Analysis of Development and Changes in the Oil and Gas Retail Industry

VerifiedAdded on 2020/01/21

|19

|4934

|118

Report

AI Summary

This report provides a comprehensive analysis of the development and recent trends within the oil and gas retail industry, focusing on the UK market. It examines the significant changes in the supply chain, including the closure of petrol filling stations and the rise of supermarket ownership. The report delves into the impact of government and regulatory policies, fiscal drivers, and environmental standards on the industry. It also explores the influence of the North Sea oil production decline, distribution, storage, transportation, and technological advancements. Furthermore, the report highlights changes in buyer behavior, recent trends in refineries, and the competitive pressures faced by traditional oil suppliers. The study concludes with an overview of the changing landscape and the factors shaping the future of the oil and gas retail sector.

DEVELOPMENT IN OIL AND GAS

RETAIL INDUSTRY

RETAIL INDUSTRY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

1.0 INTRODUCTION.....................................................................................................................4

2.0 RECENT TRENDS AND CHANGES WITHIN SUPPLY CHAIN WITHIN THE UK .......4

Recent changes in refinery..........................................................................................................8

3.0 CHANGES IN THE OWNERSHIP OF PETROL SUPPLIERS..............................................8

4.0 CHANGES IN BUYER BEHAVIOUR ................................................................................13

Recent trends in distribution.....................................................................................................14

5.0 IMPACT OF TECHNOLOGY ...............................................................................................14

6.0 CONCLUSION .......................................................................................................................15

REFERENCES..............................................................................................................................16

1.0 INTRODUCTION.....................................................................................................................4

2.0 RECENT TRENDS AND CHANGES WITHIN SUPPLY CHAIN WITHIN THE UK .......4

Recent changes in refinery..........................................................................................................8

3.0 CHANGES IN THE OWNERSHIP OF PETROL SUPPLIERS..............................................8

4.0 CHANGES IN BUYER BEHAVIOUR ................................................................................13

Recent trends in distribution.....................................................................................................14

5.0 IMPACT OF TECHNOLOGY ...............................................................................................14

6.0 CONCLUSION .......................................................................................................................15

REFERENCES..............................................................................................................................16

ILLUSTRATION INDEX

Illustration 1: North Sea Production................................................................................................6

Illustration 2: Declining of PFS in past decades..............................................................................9

Illustration 3: Asda PFS.................................................................................................................11

Illustration 4: Rising of petrol prices of different companies........................................................12

Illustration 5: Total number of PFS and total fuel volumes...........................................................13

Illustration 1: North Sea Production................................................................................................6

Illustration 2: Declining of PFS in past decades..............................................................................9

Illustration 3: Asda PFS.................................................................................................................11

Illustration 4: Rising of petrol prices of different companies........................................................12

Illustration 5: Total number of PFS and total fuel volumes...........................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.0 INTRODUCTION

In the current era of globalization, the future of oil and gas industry has changed over

time. To further elaborate, there have been recent changes and trends in the UK supply chain

downstream market which results into closing of petrol filling stations. According to Chorley

(2013), the closure of Petrol filling stations is causing a negative impact on consumers because

this will increase the minimum driving time to reach at the nearest forecourts due to lack of

options available. There may even be adverse effects of competition effects in certain areas like

customers may have to pay higher prices due to reduced options in the substitutes available in

between different petrol stations. Another recent trend is the ownership of major oil filling

station i.e. British Petroleum (BP) and Shell and now supermarkets such as Tesco, Sainsbury and

Asda are opening their petrol filling stations in the United Kingdom (Byrne, 2014). It has been

identified that the oil price per barrel is the lowest as it has ever been.

