Audit Report: Internal Control, Risk, and Fraud at DHL (2019)

VerifiedAdded on 2022/11/01

|19

|4036

|396

Report

AI Summary

This report presents an internal control audit of Dudley Health Limited (DHL), encompassing its subsidiaries: St Neville's hospital, Acuity Vision clinics, and Pellegrino Shores retirement village. The audit, conducted by Samway Baker Fitzgerald (SBF), addresses a recent fraud at Pellegrino Shores, analyzing its financial and operational impacts, including loss of revenue, damage to reputation, and increased audit costs. The report examines affected accounts and audit assertions, such as revenue, cash, and retained earnings, and assesses risks associated with a new revenue system at St. Neville's. It evaluates internal controls, identifies potential fraudulent activities, and recommends a "top-down risk assessment" approach. Furthermore, the report analyzes key account balances and risk assertions for commission expenses and cash, proposes improvements to DHL's environment control, and critiques the testing methods used by Jek Prokins, suggesting additional audit steps. The report also includes a detailed assessment of audit tests, highlighting assertions, conclusions, and additional audit processes.

Running Head: INTERNAL CONTROL AUDIT

Internal Control Audit

Student Name:

University Name:

Internal Control Audit

Student Name:

University Name:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNAL CONTROL AUDIT

Table of Contents

Question Number 1..........................................................................................................................3

Question No 2..................................................................................................................................5

a)..................................................................................................................................................5

b)..................................................................................................................................................6

c)..................................................................................................................................................6

Question No. 3.................................................................................................................................7

a)..................................................................................................................................................7

b)..................................................................................................................................................9

c)..................................................................................................................................................9

Question No. 4...............................................................................................................................10

Question No. 5...............................................................................................................................15

References......................................................................................................................................17

Table of Contents

Question Number 1..........................................................................................................................3

Question No 2..................................................................................................................................5

a)..................................................................................................................................................5

b)..................................................................................................................................................6

c)..................................................................................................................................................6

Question No. 3.................................................................................................................................7

a)..................................................................................................................................................7

b)..................................................................................................................................................9

c)..................................................................................................................................................9

Question No. 4...............................................................................................................................10

Question No. 5...............................................................................................................................15

References......................................................................................................................................17

INTERNAL CONTROL AUDIT

A memo to JekPorkins, the audit senior on the DHL assignment

Question Number 1

The risk of business affect the fraudulent affair will have various level impacts to Pellegrino

Shores. Some of these are as follows.

Loss Related to Finance: On the occurrence of a fraud, this is the first risk that happens to take

place. Thus, in this paper, the loss of qualification is not a fact on account which an appropriate

estimate of potential (Abbott et al., 2016). This is based on the feedback of the resident, which is

honest as well as other records include time and dates of check-in and checkout. Therefore, in the

particular case, the people appear to be a fraction of mix. Hence, it is doubtful to drop previous

on this type of technique.

Common Image: For the benefit of the customers, who all are busy with such unethical deeds,

the fraud may appear. Therefore, this is preparing a mentality regarding the business where it is

convinced that the people of village can be exploited easily (Ali, Ahmi & Ahmad, 2018).

Inside Morale: If the employees believe that the same is a pride of matter for them, they seek to

coordinate with a specific institution. This happens because employees have been coordinated

with a dishonest institution (Al-Matari et al., 2014). Hence, this will negatively affect their

profession growth in the succeeding period.

Overhead of Higher Audit Cost: This is a general grasp related to the occurrence of the

dishonest activities. The cost associated to audit will rise; due to this, the auditor will have to

scrutinize financial statements of each account in association with the fraud. This happens in

respect to the transaction history. People involved in this transaction as well as large due

diligence related to the whole effect that this type of transactions have on an organization. For

the organization on a general basis, high work budgets, high fees, will lead to higher overhead

cost for the Pellegrino shores (Burton et al., 2014).

Following are the accounts that this fraudulent affair will affect as well as its assertions

associated with audit:

Affected Accounts Assertions Related to Audit

Revenue generation from Operations Under the category of general class i.e.

A memo to JekPorkins, the audit senior on the DHL assignment

Question Number 1

The risk of business affect the fraudulent affair will have various level impacts to Pellegrino

Shores. Some of these are as follows.

Loss Related to Finance: On the occurrence of a fraud, this is the first risk that happens to take

place. Thus, in this paper, the loss of qualification is not a fact on account which an appropriate

estimate of potential (Abbott et al., 2016). This is based on the feedback of the resident, which is

honest as well as other records include time and dates of check-in and checkout. Therefore, in the

particular case, the people appear to be a fraction of mix. Hence, it is doubtful to drop previous

on this type of technique.

Common Image: For the benefit of the customers, who all are busy with such unethical deeds,

the fraud may appear. Therefore, this is preparing a mentality regarding the business where it is

convinced that the people of village can be exploited easily (Ali, Ahmi & Ahmad, 2018).

Inside Morale: If the employees believe that the same is a pride of matter for them, they seek to

coordinate with a specific institution. This happens because employees have been coordinated

with a dishonest institution (Al-Matari et al., 2014). Hence, this will negatively affect their

profession growth in the succeeding period.

