Financial Analysis and Valuation Report: Dietswell SA's IPO Decision

VerifiedAdded on 2020/10/22

|13

|3049

|235

Report

AI Summary

This report provides a comprehensive financial analysis of Dietswell SA, a French service provider in the oil and gas industry, focusing on its four business units: Dietswell Services, Dietswell Solutions, Facto-rig, and Dietswell Contracting. The analysis includes a detailed examination of financial ratios, such as turnover, cost of sales, contribution, gross margin, EBITDA, EBIT, and net results, for the period from 2009 to 2011. The report evaluates the company's performance, considering the impact of the global economic downturn and internal restructuring efforts. It rationalizes financial decisions based on findings, emphasizing the need for the company to utilize external funding sources to improve its debt-equity ratio. Furthermore, the report applies the Discounted Cash Flow (DCF) approach to value Dietswell SA, forecasting revenues, capital expenditures, and EBIT, and compares the results to market values. The conclusion highlights the importance of factors such as depreciation and amortization in management decision-making, recommending strategies for future growth and financial stability. The analysis also compares the results with market values during the previous trading year. The report includes tables of financial data, including unlevered free cash flow, enterprise value, and market capitalization to support its conclusions and recommendations.

FINANCIAL

DECISION

MAKING

DECISION

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report summarises that Dietswell SA has to select IPO for future perspective. It has

been analysed that company have much more equity compare to debt so they need to debt for

future business activities. There is recommanded that they has to used external sources less than

to internal sources. The company has analysis financial ratio regarding to four business units and

find that business run on credit sales and purchase. For reduction of liabilities need to use

external sources which are come by debt. The company has apply discount cash flow

methodology to compare actual and expected amounts of every year.

This report summarises that Dietswell SA has to select IPO for future perspective. It has

been analysed that company have much more equity compare to debt so they need to debt for

future business activities. There is recommanded that they has to used external sources less than

to internal sources. The company has analysis financial ratio regarding to four business units and

find that business run on credit sales and purchase. For reduction of liabilities need to use

external sources which are come by debt. The company has apply discount cash flow

methodology to compare actual and expected amounts of every year.

Table of Contents

EXECUTIVE SUMMARY ............................................................................................................2

INTRODUCTION...........................................................................................................................2

MAIN BODY...................................................................................................................................2

Financial ratio analysis of Dietswell SA referring to four business units..............................2

Company's Performance.........................................................................................................3

Rationalise of decision based on findings..............................................................................4

Valuation of Dietswell SA using an appropriate DCF approach and the forecasting

assumptions ...........................................................................................................................4

Compare result to market values during the previous trading year .......................................6

Factors are using to valuation bases for the management decision making...........................6

RECOMMENDATION...................................................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIX......................................................................................................................................9

1

EXECUTIVE SUMMARY ............................................................................................................2

INTRODUCTION...........................................................................................................................2

MAIN BODY...................................................................................................................................2

Financial ratio analysis of Dietswell SA referring to four business units..............................2

Company's Performance.........................................................................................................3

Rationalise of decision based on findings..............................................................................4

Valuation of Dietswell SA using an appropriate DCF approach and the forecasting

assumptions ...........................................................................................................................4

Compare result to market values during the previous trading year .......................................6

Factors are using to valuation bases for the management decision making...........................6

RECOMMENDATION...................................................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIX......................................................................................................................................9

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial decision making is a process which made by the financial manager relating to

the financing mix of an organization (Financial decision making. 2019). The aim of this report

is to conduct an analysis of the industry for future growth of Dietswell SA and valuation of

company regarding management decision making. Financial ratio provides accurate performance

of company regarding to decision making.. Dietswell SA is a French service provider in the oil

and gas industry. They have four business units such as Dietswell Services, Dietswell Solutions,

Facto-rig and Dietswell Contracting. The report focused on analysis of financial ratios of the

company and calculate value with the help of appropriate methodology of DCF approach and the

forecasting assumptions.

MAIN BODY

Financial ratio analysis of Dietswell SA referring to four business units

For analysing of financial ratio of Dietswell SA referring to the four business units, they

are as follows -

Dietswell Services

It has been analysed that in 2011, Dietswell services accounted for 78% of Dietswell SA

revenues. There was considering a core competency for company, generating high levels revenue

with low capital requirements. From 2012, restructuring accelerated at dietswell services with

several developments. In 2009, turn over of Dietswell services unit was EUR 8072485, growth

of the unit -28% and cost of sales is £7156960 so contribution was £915525. There is gross

margin was £679793 and EBITDA £1174307, £836682 and £45942 from 2009 to 2011 (Arnold

and et. Al, 2012). From EBITDA deduct amount of amortization and depreciation and as a result

get earning before interest and tax like as £2021171, £1961165 and £1038180. From the result of

EBITDA deduct amount of financial and exceptional result and acquire amount of net result

before tax on profit like as £1237490, £5034489 and £1271115. from the mention amount of

EBT less amount of tax and get net result of three years like in 2009 – £1237490, in 2010 –

£5034489 and in 2011 – £1271293.

