Evaluation and Revision of Diabetes Clinic Proposal for NHS Trust

VerifiedAdded on 2023/06/10

|17

|4745

|354

Report

AI Summary

This report evaluates a proposal to open a new diabetes clinic in the UK, addressing the rising prevalence of diabetes. The analysis begins with an investment appraisal using techniques like Net Present Value (NPV), Internal Rate of Return (IRR), and payback period to assess the financial viability of the initial proposal. The evaluation reveals negative NPV and zero IRR, indicating the project's unprofitability under the given financial model. The report then revises the proposal, focusing on strategies to improve financial budgeting, such as reducing fixed costs through technology investments and exploring external and internal financing options. External financing options include commercial bank loans, issuing shares, and government grants, while internal financing focuses on retained earnings. The revised proposal aims to increase annual revenue to achieve a target IRR of at least 8% and achieve a break-even point within the project's five-year timeframe. Ultimately, the report suggests that the initial proposal should be rejected due to its financial shortcomings, and emphasizes the need for cost reduction and revenue enhancement strategies to make the project financially sustainable. The report highlights the significance of investment appraisal techniques in healthcare financial planning.

Indicative project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Part - A.........................................................................................................................................3

Part – B........................................................................................................................................6

Part – C........................................................................................................................................9

Part – D......................................................................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Part - A.........................................................................................................................................3

Part – B........................................................................................................................................6

Part – C........................................................................................................................................9

Part – D......................................................................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

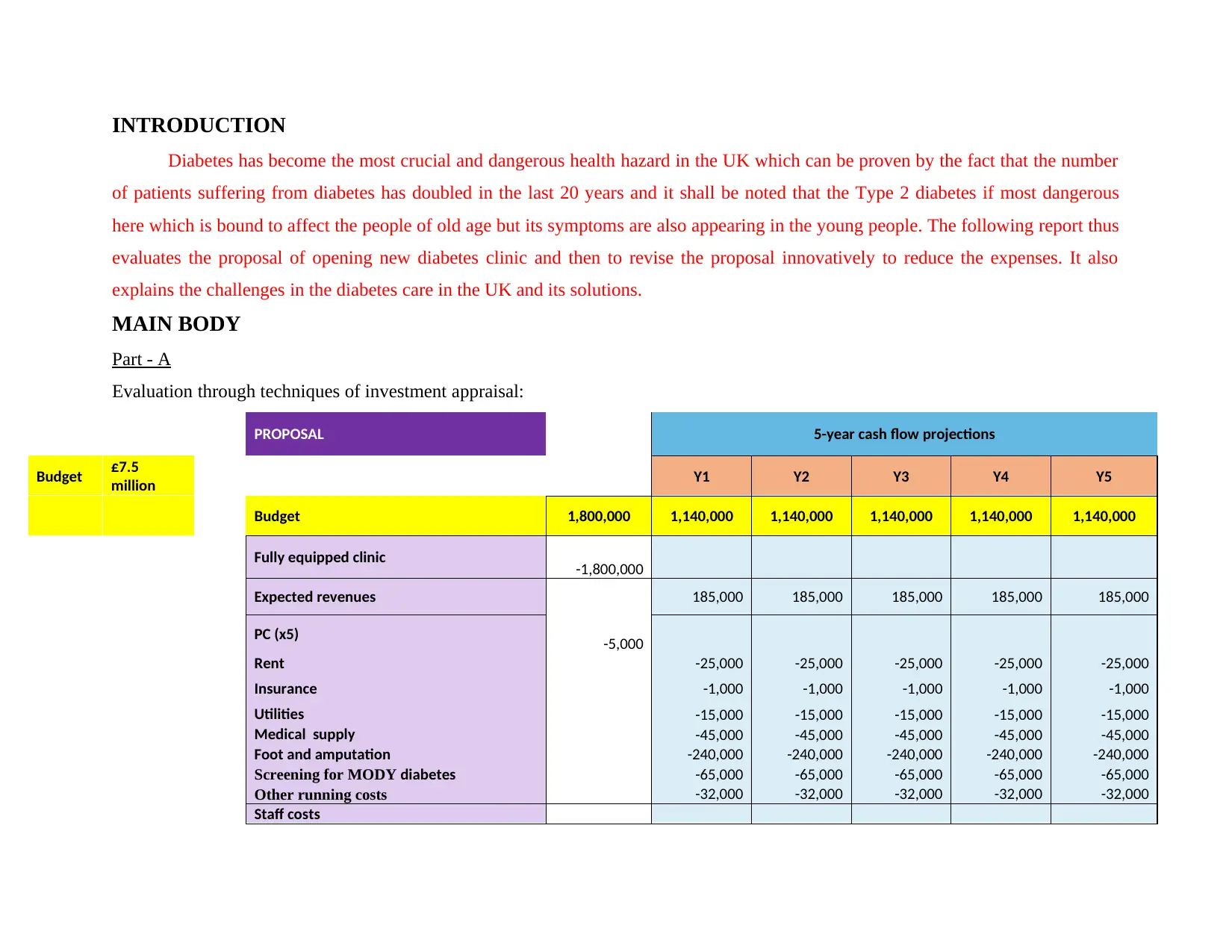

INTRODUCTION

Diabetes has become the most crucial and dangerous health hazard in the UK which can be proven by the fact that the number

of patients suffering from diabetes has doubled in the last 20 years and it shall be noted that the Type 2 diabetes if most dangerous

here which is bound to affect the people of old age but its symptoms are also appearing in the young people. The following report thus

evaluates the proposal of opening new diabetes clinic and then to revise the proposal innovatively to reduce the expenses. It also

explains the challenges in the diabetes care in the UK and its solutions.

