An Analysis of Digital Payment Impact on Commercial Bank Performance

VerifiedAdded on 2023/01/07

|28

|6563

|26

Report

AI Summary

This report delves into the effects of digital payments on commercial bank performance, examining the development of digital payment systems and their relationship with third-party payment providers. It explores the positive and negative influences, including cooperation, competition, and coopetition, within the financial sector. The report reviews prior studies, identifies research gaps, and outlines theoretical foundations such as financial intermediary and technology spillover theories. It analyzes the impact of digital payments on bank efficiency, profitability, and strategic decision-making, providing a comprehensive overview of the evolving financial landscape and its implications for commercial banks. The study also highlights the innovations in the digital payment landscape and its impact on the banking sector.

Acknowledgments

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

Table of Contents

1 Introduction..................................................................................................5

1.1 Background and Research Motivations..............................................5

1.2 Research Questions............................................................................5

1.3 Research aim and Objectives.............................................................5

1.4 Outline of the Research......................................................................5

2 Literature Review..............................................................................................5

2.1 Introduction............................................................................................5

2.2 Digital Payment and Bank’s performance......................................................5

2.2.1 The Development of Digital Payment..................................................5

2.2.2 The Relationship Between Third-Party Payment and Commercial Bank form

Positive and Negative Influence Mechanism......................................................6

2.3 Prior study and research gap.......................................................................7

2.4 Theoretical foundation............................................................................10

2.4.2 Financial Intermediary Theory-Financial disintermediation theory............10

2.4.3 Technology spillover theory............................................................11

2.5 Theoretical Framework...........................................................................11

2.6 Contributions........................................................................................15

3 References.....................................................................................................20

1 Introduction..................................................................................................5

1.1 Background and Research Motivations..............................................5

1.2 Research Questions............................................................................5

1.3 Research aim and Objectives.............................................................5

1.4 Outline of the Research......................................................................5

2 Literature Review..............................................................................................5

2.1 Introduction............................................................................................5

2.2 Digital Payment and Bank’s performance......................................................5

2.2.1 The Development of Digital Payment..................................................5

2.2.2 The Relationship Between Third-Party Payment and Commercial Bank form

Positive and Negative Influence Mechanism......................................................6

2.3 Prior study and research gap.......................................................................7

2.4 Theoretical foundation............................................................................10

2.4.2 Financial Intermediary Theory-Financial disintermediation theory............10

2.4.3 Technology spillover theory............................................................11

2.5 Theoretical Framework...........................................................................11

2.6 Contributions........................................................................................15

3 References.....................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 Introduction

1.1 Background and Research Motivations

1.2 Research Questions

1.3 Research aim and Objectives

1.4 Outline of the Research

2 Literature Review

2.1 Introduction

At first, this chapter takes a look at the current state of digital payment and

this leads naturally to third-party online payment. Then, the project introduces

the relationship between the third-party payment services market and

commercial bank from a literature review perspective. Next, combined with

the prior studies, the author makes an evaluation and comparative analysis

and finally gains some inspiration from that relevant literature. Not only that,

but the author also summarizes the research gap and makes some

assumptions based on previous study and research questions. Finally, the

study gives the innovation points and contributions to this paper.

2.2 Digital Payment and Bank’s performance

2.2.1 The Development of Digital Payment

Digital payment could be defined as the payment which is made with the help

of digital modes such as mobile applications. In order to use it, it is very

important for both the parties involved in the transaction should have digital

modes. These parties are payer and receiver. The development of internet

finance is different from that of Fintech finance outside various countries.

Represented by the developed countries, the United States have sufficient

traditional financial supplies, and the needs of public could be satisfied offline

(Patil, Rana and Dwivedi, 2018). However, most of the countries around the

world are still in the early stages of financial development while the case of

insufficient financial infrastructure and financial markets. It obviously exists a

1.1 Background and Research Motivations

1.2 Research Questions

1.3 Research aim and Objectives

1.4 Outline of the Research

2 Literature Review

2.1 Introduction

At first, this chapter takes a look at the current state of digital payment and

this leads naturally to third-party online payment. Then, the project introduces

the relationship between the third-party payment services market and

commercial bank from a literature review perspective. Next, combined with

the prior studies, the author makes an evaluation and comparative analysis

and finally gains some inspiration from that relevant literature. Not only that,

but the author also summarizes the research gap and makes some

assumptions based on previous study and research questions. Finally, the

study gives the innovation points and contributions to this paper.

2.2 Digital Payment and Bank’s performance

2.2.1 The Development of Digital Payment

Digital payment could be defined as the payment which is made with the help

of digital modes such as mobile applications. In order to use it, it is very

important for both the parties involved in the transaction should have digital

modes. These parties are payer and receiver. The development of internet

finance is different from that of Fintech finance outside various countries.

Represented by the developed countries, the United States have sufficient

traditional financial supplies, and the needs of public could be satisfied offline

(Patil, Rana and Dwivedi, 2018). However, most of the countries around the

world are still in the early stages of financial development while the case of

insufficient financial infrastructure and financial markets. It obviously exists a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

big gap with developed countries. This gap is gradually being filled due to the

emergence of internet finance. Internet finance provides strong technical

support for electronic payment system.

