Charles Sturt University ACC568 Auditing: DHL Audit Issues Report

VerifiedAdded on 2022/11/22

|15

|3533

|472

Report

AI Summary

This report, prepared by a student for an ACC568 Auditing assignment at Charles Sturt University, analyzes the audit of Dudley Health Limited (DHL). The report addresses several key issues, including business fraud at Pellegrino Shores, specifically the misappropriation of assets and manipulation of resident fees. It explores the impact of fraud on financial loss, external and internal confidence, and company morale, along with its effects on the audit process. The report also examines audit risks, differentiating between inherent, detection, and control risks, and the importance of audit strategy. Additionally, the report provides information on the additional information required in relation to the sale of medicine on the key account balance, including assets, inventory, liabilities, and equity. It discusses material misstatements and the role of control environments. Finally, it details accounts payable testing, differentiating between tests of control and substantive testing, and provides an overview of customer payment testing.

Memorandum

To: Jek Porkin

From: xxxxxxx, audit manager, Samway Baker Fitzgerald

Subject: Advice on the mentioned issues

Issue 1

Business fraud or corporate fraud basically consists of illegal activities, misappropriation of

assets, fraudulent of financial reporting and dishonesty by an individual towards a company

which will provide financial gain. It consists of all activities that can disrupt the activities of any

business (Adler et al.,2018). While sometime fraud can put question on the survival of the business

by limiting partners and clients confidence or creating mistrust inside the business. So the impact

of fraud in a business is as follows:

Financial loss – Any type of fraud mainly effect the financial statement first. Whenever

there is misappropriation of company asset or cash it creates fraud in financial reporting

which is harder to determine. In big companies it is harder to track these types of fraud

and it creates a bad impact on the companies’ goodwill. Investors would not be willing to

invest their money in such types of company where there is a chance of risk (DeFond &

Zhang,2014).

External confidence – If once a company faces fraud then it hampers the public trusts on

the organization. While if a small company faces fraud they might never be the victim as

their existence will be on stack. The bad effect of facing fraud by a company has many

To: Jek Porkin

From: xxxxxxx, audit manager, Samway Baker Fitzgerald

Subject: Advice on the mentioned issues

Issue 1

Business fraud or corporate fraud basically consists of illegal activities, misappropriation of

assets, fraudulent of financial reporting and dishonesty by an individual towards a company

which will provide financial gain. It consists of all activities that can disrupt the activities of any

business (Adler et al.,2018). While sometime fraud can put question on the survival of the business

by limiting partners and clients confidence or creating mistrust inside the business. So the impact

of fraud in a business is as follows:

Financial loss – Any type of fraud mainly effect the financial statement first. Whenever

there is misappropriation of company asset or cash it creates fraud in financial reporting

which is harder to determine. In big companies it is harder to track these types of fraud

and it creates a bad impact on the companies’ goodwill. Investors would not be willing to

invest their money in such types of company where there is a chance of risk (DeFond &

Zhang,2014).

External confidence – If once a company faces fraud then it hampers the public trusts on

the organization. While if a small company faces fraud they might never be the victim as

their existence will be on stack. The bad effect of facing fraud by a company has many

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

consequences like they may get credit at higher price and they may be refused for

membership in trade association.

Internal confidence – Fraud not only affects the moral of external but also affects the

internal of the company by disrupting their normal momentum. Especially in small

company they rely on stable growth and cultivate (Furnham & Gunter, 2015).

Company morale – Fraud’s shatters the moral and culture of the company and the persons

who are attached to it as it create embarrassments and trouble for the person who works

there. Even when an employee leaves a job and joins another it carries the tag of fraud

with him even if they were not associated with it.

Effect on audit – Fraud makes business audit more complicated and tough. After fraud

auditor has to closely look after the company’s books of account minutely. Even

sometime external auditor has to appoint to double check the data’s. Auditor sometime

has to use some other procedures to reach at the final decisions which make the audit

procedure costly.

