Audit & Assurance: Detailed Financial Analysis of DIPL Limited

VerifiedAdded on 2023/06/13

|9

|2808

|109

Report

AI Summary

This assignment provides a detailed analysis of DIPL Limited's financial statements, focusing on audit and assurance principles. It begins by utilizing analytical approaches such as trend analysis and ratio formulation to assess the company's financial health and identify potential issues. The report highlights concerns such as discrepancies between sales and stock figures, increasing debt, and declining cash balances. Furthermore, it identifies inherent and fraud risks within the company, including immoral appointment standards and incorrect record-keeping of accounts receivable. The assignment also explores how these risks can influence the preliminary audit figures and the auditor's opinion. The analysis emphasizes the importance of substantive audit procedures and strong analytical skills to provide an independent and accurate assessment of DIPL Limited's financial condition, noting that a fruitless audit report may arise from fraudulent factors and inaccurate financial measures.

qwertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

AUDIT & ASSURANCE

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

AUDIT & ASSURANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit DIPL

Answer 1

In the process of decision making, systematic methods may be helpful for an organization or

firm for the purpose of auditing and management. This just doesn’t improve the financial

aspects of the firm but also helps the nonfinancial aspects of the firm to overcome the faults

and grow. The case provided by DIPL Limited also the methods of analytical approaches

have been utilized to apex the real potential of the firm and also it helped the top level

management to make decisions. If there is by any chance any misinterpretation of the

financial statements, these processes can be taken into power to mend the false or incorrect

results (Elder et. al, 2010). Therefore it is also found that many of the organizations also use

these types of methods in order to achieve the desired objectives as it make it easier for the

firm to approach its goals.

The first ever operation conducted on the firm DIPL limited is the trend analysis. In this

process, a firm tries to find the contrast between the financial statements of the current year to

that of the past. This helps the firm to find the variations in the data and thus helping to

improve the process of decision making. Therefore it can be said that trends and patterns help

in the decision-making process of the firm and also they may help to raise the future concerns

and complication for which the firm should be ready with a rescue plan. According to the

financial statements of the firm DIPL limited, it can be clearly understood that the sale

figures are rising higher which lead to revenue generation, thus creating a positive impact for

the firm’s financial position. It should also be noticed that even the sales figures being high,

the difference between underlying stocks of company and sales is huge which is not normal

and thus becoming a matter of concern for the firm (Coram et. al, 2011). The figure of the

stocks does not give the firm a positive environment thus it should be evaluated by the

auditor as the trend followed by the financial statements of sales and stock are not in a

scrupulous manner.