Tandulwadikar (2015) proposes that digital payment as an instant convenient

and convenient way includes desktop payment, mobile payment, and digital

wallets which means no hard cash (current notes). The digital payment as an

electronic payment has become a necessary daily way which means payer

and payee both use digital modes to send and receive money(O’Leary et al.,

2003). There is a large numbers of well-known third-party payment companies

cover the whole world such as the United Kingdom Worldpay (1993), the

United States PayPal (1998), China Alipay (2004), Germany Giropay (2006),

Apple pay (2014) and Google pay (2018). As Manning (2015) investigates

that the business of banks may face challenges due to the expansion of third-

party digital payment companies because third-party payment providers such

as PayPal, and Google in the United States are establishing direct

relationships with customers over convenience. In this way, they attract some

young customers in a short time to seize the opportunity of the mobile market

and engage in the mobile payment gateway. Driven by globalization, the

demand of cross-border good are increasing. People in their home country

pay more attention to the online shopping rather than offline shopping which

means there are high potential for the third-party mobile payment

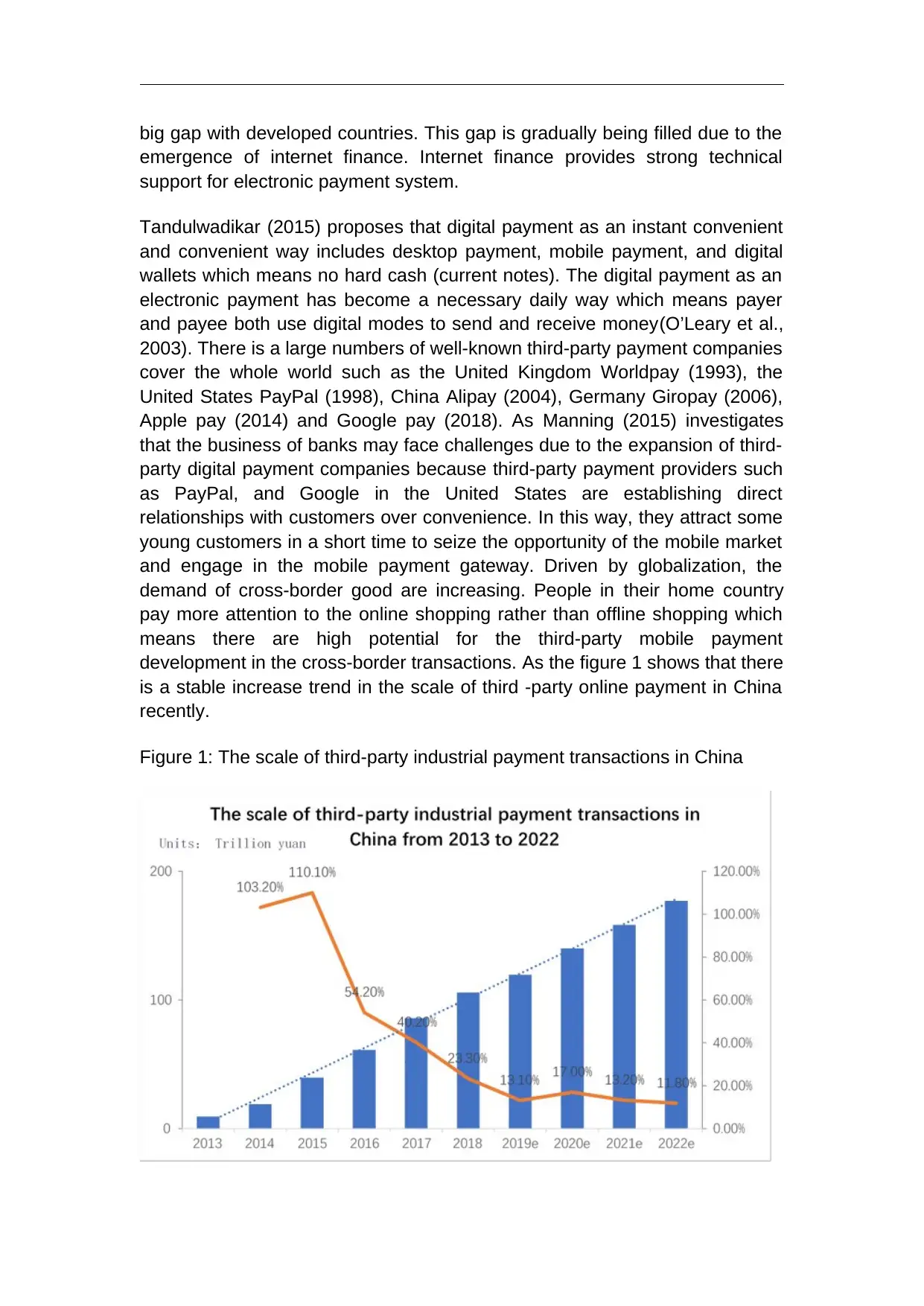

development in the cross-border transactions. As the figure 1 shows that there

is a stable increase trend in the scale of third -party online payment in China

recently.

Figure 1: The scale of third-party industrial payment transactions in China

emergence of internet finance. Internet finance provides strong technical

support for electronic payment system.