Overhead of Higher Audit Cost: This is a general grasp related to the occurrence of the

dishonest activities. The cost associated to audit will rise; due to this, the auditor will have to

scrutinize financial statements of each account in association with the fraud. This happens in

respect to the transaction history. People involved in this transaction as well as large due

diligence related to the whole effect that this type of transactions have on an organization. For

the organization on a general basis, high work budgets, high fees, will lead to higher overhead

cost for the Pellegrino shores (Burton et al., 2014).

Following are the accounts that this fraudulent affair will affect as well as its assertions

associated with audit:

Affected Accounts Assertions Related to Audit

Revenue generation from Operations Under the category of general class i.e.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNAL CONTROL AUDIT

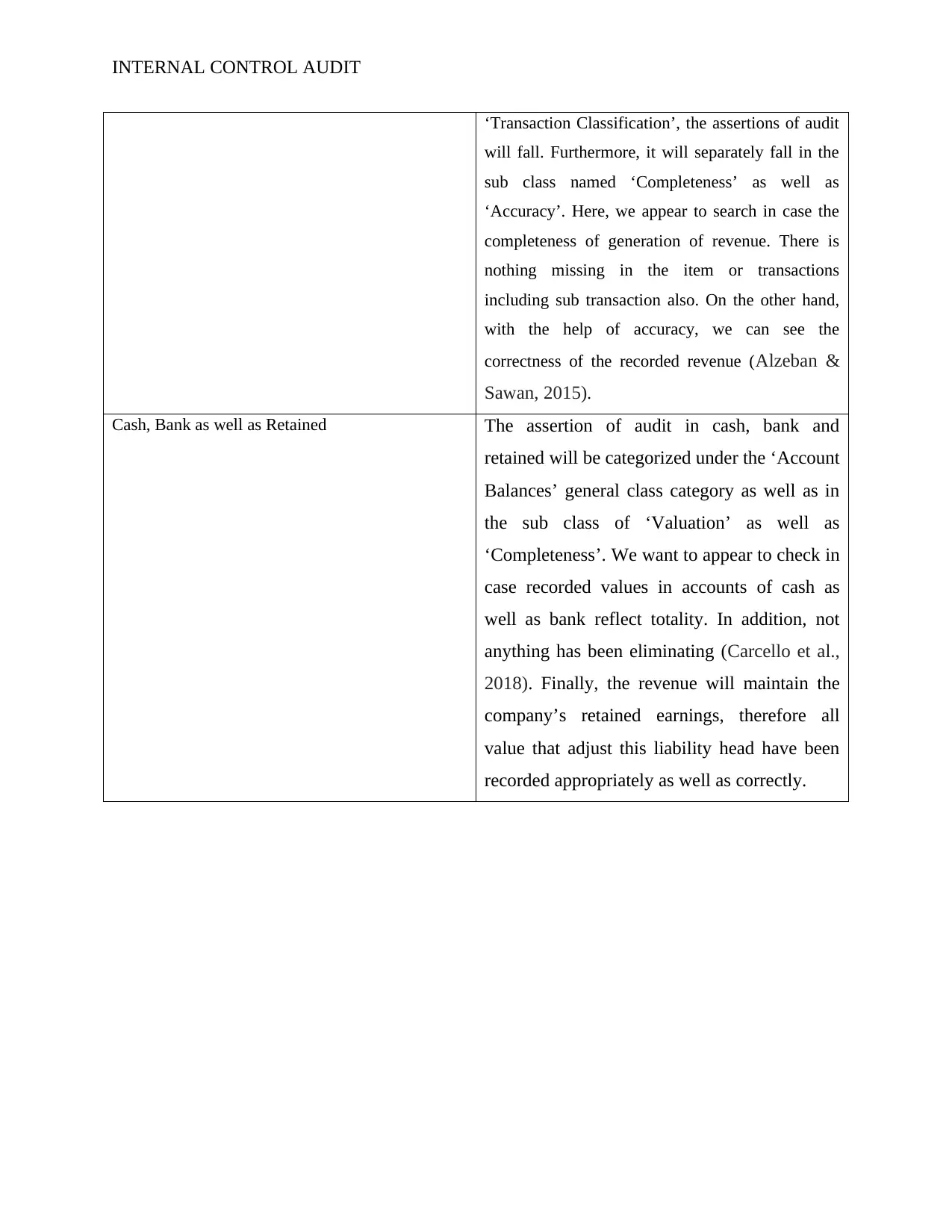

‘Transaction Classification’, the assertions of audit

will fall. Furthermore, it will separately fall in the

sub class named ‘Completeness’ as well as

‘Accuracy’. Here, we appear to search in case the

completeness of generation of revenue. There is

nothing missing in the item or transactions

including sub transaction also. On the other hand,

with the help of accuracy, we can see the

correctness of the recorded revenue (Alzeban &

Sawan, 2015).

Cash, Bank as well as Retained The assertion of audit in cash, bank and

retained will be categorized under the ‘Account

Balances’ general class category as well as in

the sub class of ‘Valuation’ as well as

‘Completeness’. We want to appear to check in

case recorded values in accounts of cash as

well as bank reflect totality. In addition, not

anything has been eliminating (Carcello et al.,

2018). Finally, the revenue will maintain the

company’s retained earnings, therefore all

value that adjust this liability head have been

recorded appropriately as well as correctly.