Dietswell Solutions

It is observed that turn over of Dietswell solutions from 2009 to 2011 is £1196151,

£1598101 and £577105. It shows growth of the company such as 237%, 34% and -64%

2

Financial decision making is a process which made by the financial manager relating to

the financing mix of an organization (Financial decision making. 2019). The aim of this report

is to conduct an analysis of the industry for future growth of Dietswell SA and valuation of

company regarding management decision making. Financial ratio provides accurate performance

of company regarding to decision making.. Dietswell SA is a French service provider in the oil

and gas industry. They have four business units such as Dietswell Services, Dietswell Solutions,

Facto-rig and Dietswell Contracting. The report focused on analysis of financial ratios of the

company and calculate value with the help of appropriate methodology of DCF approach and the

forecasting assumptions.

MAIN BODY

Financial ratio analysis of Dietswell SA referring to four business units

For analysing of financial ratio of Dietswell SA referring to the four business units, they

are as follows -

Dietswell Services

It has been analysed that in 2011, Dietswell services accounted for 78% of Dietswell SA

revenues. There was considering a core competency for company, generating high levels revenue

with low capital requirements. From 2012, restructuring accelerated at dietswell services with

several developments. In 2009, turn over of Dietswell services unit was EUR 8072485, growth

of the unit -28% and cost of sales is £7156960 so contribution was £915525. There is gross

margin was £679793 and EBITDA £1174307, £836682 and £45942 from 2009 to 2011 (Arnold

and et. Al, 2012). From EBITDA deduct amount of amortization and depreciation and as a result

get earning before interest and tax like as £2021171, £1961165 and £1038180. From the result of

EBITDA deduct amount of financial and exceptional result and acquire amount of net result

before tax on profit like as £1237490, £5034489 and £1271115. from the mention amount of

EBT less amount of tax and get net result of three years like in 2009 – £1237490, in 2010 –

£5034489 and in 2011 – £1271293.

Dietswell Solutions

It is observed that turn over of Dietswell solutions from 2009 to 2011 is £1196151,