Tandulwadikar (2015) proposes that digital payment as an instant convenient

and convenient way includes desktop payment, mobile payment, and digital

wallets which means no hard cash (current notes). The digital payment as an

electronic payment has become a necessary daily way which means payer

and payee both use digital modes to send and receive money(O’Leary et al.,

2003). There is a large numbers of well-known third-party payment companies

cover the whole world such as the United Kingdom Worldpay (1993), the

United States PayPal (1998), China Alipay (2004), Germany Giropay (2006),

Apple pay (2014) and Google pay (2018). As Manning (2015) investigates

that the business of banks may face challenges due to the expansion of third-

party digital payment companies because third-party payment providers such

as PayPal, and Google in the United States are establishing direct

relationships with customers over convenience. In this way, they attract some

young customers in a short time to seize the opportunity of the mobile market

and engage in the mobile payment gateway. Driven by globalization, the

demand of cross-border good are increasing. People in their home country

pay more attention to the online shopping rather than offline shopping which

means there are high potential for the third-party mobile payment

development in the cross-border transactions. As the figure 1 shows that there

is a stable increase trend in the scale of third -party online payment in China

recently.

Figure 1: The scale of third-party industrial payment transactions in China

The above chart is focused with analysis of scale of the third-party

payment transaction in China from year 2013 to 2022. According to the chart

the payments in year 2013 were very less but with passing of time the

payments were increased. The estimated data for year 2020 was more than

80% and it has been forecasted that till 2022 it will be increased more than

100%. It shows that with the time the third-party payment scale is developing

in China with the time. Additionally, the next topic which will be covered for the

completion of the dissertation will relate to banks from positive and negative

influence mechanism which will help to enhance the knownedge about

relationship between commercial and third party payment.

2.2.2 The Relationship Between Third-Party Payment and Commercial

Bank form Positive and Negative Influence Mechanism

The rapid development of Internet payment, especially the explosive

development of third-party payment and the rise of mobile payment, it has

become an issue of great concern in many countries because it involves part

of the business of commercial banks (DeYoung et al., 2007). It means third-

party payment companies has entered the bank activities and it accounted for

a large operational productivity in the payment field. It can be from the picture

that there is more in line when the third-party payment companies entered.

This dissertation research on the relationship between third-party payment

and commercial banks’ performance. Therefore, it is necessary to figure out

the relationship between the third-party and commercial bank. It mainly

focuses on cooperation, competition and cooperative competition (Frost and

et.al., 2018). All of them lay the foundation for the following research

(Hryckiewicz, Kryg and Tsomocos, 2020).

Cooperation

The emergence of third-party payment is an extension and supplement to the

payment service function of commercial banks, showing a cooperative

relationship with banks (Bank for International Settlements, 2003).

Commercial banks provide technical interfaces and settlement services for

third-party payments to share the profit with third-party payment companies. It

involves cooperating in payment gateway, fast payment, withholding payment

and POS trade system (Kokkola, 2010).

According to the conclusions from empirical analysis from (Zhou et al., 2008),

there is no doubt that cooperation would be increasingly in-depth for

commercial banks in China. The positive impact of third-party payment on the

operating efficiency of commercial banks mainly highlights in increasing the

payment transaction in China from year 2013 to 2022. According to the chart

the payments in year 2013 were very less but with passing of time the

payments were increased. The estimated data for year 2020 was more than

80% and it has been forecasted that till 2022 it will be increased more than

100%. It shows that with the time the third-party payment scale is developing

in China with the time. Additionally, the next topic which will be covered for the

completion of the dissertation will relate to banks from positive and negative

influence mechanism which will help to enhance the knownedge about

relationship between commercial and third party payment.

2.2.2 The Relationship Between Third-Party Payment and Commercial

Bank form Positive and Negative Influence Mechanism

The rapid development of Internet payment, especially the explosive

development of third-party payment and the rise of mobile payment, it has

become an issue of great concern in many countries because it involves part

of the business of commercial banks (DeYoung et al., 2007). It means third-

party payment companies has entered the bank activities and it accounted for

a large operational productivity in the payment field. It can be from the picture

that there is more in line when the third-party payment companies entered.

This dissertation research on the relationship between third-party payment

and commercial banks’ performance. Therefore, it is necessary to figure out

the relationship between the third-party and commercial bank. It mainly

focuses on cooperation, competition and cooperative competition (Frost and

et.al., 2018). All of them lay the foundation for the following research

(Hryckiewicz, Kryg and Tsomocos, 2020).

Cooperation

The emergence of third-party payment is an extension and supplement to the

payment service function of commercial banks, showing a cooperative

relationship with banks (Bank for International Settlements, 2003).

Commercial banks provide technical interfaces and settlement services for

third-party payments to share the profit with third-party payment companies. It

involves cooperating in payment gateway, fast payment, withholding payment

and POS trade system (Kokkola, 2010).

According to the conclusions from empirical analysis from (Zhou et al., 2008),

there is no doubt that cooperation would be increasingly in-depth for

commercial banks in China. The positive impact of third-party payment on the

operating efficiency of commercial banks mainly highlights in increasing the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

banking website users and reduce operating costs.

Competition

The third-party payment institutions and commercial banks are both exists the

business overlap and conflicting views. Therefore, it would inevitably lead to

fierce competition. When users use a third-party payment platform for online

transactions, they firsthand over funds to the third-party payment platform.