‘Transaction Classification’, the assertions of audit

will fall. Furthermore, it will separately fall in the

sub class named ‘Completeness’ as well as

‘Accuracy’. Here, we appear to search in case the

completeness of generation of revenue. There is

nothing missing in the item or transactions

including sub transaction also. On the other hand,

with the help of accuracy, we can see the

correctness of the recorded revenue (Alzeban &

Sawan, 2015).

Cash, Bank as well as Retained The assertion of audit in cash, bank and

retained will be categorized under the ‘Account

Balances’ general class category as well as in

the sub class of ‘Valuation’ as well as

‘Completeness’. We want to appear to check in

case recorded values in accounts of cash as

well as bank reflect totality. In addition, not

anything has been eliminating (Carcello et al.,

2018). Finally, the revenue will maintain the

company’s retained earnings, therefore all

value that adjust this liability head have been

recorded appropriately as well as correctly.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNAL CONTROL AUDIT

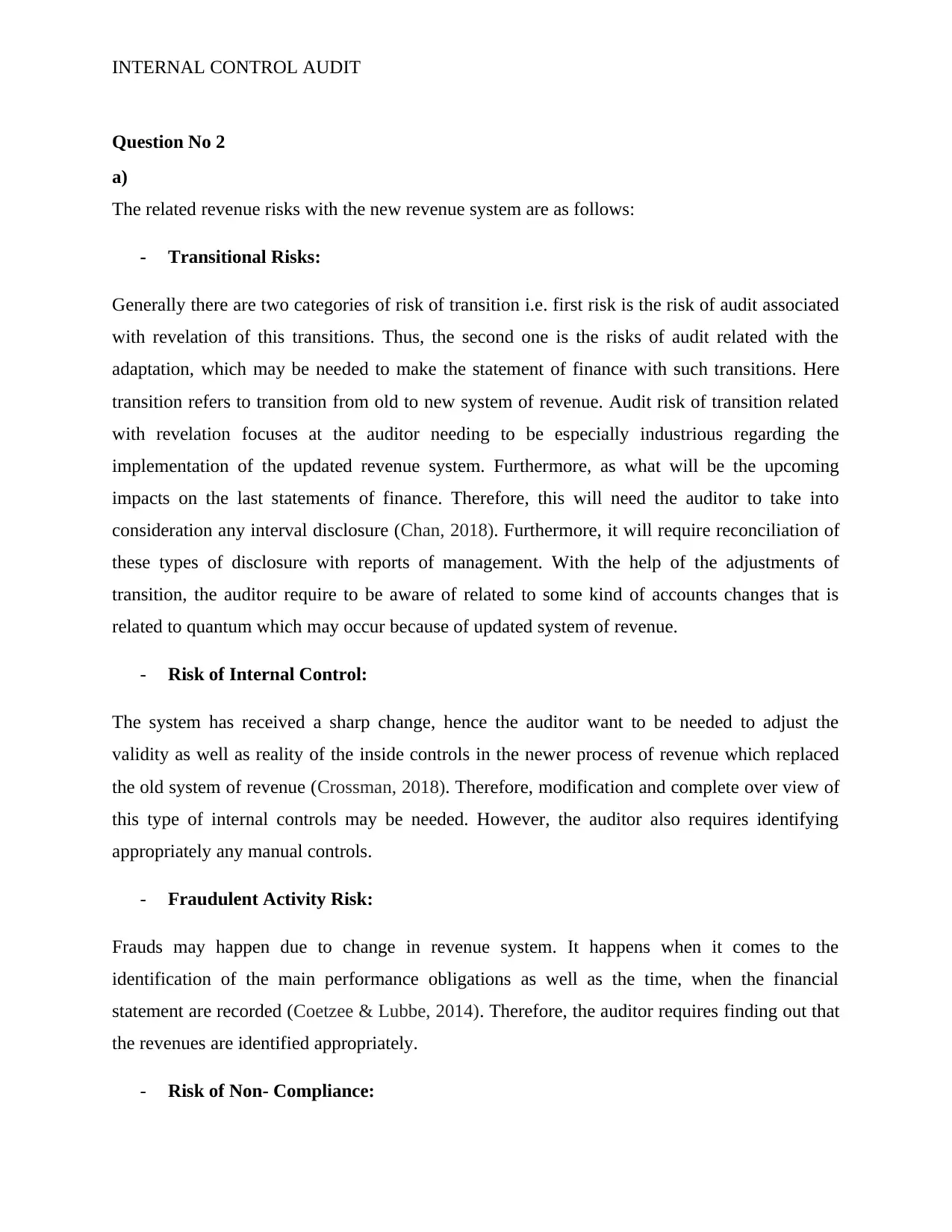

Question No 2

a)

The related revenue risks with the new revenue system are as follows:

- Transitional Risks:

Generally there are two categories of risk of transition i.e. first risk is the risk of audit associated

with revelation of this transitions. Thus, the second one is the risks of audit related with the

adaptation, which may be needed to make the statement of finance with such transitions. Here

transition refers to transition from old to new system of revenue. Audit risk of transition related

with revelation focuses at the auditor needing to be especially industrious regarding the

implementation of the updated revenue system. Furthermore, as what will be the upcoming

impacts on the last statements of finance. Therefore, this will need the auditor to take into

consideration any interval disclosure (Chan, 2018). Furthermore, it will require reconciliation of

these types of disclosure with reports of management. With the help of the adjustments of

transition, the auditor require to be aware of related to some kind of accounts changes that is

related to quantum which may occur because of updated system of revenue.