MAIN BODY

Part - A

Evaluation through techniques of investment appraisal:

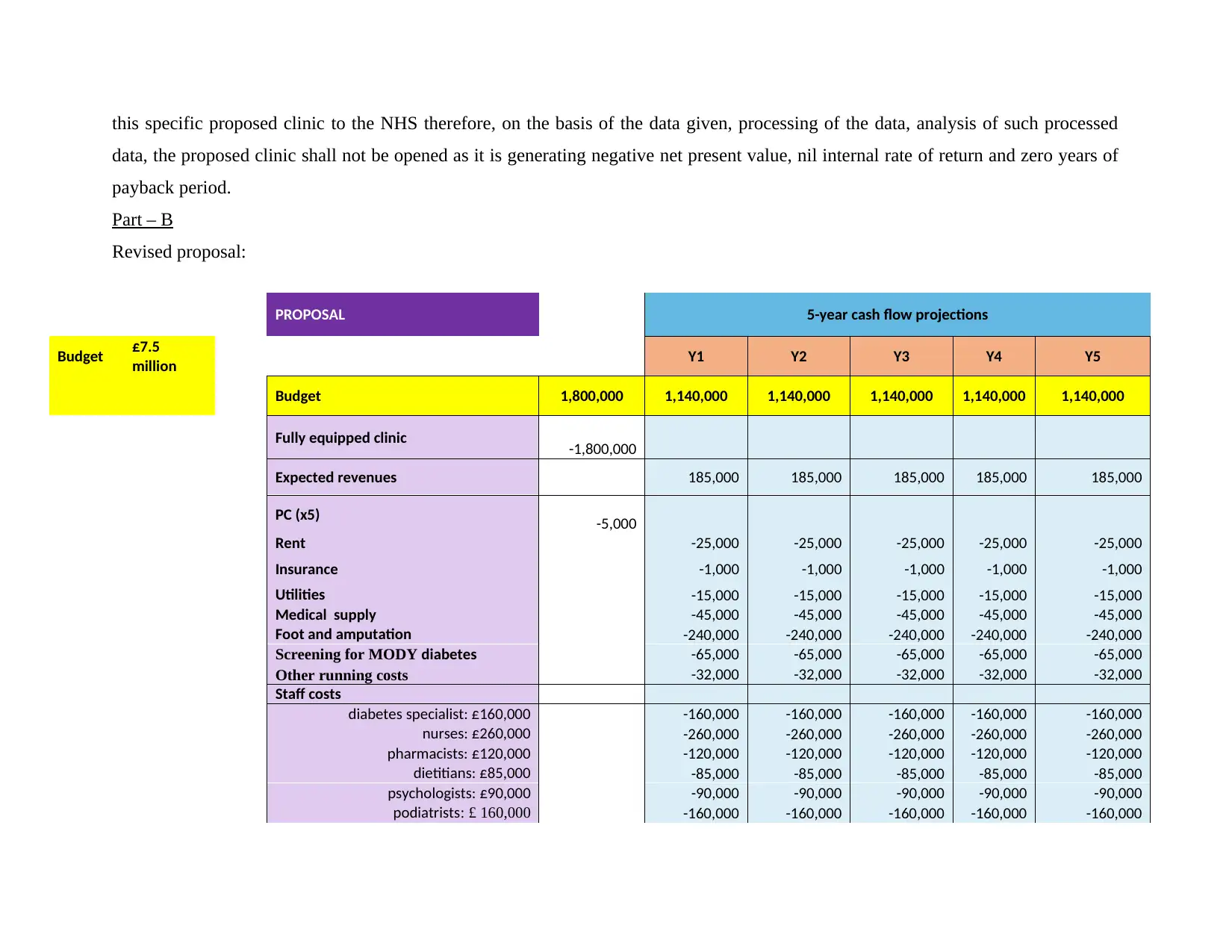

PROPOSAL 5-year cash flow projections

Budget £7.5

million Y1 Y2 Y3 Y4 Y5

Budget 1,800,000 1,140,000 1,140,000 1,140,000 1,140,000 1,140,000

Fully equipped clinic -1,800,000

Expected revenues 185,000 185,000 185,000 185,000 185,000

PC (x5) -5,000

Rent -25,000 -25,000 -25,000 -25,000 -25,000

Insurance -1,000 -1,000 -1,000 -1,000 -1,000

Utilities -15,000 -15,000 -15,000 -15,000 -15,000

Medical supply -45,000 -45,000 -45,000 -45,000 -45,000

Foot and amputation -240,000 -240,000 -240,000 -240,000 -240,000

Screening for MODY diabetes -65,000 -65,000 -65,000 -65,000 -65,000

Other running costs -32,000 -32,000 -32,000 -32,000 -32,000

Staff costs

Diabetes has become the most crucial and dangerous health hazard in the UK which can be proven by the fact that the number

of patients suffering from diabetes has doubled in the last 20 years and it shall be noted that the Type 2 diabetes if most dangerous

here which is bound to affect the people of old age but its symptoms are also appearing in the young people. The following report thus

evaluates the proposal of opening new diabetes clinic and then to revise the proposal innovatively to reduce the expenses. It also

explains the challenges in the diabetes care in the UK and its solutions.

MAIN BODY

Part - A

Evaluation through techniques of investment appraisal:

PROPOSAL 5-year cash flow projections

Budget £7.5

million Y1 Y2 Y3 Y4 Y5

Budget 1,800,000 1,140,000 1,140,000 1,140,000 1,140,000 1,140,000

Fully equipped clinic -1,800,000

Expected revenues 185,000 185,000 185,000 185,000 185,000

PC (x5) -5,000

Rent -25,000 -25,000 -25,000 -25,000 -25,000

Insurance -1,000 -1,000 -1,000 -1,000 -1,000

Utilities -15,000 -15,000 -15,000 -15,000 -15,000

Medical supply -45,000 -45,000 -45,000 -45,000 -45,000

Foot and amputation -240,000 -240,000 -240,000 -240,000 -240,000

Screening for MODY diabetes -65,000 -65,000 -65,000 -65,000 -65,000

Other running costs -32,000 -32,000 -32,000 -32,000 -32,000

Staff costs

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

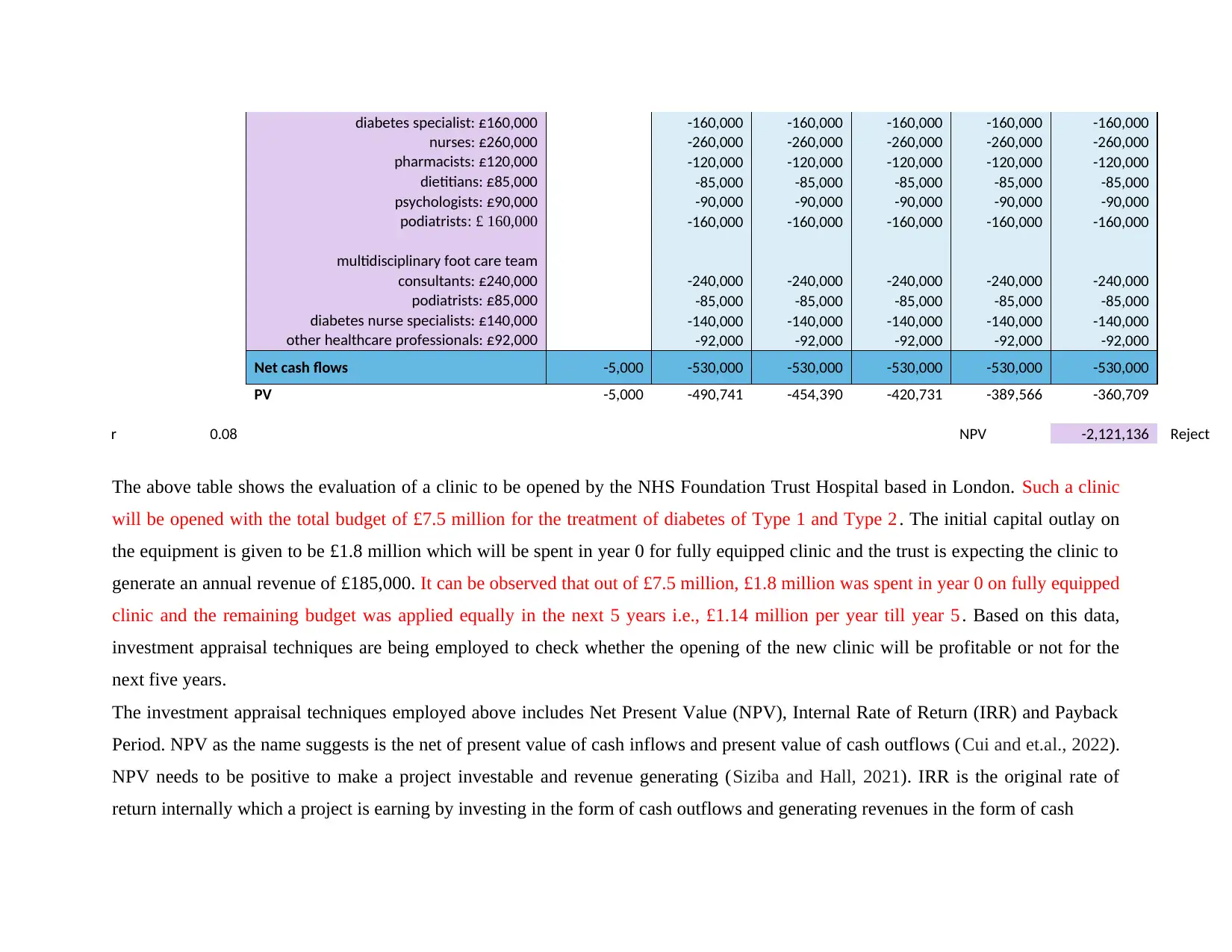

diabetes specialist: £160,000 -160,000 -160,000 -160,000 -160,000 -160,000

nurses: £260,000 -260,000 -260,000 -260,000 -260,000 -260,000

pharmacists: £120,000 -120,000 -120,000 -120,000 -120,000 -120,000

dietitians: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

psychologists: £90,000 -90,000 -90,000 -90,000 -90,000 -90,000

podiatrists: £ 160,000 -160,000 -160,000 -160,000 -160,000 -160,000

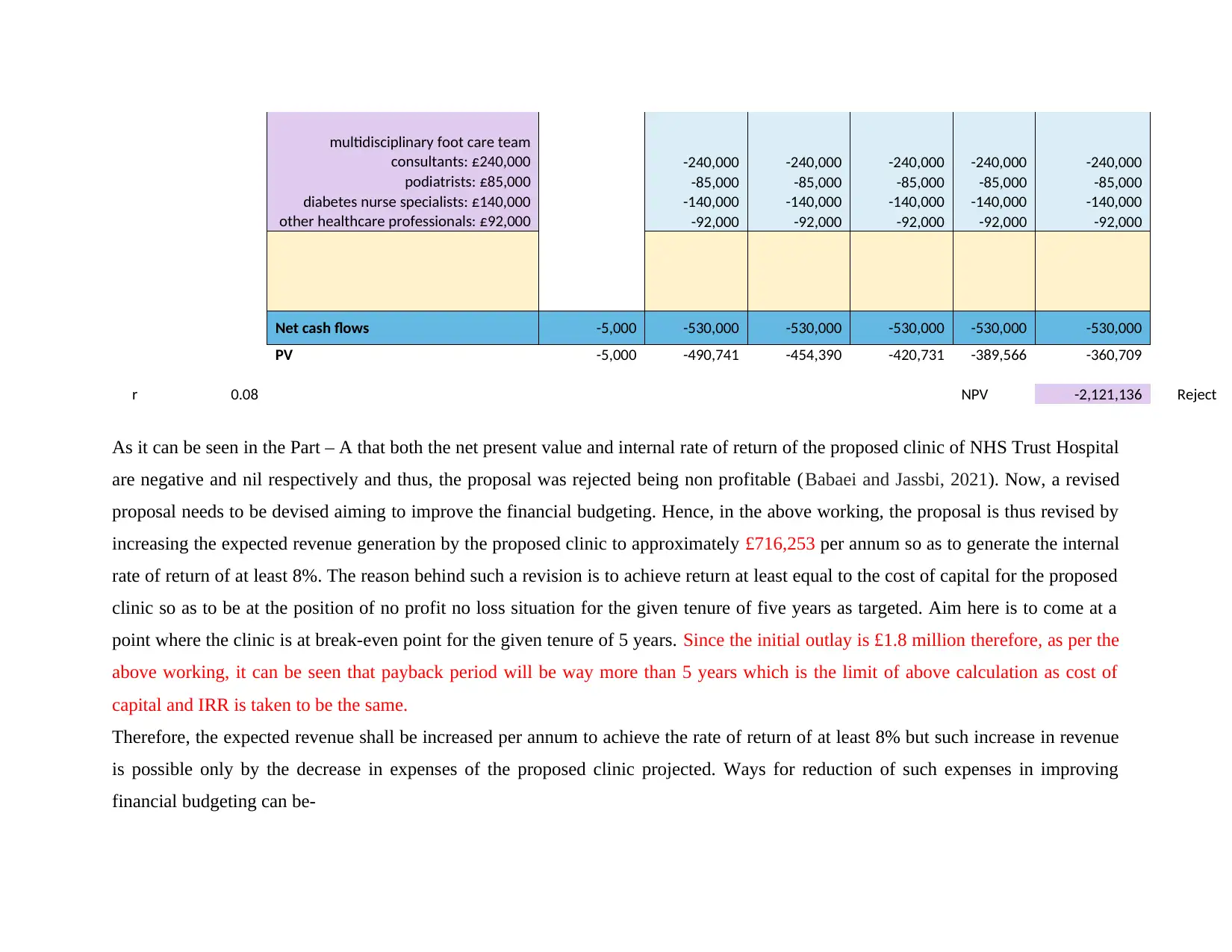

multidisciplinary foot care team

consultants: £240,000 -240,000 -240,000 -240,000 -240,000 -240,000

podiatrists: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

diabetes nurse specialists: £140,000 -140,000 -140,000 -140,000 -140,000 -140,000