2.0 RECENT TRENDS AND CHANGES WITHIN SUPPLY CHAIN

WITHIN THE UK

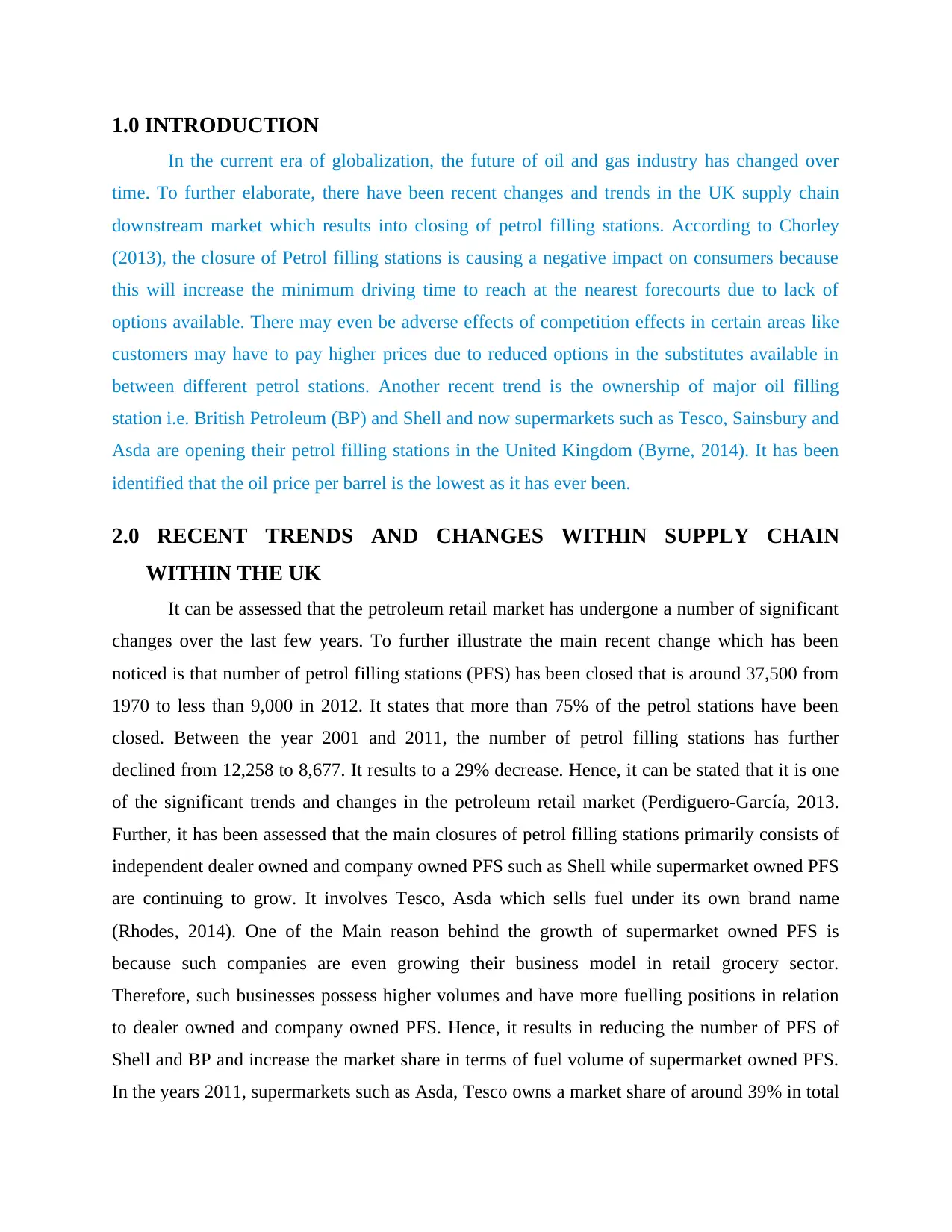

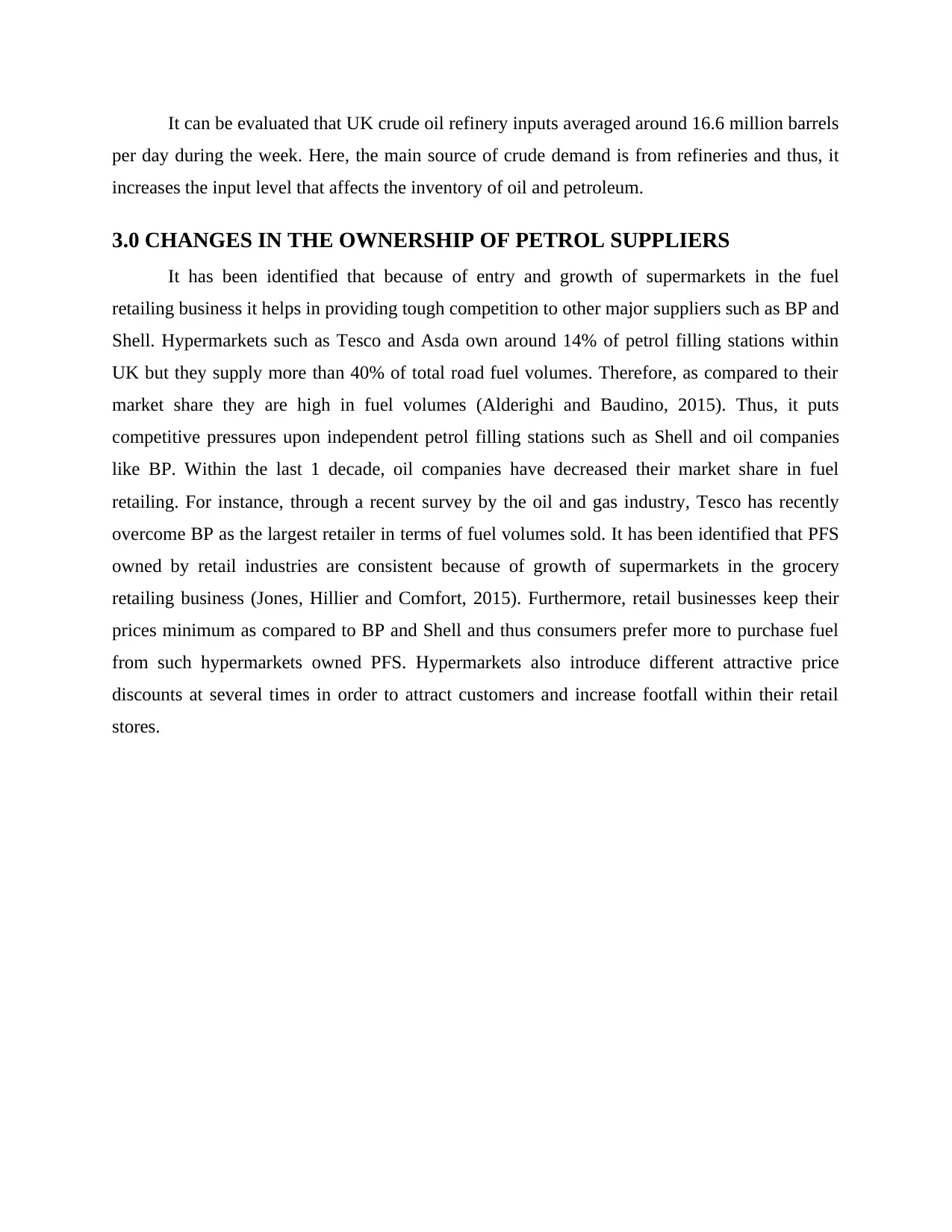

It can be assessed that the petroleum retail market has undergone a number of significant

changes over the last few years. To further illustrate the main recent change which has been

noticed is that number of petrol filling stations (PFS) has been closed that is around 37,500 from

1970 to less than 9,000 in 2012. It states that more than 75% of the petrol stations have been

closed. Between the year 2001 and 2011, the number of petrol filling stations has further

declined from 12,258 to 8,677. It results to a 29% decrease. Hence, it can be stated that it is one

of the significant trends and changes in the petroleum retail market (Perdiguero-García, 2013.

Further, it has been assessed that the main closures of petrol filling stations primarily consists of

independent dealer owned and company owned PFS such as Shell while supermarket owned PFS

are continuing to grow. It involves Tesco, Asda which sells fuel under its own brand name

(Rhodes, 2014). One of the Main reason behind the growth of supermarket owned PFS is

because such companies are even growing their business model in retail grocery sector.

Therefore, such businesses possess higher volumes and have more fuelling positions in relation

to dealer owned and company owned PFS. Hence, it results in reducing the number of PFS of

Shell and BP and increase the market share in terms of fuel volume of supermarket owned PFS.

In the years 2011, supermarkets such as Asda, Tesco owns a market share of around 39% in total

In the current era of globalization, the future of oil and gas industry has changed over

time. To further elaborate, there have been recent changes and trends in the UK supply chain

downstream market which results into closing of petrol filling stations. According to Chorley

(2013), the closure of Petrol filling stations is causing a negative impact on consumers because

this will increase the minimum driving time to reach at the nearest forecourts due to lack of

options available. There may even be adverse effects of competition effects in certain areas like

