Literature Review: Impact of Digital Disruption on Lloyd Banking Group

VerifiedAdded on 2023/06/15

|17

|5371

|109

Literature Review

AI Summary

This document presents a literature review exploring the impact of digital disruption on the banking sector, with a specific focus on Lloyd Banking Group. It begins by defining digital disruption and its effects on businesses, particularly in the banking industry. The review investigates how technological advancements, such as artificial intelligence and blockchain, are reshaping banking transactions and impacting competitive advantages. It further examines the effects of digitalization on the banking sector in the United Kingdom, considering factors like changing consumer preferences and the adoption of disruptive business models. The research aims to identify the challenges and opportunities presented by digital disruption, providing insights into how banks can adapt and thrive in this evolving landscape. The structure of the research is outlined, including chapters on introduction, literature review, research methodology, data analysis, and conclusion, ensuring a systematic approach to understanding and addressing the research questions.

Research Methods in Finance and

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Overview of the topic..................................................................................................................3

Research aim and objectives.......................................................................................................3

Research Questions.....................................................................................................................4

Research rational.........................................................................................................................4

Structure of the research..............................................................................................................4

LITERATURE REVIEW................................................................................................................6

What is the digital disruptive within banking sector...................................................................6

Which are disruptive technological advances impacting the transaction of Lloyd banking

industry?......................................................................................................................................7

How digitalisation affected the banking sector of United Kingdom?.........................................8

DATA AND METHODS..............................................................................................................10

Data ..........................................................................................................................................10

Methods ....................................................................................................................................11

TIME SCALE ...............................................................................................................................14

REFERENCES..............................................................................................................................16

2

INTRODUCTION...........................................................................................................................3

Overview of the topic..................................................................................................................3

Research aim and objectives.......................................................................................................3

Research Questions.....................................................................................................................4

Research rational.........................................................................................................................4

Structure of the research..............................................................................................................4

LITERATURE REVIEW................................................................................................................6

What is the digital disruptive within banking sector...................................................................6

Which are disruptive technological advances impacting the transaction of Lloyd banking

industry?......................................................................................................................................7

How digitalisation affected the banking sector of United Kingdom?.........................................8

DATA AND METHODS..............................................................................................................10

Data ..........................................................................................................................................10

Methods ....................................................................................................................................11

TIME SCALE ...............................................................................................................................14

REFERENCES..............................................................................................................................16

2

INTRODUCTION

Overview of the topic

With the change in the working process of the business, the concept of digital technology

gain major importance. As the business environment is so dynamic and to cope up with and run

the business it become very necessary for the organisation to adopt digital technology so that

work load can be reduced. Digital technology can be defined as using various electronic tools

and devices so that resources can be utilise and data can be stored for longer time period. Digital

technology can help the companies to gain advantages but there are some disadvantage also that

affect the business operation and will act as a hurdle to achieve goals and objectives. Digital

disruption is that act as change which either create problem or reduce the value proposition of

the company's goods and service that they offer (Skog, Wimelius and Sandberg, 2018). With the

rapid advancement the digital disruption also increased and is becoming a threat for many

industry. When digital innovation happen then digital disruption maximise. Through this many

of the company are affected by it as some of the competitor with use of technology try to provide

misused or creates bad image for the companies. This digital disruption was used so that the

rivalry can gain competitive advantage by hinder the goodwill of other competitor (Myruski and

et. Al, 2018).

In this report the company that is choosing from the banking sector is Lloyd bank. Lloyd

bank is a British retail and commercial bank and is one of the largest bank in the Britain.. The

company was founded in 1765 by John Taylor and Sampson Lloyd. It headquarter is in London,

United Kingdom. There are so many branches of the company Across England and Wales.

There are so many digital services that is offered by the bank, so the researcher has selected this

organisation so that it can be see the impact of digital disruption on the performace of te

company (Matzler and et. Al, 2018).

Research topic: Digital disruption on banking sector and its competition

Research aim and objectives

Aim:

To identify the impact of digital disruption on banking sector and its competition: A study on

Lloyd Banking Group

Objectives:

3

Overview of the topic

With the change in the working process of the business, the concept of digital technology

gain major importance. As the business environment is so dynamic and to cope up with and run

the business it become very necessary for the organisation to adopt digital technology so that

work load can be reduced. Digital technology can be defined as using various electronic tools

and devices so that resources can be utilise and data can be stored for longer time period. Digital

technology can help the companies to gain advantages but there are some disadvantage also that

affect the business operation and will act as a hurdle to achieve goals and objectives. Digital

disruption is that act as change which either create problem or reduce the value proposition of

the company's goods and service that they offer (Skog, Wimelius and Sandberg, 2018). With the

rapid advancement the digital disruption also increased and is becoming a threat for many

industry. When digital innovation happen then digital disruption maximise. Through this many

of the company are affected by it as some of the competitor with use of technology try to provide

misused or creates bad image for the companies. This digital disruption was used so that the

rivalry can gain competitive advantage by hinder the goodwill of other competitor (Myruski and

et. Al, 2018).