other healthcare professionals: £92,000 -92,000 -92,000 -92,000 -92,000 -92,000

Net cash flows -5,000 -530,000 -530,000 -530,000 -530,000 -530,000

PV -5,000 -490,741 -454,390 -420,731 -389,566 -360,709

r 0.08 NPV -2,121,136 Reject

The above table shows the evaluation of a clinic to be opened by the NHS Foundation Trust Hospital based in London. Such a clinic

will be opened with the total budget of £7.5 million for the treatment of diabetes of Type 1 and Type 2 . The initial capital outlay on

the equipment is given to be £1.8 million which will be spent in year 0 for fully equipped clinic and the trust is expecting the clinic to

generate an annual revenue of £185,000. It can be observed that out of £7.5 million, £1.8 million was spent in year 0 on fully equipped

clinic and the remaining budget was applied equally in the next 5 years i.e., £1.14 million per year till year 5 . Based on this data,

investment appraisal techniques are being employed to check whether the opening of the new clinic will be profitable or not for the

next five years.

The investment appraisal techniques employed above includes Net Present Value (NPV), Internal Rate of Return (IRR) and Payback

Period. NPV as the name suggests is the net of present value of cash inflows and present value of cash outflows (Cui and et.al., 2022).

NPV needs to be positive to make a project investable and revenue generating (Siziba and Hall, 2021). IRR is the original rate of

return internally which a project is earning by investing in the form of cash outflows and generating revenues in the form of cash

nurses: £260,000 -260,000 -260,000 -260,000 -260,000 -260,000

pharmacists: £120,000 -120,000 -120,000 -120,000 -120,000 -120,000

dietitians: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

psychologists: £90,000 -90,000 -90,000 -90,000 -90,000 -90,000

podiatrists: £ 160,000 -160,000 -160,000 -160,000 -160,000 -160,000

multidisciplinary foot care team

consultants: £240,000 -240,000 -240,000 -240,000 -240,000 -240,000

podiatrists: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

diabetes nurse specialists: £140,000 -140,000 -140,000 -140,000 -140,000 -140,000

other healthcare professionals: £92,000 -92,000 -92,000 -92,000 -92,000 -92,000

Net cash flows -5,000 -530,000 -530,000 -530,000 -530,000 -530,000

PV -5,000 -490,741 -454,390 -420,731 -389,566 -360,709

r 0.08 NPV -2,121,136 Reject

The above table shows the evaluation of a clinic to be opened by the NHS Foundation Trust Hospital based in London. Such a clinic

will be opened with the total budget of £7.5 million for the treatment of diabetes of Type 1 and Type 2 . The initial capital outlay on

the equipment is given to be £1.8 million which will be spent in year 0 for fully equipped clinic and the trust is expecting the clinic to

generate an annual revenue of £185,000. It can be observed that out of £7.5 million, £1.8 million was spent in year 0 on fully equipped

clinic and the remaining budget was applied equally in the next 5 years i.e., £1.14 million per year till year 5 . Based on this data,

investment appraisal techniques are being employed to check whether the opening of the new clinic will be profitable or not for the

next five years.

The investment appraisal techniques employed above includes Net Present Value (NPV), Internal Rate of Return (IRR) and Payback

Period. NPV as the name suggests is the net of present value of cash inflows and present value of cash outflows (Cui and et.al., 2022).

NPV needs to be positive to make a project investable and revenue generating (Siziba and Hall, 2021). IRR is the original rate of

return internally which a project is earning by investing in the form of cash outflows and generating revenues in the form of cash

inflows. It is the annual rate of return at which net present value of the project will be zero i.e.,

no profit no loss situation. Therefore, IRR shall have to be positive to be able to invest in a

project (Dabbicco and Mattei, 2021). Payback period as the name suggests means the period in

which the initial outlay of project is being recovered and the project starts to generate profits and

savings. The payback period needs to be less than the total tenure of the product to make it

eligible to be investible.

In the above calculation as the initial outlay is £1.8 million and the revenue per annum is

£185,000. So taking into account all the expenditures estimated by NHS of the new clinic to be

established categorized under staff costs, multi – disciplinary footcare team and other costs, net

cash flows of all the years comes out to be negative i.e., cash outflow instead of cash inflow from

such new clinic of NHS. So the NPV is coming at -£2,121,136 which is natural because with

such a huge outlay and such meagre revenues the clinic needs more time than 5 years to be able

to generate positive NPV. And as the NPV came negative, the IRR cannot be calculated because

the net cash flows come out to be negative from the Year 0 till the Year 5 of the budget of the

clinic i.e., the revenue needs more time than 5 years to be able to generate positive IRR (Crosby,

Devaney and Wyatt, 2018). And since the NPV is negative for all 5 years, therefore, payback

period cannot be calculated in the first 5 years of the operations of the clinic i.e., it needs to

operate for a longer period of time to produce the payback period.

It can also be observed that various other costs are given in the data provided like insurance,

utilities, rent, screening for MODY diabetes, overtime costs, medical supplies, staff costs of

diabetes specialists, nurses, pharmacists, dietitians, psychologists, podiatrists, multidisciplinary

footcare team of consultants, podiatrists, diabetes nurse specialists and other health care

professionals, overtime costs, foot and amputation costs, other running costs, etc. but if such

costs are not taken in the employment of the investment appraisal techniques, the clinic will still

yield negative net present value, negative internal rate of return and zero payback period

therefore, considering or not considering the above expenditures will not affect the decision of

setting up the diabetes clinic as in both the cases NHS will not be able to generate positive

returns or even break – even returns to keep the outflows compensated with the inflows from the

project.

It is also said that setting up of multidisciplinary footcare services in the clinics and hospitals

could lead to savings of up to £117 million but it not certain that how much savings will be from

no profit no loss situation. Therefore, IRR shall have to be positive to be able to invest in a

project (Dabbicco and Mattei, 2021). Payback period as the name suggests means the period in

which the initial outlay of project is being recovered and the project starts to generate profits and

savings. The payback period needs to be less than the total tenure of the product to make it

eligible to be investible.

In the above calculation as the initial outlay is £1.8 million and the revenue per annum is

£185,000. So taking into account all the expenditures estimated by NHS of the new clinic to be

established categorized under staff costs, multi – disciplinary footcare team and other costs, net

cash flows of all the years comes out to be negative i.e., cash outflow instead of cash inflow from

such new clinic of NHS. So the NPV is coming at -£2,121,136 which is natural because with

such a huge outlay and such meagre revenues the clinic needs more time than 5 years to be able

to generate positive NPV. And as the NPV came negative, the IRR cannot be calculated because

the net cash flows come out to be negative from the Year 0 till the Year 5 of the budget of the

clinic i.e., the revenue needs more time than 5 years to be able to generate positive IRR (Crosby,

Devaney and Wyatt, 2018). And since the NPV is negative for all 5 years, therefore, payback

period cannot be calculated in the first 5 years of the operations of the clinic i.e., it needs to

operate for a longer period of time to produce the payback period.

