Report on Capital Structure and Financing of Digi Telecommunications

VerifiedAdded on 2020/07/22

|13

|3840

|52

Report

AI Summary

This report provides a comprehensive analysis of Digi Telecommunications' capital structure and financing decisions. It begins with an introduction to capital structure, defining its components and impact on profitability. The report then critically evaluates the shareholder wealth maximization (SWM) objective, discussing its assumptions and limitations, and considering stakeholder theory. It assesses various external sources of finance available to Digi, including equity share capital and long-term debt, highlighting their advantages and disadvantages. The report further examines the factors Digi Telecommunications should consider when choosing a financing type, such as cost, control dilution, and repayment terms. A solvency ratio analysis is also included to provide insights into the company's financial health. Overall, the report offers a detailed overview of Digi's financial strategies and capital structure management.

Financing/Capital Structure Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Critically evaluating the usual assumption of corporate finance literature regarding company’s

objective pertaining to the maximization of shareholders wealth...............................................3

Assessing external sources of finance available to the company................................................5

Stating aspects that business unit needs to consider while choosing the type of finance............6

Computation of WACC and practical problems regarding the same..........................................8

CONCLUSION..............................................................................................................................10

RECOMMENDATIONS...............................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

Critically evaluating the usual assumption of corporate finance literature regarding company’s

objective pertaining to the maximization of shareholders wealth...............................................3

Assessing external sources of finance available to the company................................................5

Stating aspects that business unit needs to consider while choosing the type of finance............6

Computation of WACC and practical problems regarding the same..........................................8

CONCLUSION..............................................................................................................................10

RECOMMENDATIONS...............................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Capital structure presents the manner in which business unit has financed its overall

operations. In the context of business unit, financial structure implies for the combination or

mixture of short & long term debt, common and preferred equity. Debt-equity measure is highly

prominent which in turn provides deeper insight about the riskiness of the company. Financial

structure that is followed by the company has greater impact on its profitability and overall

success. The present report is based in Digi Telecommunication, leading mobile service provider

of Malaysia. Such business unit is listed on recognized stock exchange of Malaysia such as

MYX and provides customers with products or services like cable television, telecommunication

& mobile services. In this, report will provide deeper insight about the theoretical framework

associated with corporate finance. Besides this, it also depicts external financial sources that can

be used by the company for meeting financial requirements. Further, report will also shed light

on the WACC of Digi Telecommunications.

Critically evaluating the usual assumption of corporate finance literature regarding company’s

objective pertaining to the maximization of shareholders wealth

According to the views of Ofori‐Sasu, Abor and Osei (2017) maximization of

shareholders wealth is the main objectives of business unit while carry out activities as well as

functions. On the basis of such principle and assumption the main focus of public corporation is

to enhance or maximize return on equity share capital. Hence, managers and investors make

focus narrowly on shareholders wealth maximization. Further, Sharfman (2014) presented in

their study that SWM implies that manager should take decision in the best interest of firm’s

stakeholders. Hence, stakeholders of the firm include all the individuals and groups that

substantially affect the value of it such as personnel, customers, suppliers etc. Considering the

same, on the critical note, Heminway (2017) said that firm’s value or shareholders wealth cannot

be maximized through unhappy customers, employees and poor products. Hence, according to

stakeholders theory for SWM company needs to meet the interest of all the concerned

authorities.

Takacs Haynes, Campbell and Hitt (2017) stated in their study that objective or principle

regarding SWM is based on specific assumptions. In accordance with such objective company

Capital structure presents the manner in which business unit has financed its overall

operations. In the context of business unit, financial structure implies for the combination or

mixture of short & long term debt, common and preferred equity. Debt-equity measure is highly

prominent which in turn provides deeper insight about the riskiness of the company. Financial

structure that is followed by the company has greater impact on its profitability and overall

success. The present report is based in Digi Telecommunication, leading mobile service provider

of Malaysia. Such business unit is listed on recognized stock exchange of Malaysia such as

MYX and provides customers with products or services like cable television, telecommunication

& mobile services. In this, report will provide deeper insight about the theoretical framework

associated with corporate finance. Besides this, it also depicts external financial sources that can

be used by the company for meeting financial requirements. Further, report will also shed light

on the WACC of Digi Telecommunications.

Critically evaluating the usual assumption of corporate finance literature regarding company’s

objective pertaining to the maximization of shareholders wealth

According to the views of Ofori‐Sasu, Abor and Osei (2017) maximization of

shareholders wealth is the main objectives of business unit while carry out activities as well as

functions. On the basis of such principle and assumption the main focus of public corporation is

to enhance or maximize return on equity share capital. Hence, managers and investors make

focus narrowly on shareholders wealth maximization. Further, Sharfman (2014) presented in

their study that SWM implies that manager should take decision in the best interest of firm’s

stakeholders. Hence, stakeholders of the firm include all the individuals and groups that

substantially affect the value of it such as personnel, customers, suppliers etc. Considering the

same, on the critical note, Heminway (2017) said that firm’s value or shareholders wealth cannot

be maximized through unhappy customers, employees and poor products. Hence, according to

stakeholders theory for SWM company needs to meet the interest of all the concerned

authorities.