£1598101 and £577105. It shows growth of the company such as 237%, 34% and -64%

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

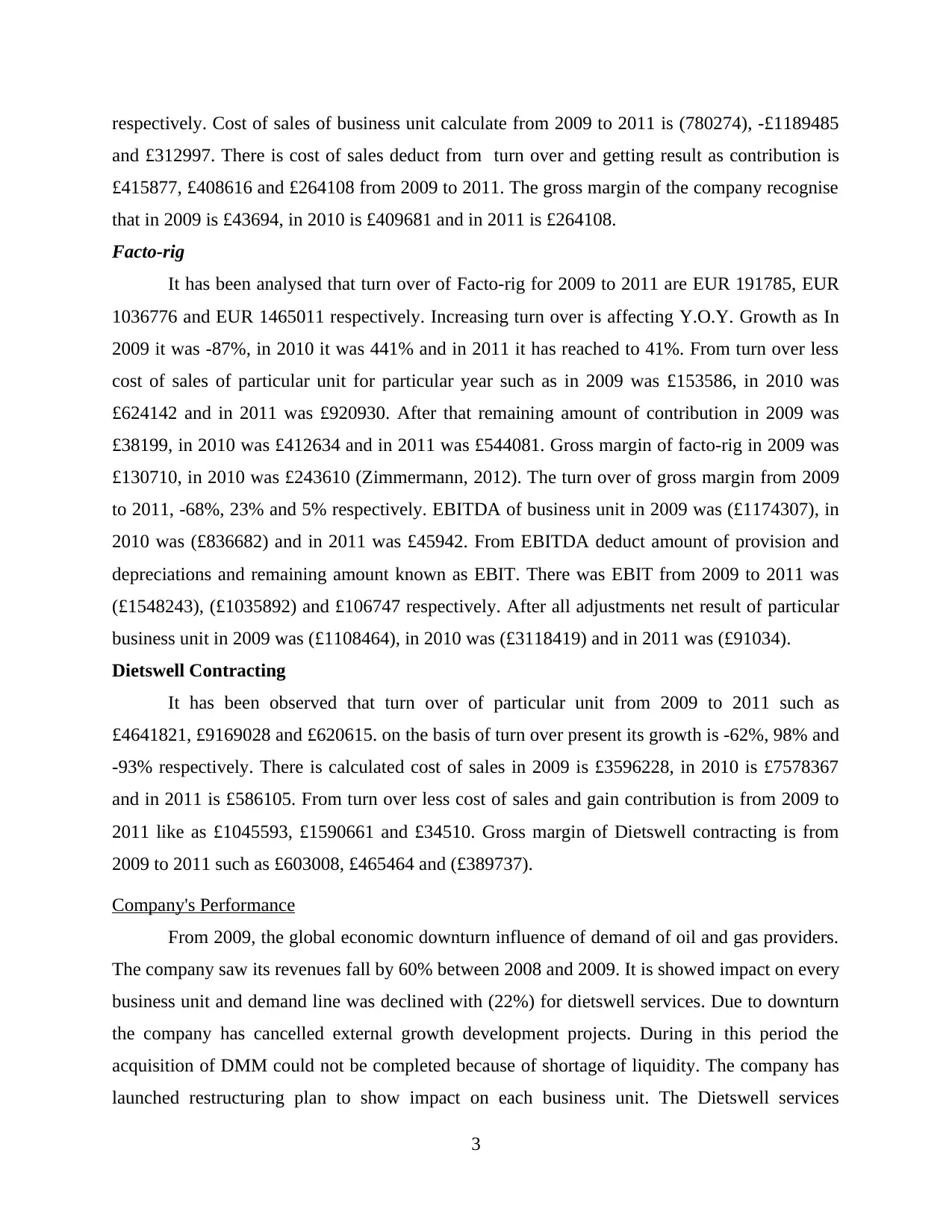

respectively. Cost of sales of business unit calculate from 2009 to 2011 is (780274), -£1189485

and £312997. There is cost of sales deduct from turn over and getting result as contribution is

£415877, £408616 and £264108 from 2009 to 2011. The gross margin of the company recognise

that in 2009 is £43694, in 2010 is £409681 and in 2011 is £264108.

Facto-rig

It has been analysed that turn over of Facto-rig for 2009 to 2011 are EUR 191785, EUR

1036776 and EUR 1465011 respectively. Increasing turn over is affecting Y.O.Y. Growth as In

2009 it was -87%, in 2010 it was 441% and in 2011 it has reached to 41%. From turn over less

cost of sales of particular unit for particular year such as in 2009 was £153586, in 2010 was

£624142 and in 2011 was £920930. After that remaining amount of contribution in 2009 was

£38199, in 2010 was £412634 and in 2011 was £544081. Gross margin of facto-rig in 2009 was

£130710, in 2010 was £243610 (Zimmermann, 2012). The turn over of gross margin from 2009

to 2011, -68%, 23% and 5% respectively. EBITDA of business unit in 2009 was (£1174307), in

2010 was (£836682) and in 2011 was £45942. From EBITDA deduct amount of provision and

depreciations and remaining amount known as EBIT. There was EBIT from 2009 to 2011 was

(£1548243), (£1035892) and £106747 respectively. After all adjustments net result of particular

business unit in 2009 was (£1108464), in 2010 was (£3118419) and in 2011 was (£91034).

Dietswell Contracting

It has been observed that turn over of particular unit from 2009 to 2011 such as

£4641821, £9169028 and £620615. on the basis of turn over present its growth is -62%, 98% and

-93% respectively. There is calculated cost of sales in 2009 is £3596228, in 2010 is £7578367

and in 2011 is £586105. From turn over less cost of sales and gain contribution is from 2009 to

2011 like as £1045593, £1590661 and £34510. Gross margin of Dietswell contracting is from

2009 to 2011 such as £603008, £465464 and (£389737).

Company's Performance

From 2009, the global economic downturn influence of demand of oil and gas providers.

The company saw its revenues fall by 60% between 2008 and 2009. It is showed impact on every

business unit and demand line was declined with (22%) for dietswell services. Due to downturn

the company has cancelled external growth development projects. During in this period the

acquisition of DMM could not be completed because of shortage of liquidity. The company has

launched restructuring plan to show impact on each business unit. The Dietswell services

3

and £312997. There is cost of sales deduct from turn over and getting result as contribution is

£415877, £408616 and £264108 from 2009 to 2011. The gross margin of the company recognise

that in 2009 is £43694, in 2010 is £409681 and in 2011 is £264108.

Facto-rig

It has been analysed that turn over of Facto-rig for 2009 to 2011 are EUR 191785, EUR

1036776 and EUR 1465011 respectively. Increasing turn over is affecting Y.O.Y. Growth as In

2009 it was -87%, in 2010 it was 441% and in 2011 it has reached to 41%. From turn over less

cost of sales of particular unit for particular year such as in 2009 was £153586, in 2010 was

£624142 and in 2011 was £920930. After that remaining amount of contribution in 2009 was

£38199, in 2010 was £412634 and in 2011 was £544081. Gross margin of facto-rig in 2009 was

£130710, in 2010 was £243610 (Zimmermann, 2012). The turn over of gross margin from 2009

to 2011, -68%, 23% and 5% respectively. EBITDA of business unit in 2009 was (£1174307), in

2010 was (£836682) and in 2011 was £45942. From EBITDA deduct amount of provision and

depreciations and remaining amount known as EBIT. There was EBIT from 2009 to 2011 was

(£1548243), (£1035892) and £106747 respectively. After all adjustments net result of particular

business unit in 2009 was (£1108464), in 2010 was (£3118419) and in 2011 was (£91034).