customers may have to pay higher prices due to reduced options in the substitutes available in

between different petrol stations. Another recent trend is the ownership of major oil filling

station i.e. British Petroleum (BP) and Shell and now supermarkets such as Tesco, Sainsbury and

Asda are opening their petrol filling stations in the United Kingdom (Byrne, 2014). It has been

identified that the oil price per barrel is the lowest as it has ever been.

2.0 RECENT TRENDS AND CHANGES WITHIN SUPPLY CHAIN

WITHIN THE UK

It can be assessed that the petroleum retail market has undergone a number of significant

changes over the last few years. To further illustrate the main recent change which has been

noticed is that number of petrol filling stations (PFS) has been closed that is around 37,500 from

1970 to less than 9,000 in 2012. It states that more than 75% of the petrol stations have been

closed. Between the year 2001 and 2011, the number of petrol filling stations has further

declined from 12,258 to 8,677. It results to a 29% decrease. Hence, it can be stated that it is one

of the significant trends and changes in the petroleum retail market (Perdiguero-García, 2013.

Further, it has been assessed that the main closures of petrol filling stations primarily consists of

independent dealer owned and company owned PFS such as Shell while supermarket owned PFS

are continuing to grow. It involves Tesco, Asda which sells fuel under its own brand name

(Rhodes, 2014). One of the Main reason behind the growth of supermarket owned PFS is

because such companies are even growing their business model in retail grocery sector.

Therefore, such businesses possess higher volumes and have more fuelling positions in relation

to dealer owned and company owned PFS. Hence, it results in reducing the number of PFS of

Shell and BP and increase the market share in terms of fuel volume of supermarket owned PFS.

In the years 2011, supermarkets such as Asda, Tesco owns a market share of around 39% in total

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

fuel volumes sold while there share in holding number of petrol filling stations was only 15%

(Da Silva and et. al., 2014).