Issue 2

Audit risks are those risk which arise when an auditor expresses an inappropriate opinion

on the financial statement even if the financial statement is free from any misstatement. Audit

risk is considered as the risk of various products but to keep this risk at limit the auditor has to

check each component at all level ( Griffiths,2016). The main purpose of audit is to reduce the

audit risk by making adequate tests and procedures as the investors and stakeholders rely on the

financial statement audited by the auditor. There are mainly three types of risk which are as

follows:

membership in trade association.

Internal confidence – Fraud not only affects the moral of external but also affects the

internal of the company by disrupting their normal momentum. Especially in small

company they rely on stable growth and cultivate (Furnham & Gunter, 2015).

Company morale – Fraud’s shatters the moral and culture of the company and the persons

who are attached to it as it create embarrassments and trouble for the person who works

there. Even when an employee leaves a job and joins another it carries the tag of fraud

with him even if they were not associated with it.

Effect on audit – Fraud makes business audit more complicated and tough. After fraud

auditor has to closely look after the company’s books of account minutely. Even

sometime external auditor has to appoint to double check the data’s. Auditor sometime

has to use some other procedures to reach at the final decisions which make the audit

procedure costly.

Issue 2

Audit risks are those risk which arise when an auditor expresses an inappropriate opinion

on the financial statement even if the financial statement is free from any misstatement. Audit

risk is considered as the risk of various products but to keep this risk at limit the auditor has to

check each component at all level ( Griffiths,2016). The main purpose of audit is to reduce the

audit risk by making adequate tests and procedures as the investors and stakeholders rely on the

financial statement audited by the auditor. There are mainly three types of risk which are as

follows:

Inherent risk – This is a type of audit risk which cannot be identified by the internal

auditor during audit. To detect this risk different series of procedure is required to be

applied to have a clear idea about audit plan, audit strategy and audit approach. Audit

plan consist of guidelines to be strictly followed which list the evidence that need to

gather while an internal audit. Audit strategy is also used to develop the audit plan by

applying different methods of audit risk (Groomer & Murthy, 2018).

Detection risk – It is a type of audit risk that occurs from poor planning. This risk cannot

be identified and corrected as it occurs when the financial team gather all material in one

place either with missing information or faulty calculation. Identifying this risk requires

deep knowledge and understanding of the nature and business of the company operations

and its financial statements.

Control risk – This risk arises due to absence or failure in the operation controls of the

entity which create the risk of material misstatement. To detect this type of risk an

organization must have a proper internal control to detect and prevent this type of risk to

arise. So proper planning for every department in every step is required to exercise proper

internal control over financial statements (Hall, 2015).

Asking question to an internal audit is the most critical part of the inquiry which allows to

understand the process, function and objectivity of the audit. So the two key question that must

be asked to an internal audit are what the process involved are and how to improve this process.

Audit strategy are the process that determines the direction, timing and scope of an audit as it

provide the guideline for developing the audit plan. It contains some statements of key decision

that is needed to plan the audit which includes the characteristics of the entity, reporting

objectives, timing of audit, nature of communication, factors required team effort, preliminary

auditor during audit. To detect this risk different series of procedure is required to be

applied to have a clear idea about audit plan, audit strategy and audit approach. Audit

plan consist of guidelines to be strictly followed which list the evidence that need to

gather while an internal audit. Audit strategy is also used to develop the audit plan by

applying different methods of audit risk (Groomer & Murthy, 2018).

Detection risk – It is a type of audit risk that occurs from poor planning. This risk cannot

be identified and corrected as it occurs when the financial team gather all material in one

place either with missing information or faulty calculation. Identifying this risk requires

deep knowledge and understanding of the nature and business of the company operations

and its financial statements.

Control risk – This risk arises due to absence or failure in the operation controls of the

entity which create the risk of material misstatement. To detect this type of risk an

organization must have a proper internal control to detect and prevent this type of risk to

arise. So proper planning for every department in every step is required to exercise proper

internal control over financial statements (Hall, 2015).

