Differential Analysis of Subassembly Production Costs: A Case Study

VerifiedAdded on 2023/03/20

|5

|1032

|72

Case Study

AI Summary

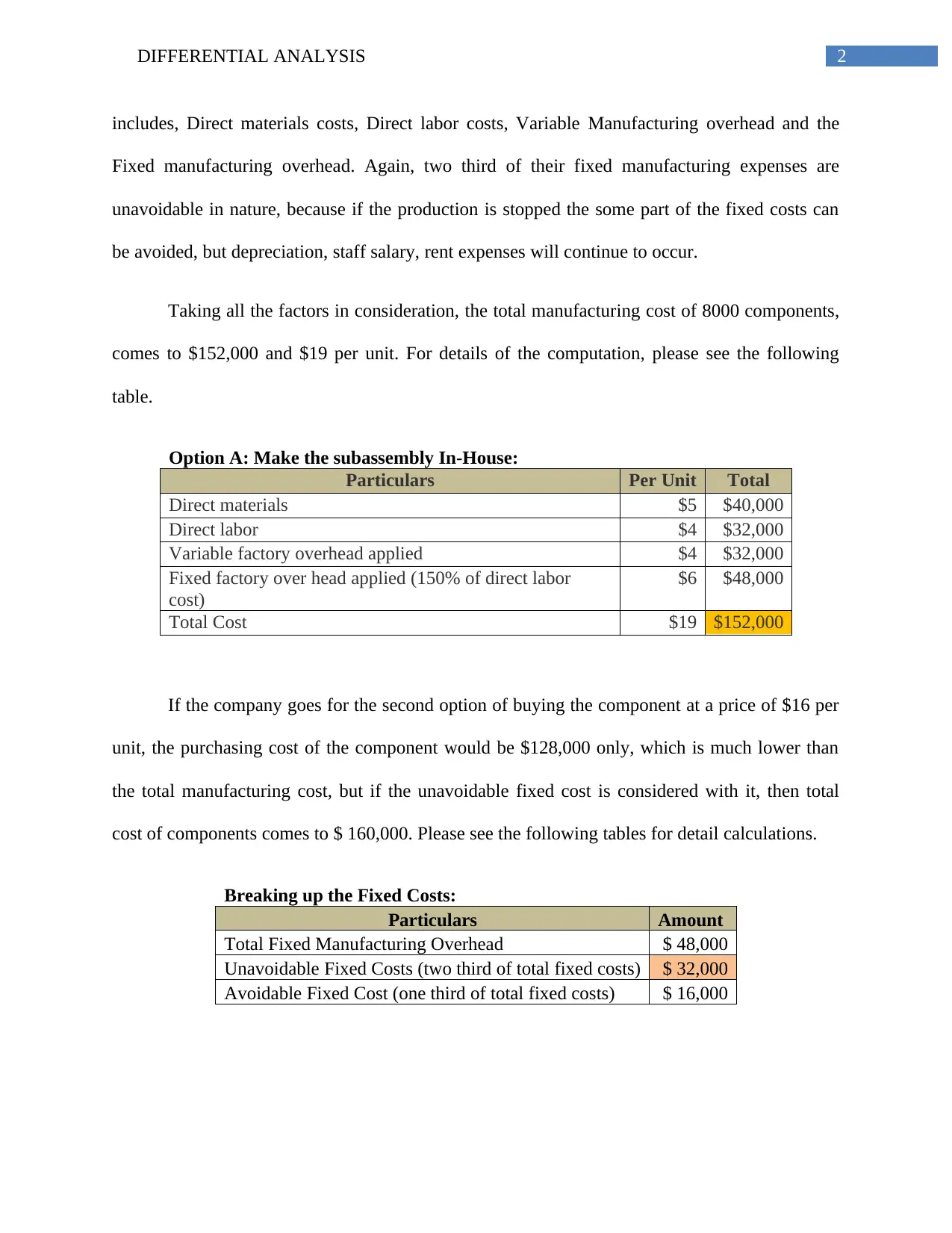

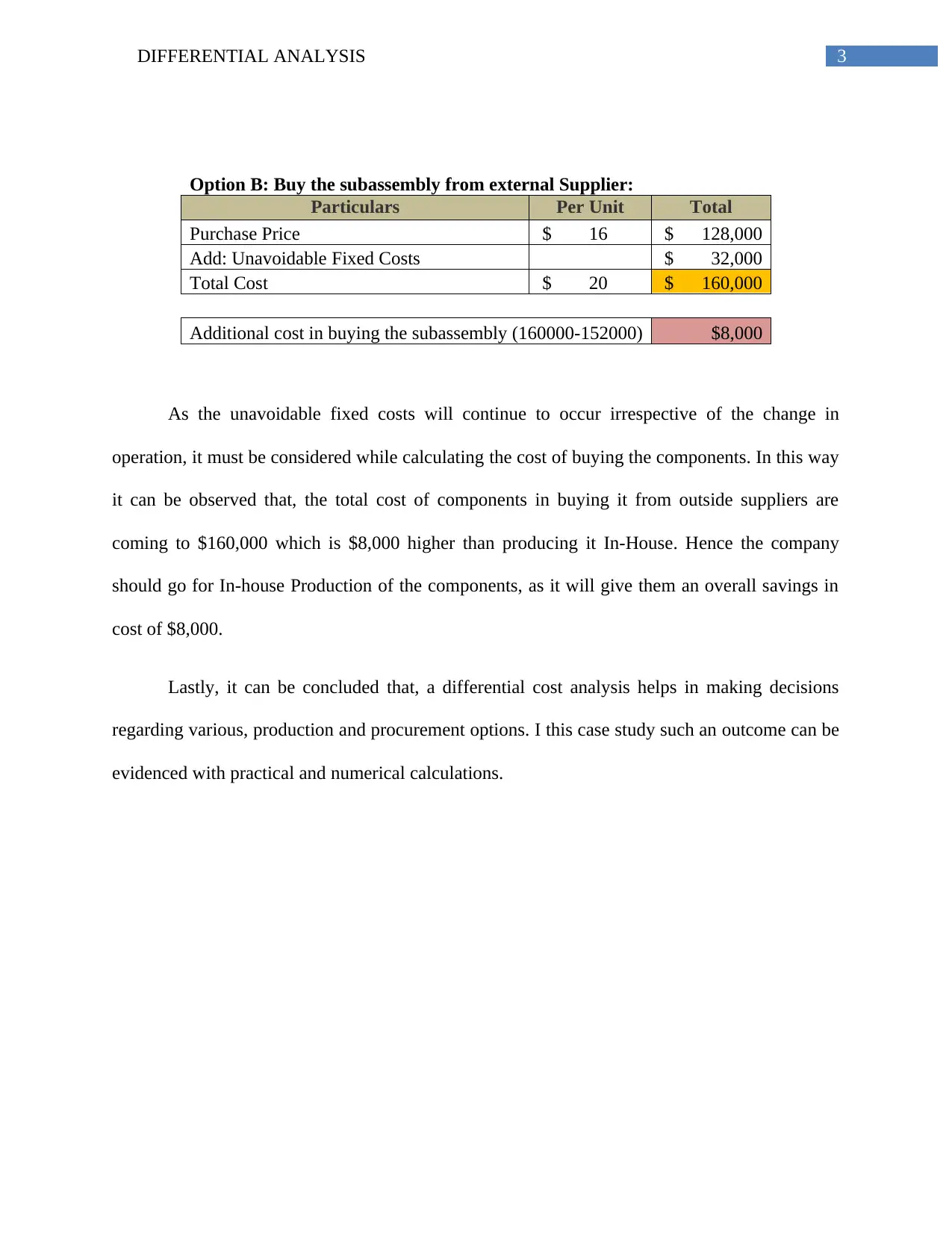

This case study analyzes a make-or-buy decision for a subassembly component, presenting a differential cost analysis. The paper outlines the cost components, including direct materials, direct labor, variable and fixed overhead, and compares the costs of in-house production versus purchasing from an external supplier. The analysis considers both avoidable and unavoidable fixed costs, calculating the total costs under each option. The study reveals that producing the subassembly in-house is more cost-effective than outsourcing, resulting in a cost savings of $8,000. The paper concludes with a recommendation for the company to continue in-house production, supported by detailed cost calculations and referencing relevant literature on management accounting and cost analysis, demonstrating the practical application of differential analysis in decision-making.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.