Audit Assurance and Compliance Report: DIPL Audit Analysis and Risks

VerifiedAdded on 2020/03/04

|11

|2825

|218

Report

AI Summary

This report provides a comprehensive analysis of audit assurance and compliance, focusing on the financial performance and associated risks of DIPL. It begins by examining analytical procedures used in the audit process, including ratio analysis and common size statements, and how these procedures inform audit planning decisions. The report then identifies and explains the inherent risks arising from the nature of DIPL's business operations, such as incorrect interpretations, improper recording of transactions, and challenges related to CEO succession. Furthermore, the report explores two significant fraud risks linked to fraudulent financial reporting, including pressures from stakeholders and employee dissatisfaction. The impact of these fraud risks on the audit plan is also discussed. The analysis incorporates financial data from 2013 to 2015, highlighting trends in profitability, solvency, and current ratios to support the risk assessments and recommendations.

Running head: AUDIT ASSURANCE AND COMPLIANCE

Audit Assurance and Compliance

Name of Student:

Name of University:

Author’s Note:

Audit Assurance and Compliance

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT ASSURANCE AND COMPLIANCE

Answer to Question 1:

Analytical procedures form an important part of the process of audit that involves the

evaluation of financial information of the organization made by the study of plausible

relationships between non-financial and financial data. The audit plan of DIPL can be developed

through the adoption of analytical procedures of the financial declarations given. There can be

variations in the identified in the relationships in the particular conditions and this involves

business changes, accounting changes, any unusual transactions, material misstatements and

random fluctuations. Planning of audit will help the auditors in maintaining the cost at prescribed

level and avoiding of any misinterpretation that can arise with the clients. The dissemination

process that is involves in analysing the financial declarations provided by DIPL is depicted in

the analytical procedures. The financial and business analysts would be able to take crucial

decisions concerning the business by deciphering the financial information’s using the

procedures of analytics (Beasley 2015).

The procedures adopted by the auditor in analysing the financial information is ratio

analysis and common size statements analysis. Common size helps in comparing the financial

declarations made by organization at different any of time or it makes the comparison between

the financial declarations information provided by two organization at one point of time. Items

that are recorded using some basis are also analysed using this method. Auditors from the

analytical procedures obtain the observation of consistency of the records amount in the financial

information. Expectations of auditors are developed for desired level of assurance from the

analytical procedures. The analysis of audit plan is done by the adoption of another analytical

procedure that is benchmarking. Any variations or deviation from the expected value id depicted

by framing the benchmarking of the actual financial declaration. Ratio analysis will help the

Answer to Question 1:

Analytical procedures form an important part of the process of audit that involves the

evaluation of financial information of the organization made by the study of plausible

relationships between non-financial and financial data. The audit plan of DIPL can be developed

through the adoption of analytical procedures of the financial declarations given. There can be

variations in the identified in the relationships in the particular conditions and this involves

business changes, accounting changes, any unusual transactions, material misstatements and

random fluctuations. Planning of audit will help the auditors in maintaining the cost at prescribed

level and avoiding of any misinterpretation that can arise with the clients. The dissemination

process that is involves in analysing the financial declarations provided by DIPL is depicted in

the analytical procedures. The financial and business analysts would be able to take crucial

decisions concerning the business by deciphering the financial information’s using the

procedures of analytics (Beasley 2015).

The procedures adopted by the auditor in analysing the financial information is ratio

analysis and common size statements analysis. Common size helps in comparing the financial

declarations made by organization at different any of time or it makes the comparison between

the financial declarations information provided by two organization at one point of time. Items

that are recorded using some basis are also analysed using this method. Auditors from the

analytical procedures obtain the observation of consistency of the records amount in the financial

information. Expectations of auditors are developed for desired level of assurance from the

analytical procedures. The analysis of audit plan is done by the adoption of another analytical

procedure that is benchmarking. Any variations or deviation from the expected value id depicted

by framing the benchmarking of the actual financial declaration. Ratio analysis will help the

2AUDIT ASSURANCE AND COMPLIANCE

auditors in ascertaining the trend of performance of organization over period (Byrnes et al.

2015).

