of the

strategy to determining materiality by explaining that materiality relies on the magnitude

and type of an object or on a mixture of both regarded in the context of the specific

conditions in which it occurs. It also establishes advice on the use of appropriate

benchmarks, like classifications of recorded revenue or of totally appropriate

classifications of operations, transactions or disclosures, which should be supported by

the practice of competent judgment in reaching the appropriate level of materiality. For

instance, it tends during the audit that current financial results are going to differ

significantly from the expected financial results that are originally used to assess

materiality for the financial statement itself and the auditor is responsible to review that

materiality.

Ten different material account balances

In accounting term, material account balance is defined as the size of recorded

account balance in the financial statement of the company during a financial year. From

the balance sheet of Vmoto Ltd for the consecutive three years some of the material

accounts in the assets and liabilities are as follows:

Assets: These are the resources that are controlled and owned by the

companies with the intention that it helps to generate required cash flow in

nearby future (Gaol and Berliana, 2019). There are the possibilities of

misstatement in these account which may impact the entire financial performance

of Vmoto Ltd.

Particular 2016 ($) 2017 ($) 2018 ($)

Cash and cash equiva- 43,61,855 31,72,792 41,93,790

5

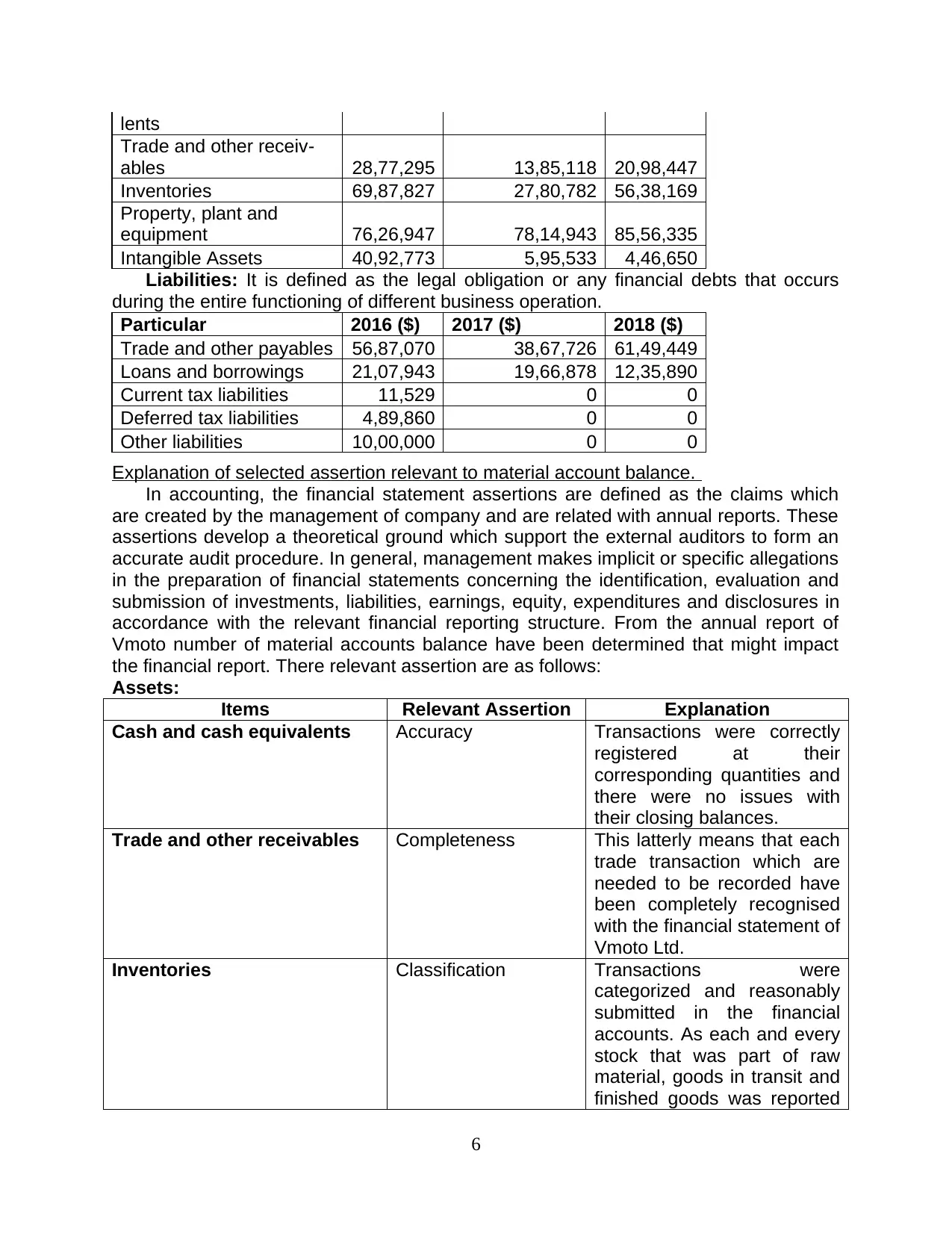

lents

Trade and other receiv-

ables 28,77,295 13,85,118 20,98,447

Inventories 69,87,827 27,80,782 56,38,169

Property, plant and

equipment 76,26,947 78,14,943 85,56,335

Intangible Assets 40,92,773 5,95,533 4,46,650

Liabilities: It is defined as the legal obligation or any financial debts that occurs

during the entire functioning of different business operation.

Particular 2016 ($) 2017 ($) 2018 ($)

Trade and other payables 56,87,070 38,67,726 61,49,449

Loans and borrowings 21,07,943 19,66,878 12,35,890

Current tax liabilities 11,529 0 0

Deferred tax liabilities 4,89,860 0 0

Other liabilities 10,00,000 0 0

Explanation of selected assertion relevant to material account balance.

In accounting, the financial statement assertions are defined as the claims which

are created by the management of company and are related with annual reports. These

assertions develop a theoretical ground which support the external auditors to form an

accurate audit procedure. In general, management makes implicit or specific allegations