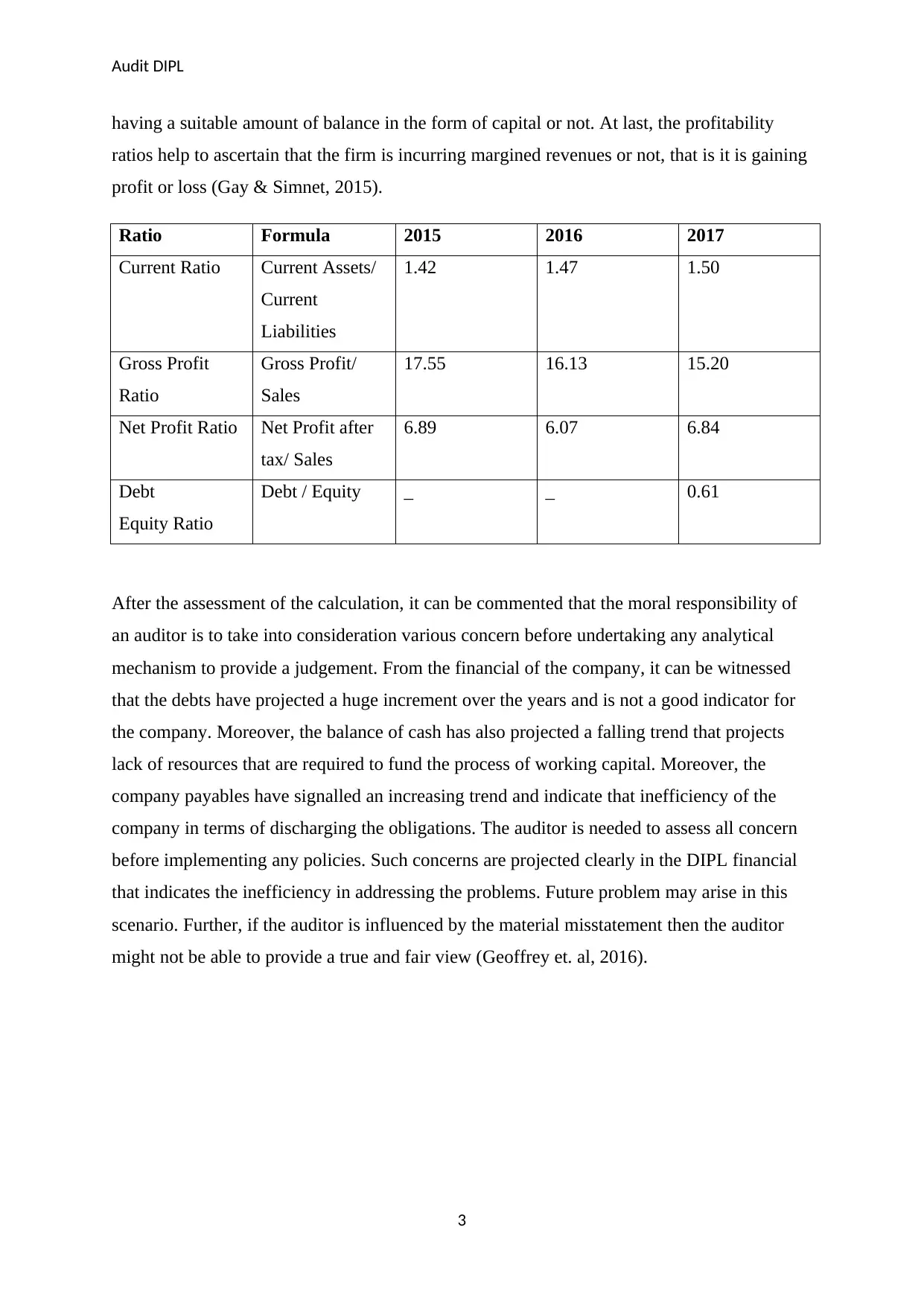

The second process consists of the formulation of the ratios which has been conducted in

order to find the true financial condition of the firm. Many ratios can be calculated for

achieving the desired results and also be compared to the last year’s figures which may be

helpful in ascertaining the true condition of the firm. The solvency, liquidity and profitability

ratios of the firm DIPL limited may be proved to be helpful for the trend and growth analysis.

Liquidity ratios are calculated to find the liquid position of the firm, i.e. to find that the firm

will be able to clear its credit balances or not. Solvency ratios help to calculate if the firm is

2

Answer 1

In the process of decision making, systematic methods may be helpful for an organization or

firm for the purpose of auditing and management. This just doesn’t improve the financial

aspects of the firm but also helps the nonfinancial aspects of the firm to overcome the faults

and grow. The case provided by DIPL Limited also the methods of analytical approaches

have been utilized to apex the real potential of the firm and also it helped the top level

management to make decisions. If there is by any chance any misinterpretation of the

financial statements, these processes can be taken into power to mend the false or incorrect

results (Elder et. al, 2010). Therefore it is also found that many of the organizations also use

these types of methods in order to achieve the desired objectives as it make it easier for the

firm to approach its goals.

The first ever operation conducted on the firm DIPL limited is the trend analysis. In this

process, a firm tries to find the contrast between the financial statements of the current year to

that of the past. This helps the firm to find the variations in the data and thus helping to

improve the process of decision making. Therefore it can be said that trends and patterns help

in the decision-making process of the firm and also they may help to raise the future concerns

and complication for which the firm should be ready with a rescue plan. According to the

financial statements of the firm DIPL limited, it can be clearly understood that the sale

figures are rising higher which lead to revenue generation, thus creating a positive impact for

the firm’s financial position. It should also be noticed that even the sales figures being high,

the difference between underlying stocks of company and sales is huge which is not normal

and thus becoming a matter of concern for the firm (Coram et. al, 2011). The figure of the

stocks does not give the firm a positive environment thus it should be evaluated by the

auditor as the trend followed by the financial statements of sales and stock are not in a

scrupulous manner.

