A Comprehensive Analysis of Current Development in Accounting Thought

VerifiedAdded on 2021/06/16

|17

|2137

|25

Essay

AI Summary

This essay provides an analysis of current developments in accounting thought, focusing on the proposals made by the Financial Accounting Standards Board (FASB) regarding changes in accounting standards, particularly updates to the income statement and disclosure of comprehensive income. The FASB's practice of soliciting comments from various companies is examined through the lens of four organizations from different sectors, assessing their acceptance or rejection of the proposed changes. The essay evaluates the comments provided by these companies to determine whether the proposal aligns with public interests and contributes to the development of better accounting standards. It also discusses the significance of the proposed changes and their potential impact on financial reporting, with the overall conclusion emphasizing the need for revisions to the proposal based on the feedback received from the companies.

Running head: CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Current Development in Accounting Thought

Name of the Student:

Name of the University:

Author’s Note:

Current Development in Accounting Thought

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Table of Contents

Answer to Question No 2................................................................................................................2

Executive Summary.....................................................................................................................2

Comment Letters.........................................................................................................................3

Introduction..................................................................................................................................3

Assessment of exposure draft being helpful in developing the interests of the public................3

Comments provided by the letter of the companies....................................................................5

Proposal significance...................................................................................................................7

Conclusion...................................................................................................................................7

Reference List..................................................................................................................................8

Appendix........................................................................................................................................10

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Table of Contents

Answer to Question No 2................................................................................................................2

Executive Summary.....................................................................................................................2

Comment Letters.........................................................................................................................3

Introduction..................................................................................................................................3

Assessment of exposure draft being helpful in developing the interests of the public................3

Comments provided by the letter of the companies....................................................................5

Proposal significance...................................................................................................................7

Conclusion...................................................................................................................................7

Reference List..................................................................................................................................8

Appendix........................................................................................................................................10

2

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Answer to Question No 2

Executive Summary

The concerned assignment is related to gaining knowledge about the proposals that are

provided by the “Financial Accounting Standards Board (FASB)” with regards to the changes in

the accounting standards. The FASB allows the proposals open for comments so that different

companies can provide their views and accordingly changes can be made in the draft. The draft

that has been propose by FASB is with regards to the “updates in the income statement and the

disclosure of the comprehensive income”. After the proposal of the draft, the draft has been kept

for comments so that views and ideas of different companies can be gathered and accordingly the

rejection and the acceptance of the proposal can be attained and in certain circumstances

amendments in the draft is possible with the help of which a better draft proposal is possible. The

assignment in order to have certain knowledge comments that have been provided a total of four

organizations who have given their comments have been selected and all the four organizations

are from four different sectors in order to have a comparative view of what all the sectors have a

view on the proposal. The acceptance and the rejection of the proposal by the companies would

be helpful in determining the fact that whether the proposal can be put into use or would be

rejected.

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Answer to Question No 2

Executive Summary

The concerned assignment is related to gaining knowledge about the proposals that are

provided by the “Financial Accounting Standards Board (FASB)” with regards to the changes in

the accounting standards. The FASB allows the proposals open for comments so that different

companies can provide their views and accordingly changes can be made in the draft. The draft

that has been propose by FASB is with regards to the “updates in the income statement and the

disclosure of the comprehensive income”. After the proposal of the draft, the draft has been kept

for comments so that views and ideas of different companies can be gathered and accordingly the

rejection and the acceptance of the proposal can be attained and in certain circumstances

amendments in the draft is possible with the help of which a better draft proposal is possible. The

assignment in order to have certain knowledge comments that have been provided a total of four

organizations who have given their comments have been selected and all the four organizations

are from four different sectors in order to have a comparative view of what all the sectors have a

view on the proposal. The acceptance and the rejection of the proposal by the companies would

be helpful in determining the fact that whether the proposal can be put into use or would be

rejected.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Comment Letters

The construction of the draft proposal has led to the draft being open for comments. The

letters that have been forwarded by the selected four companies have been listed in the Appendix

section below. The proposal has been constructed based on the available accounting standards

with respect to the income statement and comprehensive income with the help of which a base

for the updates with respect to the disclosure of the comprehensive income and upgradation on

the income statement would be understood in a better way.