in the preparation of financial statements concerning the identification, evaluation and

submission of investments, liabilities, earnings, equity, expenditures and disclosures in

accordance with the relevant financial reporting structure. From the annual report of

Vmoto number of material accounts balance have been determined that might impact

the financial report. There relevant assertion are as follows:

Assets:

Items Relevant Assertion Explanation

Cash and cash equivalents Accuracy Transactions were correctly

registered at their

corresponding quantities and

there were no issues with

their closing balances.

Trade and other receivables Completeness This latterly means that each

trade transaction which are

needed to be recorded have

been completely recognised

with the financial statement of

Vmoto Ltd.

Inventories Classification Transactions were

categorized and reasonably

submitted in the financial

accounts. As each and every

stock that was part of raw

material, goods in transit and

finished goods was reported

6

Trade and other receiv-

ables 28,77,295 13,85,118 20,98,447

Inventories 69,87,827 27,80,782 56,38,169

Property, plant and

equipment 76,26,947 78,14,943 85,56,335

Intangible Assets 40,92,773 5,95,533 4,46,650

Liabilities: It is defined as the legal obligation or any financial debts that occurs

during the entire functioning of different business operation.

Particular 2016 ($) 2017 ($) 2018 ($)

Trade and other payables 56,87,070 38,67,726 61,49,449

Loans and borrowings 21,07,943 19,66,878 12,35,890

Current tax liabilities 11,529 0 0

Deferred tax liabilities 4,89,860 0 0

Other liabilities 10,00,000 0 0

Explanation of selected assertion relevant to material account balance.

In accounting, the financial statement assertions are defined as the claims which

are created by the management of company and are related with annual reports. These

assertions develop a theoretical ground which support the external auditors to form an

accurate audit procedure. In general, management makes implicit or specific allegations

in the preparation of financial statements concerning the identification, evaluation and

submission of investments, liabilities, earnings, equity, expenditures and disclosures in

accordance with the relevant financial reporting structure. From the annual report of

Vmoto number of material accounts balance have been determined that might impact

the financial report. There relevant assertion are as follows:

Assets:

Items Relevant Assertion Explanation

Cash and cash equivalents Accuracy Transactions were correctly

registered at their

corresponding quantities and

there were no issues with

their closing balances.