The second process consists of the formulation of the ratios which has been conducted in

order to find the true financial condition of the firm. Many ratios can be calculated for

achieving the desired results and also be compared to the last year’s figures which may be

helpful in ascertaining the true condition of the firm. The solvency, liquidity and profitability

ratios of the firm DIPL limited may be proved to be helpful for the trend and growth analysis.

Liquidity ratios are calculated to find the liquid position of the firm, i.e. to find that the firm

will be able to clear its credit balances or not. Solvency ratios help to calculate if the firm is

2

Audit DIPL

having a suitable amount of balance in the form of capital or not. At last, the profitability

ratios help to ascertain that the firm is incurring margined revenues or not, that is it is gaining

profit or loss (Gay & Simnet, 2015).

Ratio Formula 2015 2016 2017

Current Ratio Current Assets/

Current

Liabilities

1.42 1.47 1.50

Gross Profit

Ratio

Gross Profit/

Sales

17.55 16.13 15.20

Net Profit Ratio Net Profit after

tax/ Sales

6.89 6.07 6.84

Debt

Equity Ratio

Debt / Equity _ _ 0.61

After the assessment of the calculation, it can be commented that the moral responsibility of

an auditor is to take into consideration various concern before undertaking any analytical

mechanism to provide a judgement. From the financial of the company, it can be witnessed

that the debts have projected a huge increment over the years and is not a good indicator for

the company. Moreover, the balance of cash has also projected a falling trend that projects

lack of resources that are required to fund the process of working capital. Moreover, the

company payables have signalled an increasing trend and indicate that inefficiency of the

company in terms of discharging the obligations. The auditor is needed to assess all concern

before implementing any policies. Such concerns are projected clearly in the DIPL financial

that indicates the inefficiency in addressing the problems. Future problem may arise in this

scenario. Further, if the auditor is influenced by the material misstatement then the auditor

might not be able to provide a true and fair view (Geoffrey et. al, 2016).

3

having a suitable amount of balance in the form of capital or not. At last, the profitability

ratios help to ascertain that the firm is incurring margined revenues or not, that is it is gaining

profit or loss (Gay & Simnet, 2015).

Ratio Formula 2015 2016 2017

Current Ratio Current Assets/

Current

Liabilities

1.42 1.47 1.50

Gross Profit

Ratio

Gross Profit/

Sales

17.55 16.13 15.20

Net Profit Ratio Net Profit after

tax/ Sales

6.89 6.07 6.84

Debt

Equity Ratio

Debt / Equity _ _ 0.61

After the assessment of the calculation, it can be commented that the moral responsibility of

an auditor is to take into consideration various concern before undertaking any analytical

mechanism to provide a judgement. From the financial of the company, it can be witnessed

that the debts have projected a huge increment over the years and is not a good indicator for

the company. Moreover, the balance of cash has also projected a falling trend that projects

lack of resources that are required to fund the process of working capital. Moreover, the

company payables have signalled an increasing trend and indicate that inefficiency of the

company in terms of discharging the obligations. The auditor is needed to assess all concern

before implementing any policies. Such concerns are projected clearly in the DIPL financial

that indicates the inefficiency in addressing the problems. Future problem may arise in this

scenario. Further, if the auditor is influenced by the material misstatement then the auditor

might not be able to provide a true and fair view (Geoffrey et. al, 2016).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit DIPL

Answer 2

a. Determination of preliminary figures

Inherent risks are the types of risks which are not easy to get rid off as they are mostly

present in the financial system of the firm. These types of risks are also not even under the

control of the internal control policies or the audit processes because these risks are not

caused by the material misstatements or error, they are caused because of internal

malfunctions prevailing in the financials of a firm (Heeler, 2009). The risks prevailing in the