Introduction

The regulations and the related standards of accounting have been the base on which the

current exposure draft has been generated. The draft is based on creating an understanding on the

developments that can be made in the income statement and thereafter a better reporting of the

comprehensive income is possible. The improvements in the accounting standards are possible

with the help of which regulations on the financial transactions are possible and monitoring and

construction of the income statement is possible in an effective manner (Anderson et al., 2016).

These updates are helpful in discovering the errors that are present and accordingly undertake

steps so that these errors can be minimised.

Assessment of exposure draft being helpful in developing the interests of the public

This assignment looks to create an understanding of the views and the comments that

have been given out the four companies that have been chosen and these letters are seen in the

FASB website and therefore assistance from the website has been taken in order to take care of

these issues (Conner, 2016). This assignment therefore undertakes a decisive evaluation of all the

comments provided by the four organizations and thereafter understands their views with the

help of which conclusive results can be obtained so that the new accounting standards would be

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Comment Letters

The construction of the draft proposal has led to the draft being open for comments. The

letters that have been forwarded by the selected four companies have been listed in the Appendix

section below. The proposal has been constructed based on the available accounting standards

with respect to the income statement and comprehensive income with the help of which a base

for the updates with respect to the disclosure of the comprehensive income and upgradation on

the income statement would be understood in a better way.

Introduction

The regulations and the related standards of accounting have been the base on which the

current exposure draft has been generated. The draft is based on creating an understanding on the

developments that can be made in the income statement and thereafter a better reporting of the

comprehensive income is possible. The improvements in the accounting standards are possible

with the help of which regulations on the financial transactions are possible and monitoring and

construction of the income statement is possible in an effective manner (Anderson et al., 2016).

These updates are helpful in discovering the errors that are present and accordingly undertake

steps so that these errors can be minimised.

Assessment of exposure draft being helpful in developing the interests of the public

This assignment looks to create an understanding of the views and the comments that

have been given out the four companies that have been chosen and these letters are seen in the

FASB website and therefore assistance from the website has been taken in order to take care of

these issues (Conner, 2016). This assignment therefore undertakes a decisive evaluation of all the

comments provided by the four organizations and thereafter understands their views with the

help of which conclusive results can be obtained so that the new accounting standards would be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

assessed and their effectiveness would be finalised. Hence, this process of offering the proposal

to the public and thereafter receiving their comments and views are understandable in mitigating

a lot of issues and problems. The other goal of the assignment is to state the method of finalising

the guiding concepts and principles that are associated to the accounting process and this would

create better standards of accounting (Okamoto, 2017). In addition, the evaluation of the

comments in order to have an understanding of the acceptance and rejection by the organizations

in order to gain the final result will be helpful in the development of better standards of

accounting.

The changes that have been proposed in the accounting standards are done in order to

look after the feelings and the sentiments of the organizations with the help of which the

performance of the business can be developed and thereafter the overall business activities would

enhance. Shi et al., (2017) provided a comment that standards and regulations of accounting try

to answer to the ideas and the understandings of the companies and accordingly gather better

results with the help of the comments that have been gathered. FASB gets assistance from these

comments as they are opinions towards the draft proposal and the use of this strategy is effective

enough in creating an better public interests (Hussey, 2017). The comments look to answer to the

changes that are recommended by FASB so that better results can be attained. There numerous

aspects on which the draft has proposed changes and in this manner answering to these questions

can be helpful in looking into the public interests.