- Risk of Internal Control:

The system has received a sharp change, hence the auditor want to be needed to adjust the

validity as well as reality of the inside controls in the newer process of revenue which replaced

the old system of revenue (Crossman, 2018). Therefore, modification and complete over view of

this type of internal controls may be needed. However, the auditor also requires identifying

appropriately any manual controls.

- Fraudulent Activity Risk:

Frauds may happen due to change in revenue system. It happens when it comes to the

identification of the main performance obligations as well as the time, when the financial

statement are recorded (Coetzee & Lubbe, 2014). Therefore, the auditor requires finding out that

the revenues are identified appropriately.

- Risk of Non- Compliance:

Question No 2

a)

The related revenue risks with the new revenue system are as follows:

- Transitional Risks:

Generally there are two categories of risk of transition i.e. first risk is the risk of audit associated

with revelation of this transitions. Thus, the second one is the risks of audit related with the

adaptation, which may be needed to make the statement of finance with such transitions. Here

transition refers to transition from old to new system of revenue. Audit risk of transition related

with revelation focuses at the auditor needing to be especially industrious regarding the

implementation of the updated revenue system. Furthermore, as what will be the upcoming

impacts on the last statements of finance. Therefore, this will need the auditor to take into

consideration any interval disclosure (Chan, 2018). Furthermore, it will require reconciliation of

these types of disclosure with reports of management. With the help of the adjustments of

transition, the auditor require to be aware of related to some kind of accounts changes that is

related to quantum which may occur because of updated system of revenue.

- Risk of Internal Control:

The system has received a sharp change, hence the auditor want to be needed to adjust the

validity as well as reality of the inside controls in the newer process of revenue which replaced

the old system of revenue (Crossman, 2018). Therefore, modification and complete over view of

this type of internal controls may be needed. However, the auditor also requires identifying

appropriately any manual controls.

- Fraudulent Activity Risk:

Frauds may happen due to change in revenue system. It happens when it comes to the

identification of the main performance obligations as well as the time, when the financial

statement are recorded (Coetzee & Lubbe, 2014). Therefore, the auditor requires finding out that

the revenues are identified appropriately.

- Risk of Non- Compliance:

INTERNAL CONTROL AUDIT

When any changes in revenue mechanism takes place, risk occurs, therefore, the auditor should

be considering the same. This is the updated system in track to the related applicable of standards

of accounting to the organization (D'Onza & Sarens, 2018).

b)

During the internal audit, the following two questions must be asked:

1. What correction has been put into place to find out that the system of billing is not

compromised to provide a proper result?

2. What are the various backup facilities followed by St. Neville’s for the whole

information which provides as the main thing for the system of billing?

c)

For finding the system of revenue of St. Neville’s, the strategy of audit would take an approach

of “top- down risk assessment”. With the help of this top-down approach, the auditor detects as

well as minimizes any kind of risks that may survive at the completely organizational level or

process levels. There is a need to follow the approach of risk assessment due to transition from

St. Neville’s own system of revenue to DHL’s off the revenue system, as the transition may be

difficult. Furthermore, there may be some errors related with invoicing or maintenance of

records that may create issues (Davidson, Desai & Gerard, 2018). Therefore, the approaches of

“top- down risk assessment” will appear to enclose the overall system of revenue for removing

all the possible gaps.

When any changes in revenue mechanism takes place, risk occurs, therefore, the auditor should

be considering the same. This is the updated system in track to the related applicable of standards

of accounting to the organization (D'Onza & Sarens, 2018).

b)

During the internal audit, the following two questions must be asked:

1. What correction has been put into place to find out that the system of billing is not

compromised to provide a proper result?

2. What are the various backup facilities followed by St. Neville’s for the whole

information which provides as the main thing for the system of billing?

c)

For finding the system of revenue of St. Neville’s, the strategy of audit would take an approach

of “top- down risk assessment”. With the help of this top-down approach, the auditor detects as

well as minimizes any kind of risks that may survive at the completely organizational level or

process levels. There is a need to follow the approach of risk assessment due to transition from

St. Neville’s own system of revenue to DHL’s off the revenue system, as the transition may be

difficult. Furthermore, there may be some errors related with invoicing or maintenance of

records that may create issues (Davidson, Desai & Gerard, 2018). Therefore, the approaches of

“top- down risk assessment” will appear to enclose the overall system of revenue for removing

all the possible gaps.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNAL CONTROL AUDIT

