Current Development of Accounting Thoughts: A Comprehensive Report

VerifiedAdded on 2023/03/17

|22

|3157

|62

Report

AI Summary

This report provides an in-depth analysis of current developments in accounting, focusing on two primary areas: the accounting practices of Pioneer Ltd and the exposure draft related to IAS 37. The first part of the report examines the accounting policies of Pioneer Ltd, highlighting issues with asset valuation, adherence to accounting standards, and the application of stakeholder theory. The analysis includes a discussion of the auditor's concerns, the company's response to criticisms, and the implications for stakeholders. The second part of the report focuses on the exposure draft concerning IAS 37, specifically addressing onerous contracts. It explores the proposed amendments, the comments from various organizations such as BDO Network, CPA Australia, and the Canadian Accounting Standards Board, and the overall impact of these changes on accounting practices. The report concludes by summarizing the key findings and implications of these developments in accounting.

Running head: Current Development in Accounting Thoughts

Current Development in Accounting Thoughts

Name of the Student

Name of the University

Author Note

Current Development in Accounting Thoughts

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Current Development of Accounting Thoughts

Table of Contents

Answer to Question 1.................................................................................................................2

Answer No 2:.............................................................................................................................5

Executive Summary...............................................................................................................5

Introduction............................................................................................................................5

Proposal..................................................................................................................................5

Comments to the proposal amendment..................................................................................6

Comment given CPA Australia..............................................................................................8

Comment of Canadian Accounting Standards Board..........................................................11

Comments of the Rio Tinto..................................................................................................14

Conclusion............................................................................................................................17

Reference..............................................................................................................................17

Current Development of Accounting Thoughts

Table of Contents

Answer to Question 1.................................................................................................................2

Answer No 2:.............................................................................................................................5

Executive Summary...............................................................................................................5

Introduction............................................................................................................................5

Proposal..................................................................................................................................5

Comments to the proposal amendment..................................................................................6

Comment given CPA Australia..............................................................................................8

Comment of Canadian Accounting Standards Board..........................................................11

Comments of the Rio Tinto..................................................................................................14

Conclusion............................................................................................................................17

Reference..............................................................................................................................17

2

Current Development of Accounting Thoughts

Answer to Question 1

The accounting system which is been chosen by the Pioneer Ltd is been shown in this

article so that it can show the business accounting information. The article is been published

in 3rd April 2019 which is been shown in the financial review of the company. The company

was following wrong accounting treatment in regards of their business which is been shown

in this article, the company is been based in Australia (Pioneer Credit Limited 2019). It also

show about the auditor and other management review upon the controversial accounting

policy of the company which is been followed in the business.

The company is been based upon Australia and it carry its business operation in

Australia and New Zealand and the company deals in providing different financial services to

the individual of the respective country (Pioneer Credit Limited 2019). The company is one

of the best in its industry and so it has got a very good brand name in the company. The

company is not able to show the proper value of their asset and this article is based upon the

accounting policy. As per the article it can be seen that the company is not able to follow the

proper policy and principle in regards for the preparation of the financial statement as it does

not able to follow the accounting standard properly and it is also been seen that the company

is not able to follow the norms as per the conceptual framework which is been followed by all

the company in the country (Pioneer Credit Limited 2019). So it can be say that the company

is not able to follow the standard properly. The Accounting policy which is been laid in the

Generally Accepted Accounting Policy has said not to be follow the unorthodox accounting

process but it can be seen that the company have followed the same for the valuation of the

financial asset of the company. It can be seen that the company is not able to the accounting

as per the accounting standard and this was also be laid by the auditor of the company.

Current Development of Accounting Thoughts

Answer to Question 1

The accounting system which is been chosen by the Pioneer Ltd is been shown in this

article so that it can show the business accounting information. The article is been published

in 3rd April 2019 which is been shown in the financial review of the company. The company

was following wrong accounting treatment in regards of their business which is been shown

in this article, the company is been based in Australia (Pioneer Credit Limited 2019). It also

show about the auditor and other management review upon the controversial accounting

policy of the company which is been followed in the business.

