Financial Decision Making, Performance Analysis, and Investment Report

VerifiedAdded on 2023/03/29

|23

|4571

|320

Report

AI Summary

This report provides a comprehensive analysis of the financial decision-making processes within Dining Group PLC, a UK-based company. It begins with a detailed business performance analysis, evaluating the company's financial statements using ratio analysis to assess profitability, liquidity, and debt-equity ratios. The analysis reveals a decline in profit-earning capacity in 2016 compared to 2015, despite revenue increases, indicating challenges in cost management. The report also examines the company's liquidity position, highlighting the need for improvements. Furthermore, the report includes an investment appraisal, evaluating a proposed investment of 120,000 million pounds, and assesses the company's average rate of return, net present value, and total cost of capital. Finally, the report recommends potential sources of funds for raising 100 million pounds and discusses non-financial factors that the board of directors should consider.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1............................................................................................................................................1

BUSINESS PERFORMANCE ANALYSIS..............................................................................1

PART 2..........................................................................................................................................12

INVESTMENT APPRAISAL..................................................................................................12

CONCLUSION..............................................................................................................................15

APPENDICES ..............................................................................................................................17

REFERENCES..............................................................................................................................18

PART 1............................................................................................................................................1

BUSINESS PERFORMANCE ANALYSIS..............................................................................1

PART 2..........................................................................................................................................12

INVESTMENT APPRAISAL..................................................................................................12

CONCLUSION..............................................................................................................................15

APPENDICES ..............................................................................................................................17

REFERENCES..............................................................................................................................18

EXECUTIVE SUMMARY

In order to have desirable profits and to attain organisational goals and objectives,

management of an organisation has to take various financial decisions during a financial year.

The report provides information regarding financial decision making of Dining group plc that is

based in UK. Its overall business performance has been analysed by its financial statements

using ratio analysis techniques that shows following results. Liquid position of the cited firm is

not good and has increased more of its finance through bank loan and other creditors. It has also

been determined that profit earning capacity of the company has been declined in 2016 than

2015. Operating cycle of the business is 16 days. Further, for making more investments, directors

have provided investment appraisal information that has been critically evaluated. Dining group

plc initial investment is 120000 million pound. During first year it will receive 20800 million

pound, same as last year it will receive 43200 million pound. Company's average rate of return is

11.2% and average annual profit was 6694 million pound. It was found that company's net

present value is 16% and total cost of capital is 3% and cited firm has an investment target

criterion of 12%. At last, sources of funds that can be used by Dining Group plc for raising funds

of 100 m has been recommended along with other non-financial factors that its board of directors

must consider.

In order to have desirable profits and to attain organisational goals and objectives,

management of an organisation has to take various financial decisions during a financial year.

The report provides information regarding financial decision making of Dining group plc that is

based in UK. Its overall business performance has been analysed by its financial statements

using ratio analysis techniques that shows following results. Liquid position of the cited firm is

not good and has increased more of its finance through bank loan and other creditors. It has also

been determined that profit earning capacity of the company has been declined in 2016 than

2015. Operating cycle of the business is 16 days. Further, for making more investments, directors

have provided investment appraisal information that has been critically evaluated. Dining group

plc initial investment is 120000 million pound. During first year it will receive 20800 million

pound, same as last year it will receive 43200 million pound. Company's average rate of return is

11.2% and average annual profit was 6694 million pound. It was found that company's net

present value is 16% and total cost of capital is 3% and cited firm has an investment target

criterion of 12%. At last, sources of funds that can be used by Dining Group plc for raising funds

of 100 m has been recommended along with other non-financial factors that its board of directors

must consider.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART 1

BUSINESS PERFORMANCE ANALYSIS

In order to measure and manage quantifiable achievements of an organisation, various

methodologies, processes, measurements and techniques are used by the management is

considered as a business performance analysis (Allan and et.al., 2015). Here, the performance of

Dining Group plc is undertaken by analysing and interpreting its financial statements using ratio

analysis technique.

Statement of Profit and Loss

Statement of profit and loss shows the profit earning capacity of the business along with

overall spendings in a financial year. Through what ways dining group plc is generating income

can be determined by analysing profit and loss statement (Authority, 2014). Income statement

includes various expenditure made during the year, revenues generated and profit earned or loss

suffered by the company during a specific period.

As per the profit and loss statement of Dining Group plc, it has been analysed that, in

2016, profit earned by firm is 29099, while in 2015, firm earned profit of 68875. This shows that,

the earning capacity of the company has reduced. However, revenues has been increased by

approximately 37% along with the increase in cost of sales by approximate 14%. In year 2016,

firm has also generated income from sale of plant property and equipment. Furthermore, finance

cost and taxation expenses in 2016 is also less than that of 2015. Thus, the only reason due to

which profit of Dining Group plc has been declined in 2016 is increase in proportion of revenue

to cost of sales. Factors that facilitated increment in revenue of the company may be increase in

the percentage of tourists in UK in 2016, or decline in competitors. While, factors that have

caused increase in cost of sales could be increase in staff and their salaries, increase in the cost of

accommodation facilities or high food material cost.

Moreover, for further analysis of company's profitability, profitable ratios such gross

profit ratio, operating profit ratio and net profit ratio has been calculated below. (APPENDIX 1)

Gross Profit ratio:

1

BUSINESS PERFORMANCE ANALYSIS

In order to measure and manage quantifiable achievements of an organisation, various

methodologies, processes, measurements and techniques are used by the management is

considered as a business performance analysis (Allan and et.al., 2015). Here, the performance of

Dining Group plc is undertaken by analysing and interpreting its financial statements using ratio

analysis technique.

Statement of Profit and Loss

Statement of profit and loss shows the profit earning capacity of the business along with

overall spendings in a financial year. Through what ways dining group plc is generating income

can be determined by analysing profit and loss statement (Authority, 2014). Income statement

includes various expenditure made during the year, revenues generated and profit earned or loss

suffered by the company during a specific period.