The third-party payment platform waits until the buyer confirms the receipt of

the goods before lending to the seller. This process actually constitutes a

settlement business. From the perspective of the development of banks, the

era of relying on deposit-loan spreads for profit is about to pass soon, and

non-asset business will be an important source of profits for banks in the

future. While, third-party institutions directly provide the same services as

banks at lower rates, which has obviously grabbed intermediate businesses of

banks(Hu, 2016). The negative impact of third-party payment on the operating

efficiency of commercial banks mainly focuses on increasing business

competition.

Coopetition

Through theoretical mathematical model, there are an evolutionary stable

strategy (ESS) which shows that cooperation and competition is bound to be

increasingly in-depth and expansive for commercial banks as well as e-

commerce financial institutions in China (Zhao et al., 2015). Furthermore, the

complementarity of participants’ core competitiveness is explored as the root

of cooperation. There is no doubt that e-commerce financial institutions and

commercial banks have their unique advantage and core competitiveness.

For instance, e-commerce financial institutions are low-cost e-commerce

customer credit evaluation capability on big data. On the other hand,

commercial banks are abundant in capital strength.

The positive and negative effects of third-party payment on commercial banks

exist at the same time. In reality, banks perform differently when facing the

impact of third-party payment due to various reasons. Therefore, this

dissertation attempts to conduct quantitative research by establishing an

empirical model in the following pages.

2.3 Prior study and research gap

As indicated in a number of studies (Schierz et al., 2010; Bezhovski, 2016;

Teoh et al., 2013; Schierz et al., 2010) literature on electronic payment

between 2010 and 2019 has been dominated by two main topics: technology

Competition

The third-party payment institutions and commercial banks are both exists the

business overlap and conflicting views. Therefore, it would inevitably lead to

fierce competition. When users use a third-party payment platform for online

transactions, they firsthand over funds to the third-party payment platform.

The third-party payment platform waits until the buyer confirms the receipt of

the goods before lending to the seller. This process actually constitutes a

settlement business. From the perspective of the development of banks, the

era of relying on deposit-loan spreads for profit is about to pass soon, and

non-asset business will be an important source of profits for banks in the

future. While, third-party institutions directly provide the same services as

banks at lower rates, which has obviously grabbed intermediate businesses of

banks(Hu, 2016). The negative impact of third-party payment on the operating

efficiency of commercial banks mainly focuses on increasing business

competition.

Coopetition

Through theoretical mathematical model, there are an evolutionary stable

strategy (ESS) which shows that cooperation and competition is bound to be

increasingly in-depth and expansive for commercial banks as well as e-

commerce financial institutions in China (Zhao et al., 2015). Furthermore, the

complementarity of participants’ core competitiveness is explored as the root

of cooperation. There is no doubt that e-commerce financial institutions and

commercial banks have their unique advantage and core competitiveness.

For instance, e-commerce financial institutions are low-cost e-commerce

customer credit evaluation capability on big data. On the other hand,

commercial banks are abundant in capital strength.

The positive and negative effects of third-party payment on commercial banks

exist at the same time. In reality, banks perform differently when facing the

impact of third-party payment due to various reasons. Therefore, this

dissertation attempts to conduct quantitative research by establishing an

empirical model in the following pages.

2.3 Prior study and research gap

As indicated in a number of studies (Schierz et al., 2010; Bezhovski, 2016;

Teoh et al., 2013; Schierz et al., 2010) literature on electronic payment

between 2010 and 2019 has been dominated by two main topics: technology

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

innovation and consumer satisfaction. Main aim of the dissertation is to

explore the relationship between the third-party online payment and

commercial bank’s performance r this purpose different theories from various

areas, such as economics, marketing or business ecosystems are used (Xia

and Chunsom, 2018; Liao, 2018). Surveys such as that conducted by Dinh et

al. (2015) have shown that Internet banking could increase the profitability of

commercial banks based on Vietnam. The random effect model and fixed

effect model are used to estimate the relationships between them. One of the

limitations with this explanation is that sample size may not be sufficient.

Secondly, Lao and Jiang (2009) combined with PEST model to describe risk

analysis of third-party online payment and found that there are many

advantages and its own shortcomings at the same time. Take the Alipay as

the example, it would promote the development of ecommerce and play

different roles with banks, consumer and other payment companies because

they are dispensable. In the meanwhile, they are also defined the B2C and

C2C as the mainly popular areas in third party payment. While, commercial

banks have not placed online payments part of their foremost business

portfolio and source of income as well. This allows for the third-party online

payment to help with cash flow and also fills the vacancy instantly. However,

this method of analysis has a number of limitations such as the Alipay case

analysis is not universal to the whole third-party payment’s companies.

Furthermore, Zhao and Sun (2012) argue that the main risk is financial risk

such as cash, credit, operational risk and so on which is not mentioned by Lao

and Jiang.

Thirdly, Gulati and Kumar (2017) first use developed two-stage network (DEA)

model to obtain overall bank operating efficiency. Then through applying a

bootstrapped truncated regression algorithm to explore the determinants of

operating efficiency. The author found that the main reason for the overall

inefficiency of the Indian banking industry is low operating efficiency. The

reasons for efficiency differences could be explained by bank scale, liquidity

position, and targeted loans cost, while the variations in profitability and

income. The research results showed that the banking industry could achieve

higher bank efficiency by improving the bank’s resource utilization and income

generation capabilities.