The company is been based upon Australia and it carry its business operation in

Australia and New Zealand and the company deals in providing different financial services to

the individual of the respective country (Pioneer Credit Limited 2019). The company is one

of the best in its industry and so it has got a very good brand name in the company. The

company is not able to show the proper value of their asset and this article is based upon the

accounting policy. As per the article it can be seen that the company is not able to follow the

proper policy and principle in regards for the preparation of the financial statement as it does

not able to follow the accounting standard properly and it is also been seen that the company

is not able to follow the norms as per the conceptual framework which is been followed by all

the company in the country (Pioneer Credit Limited 2019). So it can be say that the company

is not able to follow the standard properly. The Accounting policy which is been laid in the

Generally Accepted Accounting Policy has said not to be follow the unorthodox accounting

process but it can be seen that the company have followed the same for the valuation of the

financial asset of the company. It can be seen that the company is not able to the accounting

as per the accounting standard and this was also be laid by the auditor of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Current Development of Accounting Thoughts

The auditor of the company is also worried about the financial statement preparation

of the company as it is not been mention properly and also not as per accounting standard. It

can be said that the company have a conflict with the conceptual framework of the country as

the management have told that they will not able to change their accounting treatment which

is been followed by the company in the financial statement (Pioneer Credit Limited 2019).

The employee of the company is able to give the whistle blower and able to gave the more

information of the company. As per the accounting standard the company have to do change

in the valuation policies than only it will able to make the proper accounting statement of the

company.

The main business which the company is having is the purchase of the impaired book

and then all they are the also very effective in regards of the collection of the money from the

debtors. The price which is been agreed between the seller and the buyer so it is been valued

for the debt portfolios (Pioneer Credit Limited 2019). PWC was the auditor of the company

and as per the auditor they cannot able to get proper information about the company financial

statement so they are not able o judge whether the financial statement of the company is

showing fair value or not. So as per auditor as they were not able to get sufficient information

so they gave the company a qualified report. As per ASIC the company should value of their

asset upon amortised cost but they have valued the same upon the fair value of accounting so

it is been consider as wrong accounting treatment. As per the management communication

they are also not ready to change the policy also this make the accounting more problematic.

As per of the company accounting policy so this been consider as problem as a

auditor report also gave them qualified report so as a result it have to lose its market share

value in the stock exchange. As per the wrong accounting the company is losing all its

investors and also they are not able to hold their share price as it was losing rapidly. In last 12

months the company has lost 46% of share so it is a big problem for the company. It is the

Current Development of Accounting Thoughts

The auditor of the company is also worried about the financial statement preparation

of the company as it is not been mention properly and also not as per accounting standard. It

can be said that the company have a conflict with the conceptual framework of the country as

the management have told that they will not able to change their accounting treatment which

is been followed by the company in the financial statement (Pioneer Credit Limited 2019).

The employee of the company is able to give the whistle blower and able to gave the more

information of the company. As per the accounting standard the company have to do change

in the valuation policies than only it will able to make the proper accounting statement of the

company.

The main business which the company is having is the purchase of the impaired book

and then all they are the also very effective in regards of the collection of the money from the

debtors. The price which is been agreed between the seller and the buyer so it is been valued

for the debt portfolios (Pioneer Credit Limited 2019). PWC was the auditor of the company

and as per the auditor they cannot able to get proper information about the company financial

statement so they are not able o judge whether the financial statement of the company is

showing fair value or not. So as per auditor as they were not able to get sufficient information

so they gave the company a qualified report. As per ASIC the company should value of their

asset upon amortised cost but they have valued the same upon the fair value of accounting so

it is been consider as wrong accounting treatment. As per the management communication

they are also not ready to change the policy also this make the accounting more problematic.

As per of the company accounting policy so this been consider as problem as a

auditor report also gave them qualified report so as a result it have to lose its market share

value in the stock exchange. As per the wrong accounting the company is losing all its

investors and also they are not able to hold their share price as it was losing rapidly. In last 12

months the company has lost 46% of share so it is a big problem for the company. It is the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Current Development of Accounting Thoughts

duty of the company to provide sufficient amount of the information in the financial

statement so that it will help the user to get more understandable information of the company

financial statement.