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

assessed and their effectiveness would be finalised. Hence, this process of offering the proposal

to the public and thereafter receiving their comments and views are understandable in mitigating

a lot of issues and problems. The other goal of the assignment is to state the method of finalising

the guiding concepts and principles that are associated to the accounting process and this would

create better standards of accounting (Okamoto, 2017). In addition, the evaluation of the

comments in order to have an understanding of the acceptance and rejection by the organizations

in order to gain the final result will be helpful in the development of better standards of

accounting.

The changes that have been proposed in the accounting standards are done in order to

look after the feelings and the sentiments of the organizations with the help of which the

performance of the business can be developed and thereafter the overall business activities would

enhance. Shi et al., (2017) provided a comment that standards and regulations of accounting try

to answer to the ideas and the understandings of the companies and accordingly gather better

results with the help of the comments that have been gathered. FASB gets assistance from these

comments as they are opinions towards the draft proposal and the use of this strategy is effective

enough in creating an better public interests (Hussey, 2017). The comments look to answer to the

changes that are recommended by FASB so that better results can be attained. There numerous

aspects on which the draft has proposed changes and in this manner answering to these questions

can be helpful in looking into the public interests.

5

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Comments provided by the letter of the companies

The assignment is looking to explain the comments and the advises that have been

provided by the companies in order to gather the understanding the ideas and the understandings

of them and accordingly discover the changes that can be made with the help of which effective

level of understandings can be attained (Dyson, 2015). Therefore, the comments that have been

given by the different companies have been listed as follows:

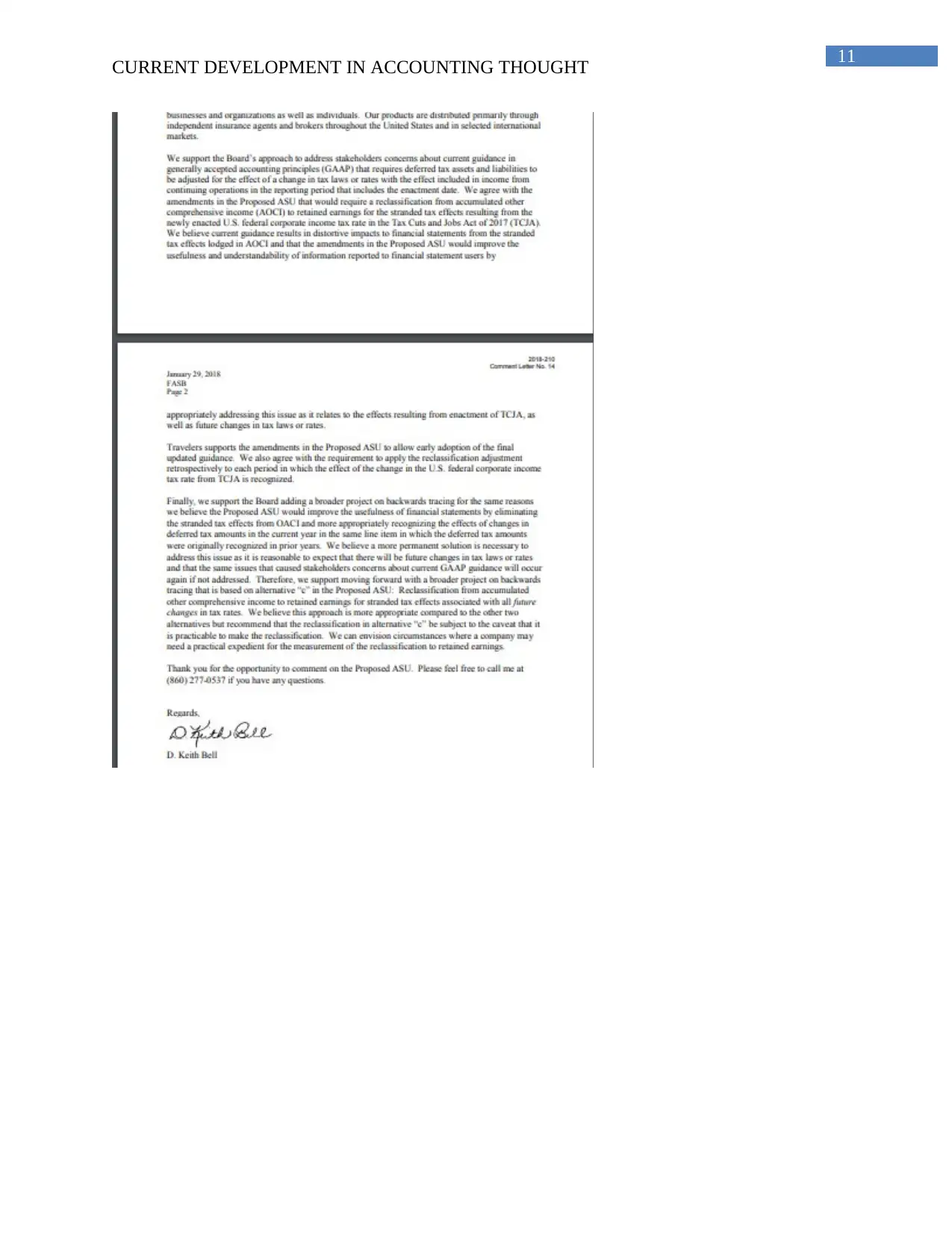

The Travellers Companies Inc

The organzaiiton that has been taken into consideration is associated with the property

and casualty services and products and mainly concentrates on providing insurances. The

opinion that has been given by the firm in their letter has highlighted the fact that they have

agreed to the propositions that have been presented in the draft and especially to the one of

providing assistance to the process of GAAP that would explain the deferred assets and

liabilities. The firm even agrees to the ASU that has been recommended with respect to the

reclassification of the comprehensive income that has been accumulated (Weidner, 2017). The

company therefore agrees to the draft proposal of FASB as this would enhance the operational

activities and therefore agrees to the changes that have been suggested.

Chevron Companies

The company is related to the energy sector and manufactures natural gas and crude oils

mainly. The company has a significant role to play in the development of the global economy.

The proposal that have been presented by FASB has been answered by the company with the

help of the letter provided on their behalf (Cipriano, 2016). The firm has provided feedback on

all the questions and has specifically concentrated on the reclassification of the asset. The letter

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Comments provided by the letter of the companies

The assignment is looking to explain the comments and the advises that have been

provided by the companies in order to gather the understanding the ideas and the understandings

of them and accordingly discover the changes that can be made with the help of which effective

level of understandings can be attained (Dyson, 2015). Therefore, the comments that have been

given by the different companies have been listed as follows:

The Travellers Companies Inc

The organzaiiton that has been taken into consideration is associated with the property

and casualty services and products and mainly concentrates on providing insurances. The

opinion that has been given by the firm in their letter has highlighted the fact that they have

agreed to the propositions that have been presented in the draft and especially to the one of

providing assistance to the process of GAAP that would explain the deferred assets and

liabilities. The firm even agrees to the ASU that has been recommended with respect to the

reclassification of the comprehensive income that has been accumulated (Weidner, 2017). The

company therefore agrees to the draft proposal of FASB as this would enhance the operational

activities and therefore agrees to the changes that have been suggested.

Chevron Companies

The company is related to the energy sector and manufactures natural gas and crude oils

mainly. The company has a significant role to play in the development of the global economy.

The proposal that have been presented by FASB has been answered by the company with the

help of the letter provided on their behalf (Cipriano, 2016). The firm has provided feedback on

all the questions and has specifically concentrated on the reclassification of the asset. The letter

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

has discovered that this company agrees to the propositions as well and even supports the timely

incorporation. The date that is suggested in the draft is even seconded and the firm agrees to the

proposal of reclassification but provides the opinion that the effect of the transformations in the

extent of tax on the foreign ancillaries can lead to the effect on the impact of the stranded taxes.