Takacs Haynes, Campbell and Hitt (2017) stated in their study that objective or principle

regarding SWM is based on specific assumptions. In accordance with such objective company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

should make efforts that maximizes or enhance the return to shareholders. In against to making

investment in equity shares, shareholders expect return in the form of capital gain and dividend

for the risk undertaken. Thus, as per such objective, the main motives of business unit are to

minimize the risk which is facing by the shareholders. Sikka and Stittle (2017) criticized such

objective on the basis the aspect that managers pay high level of attention to the wealth

maximization of shareholders. They entailed that investors are not only the stakeholders who

have an interest in firm’s operations. On the basis of such aspect, managers should develop

strategy that contributes in the welfare of employees, customers and others (Is Shareholder Value

Maximization the Right Objective, 2012). Changing legal structure and evolution of social norms

encourages large sized business unit to explore the focus of their accountabilities. In other words,

it can be mentioned that emphasis needs to be placed on other stakeholders as compared to

shareholders. On the other side, Poddar (2017) depicted that SWM is the primary objectives of

firm behind carry out activities and functions. Moreover, shareholders are the one who invest

money in the operations so they considered as real owner. Thus, referring such aspect, it can be

said that firm’s motive in relation to enhancing the value of shareholders wealth is highly

appropriate.

Patra and Dhar (2017) mentioned in the study that assumption of SWM is highly

significant which in turn enables managers and boards to resolve conflicts associated with the

long-term benefit of everyone. For instance: If management invests money for enhancing the

level of customer satisfaction then it provides opportunity to the shareholders to earn high return

on investment. In this way, first assumption pertaining to SWM helps in avoiding conflict takes

place between maximization of shareholders value and customer satisfaction. Kothari, Chance

and Ferris (2017) claimed that assumption of SWM is both unwise and ethically wrong. Findings

of such study presents that along with the shareholders, there are some other stakeholders who

have an interest in firm’s operations and affected from its success or failure. Such stakeholders

include suppliers, employees, customers and local communities etc. Firm and its managers have

accountability to ensure that shareholders are generating suitable or higher return from their

investment. However, company also owes responsibility towards other stakeholders. Referring

such aspect, it can be mentioned that SWM assumption is not highly appropriate.

investment in equity shares, shareholders expect return in the form of capital gain and dividend

for the risk undertaken. Thus, as per such objective, the main motives of business unit are to

minimize the risk which is facing by the shareholders. Sikka and Stittle (2017) criticized such

objective on the basis the aspect that managers pay high level of attention to the wealth

maximization of shareholders. They entailed that investors are not only the stakeholders who

have an interest in firm’s operations. On the basis of such aspect, managers should develop

strategy that contributes in the welfare of employees, customers and others (Is Shareholder Value

Maximization the Right Objective, 2012). Changing legal structure and evolution of social norms

encourages large sized business unit to explore the focus of their accountabilities. In other words,

it can be mentioned that emphasis needs to be placed on other stakeholders as compared to

shareholders. On the other side, Poddar (2017) depicted that SWM is the primary objectives of

firm behind carry out activities and functions. Moreover, shareholders are the one who invest

money in the operations so they considered as real owner. Thus, referring such aspect, it can be

said that firm’s motive in relation to enhancing the value of shareholders wealth is highly

appropriate.

Patra and Dhar (2017) mentioned in the study that assumption of SWM is highly

significant which in turn enables managers and boards to resolve conflicts associated with the

long-term benefit of everyone. For instance: If management invests money for enhancing the

level of customer satisfaction then it provides opportunity to the shareholders to earn high return

on investment. In this way, first assumption pertaining to SWM helps in avoiding conflict takes

place between maximization of shareholders value and customer satisfaction. Kothari, Chance

and Ferris (2017) claimed that assumption of SWM is both unwise and ethically wrong. Findings

of such study presents that along with the shareholders, there are some other stakeholders who

have an interest in firm’s operations and affected from its success or failure. Such stakeholders

include suppliers, employees, customers and local communities etc. Firm and its managers have

accountability to ensure that shareholders are generating suitable or higher return from their

investment. However, company also owes responsibility towards other stakeholders. Referring

such aspect, it can be mentioned that SWM assumption is not highly appropriate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abbott, P., Tarp, F. and Wu (2017) argued in relation to principle of shareholders wealth

maximization on different grounds or aspects. In the context of global business environment,

concept or principle of SWM is losing its significance. Moreover, it does not rely on single or

specific management objective while taking decisions. On the critical note, Hakimi and et.al.,

(2018) presented that SWM objective enhances the level of long-term competitiveness. Further,

such study entails that product market objective guides or support corporate decision making

rather than capital. They believe that business units which consider SWM as primary objective

lose their vision in relation to producing or delivering services. Hence, it can be mentioned that

the aspect of SWM creates a gap between corporation’s mission and motivation, desires as well

as capabilities of personnel. Further, Abedifar, Giudici and Hashem (2017) commented in their

study that principle regarding SWM is not only superior fiduciary standard or management

objective but also considered as societal norms. Hence, referring overall assessment, it can be

depicted that traditional principle or objective regarding SWM is not suitable and biased in

modern era.

