Comprehensive Financial Auditing and Assurance Report of DIPL Ltd.

VerifiedAdded on 2020/03/01

|9

|1848

|17

Report

AI Summary

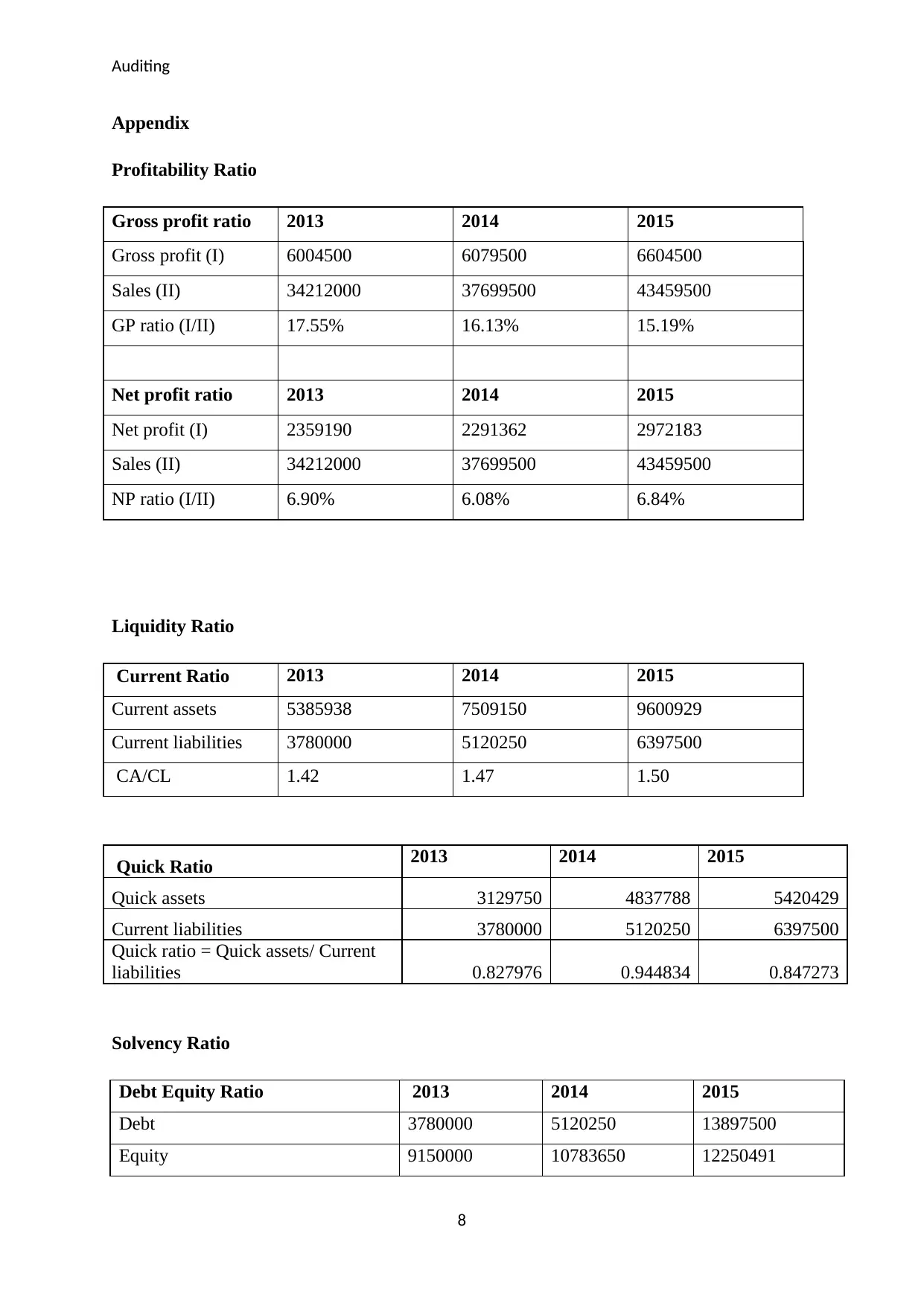

This report provides a comprehensive auditing and assurance analysis of DIPL Ltd. It begins by outlining how the auditor can utilize analytical procedures, such as financial data comparison and ratio computation, to make informed decisions and assess the company's financial performance. The report then identifies the inherent risks associated with the business, including the replacement of the IT system and the appointment of a CEO with financial interests. Furthermore, it details management risks stemming from software issues, inventory discrepancies, and strategic decisions. The report summarizes the actions that should be taken by the auditor. Finally, the report includes profitability, liquidity, and solvency ratios, which are essential for understanding the financial health of the company. The analysis highlights the need for auditors to scrutinize financial records, assess potential fraud, and ensure the accuracy of financial statements.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.