DIPL limited firm are:

1. Immoral appointment standards: While the appointment of a new executive in the firm, it

should be taken into consideration that the person is having no means of bad interest for the

firm and also he is ready for undertaking the responsibility of his position. Thus, when the

appointment of the CEO of the firm DIPL limited is conducted, it should be checked that the

person holding the post has no self-financial interest with the financial terms of the company

(Hoffelder, 2012). Whatsoever, it has already been noticed that the CEO of the firm was

trying to obtain 10 percent more profits over his current 10 percent share of profits in its

operations. This is one of the biggest dangers for the company because the top management

structure has the power to manipulate the rules and conditions of the business and as the CEO

is part of the top management structure, he may change his share of profits without the

agreement of the firm’s financial position (Carcello, 2012). The ECO of the firm may also

have changed the values in the financial statements of the firm in such a manner which may

help his to earn more interest and therefore increasing his share of profit unknowingly.

2. Incorrect record of accounts receivable: The cashier of the firm have the task of

recording all the transactions related to the money received on a regular day to day basis

which he records in the financial statement using the mails he has received in the past. This

states that the value recorded by the cashier is the value of the cheque, draft or cash which the

debtor sent through the mail. This shows that there is no mechanism present in the company

relating to the adjustments of the cheque receivable and the encashment of the cheques. Also

it have been noticed that the reconciling of the bank statements is done by another official

which lets us to the fact that there is no systematic procedure of work being followed in the

firm and this may further result in the vast differences in the financial statement of the

4

Answer 2

a. Determination of preliminary figures

Inherent risks are the types of risks which are not easy to get rid off as they are mostly

present in the financial system of the firm. These types of risks are also not even under the

control of the internal control policies or the audit processes because these risks are not

caused by the material misstatements or error, they are caused because of internal

malfunctions prevailing in the financials of a firm (Heeler, 2009). The risks prevailing in the

DIPL limited firm are:

1. Immoral appointment standards: While the appointment of a new executive in the firm, it

should be taken into consideration that the person is having no means of bad interest for the

firm and also he is ready for undertaking the responsibility of his position. Thus, when the

appointment of the CEO of the firm DIPL limited is conducted, it should be checked that the

person holding the post has no self-financial interest with the financial terms of the company

(Hoffelder, 2012). Whatsoever, it has already been noticed that the CEO of the firm was

trying to obtain 10 percent more profits over his current 10 percent share of profits in its

operations. This is one of the biggest dangers for the company because the top management

structure has the power to manipulate the rules and conditions of the business and as the CEO

is part of the top management structure, he may change his share of profits without the

agreement of the firm’s financial position (Carcello, 2012). The ECO of the firm may also

have changed the values in the financial statements of the firm in such a manner which may

help his to earn more interest and therefore increasing his share of profit unknowingly.

2. Incorrect record of accounts receivable: The cashier of the firm have the task of

recording all the transactions related to the money received on a regular day to day basis

which he records in the financial statement using the mails he has received in the past. This

states that the value recorded by the cashier is the value of the cheque, draft or cash which the

debtor sent through the mail. This shows that there is no mechanism present in the company

relating to the adjustments of the cheque receivable and the encashment of the cheques. Also

it have been noticed that the reconciling of the bank statements is done by another official

which lets us to the fact that there is no systematic procedure of work being followed in the

firm and this may further result in the vast differences in the financial statement of the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit DIPL

company which may misguide the auditors during the time of auditing and thus make them

pursue wrong judgements. Hence the issues should be cordially analyzed and then make

further judgments (Holland & Lane, 2012).

These two risk may cause massive destruction in the firm’s financial position thus letting the

downfall as it may not only change the financial position of the firm but it may also misguide

the auditors leading to the poor profit figures which have been obtained by fraudulent

measures (Merchant, 2012).