As per the profit and loss statement of Dining Group plc, it has been analysed that, in

2016, profit earned by firm is 29099, while in 2015, firm earned profit of 68875. This shows that,

the earning capacity of the company has reduced. However, revenues has been increased by

approximately 37% along with the increase in cost of sales by approximate 14%. In year 2016,

firm has also generated income from sale of plant property and equipment. Furthermore, finance

cost and taxation expenses in 2016 is also less than that of 2015. Thus, the only reason due to

which profit of Dining Group plc has been declined in 2016 is increase in proportion of revenue

to cost of sales. Factors that facilitated increment in revenue of the company may be increase in

the percentage of tourists in UK in 2016, or decline in competitors. While, factors that have

caused increase in cost of sales could be increase in staff and their salaries, increase in the cost of

accommodation facilities or high food material cost.

Moreover, for further analysis of company's profitability, profitable ratios such gross

profit ratio, operating profit ratio and net profit ratio has been calculated below. (APPENDIX 1)

Gross Profit ratio:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

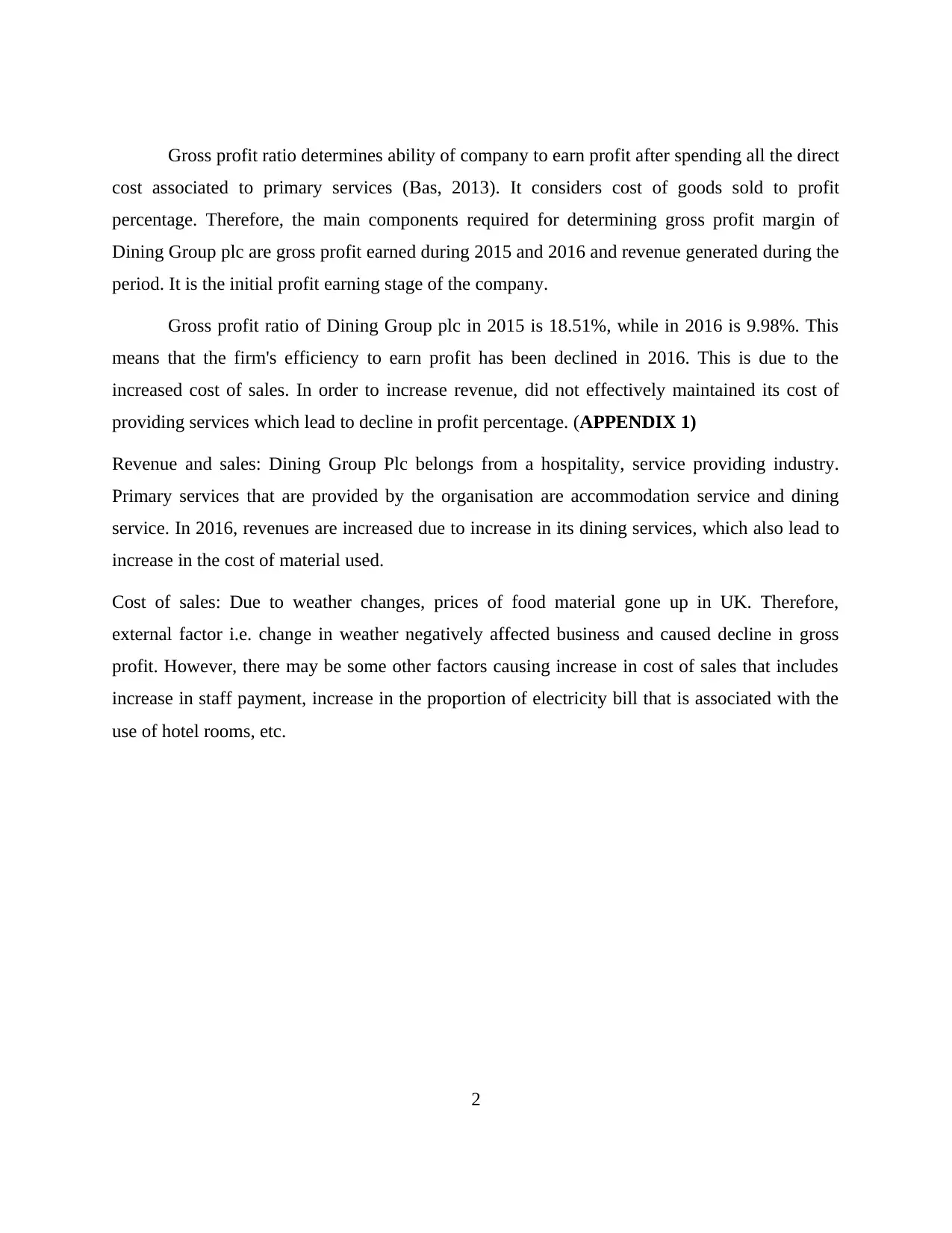

Gross profit ratio determines ability of company to earn profit after spending all the direct

cost associated to primary services (Bas, 2013). It considers cost of goods sold to profit

percentage. Therefore, the main components required for determining gross profit margin of

Dining Group plc are gross profit earned during 2015 and 2016 and revenue generated during the

period. It is the initial profit earning stage of the company.

Gross profit ratio of Dining Group plc in 2015 is 18.51%, while in 2016 is 9.98%. This

means that the firm's efficiency to earn profit has been declined in 2016. This is due to the

increased cost of sales. In order to increase revenue, did not effectively maintained its cost of

providing services which lead to decline in profit percentage. (APPENDIX 1)

Revenue and sales: Dining Group Plc belongs from a hospitality, service providing industry.