Trade and other receivables Completeness This latterly means that each

trade transaction which are

needed to be recorded have

been completely recognised

with the financial statement of

Vmoto Ltd.

Inventories Classification Transactions were

categorized and reasonably

submitted in the financial

accounts. As each and every

stock that was part of raw

material, goods in transit and

finished goods was reported

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

correctly.

Property, plant and

equipment

Occurrence This defines that each

transaction recognised in the

annual report have happen

and is already a part of

Vmoto Ltd.

Intangible Assets Cut-off All the transaction related to

the intangible assets has

been recognised

Liabilities

Items Relevant Assertion Explanation

Trade and other payables Valuation The entire balance of trade

and other payables for Vmoto

have been appropriately

valued and balanced.

Loans and borrowings Rights & Obligations This assertion simply defines

that liabilities identified in the

accounts constitute Vmoto

Ltd obligation that are

needed to be transfer within

future period.

Current tax liabilities Existence It shows that the liability

balance exit at the end of

year such as in year 2016 the

balance was $11,529 which

write off in the consecutive

year.

Deferred tax liabilities Existence This assertion helps to define

that the balance of liability

was recorded at the end of

period. From the annual

report the balance in year

2016 was $4,89,860.

Other liabilities Existence It indicates that at the closure

of accounting year, the

liability balance departure,

such as in year 2016, the

balance was $10,00,000.

Comprehensive set of audit work steps for each material account balance.

Assets:

Items

Cash and cash equivalents At first step while auditing cash and

cash equivalents auditor should list out

7

Property, plant and

equipment

Occurrence This defines that each

transaction recognised in the

annual report have happen

and is already a part of

Vmoto Ltd.

Intangible Assets Cut-off All the transaction related to

the intangible assets has

been recognised

Liabilities

Items Relevant Assertion Explanation

Trade and other payables Valuation The entire balance of trade

and other payables for Vmoto

have been appropriately

valued and balanced.

Loans and borrowings Rights & Obligations This assertion simply defines

that liabilities identified in the

accounts constitute Vmoto

Ltd obligation that are

needed to be transfer within

future period.

Current tax liabilities Existence It shows that the liability

balance exit at the end of

year such as in year 2016 the

balance was $11,529 which

write off in the consecutive

year.

Deferred tax liabilities Existence This assertion helps to define

that the balance of liability

was recorded at the end of

period. From the annual

report the balance in year

2016 was $4,89,860.

Other liabilities Existence It indicates that at the closure

of accounting year, the

liability balance departure,

such as in year 2016, the

balance was $10,00,000.

Comprehensive set of audit work steps for each material account balance.

Assets:

Items

Cash and cash equivalents At first step while auditing cash and

cash equivalents auditor should list out

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

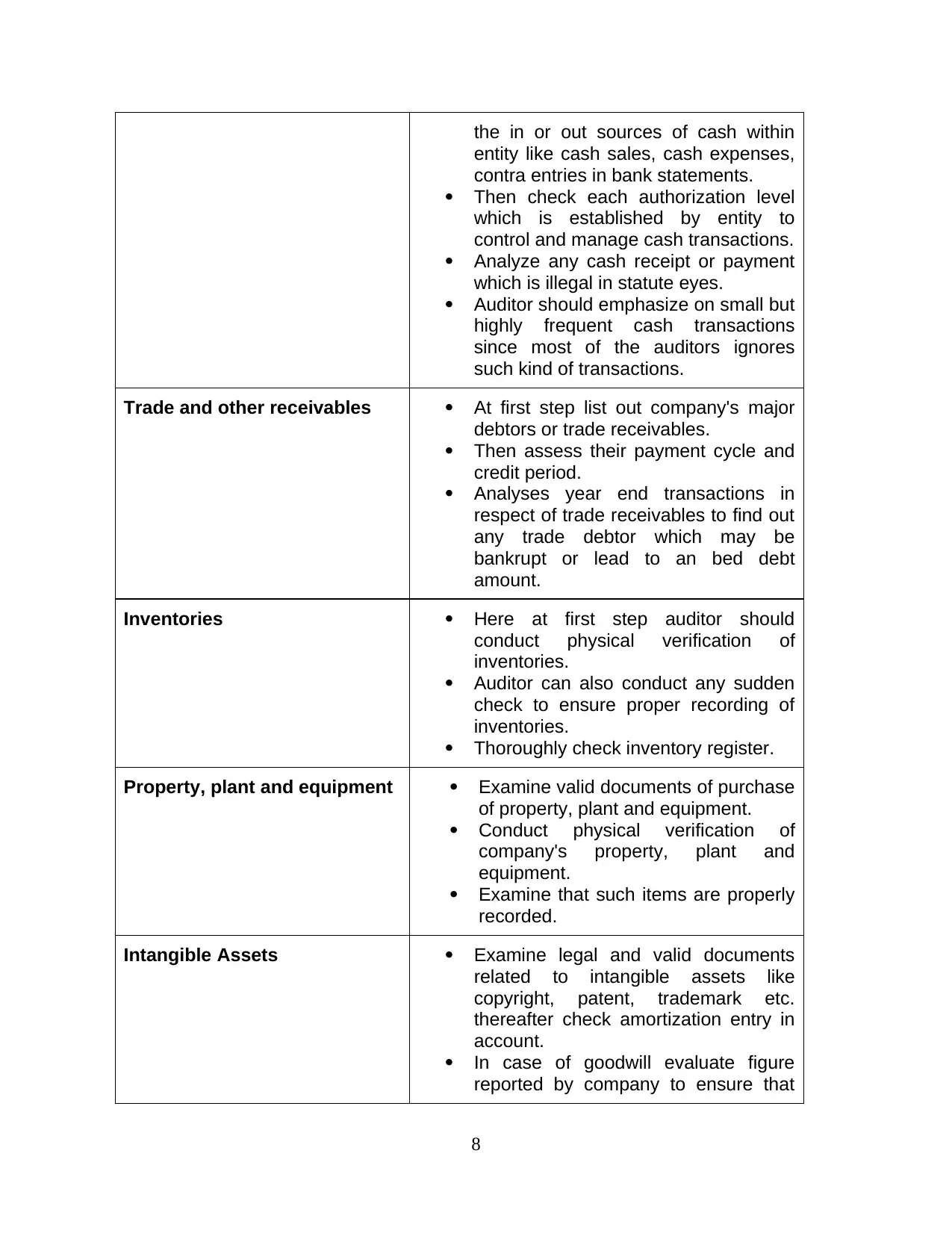

the in or out sources of cash within

entity like cash sales, cash expenses,

contra entries in bank statements.

Then check each authorization level

which is established by entity to

control and manage cash transactions.

Analyze any cash receipt or payment

which is illegal in statute eyes.

Auditor should emphasize on small but

highly frequent cash transactions

since most of the auditors ignores

such kind of transactions.

Trade and other receivables At first step list out company's major

debtors or trade receivables.

Then assess their payment cycle and

credit period.

Analyses year end transactions in

respect of trade receivables to find out

any trade debtor which may be

bankrupt or lead to an bed debt

amount.

Inventories Here at first step auditor should

conduct physical verification of

inventories.

Auditor can also conduct any sudden

check to ensure proper recording of

inventories.

Thoroughly check inventory register.

Property, plant and equipment Examine valid documents of purchase

of property, plant and equipment.

Conduct physical verification of

company's property, plant and

equipment.

Examine that such items are properly

recorded.

Intangible Assets Examine legal and valid documents

related to intangible assets like

copyright, patent, trademark etc.

thereafter check amortization entry in

account.

In case of goodwill evaluate figure

reported by company to ensure that

8

entity like cash sales, cash expenses,

contra entries in bank statements.

Then check each authorization level

which is established by entity to

control and manage cash transactions.

Analyze any cash receipt or payment

which is illegal in statute eyes.

Auditor should emphasize on small but

highly frequent cash transactions

since most of the auditors ignores

such kind of transactions.

Trade and other receivables At first step list out company's major

debtors or trade receivables.