As per the case in the article it can be said that the stakeholder theory will most

appropriate for the situation as the stakeholder also consist of the worker and the employee of

the organization. If anyone is been affected by the decision of the company than there are

consider as stakeholder as per the stakeholder theory (Pioneer Credit Limited 2019). So it is

the duty of the company to consider this while taking important decision in the activities of

the business. Stakeholder should also be consider as main part of the organization as it should

not able to consider only the interest related to the stakeholders. It should treat all the groups

equally and should take their decision accordingly. As per the article it clearly shows that the

company is not able to give appropriate information and also not able to follow proper

accounting standard so it is a problem for all the stakeholder of the company. The company

management also not able to maintain their policy as per the framework so it should be taken

into consideration as per the stakeholder theory

The article show about the Pioneer ltd policies and how it is not able to show the same

so if the company is able to follow the entire accounting standard so it will able to make more

accurate financial statement and it will also able to show proper report as per the conceptual

framework policy of the accounting standard. The company have to suffer from penalty and

also it can go for the dissolution if the company is not able to change the valuation as per the

accounting standard and conceptual framework. The company should follow the stakeholder

theory and should able to consider the client also in the financial decision of the company.

Current Development of Accounting Thoughts

duty of the company to provide sufficient amount of the information in the financial

statement so that it will help the user to get more understandable information of the company

financial statement.

As per the case in the article it can be said that the stakeholder theory will most

appropriate for the situation as the stakeholder also consist of the worker and the employee of

the organization. If anyone is been affected by the decision of the company than there are

consider as stakeholder as per the stakeholder theory (Pioneer Credit Limited 2019). So it is

the duty of the company to consider this while taking important decision in the activities of

the business. Stakeholder should also be consider as main part of the organization as it should

not able to consider only the interest related to the stakeholders. It should treat all the groups

equally and should take their decision accordingly. As per the article it clearly shows that the

company is not able to give appropriate information and also not able to follow proper

accounting standard so it is a problem for all the stakeholder of the company. The company

management also not able to maintain their policy as per the framework so it should be taken

into consideration as per the stakeholder theory

The article show about the Pioneer ltd policies and how it is not able to show the same

so if the company is able to follow the entire accounting standard so it will able to make more

accurate financial statement and it will also able to show proper report as per the conceptual

framework policy of the accounting standard. The company have to suffer from penalty and

also it can go for the dissolution if the company is not able to change the valuation as per the

accounting standard and conceptual framework. The company should follow the stakeholder

theory and should able to consider the client also in the financial decision of the company.

5

Current Development of Accounting Thoughts

Answer No 2:

Executive Summary

The report show about the exposure draft which is related IAS 37. It show about the

changes which are came by IASB and also the review which are been given by different

company upon the change which are done by IASB.

Introduction

This part is been based upon the analysis of the exposure draft that is been issued in

the International Accounting Standard Board which is been consider as per the public for the

business reporting framework (AASB Standard 2014). The draft is been based upon the IAS

37 which is been related to the Provision, Contingent Liabilities and the Current Asset. It

shows about the details in regard of the Onerous Contracts – Cost of Fulfilling a contract

(Buchanan 2019, 1 April). It show the for and against of the recommendations that is been

shown in the exposure draft. It also shows about the different theories which are there in the

draft.

Proposal

The contract which show the unavoidable cost which is been there in the exceed of

the economic benefit is been treated as Onerous Contract. As per the IAS 37 it also discuss

about the contract portrays unavoidable cost as it is the least of the payment which is been

made on the penalty which have arise for the non-performance of the contract and cost spend

upon the performance of the contract (Buchanan 2019, 1 April). It is not able to show the

valuation of the cost for the fulfilment of the contract in the business. The main point which

is shown in the article is about the cost of the contract which are related to the construction.

The issue which can be shown in the IAS 37 is the identification of the costs. It can be said

that the company use different cost treatment and it also differ from one company to another

Current Development of Accounting Thoughts

Answer No 2:

Executive Summary

The report show about the exposure draft which is related IAS 37. It show about the

changes which are came by IASB and also the review which are been given by different

company upon the change which are done by IASB.

Introduction

This part is been based upon the analysis of the exposure draft that is been issued in

the International Accounting Standard Board which is been consider as per the public for the

business reporting framework (AASB Standard 2014). The draft is been based upon the IAS

37 which is been related to the Provision, Contingent Liabilities and the Current Asset. It

shows about the details in regard of the Onerous Contracts – Cost of Fulfilling a contract

(Buchanan 2019, 1 April). It show the for and against of the recommendations that is been

shown in the exposure draft. It also shows about the different theories which are there in the

draft.