Primary services that are provided by the organisation are accommodation service and dining

service. In 2016, revenues are increased due to increase in its dining services, which also lead to

increase in the cost of material used.

Cost of sales: Due to weather changes, prices of food material gone up in UK. Therefore,

external factor i.e. change in weather negatively affected business and caused decline in gross

profit. However, there may be some other factors causing increase in cost of sales that includes

increase in staff payment, increase in the proportion of electricity bill that is associated with the

use of hotel rooms, etc.

2

cost associated to primary services (Bas, 2013). It considers cost of goods sold to profit

percentage. Therefore, the main components required for determining gross profit margin of

Dining Group plc are gross profit earned during 2015 and 2016 and revenue generated during the

period. It is the initial profit earning stage of the company.

Gross profit ratio of Dining Group plc in 2015 is 18.51%, while in 2016 is 9.98%. This

means that the firm's efficiency to earn profit has been declined in 2016. This is due to the

increased cost of sales. In order to increase revenue, did not effectively maintained its cost of

providing services which lead to decline in profit percentage. (APPENDIX 1)

Revenue and sales: Dining Group Plc belongs from a hospitality, service providing industry.

Primary services that are provided by the organisation are accommodation service and dining

service. In 2016, revenues are increased due to increase in its dining services, which also lead to

increase in the cost of material used.

Cost of sales: Due to weather changes, prices of food material gone up in UK. Therefore,

external factor i.e. change in weather negatively affected business and caused decline in gross

profit. However, there may be some other factors causing increase in cost of sales that includes

increase in staff payment, increase in the proportion of electricity bill that is associated with the

use of hotel rooms, etc.

2

2015 2016

0

100000

200000

300000

400000

500000

600000

700000

800000

2015 2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00 18.51

9.98

From the above graph it can be seen that, revenues has been increased from the past year

but profit has been declined. Decline in gross profit indicates that the organisation is not

performing well in the hospitality sector.

Operating Profit Ratio

3

Gross income

Net sales

G ros s profit ratio

0

100000

200000

300000

400000

500000

600000

700000

800000

2015 2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00 18.51

9.98

From the above graph it can be seen that, revenues has been increased from the past year

but profit has been declined. Decline in gross profit indicates that the organisation is not

performing well in the hospitality sector.

Operating Profit Ratio

3

Gross income

Net sales

G ros s profit ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

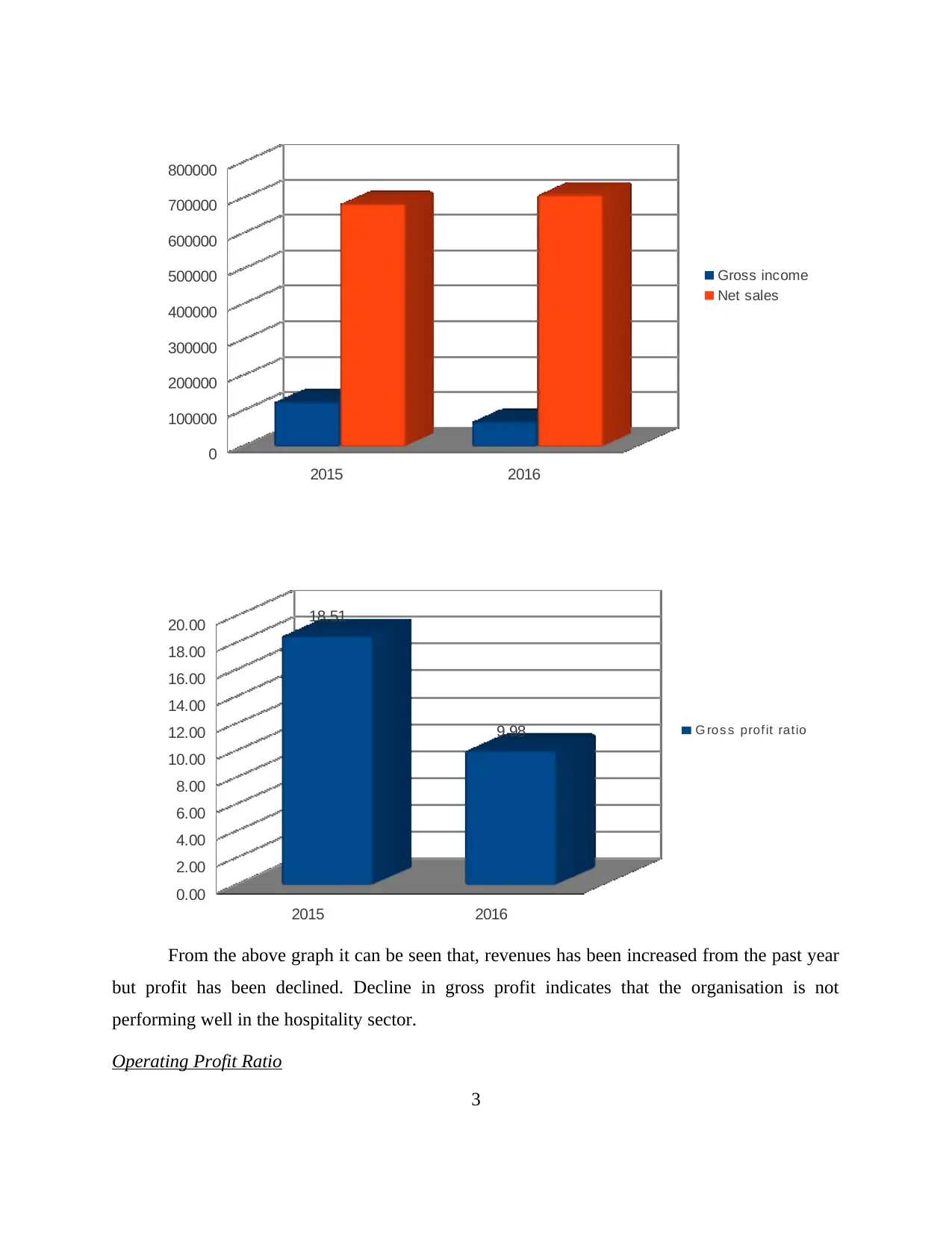

Operating profit also takes into consideration, fixed operating expenses and depreciation