In this report the company that is choosing from the banking sector is Lloyd bank. Lloyd

bank is a British retail and commercial bank and is one of the largest bank in the Britain.. The

company was founded in 1765 by John Taylor and Sampson Lloyd. It headquarter is in London,

United Kingdom. There are so many branches of the company Across England and Wales.

There are so many digital services that is offered by the bank, so the researcher has selected this

organisation so that it can be see the impact of digital disruption on the performace of te

company (Matzler and et. Al, 2018).

Research topic: Digital disruption on banking sector and its competition

Research aim and objectives

Aim:

To identify the impact of digital disruption on banking sector and its competition: A study on

Lloyd Banking Group

Objectives:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To understand the concept of Digital Disruptive within banking sector.

To identify the impact of disruptive technological advances on transaction in banking

sector.

To know the affect of Digitalisation on banking sector of United Kingdom.

Research Questions

What is the digital disruptive within banking sector?

Which are disruptive technological advances impacting the transaction of Lloyd banking

industry?

How digitalisation affected the banking sector of United Kingdom?

Research rational

The topic is selected for carrying out the research on the impact of digital disruptive on

banking sector. The main reason behind choosing the the research topic is to full fill two

subjective that is Personal and Professional. In respect to the personal aim it will help in

determining the affect of digital disruption ad the technology that act as a challenge while dong

any banking transaction. This will simultaneously aid in knowing the tools and techniques about

the networks and devices so that they can be acquire by the individual in their own skills and

knowledge. The another personal benefit that can be gained by this research is that knowing the

impact of various social disruption that occurs on the banks , so that it cab be used in future for

effective solving the problem. In respect to the professional aim, the benefit of this research is

that it will help to utilise the skills and knowledge and find the right job in that field. In further

this would also help in developing a sound professional career along with building the effective

job personality that will assist in solving all the queries that will occurs in the organisation in

more affective and efficient manner. It was also help to gain the detail knowledge about the

challenges that will face when the professional career will be developed in the field of digital

technology (Geissinger, Laurell and Sandström, 2020).

Structure of the research

There are various chapter that are covered while writing the research. They are used for

effective completion of each activity that are there in the report so that research can be completed

in systematic and efficient manner. These chapter are discussed below in detail manner:

4

To identify the impact of disruptive technological advances on transaction in banking

sector.

To know the affect of Digitalisation on banking sector of United Kingdom.

Research Questions

What is the digital disruptive within banking sector?

Which are disruptive technological advances impacting the transaction of Lloyd banking

industry?

How digitalisation affected the banking sector of United Kingdom?

Research rational

The topic is selected for carrying out the research on the impact of digital disruptive on

banking sector. The main reason behind choosing the the research topic is to full fill two

subjective that is Personal and Professional. In respect to the personal aim it will help in

determining the affect of digital disruption ad the technology that act as a challenge while dong

any banking transaction. This will simultaneously aid in knowing the tools and techniques about

the networks and devices so that they can be acquire by the individual in their own skills and

knowledge. The another personal benefit that can be gained by this research is that knowing the

impact of various social disruption that occurs on the banks , so that it cab be used in future for

effective solving the problem. In respect to the professional aim, the benefit of this research is

that it will help to utilise the skills and knowledge and find the right job in that field. In further

this would also help in developing a sound professional career along with building the effective

job personality that will assist in solving all the queries that will occurs in the organisation in

more affective and efficient manner. It was also help to gain the detail knowledge about the

challenges that will face when the professional career will be developed in the field of digital

technology (Geissinger, Laurell and Sandström, 2020).

Structure of the research

There are various chapter that are covered while writing the research. They are used for

effective completion of each activity that are there in the report so that research can be completed

in systematic and efficient manner. These chapter are discussed below in detail manner:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Chapter 1: Introduction: This is the first chapter of the report which covered different

information such as Overview of the research topic, background of the topic, research aim and

objectives, significance of the study, research problem, rational of research and many more. All

of these are the important information that help the researcher in completing the other chapters of

the report in effective manner.

Chapter 2: Literature review: The second chapter of the report is Literature review that cover

all the past publish data of the report topic. This part is written in the research so that secondary

data can be collected from various sources like books. Journal, online sites, magazine and many

more. This also help the investigator to answer the research question in very better way and in

detail knowledge.

Chapter 3: Research methodology: This chapter helps in gathering accurate and exact

information from different methods. In this various components are included that is approach,

philosophy, strategy, choice, design data collection, time horizon, sampling and research ethics.

