Cost Analysis and Recommendations for Digital Solutions Inc.

VerifiedAdded on 2023/06/03

|8

|1190

|127

Case Study

AI Summary

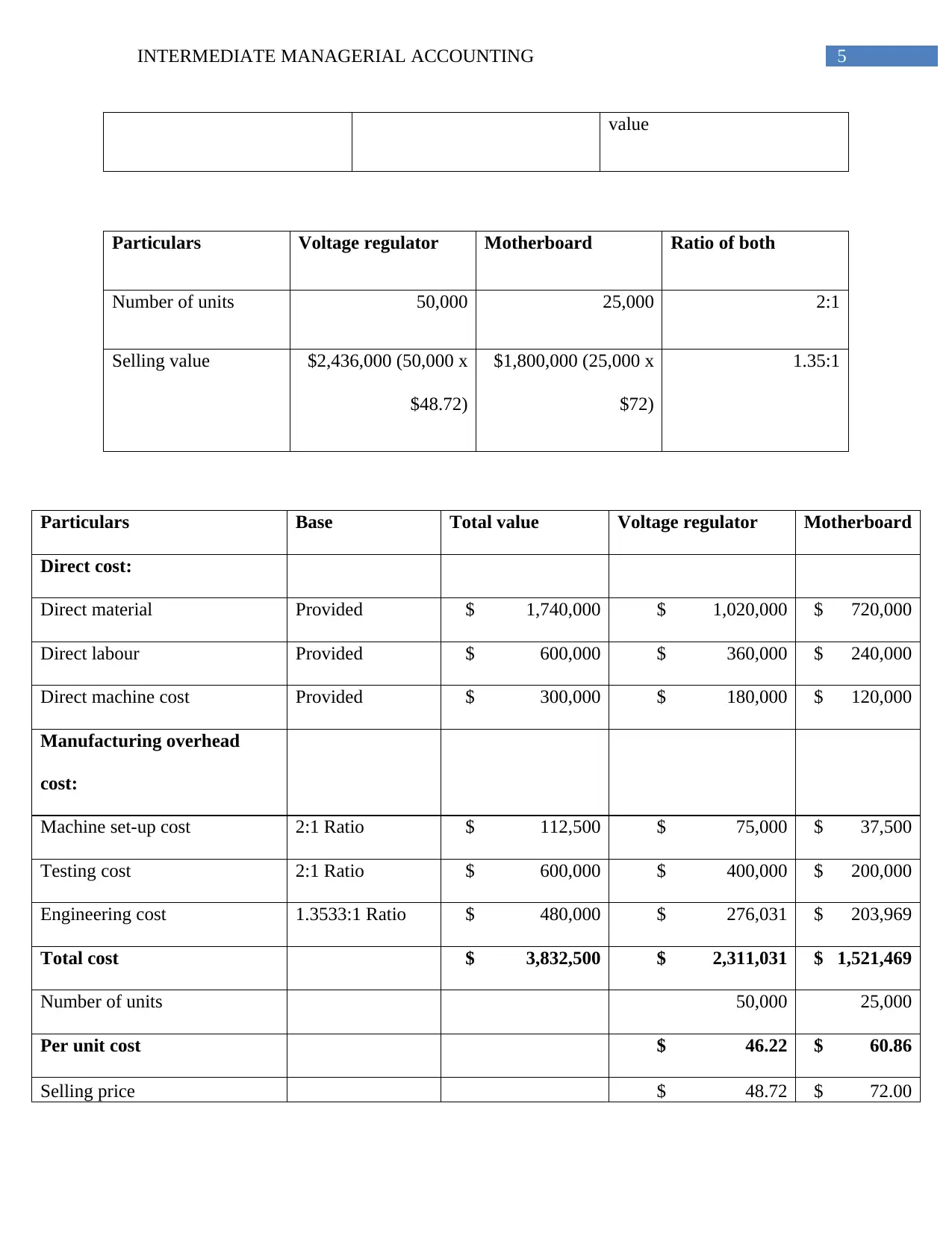

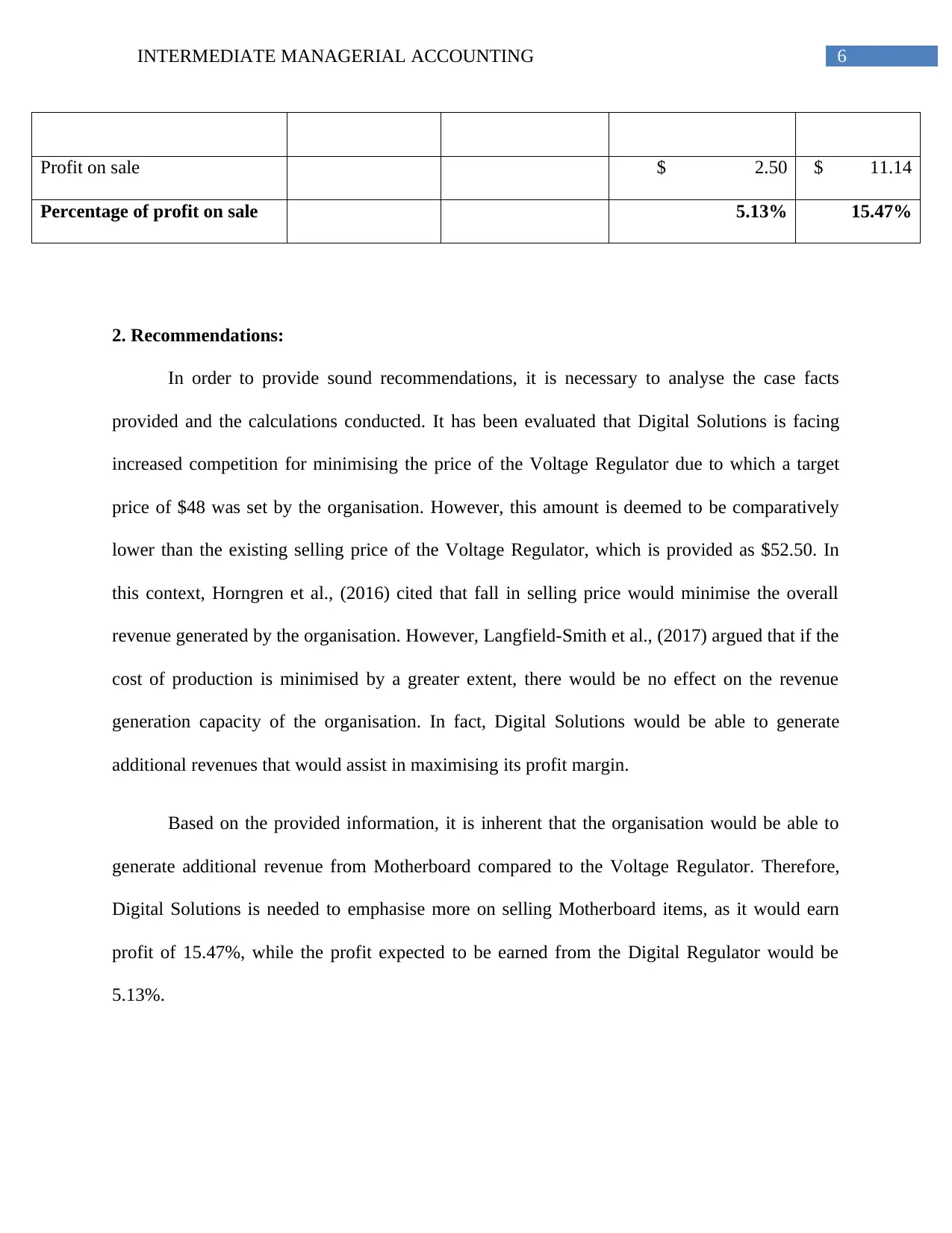

This case study examines Digital Solutions Inc., a manufacturer of Voltage Regulators and Motherboards, focusing on cost analysis and pricing strategies. The analysis includes activity-based allocation of overhead costs, markup on full product cost, target cost per unit for a new voltage regulator, and achievements of cost reduction targets. The study identifies that the current overhead allocation method is inaccurate and proposes a refined approach based on activity cost pools and cost drivers such as machine setup, testing, and engineering. The recommendations emphasize shifting focus towards Motherboard sales due to their higher profit margin compared to Voltage Regulators, despite the company's efforts to reduce the Voltage Regulator's cost and set a competitive target price. The analysis also highlights the importance of accurate cost allocation for informed decision-making and improved profitability.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.