Asking question to an internal audit is the most critical part of the inquiry which allows to

understand the process, function and objectivity of the audit. So the two key question that must

be asked to an internal audit are what the process involved are and how to improve this process.

Audit strategy are the process that determines the direction, timing and scope of an audit as it

provide the guideline for developing the audit plan. It contains some statements of key decision

that is needed to plan the audit which includes the characteristics of the entity, reporting

objectives, timing of audit, nature of communication, factors required team effort, preliminary

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

activities required, knowledge gained form the entity and the resources available for the entity.

Small entity requires short audit strategy in the form of memo. Audit strategy consist of different

audit approach like risk based audit or top down approach which is used by the auditor during

the process of audit. It defines and set the objectives of audit with planning required to execute

an audit (Knechel & Salterio, 2016). Audit strategy is very important for the success of an audit

engagement by following some of the key points are as follows:

Auditor should identify and defines the scope of audit which is very important for

starting the audit process. As auditor has to follow international auditing standards and

client has to prepare his financial statement according to US GAAP.

By identifying the objective of audit which helps the auditor to set the time required for

audit by stating the disclaimer in the audit report.

Audit strategy helps the auditor to identify the key area of audit engagement that requires

professional judgment.

Issue 3

Additional information required in relation to the sale of medicine on the key account

balance are as follows:

Assets – To operate successfully every business requires asset which includes cash, stock,

building, tools, land, vehicle and also the money due from the customers (Power &

Gendron, 2015).

Inventory – Stock are the important part of the business which can be the raw material to

produce saleable items or the finished products to sell.

Small entity requires short audit strategy in the form of memo. Audit strategy consist of different

audit approach like risk based audit or top down approach which is used by the auditor during

the process of audit. It defines and set the objectives of audit with planning required to execute

an audit (Knechel & Salterio, 2016). Audit strategy is very important for the success of an audit

engagement by following some of the key points are as follows:

Auditor should identify and defines the scope of audit which is very important for

starting the audit process. As auditor has to follow international auditing standards and

client has to prepare his financial statement according to US GAAP.

By identifying the objective of audit which helps the auditor to set the time required for

audit by stating the disclaimer in the audit report.

Audit strategy helps the auditor to identify the key area of audit engagement that requires

professional judgment.

Issue 3

Additional information required in relation to the sale of medicine on the key account

balance are as follows:

Assets – To operate successfully every business requires asset which includes cash, stock,

building, tools, land, vehicle and also the money due from the customers (Power &

Gendron, 2015).

Inventory – Stock are the important part of the business which can be the raw material to

produce saleable items or the finished products to sell.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Liabilities – Money that a company owes to other in the form of loan, bond credit

purchase and many others are known as liability of a company.

Equity – Money which are invested by the investors in the company is considered to be

the equity.

It’s not possible for an auditor to detect all the misstatement in the key account balance so they

mainly focus on material misstatement (Ren et al., 2015). Material misstatement influence the

decision making of the financial statement which arises due to fraud or error. So the risk of

material misstatement can be of two type which are as stated below:

Inherent risk – This risk are due to error or omission of financial statement due to the

factors other than internal. This risk is most likely to occur when there is complex

transaction and it represent failure of internal control.

Control risk – This risk arises when there is material misstated due to failure of internal

control used in the business. For this a business may experience asset loss but the

financial statement shows profit instead of actual loss. Implementing control system helps

to avoid this risk but can cost high.

Control environment are set of action taken by the management that sets the day to day activities

to control the environment which comprises of policies and procedures taken by the management

to deal with issues (Sandvig et al., 2014). International institute of audit defines the control

environment as the foundation on which the internal control system operates which helps the

organization to achieve its strategic objectives, provide accurate financial statement to the

internal and external stakeholders, helps to operate business efficiently and effectively by

following all laws and regulation and safeguarding its assets. Organization that established a well

purchase and many others are known as liability of a company.

Equity – Money which are invested by the investors in the company is considered to be

the equity.