and is the second main component in Profit and Loss statement (Bogdan, 2015). Operating ratio

for Dining Group plc has been calculated that shows 4.47% in 2016 and 12.97% in 2015. This

shows a huge decline in operating profit margin of the company. From the profit and loss

statement it is also visible that organisation has generated operating income from sale of plant,

property and equipment amounted to 1150, which was not generated in 2015. This means that,

firm has generated an extra revenue this year. However, operating cost of business in 2015

shows 38010 and in 2016 shows 40364, from this analysis it can be said that, business has also

incurred extra operating cost in 2016 which caused decline in operating margin of the company.

Reason behind decrease in operating income is increase in operating cost of the company i.e.

may be the company has charged more depreciation or have incurred more operating expenses

such as selling, general and administrative expenses, etc. (APPENDIX 1)

2015 2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00 12.97

4.49

Above graphical representation shows the difference between operating profit margin of

Dining group plc in year 2015 and 2016.

Net profit Ratio

Net profit ratio determines actual profit earning capacity of the business. This is the main

third component of income statement. Net profit is the final profit of company which is

4

O perating profit ratio

and is the second main component in Profit and Loss statement (Bogdan, 2015). Operating ratio

for Dining Group plc has been calculated that shows 4.47% in 2016 and 12.97% in 2015. This

shows a huge decline in operating profit margin of the company. From the profit and loss

statement it is also visible that organisation has generated operating income from sale of plant,

property and equipment amounted to 1150, which was not generated in 2015. This means that,

firm has generated an extra revenue this year. However, operating cost of business in 2015

shows 38010 and in 2016 shows 40364, from this analysis it can be said that, business has also

incurred extra operating cost in 2016 which caused decline in operating margin of the company.

Reason behind decrease in operating income is increase in operating cost of the company i.e.

may be the company has charged more depreciation or have incurred more operating expenses

such as selling, general and administrative expenses, etc. (APPENDIX 1)

2015 2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00 12.97

4.49

Above graphical representation shows the difference between operating profit margin of

Dining group plc in year 2015 and 2016.

Net profit Ratio

Net profit ratio determines actual profit earning capacity of the business. This is the main

third component of income statement. Net profit is the final profit of company which is

4

O perating profit ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

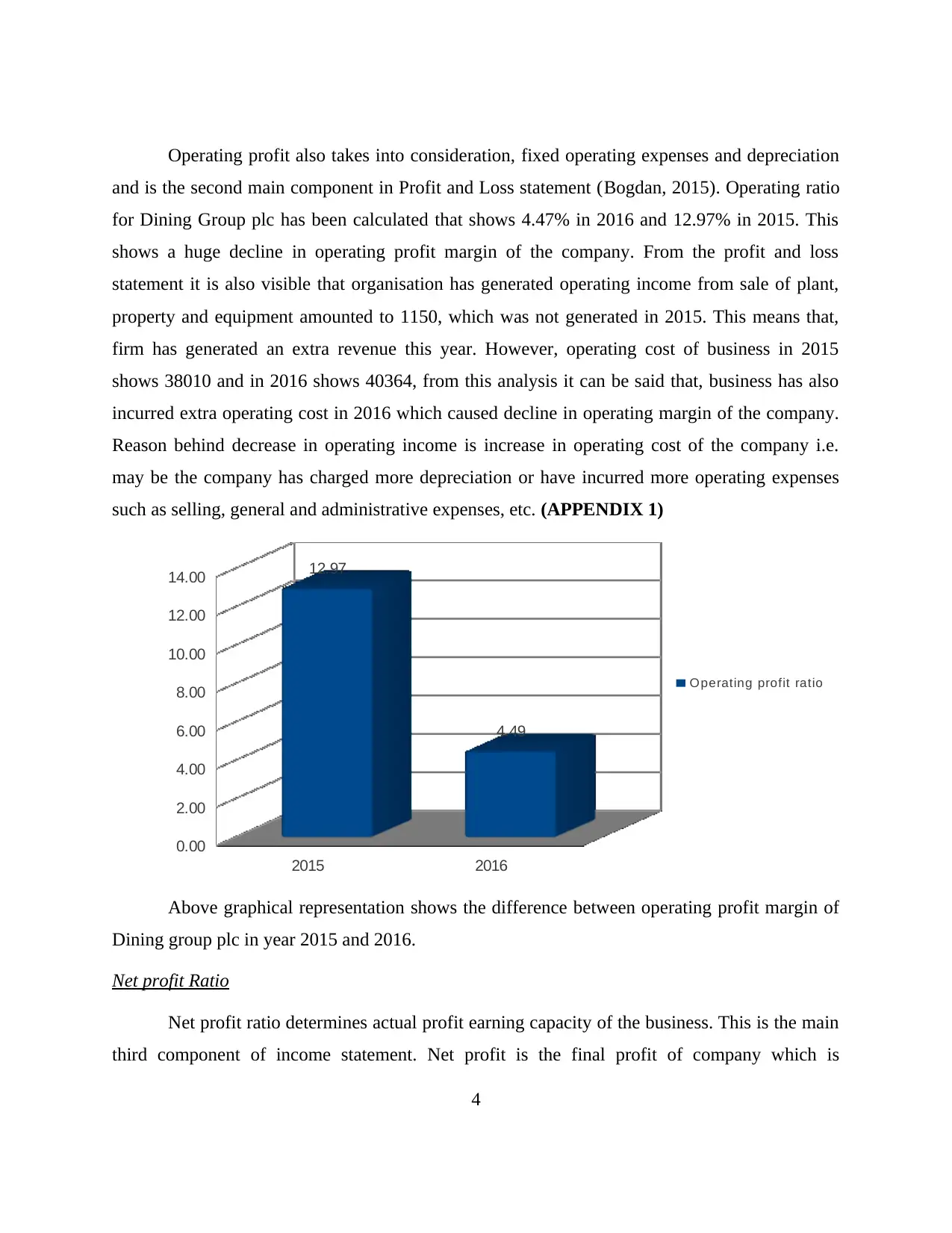

distributed among owners and shareholders of company (Hair, 2015). Owners of the company