Dietswell Contracting

It has been observed that turn over of particular unit from 2009 to 2011 such as

£4641821, £9169028 and £620615. on the basis of turn over present its growth is -62%, 98% and

-93% respectively. There is calculated cost of sales in 2009 is £3596228, in 2010 is £7578367

and in 2011 is £586105. From turn over less cost of sales and gain contribution is from 2009 to

2011 like as £1045593, £1590661 and £34510. Gross margin of Dietswell contracting is from

2009 to 2011 such as £603008, £465464 and (£389737).

Company's Performance

From 2009, the global economic downturn influence of demand of oil and gas providers.

The company saw its revenues fall by 60% between 2008 and 2009. It is showed impact on every

business unit and demand line was declined with (22%) for dietswell services. Due to downturn

the company has cancelled external growth development projects. During in this period the

acquisition of DMM could not be completed because of shortage of liquidity. The company has

launched restructuring plan to show impact on each business unit. The Dietswell services

3

consolidate of the strategic position with current key clients. They are taking priority on high

margin services like as turnkey project management. Dietswell solution in 2007, appeal of the

higher margin offshore businesses. The management of the factorig was approached by a swiss

company with a EUR 350000 cash offer for 50% of the business. This transaction related to joint

venture and owned by dietswell and SGS equally. In the mid of 2012, both platforms of business

units like dietswell service and factorig could be operated at a day rate of USD 350000 with a

contribution margin of 35%.

Rationalise of decision based on findings

It has been find that company is using its internal funds more than external funds. It is

find to the company that should use external funds to survive in the market. The Ideal debt equity

ratio is 2:1 which depicts that business entities should use external funds more than internal. The

Dietswell SA's debt equity ratio is not according to ideal (Lichtenberg, Ficker and Rahman-

Filipiak, 2016). So when company analysed Cost of debt so recognised that total debt of an

organisation in 2012 is £3782209 and interest rate is 5.60%. The Dietswell SA has to decreased

of accounts receivable due to maintain balance of cash. When company sale out of products in

cash so cash balance increases and performance of the company shows in effective way. If

company have liquidity so they are purchase products in cash not to in credit. The effect shows

in positive manner because liability of company is decreasing.