Proposal

The contract which show the unavoidable cost which is been there in the exceed of

the economic benefit is been treated as Onerous Contract. As per the IAS 37 it also discuss

about the contract portrays unavoidable cost as it is the least of the payment which is been

made on the penalty which have arise for the non-performance of the contract and cost spend

upon the performance of the contract (Buchanan 2019, 1 April). It is not able to show the

valuation of the cost for the fulfilment of the contract in the business. The main point which

is shown in the article is about the cost of the contract which are related to the construction.

The issue which can be shown in the IAS 37 is the identification of the costs. It can be said

that the company use different cost treatment and it also differ from one company to another

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Current Development of Accounting Thoughts

so as per the understanding the user it should provide proper clarification should be given by

the company.

It should be said they there should be changes in the onerous contract so that it can

able to give proper framework which is been followed by the companies in different country

so it should be changed (Deegan 2014). The changes which are been done the committee

help to give details of the definition of the onerous contract and also how the company can

able to measure the contract so that it can able to fulfil the requirement of the contract of the

business.

Comments to the proposal amendment

Comment of BPO Network

The changes which are been suggested by the IASB, is not able to satisfy the

expectation of the BDO network so it made the comment upon it. The reason of the same is

been shown below:

o The changes are not appropriate as it should take into consideration all the cost which

are been spend by the company as there are directly related to the coast estimation of

the contract.

o The non-incremental cost which is to be considering in future are included as onerous

contract. So the changes which are been done in IASB is not able to take the operating

losses which are done by the company in future so it is not a proper change which is

done by IASB. The changes are not appropriate as it is not real about the provision

which is related to cost of the contract.

o The amendments which are been made is not able to fulfil the definition of the

onerous contract. As it show about the unavoidable cost as it should not be able to

record the same.

Current Development of Accounting Thoughts

so as per the understanding the user it should provide proper clarification should be given by

the company.

It should be said they there should be changes in the onerous contract so that it can

able to give proper framework which is been followed by the companies in different country

so it should be changed (Deegan 2014). The changes which are been done the committee

help to give details of the definition of the onerous contract and also how the company can

able to measure the contract so that it can able to fulfil the requirement of the contract of the

business.

Comments to the proposal amendment

Comment of BPO Network

The changes which are been suggested by the IASB, is not able to satisfy the

expectation of the BDO network so it made the comment upon it. The reason of the same is

been shown below:

o The changes are not appropriate as it should take into consideration all the cost which

are been spend by the company as there are directly related to the coast estimation of

the contract.

o The non-incremental cost which is to be considering in future are included as onerous

contract. So the changes which are been done in IASB is not able to take the operating

losses which are done by the company in future so it is not a proper change which is

done by IASB. The changes are not appropriate as it is not real about the provision

which is related to cost of the contract.

o The amendments which are been made is not able to fulfil the definition of the

onerous contract. As it show about the unavoidable cost as it should not be able to

record the same.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Current Development of Accounting Thoughts