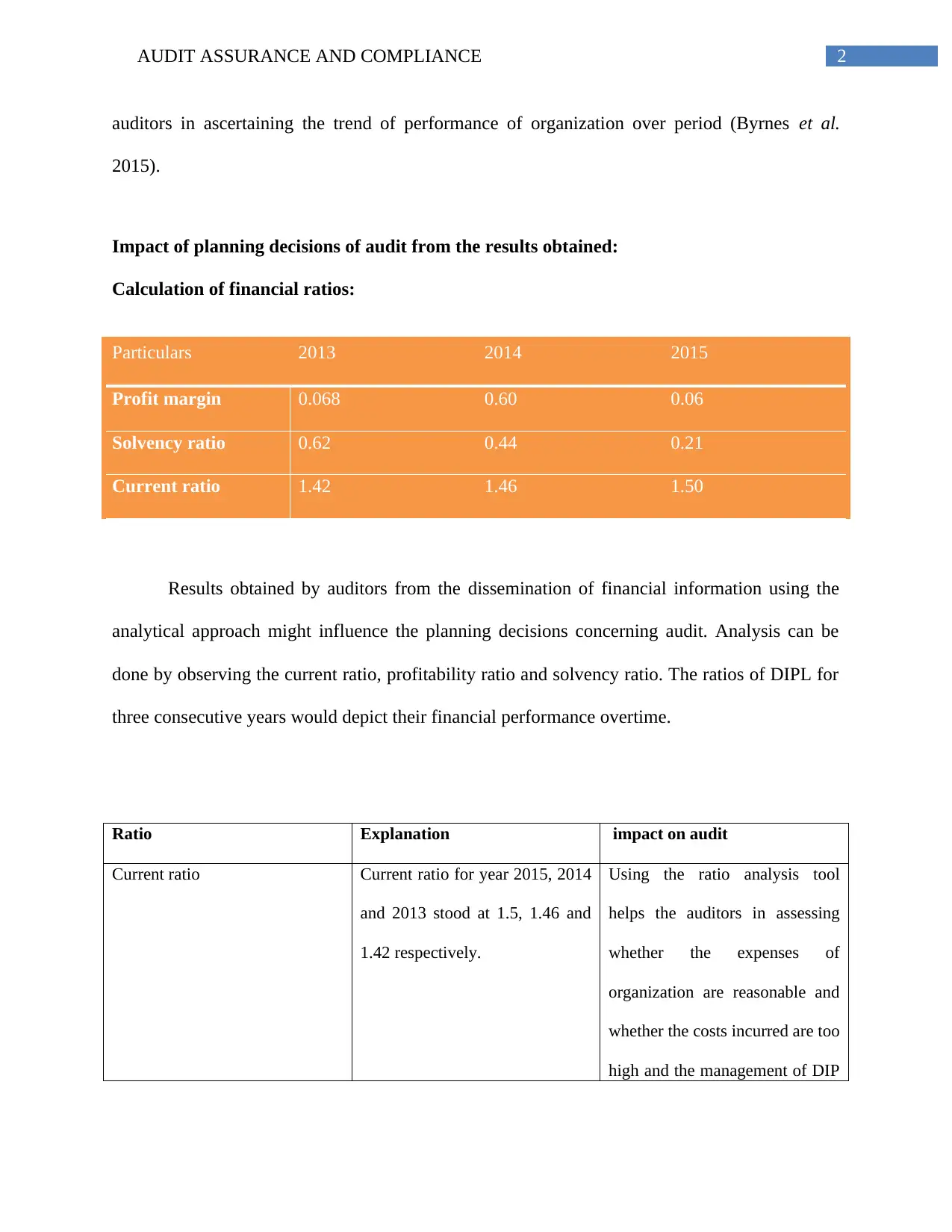

Impact of planning decisions of audit from the results obtained:

Calculation of financial ratios:

Particulars 2013 2014 2015

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Current ratio 1.42 1.46 1.50

Results obtained by auditors from the dissemination of financial information using the

analytical approach might influence the planning decisions concerning audit. Analysis can be

done by observing the current ratio, profitability ratio and solvency ratio. The ratios of DIPL for

three consecutive years would depict their financial performance overtime.