3.0 Impact of Government and regulatory policies

It can be stated that UK government develops different regulatory policies for the supply

of oil and gas reserves. However, through development of such policies, it affects the closing of

petrol filling stations so that its number would decrease up to a great extent. Government

develops legislation in order to provide license to various hypermarkets in order to start their

independent PFS and thus, to provide oil to consumers at low and attractive prices. It can be

assessed that government policy and regulations have an effective impact on PFS businesses and

are also a key driver for individual behaviour and investment needs. It also involves various

government related drivers that have been grouped into fiscal drivers, environmental and safety

standards and various other regulatory policies (Polemis and Fotis, 2014).

Fiscal drivers- It involves the main fiscal driver which is tax that influences the PFS

businesses such as Fuel Duty, VAT and Corporation tax. Thus, it affects the PFS business

in many ways (Byrne, 2014).

1. Fuel Duty- Oil and gas businesses are facing issues in relation to fuel duty and Vat that is

currently more than 60% of the final retail price. However, fuel duty is currently 57.95ppl

for both petrol and diesel while VAT is charged at 20%. However, the impact of fuel duty

and Vat upon different types of PFS owners differs on payment terms that independent

dealers and hypermarkets are subject to (Valadkhani, Smyth and Vahid, 2015).

2. Corporation tax- Here, it can be evaluated that the minimum rate of corporation tax has

been minimized from 28% in 2010 to 23% in 2013. Businesses ho make profits less that

Pound 300,000 every year which is required to pay the lower tax (Rhodes, 2014).

Environmental and safety policy- It is essential for PFS owners to develop

environmental and safety policy that is given in the characteristics of petroleum products.

However, it is essential for the industrial participants to develop the environmental safety

policies with regard to PFS so that environment can be protected (Zlatcu, Kubinschi and

Barnea, 2015). Other regulatory policies- Here, it involves planning system which is essential to

protect the retailers in order to acquire development of oil and gas business so that the

best results can be attained. However, a supermarket can build new PFS at the site of

(Da Silva and et. al., 2014).

3.0 Impact of Government and regulatory policies

It can be stated that UK government develops different regulatory policies for the supply

of oil and gas reserves. However, through development of such policies, it affects the closing of

petrol filling stations so that its number would decrease up to a great extent. Government

develops legislation in order to provide license to various hypermarkets in order to start their

independent PFS and thus, to provide oil to consumers at low and attractive prices. It can be

assessed that government policy and regulations have an effective impact on PFS businesses and

are also a key driver for individual behaviour and investment needs. It also involves various

government related drivers that have been grouped into fiscal drivers, environmental and safety

standards and various other regulatory policies (Polemis and Fotis, 2014).

Fiscal drivers- It involves the main fiscal driver which is tax that influences the PFS

businesses such as Fuel Duty, VAT and Corporation tax. Thus, it affects the PFS business

in many ways (Byrne, 2014).

1. Fuel Duty- Oil and gas businesses are facing issues in relation to fuel duty and Vat that is

currently more than 60% of the final retail price. However, fuel duty is currently 57.95ppl

for both petrol and diesel while VAT is charged at 20%. However, the impact of fuel duty

and Vat upon different types of PFS owners differs on payment terms that independent

dealers and hypermarkets are subject to (Valadkhani, Smyth and Vahid, 2015).

2. Corporation tax- Here, it can be evaluated that the minimum rate of corporation tax has

been minimized from 28% in 2010 to 23% in 2013. Businesses ho make profits less that

Pound 300,000 every year which is required to pay the lower tax (Rhodes, 2014).

Environmental and safety policy- It is essential for PFS owners to develop

environmental and safety policy that is given in the characteristics of petroleum products.

However, it is essential for the industrial participants to develop the environmental safety

policies with regard to PFS so that environment can be protected (Zlatcu, Kubinschi and

Barnea, 2015). Other regulatory policies- Here, it involves planning system which is essential to

protect the retailers in order to acquire development of oil and gas business so that the

best results can be attained. However, a supermarket can build new PFS at the site of

supermarket store and the planning process does not consider the existing availability and

choice of PFS in the particular area (Da Silva and et. al., 2014).