Then assess their payment cycle and

credit period.

Analyses year end transactions in

respect of trade receivables to find out

any trade debtor which may be

bankrupt or lead to an bed debt

amount.

Inventories Here at first step auditor should

conduct physical verification of

inventories.

Auditor can also conduct any sudden

check to ensure proper recording of

inventories.

Thoroughly check inventory register.

Property, plant and equipment Examine valid documents of purchase

of property, plant and equipment.

Conduct physical verification of

company's property, plant and

equipment.

Examine that such items are properly

recorded.

Intangible Assets Examine legal and valid documents

related to intangible assets like

copyright, patent, trademark etc.

thereafter check amortization entry in

account.

In case of goodwill evaluate figure

reported by company to ensure that

8

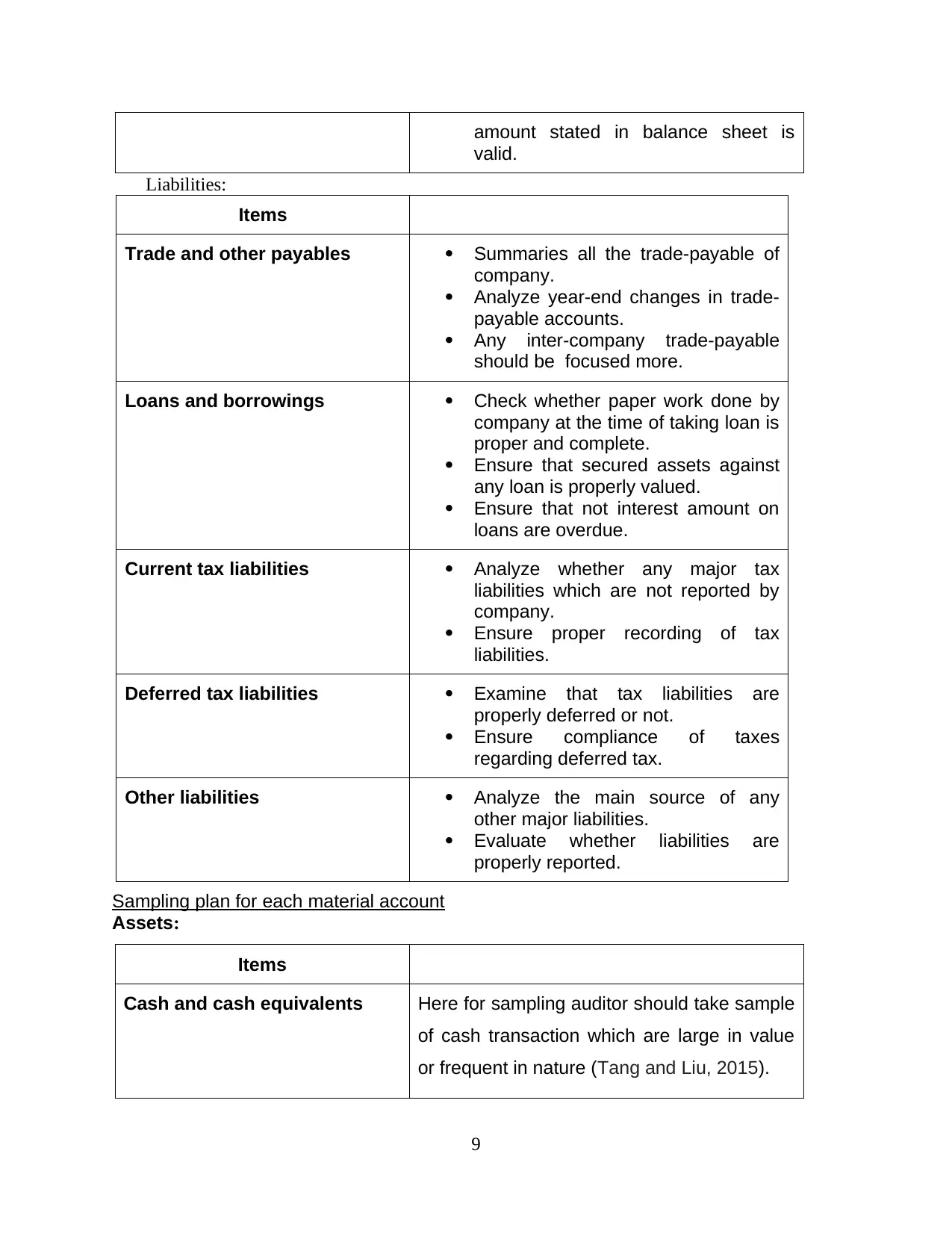

amount stated in balance sheet is

valid.