Current Development of Accounting Thoughts

8

Current Development of Accounting Thoughts

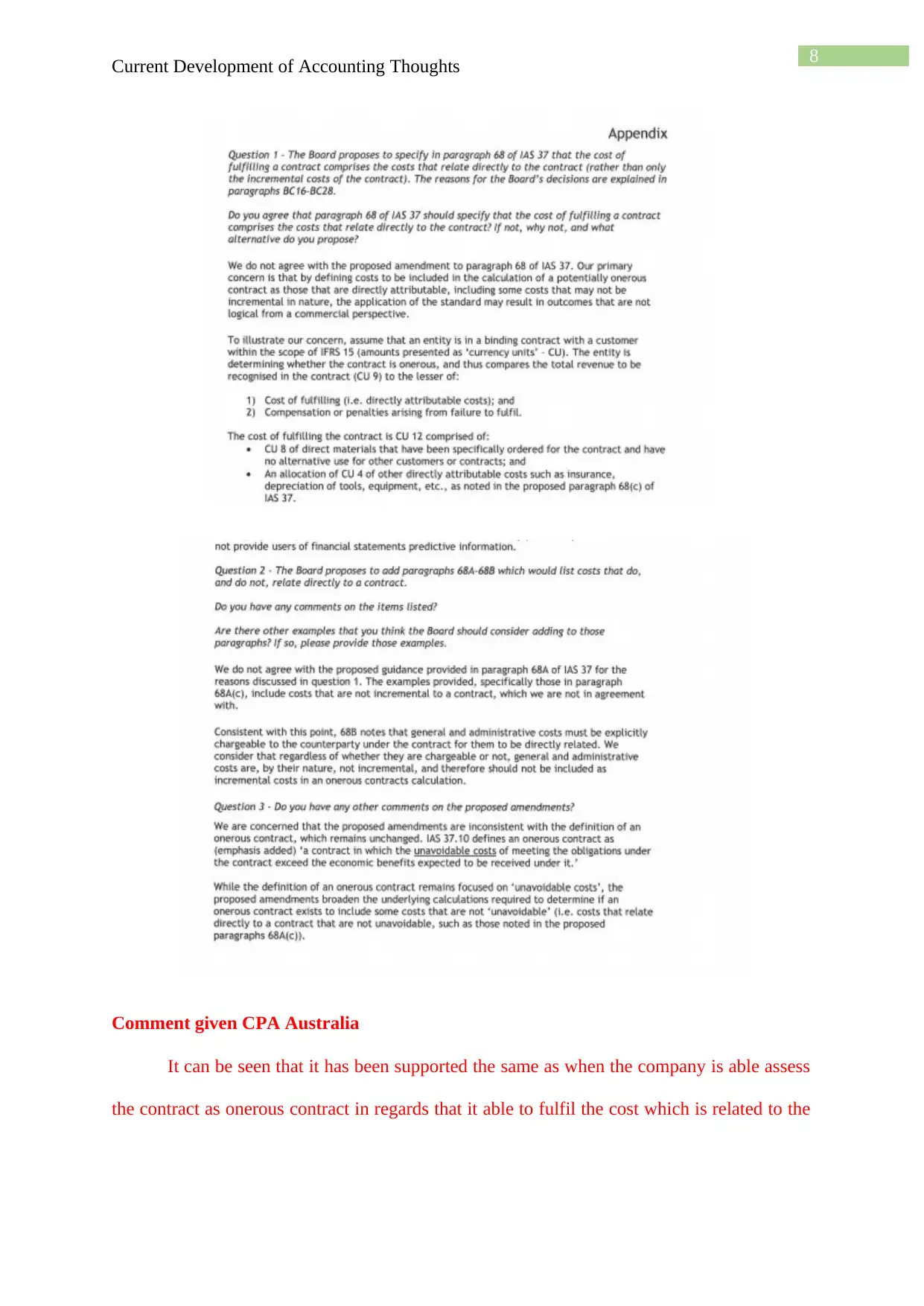

Comment given CPA Australia

It can be seen that it has been supported the same as when the company is able assess

the contract as onerous contract in regards that it able to fulfil the cost which is related to the

Current Development of Accounting Thoughts

Comment given CPA Australia

It can be seen that it has been supported the same as when the company is able assess

the contract as onerous contract in regards that it able to fulfil the cost which is related to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Current Development of Accounting Thoughts

contract as per the incremental cost that is should be consider initially for the purpose of the

analysing of the same. The reason for the same is been shown below:

o It able to satisfy the cost as it shows about the onerous contract as it is been directly

related to the contract and not only the incremental contract of the same. It show that

due to this reason it will able to give an proper accounting and able to give proper

report of the same.

o It is not able to agreed about the changes which are there in the paragraph 68B as the

charges of the general and administrative cost are not able to show whether they are

as it cannot able to determine the cost related or not.

Current Development of Accounting Thoughts

contract as per the incremental cost that is should be consider initially for the purpose of the

analysing of the same. The reason for the same is been shown below:

o It able to satisfy the cost as it shows about the onerous contract as it is been directly

related to the contract and not only the incremental contract of the same. It show that

due to this reason it will able to give an proper accounting and able to give proper

report of the same.

o It is not able to agreed about the changes which are there in the paragraph 68B as the

charges of the general and administrative cost are not able to show whether they are

as it cannot able to determine the cost related or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Current Development of Accounting Thoughts