It’s not possible for an auditor to detect all the misstatement in the key account balance so they

mainly focus on material misstatement (Ren et al., 2015). Material misstatement influence the

decision making of the financial statement which arises due to fraud or error. So the risk of

material misstatement can be of two type which are as stated below:

Inherent risk – This risk are due to error or omission of financial statement due to the

factors other than internal. This risk is most likely to occur when there is complex

transaction and it represent failure of internal control.

Control risk – This risk arises when there is material misstated due to failure of internal

control used in the business. For this a business may experience asset loss but the

financial statement shows profit instead of actual loss. Implementing control system helps

to avoid this risk but can cost high.

Control environment are set of action taken by the management that sets the day to day activities

to control the environment which comprises of policies and procedures taken by the management

to deal with issues (Sandvig et al., 2014). International institute of audit defines the control

environment as the foundation on which the internal control system operates which helps the

organization to achieve its strategic objectives, provide accurate financial statement to the

internal and external stakeholders, helps to operate business efficiently and effectively by

following all laws and regulation and safeguarding its assets. Organization that established a well

control environment are more efficient in its operation and achieve its objectives. Principles

related to control environment are as follows:

Commitment to integrity and ethical values

Independence to the board of directors.

Establishing organizational authority, structure and responsibility.

Attract, develop and maintain competent people.

Maintaining internal control responsibilities.

Entity faces risk from both internal and external sources which are included in the control

environment (Shen et al., 2017). So a precondition risk assessment has been established with the

objective of identifying, assessing and managing risk to achieve the entity’s objective. It is

established before administration can identify the risk and take necessary steps. It shows the

effectiveness and efficiency of the operation and performance to achieve financial goals.

Identifying and analyzing the risk is a critical component of internal control system and its

effectiveness on risk at all level. Risk assessment are very important part of the internal system

as it help to create awareness for risk, identify the risk, control program for any hazard,

determining the adequacy of control measures, prevent risk especially at the planning stage,

applying control measures and meeting all legal requirements.

Customer payment testing is a payment gateway system which is an e-commerce application that

approve payment of the customers (Sookhak, 2015). It from as medium between the purchaser and

seller by encrypting sensitive information. Customer payment testing includes the following:

Functional testing – It is the base function of the payment system which verifies the

application as per the order, calculation and tax charges country wise.

related to control environment are as follows:

Commitment to integrity and ethical values

Independence to the board of directors.

Establishing organizational authority, structure and responsibility.

Attract, develop and maintain competent people.

Maintaining internal control responsibilities.

Entity faces risk from both internal and external sources which are included in the control

environment (Shen et al., 2017). So a precondition risk assessment has been established with the

objective of identifying, assessing and managing risk to achieve the entity’s objective. It is

established before administration can identify the risk and take necessary steps. It shows the

effectiveness and efficiency of the operation and performance to achieve financial goals.

Identifying and analyzing the risk is a critical component of internal control system and its

effectiveness on risk at all level. Risk assessment are very important part of the internal system

as it help to create awareness for risk, identify the risk, control program for any hazard,

determining the adequacy of control measures, prevent risk especially at the planning stage,

applying control measures and meeting all legal requirements.

Customer payment testing is a payment gateway system which is an e-commerce application that

approve payment of the customers (Sookhak, 2015). It from as medium between the purchaser and

seller by encrypting sensitive information. Customer payment testing includes the following:

Functional testing – It is the base function of the payment system which verifies the

application as per the order, calculation and tax charges country wise.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Integration – It integrate test checking of all service.

Performance – It identifies various performance check of gateways to check its

efficiency.

Issue 4

Accounts payable test is designed to enable the employer to identify the potential hiring

by evaluating the skills of working and readiness to job.

TEST TYPES OF TEST KEY ASSERTION COMCLUSION

1 Test of control This is an accounting

procedures that test the

effectiveness of controls

used by entity to prevent or

detect the material

misstatement (Reeves,

Culverwell & Wittman,

2017).

Here auditor relies on the

client control system to

perform the auditing

activities. If this test failed

to achieve its objective then

then the auditor will

This test is done

on sample

transaction that

occurred

throughout the

year which will

provide the

evidence of

reliability of the

control system in

the reporting

period.