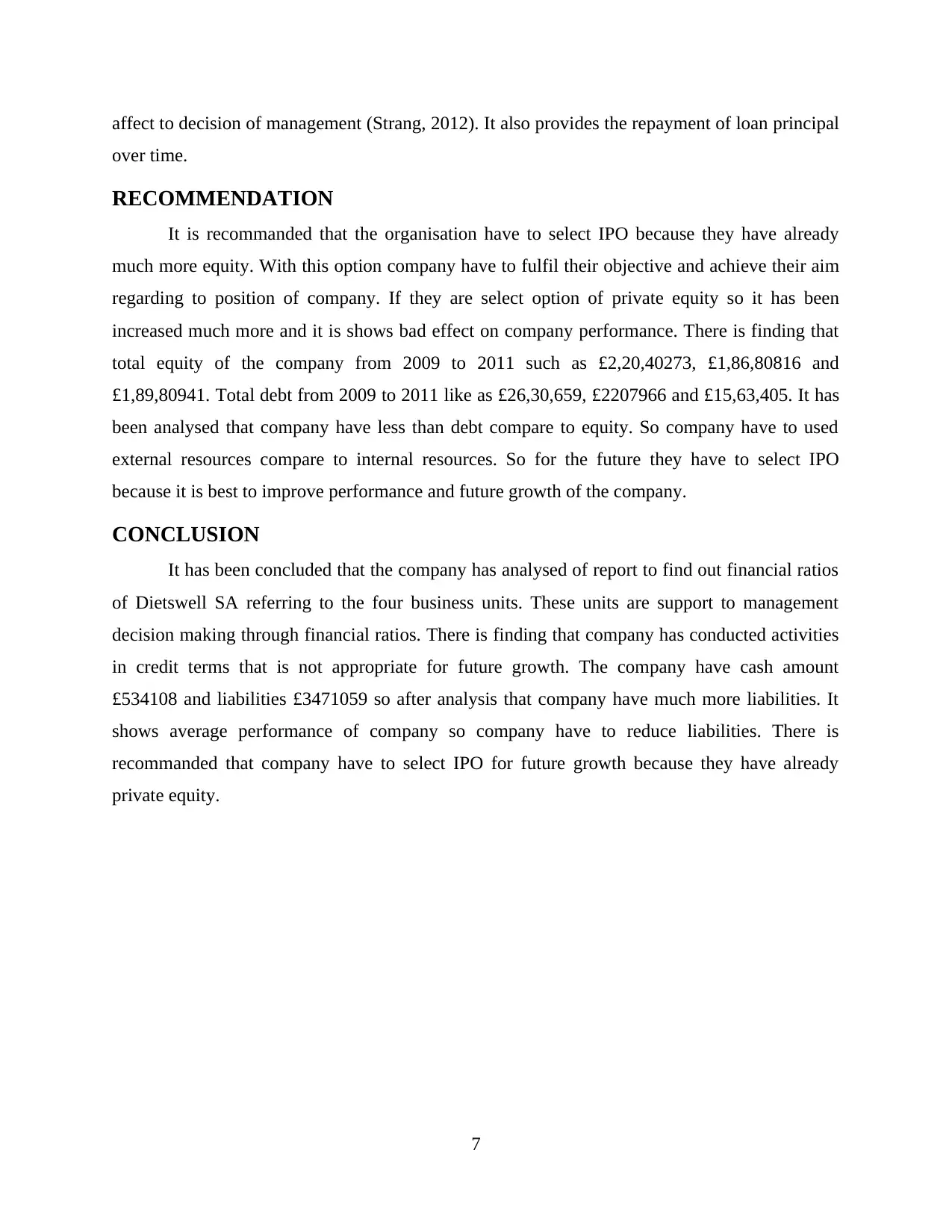

Valuation of Dietswell SA using an appropriate DCF approach and the forecasting assumptions

The management of the organisation has to forecast for the years 2012 to 2015. It is

based on forecasting assumption and figures of financial information were more difficult. There

is set goals and financial figures based on past years, they are as follows -

The management has analysed revenue will growth with 8.7% from 2015 until 2018 after

which the growth was expected to settle in mature business (Duclos, 2015).

The capital expenditure will be drastically reduced from year 2012 and it should remain

constant at 4% of revenue.

In 2016 EBIT should improve with 8% of revenues.

There is expected about net working capital will increase yearly and has to stabilize at

2% of revenue from 2016.

Discounted cash flow 2011 2012 2013 2014 2015

4

margin services like as turnkey project management. Dietswell solution in 2007, appeal of the

higher margin offshore businesses. The management of the factorig was approached by a swiss

company with a EUR 350000 cash offer for 50% of the business. This transaction related to joint

venture and owned by dietswell and SGS equally. In the mid of 2012, both platforms of business

units like dietswell service and factorig could be operated at a day rate of USD 350000 with a

contribution margin of 35%.

Rationalise of decision based on findings

It has been find that company is using its internal funds more than external funds. It is

find to the company that should use external funds to survive in the market. The Ideal debt equity

ratio is 2:1 which depicts that business entities should use external funds more than internal. The

Dietswell SA's debt equity ratio is not according to ideal (Lichtenberg, Ficker and Rahman-

Filipiak, 2016). So when company analysed Cost of debt so recognised that total debt of an

organisation in 2012 is £3782209 and interest rate is 5.60%. The Dietswell SA has to decreased

of accounts receivable due to maintain balance of cash. When company sale out of products in

cash so cash balance increases and performance of the company shows in effective way. If

company have liquidity so they are purchase products in cash not to in credit. The effect shows

in positive manner because liability of company is decreasing.

Valuation of Dietswell SA using an appropriate DCF approach and the forecasting assumptions

The management of the organisation has to forecast for the years 2012 to 2015. It is

based on forecasting assumption and figures of financial information were more difficult. There

is set goals and financial figures based on past years, they are as follows -

The management has analysed revenue will growth with 8.7% from 2015 until 2018 after

which the growth was expected to settle in mature business (Duclos, 2015).

The capital expenditure will be drastically reduced from year 2012 and it should remain

constant at 4% of revenue.

In 2016 EBIT should improve with 8% of revenues.

There is expected about net working capital will increase yearly and has to stabilize at

2% of revenue from 2016.