Current Development of Accounting Thoughts

11

Current Development of Accounting Thoughts

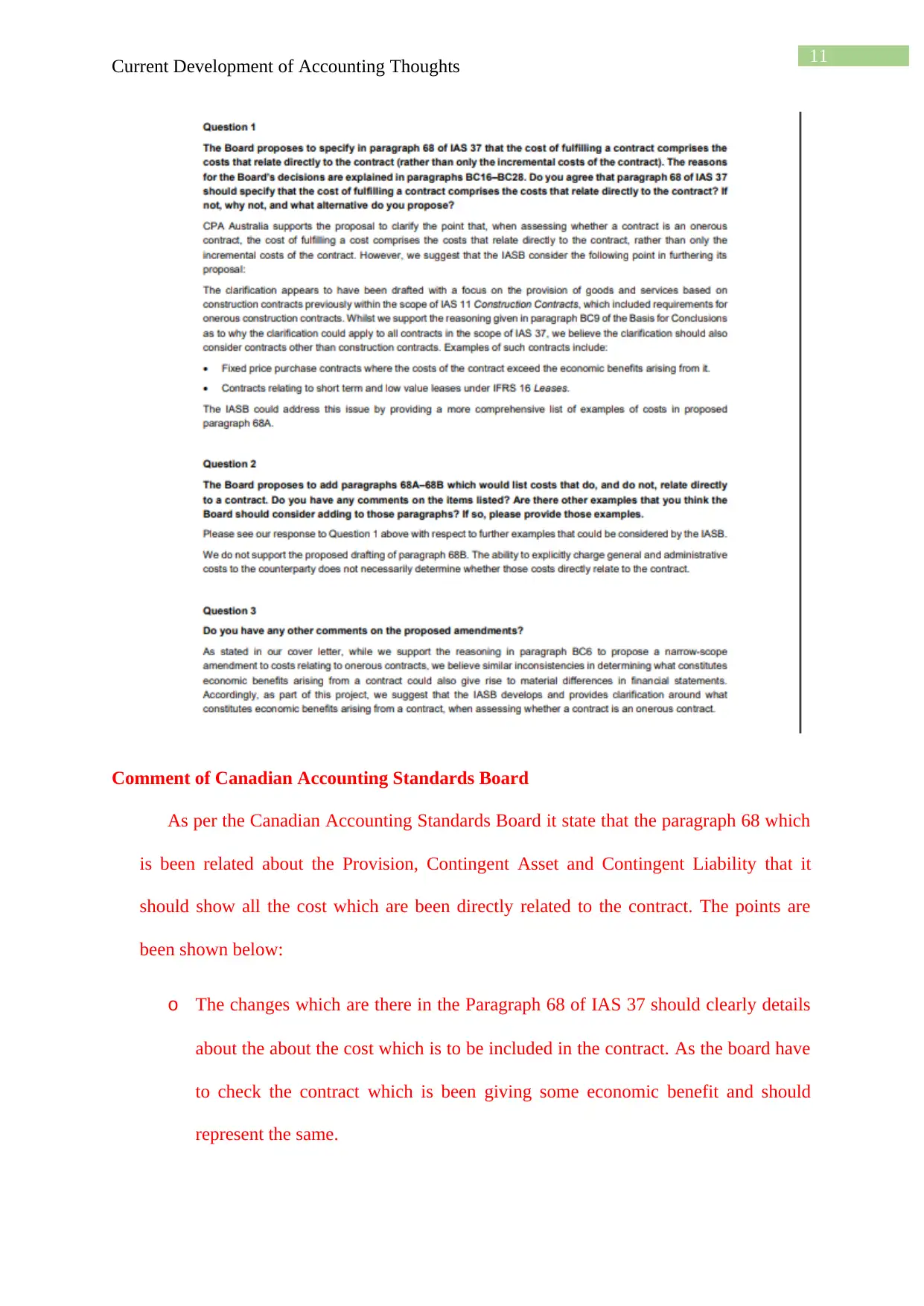

Comment of Canadian Accounting Standards Board

As per the Canadian Accounting Standards Board it state that the paragraph 68 which

is been related about the Provision, Contingent Asset and Contingent Liability that it

should show all the cost which are been directly related to the contract. The points are

been shown below:

o The changes which are there in the Paragraph 68 of IAS 37 should clearly details

about the about the cost which is to be included in the contract. As the board have

to check the contract which is been giving some economic benefit and should

represent the same.

Current Development of Accounting Thoughts

Comment of Canadian Accounting Standards Board

As per the Canadian Accounting Standards Board it state that the paragraph 68 which

is been related about the Provision, Contingent Asset and Contingent Liability that it

should show all the cost which are been directly related to the contract. The points are

been shown below:

o The changes which are there in the Paragraph 68 of IAS 37 should clearly details

about the about the cost which is to be included in the contract. As the board have

to check the contract which is been giving some economic benefit and should

represent the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.