They all help the examiner to gather the reliable and valid information by using main

methodology.

Chapter 4: Data analysis and findings: This is the another chapter that helps in analysing the

collected data by using various analytics tool so that accurate information can be obtained.

Within this part, if the data is quantitative then the questionnaire is analysed by using frequency

distribution and in Qualitative the data is obtained by interview , the analyses is made by using

thematic. These both tool has different result is based on the type of collected data.

Chapter 5: Conclusion: It is the last chapter of the research that include short summary of all

the chapters. In recommendation, some suggestion are provided to the organisation so that they

can improve the digital disruption within banking sector (Williams, 2018).

5

information such as Overview of the research topic, background of the topic, research aim and

objectives, significance of the study, research problem, rational of research and many more. All

of these are the important information that help the researcher in completing the other chapters of

the report in effective manner.

Chapter 2: Literature review: The second chapter of the report is Literature review that cover

all the past publish data of the report topic. This part is written in the research so that secondary

data can be collected from various sources like books. Journal, online sites, magazine and many

more. This also help the investigator to answer the research question in very better way and in

detail knowledge.

Chapter 3: Research methodology: This chapter helps in gathering accurate and exact

information from different methods. In this various components are included that is approach,

philosophy, strategy, choice, design data collection, time horizon, sampling and research ethics.

They all help the examiner to gather the reliable and valid information by using main

methodology.

Chapter 4: Data analysis and findings: This is the another chapter that helps in analysing the

collected data by using various analytics tool so that accurate information can be obtained.

Within this part, if the data is quantitative then the questionnaire is analysed by using frequency

distribution and in Qualitative the data is obtained by interview , the analyses is made by using

thematic. These both tool has different result is based on the type of collected data.

Chapter 5: Conclusion: It is the last chapter of the research that include short summary of all

the chapters. In recommendation, some suggestion are provided to the organisation so that they

can improve the digital disruption within banking sector (Williams, 2018).

5

LITERATURE REVIEW

What is the digital disruptive within banking sector.

According to Nuyens (2019) , Digital Disruption is an effect, that changes the way of

working when digital networks are being used. This disruption is caused due to acquiring of

various network based devices and channels for working. This change can be happen to the value

of goods and service or the image of the organisation. With the fast changing taste and

preference of the buyers, many technological advancement are being made. This advantages

creates problem and are used in bad ways. The rapid uses of mobile and shifting of the work

there is increase in digital disruptive which are affecting the company as well as help the others

to gain competitive advantages. One of he most important sector that is worse affected by the

term is banking sector. There are so many challenges that are being faced by the the firms hat are

operated there because most of their works are done using digital networks. There are four

distinct components of digital disruption these are as follow:

Technology: Technology includes those belongings like inventions, design etc.

Business: Some of elements that is covered in this is pricing, delivering and developing the

goods and services.

Industry: Includes Consumers, market, methods, process and many more.

Society: Covers culture, cast, religion, habits and taste and preferences (Wollmann, Kühn and

Kempf, 2020).

By using Digital disruption it helps the company to gain competitive advantages. When there is

any digital gap then the banking sector understand that the needs of the buyers are changing and

is becoming a major concern so that they can change themselves according to the technique their

buyer wants. They provide them the idea which they can apply in their services so that they can

cope up with the trend. Some of the digital disruption business model are:

The subscription model: In this Disruptive model the buyer use lock in technology in which

they buy product and services by purchasing the subscription. Like Netflix, Apple music and

many more.

The Freemium model: These disrupts while digital sampling in which the purchase fund for

some basic product and services with some data instead of money, such as Spotify, LinkedIn etc.

6

What is the digital disruptive within banking sector.

According to Nuyens (2019) , Digital Disruption is an effect, that changes the way of

working when digital networks are being used. This disruption is caused due to acquiring of

various network based devices and channels for working. This change can be happen to the value

of goods and service or the image of the organisation. With the fast changing taste and

preference of the buyers, many technological advancement are being made. This advantages

creates problem and are used in bad ways. The rapid uses of mobile and shifting of the work

there is increase in digital disruptive which are affecting the company as well as help the others

to gain competitive advantages. One of he most important sector that is worse affected by the

term is banking sector. There are so many challenges that are being faced by the the firms hat are

operated there because most of their works are done using digital networks. There are four

distinct components of digital disruption these are as follow:

Technology: Technology includes those belongings like inventions, design etc.

Business: Some of elements that is covered in this is pricing, delivering and developing the

goods and services.

Industry: Includes Consumers, market, methods, process and many more.

Society: Covers culture, cast, religion, habits and taste and preferences (Wollmann, Kühn and

Kempf, 2020).