Size of the

company does not

Performance – It identifies various performance check of gateways to check its

efficiency.

Issue 4

Accounts payable test is designed to enable the employer to identify the potential hiring

by evaluating the skills of working and readiness to job.

TEST TYPES OF TEST KEY ASSERTION COMCLUSION

1 Test of control This is an accounting

procedures that test the

effectiveness of controls

used by entity to prevent or

detect the material

misstatement (Reeves,

Culverwell & Wittman,

2017).

Here auditor relies on the

client control system to

perform the auditing

activities. If this test failed

to achieve its objective then

then the auditor will

This test is done

on sample

transaction that

occurred

throughout the

year which will

provide the

evidence of

reliability of the

control system in

the reporting

period.

Size of the

company does not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

perform a substantive test

which will increase the cost

of auditing.

Test of control is classified

into three which are the

followings:

Re-performance –

At this stage auditor

initiate new

transaction to see the

control that are used

by the client to

check its

effectiveness (Xia et

al., 2015).

Observation –

Auditor also

observes the

business process

which controls the

elements of process.

Inspection –

Business documents

matters in this test

as its main

objective is to

check the proper

functioning of

control system.

When an auditor

face error in test

of control it

further apply

testing. Further if

any error is found

then the auditor

will consider it as

a systematic

control defect

which cannot be

rectified by the

auditor.

which will increase the cost

of auditing.

Test of control is classified

into three which are the

followings:

Re-performance –

At this stage auditor

initiate new

transaction to see the

control that are used

by the client to

check its

effectiveness (Xia et

al., 2015).

Observation –

Auditor also

observes the

business process

which controls the

elements of process.

Inspection –

Business documents

matters in this test

as its main

objective is to

check the proper

functioning of

control system.

When an auditor

face error in test

of control it

further apply

testing. Further if

any error is found

then the auditor

will consider it as

a systematic

control defect

which cannot be

rectified by the

auditor.