are keen to know whether their business is profitable and can provide them good amount of

profit share or not. From the calculation of net margin ratio of Dining Group Plcit has been

analysed that like gross profit ratio and operating ratio, business has also shown a significant

decline in net margin ratio. Net earning capacity of the company in 2016 has decreased to more

than half from 2015. (APPENDIX 1)

2015 2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00 10.05

4.09

From the overall analysis of statement of profit and loss, it has been identified that Dining

Group plc was able to manage and lower its finance cost and tax charges, however, even then the

profit earning capacity of the company has been declined in 2016 than 2015.

Statement of Financial Position

Statement of financial position shows financial stability and financial position of the firm.

It is important to know financial position of the firm which in turn helps in determining the

liquidity position and credit conditions of the organisation. Main components of balance Sheet

are entity's assets, liabilities and equity (Homburg, Stierl and Bornemann, 2013). Various

information can be derived from the statement of financial position such as investments of share

holders, other investments, fixed assets, cash in hand and at bank, amount that is owed by the

company and amount that is owed to the company, etc. This is an important report that provides

5

Net m argin

are keen to know whether their business is profitable and can provide them good amount of

profit share or not. From the calculation of net margin ratio of Dining Group Plcit has been

analysed that like gross profit ratio and operating ratio, business has also shown a significant

decline in net margin ratio. Net earning capacity of the company in 2016 has decreased to more

than half from 2015. (APPENDIX 1)

2015 2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00 10.05

4.09

From the overall analysis of statement of profit and loss, it has been identified that Dining

Group plc was able to manage and lower its finance cost and tax charges, however, even then the

profit earning capacity of the company has been declined in 2016 than 2015.

Statement of Financial Position

Statement of financial position shows financial stability and financial position of the firm.

It is important to know financial position of the firm which in turn helps in determining the

liquidity position and credit conditions of the organisation. Main components of balance Sheet

are entity's assets, liabilities and equity (Homburg, Stierl and Bornemann, 2013). Various

information can be derived from the statement of financial position such as investments of share

holders, other investments, fixed assets, cash in hand and at bank, amount that is owed by the

company and amount that is owed to the company, etc. This is an important report that provides

5

Net m argin

relevant information to the external users of firm that significantly affects their decisions. It

includes calculating ratios like; profitability, liquidity, efficiency, debt equity ratios and so on. In

addition to this, comparison between last years' performances of entity and with other

competitive organisations are also interpreted. Here, financial position of the Dining Group plc is

analysed by calculating some financial performance ratios. (APPENDIX 2)