Ratio Explanation impact on audit

Current ratio Current ratio for year 2015, 2014

and 2013 stood at 1.5, 1.46 and

1.42 respectively.

Using the ratio analysis tool

helps the auditors in assessing

whether the expenses of

organization are reasonable and

whether the costs incurred are too

high and the management of DIP

auditors in ascertaining the trend of performance of organization over period (Byrnes et al.

2015).

Impact of planning decisions of audit from the results obtained:

Calculation of financial ratios:

Particulars 2013 2014 2015

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Current ratio 1.42 1.46 1.50

Results obtained by auditors from the dissemination of financial information using the

analytical approach might influence the planning decisions concerning audit. Analysis can be

done by observing the current ratio, profitability ratio and solvency ratio. The ratios of DIPL for

three consecutive years would depict their financial performance overtime.

Ratio Explanation impact on audit

Current ratio Current ratio for year 2015, 2014

and 2013 stood at 1.5, 1.46 and

1.42 respectively.

Using the ratio analysis tool

helps the auditors in assessing

whether the expenses of

organization are reasonable and

whether the costs incurred are too

high and the management of DIP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT ASSURANCE AND COMPLIANCE

has necessary resources and they

take necessary measures to

restrain any unfavourable

happenings.

Solvency ratio Solvency ratio of DIPL for

finance year 2013, 2014 and

2015 stood at .62, 0.44 and 0.21

respectively.

The auditor would use factor of

assessment in analysing whether

the organization is experiencing

sufficient cash flow for meeting

the overall and short-term

obligations faced by

organizations (Baker et al. 2014).

Profitability ratio Profitability ratio for the year

2013 stood at 0.068, for financial

year 2014 it stood at 0.60 and

0.06 in year 2015 respectively.

Analysis of this particular ratio

depicts the growth of net income

as against net sales of DIPL.

Relative position of organization

can be easily ascertained with the

application of the tool of ratio

analysis and recognition of the

factors that has led to any

undesirable situations obtained.

Answer to Question 2:

Identification of inherent risk factors that arise from nature of business operations of DIPL

The various types of the risks assessed for the audit process has been comprised based on

the incidence associated to the material misstatements in the financial announcements of the

specific concerns. It can be however be discerned that the various types of the considerations

has necessary resources and they

take necessary measures to

restrain any unfavourable

happenings.

Solvency ratio Solvency ratio of DIPL for

finance year 2013, 2014 and

2015 stood at .62, 0.44 and 0.21

respectively.

The auditor would use factor of

assessment in analysing whether

the organization is experiencing

sufficient cash flow for meeting

the overall and short-term

obligations faced by

organizations (Baker et al. 2014).

Profitability ratio Profitability ratio for the year

2013 stood at 0.068, for financial

year 2014 it stood at 0.60 and

0.06 in year 2015 respectively.

Analysis of this particular ratio

depicts the growth of net income

as against net sales of DIPL.

Relative position of organization

can be easily ascertained with the

application of the tool of ratio

analysis and recognition of the

factors that has led to any

undesirable situations obtained.

Answer to Question 2:

Identification of inherent risk factors that arise from nature of business operations of DIPL

The various types of the risks assessed for the audit process has been comprised based on

the incidence associated to the material misstatements in the financial announcements of the

specific concerns. It can be however be discerned that the various types of the considerations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT ASSURANCE AND COMPLIANCE

associated to the systematic and the various types of the unsystematic risks to state about the

various types of the risks for the financial declarations of the corporation. The various types of

the other risks detected have been applicable to both financial and the non-financial factors

which can be averted in a particular organisation thereby reflecting the true and the fair view of

the various types of the financial declarations. Nevertheless, the evaluator may find it demanding

for the detection certain risks. The different types of the correlated risks have been included for

omission along with the varied range of errors and not thinkable for a particular bookkeeper. In

this aspect the inherent risk may arise due to the overall nature of the business organisation of

DIPL (Duncan, B. and Whittington 2014).

The significant concerns towards the various types of the inherent risks has been

categorised as per environmental and material misstatements with the falsified exercises. The

environmental facets has been further seen to be directed towards the inherent risks and the swift

alterations in associated areas such as valuation of inventory, stiff competition in the market and

the shortage associated to the capital (Eilifsen et al. 2013).