Answer 2(b)

Identification of the factors

Fraud risks are the risks that prevail inside the firm’s financial condition which may have

been caused because of the fraud measures of the management of any other officials. The

main fraud risks that may prevail in the case of DIPL limited are:

1. Inventory valuation: After analyzing the financial information, it is seen that the sales

have increased but it is not appropriate that the stock turnover has not depicted a downward

trend. This may be a huge factor of risk for the company as there may have been

manipulation in the management or accounts which have to lead to the inaccurate increase in

the inventory turnover (Cappelleto, 2010).

2. Mail revenue recognition: The Company may face problems because the cashier uses

mails to check the encashment of the cheques. The reason for the risk is that there is no prior

information which can be used to match the values of the cheque and the bank statement. The

officials may manipulate the data thus committing a fraud with the firm which may not be

recognized by it. The officials of the company may not report the actual resources of the

company and thus credit the same personal account (Kaplan, 2011). This will not only result

in the degradation of firm’s financial condition but it will also lead to the damage of firm’s

reputation. Hence a proper reconciliation system and a trusted official must be appointed in

order to check this fraud which will not only help the firm to have strong governance over its

employees but also it will help to create transparency of the financial transaction (Black,

2010).

5

company which may misguide the auditors during the time of auditing and thus make them

pursue wrong judgements. Hence the issues should be cordially analyzed and then make

further judgments (Holland & Lane, 2012).

These two risk may cause massive destruction in the firm’s financial position thus letting the

downfall as it may not only change the financial position of the firm but it may also misguide

the auditors leading to the poor profit figures which have been obtained by fraudulent

measures (Merchant, 2012).

Answer 2(b)

Identification of the factors

Fraud risks are the risks that prevail inside the firm’s financial condition which may have

been caused because of the fraud measures of the management of any other officials. The

main fraud risks that may prevail in the case of DIPL limited are:

1. Inventory valuation: After analyzing the financial information, it is seen that the sales

have increased but it is not appropriate that the stock turnover has not depicted a downward

trend. This may be a huge factor of risk for the company as there may have been

manipulation in the management or accounts which have to lead to the inaccurate increase in

the inventory turnover (Cappelleto, 2010).

2. Mail revenue recognition: The Company may face problems because the cashier uses

mails to check the encashment of the cheques. The reason for the risk is that there is no prior

information which can be used to match the values of the cheque and the bank statement. The

officials may manipulate the data thus committing a fraud with the firm which may not be

recognized by it. The officials of the company may not report the actual resources of the

company and thus credit the same personal account (Kaplan, 2011). This will not only result

in the degradation of firm’s financial condition but it will also lead to the damage of firm’s

reputation. Hence a proper reconciliation system and a trusted official must be appointed in

order to check this fraud which will not only help the firm to have strong governance over its

employees but also it will help to create transparency of the financial transaction (Black,

2010).

5

Audit DIPL

Therefore it should be duly noted that these two above mentioned risks are kept in mind and

tried to be corrected as soon as possible otherwise the business may suffer great loss in future

because of the incompetent employees and the deteriorated finance system (Livne, 2015).

This may also result in the auditor’s mishandling of the reports thus leading to a bad opinion

of the auditor for the firm.

Answer 2(c)

Influence on the preliminary figure

A fruitless audit report may be created if there are too many fraudulent factors prevailing

inside a business firm. Fraud measures affect the audit process directly thus leading to the

manipulation of the auditor's opinion by the inaccurate and inattentive financial measures of

the firm. The above-mentioned risks should be formerly taken into light and measures should

be taken to remove present risks as they create a dissentious impact over the firm’s financial

condition which may have been made in order to earn maximum revenues or good reputation

(Ruhnke & Schmidt, 2014). Because of the prevailing problem with the recording of the trade

receivables, the auditor may leave with a bad concern of the financial position of the firm

thus calling the financial statements of the firm to be false (Niemi & Sundgren, 2012). This

will be caused because the auditor would have noticed that the transactions entered in the

statements are in the wrong period or the transactions are not verified which may lead to the

claim of false statements (Manoharan, 2011). If there is no sufficient information available

about the fraudulent activities then the auditor cannot report or make any bad opinion about

the firm whereas if he will notice any difference or malpractice of the firm then he may

question the same and make a bad opinion about the firm’s financial condition (Roach, 2010).