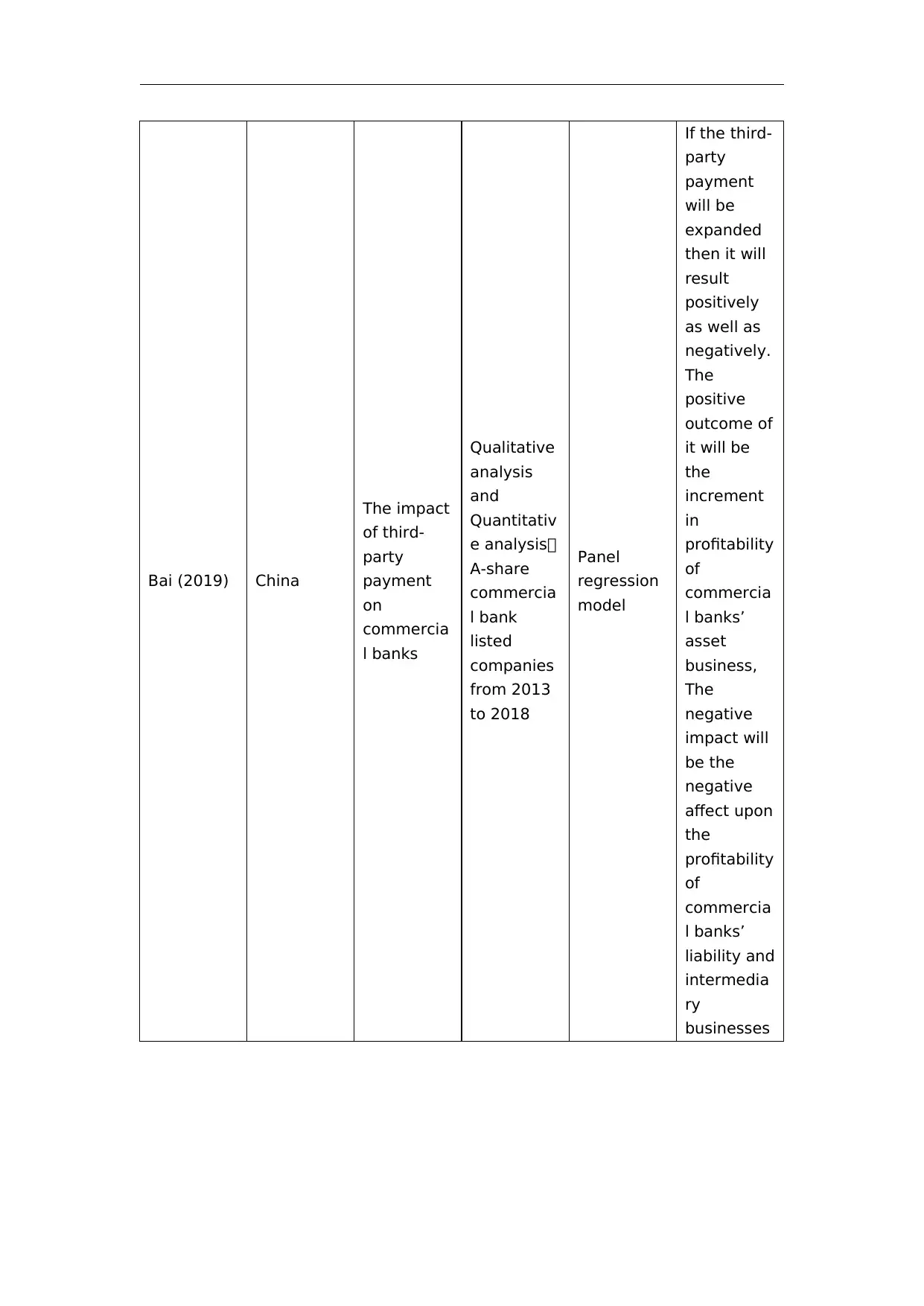

Finally, the emerging method of transaction through third-party platform bring

great attention to its impact on traditional bank sector. Bai (2019) compares

the comparative competitive advantages of commercial Banks and third-party

payment platforms, and further explored the possible influences and ways of

third-party payment on banks' traditional deposit, loan and remittance

business, consulting business, deposit structure and loan market. Combined

with data and cases, it uses panel regression model to explore the impact of

explore the relationship between the third-party online payment and

commercial bank’s performance r this purpose different theories from various

areas, such as economics, marketing or business ecosystems are used (Xia

and Chunsom, 2018; Liao, 2018). Surveys such as that conducted by Dinh et

al. (2015) have shown that Internet banking could increase the profitability of

commercial banks based on Vietnam. The random effect model and fixed

effect model are used to estimate the relationships between them. One of the

limitations with this explanation is that sample size may not be sufficient.

Secondly, Lao and Jiang (2009) combined with PEST model to describe risk

analysis of third-party online payment and found that there are many

advantages and its own shortcomings at the same time. Take the Alipay as

the example, it would promote the development of ecommerce and play

different roles with banks, consumer and other payment companies because

they are dispensable. In the meanwhile, they are also defined the B2C and

C2C as the mainly popular areas in third party payment. While, commercial

banks have not placed online payments part of their foremost business

portfolio and source of income as well. This allows for the third-party online

payment to help with cash flow and also fills the vacancy instantly. However,

this method of analysis has a number of limitations such as the Alipay case

analysis is not universal to the whole third-party payment’s companies.