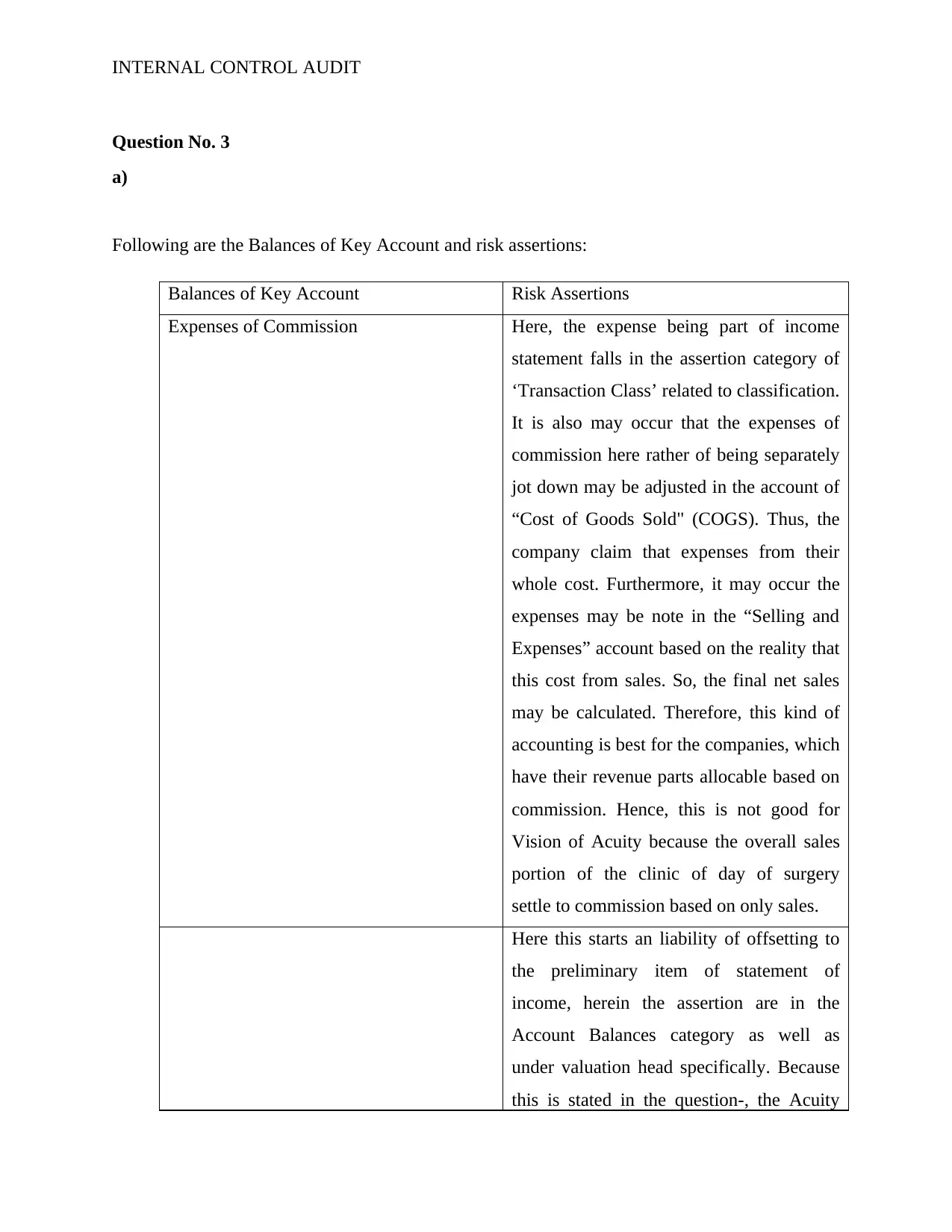

Question No. 3

a)

Following are the Balances of Key Account and risk assertions:

Balances of Key Account Risk Assertions

Expenses of Commission Here, the expense being part of income

statement falls in the assertion category of

‘Transaction Class’ related to classification.

It is also may occur that the expenses of

commission here rather of being separately

jot down may be adjusted in the account of

“Cost of Goods Sold" (COGS). Thus, the

company claim that expenses from their

whole cost. Furthermore, it may occur the

expenses may be note in the “Selling and

Expenses” account based on the reality that

this cost from sales. So, the final net sales

may be calculated. Therefore, this kind of

accounting is best for the companies, which

have their revenue parts allocable based on

commission. Hence, this is not good for

Vision of Acuity because the overall sales

portion of the clinic of day of surgery

settle to commission based on only sales.

Here this starts an liability of offsetting to

the preliminary item of statement of

income, herein the assertion are in the

Account Balances category as well as

under valuation head specifically. Because

this is stated in the question-, the Acuity

Question No. 3

a)

Following are the Balances of Key Account and risk assertions:

Balances of Key Account Risk Assertions

Expenses of Commission Here, the expense being part of income

statement falls in the assertion category of

‘Transaction Class’ related to classification.

It is also may occur that the expenses of

commission here rather of being separately

jot down may be adjusted in the account of

“Cost of Goods Sold" (COGS). Thus, the

company claim that expenses from their

whole cost. Furthermore, it may occur the

expenses may be note in the “Selling and

Expenses” account based on the reality that

this cost from sales. So, the final net sales

may be calculated. Therefore, this kind of

accounting is best for the companies, which

have their revenue parts allocable based on

commission. Hence, this is not good for

Vision of Acuity because the overall sales

portion of the clinic of day of surgery

settle to commission based on only sales.

Here this starts an liability of offsetting to

the preliminary item of statement of

income, herein the assertion are in the

Account Balances category as well as

under valuation head specifically. Because

this is stated in the question-, the Acuity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNAL CONTROL AUDIT

Vision succeeds its team of sales

immediately at the time of revenue

generation (Ege, 2014). To put in this place

there are various types of mechanisms.

Therefore, the company rather

appropriately the value of liability jot

downing may consider it from credit to

account of cash (Eulerich, Kremin &

Wood, 2019).