By using Digital disruption it helps the company to gain competitive advantages. When there is

any digital gap then the banking sector understand that the needs of the buyers are changing and

is becoming a major concern so that they can change themselves according to the technique their

buyer wants. They provide them the idea which they can apply in their services so that they can

cope up with the trend. Some of the digital disruption business model are:

The subscription model: In this Disruptive model the buyer use lock in technology in which

they buy product and services by purchasing the subscription. Like Netflix, Apple music and

many more.

The Freemium model: These disrupts while digital sampling in which the purchase fund for

some basic product and services with some data instead of money, such as Spotify, LinkedIn etc.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Access over ownership model: In this digital disruption is occur when company give

access to see the goods and service but can be used when they are purchased. Example of this

model are Zip car, Peer buy, AirBnB etc.

if digital disruption is to be made in the banking sector then it would happen by two factors.

These are the Supply side that means developing the technology and the problem is created and

the demand side in which disruption occur when buyers expectation form the bank service

changes. The Banking sector uses different disruptive digital technologies these can be Artificial

intelligence, Block chain and Robotics. These technology affect the business growth and

performance of the company (Alam, Gupta and Zameni, 2019).

Which are disruptive technological advances impacting the transaction of Lloyd banking

industry?

According to Disruption, (2021) There are various types of disruptive technological

advancement which are being used in the banking industry. As almost every advances are

regarding as the lost of the next big things which are being used in the organisation for longer

duration. Further, not every emerging technology will alter the business or the social landscape.

Disruptive technologies are the advances which are transforming the life, global economy and

the business especially the banking industry which can helps the business sin achieving their

goals ad objectives and do their work easier as compared to the other business. There are various

types of technologies which are coming in the banking industry in order to develop their

effectiveness and achieving their goals. Some of disruptive technologies which are being used in

the Lloyd banking industry. These are Artificial intelligence- as in banking and the service

sectors, it is pressure to adopt new and latest technologies which can impact their customers and

also in this employees get satisfied with the banking services. Further, this will be resulting in

saving the cost of company and also by this there is a expectation rise in the company profits.

Further, the Lloyd banking industry, is using artificial intelligence which is a customer service

from the robots and the chat box. There are various banking institutions which are resulting in

gaining more information (Makhija, and Chacko, 2021). This helps the customer facing way is

AI which is the deployed is to enhanced the mobile banking that helps in allowing the 24/7

access top the customer which helps the customer in allowing to continue their transaction and

check anything in 24/7 hours.

7

access to see the goods and service but can be used when they are purchased. Example of this

model are Zip car, Peer buy, AirBnB etc.

if digital disruption is to be made in the banking sector then it would happen by two factors.

These are the Supply side that means developing the technology and the problem is created and

the demand side in which disruption occur when buyers expectation form the bank service

changes. The Banking sector uses different disruptive digital technologies these can be Artificial

intelligence, Block chain and Robotics. These technology affect the business growth and

performance of the company (Alam, Gupta and Zameni, 2019).

Which are disruptive technological advances impacting the transaction of Lloyd banking

industry?

According to Disruption, (2021) There are various types of disruptive technological

advancement which are being used in the banking industry. As almost every advances are

regarding as the lost of the next big things which are being used in the organisation for longer

duration. Further, not every emerging technology will alter the business or the social landscape.

Disruptive technologies are the advances which are transforming the life, global economy and

the business especially the banking industry which can helps the business sin achieving their

goals ad objectives and do their work easier as compared to the other business. There are various

types of technologies which are coming in the banking industry in order to develop their

effectiveness and achieving their goals. Some of disruptive technologies which are being used in

the Lloyd banking industry. These are Artificial intelligence- as in banking and the service

sectors, it is pressure to adopt new and latest technologies which can impact their customers and

also in this employees get satisfied with the banking services. Further, this will be resulting in

saving the cost of company and also by this there is a expectation rise in the company profits.

Further, the Lloyd banking industry, is using artificial intelligence which is a customer service

from the robots and the chat box. There are various banking institutions which are resulting in

gaining more information (Makhija, and Chacko, 2021). This helps the customer facing way is

AI which is the deployed is to enhanced the mobile banking that helps in allowing the 24/7

access top the customer which helps the customer in allowing to continue their transaction and

check anything in 24/7 hours.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The next disruptive technology which is being used in the bank is Block chain- as it is a

technology which is used in the banking industry and it is also distributed the databases that can

helps in tracking of the transactions in a permanent and the verifiable way. This is a block chain

which disrupt banks in the way and in the internet media. These block chain are transparent and

these are highly secure and safe and also relatively cheap while operating its services. There are

more financial institution which realize how the block chain can improve the security and the

improve the customer satisfaction. Block chain is helping in supporting of the banking ways and

it is showing the used for payments and also it is a way their capital markets work. The next

disruptive technology is big data which is one of the way to determine the technology influence

on the banking industry and currently Lloyd banking industry is one of bank which is using big

data and business analytics solutions (Martino, 2021). This includes amount of data generated by

the finance industry. It includes certain things like ATM withdrawal, credit scores, credit card

transactions and the credit scores etc. these technologies are used in the Lloyd banking industry

as impacting the transaction.