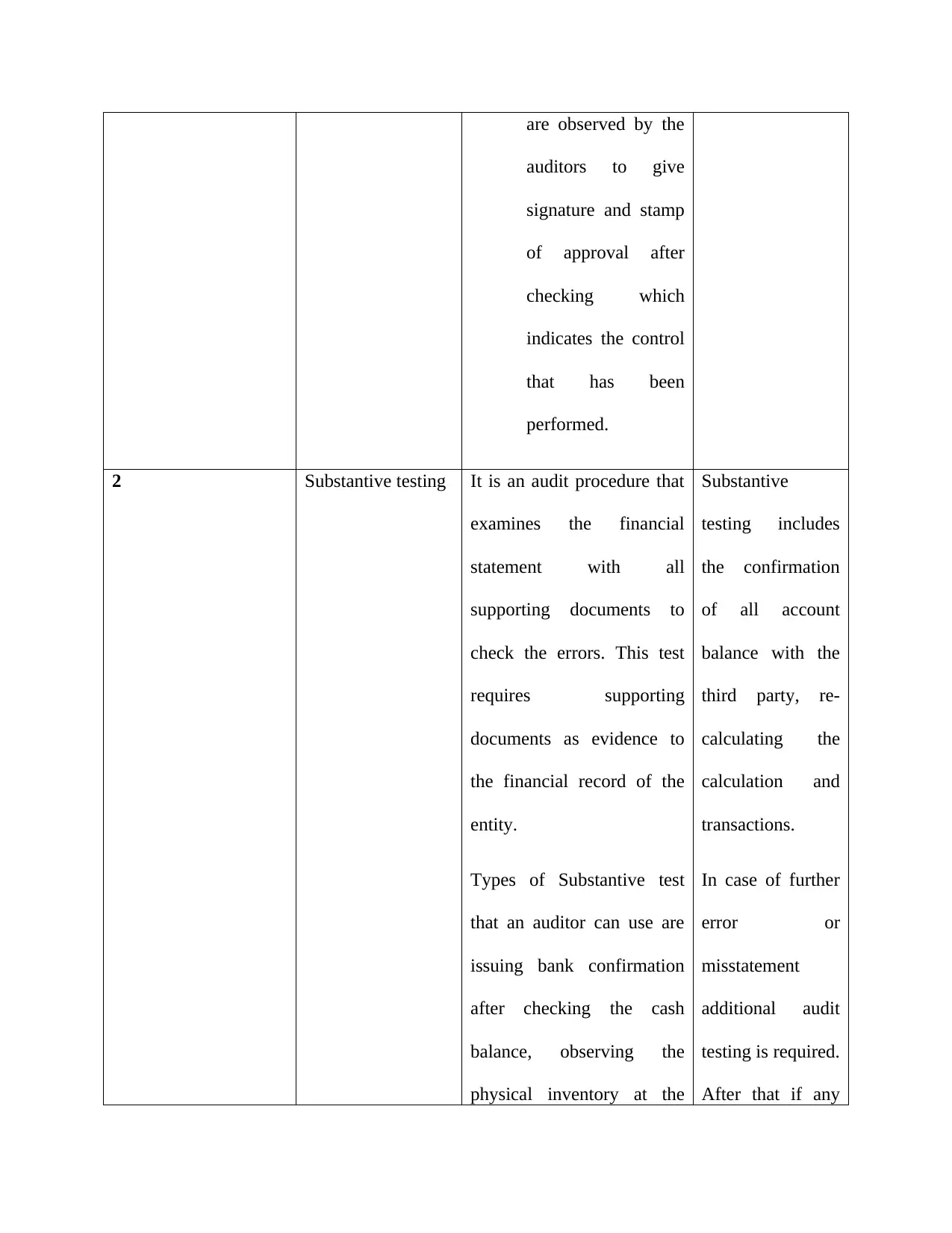

are observed by the

auditors to give

signature and stamp

of approval after

checking which

indicates the control

that has been

performed.

2 Substantive testing It is an audit procedure that

examines the financial

statement with all

supporting documents to

check the errors. This test

requires supporting

documents as evidence to

the financial record of the

entity.

Types of Substantive test

that an auditor can use are

issuing bank confirmation

after checking the cash

balance, observing the

physical inventory at the

Substantive

testing includes

the confirmation

of all account

balance with the

third party, re-

calculating the

calculation and

transactions.

In case of further

error or

misstatement

additional audit

testing is required.

After that if any

auditors to give

signature and stamp

of approval after

checking which

indicates the control

that has been

performed.

2 Substantive testing It is an audit procedure that

examines the financial

statement with all

supporting documents to

check the errors. This test

requires supporting

documents as evidence to

the financial record of the

entity.

Types of Substantive test

that an auditor can use are

issuing bank confirmation

after checking the cash

balance, observing the

physical inventory at the

Substantive

testing includes

the confirmation

of all account

balance with the

third party, re-

calculating the

calculation and

transactions.

In case of further

error or

misstatement

additional audit

testing is required.

