Audit and Assurance Report: Analysis of DIPL Financial Statements

VerifiedAdded on 2020/03/02

|10

|2246

|144

Report

AI Summary

This report presents an audit and assurance analysis of DIPL's financial statements, focusing on the application of analytic procedures, determination of inherent risk factors, and identification of potential misstatements. The analysis includes solvency, profit margin, and current ratio calculations, along with a discussion of factors contributing to financial risks, such as employee proficiency and management integrity. The report also explores risk factors related to fraudulent financial reporting, including loss of assets and excessive pressure on employees and management. References to relevant auditing and assurance resources are also provided. The report aims to provide a comprehensive overview of the financial health and potential risks associated with DIPL's operations.

Running head: AUDIT AND ASSURANCE

Audit and Assurance

Name of Student:

Name of University:

Author’s Note:

Audit and Assurance

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT AND ASSURANCE

Table of Contents

Answer of Question 1:.....................................................................................................................2

Application of the analytic procedures to DIPL’s financial report information:.........................2

Answer to Question 2:.....................................................................................................................3

Determination of the risk factors inherent, arising from the nature of DIPL’s Business

operations:....................................................................................................................................3

Answer to question 3:......................................................................................................................7

Identification as well as the explanation of two major risk factors connected to the

misstatements arising from the fraudulent financial reporting:...................................................7

References:......................................................................................................................................8

Table of Contents

Answer of Question 1:.....................................................................................................................2

Application of the analytic procedures to DIPL’s financial report information:.........................2

Answer to Question 2:.....................................................................................................................3

Determination of the risk factors inherent, arising from the nature of DIPL’s Business

operations:....................................................................................................................................3

Answer to question 3:......................................................................................................................7

Identification as well as the explanation of two major risk factors connected to the

misstatements arising from the fraudulent financial reporting:...................................................7

References:......................................................................................................................................8

2AUDIT AND ASSURANCE

Answer of Question 1:

Application of the analytic procedures to DIPL’s financial report information:

The most important nature of the economic report of the DIPL has been useful in

development of the plan of audit. The time of undertaking the audit follows the planning process

of auditing. Overall the assessor maintains the audit costs up to a level or a stage which is more

or less reasonable. It has been found that this helps the maintenance of the audit cost as well

helps in the misunderstanding related to the clients. DIPL’s economic statement is related to the

dissemination from the firm’s financial declaration.

Approach in an analytic sense for the common size is dependent upon the financial

statement as well as the common point of references. Further it has been found out that this is

helpful in the comparison of the economic statements that are related to different corporations.

Related to this the assessors can deem the several items that have been discussed in the financial

report. An example can be cited as, the registering procedure of the items like the net assets as

well as the liabilities associated with the owner’s in the company’s report. It is of a financial

nature. It also helps to understand the deviation from the usual process of reporting (Hayes,

Wallage and Gortemaker 2014).

Furthermore, it is found that the analysis of ratios can be considered as a suitable analytic

technique used for the audit plan assessment as well as the declarations of an economic nature.

Procedural analysis of results influencing the audit planning decisions:

The most significant result of the decision regarding to the planning has been deemed

important for the result analysis. The results of the analysis have been found to be influenced by

Answer of Question 1:

Application of the analytic procedures to DIPL’s financial report information:

The most important nature of the economic report of the DIPL has been useful in

development of the plan of audit. The time of undertaking the audit follows the planning process

of auditing. Overall the assessor maintains the audit costs up to a level or a stage which is more

or less reasonable. It has been found that this helps the maintenance of the audit cost as well

helps in the misunderstanding related to the clients. DIPL’s economic statement is related to the

dissemination from the firm’s financial declaration.

Approach in an analytic sense for the common size is dependent upon the financial

statement as well as the common point of references. Further it has been found out that this is

helpful in the comparison of the economic statements that are related to different corporations.