Assessing external sources of finance available to the company

External sources of finance imply for the one that are available outside the boundaries of

firm. Usually, company undertakes both internal and external financial sources for meeting

monetary requirements. In the context of Digi Telecommunications, external monetary sources

available are enumerated below:

Equity share capital: By issuing equity share capital concerned telecommunication

company can generate funds and thereby would become able to execute plan. Earning higher

returns is one of the main motives of investors behind investing money in shares or securities.

Hence, investors prefer to invest more money in the venture which in turn offering higher

returns. Thus, through issuing share capital business unit can attract both existing and potential

shareholders. In the case of equity share capital, firm offers dividend to the shareholders when it

earns sufficient margin. Thus, equity shares do not impose fixed monetary obligation in front of

firm.

Long-term debt or bank loan: This is another most effectual funding source that is

undertaken by the company for fulfilling monetary requirements. Long term debt includes bank

loan that is undertaken by financial institution for the period exceeding 12 months. Hence, by

maximization on different grounds or aspects. In the context of global business environment,

concept or principle of SWM is losing its significance. Moreover, it does not rely on single or

specific management objective while taking decisions. On the critical note, Hakimi and et.al.,

(2018) presented that SWM objective enhances the level of long-term competitiveness. Further,

such study entails that product market objective guides or support corporate decision making

rather than capital. They believe that business units which consider SWM as primary objective

lose their vision in relation to producing or delivering services. Hence, it can be mentioned that

the aspect of SWM creates a gap between corporation’s mission and motivation, desires as well

as capabilities of personnel. Further, Abedifar, Giudici and Hashem (2017) commented in their

study that principle regarding SWM is not only superior fiduciary standard or management

objective but also considered as societal norms. Hence, referring overall assessment, it can be

depicted that traditional principle or objective regarding SWM is not suitable and biased in

modern era.

Assessing external sources of finance available to the company

External sources of finance imply for the one that are available outside the boundaries of

firm. Usually, company undertakes both internal and external financial sources for meeting

monetary requirements. In the context of Digi Telecommunications, external monetary sources

available are enumerated below:

Equity share capital: By issuing equity share capital concerned telecommunication

company can generate funds and thereby would become able to execute plan. Earning higher

returns is one of the main motives of investors behind investing money in shares or securities.

Hence, investors prefer to invest more money in the venture which in turn offering higher

returns. Thus, through issuing share capital business unit can attract both existing and potential

shareholders. In the case of equity share capital, firm offers dividend to the shareholders when it

earns sufficient margin. Thus, equity shares do not impose fixed monetary obligation in front of

firm.

Long-term debt or bank loan: This is another most effectual funding source that is

undertaken by the company for fulfilling monetary requirements. Long term debt includes bank

loan that is undertaken by financial institution for the period exceeding 12 months. Hence, by

approaching banking institution for loan firm can generate enough funds needed for the

concerned projects. Moreover, banks also prefer to lend money to the companies which are

growing continuously. Along with this, interest on loan offers high income to the bank so they

ready to provide leading companies with financial assistance. Thus, by taking loan Digi

Telecommunication can finance the concerned project and would become able to get tax

benefits. This is one of the main differences that take place between concerned external sources

such as equity issuance and long-term debt. Unlike share capital, long-term debt source imposes

fixed monetary burden in terms of interest payment.

Stating aspects that business unit needs to consider while choosing the type of finance

Considering the current situation of Digi Telecommunications, it can be depicted that

firm should keep in mind following aspects while making selection of financial source such as:

Cost: At the time of making selection of funding source business unit should consider

the cost of finance. Moreover, the aim of business unit is to maximize the owner’s

wealth by reducing the cost of finance. Thus, it is highly important for the firm to

consider cost of finance while choosing one over another. For instance: If shareholders

perceive the aspect of additional borrowing as bankruptcy risk then they require

additional return to compensate such risk.

In addition to this, Digi Telecommunication also consider solvency ratio while making

selection of funding source. Moreover, high debt level closely impacts the profitability of

firm due to the rise in operating expenses such as interest. The rationale behind this, in

equities company offer dividend to the shareholders only when it generates enough

margin. However, when company takes decision in relation to fulfilling monetary

requirements through issuing new shares then it leads changes in management and

strategic focus (What factors you need to consider when choosing a source of finance in

business, 2018). Further, in the case of new shares issuance uncertainty pertaining to the

success of issuance of new shares. Thus, considering the current level of gearing firm

should select funding source.

Dilution of control: It is another main factors that need to be considered while choosing

financial source. Moreover, when company issues more equity then it may result into

high dilution of control among existing shareholders. Hence, if Digi Telecommunication

concerned projects. Moreover, banks also prefer to lend money to the companies which are

growing continuously. Along with this, interest on loan offers high income to the bank so they

ready to provide leading companies with financial assistance. Thus, by taking loan Digi

Telecommunication can finance the concerned project and would become able to get tax

benefits. This is one of the main differences that take place between concerned external sources

such as equity issuance and long-term debt. Unlike share capital, long-term debt source imposes

fixed monetary burden in terms of interest payment.