It can also be observed that various other costs are given in the data provided like insurance,

utilities, rent, screening for MODY diabetes, overtime costs, medical supplies, staff costs of

diabetes specialists, nurses, pharmacists, dietitians, psychologists, podiatrists, multidisciplinary

footcare team of consultants, podiatrists, diabetes nurse specialists and other health care

professionals, overtime costs, foot and amputation costs, other running costs, etc. but if such

costs are not taken in the employment of the investment appraisal techniques, the clinic will still

yield negative net present value, negative internal rate of return and zero payback period

therefore, considering or not considering the above expenditures will not affect the decision of

setting up the diabetes clinic as in both the cases NHS will not be able to generate positive

returns or even break – even returns to keep the outflows compensated with the inflows from the

project.

It is also said that setting up of multidisciplinary footcare services in the clinics and hospitals

could lead to savings of up to £117 million but it not certain that how much savings will be from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this specific proposed clinic to the NHS therefore, on the basis of the data given, processing of the data, analysis of such processed

data, the proposed clinic shall not be opened as it is generating negative net present value, nil internal rate of return and zero years of

payback period.

Part – B

Revised proposal:

PROPOSAL 5-year cash flow projections

Budget £7.5

million Y1 Y2 Y3 Y4 Y5

Budget 1,800,000 1,140,000 1,140,000 1,140,000 1,140,000 1,140,000

Fully equipped clinic -1,800,000

Expected revenues 185,000 185,000 185,000 185,000 185,000

PC (x5) -5,000

Rent -25,000 -25,000 -25,000 -25,000 -25,000

Insurance -1,000 -1,000 -1,000 -1,000 -1,000

Utilities -15,000 -15,000 -15,000 -15,000 -15,000

Medical supply -45,000 -45,000 -45,000 -45,000 -45,000

Foot and amputation -240,000 -240,000 -240,000 -240,000 -240,000

Screening for MODY diabetes -65,000 -65,000 -65,000 -65,000 -65,000

Other running costs -32,000 -32,000 -32,000 -32,000 -32,000

Staff costs

diabetes specialist: £160,000 -160,000 -160,000 -160,000 -160,000 -160,000

nurses: £260,000 -260,000 -260,000 -260,000 -260,000 -260,000

pharmacists: £120,000 -120,000 -120,000 -120,000 -120,000 -120,000

dietitians: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

psychologists: £90,000 -90,000 -90,000 -90,000 -90,000 -90,000

podiatrists: £ 160,000 -160,000 -160,000 -160,000 -160,000 -160,000

data, the proposed clinic shall not be opened as it is generating negative net present value, nil internal rate of return and zero years of

payback period.

Part – B

Revised proposal:

PROPOSAL 5-year cash flow projections

Budget £7.5

million Y1 Y2 Y3 Y4 Y5

Budget 1,800,000 1,140,000 1,140,000 1,140,000 1,140,000 1,140,000

Fully equipped clinic -1,800,000

Expected revenues 185,000 185,000 185,000 185,000 185,000

PC (x5) -5,000

Rent -25,000 -25,000 -25,000 -25,000 -25,000

Insurance -1,000 -1,000 -1,000 -1,000 -1,000

Utilities -15,000 -15,000 -15,000 -15,000 -15,000

Medical supply -45,000 -45,000 -45,000 -45,000 -45,000

Foot and amputation -240,000 -240,000 -240,000 -240,000 -240,000

Screening for MODY diabetes -65,000 -65,000 -65,000 -65,000 -65,000

Other running costs -32,000 -32,000 -32,000 -32,000 -32,000

Staff costs

diabetes specialist: £160,000 -160,000 -160,000 -160,000 -160,000 -160,000

nurses: £260,000 -260,000 -260,000 -260,000 -260,000 -260,000

pharmacists: £120,000 -120,000 -120,000 -120,000 -120,000 -120,000

dietitians: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

psychologists: £90,000 -90,000 -90,000 -90,000 -90,000 -90,000

podiatrists: £ 160,000 -160,000 -160,000 -160,000 -160,000 -160,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

multidisciplinary foot care team

consultants: £240,000 -240,000 -240,000 -240,000 -240,000 -240,000

podiatrists: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

diabetes nurse specialists: £140,000 -140,000 -140,000 -140,000 -140,000 -140,000

other healthcare professionals: £92,000 -92,000 -92,000 -92,000 -92,000 -92,000

Net cash flows -5,000 -530,000 -530,000 -530,000 -530,000 -530,000

PV -5,000 -490,741 -454,390 -420,731 -389,566 -360,709

r 0.08 NPV -2,121,136 Reject

As it can be seen in the Part – A that both the net present value and internal rate of return of the proposed clinic of NHS Trust Hospital

are negative and nil respectively and thus, the proposal was rejected being non profitable (Babaei and Jassbi, 2021). Now, a revised

proposal needs to be devised aiming to improve the financial budgeting. Hence, in the above working, the proposal is thus revised by

increasing the expected revenue generation by the proposed clinic to approximately £716,253 per annum so as to generate the internal

rate of return of at least 8%. The reason behind such a revision is to achieve return at least equal to the cost of capital for the proposed

clinic so as to be at the position of no profit no loss situation for the given tenure of five years as targeted. Aim here is to come at a

point where the clinic is at break-even point for the given tenure of 5 years. Since the initial outlay is £1.8 million therefore, as per the

above working, it can be seen that payback period will be way more than 5 years which is the limit of above calculation as cost of

capital and IRR is taken to be the same.