Furthermore, Zhao and Sun (2012) argue that the main risk is financial risk

such as cash, credit, operational risk and so on which is not mentioned by Lao

and Jiang.

Thirdly, Gulati and Kumar (2017) first use developed two-stage network (DEA)

model to obtain overall bank operating efficiency. Then through applying a

bootstrapped truncated regression algorithm to explore the determinants of

operating efficiency. The author found that the main reason for the overall

inefficiency of the Indian banking industry is low operating efficiency. The

reasons for efficiency differences could be explained by bank scale, liquidity

position, and targeted loans cost, while the variations in profitability and

income. The research results showed that the banking industry could achieve

higher bank efficiency by improving the bank’s resource utilization and income

generation capabilities.

Finally, the emerging method of transaction through third-party platform bring

great attention to its impact on traditional bank sector. Bai (2019) compares

the comparative competitive advantages of commercial Banks and third-party

payment platforms, and further explored the possible influences and ways of

third-party payment on banks' traditional deposit, loan and remittance

business, consulting business, deposit structure and loan market. Combined

with data and cases, it uses panel regression model to explore the impact of

third-party payment on commercial banks. The result shows that the

expansion of third-party payment will have a positive impact on the profitability

of commercial banks’ asset business, and negatively affect the profitability of

commercial banks’ liability and intermediary businesses. It means third-party

payment would promote the innovation and transformation of commercial

banks. Finally, there are some corresponding policy recommendations for the

development of commercial banks in the new situation. The explained

variables are the three business indicators of commercial banks, and the

explanatory variables are the third-party payment scale indicators This

method and third-party payment variables are also used in this dissertation.

Through combing and reviewing related literature, it can be found that there

are plenty of research results focusing on the relationship between the

Internet finance field and the operating efficiency of commercial banks. There

are quite a few scholars focuses the specific field about the relationship

between third-party payment and commercial bank performance.

Furthermore, regarding the degree of impact on the operating efficiency of

commercial banks, most of the research focuses on profitability, and there are

quite a few studies on other operating principles of banks. At the same time,

there are some scholars studying the influence of commercial banks on

Internet finance which are basically qualitative research around theoretical

analysis, or on Internet finance as a whole to construct an Internet finance

index. Most research results insist the views is that in the initial growth stage

of Internet finance, it has fierce competition and squeeze on commercial

banks, which is mainly a negative restraint. However, commercial banks have

also accepted the spirit of openness and collaboration on the Internet

recently, which are more functional complementarity and cooperation to

achieve mutual benefit and win-win results. The development of third-party

payment, the society pays a larger amount of attention to it. Therefore, it is

necessary to conduct a special research from the perspective of third-party

payment from quantitative analysis to find the relationship between them.

Table1. Article included in systematic literature review

Authors Country Context Method Study

Measures Results

expansion of third-party payment will have a positive impact on the profitability

of commercial banks’ asset business, and negatively affect the profitability of

commercial banks’ liability and intermediary businesses. It means third-party

payment would promote the innovation and transformation of commercial

banks. Finally, there are some corresponding policy recommendations for the

development of commercial banks in the new situation. The explained

variables are the three business indicators of commercial banks, and the

explanatory variables are the third-party payment scale indicators This

method and third-party payment variables are also used in this dissertation.

Through combing and reviewing related literature, it can be found that there

are plenty of research results focusing on the relationship between the

Internet finance field and the operating efficiency of commercial banks. There

are quite a few scholars focuses the specific field about the relationship

between third-party payment and commercial bank performance.

Furthermore, regarding the degree of impact on the operating efficiency of

commercial banks, most of the research focuses on profitability, and there are

quite a few studies on other operating principles of banks. At the same time,

there are some scholars studying the influence of commercial banks on

Internet finance which are basically qualitative research around theoretical

analysis, or on Internet finance as a whole to construct an Internet finance

index. Most research results insist the views is that in the initial growth stage

of Internet finance, it has fierce competition and squeeze on commercial

banks, which is mainly a negative restraint. However, commercial banks have

also accepted the spirit of openness and collaboration on the Internet

recently, which are more functional complementarity and cooperation to

achieve mutual benefit and win-win results. The development of third-party

payment, the society pays a larger amount of attention to it. Therefore, it is

necessary to conduct a special research from the perspective of third-party

payment from quantitative analysis to find the relationship between them.