Liabilities:

Items

Trade and other payables Summaries all the trade-payable of

company.

Analyze year-end changes in trade-

payable accounts.

Any inter-company trade-payable

should be focused more.

Loans and borrowings Check whether paper work done by

company at the time of taking loan is

proper and complete.

Ensure that secured assets against

any loan is properly valued.

Ensure that not interest amount on

loans are overdue.

Current tax liabilities Analyze whether any major tax

liabilities which are not reported by

company.

Ensure proper recording of tax

liabilities.

Deferred tax liabilities Examine that tax liabilities are

properly deferred or not.

Ensure compliance of taxes

regarding deferred tax.

Other liabilities Analyze the main source of any

other major liabilities.

Evaluate whether liabilities are

properly reported.

Sampling plan for each material account

Assets:

Items

Cash and cash equivalents Here for sampling auditor should take sample

of cash transaction which are large in value

or frequent in nature (Tang and Liu, 2015).

9

valid.

Liabilities:

Items

Trade and other payables Summaries all the trade-payable of

company.

Analyze year-end changes in trade-

payable accounts.

Any inter-company trade-payable

should be focused more.

Loans and borrowings Check whether paper work done by

company at the time of taking loan is

proper and complete.

Ensure that secured assets against

any loan is properly valued.

Ensure that not interest amount on

loans are overdue.

Current tax liabilities Analyze whether any major tax

liabilities which are not reported by

company.

Ensure proper recording of tax

liabilities.

Deferred tax liabilities Examine that tax liabilities are

properly deferred or not.

Ensure compliance of taxes

regarding deferred tax.

Other liabilities Analyze the main source of any

other major liabilities.

Evaluate whether liabilities are

properly reported.

Sampling plan for each material account

Assets:

Items

Cash and cash equivalents Here for sampling auditor should take sample

of cash transaction which are large in value

or frequent in nature (Tang and Liu, 2015).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