How digitalisation affected the banking sector of United Kingdom?

According to McNulty, and Milne, (2021) Digital is refers to the new buzz which is used

in every sector. This is all around the globe which is shifting towards the digitalisation process.

There are certain sizes which are across all the regions and which is making huge investments in

the digital initiatives. Adoption of the digitalization is most important because this helps in

banking sector for achievement of the organisational goals and objectives. Digitalisation is

affecting the banking industry in positive and negative ways. As it provides convenience to the

customers and also helping in saving their time and cost. Further, digitalisation is the manual

process which includes certain transactions and activities into the digital services. This is all

across the world and this will be helping the company in enhancing their growth opportunities as

well. Digitalisation has reduces the human errors and also it builds the customer loyalty. Today,

in this people are having access to their banks in their smart phones and they can easily handle

their transactions and make payments to nay person through using smart phones. This has made

convenience for the customers. On the next hand, digitalisation has saved the time of banking

industry and also by this they could handle the customer complaints in most effective manner

and providing them online banking which is resulting in attracting more of the customers. Now a

8

technology which is used in the banking industry and it is also distributed the databases that can

helps in tracking of the transactions in a permanent and the verifiable way. This is a block chain

which disrupt banks in the way and in the internet media. These block chain are transparent and

these are highly secure and safe and also relatively cheap while operating its services. There are

more financial institution which realize how the block chain can improve the security and the

improve the customer satisfaction. Block chain is helping in supporting of the banking ways and

it is showing the used for payments and also it is a way their capital markets work. The next

disruptive technology is big data which is one of the way to determine the technology influence

on the banking industry and currently Lloyd banking industry is one of bank which is using big

data and business analytics solutions (Martino, 2021). This includes amount of data generated by

the finance industry. It includes certain things like ATM withdrawal, credit scores, credit card

transactions and the credit scores etc. these technologies are used in the Lloyd banking industry

as impacting the transaction.

How digitalisation affected the banking sector of United Kingdom?

According to McNulty, and Milne, (2021) Digital is refers to the new buzz which is used

in every sector. This is all around the globe which is shifting towards the digitalisation process.

There are certain sizes which are across all the regions and which is making huge investments in

the digital initiatives. Adoption of the digitalization is most important because this helps in

banking sector for achievement of the organisational goals and objectives. Digitalisation is

affecting the banking industry in positive and negative ways. As it provides convenience to the

customers and also helping in saving their time and cost. Further, digitalisation is the manual

process which includes certain transactions and activities into the digital services. This is all

across the world and this will be helping the company in enhancing their growth opportunities as

well. Digitalisation has reduces the human errors and also it builds the customer loyalty. Today,

in this people are having access to their banks in their smart phones and they can easily handle

their transactions and make payments to nay person through using smart phones. This has made

convenience for the customers. On the next hand, digitalisation has saved the time of banking

industry and also by this they could handle the customer complaints in most effective manner

and providing them online banking which is resulting in attracting more of the customers. Now a

8

days many of the commercial banks have started using digital customer services in order to

remain be competitive and relevant in the race.

Banks are getting various benefits of using these disruptive technologies such as it helps

in generating revenue through several channels. The other commercial banks have shifted

towards achievement of adopting of the newer technologies. As E- banking is resulting in

reducing the cost dramatically and also it generated more revenue as compared to the traditional

method (Alshawaaf, and Lee, 2021). Use of automation and the Bank mechanization and the

introduction of MICR which is based on the cheque processing. In relation with the Lloyd

banking industry, they are developing new technologies which is impacting their business in

positive ways such as Big data, artificial intelligence and cloud computing etc. which helps the

banks in storing there customer data and information effectively and resulting in managing all

the task effectively. However, there could be negative effects of digitalisation which is resulting

in reducing performance of banks. As these digital technological technologies can be risky and

this is affecting the performance as well. It should be secure and efficient in managing their data

and informational and resulting in developing true information. Further, these technologies could

be costly to the banks while managing and also it needs professional IT departments in order to

manage it (de la Feria, and Maffini, 2021). So, it is being analysed that digitalisation is impacting

the business in most effective way and also impacting the banking profits as well.

9

remain be competitive and relevant in the race.