Table1. Article included in systematic literature review

Authors Country Context Method Study

Measures Results

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

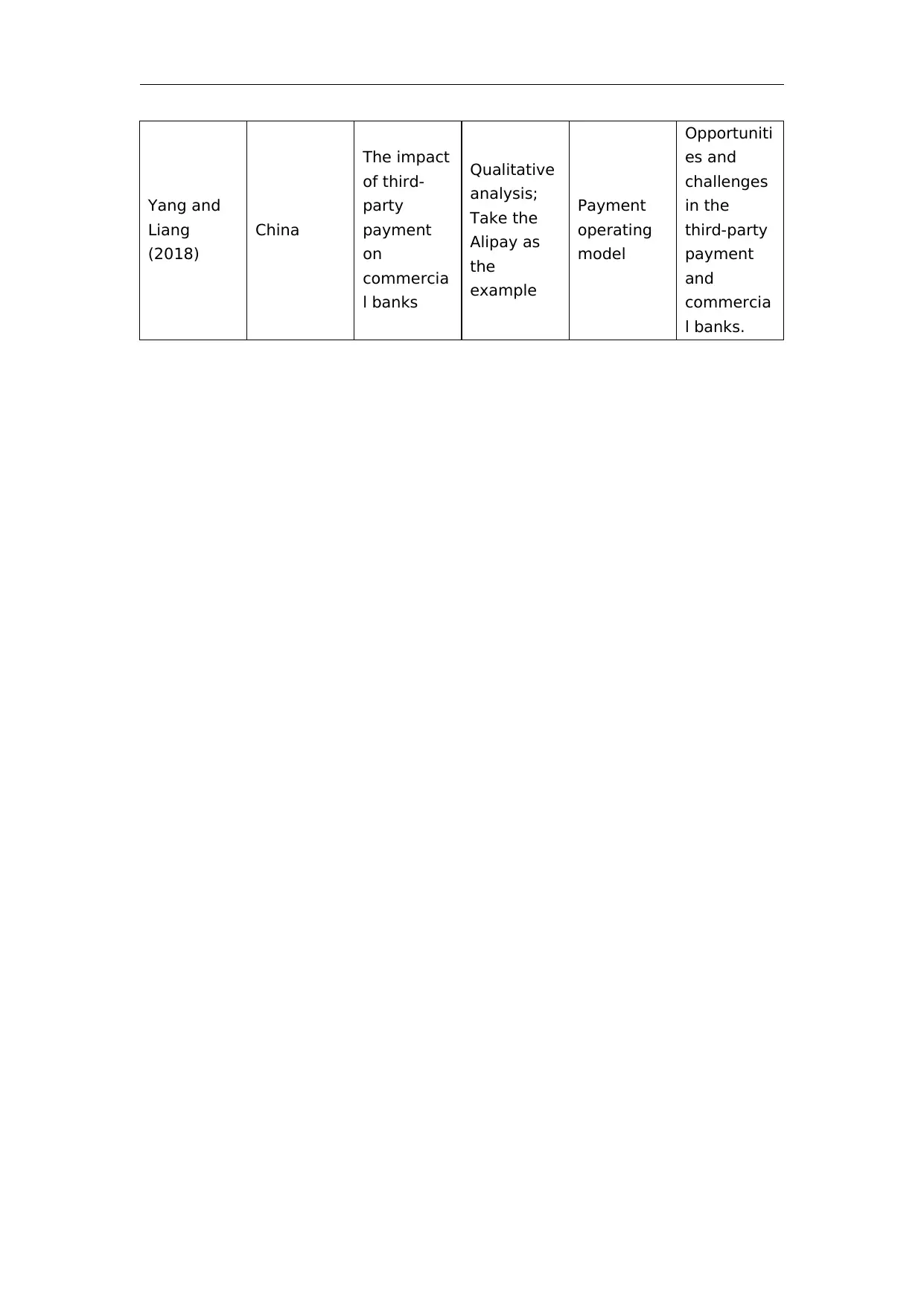

Yang and

Liang

(2018)

China

The impact

of third-

party

payment

on

commercia

l banks

Qualitative

analysis;

Take the

Alipay as

the

example

Payment

operating

model

Opportuniti

es and

challenges

in the

third-party

payment

and

commercia

l banks.

Liang

(2018)

China

The impact

of third-

party

payment

on

commercia

l banks

Qualitative

analysis;

Take the

Alipay as

the

example

Payment

operating

model

Opportuniti

es and

challenges

in the

third-party

payment

and

commercia

l banks.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bai (2019) China

The impact

of third-

party

payment

on

commercia

l banks

Qualitative

analysis

and

Quantitativ

e analysis;

A-share

commercia

l bank

listed

companies

from 2013

to 2018

Panel

regression

model

If the third-

party

payment

will be

expanded

then it will

result

positively

as well as

negatively.

The

positive

outcome of

it will be

the

increment

in

profitability

of

commercia

l banks’

asset

business,

The

negative

impact will

be the

negative

affect upon

the

profitability

of

commercia

l banks’

liability and

intermedia

ry

businesses

The impact

of third-

party

payment

on

commercia

l banks

Qualitative

analysis

and

Quantitativ

e analysis;

A-share

commercia

l bank

listed

companies

from 2013

to 2018

Panel

regression

model

If the third-

party

payment

will be

expanded

then it will

result

positively

as well as

negatively.