Stating aspects that business unit needs to consider while choosing the type of finance

Considering the current situation of Digi Telecommunications, it can be depicted that

firm should keep in mind following aspects while making selection of financial source such as:

Cost: At the time of making selection of funding source business unit should consider

the cost of finance. Moreover, the aim of business unit is to maximize the owner’s

wealth by reducing the cost of finance. Thus, it is highly important for the firm to

consider cost of finance while choosing one over another. For instance: If shareholders

perceive the aspect of additional borrowing as bankruptcy risk then they require

additional return to compensate such risk.

In addition to this, Digi Telecommunication also consider solvency ratio while making

selection of funding source. Moreover, high debt level closely impacts the profitability of

firm due to the rise in operating expenses such as interest. The rationale behind this, in

equities company offer dividend to the shareholders only when it generates enough

margin. However, when company takes decision in relation to fulfilling monetary

requirements through issuing new shares then it leads changes in management and

strategic focus (What factors you need to consider when choosing a source of finance in

business, 2018). Further, in the case of new shares issuance uncertainty pertaining to the

success of issuance of new shares. Thus, considering the current level of gearing firm

should select funding source.

Dilution of control: It is another main factors that need to be considered while choosing

financial source. Moreover, when company issues more equity then it may result into

high dilution of control among existing shareholders. Hence, if Digi Telecommunication

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

does not want to lose their control then it should not focus on issuing or taking resort of

debt. The reason behind this, once the loan is paid back then the relationship ceases. On

the contrary to this, in the case of shares, investors remain in the company until they are

brought out and firm is sold.

Besides this, while selecting funding source Digi Telecommunication should consider the

length of time. For instance: If business unit needs fund for long time period then firm

can take resort of debentures, shares and long term loan. On the other side, to fulfill

monetary needs for short period company should focus on undertaking bank overdraft etc

sources.

Company should also consider repayment terms and conditions while choosing source of

finance. In the case of longer loan, significant amount of interest needs to be paid over

the time frame. However, short term loans demand for high periodic payments. Thus, by

taking into account the level of principal and interest firm should select financing source.

Further, Digi Telecommunication should also focus on conducting cash flow to debt

analysis during high as well as low revenue cycles. This in turn provides high level of

assistance in determining borrowing capacity of an organization. Thus, by determining or

evaluating firm’s ability in relation to making payment of expenses and loan helps in

evaluating debt capacity.

Hence, after making evaluation of all the above depicted sources Digi telecommunication

should select the source that positively contributes in the financial structure and organizational gr

growth.

Working note:

Solvency ratio analysis

Particulars Formula 2015 2016

Group Group

Long-term debt 25,376 1,798,837

Shareholders’ equity 519,362 (Annual

report of Digi

Telecommunications,

519,270

debt. The reason behind this, once the loan is paid back then the relationship ceases. On

the contrary to this, in the case of shares, investors remain in the company until they are

brought out and firm is sold.

Besides this, while selecting funding source Digi Telecommunication should consider the

length of time. For instance: If business unit needs fund for long time period then firm

can take resort of debentures, shares and long term loan. On the other side, to fulfill

monetary needs for short period company should focus on undertaking bank overdraft etc

sources.

Company should also consider repayment terms and conditions while choosing source of

finance. In the case of longer loan, significant amount of interest needs to be paid over

the time frame. However, short term loans demand for high periodic payments. Thus, by

taking into account the level of principal and interest firm should select financing source.

Further, Digi Telecommunication should also focus on conducting cash flow to debt

analysis during high as well as low revenue cycles. This in turn provides high level of

assistance in determining borrowing capacity of an organization. Thus, by determining or

evaluating firm’s ability in relation to making payment of expenses and loan helps in

evaluating debt capacity.

Hence, after making evaluation of all the above depicted sources Digi telecommunication

should select the source that positively contributes in the financial structure and organizational gr

growth.

Working note:

Solvency ratio analysis

Particulars Formula 2015 2016

Group Group

Long-term debt 25,376 1,798,837

Shareholders’ equity 519,362 (Annual

report of Digi

Telecommunications,

519,270

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2016)

Debt-equity ratio Long-term debt /

Shareholders’ equity

.48 3.46

Interpretation: The above depicted table shows that debt-equity ratio of Digi

Telecommunications was .48 and 3.46 in FY 2015 and 2016. This aspect shows that in 2015,

debt equity ratio of Digi telecommunications was near to the ideal ratio such as .5:1 which in

turn considered as good. However, in the accounting year 2016, debt-equity ratio of the company

accounted for 3.46 respectively. It presents that in 2016, firm has fulfilled more of its financial

needs via debt sources rather than equity. In comparison to 2015 and ideal standard it can be

depicted that in FY 2016 debt-equity of Digi Telecommunications was not good. Moreover,

high debt level negatively affects profit margin due to high interest payment on long-term debt.

Hence, referring such aspect it can be stated that solvency position of the company was not good

in 2016 as it contains high debt. Thus, for making improvement in solvency position or aspect

firm should issue shares in the near future. This in turn helps in developing optimal and balanced

capital structure.

Computation of WACC and practical problems regarding the same

Weighted average cost of capital (WACC) implies for the rate of return that company is

expecting to compensate all its different investors. WACC is considered as firm’s cost of capital

which in turn presents the minimum return that a company needs to earn from existing assets to

satisfy different stakeholders such as creditors, owners, capital providers etc. Business unit meets

its financial requirement from wide range of sources such as equity share capital, debt etc.