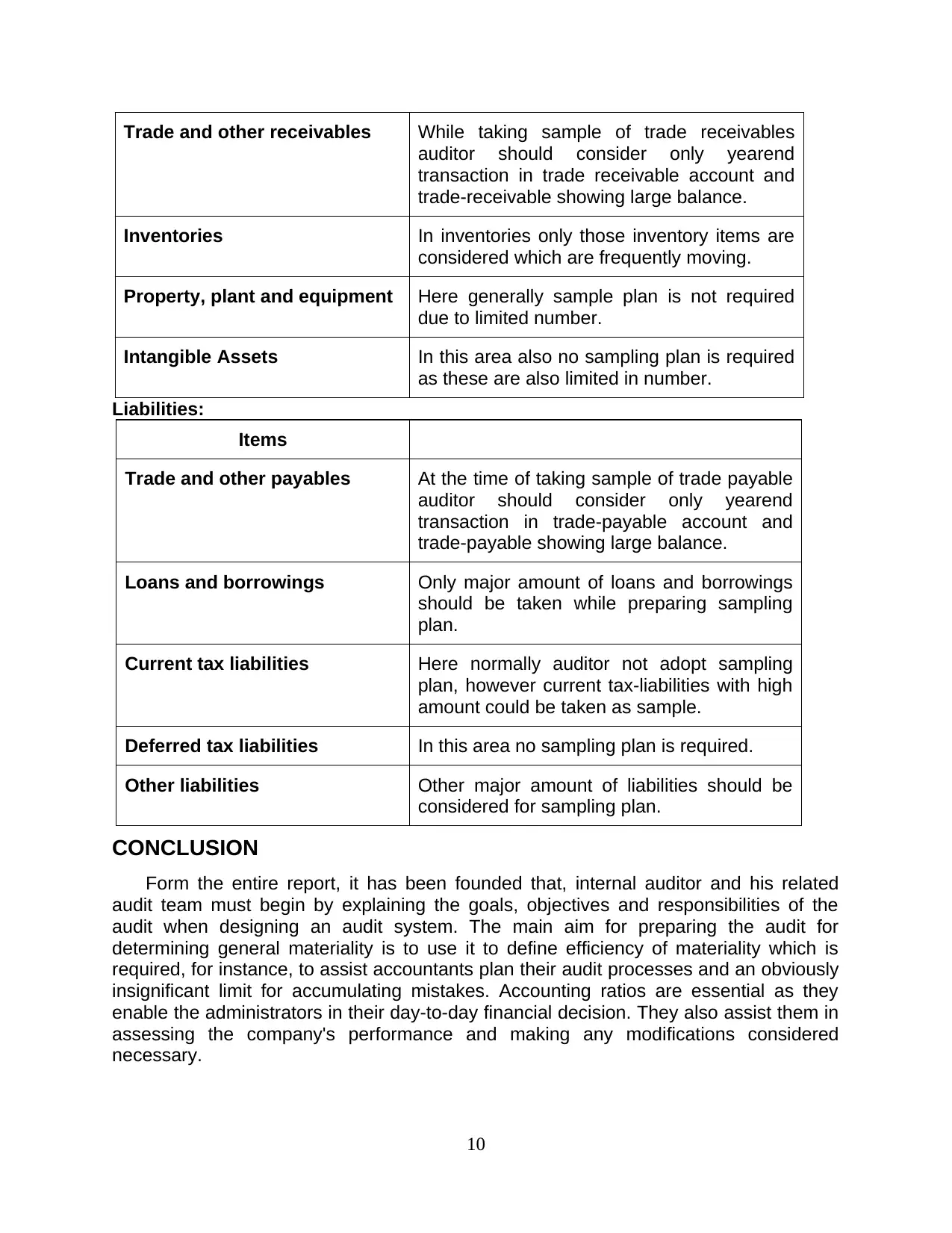

Trade and other receivables While taking sample of trade receivables

auditor should consider only yearend

transaction in trade receivable account and

trade-receivable showing large balance.

Inventories In inventories only those inventory items are

considered which are frequently moving.

Property, plant and equipment Here generally sample plan is not required

due to limited number.

Intangible Assets In this area also no sampling plan is required

as these are also limited in number.

Liabilities:

Items

Trade and other payables At the time of taking sample of trade payable

auditor should consider only yearend

transaction in trade-payable account and

trade-payable showing large balance.

Loans and borrowings Only major amount of loans and borrowings

should be taken while preparing sampling

plan.

Current tax liabilities Here normally auditor not adopt sampling

plan, however current tax-liabilities with high

amount could be taken as sample.

Deferred tax liabilities In this area no sampling plan is required.

Other liabilities Other major amount of liabilities should be

considered for sampling plan.

CONCLUSION

Form the entire report, it has been founded that, internal auditor and his related

audit team must begin by explaining the goals, objectives and responsibilities of the

audit when designing an audit system. The main aim for preparing the audit for

determining general materiality is to use it to define efficiency of materiality which is

required, for instance, to assist accountants plan their audit processes and an obviously

insignificant limit for accumulating mistakes. Accounting ratios are essential as they

enable the administrators in their day-to-day financial decision. They also assist them in

assessing the company's performance and making any modifications considered

necessary.

10

auditor should consider only yearend

transaction in trade receivable account and

trade-receivable showing large balance.

Inventories In inventories only those inventory items are

considered which are frequently moving.

Property, plant and equipment Here generally sample plan is not required

due to limited number.

Intangible Assets In this area also no sampling plan is required

as these are also limited in number.

Liabilities:

Items

Trade and other payables At the time of taking sample of trade payable

auditor should consider only yearend

transaction in trade-payable account and

trade-payable showing large balance.