The inventory valuation system of the firm was also inappropriate and this may result to

attract the auditor’s attention towards it. It may happen that the values of the inventories have

been changed by the officials in order to steal the goods which may result in the auditor’s

unsatisfactory opinion (Merchant, 2012). Thus because of such prevailing fraudulent

measures, an auditor must always be attentive and he must use his best skills while

conducting the audit process for a firm.

From the computation below, it can be commented that the auditor needs to be substantive in

nature with a strong eye on analytical skills because the auditor needs to provide an

independent opinion. Moreover, there is no regulation that can stop the auditor from

conducting an audit and following the proper mechanism.

6

Therefore it should be duly noted that these two above mentioned risks are kept in mind and

tried to be corrected as soon as possible otherwise the business may suffer great loss in future

because of the incompetent employees and the deteriorated finance system (Livne, 2015).

This may also result in the auditor’s mishandling of the reports thus leading to a bad opinion

of the auditor for the firm.

Answer 2(c)

Influence on the preliminary figure

A fruitless audit report may be created if there are too many fraudulent factors prevailing

inside a business firm. Fraud measures affect the audit process directly thus leading to the

manipulation of the auditor's opinion by the inaccurate and inattentive financial measures of

the firm. The above-mentioned risks should be formerly taken into light and measures should

be taken to remove present risks as they create a dissentious impact over the firm’s financial

condition which may have been made in order to earn maximum revenues or good reputation

(Ruhnke & Schmidt, 2014). Because of the prevailing problem with the recording of the trade

receivables, the auditor may leave with a bad concern of the financial position of the firm

thus calling the financial statements of the firm to be false (Niemi & Sundgren, 2012). This

will be caused because the auditor would have noticed that the transactions entered in the

statements are in the wrong period or the transactions are not verified which may lead to the

claim of false statements (Manoharan, 2011). If there is no sufficient information available

about the fraudulent activities then the auditor cannot report or make any bad opinion about

the firm whereas if he will notice any difference or malpractice of the firm then he may

question the same and make a bad opinion about the firm’s financial condition (Roach, 2010).

The inventory valuation system of the firm was also inappropriate and this may result to

attract the auditor’s attention towards it. It may happen that the values of the inventories have

been changed by the officials in order to steal the goods which may result in the auditor’s

unsatisfactory opinion (Merchant, 2012). Thus because of such prevailing fraudulent

measures, an auditor must always be attentive and he must use his best skills while

conducting the audit process for a firm.

From the computation below, it can be commented that the auditor needs to be substantive in

nature with a strong eye on analytical skills because the auditor needs to provide an

independent opinion. Moreover, there is no regulation that can stop the auditor from

conducting an audit and following the proper mechanism.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit DIPL