The Goodyear Tire and Rubber Company

This company is related to the production of tires and other products related to tires and

in accordance to proposal that is constructed by the FASB, the firm does not agree to the process

of reclassification and the demand for the alterations as the company feels that it would lead to a

higher amount for the taxes that are stranded and thereby defeating the intention of the changes.

The firm however, agrees to the process of backward tracing that is recommend by FASB

in the draft as this would take away the effects of the stranded taxes from the constructors of the

financial statements (Xu, & Doupnik 2016).

American Bankers Association

This body has the function of taking care of the operations of banking that is performed

in United States. All the concerns and the issues related to banking are taken care of and thereby

proper banking model can be maintained. The association is happy to be able to able to express

their feelings with respect to this draft and thereafter the association feels that the recommended

process would create a better value in accordance to the comprehensive income and feels that the

earnings that have been attained can misled the investors and therefore have additional pressure

on the management (Kim, 2016). This changes will not be assistive to the banks as in certain

cases the stranded value may have an impact on the degree of capital. Hence, the overall the

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

has discovered that this company agrees to the propositions as well and even supports the timely

incorporation. The date that is suggested in the draft is even seconded and the firm agrees to the

proposal of reclassification but provides the opinion that the effect of the transformations in the

extent of tax on the foreign ancillaries can lead to the effect on the impact of the stranded taxes.

The Goodyear Tire and Rubber Company

This company is related to the production of tires and other products related to tires and

in accordance to proposal that is constructed by the FASB, the firm does not agree to the process

of reclassification and the demand for the alterations as the company feels that it would lead to a

higher amount for the taxes that are stranded and thereby defeating the intention of the changes.

The firm however, agrees to the process of backward tracing that is recommend by FASB

in the draft as this would take away the effects of the stranded taxes from the constructors of the

financial statements (Xu, & Doupnik 2016).

American Bankers Association

This body has the function of taking care of the operations of banking that is performed

in United States. All the concerns and the issues related to banking are taken care of and thereby

proper banking model can be maintained. The association is happy to be able to able to express

their feelings with respect to this draft and thereafter the association feels that the recommended

process would create a better value in accordance to the comprehensive income and feels that the

earnings that have been attained can misled the investors and therefore have additional pressure

on the management (Kim, 2016). This changes will not be assistive to the banks as in certain

cases the stranded value may have an impact on the degree of capital. Hence, the overall the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

proposal states that the association disagrees to the proposal as these proposals can have an

impact on the financial documentation and transactions of the banks.

Proposal significance

The proposal has identified that the changes that have been proposed are vital as the

alterations in the process of creating the income statement and explanation of the comprehensive

income would be assistive in the development of the income statement that can be implemented

and accordingly better outcome would be created.

Conclusion

The outcome that has been discovered from the letters provided by the companies

explains the fact that changes in the proposal draft needs to be undertaken with the help of which

better income statement and explanation of the comprehensive income can be done.

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

proposal states that the association disagrees to the proposal as these proposals can have an

impact on the financial documentation and transactions of the banks.

Proposal significance

The proposal has identified that the changes that have been proposed are vital as the

alterations in the process of creating the income statement and explanation of the comprehensive

income would be assistive in the development of the income statement that can be implemented

and accordingly better outcome would be created.

Conclusion

The outcome that has been discovered from the letters provided by the companies

explains the fact that changes in the proposal draft needs to be undertaken with the help of which

better income statement and explanation of the comprehensive income can be done.

8

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Reference List

Anderson, U. L., Doxey, M. M., Geiger, M. A., Gist, W. E., Janvrin, D. J., & Polinski, P. W.

(2016). Comments by the Auditing Standards Committee of the Auditing Section of the

American Accounting Association on FASB Exposure Draft of Proposed Accounting

Standard Update: Notes to Financial Statements (Topic 235): Assessing Whether

Disclosures Are Material: Participating Committee Members. Current Issues in

Auditing, 10(2), C1-C9.

Cipriano, M. (2016). Bad Will: Why the FASB's Proposed Fix of Goodwill Accounting Will Not

Fix the Goodwill Problem. Journal of Corporate Accounting & Finance, 27(6), 89-92.