Discounted cash flow 2011 2012 2013 2014 2015

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

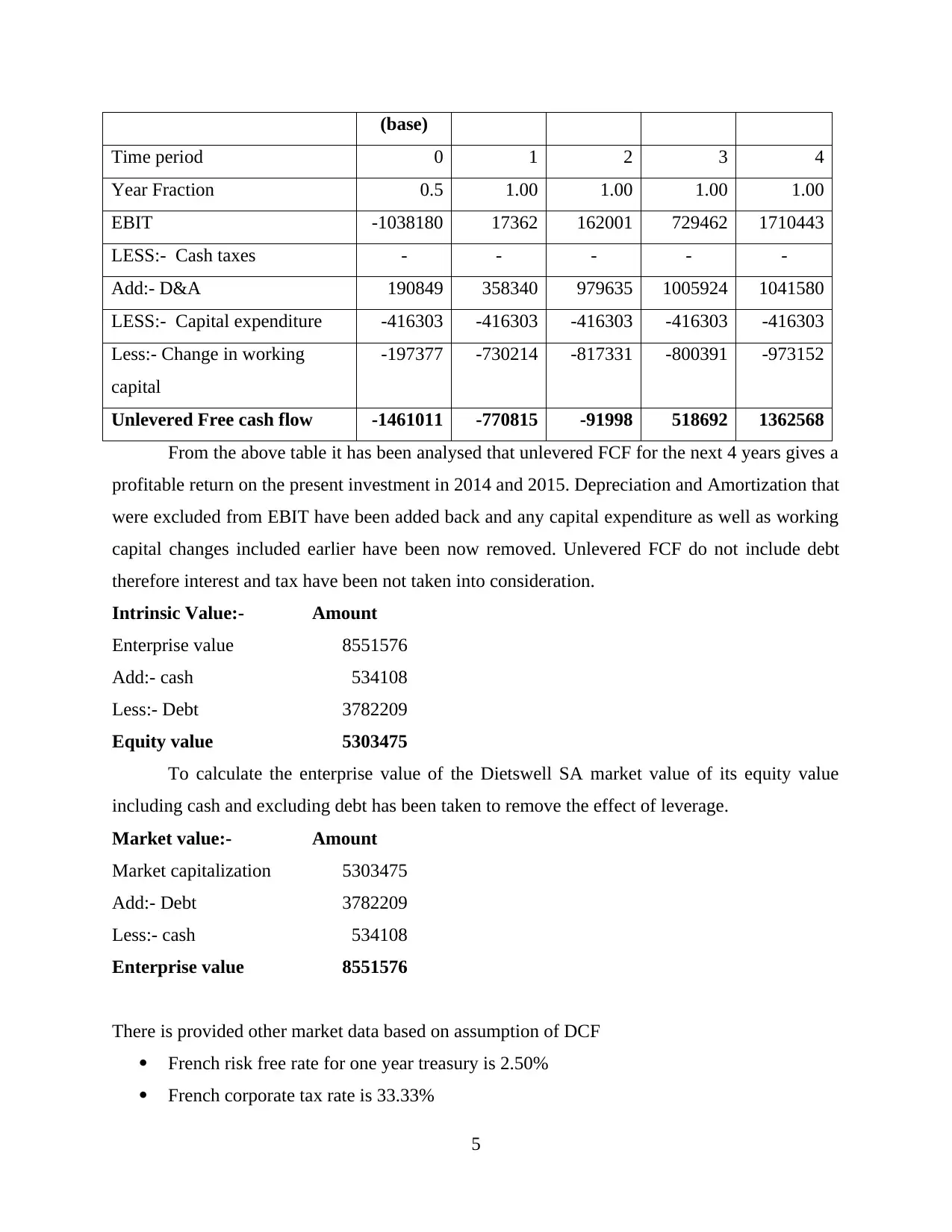

(base)

Time period 0 1 2 3 4

Year Fraction 0.5 1.00 1.00 1.00 1.00

EBIT -1038180 17362 162001 729462 1710443

LESS:- Cash taxes - - - - -

Add:- D&A 190849 358340 979635 1005924 1041580

LESS:- Capital expenditure -416303 -416303 -416303 -416303 -416303

Less:- Change in working

capital

-197377 -730214 -817331 -800391 -973152

Unlevered Free cash flow -1461011 -770815 -91998 518692 1362568

From the above table it has been analysed that unlevered FCF for the next 4 years gives a

profitable return on the present investment in 2014 and 2015. Depreciation and Amortization that

were excluded from EBIT have been added back and any capital expenditure as well as working

capital changes included earlier have been now removed. Unlevered FCF do not include debt

therefore interest and tax have been not taken into consideration.

Intrinsic Value:- Amount

Enterprise value 8551576

Add:- cash 534108

Less:- Debt 3782209

Equity value 5303475

To calculate the enterprise value of the Dietswell SA market value of its equity value

including cash and excluding debt has been taken to remove the effect of leverage.

Market value:- Amount

Market capitalization 5303475

Add:- Debt 3782209

Less:- cash 534108

Enterprise value 8551576

There is provided other market data based on assumption of DCF

French risk free rate for one year treasury is 2.50%

French corporate tax rate is 33.33%

5

Time period 0 1 2 3 4

Year Fraction 0.5 1.00 1.00 1.00 1.00

EBIT -1038180 17362 162001 729462 1710443

LESS:- Cash taxes - - - - -

Add:- D&A 190849 358340 979635 1005924 1041580

LESS:- Capital expenditure -416303 -416303 -416303 -416303 -416303

Less:- Change in working

capital

-197377 -730214 -817331 -800391 -973152

Unlevered Free cash flow -1461011 -770815 -91998 518692 1362568

From the above table it has been analysed that unlevered FCF for the next 4 years gives a

profitable return on the present investment in 2014 and 2015. Depreciation and Amortization that

were excluded from EBIT have been added back and any capital expenditure as well as working

capital changes included earlier have been now removed. Unlevered FCF do not include debt

therefore interest and tax have been not taken into consideration.

Intrinsic Value:- Amount

Enterprise value 8551576

Add:- cash 534108

Less:- Debt 3782209

Equity value 5303475

To calculate the enterprise value of the Dietswell SA market value of its equity value

including cash and excluding debt has been taken to remove the effect of leverage.

Market value:- Amount

Market capitalization 5303475

Add:- Debt 3782209

Less:- cash 534108

Enterprise value 8551576

There is provided other market data based on assumption of DCF

French risk free rate for one year treasury is 2.50%

French corporate tax rate is 33.33%

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

French market risk premium is 550bps

There is estimated to Debt to equity ratio of the company will 44%

It is estimated that average tax rate of industry in 2011 is 12% and reason of low rate is

lower emerging markets tax rates.