After that if any

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

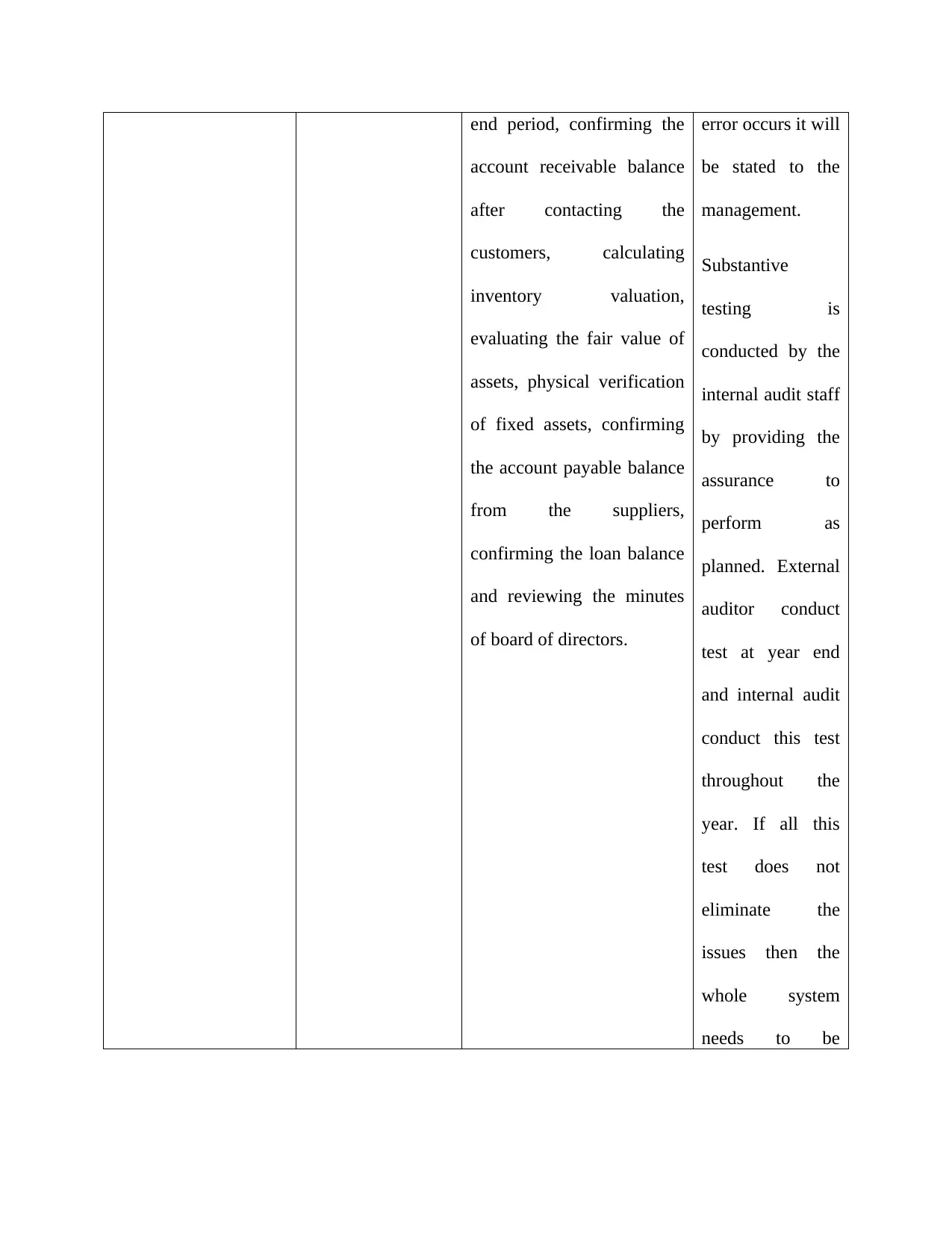

end period, confirming the

account receivable balance

after contacting the

customers, calculating

inventory valuation,

evaluating the fair value of

assets, physical verification

of fixed assets, confirming

the account payable balance

from the suppliers,

confirming the loan balance

and reviewing the minutes

of board of directors.

error occurs it will

be stated to the

management.

Substantive

testing is

conducted by the

internal audit staff

by providing the

assurance to

perform as

planned. External

auditor conduct

test at year end

and internal audit

conduct this test

throughout the

year. If all this

test does not

eliminate the

issues then the

whole system

needs to be

account receivable balance

after contacting the

customers, calculating

inventory valuation,

evaluating the fair value of

assets, physical verification

of fixed assets, confirming

the account payable balance

from the suppliers,

confirming the loan balance

and reviewing the minutes

of board of directors.

error occurs it will

be stated to the

management.

Substantive

testing is

conducted by the

internal audit staff

by providing the

assurance to

perform as

planned. External

auditor conduct

test at year end

and internal audit

conduct this test

throughout the

year. If all this

test does not

eliminate the

issues then the

whole system

needs to be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

improved.