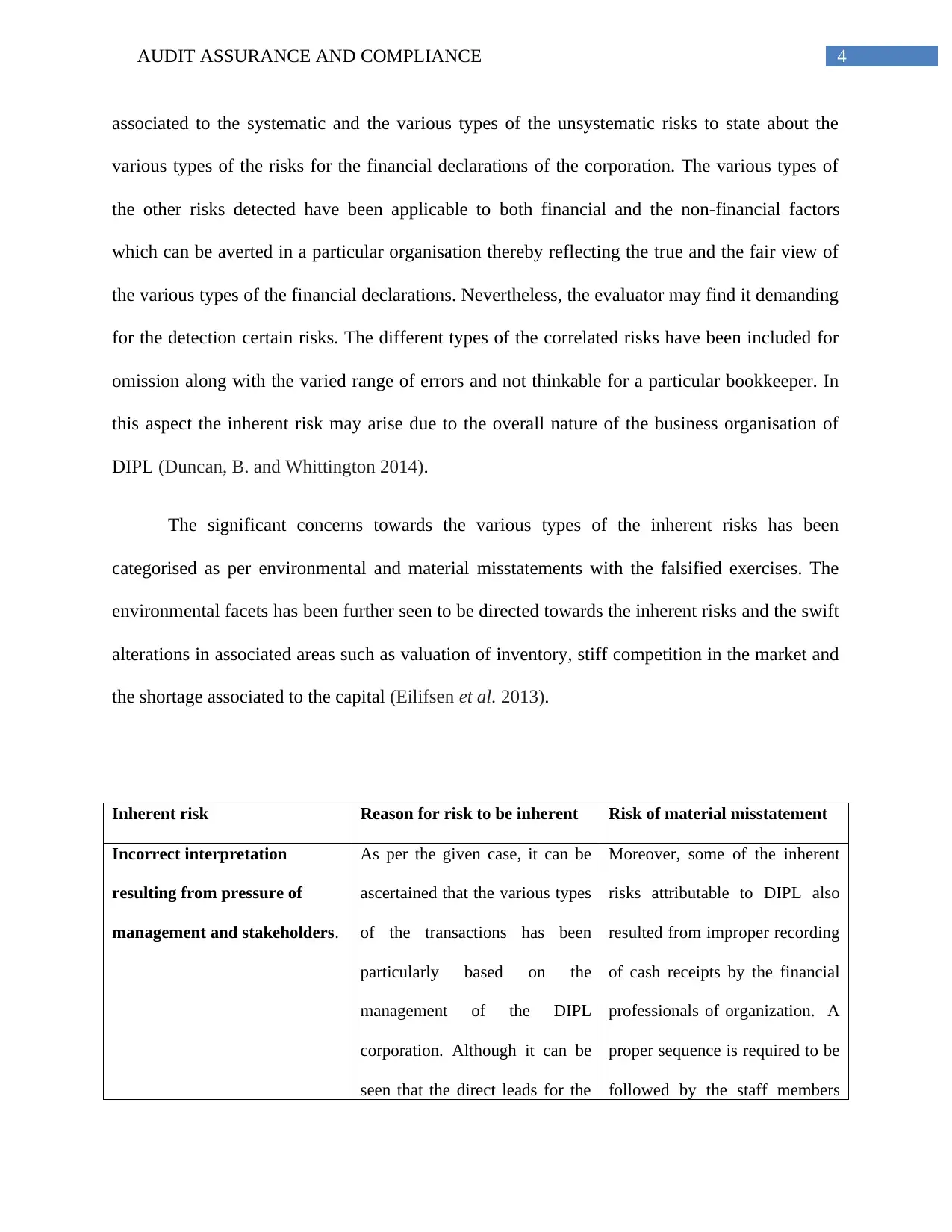

Inherent risk Reason for risk to be inherent Risk of material misstatement

Incorrect interpretation

resulting from pressure of

management and stakeholders.