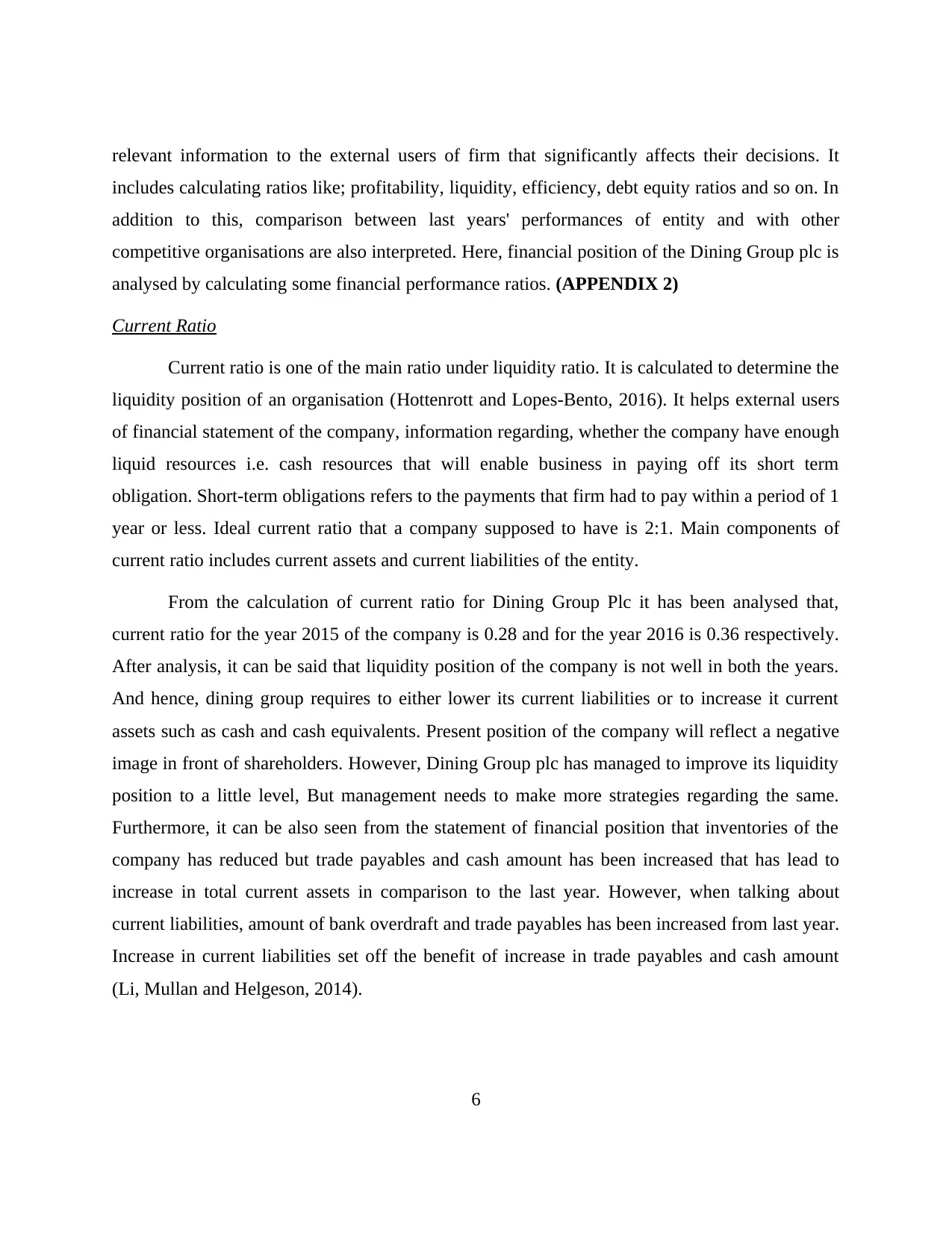

Current Ratio

Current ratio is one of the main ratio under liquidity ratio. It is calculated to determine the

liquidity position of an organisation (Hottenrott and Lopes‐Bento, 2016). It helps external users

of financial statement of the company, information regarding, whether the company have enough

liquid resources i.e. cash resources that will enable business in paying off its short term

obligation. Short-term obligations refers to the payments that firm had to pay within a period of 1

year or less. Ideal current ratio that a company supposed to have is 2:1. Main components of

current ratio includes current assets and current liabilities of the entity.

From the calculation of current ratio for Dining Group Plc it has been analysed that,

current ratio for the year 2015 of the company is 0.28 and for the year 2016 is 0.36 respectively.

After analysis, it can be said that liquidity position of the company is not well in both the years.

And hence, dining group requires to either lower its current liabilities or to increase it current

assets such as cash and cash equivalents. Present position of the company will reflect a negative

image in front of shareholders. However, Dining Group plc has managed to improve its liquidity

position to a little level, But management needs to make more strategies regarding the same.

Furthermore, it can be also seen from the statement of financial position that inventories of the

company has reduced but trade payables and cash amount has been increased that has lead to

increase in total current assets in comparison to the last year. However, when talking about

current liabilities, amount of bank overdraft and trade payables has been increased from last year.

Increase in current liabilities set off the benefit of increase in trade payables and cash amount

(Li, Mullan and Helgeson, 2014).

6

includes calculating ratios like; profitability, liquidity, efficiency, debt equity ratios and so on. In

addition to this, comparison between last years' performances of entity and with other

competitive organisations are also interpreted. Here, financial position of the Dining Group plc is

analysed by calculating some financial performance ratios. (APPENDIX 2)

Current Ratio

Current ratio is one of the main ratio under liquidity ratio. It is calculated to determine the

liquidity position of an organisation (Hottenrott and Lopes‐Bento, 2016). It helps external users

of financial statement of the company, information regarding, whether the company have enough

liquid resources i.e. cash resources that will enable business in paying off its short term

obligation. Short-term obligations refers to the payments that firm had to pay within a period of 1

year or less. Ideal current ratio that a company supposed to have is 2:1. Main components of

current ratio includes current assets and current liabilities of the entity.

From the calculation of current ratio for Dining Group Plc it has been analysed that,

current ratio for the year 2015 of the company is 0.28 and for the year 2016 is 0.36 respectively.

After analysis, it can be said that liquidity position of the company is not well in both the years.

And hence, dining group requires to either lower its current liabilities or to increase it current

assets such as cash and cash equivalents. Present position of the company will reflect a negative

image in front of shareholders. However, Dining Group plc has managed to improve its liquidity

position to a little level, But management needs to make more strategies regarding the same.

Furthermore, it can be also seen from the statement of financial position that inventories of the

company has reduced but trade payables and cash amount has been increased that has lead to

increase in total current assets in comparison to the last year. However, when talking about

current liabilities, amount of bank overdraft and trade payables has been increased from last year.

Increase in current liabilities set off the benefit of increase in trade payables and cash amount

(Li, Mullan and Helgeson, 2014).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2015 2016