Banks are getting various benefits of using these disruptive technologies such as it helps

in generating revenue through several channels. The other commercial banks have shifted

towards achievement of adopting of the newer technologies. As E- banking is resulting in

reducing the cost dramatically and also it generated more revenue as compared to the traditional

method (Alshawaaf, and Lee, 2021). Use of automation and the Bank mechanization and the

introduction of MICR which is based on the cheque processing. In relation with the Lloyd

banking industry, they are developing new technologies which is impacting their business in

positive ways such as Big data, artificial intelligence and cloud computing etc. which helps the

banks in storing there customer data and information effectively and resulting in managing all

the task effectively. However, there could be negative effects of digitalisation which is resulting

in reducing performance of banks. As these digital technological technologies can be risky and

this is affecting the performance as well. It should be secure and efficient in managing their data

and informational and resulting in developing true information. Further, these technologies could

be costly to the banks while managing and also it needs professional IT departments in order to

manage it (de la Feria, and Maffini, 2021). So, it is being analysed that digitalisation is impacting

the business in most effective way and also impacting the banking profits as well.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DATA AND METHODS

Data

Sources: Primary and secondary are the two backbone through which data can be

gathered so that research aim and objective can be achieved. Primary sources of data the name

itself says the first hand data which are not used earlier. This type of information is gathered by

the researcher for their report so that they can complete the whole research and can find out the

gap between the past data and the present data. All the information that is covered in this is new

and is related to the present perception and thoughts. Some of the sources through which primary

data can be collected is letters, diaries, interview, filling up of questionnaire, video and many

more. The data is collected by the investigator is reliable information and is gathered according

to the needs and wants of the investigator (Tijhuis and et. al, 2019). On the other hand secondary

source of data is not fresh and type of information that is gathered in this is second hand. This

type of data is used by many examiner before. This type of information is gathered by the

investigator so as to gain detail understanding about the topic that is selected by the researcher.

Books, journal, magazine, articles, online sites and many more are some of the sources of

secondary data. This type of data is not fresh and there is some chance of being failed because it

contain past information that does not belong to the current perception of the respondent. One of

the main advantage to use this source is that data can be gathered in limited time and also the

examiner get the idea to which primary source will be best to collect accurate information for

this. The secondary source of data is generated by someone else and used by the other examiner,

student or many other stakeholder so that they can complete the report on shorter time period

(Chan and et. Al, 2018).

Period: Period refers to the time within which the investigation can be completed. It is

very important for the examiner to identify the time frame work so that exact time can be get in

which report can be completed. Cross-sectional ad longitudinal are two time framework. In cross

sectional time Horizon the data is collected at single time. This is time consuming and cheap

process. Longitudinal time horizon the data is collected multiple time so that if any changes

occurs then can be turn according to this. The time period to collect this is long in comparison

with the cross-sectional time because information is gathered repeatedly with the time (Pineda

and Morales, 2018)

10

Data

Sources: Primary and secondary are the two backbone through which data can be

gathered so that research aim and objective can be achieved. Primary sources of data the name

itself says the first hand data which are not used earlier. This type of information is gathered by

the researcher for their report so that they can complete the whole research and can find out the

gap between the past data and the present data. All the information that is covered in this is new

and is related to the present perception and thoughts. Some of the sources through which primary

data can be collected is letters, diaries, interview, filling up of questionnaire, video and many

more. The data is collected by the investigator is reliable information and is gathered according

to the needs and wants of the investigator (Tijhuis and et. al, 2019). On the other hand secondary

source of data is not fresh and type of information that is gathered in this is second hand. This

type of data is used by many examiner before. This type of information is gathered by the

investigator so as to gain detail understanding about the topic that is selected by the researcher.

Books, journal, magazine, articles, online sites and many more are some of the sources of

secondary data. This type of data is not fresh and there is some chance of being failed because it

contain past information that does not belong to the current perception of the respondent. One of

the main advantage to use this source is that data can be gathered in limited time and also the

examiner get the idea to which primary source will be best to collect accurate information for

this. The secondary source of data is generated by someone else and used by the other examiner,

student or many other stakeholder so that they can complete the report on shorter time period

(Chan and et. Al, 2018).

Period: Period refers to the time within which the investigation can be completed. It is

very important for the examiner to identify the time frame work so that exact time can be get in

which report can be completed. Cross-sectional ad longitudinal are two time framework. In cross

sectional time Horizon the data is collected at single time. This is time consuming and cheap

process. Longitudinal time horizon the data is collected multiple time so that if any changes

occurs then can be turn according to this. The time period to collect this is long in comparison

with the cross-sectional time because information is gathered repeatedly with the time (Pineda

and Morales, 2018)

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variables: From the above research topic to identify the impact of digital disruption on

banking sector and its competition. In this Banking sector and Competition is the dependent

variable on Digital disruption that is Independent variable. The independent and dependent

variable shows the cause and affect relationship between the variables. In which independent is

cause and dependent is the effect. The independent variable is the one who affect the other when

they change or something happen with them. The dependent is one who is affected when the

other variable change. There is an direct relation with them so if independent variant turn or

manipulate then dependent variants has affected by them (Calder and et. al, 2021).