Related to this the assessors can deem the several items that have been discussed in the financial

report. An example can be cited as, the registering procedure of the items like the net assets as

well as the liabilities associated with the owner’s in the company’s report. It is of a financial

nature. It also helps to understand the deviation from the usual process of reporting (Hayes,

Wallage and Gortemaker 2014).

Furthermore, it is found that the analysis of ratios can be considered as a suitable analytic

technique used for the audit plan assessment as well as the declarations of an economic nature.

Procedural analysis of results influencing the audit planning decisions:

The most significant result of the decision regarding to the planning has been deemed

important for the result analysis. The results of the analysis have been found to be influenced by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT AND ASSURANCE

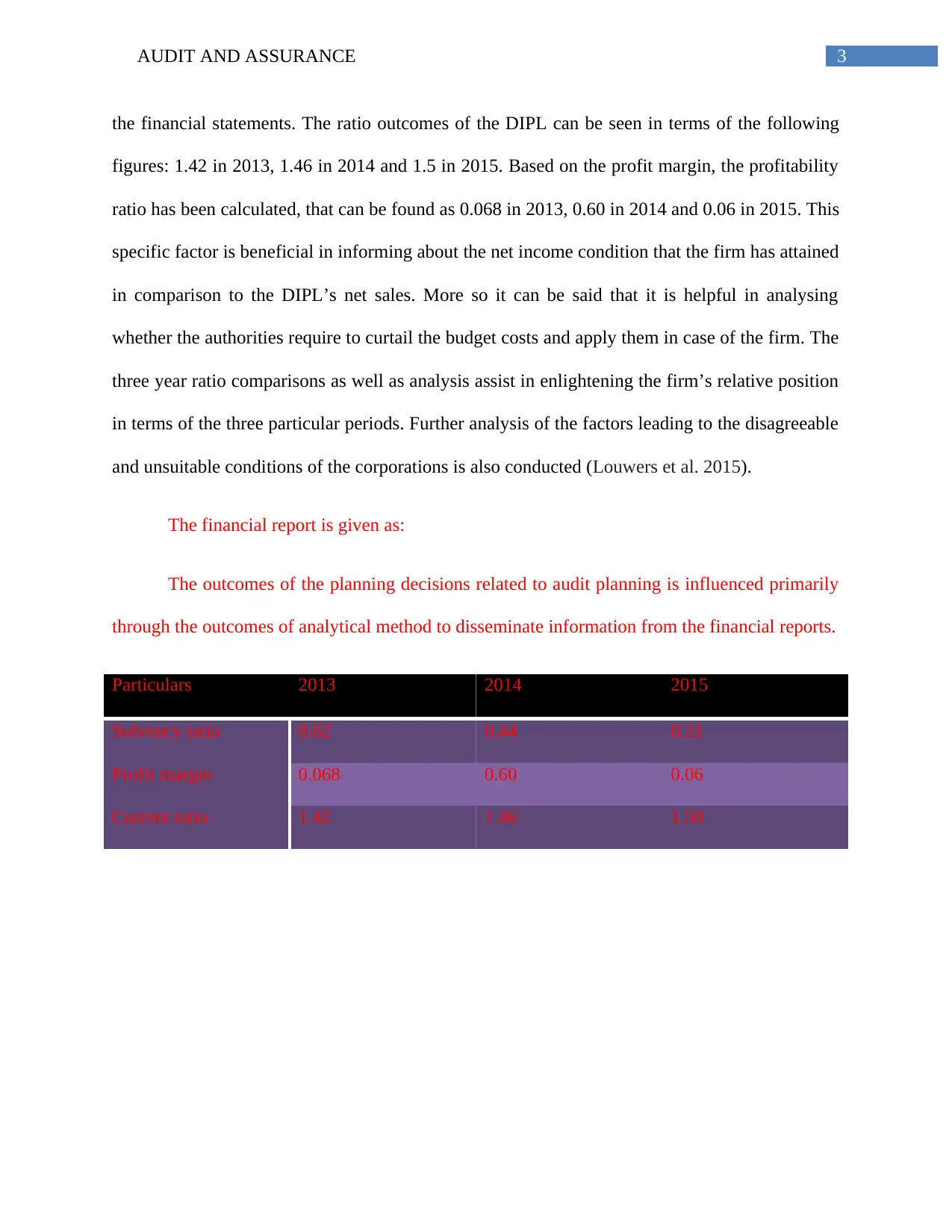

the financial statements. The ratio outcomes of the DIPL can be seen in terms of the following