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.28

0.36

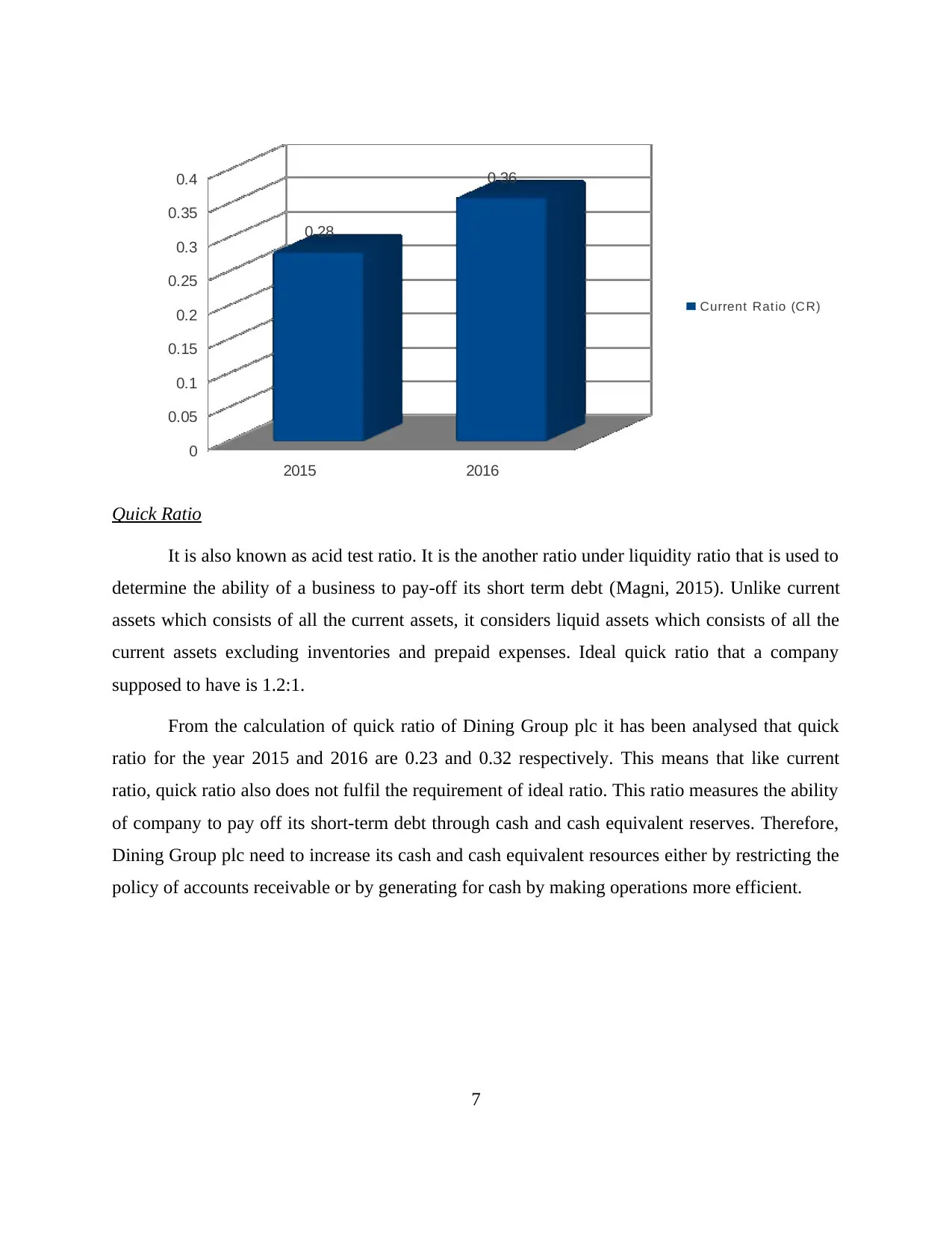

Quick Ratio

It is also known as acid test ratio. It is the another ratio under liquidity ratio that is used to

determine the ability of a business to pay-off its short term debt (Magni, 2015). Unlike current

assets which consists of all the current assets, it considers liquid assets which consists of all the

current assets excluding inventories and prepaid expenses. Ideal quick ratio that a company

supposed to have is 1.2:1.

From the calculation of quick ratio of Dining Group plc it has been analysed that quick

ratio for the year 2015 and 2016 are 0.23 and 0.32 respectively. This means that like current

ratio, quick ratio also does not fulfil the requirement of ideal ratio. This ratio measures the ability

of company to pay off its short-term debt through cash and cash equivalent reserves. Therefore,

Dining Group plc need to increase its cash and cash equivalent resources either by restricting the

policy of accounts receivable or by generating for cash by making operations more efficient.

7

Current Ratio (CR)

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.28

0.36

Quick Ratio

It is also known as acid test ratio. It is the another ratio under liquidity ratio that is used to

determine the ability of a business to pay-off its short term debt (Magni, 2015). Unlike current

assets which consists of all the current assets, it considers liquid assets which consists of all the

current assets excluding inventories and prepaid expenses. Ideal quick ratio that a company

supposed to have is 1.2:1.

From the calculation of quick ratio of Dining Group plc it has been analysed that quick

ratio for the year 2015 and 2016 are 0.23 and 0.32 respectively. This means that like current

ratio, quick ratio also does not fulfil the requirement of ideal ratio. This ratio measures the ability

of company to pay off its short-term debt through cash and cash equivalent reserves. Therefore,

Dining Group plc need to increase its cash and cash equivalent resources either by restricting the

policy of accounts receivable or by generating for cash by making operations more efficient.