From Algerian risk free rate premium over AAA rated countries is 200bps

Corporate tax rate of Algerian is 25%

It is analysed risk premium on the basis of market and lending of Algerian is 1000 bps

and 770bps.

Compare result to market values during the previous trading year

It has been analysed that the assumptions of regarding to EBIT is increased by 4% every

year from 2009 to 2011 so there is not necessary to increases by 8% in expected year. Revenues

of the company presents as 14%, 5% and 5% but in expected year calculated is 8.7%. There is

after analyses see that expected year and actual year growth is not equal but organisation has to

change their policies so it will happen in future (Blakemore and Robbins, 2012). From the above

calculations, Un-levered Free Cash Flows (FCF) projected for years 2012 to 2015 show an

initial loss for taking this investment however, these losses are recovered in the subsequent years.

Enterprise value helps in comparing worth of companies by removing the debt-equity element

from the structure. Since equity value is less than the enterprise value, we can say that the

valuation made is in favour of Dietswell SA.

Factors are using to valuation bases for the management decision making

There are using many factors for valuation and these are affect to decision making of

management, they are as follows -

Depreciation – It is important factor that are related to management decision. It is a

method to calculate life of assets in particular years. And it provides estimate life of particular

assets for future perspective. It is calculated by two methods which are as below -

Straight line method

Written down value

The company has applied straight line method to calculate depreciation on assets.

Amortization – In this factor recognise value of assets and it is important to calculate

because it is analysed routine value of intangible assets. It is based on accounting term and

process of allocating the cost of an intangible asset for particular time period. The value of assets

6

There is estimated to Debt to equity ratio of the company will 44%

It is estimated that average tax rate of industry in 2011 is 12% and reason of low rate is

lower emerging markets tax rates.

From Algerian risk free rate premium over AAA rated countries is 200bps

Corporate tax rate of Algerian is 25%

It is analysed risk premium on the basis of market and lending of Algerian is 1000 bps

and 770bps.

Compare result to market values during the previous trading year

It has been analysed that the assumptions of regarding to EBIT is increased by 4% every

year from 2009 to 2011 so there is not necessary to increases by 8% in expected year. Revenues

of the company presents as 14%, 5% and 5% but in expected year calculated is 8.7%. There is

after analyses see that expected year and actual year growth is not equal but organisation has to

change their policies so it will happen in future (Blakemore and Robbins, 2012). From the above

calculations, Un-levered Free Cash Flows (FCF) projected for years 2012 to 2015 show an

initial loss for taking this investment however, these losses are recovered in the subsequent years.

Enterprise value helps in comparing worth of companies by removing the debt-equity element

from the structure. Since equity value is less than the enterprise value, we can say that the

valuation made is in favour of Dietswell SA.

Factors are using to valuation bases for the management decision making

There are using many factors for valuation and these are affect to decision making of

management, they are as follows -

Depreciation – It is important factor that are related to management decision. It is a

method to calculate life of assets in particular years. And it provides estimate life of particular

assets for future perspective. It is calculated by two methods which are as below -

Straight line method

Written down value

The company has applied straight line method to calculate depreciation on assets.

Amortization – In this factor recognise value of assets and it is important to calculate

because it is analysed routine value of intangible assets. It is based on accounting term and

process of allocating the cost of an intangible asset for particular time period. The value of assets

6

affect to decision of management (Strang, 2012). It also provides the repayment of loan principal

over time.

RECOMMENDATION

It is recommanded that the organisation have to select IPO because they have already

much more equity. With this option company have to fulfil their objective and achieve their aim

regarding to position of company. If they are select option of private equity so it has been

increased much more and it is shows bad effect on company performance. There is finding that

total equity of the company from 2009 to 2011 such as £2,20,40273, £1,86,80816 and

£1,89,80941. Total debt from 2009 to 2011 like as £26,30,659, £2207966 and £15,63,405. It has

been analysed that company have less than debt compare to equity. So company have to used

external resources compare to internal resources. So for the future they have to select IPO

because it is best to improve performance and future growth of the company.

CONCLUSION

It has been concluded that the company has analysed of report to find out financial ratios

of Dietswell SA referring to the four business units. These units are support to management

decision making through financial ratios. There is finding that company has conducted activities

in credit terms that is not appropriate for future growth. The company have cash amount

£534108 and liabilities £3471059 so after analysis that company have much more liabilities. It

shows average performance of company so company have to reduce liabilities. There is

recommanded that company have to select IPO for future growth because they have already

private equity.

7

over time.

RECOMMENDATION

It is recommanded that the organisation have to select IPO because they have already

much more equity. With this option company have to fulfil their objective and achieve their aim

regarding to position of company. If they are select option of private equity so it has been

increased much more and it is shows bad effect on company performance. There is finding that

total equity of the company from 2009 to 2011 such as £2,20,40273, £1,86,80816 and

£1,89,80941. Total debt from 2009 to 2011 like as £26,30,659, £2207966 and £15,63,405. It has

been analysed that company have less than debt compare to equity. So company have to used

external resources compare to internal resources. So for the future they have to select IPO

because it is best to improve performance and future growth of the company.