As per the given case, it can be

ascertained that the various types

of the transactions has been

particularly based on the

management of the DIPL

corporation. Although it can be

seen that the direct leads for the

Moreover, some of the inherent

risks attributable to DIPL also

resulted from improper recording

of cash receipts by the financial

professionals of organization. A

proper sequence is required to be

followed by the staff members

associated to the systematic and the various types of the unsystematic risks to state about the

various types of the risks for the financial declarations of the corporation. The various types of

the other risks detected have been applicable to both financial and the non-financial factors

which can be averted in a particular organisation thereby reflecting the true and the fair view of

the various types of the financial declarations. Nevertheless, the evaluator may find it demanding

for the detection certain risks. The different types of the correlated risks have been included for

omission along with the varied range of errors and not thinkable for a particular bookkeeper. In

this aspect the inherent risk may arise due to the overall nature of the business organisation of

DIPL (Duncan, B. and Whittington 2014).

The significant concerns towards the various types of the inherent risks has been

categorised as per environmental and material misstatements with the falsified exercises. The

environmental facets has been further seen to be directed towards the inherent risks and the swift

alterations in associated areas such as valuation of inventory, stiff competition in the market and

the shortage associated to the capital (Eilifsen et al. 2013).

Inherent risk Reason for risk to be inherent Risk of material misstatement

Incorrect interpretation

resulting from pressure of

management and stakeholders.

As per the given case, it can be

ascertained that the various types

of the transactions has been

particularly based on the

management of the DIPL

corporation. Although it can be

seen that the direct leads for the

Moreover, some of the inherent

risks attributable to DIPL also

resulted from improper recording

of cash receipts by the financial

professionals of organization. A

proper sequence is required to be

followed by the staff members

5AUDIT ASSURANCE AND COMPLIANCE

inconsistencies can be ineffectual

for the planning of the marketing

and the sales activities. In

addition to this, the various types

of the financial declarations will

be able to accomplish the

preferred profit level and

revenues generated from sales.

The failure of the management in

the firm has been further seen to

be based on the various types of

consideration related to the

specific requirements and

consequent adjustment of the

functionalities in the corporation.

It can be concluded that the

business organization has

experienced several failures due

to the different types of the micro

and the macroeconomic facets,

which may help in the existence

of the economic, social and the

political factors. The sales figure

has subsequently reflected the

sales figure and the diverse

nature of the inherent risks

and accountants of organization

for recording of the accounts

receivable. It is also essential on

their parts to have proper

maintenance of accounts

receivable ledger. There are

complexities involved in the

recoding and maintaining the

accounts and therefore, the bank

reconciliation statements of DIPL

should be properly recorded.

There can be diverse risks to

DIPL resulting from improper

registration of revenue generated

from e book and recording of the

accounts concerning reprinting of

books (Kumar and Sharma

2015). Furthermore, the valuation

process involves in the balancing

the inventories was also not

proper.

inconsistencies can be ineffectual

for the planning of the marketing

and the sales activities. In

addition to this, the various types

of the financial declarations will

be able to accomplish the

preferred profit level and

revenues generated from sales.

The failure of the management in

the firm has been further seen to

be based on the various types of

consideration related to the

specific requirements and

consequent adjustment of the

functionalities in the corporation.

It can be concluded that the

business organization has

experienced several failures due

to the different types of the micro

and the macroeconomic facets,

which may help in the existence

of the economic, social and the

political factors. The sales figure

has subsequently reflected the

sales figure and the diverse

nature of the inherent risks

and accountants of organization

for recording of the accounts

receivable. It is also essential on

their parts to have proper

maintenance of accounts

receivable ledger. There are

complexities involved in the

recoding and maintaining the

accounts and therefore, the bank

reconciliation statements of DIPL

should be properly recorded.

There can be diverse risks to

DIPL resulting from improper

registration of revenue generated

from e book and recording of the

accounts concerning reprinting of

books (Kumar and Sharma

2015). Furthermore, the valuation

process involves in the balancing

the inventories was also not

proper.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT ASSURANCE AND COMPLIANCE

(Louwers et al. 2015).

Succession of CEO procedure Another inherent risk faced by

DIPL is the procedure that is

involved in succession of CEO as

it is difficult and very complex.