Conner, B. (2016). Healthcare not-for-profits: FASB exposure draft highlights flexibility in

financial statement presentation. Healthcare financial management: journal of the

Healthcare Financial Management Association, 70(3), 34-37.

Dyson, R. A. (2015). Commentary on FASB's Proposed Changes to Nonprofit Financial

Statements: Overhaul Falls Short on Usefulness and Practicality. The CPA

Journal, 85(10), 11.

Hussey, R. (2017, May). Leasing of Assets: A Content Analysis of Comment. In GAI

International Academic Conferences Proceedings (p. 23).

Kim, J. H. (2016). Presentation formats of other comprehensive income after accounting

standards update 2011-05. Research in Accounting Regulation, 28(2), 118-122.

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Reference List

Anderson, U. L., Doxey, M. M., Geiger, M. A., Gist, W. E., Janvrin, D. J., & Polinski, P. W.

(2016). Comments by the Auditing Standards Committee of the Auditing Section of the

American Accounting Association on FASB Exposure Draft of Proposed Accounting

Standard Update: Notes to Financial Statements (Topic 235): Assessing Whether

Disclosures Are Material: Participating Committee Members. Current Issues in

Auditing, 10(2), C1-C9.

Cipriano, M. (2016). Bad Will: Why the FASB's Proposed Fix of Goodwill Accounting Will Not

Fix the Goodwill Problem. Journal of Corporate Accounting & Finance, 27(6), 89-92.

Conner, B. (2016). Healthcare not-for-profits: FASB exposure draft highlights flexibility in

financial statement presentation. Healthcare financial management: journal of the

Healthcare Financial Management Association, 70(3), 34-37.

Dyson, R. A. (2015). Commentary on FASB's Proposed Changes to Nonprofit Financial

Statements: Overhaul Falls Short on Usefulness and Practicality. The CPA

Journal, 85(10), 11.

Hussey, R. (2017, May). Leasing of Assets: A Content Analysis of Comment. In GAI

International Academic Conferences Proceedings (p. 23).

Kim, J. H. (2016). Presentation formats of other comprehensive income after accounting

standards update 2011-05. Research in Accounting Regulation, 28(2), 118-122.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Okamoto, N. (2017). Norm entrepreneur lobbying and persuasion: A case study involving the

IASB's modification of an exposure draft. Research in Accounting Regulation, 29(2),

129-138.

Shi, L., Wang, P., & Zhou, N. (2017). Enhanced disclosure of other comprehensive income and

increased usefulness of net income: The implications of Accounting Standards Update

2011–05. Research in Accounting Regulation, 29(2), 139-144.

Weidner, D. J. (2017). New FASB Rules for Leases: A Sarbanes-Oxley Promise

Delivered. Business Lawyer, 72(2), 367.

Xu, Y., & Doupnik, T. (2016). The impact of different types and amounts of guidance on the

implementation of an accounting principle. Research in Accounting Regulation, 28(2),

66-76.

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Okamoto, N. (2017). Norm entrepreneur lobbying and persuasion: A case study involving the

IASB's modification of an exposure draft. Research in Accounting Regulation, 29(2),

129-138.

Shi, L., Wang, P., & Zhou, N. (2017). Enhanced disclosure of other comprehensive income and

increased usefulness of net income: The implications of Accounting Standards Update

2011–05. Research in Accounting Regulation, 29(2), 139-144.

Weidner, D. J. (2017). New FASB Rules for Leases: A Sarbanes-Oxley Promise

Delivered. Business Lawyer, 72(2), 367.

Xu, Y., & Doupnik, T. (2016). The impact of different types and amounts of guidance on the

implementation of an accounting principle. Research in Accounting Regulation, 28(2),

66-76.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Appendix

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

Appendix

11

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

CURRENT DEVELOPMENT IN ACCOUNTING THOUGHT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.