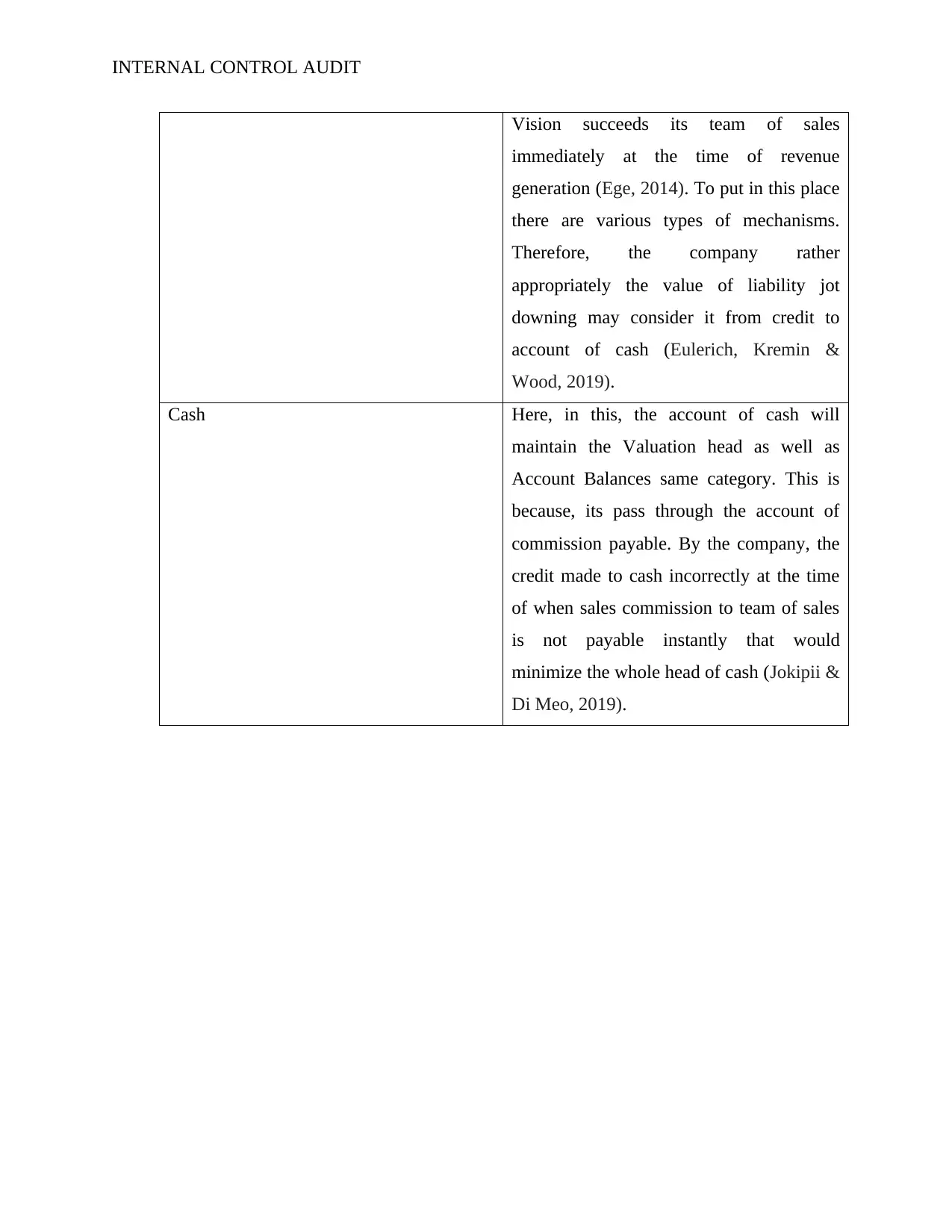

Cash Here, in this, the account of cash will

maintain the Valuation head as well as

Account Balances same category. This is

because, its pass through the account of

commission payable. By the company, the

credit made to cash incorrectly at the time

of when sales commission to team of sales

is not payable instantly that would

minimize the whole head of cash (Jokipii &

Di Meo, 2019).

Vision succeeds its team of sales

immediately at the time of revenue

generation (Ege, 2014). To put in this place

there are various types of mechanisms.

Therefore, the company rather

appropriately the value of liability jot

downing may consider it from credit to

account of cash (Eulerich, Kremin &

Wood, 2019).

Cash Here, in this, the account of cash will

maintain the Valuation head as well as

Account Balances same category. This is

because, its pass through the account of

commission payable. By the company, the

credit made to cash incorrectly at the time

of when sales commission to team of sales

is not payable instantly that would

minimize the whole head of cash (Jokipii &

Di Meo, 2019).