Methods

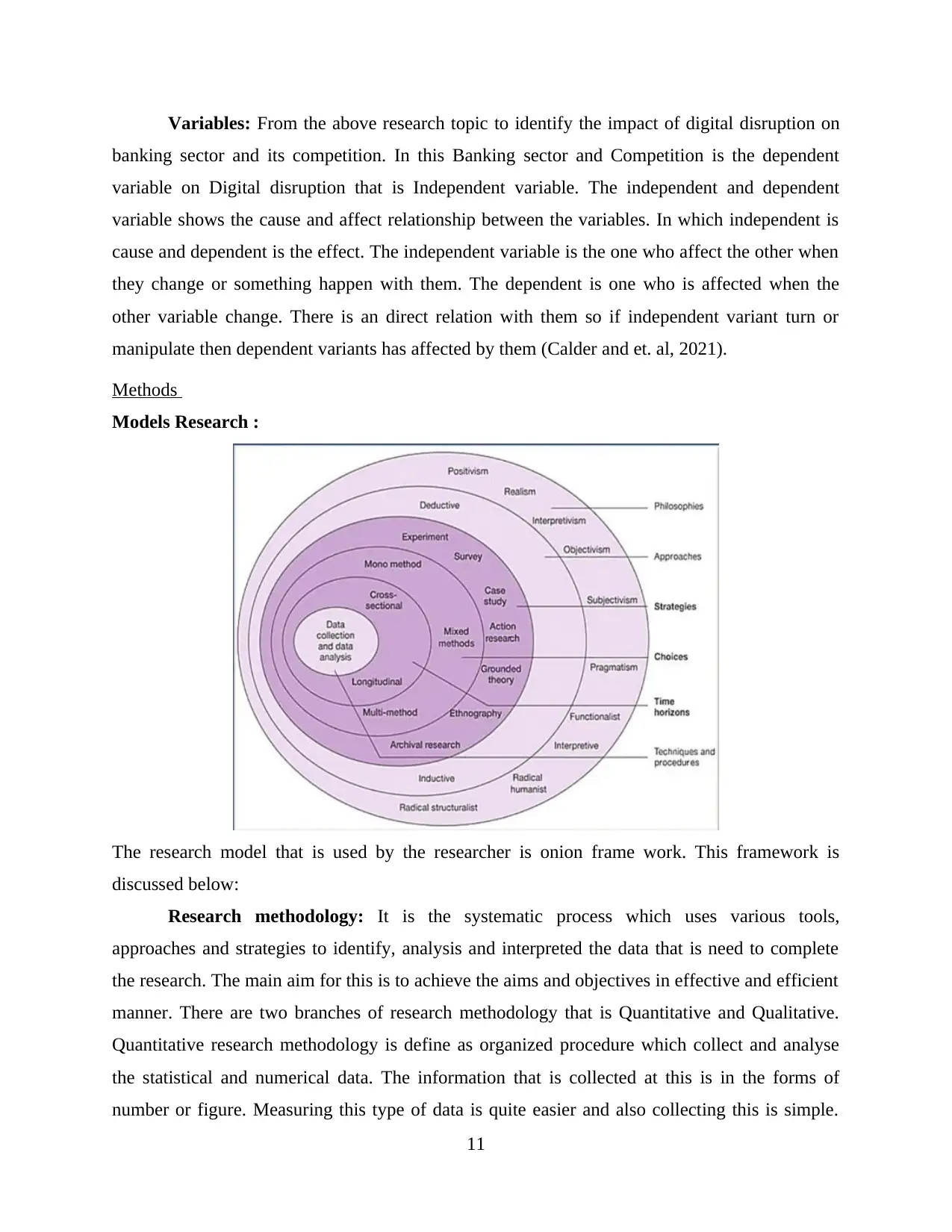

Models Research :

The research model that is used by the researcher is onion frame work. This framework is

discussed below:

Research methodology: It is the systematic process which uses various tools,

approaches and strategies to identify, analysis and interpreted the data that is need to complete

the research. The main aim for this is to achieve the aims and objectives in effective and efficient

manner. There are two branches of research methodology that is Quantitative and Qualitative.

Quantitative research methodology is define as organized procedure which collect and analyse

the statistical and numerical data. The information that is collected at this is in the forms of

number or figure. Measuring this type of data is quite easier and also collecting this is simple.