figures: 1.42 in 2013, 1.46 in 2014 and 1.5 in 2015. Based on the profit margin, the profitability

ratio has been calculated, that can be found as 0.068 in 2013, 0.60 in 2014 and 0.06 in 2015. This

specific factor is beneficial in informing about the net income condition that the firm has attained

in comparison to the DIPL’s net sales. More so it can be said that it is helpful in analysing

whether the authorities require to curtail the budget costs and apply them in case of the firm. The

three year ratio comparisons as well as analysis assist in enlightening the firm’s relative position

in terms of the three particular periods. Further analysis of the factors leading to the disagreeable

and unsuitable conditions of the corporations is also conducted (Louwers et al. 2015).

The financial report is given as:

The outcomes of the planning decisions related to audit planning is influenced primarily

through the outcomes of analytical method to disseminate information from the financial reports.

Particulars 2013 2014 2015

Solvency ratio 0.62 0.44 0.21

Profit margin 0.068 0.60 0.06

Current ratio 1.42 1.46 1.50

the financial statements. The ratio outcomes of the DIPL can be seen in terms of the following

figures: 1.42 in 2013, 1.46 in 2014 and 1.5 in 2015. Based on the profit margin, the profitability

ratio has been calculated, that can be found as 0.068 in 2013, 0.60 in 2014 and 0.06 in 2015. This

specific factor is beneficial in informing about the net income condition that the firm has attained

in comparison to the DIPL’s net sales. More so it can be said that it is helpful in analysing

whether the authorities require to curtail the budget costs and apply them in case of the firm. The

three year ratio comparisons as well as analysis assist in enlightening the firm’s relative position

in terms of the three particular periods. Further analysis of the factors leading to the disagreeable

and unsuitable conditions of the corporations is also conducted (Louwers et al. 2015).

The financial report is given as:

The outcomes of the planning decisions related to audit planning is influenced primarily

through the outcomes of analytical method to disseminate information from the financial reports.

Particulars 2013 2014 2015

Solvency ratio 0.62 0.44 0.21

Profit margin 0.068 0.60 0.06

Current ratio 1.42 1.46 1.50

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT AND ASSURANCE

Answer to Question 2:

Determination of the risk factors inherent, arising from the nature of DIPL’s Business

operations:

The vital factor has been found to be based on the auditing that comprises of the related

incidents in connection to the material misstatements as well as the economic declarations

related to a specific nature. It can be stated however, that forms of the systematic as also the

unsystematic risks has been found to further show the process in which the corporations take

financial misstatements into consideration. Regardless of this, the allied risks can be seen to be

based on the financial as well as the non-financial factors which are quite possible (Knechel and

Salterio 2016). These factors can help in warding off a particular corporation for showing a

genuine and fair viewpoint of those financial decisions which are pertinent in nature. The

identifiable risks can be connected further with the several risk associations depending on the

omission of the risks connected to various errors, that is not probable for a specific bookkeeper.

With regard to the core of the diverse mistakes committed, the specific nature of bookkeeping

possesses certain inherent risks that are found to occur from the way of the operations.