7

Current Ratio (CR)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2015 2016

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.23

0.32

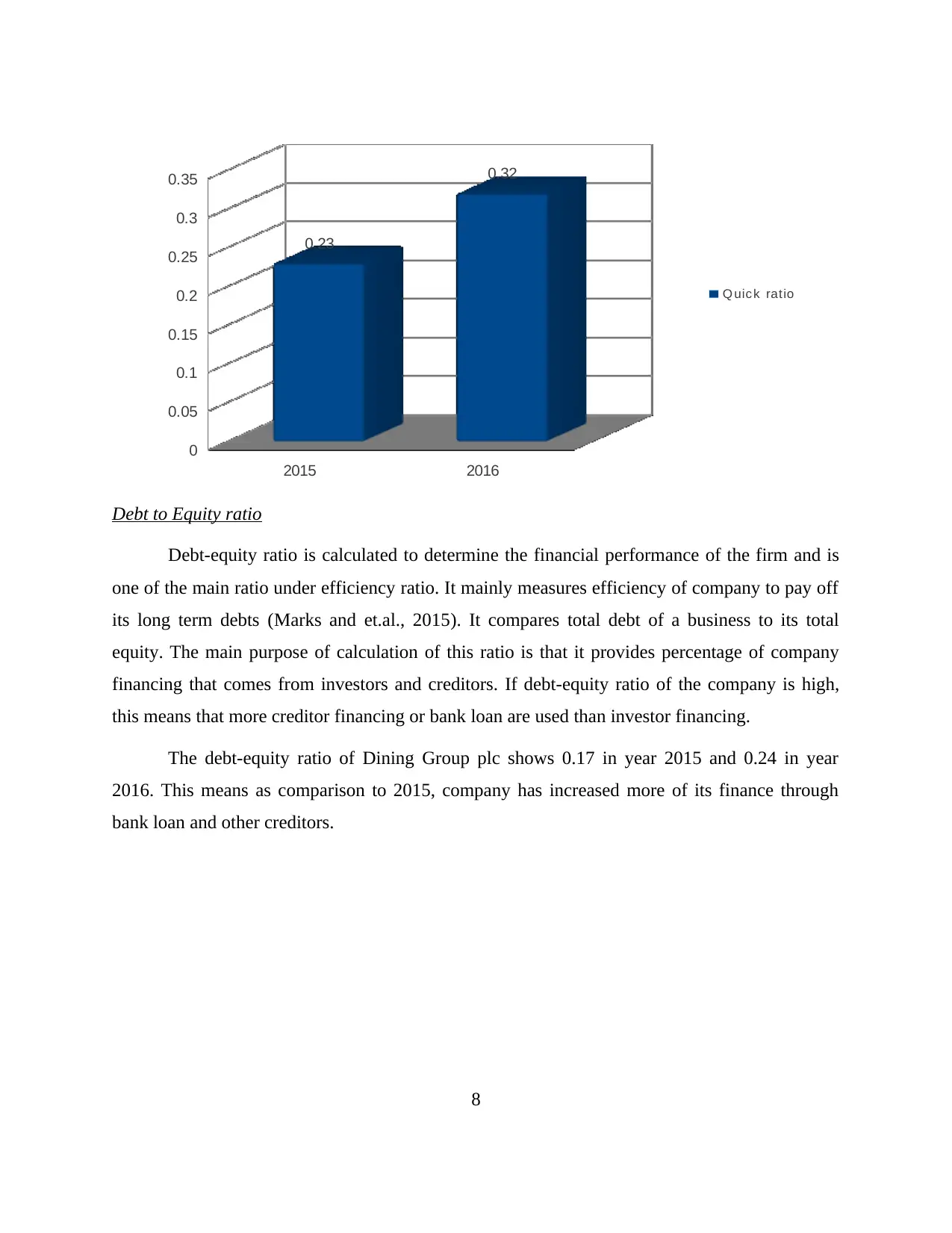

Debt to Equity ratio

Debt-equity ratio is calculated to determine the financial performance of the firm and is

one of the main ratio under efficiency ratio. It mainly measures efficiency of company to pay off

its long term debts (Marks and et.al., 2015). It compares total debt of a business to its total

equity. The main purpose of calculation of this ratio is that it provides percentage of company

financing that comes from investors and creditors. If debt-equity ratio of the company is high,

this means that more creditor financing or bank loan are used than investor financing.

The debt-equity ratio of Dining Group plc shows 0.17 in year 2015 and 0.24 in year

2016. This means as comparison to 2015, company has increased more of its finance through

bank loan and other creditors.

8

Q uic k ratio

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.23

0.32

Debt to Equity ratio

Debt-equity ratio is calculated to determine the financial performance of the firm and is

one of the main ratio under efficiency ratio. It mainly measures efficiency of company to pay off

its long term debts (Marks and et.al., 2015). It compares total debt of a business to its total

equity. The main purpose of calculation of this ratio is that it provides percentage of company

financing that comes from investors and creditors. If debt-equity ratio of the company is high,

this means that more creditor financing or bank loan are used than investor financing.

The debt-equity ratio of Dining Group plc shows 0.17 in year 2015 and 0.24 in year

2016. This means as comparison to 2015, company has increased more of its finance through

bank loan and other creditors.

8

Q uic k ratio

2015 2016

0

0.05

0.1

0.15

0.2

0.25

Statement of Cash Flow

It is one of the main financial statement prepared by an entity. It shows the overall flow

of cash in a specific period of time from all the activities i.e. operating, financing and investment

activities (Noyes and et.al., 2014). This report helps external users in knowing the amount of

cash generated from all the activities and amount of cash spent in all the activities. It is generally

made for a period of financial year. In short it is the summary of cash inflows and cash outflows

of the company that also tells cash at the beginning and at the end held by company.

Cash flow form Operating activities

It determines the amount of cash generated by a company from regular and ongoing

business activities such as selling goods and service providing activities. It does not consider

investment costs or long-term capital (Oladotun and Edosa, 2017). However, it does consists

earnings before interest. From the statement of cash flow from Dining Group plc it has been

analysed that, the company has generated 32401 from operating activities in year 2016. it is also

visible that inventories has been decreased from 757 and trade receivables and trade payables has

been increased from 5973 and 117361 respectively. Increase in trade receivables is considered

negative under operating activities because, services has been provided but cash has not yet

received.

9

Debt to equity ratio

0

0.05

0.1

0.15

0.2

0.25

Statement of Cash Flow

It is one of the main financial statement prepared by an entity. It shows the overall flow

of cash in a specific period of time from all the activities i.e. operating, financing and investment

activities (Noyes and et.al., 2014). This report helps external users in knowing the amount of

cash generated from all the activities and amount of cash spent in all the activities. It is generally

made for a period of financial year. In short it is the summary of cash inflows and cash outflows

of the company that also tells cash at the beginning and at the end held by company.

Cash flow form Operating activities

It determines the amount of cash generated by a company from regular and ongoing

business activities such as selling goods and service providing activities. It does not consider

investment costs or long-term capital (Oladotun and Edosa, 2017). However, it does consists

earnings before interest. From the statement of cash flow from Dining Group plc it has been

analysed that, the company has generated 32401 from operating activities in year 2016. it is also

visible that inventories has been decreased from 757 and trade receivables and trade payables has

been increased from 5973 and 117361 respectively. Increase in trade receivables is considered

negative under operating activities because, services has been provided but cash has not yet

received.

9

Debt to equity ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.