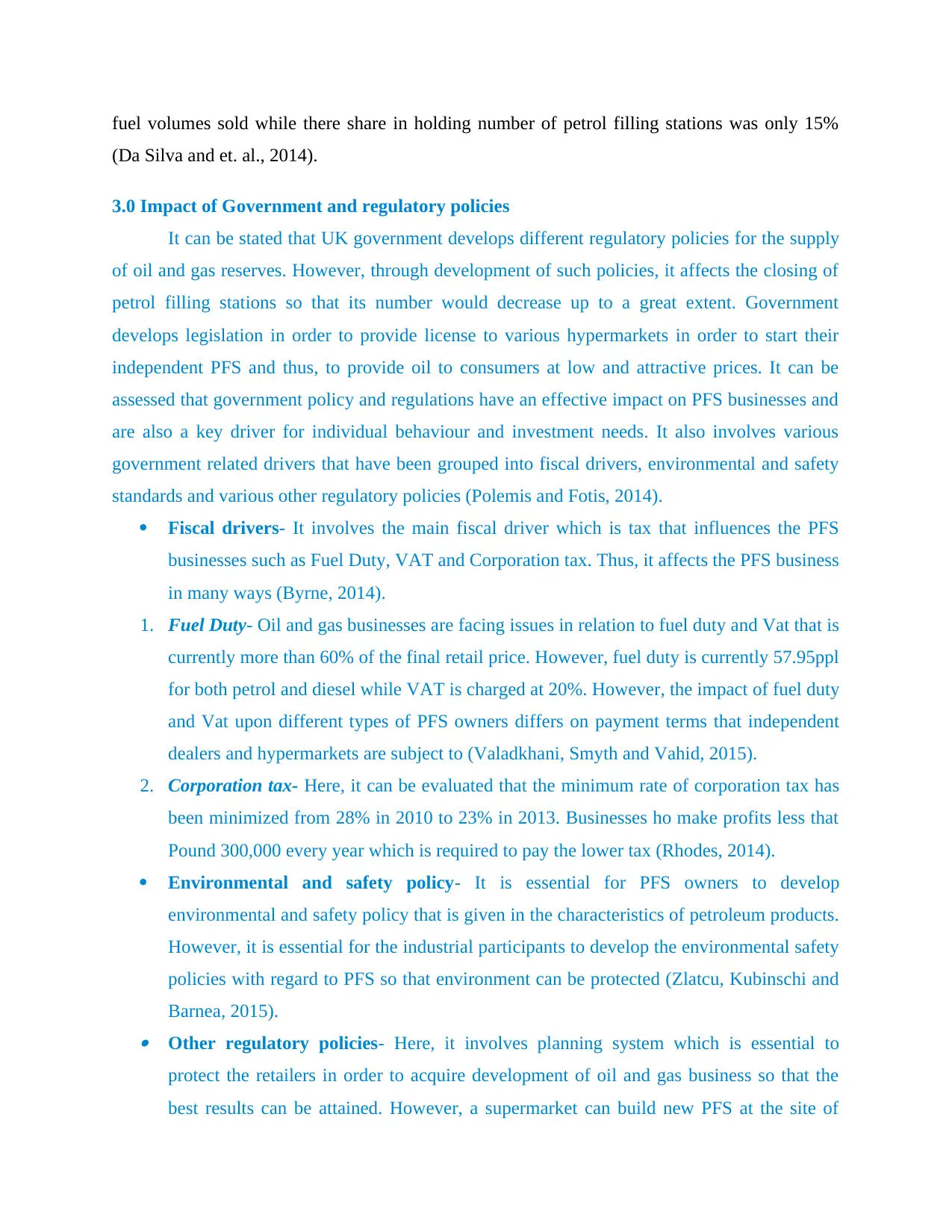

Impact of North Sea

It can be assessed that North Sea oil fields are carrying out losses of money for every

barrel they produce. Further, in future exploration, investment decreases thousands of jobs

because of fall in global oil prices. It can be stated that the energy market in the UK helps in

carrying out different factors such as supply side, shaping the market and shaping the UK's

energy mix. North seas oil and gas output is declining and thus, government is required to look

for increasing output and have adopted the proposals in order to supply the products. Further,

shaping the market is a long term shift in the UK's energy mix. It helps in sharing total energy

demand provided by electricity and gas that helps in growing the role of manufacturing in the

economy which has declined. Moreover, UK's energy mix states that government policy involves

the Climate Change Act 2008 and Energy Act 2013 (Gunn and Mont, 2014).

Illustration 1: North Sea Production

(Source: Rhodes, 2014)

choice of PFS in the particular area (Da Silva and et. al., 2014).

Impact of North Sea

It can be assessed that North Sea oil fields are carrying out losses of money for every

barrel they produce. Further, in future exploration, investment decreases thousands of jobs

because of fall in global oil prices. It can be stated that the energy market in the UK helps in

carrying out different factors such as supply side, shaping the market and shaping the UK's

energy mix. North seas oil and gas output is declining and thus, government is required to look

for increasing output and have adopted the proposals in order to supply the products. Further,

shaping the market is a long term shift in the UK's energy mix. It helps in sharing total energy

demand provided by electricity and gas that helps in growing the role of manufacturing in the

economy which has declined. Moreover, UK's energy mix states that government policy involves

the Climate Change Act 2008 and Energy Act 2013 (Gunn and Mont, 2014).

Illustration 1: North Sea Production

(Source: Rhodes, 2014)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Source: BBC News, 2015)

Above figure signifies that there is considerable amount of downfall in the production of

oil and gas barrel from North Sea in recent time.

Low oil prices are affecting PFS supply

Here, the impact of falling oil prices is that it enhances the visibility in the global

economy. However, the drop in oil prices affect the PFS supply which shows modest global

recoveries as it benefits the oil importers in order to provide economic and financial benefits

(Polemis and Fotis, 2014).

4.0 Distribution, storage and transportation

Distribution, storage and transportation are the major factors that influence the supply

within UK as it is essential for oil companies to make effective distribution channel so that

products can be delivered to consumers effectively and efficiently. Also, storage is another factor

that is essential for companies to store the crude oil and supply to the customers whenever

required. Another challenge faced by UK oil and gas retail industry in relation to independent

dealers continues to face pressure on their business models. However, fuel suppliers such as BP

and Shell faces competition from supermarkets and up to a great extent from company owned

sites they try to provide competitive prices to attract consumers (Gunn and Mont, 2014).