Depending on the available considerations which have been mentioned in the report, it

can be clearly and surely stated that several transactions are available related to the accountants

which are not usually seen with the DIPL corporation. The direct lead which is sequential with

regard to the inconsistencies, specifically associated with the accountants or otherwise. This is

not usually seen in case of the DIPL Corporation (Nalewaik and Mills 2016). The direct as well

as chronological lead are specifically related to the ineffective planning of the activities

regarding the sales. Additionally it can be said that the pecuniary declarations have been found to

expose the fact that the corporation has failed to achieve the pre-determined profit level from the

Answer to Question 2:

Determination of the risk factors inherent, arising from the nature of DIPL’s Business

operations:

The vital factor has been found to be based on the auditing that comprises of the related

incidents in connection to the material misstatements as well as the economic declarations

related to a specific nature. It can be stated however, that forms of the systematic as also the

unsystematic risks has been found to further show the process in which the corporations take

financial misstatements into consideration. Regardless of this, the allied risks can be seen to be

based on the financial as well as the non-financial factors which are quite possible (Knechel and

Salterio 2016). These factors can help in warding off a particular corporation for showing a

genuine and fair viewpoint of those financial decisions which are pertinent in nature. The

identifiable risks can be connected further with the several risk associations depending on the

omission of the risks connected to various errors, that is not probable for a specific bookkeeper.

With regard to the core of the diverse mistakes committed, the specific nature of bookkeeping

possesses certain inherent risks that are found to occur from the way of the operations.

Depending on the available considerations which have been mentioned in the report, it

can be clearly and surely stated that several transactions are available related to the accountants

which are not usually seen with the DIPL corporation. The direct lead which is sequential with

regard to the inconsistencies, specifically associated with the accountants or otherwise. This is

not usually seen in case of the DIPL Corporation (Nalewaik and Mills 2016). The direct as well

as chronological lead are specifically related to the ineffective planning of the activities

regarding the sales. Additionally it can be said that the pecuniary declarations have been found to

expose the fact that the corporation has failed to achieve the pre-determined profit level from the

5AUDIT AND ASSURANCE

sales-based revenue. Particularly the failures due to the management have been recognised in

terms of the particular requirements which have been recognised with resulting adjustments of

the functionalities.

Separately from the workers, the overall risk has been escalated by the DIPL

Corporation. The lack of proficiency and know-how of the employees, there has been increasing

rise of the inherent risks (Beasley 2015). This is due to the fact that the staff members in many

cases do not have the requisite competency. The non-proficient nature of the workforce can help

increase the risk to stop the committing of mistakes. The exclusion or the removal of the errors

as well as the cases in which misstatement have been stated are purely on the basis of the

economic announcements (Arens et al. 2016).

The facts that are noteworthy in relation to the existing risks can be divided into several

categories. This is done on the basis of segments exclusively formed for the environmental issues

as also the external facets, misstatements of materialistic nature in the earlier time periods as well

as the exercises which are falsified. Based on the given scenario’s evaluation it has been found

that the DIPL has been capable of reflection on the risks which are noteworthy and need to be

removed in the procedure of CEO succession (Barton and Bruder 2014). Overall it can be said

that the Chief Executive Officer is obviously a different candidate in comparison to the others.

Some of the risks can be considered to have an involvement with the procedural quality for the

selection as well as the handling process (Hayes, Wallage and Gortemaker 2014). There are

numerous risks which are associated with the process and its initiation without following the

strategy, as also the derisory involvement of the CEO and the candidate departure (Duncan and

Whittington 2014).

sales-based revenue. Particularly the failures due to the management have been recognised in

terms of the particular requirements which have been recognised with resulting adjustments of

the functionalities.

Separately from the workers, the overall risk has been escalated by the DIPL

Corporation. The lack of proficiency and know-how of the employees, there has been increasing

rise of the inherent risks (Beasley 2015). This is due to the fact that the staff members in many

cases do not have the requisite competency. The non-proficient nature of the workforce can help

increase the risk to stop the committing of mistakes. The exclusion or the removal of the errors

as well as the cases in which misstatement have been stated are purely on the basis of the

economic announcements (Arens et al. 2016).