Therefore, the expected revenue shall be increased per annum to achieve the rate of return of at least 8% but such increase in revenue

is possible only by the decrease in expenses of the proposed clinic projected. Ways for reduction of such expenses in improving

financial budgeting can be-

consultants: £240,000 -240,000 -240,000 -240,000 -240,000 -240,000

podiatrists: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

diabetes nurse specialists: £140,000 -140,000 -140,000 -140,000 -140,000 -140,000

other healthcare professionals: £92,000 -92,000 -92,000 -92,000 -92,000 -92,000

Net cash flows -5,000 -530,000 -530,000 -530,000 -530,000 -530,000

PV -5,000 -490,741 -454,390 -420,731 -389,566 -360,709

r 0.08 NPV -2,121,136 Reject

As it can be seen in the Part – A that both the net present value and internal rate of return of the proposed clinic of NHS Trust Hospital

are negative and nil respectively and thus, the proposal was rejected being non profitable (Babaei and Jassbi, 2021). Now, a revised

proposal needs to be devised aiming to improve the financial budgeting. Hence, in the above working, the proposal is thus revised by

increasing the expected revenue generation by the proposed clinic to approximately £716,253 per annum so as to generate the internal

rate of return of at least 8%. The reason behind such a revision is to achieve return at least equal to the cost of capital for the proposed

clinic so as to be at the position of no profit no loss situation for the given tenure of five years as targeted. Aim here is to come at a

point where the clinic is at break-even point for the given tenure of 5 years. Since the initial outlay is £1.8 million therefore, as per the

above working, it can be seen that payback period will be way more than 5 years which is the limit of above calculation as cost of

capital and IRR is taken to be the same.

Therefore, the expected revenue shall be increased per annum to achieve the rate of return of at least 8% but such increase in revenue

is possible only by the decrease in expenses of the proposed clinic projected. Ways for reduction of such expenses in improving

financial budgeting can be-

To focus on the fixed costs incurred by the entities and not ignore them. These will be

incurred consistently for long period of time therefore, any opportunity to be able to save

these costs can be very beneficial for the entity. This can be done by fairly exploring through

various options of availing services in return of fixed costs and settle at the minimum one.

Try grabbing better prices from the competitor suppliers which will definitely result in

reduction of fixed costs.

Investment in technology which will help achieve maximum efficiency and help reduce

redundant activities on which incurring cost was unnecessary and thus will increase the

productivity of the entity. Like, the GIRFT advised that implementing the multidisciplinary

footcare services can result in savings of up to £117 million to the NHS (Pankhurst and

Edmonds, 2018). These savings to the NHS are because of reduction in the length of

admissions, readmissions and stay.

Sources of finance:

External Financing –

Finance from commercial banks – One of the most common sources of finance for any entity

is loans from commercial banks which are available to the entities depending upon their

credibility, forecasted financial statements, etc. Such loans are usually provided for a year

and may extend up to the tenure requested by the entity as longer will be the tenure, more

will be the interest income of the banks.

Issuing of own shares – Another way of raising funds for the operations of the entity is by

issuing of own shares in the form of Initial Public Offer (IPO) or Further Public Offer (FPO)

(Shrotriya, 2019). This kind of financing is only apt for large scale entities as the process of

issuing own shares in the market is very complex and requires assistance by various experts

and legal advisories.

Government grants and subsidiaries – For entities like NHS, best way to fund the opening up

of clinics and hospitals is through government grants and subsidiaries (Sources of Funding.

2022). Although getting grants and subsidiaries in itself is a tedious task as the explanation is

to be given regarding detail of the project, income, revenue or benefits of the project,

forecasts of the projects of several years, and other legal formalities which will require

assistance of experts and legal advisories.

Internal Financing –

incurred consistently for long period of time therefore, any opportunity to be able to save

these costs can be very beneficial for the entity. This can be done by fairly exploring through

various options of availing services in return of fixed costs and settle at the minimum one.

Try grabbing better prices from the competitor suppliers which will definitely result in

reduction of fixed costs.

Investment in technology which will help achieve maximum efficiency and help reduce

redundant activities on which incurring cost was unnecessary and thus will increase the

productivity of the entity. Like, the GIRFT advised that implementing the multidisciplinary

footcare services can result in savings of up to £117 million to the NHS (Pankhurst and

Edmonds, 2018). These savings to the NHS are because of reduction in the length of

admissions, readmissions and stay.

Sources of finance:

External Financing –

Finance from commercial banks – One of the most common sources of finance for any entity

is loans from commercial banks which are available to the entities depending upon their

credibility, forecasted financial statements, etc. Such loans are usually provided for a year

and may extend up to the tenure requested by the entity as longer will be the tenure, more

will be the interest income of the banks.

Issuing of own shares – Another way of raising funds for the operations of the entity is by

issuing of own shares in the form of Initial Public Offer (IPO) or Further Public Offer (FPO)

(Shrotriya, 2019). This kind of financing is only apt for large scale entities as the process of

issuing own shares in the market is very complex and requires assistance by various experts

and legal advisories.

Government grants and subsidiaries – For entities like NHS, best way to fund the opening up

of clinics and hospitals is through government grants and subsidiaries (Sources of Funding.

2022). Although getting grants and subsidiaries in itself is a tedious task as the explanation is

to be given regarding detail of the project, income, revenue or benefits of the project,

forecasts of the projects of several years, and other legal formalities which will require

assistance of experts and legal advisories.

Internal Financing –

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Retained earnings – Retained earnings are a source of internal financing for the organisation

on which no costs have to be incurred and is earned from the earnings and profits of the same

through its operations.

National Health Services (NHS) is prominently funded through taxation in general from the

public to the government of various types of taxes and another prominent source of funding is

contributions from the national insurance. Such national insurance contributions are made by the

employers as well as employees out of their remunerations to the government and then utilized

by the government in the funding of NHS.

Current challenges in diabetes care in the UK:

Assessment of various measures and provision established in the UK for care of diabetes

shows no significant measurable key performance indicators (KPIs). There are signification

variations in the data collected and relevance of such data across the UK.

There are significant variations in the care methods devised across the UK which are due to

clinical, local, financial, regional or even demographic factors.

Education among the patients who are diagnosed currently and the ones who are ill for a long

time is seen as an obstacle. These people do not attend the courses offered by the government

and are thus ignorant of the effects of such a disease.

Such challenges can be tackled by imparting educational courses to the patients at large and

motivating them to attend such courses along with proper implementation of the data analysis

measures and providing professional trained counsellors to the patients in need. Such counselling

sessions are helpful in coping with the depression and anxiety among the patients.