Above figure signifies that there is considerable amount of downfall in the production of

oil and gas barrel from North Sea in recent time.

Low oil prices are affecting PFS supply

Here, the impact of falling oil prices is that it enhances the visibility in the global

economy. However, the drop in oil prices affect the PFS supply which shows modest global

recoveries as it benefits the oil importers in order to provide economic and financial benefits

(Polemis and Fotis, 2014).

4.0 Distribution, storage and transportation

Distribution, storage and transportation are the major factors that influence the supply

within UK as it is essential for oil companies to make effective distribution channel so that

products can be delivered to consumers effectively and efficiently. Also, storage is another factor

that is essential for companies to store the crude oil and supply to the customers whenever

required. Another challenge faced by UK oil and gas retail industry in relation to independent

dealers continues to face pressure on their business models. However, fuel suppliers such as BP

and Shell faces competition from supermarkets and up to a great extent from company owned

sites they try to provide competitive prices to attract consumers (Gunn and Mont, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Moreover, on the supply side, it has been assessed that over last few decades, there has been

some rationalisation within distribution terminals and the secondary distribution network such as

road tankers. Here, most of the major oil companies outsource their road distribution operations

and thus, it leads to efficiencies and cost savings in the sector but it also results into closing of

petrol filling stations (Zlatcu, Kubinschi and Barnea, 2015). There are various refineries which

have been closed down since 1990's till 2014. The refineries that have been closed down in 2014

are Mantove Refibnery, Milford Haven Refinery, Muroran Refinery and Tokuyama Refinery,

etc. Refineries are the basic parts that are used for storage and distribution so that the best results

can be attained. Main reason for sudden spate of refinery closure stated that due to high oil prices

on the lack of refining capacity, it results in closing down of refineries.

Impact of Technology

Also, it has been assessed that there is downstream of UK oil and gas market because of

closures of different independent PFS. Further, there has been a changing mix of market players

with supermarkets gaining a larger share of market volumes through larger petrol filling stations

and by selling higher annual volumes relative to companies and dealers. Supermarkets such as

Asda and Tesco are emerging and able to fulfil the demand for high volumes as they have more

storage capacity (Valadkhani, Smyth and Vahid, 2015). Further, government also introduces

effective technology such as oil tankers by using bio gas fuel as well as it does not use oil or

petrol that helps in making cost effective supply. Another change introduced in the supply of UK

petroleum market is that there has been considerable fragmentation in the fuel supply chain over

last few years. It involves rationalisation of storage terminals, outsourcing of fuel road

distribution network and introducing innovative technology, etc. (Polemis and Fotis, 2014).

Recent changes in refinery

It can be assessed that recent changes in North Sea oil production has become a threat to

the owners of various refineries which results in losing of jobs of various employees. It was a

mutual decision to close down the refinery permanently. Refinery was facing many challenges in

the form of rising competition from mega refineries in Asia and Middle East through sharing of

production costs with the petrochemical business.

some rationalisation within distribution terminals and the secondary distribution network such as

road tankers. Here, most of the major oil companies outsource their road distribution operations

and thus, it leads to efficiencies and cost savings in the sector but it also results into closing of

petrol filling stations (Zlatcu, Kubinschi and Barnea, 2015). There are various refineries which

have been closed down since 1990's till 2014. The refineries that have been closed down in 2014

are Mantove Refibnery, Milford Haven Refinery, Muroran Refinery and Tokuyama Refinery,

etc. Refineries are the basic parts that are used for storage and distribution so that the best results

can be attained. Main reason for sudden spate of refinery closure stated that due to high oil prices

on the lack of refining capacity, it results in closing down of refineries.

Impact of Technology

Also, it has been assessed that there is downstream of UK oil and gas market because of

closures of different independent PFS. Further, there has been a changing mix of market players

with supermarkets gaining a larger share of market volumes through larger petrol filling stations

and by selling higher annual volumes relative to companies and dealers. Supermarkets such as

Asda and Tesco are emerging and able to fulfil the demand for high volumes as they have more

storage capacity (Valadkhani, Smyth and Vahid, 2015). Further, government also introduces

effective technology such as oil tankers by using bio gas fuel as well as it does not use oil or

petrol that helps in making cost effective supply. Another change introduced in the supply of UK

petroleum market is that there has been considerable fragmentation in the fuel supply chain over

last few years. It involves rationalisation of storage terminals, outsourcing of fuel road

distribution network and introducing innovative technology, etc. (Polemis and Fotis, 2014).

Recent changes in refinery

It can be assessed that recent changes in North Sea oil production has become a threat to

the owners of various refineries which results in losing of jobs of various employees. It was a

mutual decision to close down the refinery permanently. Refinery was facing many challenges in

the form of rising competition from mega refineries in Asia and Middle East through sharing of

production costs with the petrochemical business.