The

positive

outcome of

it will be

the

increment

in

profitability

of

commercia

l banks’

asset

business,

The

negative

impact will

be the

negative

affect upon

the

profitability

of

commercia

l banks’

liability and

intermedia

ry

businesses

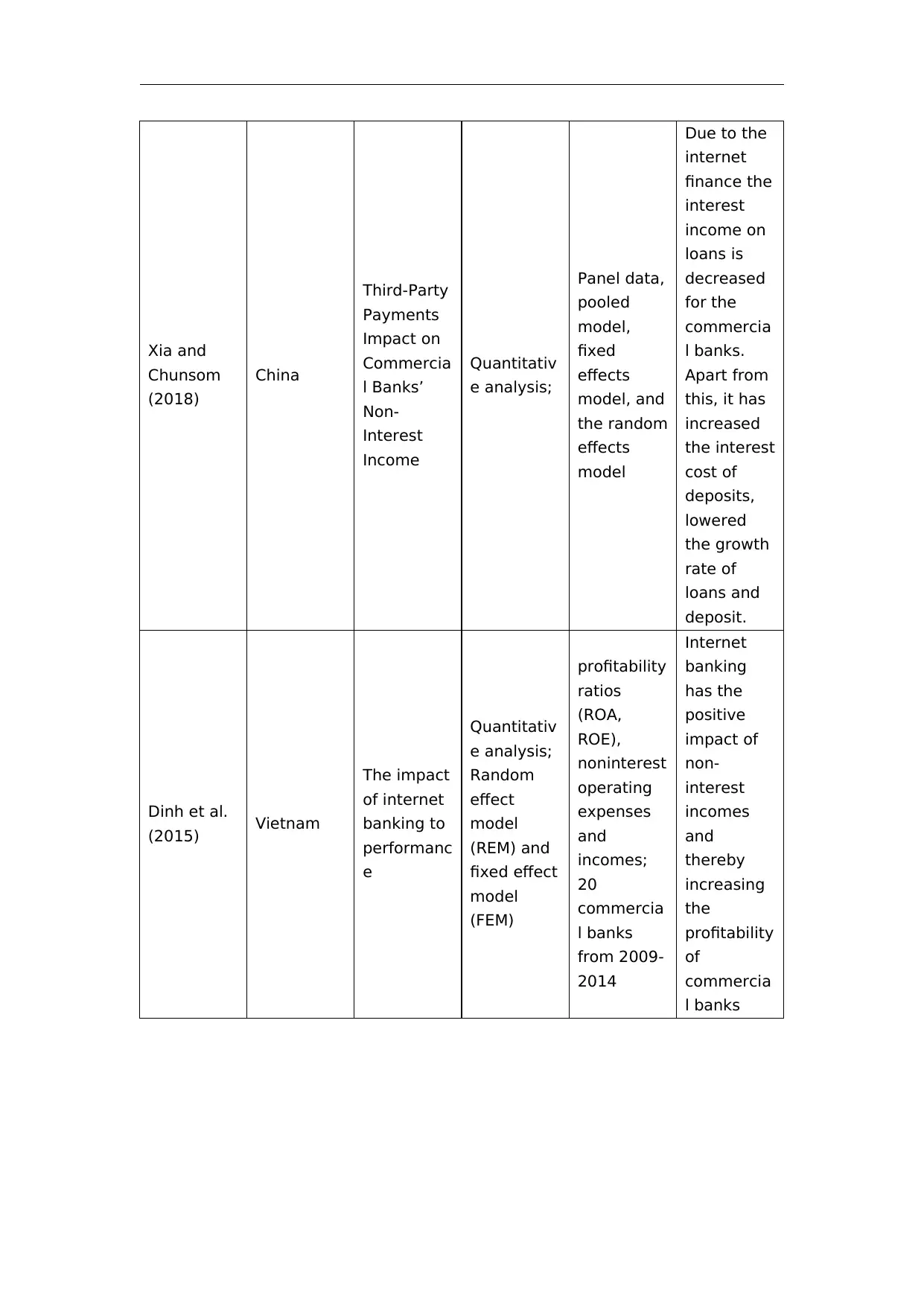

Xia and

Chunsom

(2018)

China

Third-Party

Payments

Impact on

Commercia

l Banks’

Non-

Interest

Income

Quantitativ

e analysis;

Panel data,

pooled

model,

fixed

effects

model, and

the random

effects

model

Due to the

internet

finance the

interest

income on

loans is

decreased

for the

commercia

l banks.

Apart from

this, it has

increased

the interest

cost of

deposits,

lowered

the growth

rate of

loans and

deposit.

Dinh et al.

(2015) Vietnam

The impact

of internet

banking to

performanc

e

Quantitativ

e analysis;

Random

effect

model

(REM) and

fixed effect

model

(FEM)

profitability

ratios

(ROA,

ROE),

noninterest

operating

expenses

and

incomes;

20

commercia

l banks

from 2009-

2014

Internet

banking

has the

positive

impact of

non-

interest

incomes

and

thereby

increasing

the

profitability

of

commercia

l banks

Chunsom

(2018)

China

Third-Party

Payments

Impact on

Commercia

l Banks’

Non-

Interest

Income

Quantitativ

e analysis;

Panel data,

pooled

model,

fixed

effects

model, and

the random

effects

model

Due to the

internet

finance the

interest

income on

loans is

decreased

for the

commercia

l banks.

Apart from

this, it has

increased

the interest

cost of

deposits,

lowered

the growth

rate of

loans and

deposit.

Dinh et al.

(2015) Vietnam

The impact

of internet

banking to

performanc

e

Quantitativ

e analysis;

Random

effect

model

(REM) and

fixed effect

model

(FEM)

profitability

ratios

(ROA,

ROE),

noninterest

operating

expenses

and

incomes;

20

commercia

l banks

from 2009-

2014

Internet

banking

has the

positive

impact of

non-

interest

incomes

and

thereby

increasing

the

profitability

of

commercia

l banks

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.