Issue 5

Regulation in standard of work hour pay and overtime protect the workers who are required to

work for more than the ongoing rate. This regulation is invented to discourage the use of

overtime (Yuan & Yu, 2013). Overtime raises employment cost and forces the economic to reduce

the employment. The overtime pay regulation has little effect on the worker who work overtime.

The risk of overtime are as follows:

Overtime reduces the employment of both skilled and unskilled people.

Overtime worker are more skilled then other employees and their work may not be up to

the standard.

It increases the competition for job who are employed.

Expands the overtime pay regulation which has little effect on the shares of workers.

Raise labor cost which can lead to reduction in overall employment.

Overtime pay can increase the hourly wage of few worker and also encourage work by

increasing employment. Overtime regulation does not stay valid when worker and employer

adjust to the regulation. Sometime this regulation fail to increase job and actually reduce

employment (Zadek, Evans & Pruzan, 2013).

Internal control consist of set of activities that are used in the normal operating procedures of the

organization by safeguarding the assets, reducing errors and ensuring proper functioning of

operation. Internal control increases with the increase in size of the entity because owner don’t

get time to maintain when the number of employee increases. Even if a company transfer itself to

Issue 5

Regulation in standard of work hour pay and overtime protect the workers who are required to

work for more than the ongoing rate. This regulation is invented to discourage the use of

overtime (Yuan & Yu, 2013). Overtime raises employment cost and forces the economic to reduce

the employment. The overtime pay regulation has little effect on the worker who work overtime.

The risk of overtime are as follows:

Overtime reduces the employment of both skilled and unskilled people.

Overtime worker are more skilled then other employees and their work may not be up to

the standard.

It increases the competition for job who are employed.

Expands the overtime pay regulation which has little effect on the shares of workers.

Raise labor cost which can lead to reduction in overall employment.

Overtime pay can increase the hourly wage of few worker and also encourage work by

increasing employment. Overtime regulation does not stay valid when worker and employer

adjust to the regulation. Sometime this regulation fail to increase job and actually reduce

employment (Zadek, Evans & Pruzan, 2013).

Internal control consist of set of activities that are used in the normal operating procedures of the

organization by safeguarding the assets, reducing errors and ensuring proper functioning of

operation. Internal control increases with the increase in size of the entity because owner don’t

get time to maintain when the number of employee increases. Even if a company transfer itself to

public company or when a company’s share are listed in stock exchange there is always a need

of additional internal control system which tend to increase the cost only. Internal control

consist of some policies and procedure that an entity uses to protect its asset and data by

maximizing its operation. Type of internal control are as follows:

Detective internal control – This internal control is designed to find the errors after their

occurrence which serve as a check balance system to determine the efficiency of the

policy. It finds the problem within the companies’ process. A small company can

implement this control easily through management supervision but a large firm required

more integrated system which is adequate to control companies operation.

Preventive internal control – This internal control are kept to keep the errors and

misstatement to occur as it works on regular basis. It keeps the loss and error from

occurring by segregating duties and protecting assets. This control includes checking of

clerical works, backing up the computer data’s, checking on employees or employers,

segregating duties and approving transactions. This control is integrated in the system to

function on a continuous process (Yu et al., 2015).

of additional internal control system which tend to increase the cost only. Internal control

consist of some policies and procedure that an entity uses to protect its asset and data by

maximizing its operation. Type of internal control are as follows:

Detective internal control – This internal control is designed to find the errors after their

occurrence which serve as a check balance system to determine the efficiency of the

policy. It finds the problem within the companies’ process. A small company can

implement this control easily through management supervision but a large firm required

more integrated system which is adequate to control companies operation.

Preventive internal control – This internal control are kept to keep the errors and

misstatement to occur as it works on regular basis. It keeps the loss and error from

occurring by segregating duties and protecting assets. This control includes checking of

clerical works, backing up the computer data’s, checking on employees or employers,

segregating duties and approving transactions. This control is integrated in the system to

function on a continuous process (Yu et al., 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.