It can be evaluated that UK crude oil refinery inputs averaged around 16.6 million barrels

per day during the week. Here, the main source of crude demand is from refineries and thus, it

increases the input level that affects the inventory of oil and petroleum.

3.0 CHANGES IN THE OWNERSHIP OF PETROL SUPPLIERS

It has been identified that because of entry and growth of supermarkets in the fuel

retailing business it helps in providing tough competition to other major suppliers such as BP and

Shell. Hypermarkets such as Tesco and Asda own around 14% of petrol filling stations within

UK but they supply more than 40% of total road fuel volumes. Therefore, as compared to their

market share they are high in fuel volumes (Alderighi and Baudino, 2015). Thus, it puts

competitive pressures upon independent petrol filling stations such as Shell and oil companies

like BP. Within the last 1 decade, oil companies have decreased their market share in fuel

retailing. For instance, through a recent survey by the oil and gas industry, Tesco has recently

overcome BP as the largest retailer in terms of fuel volumes sold. It has been identified that PFS

owned by retail industries are consistent because of growth of supermarkets in the grocery

retailing business (Jones, Hillier and Comfort, 2015). Furthermore, retail businesses keep their

prices minimum as compared to BP and Shell and thus consumers prefer more to purchase fuel

from such hypermarkets owned PFS. Hypermarkets also introduce different attractive price

discounts at several times in order to attract customers and increase footfall within their retail

stores.

per day during the week. Here, the main source of crude demand is from refineries and thus, it

increases the input level that affects the inventory of oil and petroleum.

3.0 CHANGES IN THE OWNERSHIP OF PETROL SUPPLIERS

It has been identified that because of entry and growth of supermarkets in the fuel

retailing business it helps in providing tough competition to other major suppliers such as BP and

Shell. Hypermarkets such as Tesco and Asda own around 14% of petrol filling stations within

UK but they supply more than 40% of total road fuel volumes. Therefore, as compared to their

market share they are high in fuel volumes (Alderighi and Baudino, 2015). Thus, it puts

competitive pressures upon independent petrol filling stations such as Shell and oil companies

like BP. Within the last 1 decade, oil companies have decreased their market share in fuel

retailing. For instance, through a recent survey by the oil and gas industry, Tesco has recently

overcome BP as the largest retailer in terms of fuel volumes sold. It has been identified that PFS

owned by retail industries are consistent because of growth of supermarkets in the grocery

retailing business (Jones, Hillier and Comfort, 2015). Furthermore, retail businesses keep their

prices minimum as compared to BP and Shell and thus consumers prefer more to purchase fuel

from such hypermarkets owned PFS. Hypermarkets also introduce different attractive price

discounts at several times in order to attract customers and increase footfall within their retail

stores.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Illustration 2: Declining of PFS in past decades

(Source: Hood, Clarke and Clarke, 2015)

However, it has been assessed that if the prices of oil is decreasing day by day in the

international market than also companies such as BP and Shell is enhancing their prices for fuel

because of high labour cost and other expenditures. Thus, it is another crucial recent change in

trends of supply chain. Due to regular increase in prices of fuel by BP and Shell consumers

shifted to hypermarket owners of fuel i.e. Asda, and Sainsbury's. They provide fuel at low prices

and thus attract potential consumers (Gunn and Mont, 2014).

Refinery cut backs and how storage capacity has affected petrol station supply

It can be assessed that closures of petrol stations and cutbacks in storage capacity have

made UK more vulnerable in regard to supply oil. Due to rationalisation it affects the storage

depots and refineries have minimized the amount of petrol and diesel stocks at filling stations.

However, currently the stock levels are enough to meet individual demand for six to eight days

but there are several operators who are running short of capacity (Jones, Hillier and Comfort,

2015). However, it states that during supply disruption, it will quickly run out of petrol.

Additionally, it has been identified that there are certain oil companies who have

expanded the fuel retailing market through focusing upon the upstream oil and gas production.

For instance, Total Oil and Gas Company have recently disposed of its retail petrol filling station

network to Rontec while some of its PFS were sold to Shell. It is all because of decreasing in

(Source: Hood, Clarke and Clarke, 2015)

However, it has been assessed that if the prices of oil is decreasing day by day in the

international market than also companies such as BP and Shell is enhancing their prices for fuel

because of high labour cost and other expenditures. Thus, it is another crucial recent change in

trends of supply chain. Due to regular increase in prices of fuel by BP and Shell consumers

shifted to hypermarket owners of fuel i.e. Asda, and Sainsbury's. They provide fuel at low prices

and thus attract potential consumers (Gunn and Mont, 2014).

Refinery cut backs and how storage capacity has affected petrol station supply

It can be assessed that closures of petrol stations and cutbacks in storage capacity have

made UK more vulnerable in regard to supply oil. Due to rationalisation it affects the storage

depots and refineries have minimized the amount of petrol and diesel stocks at filling stations.