Hence, WACC is calculated by taking into account the weight of each element mentioned in

capital structure. WACC assessment is mainly based on some assumptions that financial

structure of the company will be similar to the existing one (Evaluating New Projects with

Weighted Average Cost of Capital, 2018). Along with this, it also assumes that no changes will

take place in the risk of new projects. In other words, it can be depicted that computation is based

on the assumption that similar kind of risk exists.

In the context of Digi telecommunication practical problem which in turn creates difficulty in

front of managers while calculating WACC are enumerated below:

Debt-equity ratio Long-term debt /

Shareholders’ equity

.48 3.46

Interpretation: The above depicted table shows that debt-equity ratio of Digi

Telecommunications was .48 and 3.46 in FY 2015 and 2016. This aspect shows that in 2015,

debt equity ratio of Digi telecommunications was near to the ideal ratio such as .5:1 which in

turn considered as good. However, in the accounting year 2016, debt-equity ratio of the company

accounted for 3.46 respectively. It presents that in 2016, firm has fulfilled more of its financial

needs via debt sources rather than equity. In comparison to 2015 and ideal standard it can be

depicted that in FY 2016 debt-equity of Digi Telecommunications was not good. Moreover,

high debt level negatively affects profit margin due to high interest payment on long-term debt.

Hence, referring such aspect it can be stated that solvency position of the company was not good

in 2016 as it contains high debt. Thus, for making improvement in solvency position or aspect

firm should issue shares in the near future. This in turn helps in developing optimal and balanced

capital structure.

Computation of WACC and practical problems regarding the same

Weighted average cost of capital (WACC) implies for the rate of return that company is

expecting to compensate all its different investors. WACC is considered as firm’s cost of capital

which in turn presents the minimum return that a company needs to earn from existing assets to

satisfy different stakeholders such as creditors, owners, capital providers etc. Business unit meets

its financial requirement from wide range of sources such as equity share capital, debt etc.

Hence, WACC is calculated by taking into account the weight of each element mentioned in

capital structure. WACC assessment is mainly based on some assumptions that financial

structure of the company will be similar to the existing one (Evaluating New Projects with

Weighted Average Cost of Capital, 2018). Along with this, it also assumes that no changes will

take place in the risk of new projects. In other words, it can be depicted that computation is based

on the assumption that similar kind of risk exists.

In the context of Digi telecommunication practical problem which in turn creates difficulty in

front of managers while calculating WACC are enumerated below:

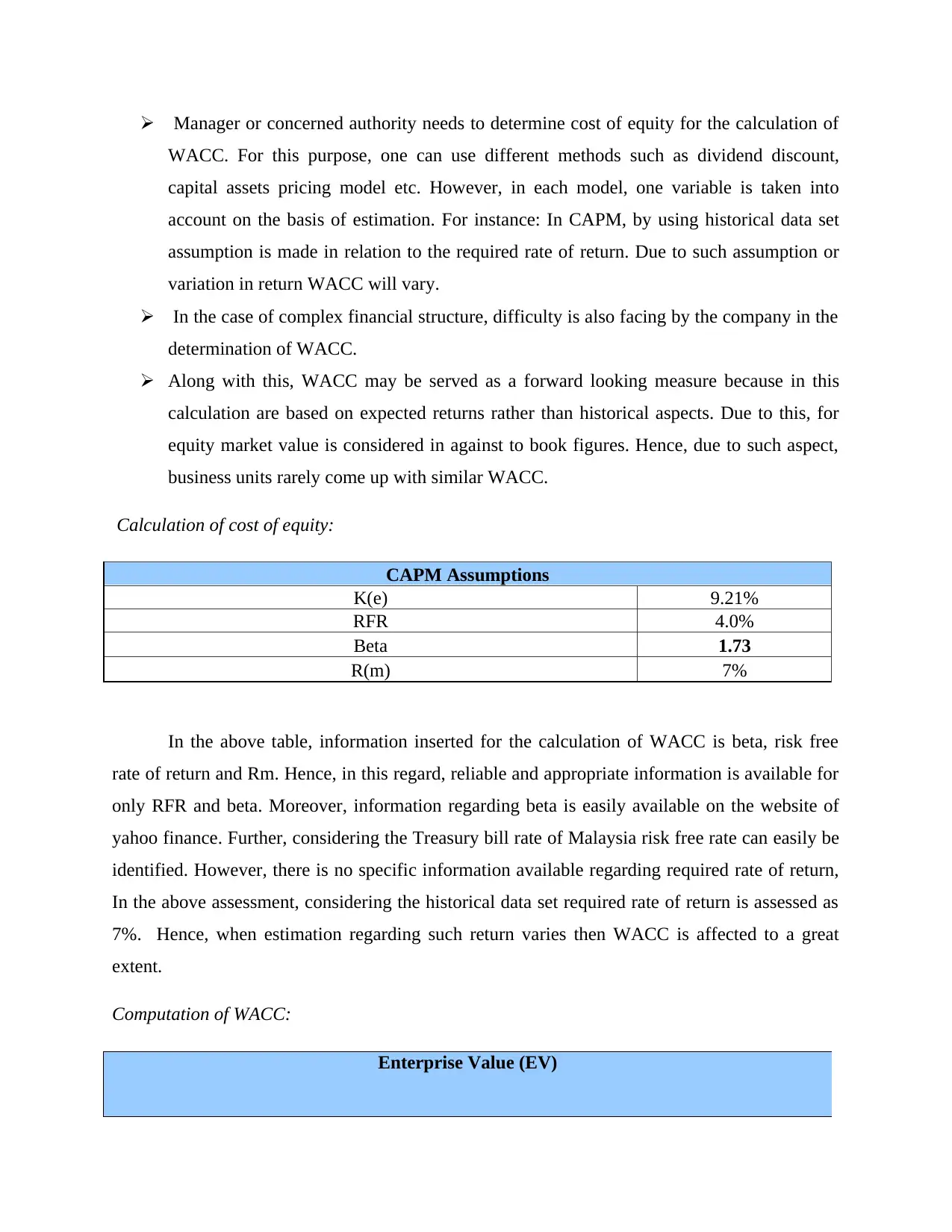

Manager or concerned authority needs to determine cost of equity for the calculation of

WACC. For this purpose, one can use different methods such as dividend discount,

capital assets pricing model etc. However, in each model, one variable is taken into

account on the basis of estimation. For instance: In CAPM, by using historical data set

assumption is made in relation to the required rate of return. Due to such assumption or

variation in return WACC will vary.

In the case of complex financial structure, difficulty is also facing by the company in the

determination of WACC.

Along with this, WACC may be served as a forward looking measure because in this

calculation are based on expected returns rather than historical aspects. Due to this, for

equity market value is considered in against to book figures. Hence, due to such aspect,

business units rarely come up with similar WACC.

Calculation of cost of equity:

CAPM Assumptions

K(e) 9.21%

RFR 4.0%

Beta 1.73

R(m) 7%

In the above table, information inserted for the calculation of WACC is beta, risk free

rate of return and Rm. Hence, in this regard, reliable and appropriate information is available for

only RFR and beta. Moreover, information regarding beta is easily available on the website of

yahoo finance. Further, considering the Treasury bill rate of Malaysia risk free rate can easily be

identified. However, there is no specific information available regarding required rate of return,

In the above assessment, considering the historical data set required rate of return is assessed as

7%. Hence, when estimation regarding such return varies then WACC is affected to a great

extent.

Computation of WACC:

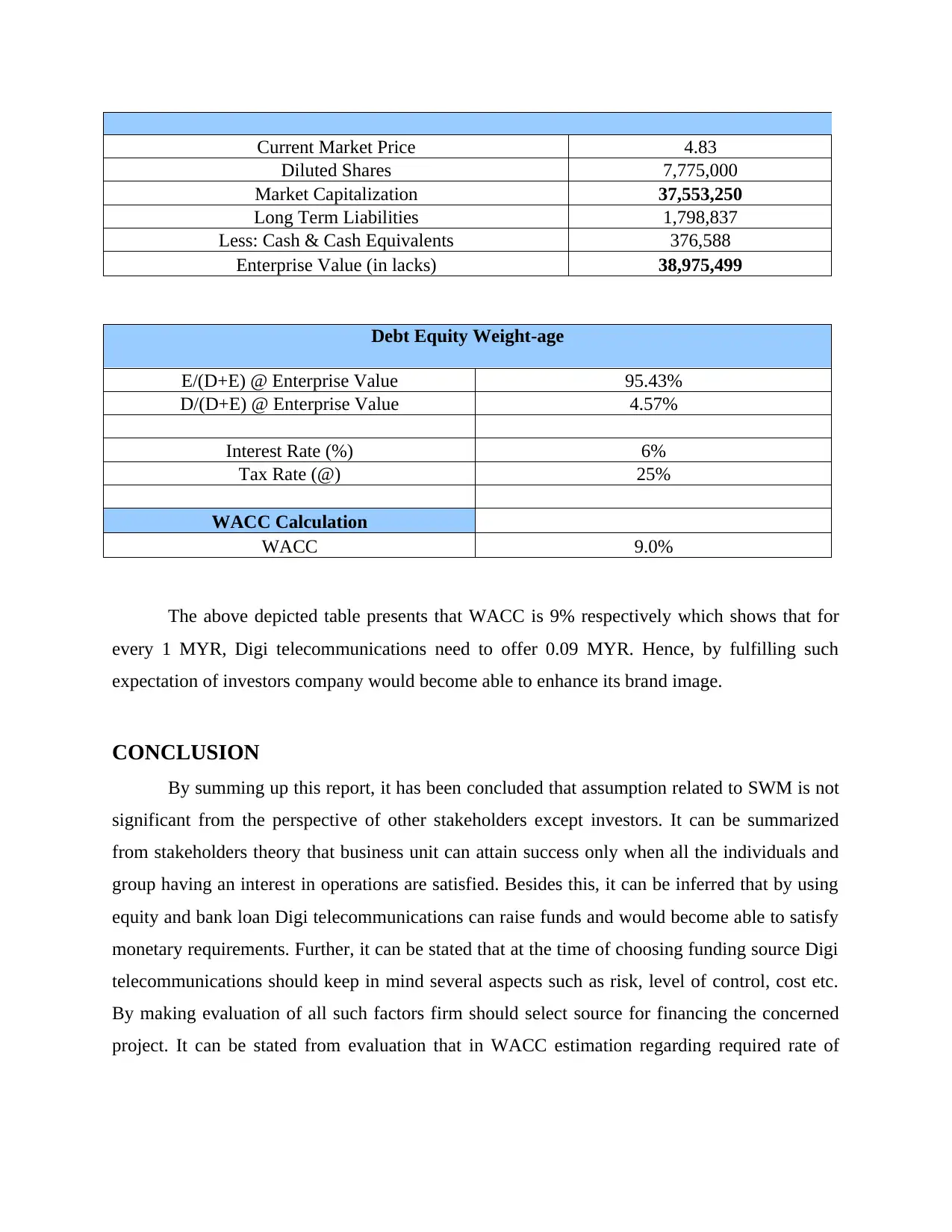

Enterprise Value (EV)

WACC. For this purpose, one can use different methods such as dividend discount,

capital assets pricing model etc. However, in each model, one variable is taken into

account on the basis of estimation. For instance: In CAPM, by using historical data set

assumption is made in relation to the required rate of return. Due to such assumption or

variation in return WACC will vary.

In the case of complex financial structure, difficulty is also facing by the company in the

determination of WACC.

Along with this, WACC may be served as a forward looking measure because in this

calculation are based on expected returns rather than historical aspects. Due to this, for

equity market value is considered in against to book figures. Hence, due to such aspect,

business units rarely come up with similar WACC.

Calculation of cost of equity:

CAPM Assumptions

K(e) 9.21%

RFR 4.0%

Beta 1.73

R(m) 7%

In the above table, information inserted for the calculation of WACC is beta, risk free

rate of return and Rm. Hence, in this regard, reliable and appropriate information is available for

only RFR and beta. Moreover, information regarding beta is easily available on the website of

yahoo finance. Further, considering the Treasury bill rate of Malaysia risk free rate can easily be

identified. However, there is no specific information available regarding required rate of return,

In the above assessment, considering the historical data set required rate of return is assessed as

7%. Hence, when estimation regarding such return varies then WACC is affected to a great

extent.

Computation of WACC:

Enterprise Value (EV)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current Market Price 4.83

Diluted Shares 7,775,000

Market Capitalization 37,553,250

Long Term Liabilities 1,798,837

Less: Cash & Cash Equivalents 376,588

Enterprise Value (in lacks) 38,975,499

Debt Equity Weight-age

E/(D+E) @ Enterprise Value 95.43%

D/(D+E) @ Enterprise Value 4.57%

Interest Rate (%) 6%

Tax Rate (@) 25%

WACC Calculation

WACC 9.0%

The above depicted table presents that WACC is 9% respectively which shows that for

every 1 MYR, Digi telecommunications need to offer 0.09 MYR. Hence, by fulfilling such

expectation of investors company would become able to enhance its brand image.

CONCLUSION

By summing up this report, it has been concluded that assumption related to SWM is not

significant from the perspective of other stakeholders except investors. It can be summarized

from stakeholders theory that business unit can attain success only when all the individuals and

group having an interest in operations are satisfied. Besides this, it can be inferred that by using

equity and bank loan Digi telecommunications can raise funds and would become able to satisfy

monetary requirements. Further, it can be stated that at the time of choosing funding source Digi

telecommunications should keep in mind several aspects such as risk, level of control, cost etc.

By making evaluation of all such factors firm should select source for financing the concerned

project. It can be stated from evaluation that in WACC estimation regarding required rate of

Diluted Shares 7,775,000

Market Capitalization 37,553,250

Long Term Liabilities 1,798,837

Less: Cash & Cash Equivalents 376,588

Enterprise Value (in lacks) 38,975,499

Debt Equity Weight-age

E/(D+E) @ Enterprise Value 95.43%

D/(D+E) @ Enterprise Value 4.57%

Interest Rate (%) 6%

Tax Rate (@) 25%

WACC Calculation

WACC 9.0%

The above depicted table presents that WACC is 9% respectively which shows that for

every 1 MYR, Digi telecommunications need to offer 0.09 MYR. Hence, by fulfilling such

expectation of investors company would become able to enhance its brand image.

CONCLUSION

By summing up this report, it has been concluded that assumption related to SWM is not

significant from the perspective of other stakeholders except investors. It can be summarized

from stakeholders theory that business unit can attain success only when all the individuals and

group having an interest in operations are satisfied. Besides this, it can be inferred that by using

equity and bank loan Digi telecommunications can raise funds and would become able to satisfy

monetary requirements. Further, it can be stated that at the time of choosing funding source Digi

telecommunications should keep in mind several aspects such as risk, level of control, cost etc.

By making evaluation of all such factors firm should select source for financing the concerned

project. It can be stated from evaluation that in WACC estimation regarding required rate of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

return is made. Hence, variations take place in such estimations have greater influence on

WACC and thereby decision making of investors.

RECOMMENDATIONS

Digi Telecommunication is advised to lay focus on developing suitable and strategic

framework that meets the objective of all stakeholders. Moreover, by placing emphasis

only on SWM company would not become able to achieve success or gain competitive

edge over others.