CONCLUSION

It has been concluded that the company has analysed of report to find out financial ratios

of Dietswell SA referring to the four business units. These units are support to management

decision making through financial ratios. There is finding that company has conducted activities

in credit terms that is not appropriate for future growth. The company have cash amount

£534108 and liabilities £3471059 so after analysis that company have much more liabilities. It

shows average performance of company so company have to reduce liabilities. There is

recommanded that company have to select IPO for future growth because they have already

private equity.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journal

Arnold, V. and et. al, 2012. The impact of tagging qualitative financial information on investor

decision making: Implications for XBRL. International Journal of Accounting

Information Systems. 13(1). pp.2-20.

Zimmermann, H. J., 2012. Fuzzy sets, decision making, and expert systems (Vol. 10). Springer

Science & Business Media.

Starcke, K. and Brand, M., 2012. Decision making under stress: a selective review. Neuroscience

& Biobehavioral Reviews. 36(4). pp.1228-1248.

Lichtenberg, P. A., Ficker, L. J. and Rahman-Filipiak, A., 2016. Financial decision-making

abilities and financial exploitation in older African Americans: Preliminary validity

evidence for the Lichtenberg Financial Decision Rating Scale (LFDRS). Journal of

elder abuse & neglect. 28(1). pp.14-33.

Duclos, R., 2015. The psychology of investment behavior:(De) biasing financial decision‐making

one graph at a time. Journal of Consumer psychology. 25(2). pp.317-325.

Blakemore, S. J. and Robbins, T. W., 2012. Decision-making in the adolescent brain. Nature

neuroscience. 15(9). p.1184.

Strang, K. D., 2012. Applied financial non-linear programming models for decision making.

International Journal of Applied Decision Sciences. 5(4). pp.370-395.

Online

Financial decision making. 2019. [online]. Available through:

<https://www.edx.org/course/financial-decision-making-usmx-umuc-af6010>

8

Books and Journal

Arnold, V. and et. al, 2012. The impact of tagging qualitative financial information on investor

decision making: Implications for XBRL. International Journal of Accounting

Information Systems. 13(1). pp.2-20.

Zimmermann, H. J., 2012. Fuzzy sets, decision making, and expert systems (Vol. 10). Springer

Science & Business Media.

Starcke, K. and Brand, M., 2012. Decision making under stress: a selective review. Neuroscience

& Biobehavioral Reviews. 36(4). pp.1228-1248.

Lichtenberg, P. A., Ficker, L. J. and Rahman-Filipiak, A., 2016. Financial decision-making

abilities and financial exploitation in older African Americans: Preliminary validity

evidence for the Lichtenberg Financial Decision Rating Scale (LFDRS). Journal of

elder abuse & neglect. 28(1). pp.14-33.

Duclos, R., 2015. The psychology of investment behavior:(De) biasing financial decision‐making

one graph at a time. Journal of Consumer psychology. 25(2). pp.317-325.

Blakemore, S. J. and Robbins, T. W., 2012. Decision-making in the adolescent brain. Nature

neuroscience. 15(9). p.1184.

Strang, K. D., 2012. Applied financial non-linear programming models for decision making.

International Journal of Applied Decision Sciences. 5(4). pp.370-395.

Online

Financial decision making. 2019. [online]. Available through:

<https://www.edx.org/course/financial-decision-making-usmx-umuc-af6010>

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

4 year plan of Dietswell SA

Revenues of four business unit

9

4 year plan of Dietswell SA

Revenues of four business unit

9

Current ratio – current assets/current liabilities

Particular 2009 2010 2011

Current Assets 7738778 4024712 5154515

Current Liabilities 3683825 1991671 3471059

Current Ratio 2.1 2.02 1.48

Quick ratio = quick assets/current liabilities

Particular 2009 2010 2011

Quick assets 7738778 4024712 5154515

Current Liabilities 3683825 1991671 3471059

Quick ratio 2.1 2.02 1.48

Net profit ratio = Net income/net sales*100

Particular 2009 2010 2011

Net income 922142 -4109026 -5795278

Net sales 2762312.8 1001852.06 1201746.2

Net profit ratio 33.38% -410.14% -482.24%

10

Particular 2009 2010 2011

Current Assets 7738778 4024712 5154515

Current Liabilities 3683825 1991671 3471059

Current Ratio 2.1 2.02 1.48

Quick ratio = quick assets/current liabilities

Particular 2009 2010 2011

Quick assets 7738778 4024712 5154515

Current Liabilities 3683825 1991671 3471059

Quick ratio 2.1 2.02 1.48

Net profit ratio = Net income/net sales*100

Particular 2009 2010 2011

Net income 922142 -4109026 -5795278

Net sales 2762312.8 1001852.06 1201746.2

Net profit ratio 33.38% -410.14% -482.24%

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.