However, currently the stock levels are enough to meet individual demand for six to eight days

but there are several operators who are running short of capacity (Jones, Hillier and Comfort,

2015). However, it states that during supply disruption, it will quickly run out of petrol.

Additionally, it has been identified that there are certain oil companies who have

expanded the fuel retailing market through focusing upon the upstream oil and gas production.

For instance, Total Oil and Gas Company have recently disposed of its retail petrol filling station

network to Rontec while some of its PFS were sold to Shell. It is all because of decreasing in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

consumer preference to fill the fuel from such independent owners and shift to hypermarket fuel

stations. Because companies like Asda and Tesco do not raise their fuel prices constantly and

provide relatively low cost prices to individuals in order to retail them for long term. The fuel

provided by supermarkets are good in the form of brand because they itself own a good brand

image in retail grocery store (Hood, Clarke and Clarke, 2015). Further, closing down of PFS

results into capital intensive because for every Pound 1 made by a PFS then they to give Pound 3

that involves cost of labour, wages etc. Thus, due to this PFS are not able to make profits and

results into closing down. Further, another reason of closing down number of PFS is that laws

and regulations and environmental standards are not appropriate that impacts the PFS closing

down (Perdiguero-García, 2013).

Thus, expanding their business in oil and gas segment, it is essential for firm to undertake

competitive prices in order to attract potential buyers and enhance their sales of fuel volumes

which are increasing day by day as compared to Shell and BP. However, in the late 1980's the

growth of supermarket in fuel retailing has been noticed. Main aim of opening a PFS at a

supermarket location is to attract consumers to the main retail store. Therefore, company

provides various promotional offers such as discount on fuel and which can be availed while

shopping in the retail store (von Rosenstiel, Heuermann and Hüsig, 2015). Thus, such

promotions can help in benefiting retailers such as Asda, Tesco, Sainsbury and Morrisons.

stations. Because companies like Asda and Tesco do not raise their fuel prices constantly and

provide relatively low cost prices to individuals in order to retail them for long term. The fuel

provided by supermarkets are good in the form of brand because they itself own a good brand

image in retail grocery store (Hood, Clarke and Clarke, 2015). Further, closing down of PFS

results into capital intensive because for every Pound 1 made by a PFS then they to give Pound 3

that involves cost of labour, wages etc. Thus, due to this PFS are not able to make profits and

results into closing down. Further, another reason of closing down number of PFS is that laws

and regulations and environmental standards are not appropriate that impacts the PFS closing

down (Perdiguero-García, 2013).

Thus, expanding their business in oil and gas segment, it is essential for firm to undertake

competitive prices in order to attract potential buyers and enhance their sales of fuel volumes

which are increasing day by day as compared to Shell and BP. However, in the late 1980's the

growth of supermarket in fuel retailing has been noticed. Main aim of opening a PFS at a

supermarket location is to attract consumers to the main retail store. Therefore, company

provides various promotional offers such as discount on fuel and which can be availed while

shopping in the retail store (von Rosenstiel, Heuermann and Hüsig, 2015). Thus, such

promotions can help in benefiting retailers such as Asda, Tesco, Sainsbury and Morrisons.

Illustration 3: Asda PFS

(Source: Abdelrehim, Maltby and Toms, 2015)

It can be assessed that major oil companies have come under pressure because of their

hike in fuel prices and thus their market share declines constantly as compared to supermarket

competitors. BP and Murco have increased their fuel prices to 3.4p per litre while Esso, Total

and Texaco have also increase their prices by an average of 3.3p. In comparison to these prices

of Tesco and Sainsbury just raises their price to 1.7p and 1.9p per litre. Among all Asda is still

the cheapest price holder (Albalate and Perdiguero, 2015). Thus, it can be evaluated from the

below table that there are different oil companies providing different price range for fuel. But it

shows that hypermarket owners provide fuel at relatively low prices as compared to other

independent owners such as BP and Shell. Therefore, consumers are more likely to purchase fuel

from PFS of Asda. Tesco and Salisbury because they also provide attractive discount prices to

attract potential consumers to visit their retail store and enhance the sales of grocery as well

(Wang, 2015).

(Source: Abdelrehim, Maltby and Toms, 2015)

It can be assessed that major oil companies have come under pressure because of their

hike in fuel prices and thus their market share declines constantly as compared to supermarket

competitors. BP and Murco have increased their fuel prices to 3.4p per litre while Esso, Total

and Texaco have also increase their prices by an average of 3.3p. In comparison to these prices

of Tesco and Sainsbury just raises their price to 1.7p and 1.9p per litre. Among all Asda is still

the cheapest price holder (Albalate and Perdiguero, 2015). Thus, it can be evaluated from the

below table that there are different oil companies providing different price range for fuel. But it

shows that hypermarket owners provide fuel at relatively low prices as compared to other

independent owners such as BP and Shell. Therefore, consumers are more likely to purchase fuel

from PFS of Asda. Tesco and Salisbury because they also provide attractive discount prices to

attract potential consumers to visit their retail store and enhance the sales of grocery as well

(Wang, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.