Comprehensive Audit Report: DIPL Printing Press Financial Analysis

VerifiedAdded on 2020/03/02

|8

|1161

|38

Report

AI Summary

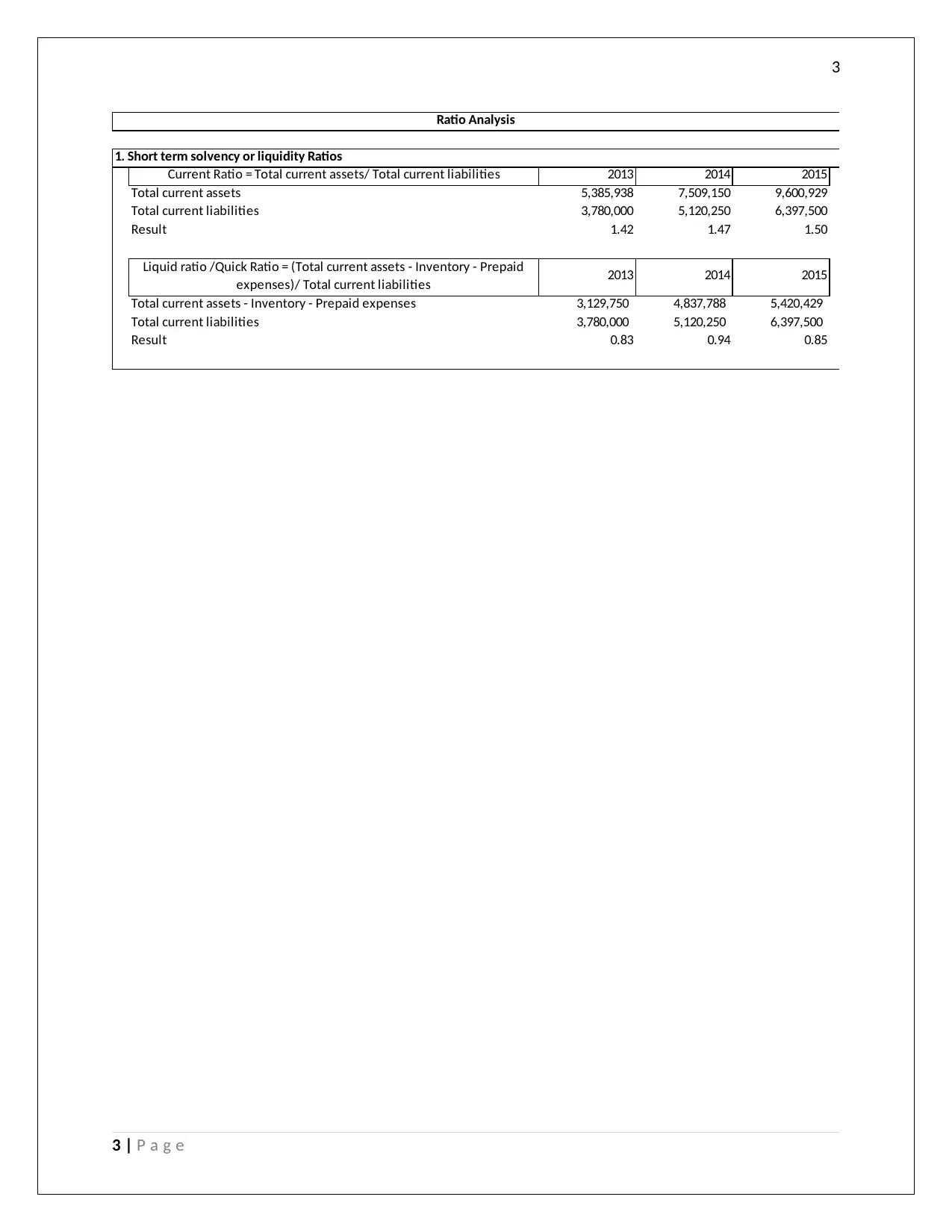

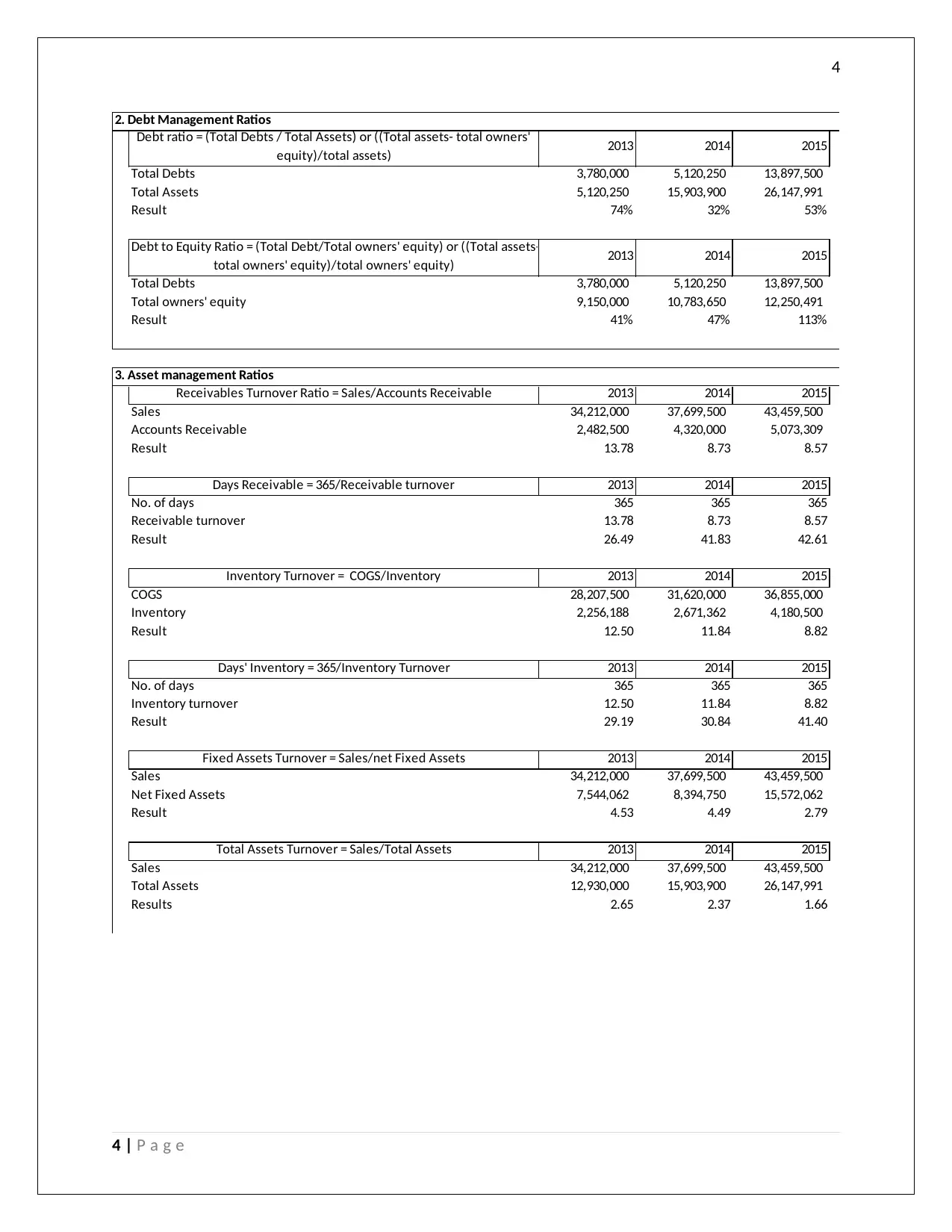

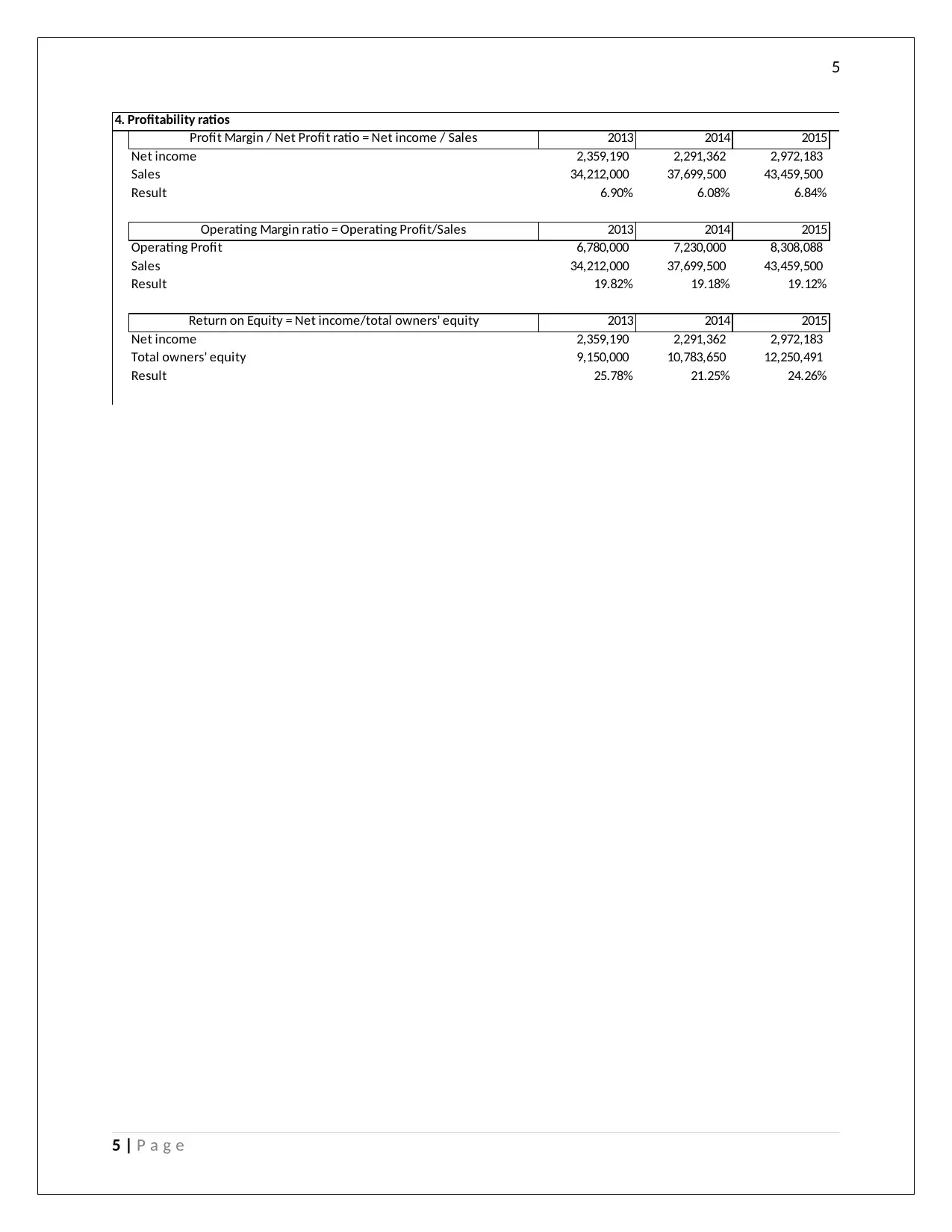

This report presents an audit of DIPL Printing Press, examining its financial statements, internal controls, and potential risks and fraud. The audit includes substantive and analytical procedures, such as ratio analysis and trend analysis, to assess the company's financial position, profitability, debt management, and liquidity. The report identifies inherent risks related to changes in accounting policies, non-routine work like IT system installation, and lack of segregation of duties, highlighting potential fraud elements. The auditor emphasizes the importance of mitigating these risks through proper controls, verification of documents, and reconciliation of accounts. The analysis incorporates relevant literature and provides recommendations for improving financial reporting and governance.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.