Risks are also associated with the

quality of procedures involved in

succeeding CEO and the

procedures of succeeding CEO.

Some of the facets that would

leave the company at inherent

risks are delaying the process of

succession, does not complying

with the strategy while initiating

the process along with departing

some of the candidates that

would lead to some risks

(Malyshkin 2013).

The different types of the

workers of the DIPL have

escalated the overall risks

inherent with it. Because of the

lack of the proficiency of the

employees the inherent risk of

the corporations has been also

increased to a subsequent level.

This has been mainly observed

competency level of the members

of the staff and the business

concerns. It has been further

determined that the non-

proficient workforces may also

make enhancements in the

inherent risks who are bound to

make mistakes for the errors in

the exclusion and the misstated

pecuniary announcements

(Beasley 2015).

(Louwers et al. 2015).

Succession of CEO procedure Another inherent risk faced by

DIPL is the procedure that is

involved in succession of CEO as

it is difficult and very complex.

Risks are also associated with the

quality of procedures involved in

succeeding CEO and the

procedures of succeeding CEO.

Some of the facets that would

leave the company at inherent

risks are delaying the process of

succession, does not complying

with the strategy while initiating

the process along with departing

some of the candidates that

would lead to some risks

(Malyshkin 2013).

The different types of the

workers of the DIPL have

escalated the overall risks

inherent with it. Because of the

lack of the proficiency of the

employees the inherent risk of

the corporations has been also

increased to a subsequent level.

This has been mainly observed

competency level of the members

of the staff and the business

concerns. It has been further

determined that the non-

proficient workforces may also

make enhancements in the

inherent risks who are bound to

make mistakes for the errors in

the exclusion and the misstated

pecuniary announcements

(Beasley 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT ASSURANCE AND COMPLIANCE

After the evaluation of the given case study, it was ascertained that some

of the issues are also involved in the implementation of the novel IT system. DIPL suffered

shortage of employees and several issues were faced while the execution of process. Testing of

the system, its installation and reconciliation was not done with the required number of staffs.

Some of the transactions of organization were not properly apportioned that was ascertained

during the process of initial testing. Therefore, there was some omissions of the particular

financial declarations and some of the material misstatements resulting from the inappropriate

recording of the transactions and thereby leading to the leading to some sort of inherent risks.

Answer to Question 3:

Explanation and identification of two fraud risks arising from fraudulent financial

reporting:

Fraud risks are attributable to organization from various facets such as employees

workloads, meeting the needs of stakeholders particularly shareholders. An organization can face

high level of fraud risks because of management pressure to attain specific level of performance

for meeting the needs of investors. In order to prevent the generation of guarantees, employees

have strong pressure from specific financial results.

Types of fraud risks Impact of identified risks in conducting audit

fraudulent financial reporting There can be risk that arise from risk of fraudulent

financial reporting. Outside financiers or investors

pressurize the organization for declaring the

particular financial results and from management to

meet specific financial goals. The credit rating

agencies also requires organization to maintain

After the evaluation of the given case study, it was ascertained that some

of the issues are also involved in the implementation of the novel IT system. DIPL suffered

shortage of employees and several issues were faced while the execution of process. Testing of

the system, its installation and reconciliation was not done with the required number of staffs.

Some of the transactions of organization were not properly apportioned that was ascertained

during the process of initial testing. Therefore, there was some omissions of the particular

financial declarations and some of the material misstatements resulting from the inappropriate

recording of the transactions and thereby leading to the leading to some sort of inherent risks.

Answer to Question 3:

Explanation and identification of two fraud risks arising from fraudulent financial

reporting:

Fraud risks are attributable to organization from various facets such as employees

workloads, meeting the needs of stakeholders particularly shareholders. An organization can face

high level of fraud risks because of management pressure to attain specific level of performance

for meeting the needs of investors. In order to prevent the generation of guarantees, employees

have strong pressure from specific financial results.

Types of fraud risks Impact of identified risks in conducting audit

fraudulent financial reporting There can be risk that arise from risk of fraudulent

financial reporting. Outside financiers or investors

pressurize the organization for declaring the

particular financial results and from management to

meet specific financial goals. The credit rating

agencies also requires organization to maintain

8AUDIT ASSURANCE AND COMPLIANCE

particular level of ratio in order to enable them

granting the loan or debt amount (Davidson et al.