Loans and borrowings Only major amount of loans and borrowings

should be taken while preparing sampling

plan.

Current tax liabilities Here normally auditor not adopt sampling

plan, however current tax-liabilities with high

amount could be taken as sample.

Deferred tax liabilities In this area no sampling plan is required.

Other liabilities Other major amount of liabilities should be

considered for sampling plan.

CONCLUSION

Form the entire report, it has been founded that, internal auditor and his related

audit team must begin by explaining the goals, objectives and responsibilities of the

audit when designing an audit system. The main aim for preparing the audit for

determining general materiality is to use it to define efficiency of materiality which is

required, for instance, to assist accountants plan their audit processes and an obviously

insignificant limit for accumulating mistakes. Accounting ratios are essential as they

enable the administrators in their day-to-day financial decision. They also assist them in

assessing the company's performance and making any modifications considered

necessary.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Austin, A. A. and Carpenter, T., 2018. Game On: Making Audit Firm Communication

More Engaging to Improve Auditors’ Fraud Actions during Evidence

Evaluation. Available at SSRN 2951396.

Cantore, N., 2017. Factors affecting the adoption of energy efficiency in the

manufacturing sector of developing countries. Energy Efficiency. 10(3). pp.743-

752.

Gaol, L. and Berliana, M., 2019. Time Budget Pressure, Auditor Locus Of Control And

Audit Quality Reduction Behavior. Auditor Locus Of Control And Audit Quality

Reduction Behavior (August 20, 2019).

Lim, D., 2018. Quality assurance in higher education: A study of developing countries: A

study of developing countries. Routledge.

McEwen, L. A., Griffiths, J. and Schultz, K., 2015. Developing and successfully

implementing a competency-based portfolio assessment system in a

postgraduate family medicine residency program. Academic Medicine. 90(11).

pp.1515-1526.

Shafritz, J., 2018. The dictionary of public policy and administration. Routledge.

Tang, C. and Liu, J., 2015. Selecting a trusted cloud service provider for your SaaS

program. Computers & Security. 50. pp.60-73.

Online

About Vmoto Limited. 2019. [Online] Available Through:

< http://www.vmoto.com/>

Annual Report Vmoto Ltd. 2017. [Online] Available Through:

<http://www.vmoto.com/assets/uploads/20180517/2018051712333861064>.

Annual Report Vmoto Ltd. 2018. [Online] Available Through:

< http://www.vmoto.com/assets/uploads/20190411/2019041114411803034.pdf>.

11

Books and Journals:

Austin, A. A. and Carpenter, T., 2018. Game On: Making Audit Firm Communication

More Engaging to Improve Auditors’ Fraud Actions during Evidence

Evaluation. Available at SSRN 2951396.

Cantore, N., 2017. Factors affecting the adoption of energy efficiency in the

manufacturing sector of developing countries. Energy Efficiency. 10(3). pp.743-

752.

Gaol, L. and Berliana, M., 2019. Time Budget Pressure, Auditor Locus Of Control And

Audit Quality Reduction Behavior. Auditor Locus Of Control And Audit Quality

Reduction Behavior (August 20, 2019).

Lim, D., 2018. Quality assurance in higher education: A study of developing countries: A

study of developing countries. Routledge.

McEwen, L. A., Griffiths, J. and Schultz, K., 2015. Developing and successfully

implementing a competency-based portfolio assessment system in a

postgraduate family medicine residency program. Academic Medicine. 90(11).

pp.1515-1526.

Shafritz, J., 2018. The dictionary of public policy and administration. Routledge.

Tang, C. and Liu, J., 2015. Selecting a trusted cloud service provider for your SaaS

program. Computers & Security. 50. pp.60-73.

Online

About Vmoto Limited. 2019. [Online] Available Through:

< http://www.vmoto.com/>

Annual Report Vmoto Ltd. 2017. [Online] Available Through:

<http://www.vmoto.com/assets/uploads/20180517/2018051712333861064>.

Annual Report Vmoto Ltd. 2018. [Online] Available Through:

< http://www.vmoto.com/assets/uploads/20190411/2019041114411803034.pdf>.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.