Part – C

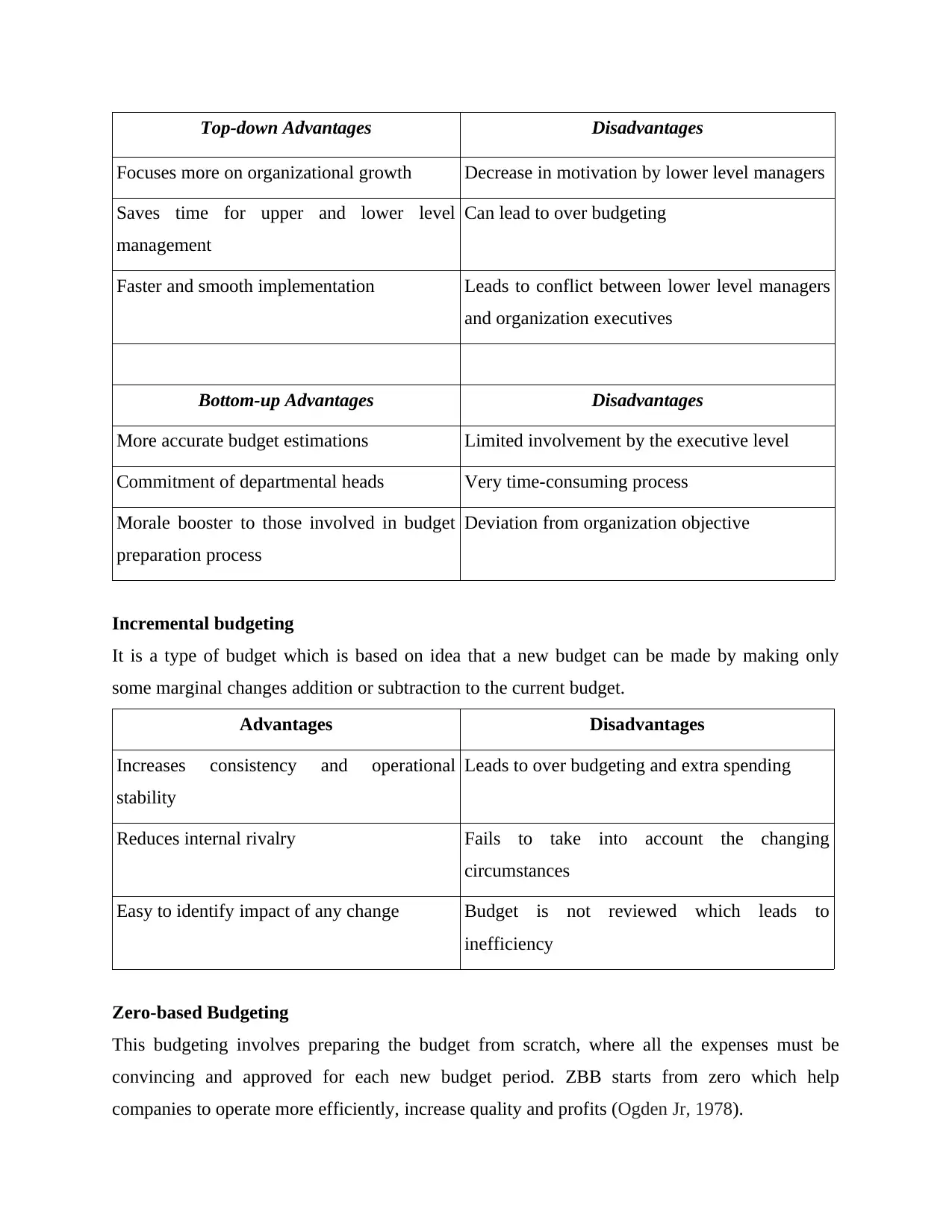

Top-down & Bottom-up Approach

Top-down approach refers to a budgeting method where high level budget for the company is

being prepared by senior management and it is passed on to departmental managers for

implementing. Whereas Bottom-up approach refers to budgets made by all the departmental

heads and submitted for review to senior management (Moore, 1980). It is also known as

participative budgeting because departmental managers are responsible for creating budget for

the company.

on which no costs have to be incurred and is earned from the earnings and profits of the same

through its operations.

National Health Services (NHS) is prominently funded through taxation in general from the

public to the government of various types of taxes and another prominent source of funding is

contributions from the national insurance. Such national insurance contributions are made by the

employers as well as employees out of their remunerations to the government and then utilized

by the government in the funding of NHS.

Current challenges in diabetes care in the UK:

Assessment of various measures and provision established in the UK for care of diabetes

shows no significant measurable key performance indicators (KPIs). There are signification

variations in the data collected and relevance of such data across the UK.

There are significant variations in the care methods devised across the UK which are due to

clinical, local, financial, regional or even demographic factors.

Education among the patients who are diagnosed currently and the ones who are ill for a long

time is seen as an obstacle. These people do not attend the courses offered by the government

and are thus ignorant of the effects of such a disease.

Such challenges can be tackled by imparting educational courses to the patients at large and

motivating them to attend such courses along with proper implementation of the data analysis

measures and providing professional trained counsellors to the patients in need. Such counselling

sessions are helpful in coping with the depression and anxiety among the patients.

Part – C

Top-down & Bottom-up Approach

Top-down approach refers to a budgeting method where high level budget for the company is

being prepared by senior management and it is passed on to departmental managers for

implementing. Whereas Bottom-up approach refers to budgets made by all the departmental

heads and submitted for review to senior management (Moore, 1980). It is also known as

participative budgeting because departmental managers are responsible for creating budget for

the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Top-down Advantages Disadvantages

Focuses more on organizational growth Decrease in motivation by lower level managers

Saves time for upper and lower level

management

Can lead to over budgeting

Faster and smooth implementation Leads to conflict between lower level managers

and organization executives

Bottom-up Advantages Disadvantages

More accurate budget estimations Limited involvement by the executive level

Commitment of departmental heads Very time-consuming process

Morale booster to those involved in budget

preparation process

Deviation from organization objective

Incremental budgeting

It is a type of budget which is based on idea that a new budget can be made by making only

some marginal changes addition or subtraction to the current budget.

Advantages Disadvantages

Increases consistency and operational

stability

Leads to over budgeting and extra spending

Reduces internal rivalry Fails to take into account the changing

circumstances

Easy to identify impact of any change Budget is not reviewed which leads to

inefficiency

Zero-based Budgeting

This budgeting involves preparing the budget from scratch, where all the expenses must be

convincing and approved for each new budget period. ZBB starts from zero which help

companies to operate more efficiently, increase quality and profits (Ogden Jr, 1978).

Focuses more on organizational growth Decrease in motivation by lower level managers

Saves time for upper and lower level

management

Can lead to over budgeting

Faster and smooth implementation Leads to conflict between lower level managers

and organization executives

Bottom-up Advantages Disadvantages

More accurate budget estimations Limited involvement by the executive level

Commitment of departmental heads Very time-consuming process

Morale booster to those involved in budget

preparation process

Deviation from organization objective

Incremental budgeting

It is a type of budget which is based on idea that a new budget can be made by making only

some marginal changes addition or subtraction to the current budget.

