Financial Analysis and Audit Assurance Report for DIPL Company

VerifiedAdded on 2020/02/24

|11

|1389

|45

Report

AI Summary

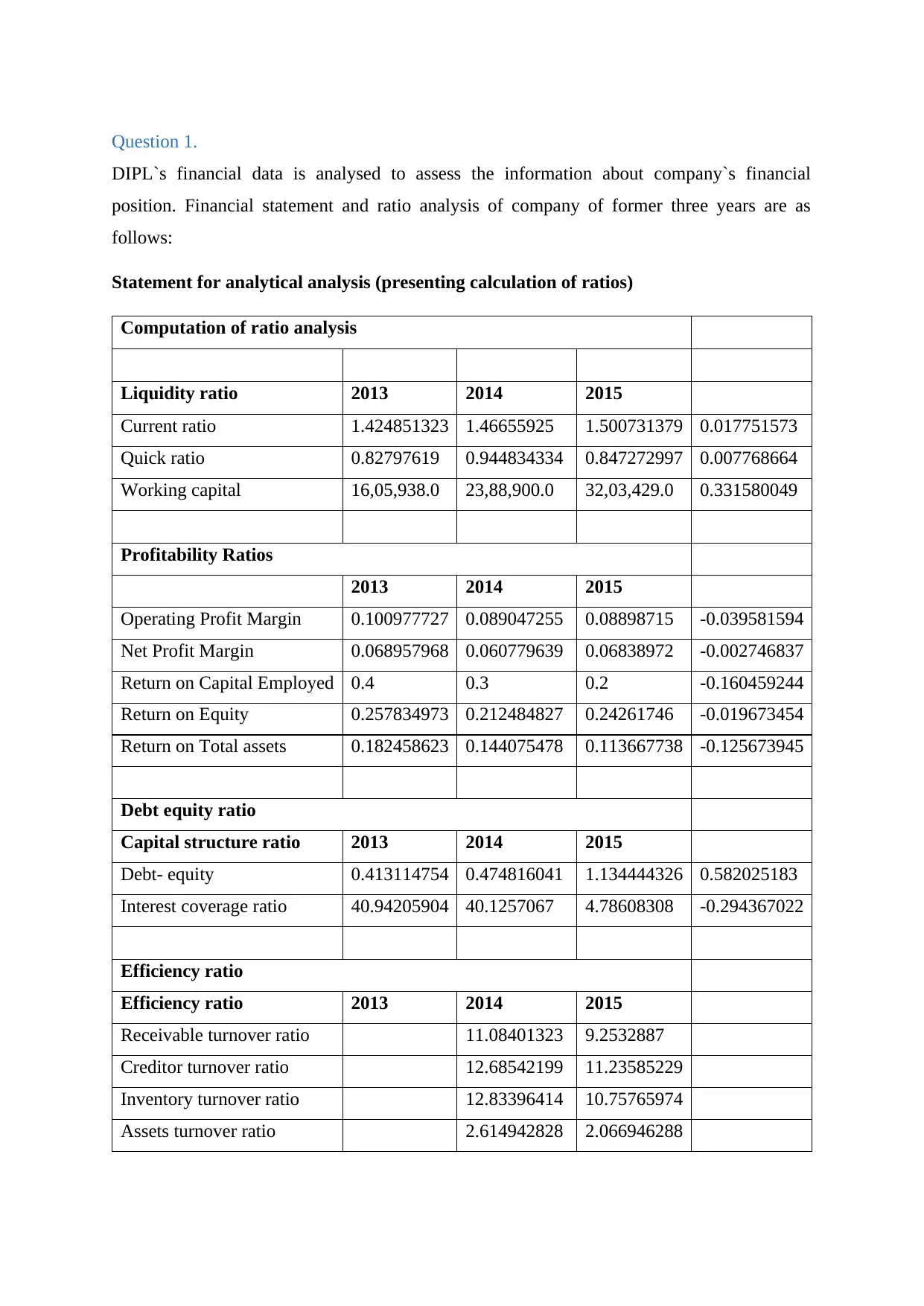

This report analyzes the financial statements and audit of DIPL, an Australian printing company. It examines the company's financial position through ratio analysis, including liquidity, profitability, and capital structure ratios, over a three-year period. The analysis reveals changes in business strategies and their impact on financial factors, highlighting potential misstatements and inherent risks. The report identifies key fraud risk factors, such as interest amount discrepancies and changes in the debt-to-equity ratio, which suggest manipulation of financial information to potentially reduce tax liabilities and impress stakeholders. The conclusion emphasizes the unethical practices observed, including the manipulation of financial statements and the recording of transactions to serve the company's interests. The report also references various sources related to audit risk, risk management, and accounting principles.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.