INTERNAL CONTROL AUDIT

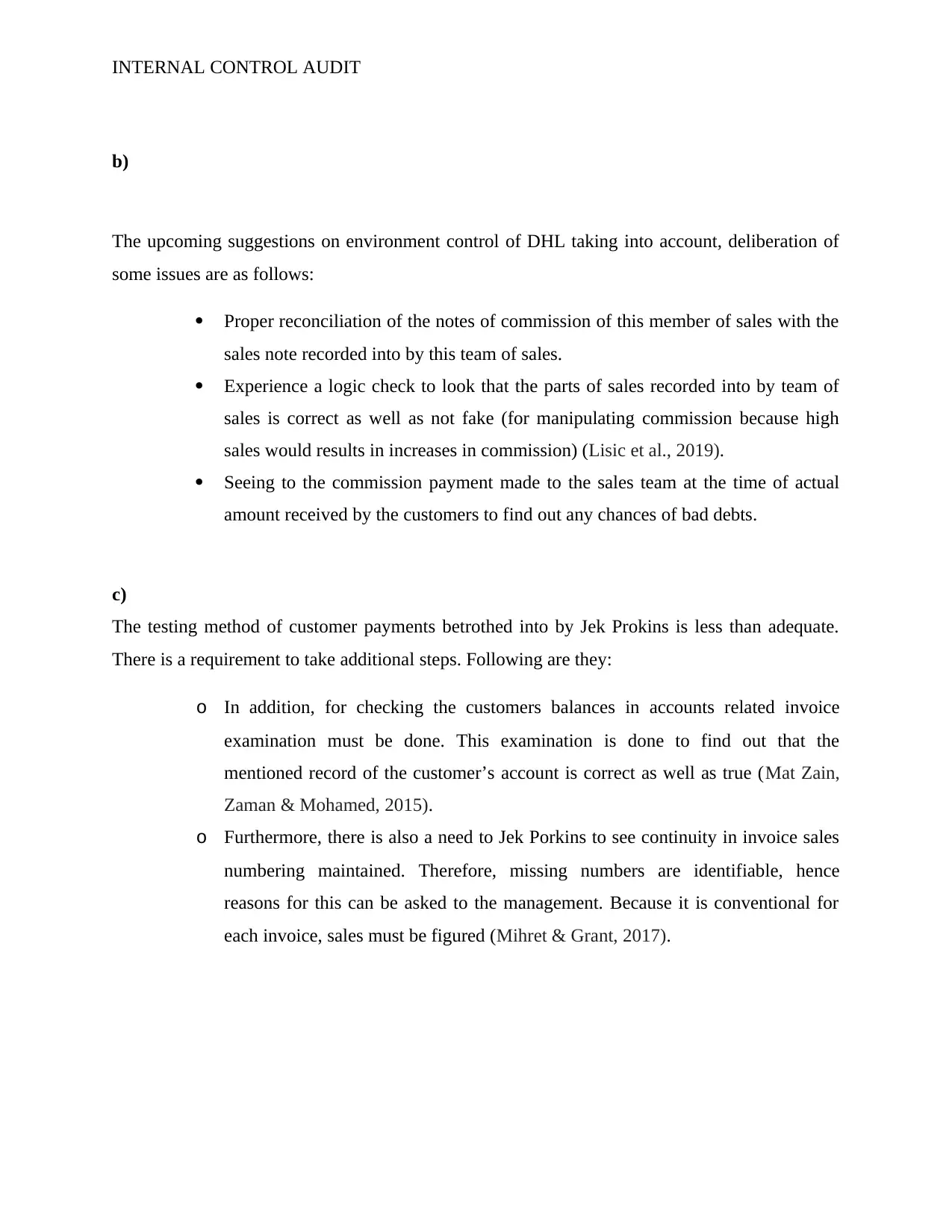

b)

The upcoming suggestions on environment control of DHL taking into account, deliberation of

some issues are as follows:

Proper reconciliation of the notes of commission of this member of sales with the

sales note recorded into by this team of sales.

Experience a logic check to look that the parts of sales recorded into by team of

sales is correct as well as not fake (for manipulating commission because high

sales would results in increases in commission) (Lisic et al., 2019).

Seeing to the commission payment made to the sales team at the time of actual

amount received by the customers to find out any chances of bad debts.

c)

The testing method of customer payments betrothed into by Jek Prokins is less than adequate.

There is a requirement to take additional steps. Following are they:

o In addition, for checking the customers balances in accounts related invoice

examination must be done. This examination is done to find out that the

mentioned record of the customer’s account is correct as well as true (Mat Zain,

Zaman & Mohamed, 2015).

o Furthermore, there is also a need to Jek Porkins to see continuity in invoice sales

numbering maintained. Therefore, missing numbers are identifiable, hence

reasons for this can be asked to the management. Because it is conventional for

each invoice, sales must be figured (Mihret & Grant, 2017).

b)

The upcoming suggestions on environment control of DHL taking into account, deliberation of

some issues are as follows:

Proper reconciliation of the notes of commission of this member of sales with the

sales note recorded into by this team of sales.

Experience a logic check to look that the parts of sales recorded into by team of

sales is correct as well as not fake (for manipulating commission because high

sales would results in increases in commission) (Lisic et al., 2019).

Seeing to the commission payment made to the sales team at the time of actual

amount received by the customers to find out any chances of bad debts.

c)

The testing method of customer payments betrothed into by Jek Prokins is less than adequate.

There is a requirement to take additional steps. Following are they:

o In addition, for checking the customers balances in accounts related invoice

examination must be done. This examination is done to find out that the

mentioned record of the customer’s account is correct as well as true (Mat Zain,

Zaman & Mohamed, 2015).

o Furthermore, there is also a need to Jek Porkins to see continuity in invoice sales

numbering maintained. Therefore, missing numbers are identifiable, hence

reasons for this can be asked to the management. Because it is conventional for

each invoice, sales must be figured (Mihret & Grant, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNAL CONTROL AUDIT

Question No. 4

Test Test Type Main Assertion Moderateness

of conclusion

Additional

Audit Process

1

Substantive

Test

The assertions

this test appears

to highlight is

the cut –off

assertion under

Transaction

Classes to find

whether the

payable of

accounts has

been

appropriately

recorded for

the time frame

under the

preview of this

particular audit.