Advantages Disadvantages

Increases consistency and operational

stability

Leads to over budgeting and extra spending

Reduces internal rivalry Fails to take into account the changing

circumstances

Easy to identify impact of any change Budget is not reviewed which leads to

inefficiency

Zero-based Budgeting

This budgeting involves preparing the budget from scratch, where all the expenses must be

convincing and approved for each new budget period. ZBB starts from zero which help

companies to operate more efficiently, increase quality and profits (Ogden Jr, 1978).

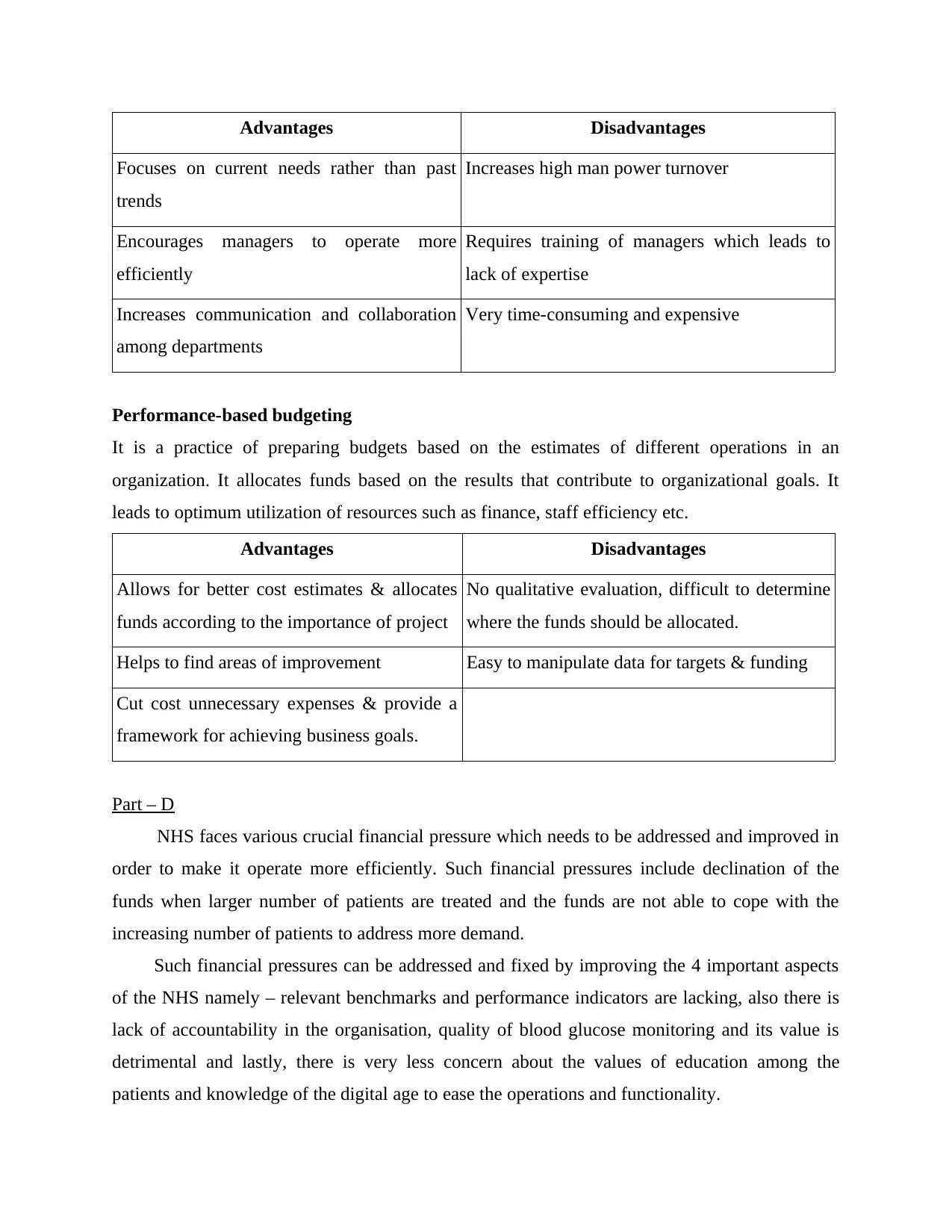

Advantages Disadvantages

Focuses on current needs rather than past

trends

Increases high man power turnover

Encourages managers to operate more

efficiently

Requires training of managers which leads to

lack of expertise

Increases communication and collaboration

among departments

Very time-consuming and expensive

Performance-based budgeting

It is a practice of preparing budgets based on the estimates of different operations in an

organization. It allocates funds based on the results that contribute to organizational goals. It

leads to optimum utilization of resources such as finance, staff efficiency etc.

Advantages Disadvantages

Allows for better cost estimates & allocates

funds according to the importance of project

No qualitative evaluation, difficult to determine

where the funds should be allocated.

Helps to find areas of improvement Easy to manipulate data for targets & funding

Cut cost unnecessary expenses & provide a

framework for achieving business goals.

Part – D

NHS faces various crucial financial pressure which needs to be addressed and improved in

order to make it operate more efficiently. Such financial pressures include declination of the

funds when larger number of patients are treated and the funds are not able to cope with the

increasing number of patients to address more demand.

Such financial pressures can be addressed and fixed by improving the 4 important aspects

of the NHS namely – relevant benchmarks and performance indicators are lacking, also there is

lack of accountability in the organisation, quality of blood glucose monitoring and its value is

detrimental and lastly, there is very less concern about the values of education among the

patients and knowledge of the digital age to ease the operations and functionality.

Focuses on current needs rather than past

trends

Increases high man power turnover

Encourages managers to operate more

efficiently

Requires training of managers which leads to

lack of expertise

Increases communication and collaboration

among departments

Very time-consuming and expensive

Performance-based budgeting

It is a practice of preparing budgets based on the estimates of different operations in an

organization. It allocates funds based on the results that contribute to organizational goals. It

leads to optimum utilization of resources such as finance, staff efficiency etc.

Advantages Disadvantages

Allows for better cost estimates & allocates

funds according to the importance of project

No qualitative evaluation, difficult to determine

where the funds should be allocated.

Helps to find areas of improvement Easy to manipulate data for targets & funding

Cut cost unnecessary expenses & provide a

framework for achieving business goals.

Part – D

NHS faces various crucial financial pressure which needs to be addressed and improved in

order to make it operate more efficiently. Such financial pressures include declination of the

funds when larger number of patients are treated and the funds are not able to cope with the

increasing number of patients to address more demand.

Such financial pressures can be addressed and fixed by improving the 4 important aspects

of the NHS namely – relevant benchmarks and performance indicators are lacking, also there is

lack of accountability in the organisation, quality of blood glucose monitoring and its value is

detrimental and lastly, there is very less concern about the values of education among the

patients and knowledge of the digital age to ease the operations and functionality.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.