11

banking sector and its competition. In this Banking sector and Competition is the dependent

variable on Digital disruption that is Independent variable. The independent and dependent

variable shows the cause and affect relationship between the variables. In which independent is

cause and dependent is the effect. The independent variable is the one who affect the other when

they change or something happen with them. The dependent is one who is affected when the

other variable change. There is an direct relation with them so if independent variant turn or

manipulate then dependent variants has affected by them (Calder and et. al, 2021).

Methods

Models Research :

The research model that is used by the researcher is onion frame work. This framework is

discussed below:

Research methodology: It is the systematic process which uses various tools,

approaches and strategies to identify, analysis and interpreted the data that is need to complete

the research. The main aim for this is to achieve the aims and objectives in effective and efficient

manner. There are two branches of research methodology that is Quantitative and Qualitative.

Quantitative research methodology is define as organized procedure which collect and analyse

the statistical and numerical data. The information that is collected at this is in the forms of

number or figure. Measuring this type of data is quite easier and also collecting this is simple.

11

Qualitative methodology is used when the examiner do not want to gather the information in the

form of numbers rather the examine try to collect the emotions and felling while collecting this

data. This type of information is collected so that detail understanding can be get from the topic

chosen. An in depth detail is provide in this type of research methodology. Here an open

communication is made between the researcher and the respondent.

In this report the examiner has chosen qualitative research methodology because they want to get

in depth information about the digital disruption on banking sector (Snyder, 2019).

Research philosophy: In this part of onion framework a set of principle are belief are

being mentioned through which the research is to be conducted. The researcher study three

philosophy that is Ontology, Epistemology and Apology. Ontology philosophy is used when the

researcher want to know the authenticity of the data, Epistemology is used when valid

information is to be obtained and apology is used when the perception need to be gained. In this

report the examiner is used the Epistemology Philosophy. Positivism and interpretivism are two

type of Epistemology. In this interpretivism is used by the researcher because they want to

observe the perception and the reality of the information (Kumar, 2018).

Research approach: The next layer of the onion framework is research approach in

which accurate approach is chosen to analysis the data. Deductive and inductive are the

approaches to analyse the information. Deductive approach is used when the information is in

numerics and inductive is used when they are not in the form of numbers. In Deductive the test is

made on Existing hypothesis and in deductive is used when new theory is need to be developed.

In this report the investigator will choose inductive approach because the information is bin the

form of qualitative and a new hypothesis will be developed by gaining the data (Novikov and

Novikov, 2019).

Research strategy: This is the third layer of the model which provide the strategy that

can be used to obtained the data from the respondent. There are so many strategy such as Survey,

Action research, experimental, case study and literature review. In this research topic the

researcher will choose case study to obtained the data from the respondent.

Research Choice: The next layer in the research onion is research choice. They suggest

three choices that is Mono method, Mixed method, Multi method. Mono method is chosen when

one of the type s selected that is quantitative and qualitative. Mixed is used when both the type is

selected to gain information and Multi method is selected when the data is of two more type of

12

form of numbers rather the examine try to collect the emotions and felling while collecting this

data. This type of information is collected so that detail understanding can be get from the topic

chosen. An in depth detail is provide in this type of research methodology. Here an open

communication is made between the researcher and the respondent.

In this report the examiner has chosen qualitative research methodology because they want to get

in depth information about the digital disruption on banking sector (Snyder, 2019).

Research philosophy: In this part of onion framework a set of principle are belief are

being mentioned through which the research is to be conducted. The researcher study three

philosophy that is Ontology, Epistemology and Apology. Ontology philosophy is used when the

researcher want to know the authenticity of the data, Epistemology is used when valid

information is to be obtained and apology is used when the perception need to be gained. In this

report the examiner is used the Epistemology Philosophy. Positivism and interpretivism are two

type of Epistemology. In this interpretivism is used by the researcher because they want to

observe the perception and the reality of the information (Kumar, 2018).

Research approach: The next layer of the onion framework is research approach in

which accurate approach is chosen to analysis the data. Deductive and inductive are the

approaches to analyse the information. Deductive approach is used when the information is in

numerics and inductive is used when they are not in the form of numbers. In Deductive the test is

made on Existing hypothesis and in deductive is used when new theory is need to be developed.

In this report the investigator will choose inductive approach because the information is bin the

form of qualitative and a new hypothesis will be developed by gaining the data (Novikov and

Novikov, 2019).

Research strategy: This is the third layer of the model which provide the strategy that

can be used to obtained the data from the respondent. There are so many strategy such as Survey,

Action research, experimental, case study and literature review. In this research topic the

researcher will choose case study to obtained the data from the respondent.

Research Choice: The next layer in the research onion is research choice. They suggest

three choices that is Mono method, Mixed method, Multi method. Mono method is chosen when

one of the type s selected that is quantitative and qualitative. Mixed is used when both the type is

selected to gain information and Multi method is selected when the data is of two more type of

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.