The facts that are noteworthy in relation to the existing risks can be divided into several

categories. This is done on the basis of segments exclusively formed for the environmental issues

as also the external facets, misstatements of materialistic nature in the earlier time periods as well

as the exercises which are falsified. Based on the given scenario’s evaluation it has been found

that the DIPL has been capable of reflection on the risks which are noteworthy and need to be

removed in the procedure of CEO succession (Barton and Bruder 2014). Overall it can be said

that the Chief Executive Officer is obviously a different candidate in comparison to the others.

Some of the risks can be considered to have an involvement with the procedural quality for the

selection as well as the handling process (Hayes, Wallage and Gortemaker 2014). There are

numerous risks which are associated with the process and its initiation without following the

strategy, as also the derisory involvement of the CEO and the candidate departure (Duncan and

Whittington 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT AND ASSURANCE

Based on the case analysis, it can be additionally revealed that the different types of

implementations for innovative IT processes have caused specific problems. DIPL did not

process enough staff members to handle the implementation and the reconciliation procedure

before the new arrangement before the end of the year (DeFond and Zhang 2014). The procedure

of primary testing initially, has shown that appropriate amount of time was not given to the

transactions. This led to various incidents of materialistic misstatements. Other inherent risks of

omission in specific financial declarations were also found (Eilifsen et al. 2013).

Additionally the cash receipts as also the recording were seen to be performed by the

expertise of the finance professionals (Waldron 2016). The risks were not handled appropriately

at first. The total members of the staff were required to abide by the correct sequence of

Receivable Accounts as also the request of Accounts Receivable ledger for its perfect

maintenance (Knechel and Salterio 2016). Additionally, there was also the requirement of the

bank reconciliation appropriately. The register of e-book generated revenues as well as textbook

reprinting have chances of leading to different nature of complexities involved in the particular

procedure.

Also it can be said that the process of evaluation of the raw material inventory was not

appropriate as the existing paper cost was notably higher than the average paper cost.

The way in which risk can affect the material misstatement in the financial report:

The nature of risk identification is connected to the material misstatements.

Excessive pressure on the management as well as the employees:

Based on the case analysis, it can be additionally revealed that the different types of

implementations for innovative IT processes have caused specific problems. DIPL did not

process enough staff members to handle the implementation and the reconciliation procedure

before the new arrangement before the end of the year (DeFond and Zhang 2014). The procedure

of primary testing initially, has shown that appropriate amount of time was not given to the

transactions. This led to various incidents of materialistic misstatements. Other inherent risks of

omission in specific financial declarations were also found (Eilifsen et al. 2013).

Additionally the cash receipts as also the recording were seen to be performed by the

expertise of the finance professionals (Waldron 2016). The risks were not handled appropriately

at first. The total members of the staff were required to abide by the correct sequence of

Receivable Accounts as also the request of Accounts Receivable ledger for its perfect

maintenance (Knechel and Salterio 2016). Additionally, there was also the requirement of the

bank reconciliation appropriately. The register of e-book generated revenues as well as textbook

reprinting have chances of leading to different nature of complexities involved in the particular

procedure.

Also it can be said that the process of evaluation of the raw material inventory was not

appropriate as the existing paper cost was notably higher than the average paper cost.

The way in which risk can affect the material misstatement in the financial report:

The nature of risk identification is connected to the material misstatements.

Excessive pressure on the management as well as the employees:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT AND ASSURANCE

The excessive burden on the members of the staff affects the bookkeeping. There have

been certain qualities for example the propensity to encounter concerns regarding the flow of

cash, low level of liquidity along with the operating outcomes (Cannon and Bedard 2016).

Entire management integrity:

DIPL lacks the integrity and requisites. It is hence expected that they will be prepared for

their loss of reputation.

Unusual pressure on the managements:

In many cases the material misstatements cause financial declarations.