Same class the

assertion based

on accuracy to

find out that the

payable account

reconcile with

the balances and

invoices of

supplier as well

Here it is stated

that not less than

85% of the

sample were

recorded. In

terms of the

quantum as well

as period, this

two had

mistakes

pertaining to

values involved

that are mini

scale. Therefore,

the conclusion

of the audit

reached is

acceptable

(Oussii, &

Boulila Taktak,

2018).

The additional

audit process

includes finding

that such

balances of

accounts

payable comply

with ‘Generally

Accepted

Accounting

Principles’

(GAAP). This

will be searched

with the help of

audit trail of this

type of

balances.

Furthermore,

the auditor can

experience a

lawful search of

suppliers to find

out, this has not

been prepared

any kind of fake

amounts

Question No. 4

Test Test Type Main Assertion Moderateness

of conclusion

Additional

Audit Process

1

Substantive

Test

The assertions

this test appears

to highlight is

the cut –off

assertion under

Transaction

Classes to find

whether the

payable of

accounts has

been

appropriately

recorded for

the time frame

under the

preview of this

particular audit.

Same class the

assertion based

on accuracy to

find out that the

payable account

reconcile with

the balances and

invoices of

supplier as well

Here it is stated

that not less than

85% of the

sample were

recorded. In

terms of the

quantum as well

as period, this

two had

mistakes

pertaining to

values involved

that are mini

scale. Therefore,

the conclusion

of the audit

reached is

acceptable

(Oussii, &

Boulila Taktak,

2018).

The additional

audit process

includes finding

that such

balances of

accounts

payable comply

with ‘Generally

Accepted

Accounting

Principles’

(GAAP). This

will be searched

with the help of

audit trail of this

type of

balances.

Furthermore,

the auditor can

experience a

lawful search of

suppliers to find

out, this has not

been prepared

any kind of fake

amounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNAL CONTROL AUDIT

as the Good

Received Notes

(GRNs)

payable of

accounts by

DHL. Finally,

With the help of

auditor, any

types of open

files having

paper trail or

paperwork,

which says

reconciled, must

be again

checked.

Therefore, audit

processes must

be designed

involving this

type of

searches.

2 Test of Control

The assertion

highlight with

this test involves

to correctness in

the head of

‘Transaction

Classes. Here, in

all the values

associated with

the discounts as

well as

amounting has

The conclusion

of audit so

extended cannot

be consider to be

acceptable due

to reality that 15

percent of the

whole sample of

test had

mistakes (three

from twenty ),

this errors are

Considering, the

conclusion of

audit so

extended is

unacceptable,

further audit

processes would

include

searching out

the main eras of

deficiency in

the process of

as the Good

Received Notes

(GRNs)

payable of

accounts by

DHL. Finally,

With the help of

auditor, any

types of open

files having

paper trail or

paperwork,

which says

reconciled, must

be again

checked.

Therefore, audit

processes must

be designed

involving this

type of

searches.

2 Test of Control

The assertion

highlight with

this test involves

to correctness in

the head of

‘Transaction

Classes. Here, in

all the values

associated with

the discounts as

well as

amounting has

The conclusion

of audit so

extended cannot

be consider to be

acceptable due

to reality that 15

percent of the

whole sample of

test had

mistakes (three

from twenty ),

this errors are

Considering, the

conclusion of

audit so

extended is

unacceptable,

further audit

processes would

include

searching out

the main eras of

deficiency in

the process of

INTERNAL CONTROL AUDIT

been properly

quantified.

Therefore, there

is non-existence

of any errors

with respect to

the correctness

as well as

appropriateness

related to the

same (Pizzini,

Lin, &

Ziegenfuss,

2014).

material.

Appeal of

misleading rates

of deduction

will

correspondingly

over state as

well as

understate the

account of

indirect income.

"Discount

received" as

well as it will

affect the

balances of

accounts

payable.

Furthermore, if

with the help of

purchase

manager if such

type of invoices

are not

authorized, it

may like that

DHL want to

enter a system

where there are

fictitious bills of

suppliers. This

inside or

internal control.

Furthermore,

the department

as well as the

person who all

are responsible

for fulfill this

invoices must

be brought

under audit

preview. Hence,

they can see

how the

invoices are

prepared with

the incorrect

rates of

discounts at the

time when these

statements were

not sanction

with the help of

the Manager of

Purchase.

been properly

quantified.

Therefore, there

is non-existence

of any errors

with respect to

the correctness

as well as

appropriateness

related to the

same (Pizzini,

Lin, &

Ziegenfuss,

2014).

material.

Appeal of

misleading rates

of deduction

will

correspondingly

over state as

well as

understate the

account of

indirect income.

"Discount

received" as

well as it will

affect the

balances of

accounts

payable.

Furthermore, if

with the help of

purchase

manager if such

type of invoices

are not

authorized, it

may like that

DHL want to

enter a system

where there are

fictitious bills of

suppliers. This

inside or

internal control.

Furthermore,

the department

as well as the

person who all

are responsible

for fulfill this

invoices must

be brought

under audit

preview. Hence,

they can see

how the

invoices are

prepared with

the incorrect

rates of

discounts at the

time when these

statements were

not sanction

with the help of

the Manager of

Purchase.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.