2013). In all these events, high amount of fraud

risks can arise in organization when the employees

are not able to maintain the required financial

balance. It can be observed from the case study that

the revenue of DIPL has increased over the year

from 2013 to 2015. Moreover, net profit and gross

profit also witnessed from the case study. There has

also been escalation in the total value of assets and

liabilities.

DIPL has also obtained loan amount of

7.5million from BDO finance and the acquisition of

loan amount comes with certain types of

agreement. This type of agreement might be related

to the maintenance of solvency ratio at the

particular level. Debt ratio of DIPL should be

maintained within the value one and current ratio

should be around `1.5. It is indicative of the fact

that this particular type of financial requirement by

creditors and credit agencies would pressurize the

organization to maintain certain types of financial

agreement for acquiring the required amount of

loans. Organization might be involved in improper

projections of the financial information’s and this

particular level of ratio in order to enable them

granting the loan or debt amount (Davidson et al.

2013). In all these events, high amount of fraud

risks can arise in organization when the employees

are not able to maintain the required financial

balance. It can be observed from the case study that

the revenue of DIPL has increased over the year

from 2013 to 2015. Moreover, net profit and gross

profit also witnessed from the case study. There has

also been escalation in the total value of assets and

liabilities.

DIPL has also obtained loan amount of

7.5million from BDO finance and the acquisition of

loan amount comes with certain types of

agreement. This type of agreement might be related

to the maintenance of solvency ratio at the

particular level. Debt ratio of DIPL should be

maintained within the value one and current ratio

should be around `1.5. It is indicative of the fact

that this particular type of financial requirement by

creditors and credit agencies would pressurize the

organization to maintain certain types of financial

agreement for acquiring the required amount of

loans. Organization might be involved in improper

projections of the financial information’s and this

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT ASSURANCE AND COMPLIANCE

would results from fraudulent activities (Davidson

et al. 2013).

Workers getting engaged in fraud activities Another fraud risks that can arise in DIPL is

engagement of workers in the fraudulent activities

resulting from their dissatisfaction. It has been

ascertained from the case study that acquisition of

novel accounting system has put huge pressure on

employees as they have lack of knowledge

concerning some technicalities and they are

required to work beyond their working hours.

Fraud might arise from the issues faced by workers

during the process of installation of the system.

This would results from material misstatements as

the reconciliation of the accounts would also be

done in improper way. Certain transactions at the

end of year was not properly allocated resulting

from the inappropriate execution and handling of

the new accounting system (Duncan and

Whittington 2014).

would results from fraudulent activities (Davidson

et al. 2013).

Workers getting engaged in fraud activities Another fraud risks that can arise in DIPL is

engagement of workers in the fraudulent activities

resulting from their dissatisfaction. It has been

ascertained from the case study that acquisition of

novel accounting system has put huge pressure on

employees as they have lack of knowledge

concerning some technicalities and they are

required to work beyond their working hours.

Fraud might arise from the issues faced by workers

during the process of installation of the system.

This would results from material misstatements as

the reconciliation of the accounts would also be

done in improper way. Certain transactions at the

end of year was not properly allocated resulting

from the inappropriate execution and handling of

the new accounting system (Duncan and

Whittington 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT ASSURANCE AND COMPLIANCE

Impact of fraud risks on audit plan:

The process of valuation of raw material inventories of DIPL was not appropriate and this

was investigated because of high average costs. It is required by auditors to monitor different

activities at different times during the installation of the novel accounting system. Evaluation of

the financial statements and monitoring of the control mechanism of DIPL from different time

would help in detecting the risks that is associated with the financial reporting (Hayes et al.

2014).

Impact of fraud risks on audit plan:

The process of valuation of raw material inventories of DIPL was not appropriate and this

was investigated because of high average costs. It is required by auditors to monitor different

activities at different times during the installation of the novel accounting system. Evaluation of

the financial statements and monitoring of the control mechanism of DIPL from different time

would help in detecting the risks that is associated with the financial reporting (Hayes et al.

2014).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.