Further, referring the outcome of debt-equity ratio it is recommended to Digi

Telecommunications that focus needs to be placed on the maintenance of ideal standard

such as .5:1. The rationale behind this, increasing debt level imposes financial burden in

front of firm regarding interest payment. Moreover, in the case of debt, firm has to make

interest payment whether it generates enough profit or not.

In order to deal with the issues of WACC regarding making estimation about the

required rate of return analyst should consider historical returns not less than of 5 years.

Hence, such assessment will provide high level of assistance in making appropriate

estimation regarding market return.

WACC and thereby decision making of investors.

RECOMMENDATIONS

Digi Telecommunication is advised to lay focus on developing suitable and strategic

framework that meets the objective of all stakeholders. Moreover, by placing emphasis

only on SWM company would not become able to achieve success or gain competitive

edge over others.

Further, referring the outcome of debt-equity ratio it is recommended to Digi

Telecommunications that focus needs to be placed on the maintenance of ideal standard

such as .5:1. The rationale behind this, increasing debt level imposes financial burden in

front of firm regarding interest payment. Moreover, in the case of debt, firm has to make

interest payment whether it generates enough profit or not.

In order to deal with the issues of WACC regarding making estimation about the

required rate of return analyst should consider historical returns not less than of 5 years.

Hence, such assessment will provide high level of assistance in making appropriate

estimation regarding market return.

REFERENCES

Books and Journals

Abbott, P., Tarp, F. and Wu, C., 2017. Structural Transformation, Biased Technological Change

and Employment in Vietnam. The European Journal of Development Research. 29(1). pp.54-

72.

Abedifar, P., Giudici, P. and Hashem, S. Q., 2017. Heterogeneous market structure and systemic

risk: Evidence from dual banking systems. Journal of Financial Stability. 33. pp.96-119.

Gunawan, G., 2017. Pengaruh Karakteristik Perusahaan dan Kepemilikan terhadap Utang

Perusahaan Real Estat yang Terdaftar di Bursa Efek Indonesia Periode 2008-2013. Jurnal

Keuangan dan Perbankan. 12(2). pp.165-184.

Hakimi, A. and et.al., 2018. Do board characteristics affect bank performance? Evidence from

the Bahrain Islamic banks. Journal of Islamic Accounting and Business Research, (just-

accepted), pp.00-00.

Heminway, J. M., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional

Law, and Organic Documents. Wash. & Lee L. Rev.. 74. p.939.

Janusz, G. and et.al., 2017. Global Crisis in the Central-Eastern European Region-Influence on

Finanacial Systems and Small and Medium-Sized Enterprises. Tematski zbornici. pp.274-

274.

Kothari, P., Chance, D. and Ferris, S., 2017. Brag, Brag, Brag: Corporate Crowing and

Shareholder Wealth. Sage publications.

Ofori‐Sasu, D., Abor, J. Y. and Osei, A. K., 2017. Dividend policy and shareholders’ value:

evidence from listed companies in Ghana. African Development Review. 29(2). pp.293-304.

Patra, A. and Dhar, P., 2017. Impact of Dividend Policy on Shareholders’ Value: A Study on

Apollo Hospitals Ltd. Bharatiya Vidya Bhavan Institute of Management Science, Kolkata-97.

p.11.

Books and Journals

Abbott, P., Tarp, F. and Wu, C., 2017. Structural Transformation, Biased Technological Change

and Employment in Vietnam. The European Journal of Development Research. 29(1). pp.54-

72.

Abedifar, P., Giudici, P. and Hashem, S. Q., 2017. Heterogeneous market structure and systemic

risk: Evidence from dual banking systems. Journal of Financial Stability. 33. pp.96-119.

Gunawan, G., 2017. Pengaruh Karakteristik Perusahaan dan Kepemilikan terhadap Utang

Perusahaan Real Estat yang Terdaftar di Bursa Efek Indonesia Periode 2008-2013. Jurnal

Keuangan dan Perbankan. 12(2). pp.165-184.

Hakimi, A. and et.al., 2018. Do board characteristics affect bank performance? Evidence from

the Bahrain Islamic banks. Journal of Islamic Accounting and Business Research, (just-

accepted), pp.00-00.

Heminway, J. M., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional

Law, and Organic Documents. Wash. & Lee L. Rev.. 74. p.939.

Janusz, G. and et.al., 2017. Global Crisis in the Central-Eastern European Region-Influence on

Finanacial Systems and Small and Medium-Sized Enterprises. Tematski zbornici. pp.274-

274.

Kothari, P., Chance, D. and Ferris, S., 2017. Brag, Brag, Brag: Corporate Crowing and

Shareholder Wealth. Sage publications.

Ofori‐Sasu, D., Abor, J. Y. and Osei, A. K., 2017. Dividend policy and shareholders’ value:

evidence from listed companies in Ghana. African Development Review. 29(2). pp.293-304.

Patra, A. and Dhar, P., 2017. Impact of Dividend Policy on Shareholders’ Value: A Study on

Apollo Hospitals Ltd. Bharatiya Vidya Bhavan Institute of Management Science, Kolkata-97.

p.11.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.