Auditing Assignment: Dick Smith's Going Concern and Audit Opinion

VerifiedAdded on 2021/10/27

|6

|1532

|24

Report

AI Summary

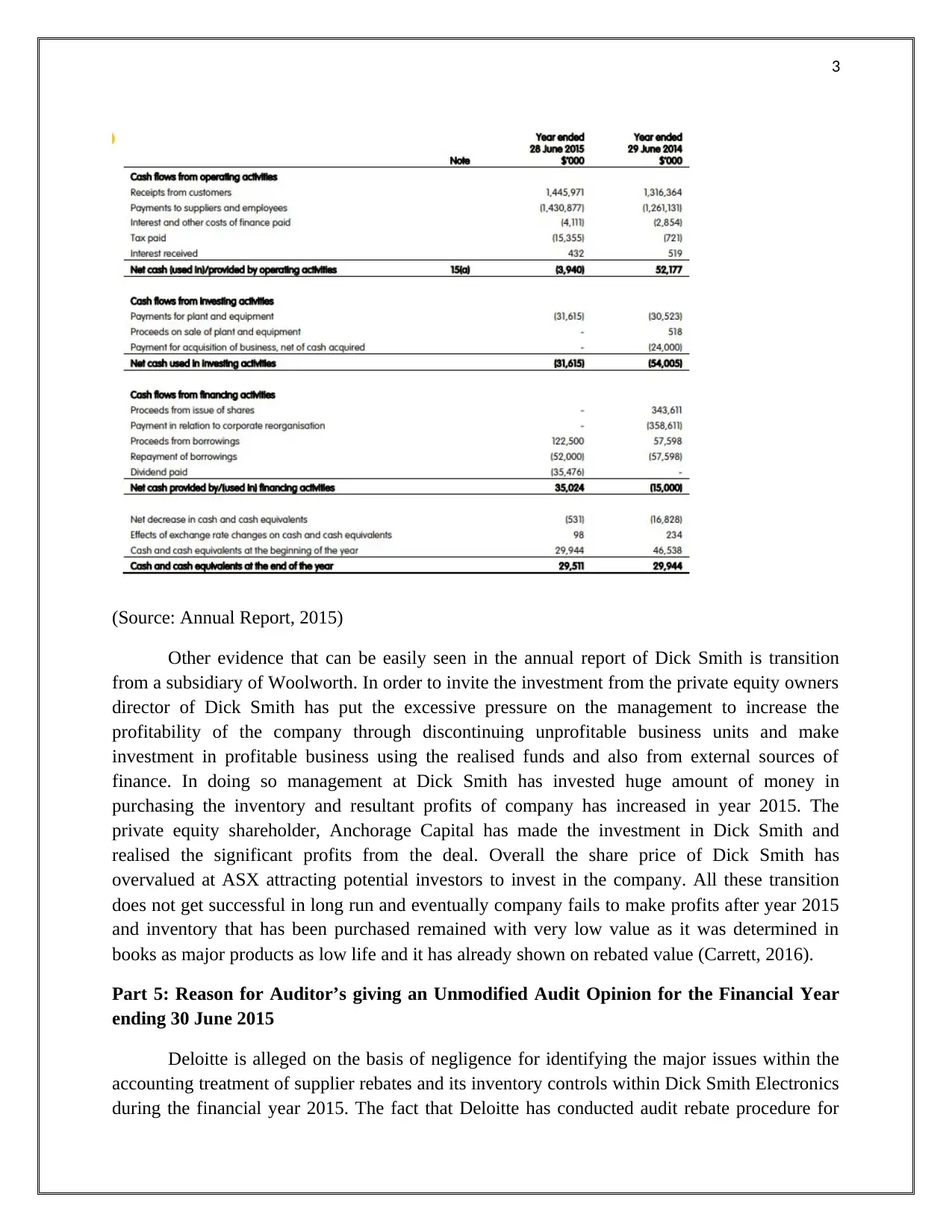

This report provides an analysis of the Dick Smith case, focusing on the company's going concern issues and the audit opinion provided by Deloitte. The report examines evidence from the annual report indicating violations of the going concern principle, such as excessive payments to suppliers, declining cash flow despite increased revenue, and inflated inventory values. It highlights the role of 'Real Activities Management' by senior management in manipulating sales and inventory figures, leading to a shortage of working capital and eventual liquidation. The report also discusses the transition from a Woolworth subsidiary, the pressure to increase profitability, and the overvaluation of shares. Furthermore, it explores the reasons behind Deloitte's unmodified audit opinion, including the difficulty in identifying real management activities and potential concerns about questioning the company for accounting fraud. The report also delves into Deloitte's legal liability as an auditor, emphasizing the importance of due care, relevant skills, and ethical conduct in providing opinions on financial statements. The conclusion suggests that Deloitte may not have fulfilled its legal liabilities, leading to an unmodified audit opinion despite material misstatements.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.