Nature of business entity:

The rising growth procedure of the DIPL corporation have been thought of in connection

to the competitive scenario. There is a possibility of these factors affecting the overall nature of

the risk connected to the business as well as the planning structure of the audit.

Answer to question 3:

Identification as well as the explanation of two major risk factors connected to the

misstatements arising from the fraudulent financial reporting:

Popularly known explanations of the fraud risks connected to the material misstatements are

listed below:

Loss of Assets The involved fraud risk due to workplace dissatisfaction put excessive

pressure on the employees. It also leads to several problems.

Incidence of fraud in the Excessive burden on the employees may lead to materialistic

The excessive burden on the members of the staff affects the bookkeeping. There have

been certain qualities for example the propensity to encounter concerns regarding the flow of

cash, low level of liquidity along with the operating outcomes (Cannon and Bedard 2016).

Entire management integrity:

DIPL lacks the integrity and requisites. It is hence expected that they will be prepared for

their loss of reputation.

Unusual pressure on the managements:

In many cases the material misstatements cause financial declarations.

Nature of business entity:

The rising growth procedure of the DIPL corporation have been thought of in connection

to the competitive scenario. There is a possibility of these factors affecting the overall nature of

the risk connected to the business as well as the planning structure of the audit.

Answer to question 3:

Identification as well as the explanation of two major risk factors connected to the

misstatements arising from the fraudulent financial reporting:

Popularly known explanations of the fraud risks connected to the material misstatements are

listed below:

Loss of Assets The involved fraud risk due to workplace dissatisfaction put excessive

pressure on the employees. It also leads to several problems.

Incidence of fraud in the Excessive burden on the employees may lead to materialistic

8AUDIT AND ASSURANCE

engagement of workforce misstatements

Fraud of financial reporting Certain types of fraud may occur due to excessive expectation from the

financers on specific performance

Unsuitable average cost Depending on the depictions made in the report, it can be clearly stated

that the valuation of the raw material was not appropriate

engagement of workforce misstatements

Fraud of financial reporting Certain types of fraud may occur due to excessive expectation from the

financers on specific performance

Unsuitable average cost Depending on the depictions made in the report, it can be clearly stated

that the valuation of the raw material was not appropriate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT AND ASSURANCE

References:

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance services.

Pearson.

Barton, H. and Bruder, N., 2014. A guide to local environmental auditing. Routledge.

Beasley, M.S., 2015. Auditing cases: An interactive learning approach. Prentice Hall.

Cannon, N. and Bedard, J.C., 2016. Auditing challenging fair value measurements: Evidence

from the field. The Accounting Review.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance and

audit: Does this equal security?. In Proceedings of the 7th International Conference on Security

of Information and Networks (p. 77). ACM.

Eilifsen, A., Messier, W.F., Glover, S.M. and Prawitt, D.F., 2013. Auditing and assurance

services. McGraw-Hill.

Hayes, R., Wallage, P. and Gortemaker, H., 2014. Principles of auditing: an introduction to

international standards on auditing. Pearson Higher Ed.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C., 2015. Auditing

& assurance services. McGraw-Hill Education.

References:

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance services.

Pearson.

Barton, H. and Bruder, N., 2014. A guide to local environmental auditing. Routledge.

Beasley, M.S., 2015. Auditing cases: An interactive learning approach. Prentice Hall.

Cannon, N. and Bedard, J.C., 2016. Auditing challenging fair value measurements: Evidence

from the field. The Accounting Review.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance and

audit: Does this equal security?. In Proceedings of the 7th International Conference on Security

of Information and Networks (p. 77). ACM.

Eilifsen, A., Messier, W.F., Glover, S.M. and Prawitt, D.F., 2013. Auditing and assurance

services. McGraw-Hill.

Hayes, R., Wallage, P. and Gortemaker, H., 2014. Principles of auditing: an introduction to

international standards on auditing. Pearson Higher Ed.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C., 2015. Auditing

& assurance services. McGraw-Hill Education.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.