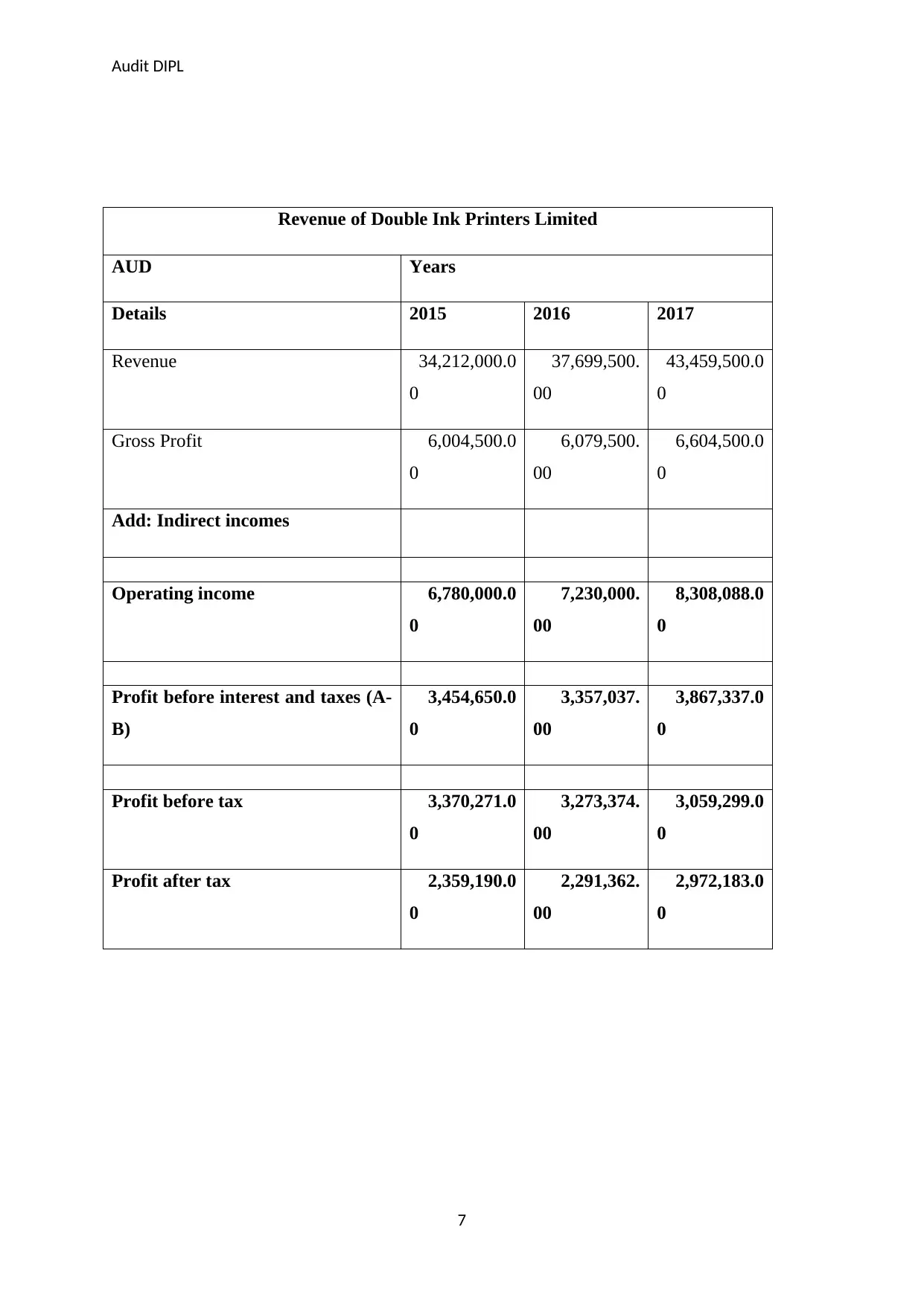

Revenue of Double Ink Printers Limited

AUD Years

Details 2015 2016 2017

Revenue 34,212,000.0

0

37,699,500.

00

43,459,500.0

0

Gross Profit 6,004,500.0

0

6,079,500.

00

6,604,500.0

0

Add: Indirect incomes

Operating income 6,780,000.0

0

7,230,000.

00

8,308,088.0

0

Profit before interest and taxes (A-

B)

3,454,650.0

0

3,357,037.

00

3,867,337.0

0

Profit before tax 3,370,271.0

0

3,273,374.

00

3,059,299.0

0

Profit after tax 2,359,190.0

0

2,291,362.

00

2,972,183.0

0

7

Revenue of Double Ink Printers Limited

AUD Years

Details 2015 2016 2017

Revenue 34,212,000.0

0

37,699,500.

00

43,459,500.0

0

Gross Profit 6,004,500.0

0

6,079,500.

00

6,604,500.0

0

Add: Indirect incomes

Operating income 6,780,000.0

0

7,230,000.

00

8,308,088.0

0

Profit before interest and taxes (A-

B)

3,454,650.0

0

3,357,037.

00

3,867,337.0

0

Profit before tax 3,370,271.0

0

3,273,374.

00

3,059,299.0

0

Profit after tax 2,359,190.0

0

2,291,362.

00

2,972,183.0

0

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit DIPL

References

Black, W. K. (2010). Epidemics of “Control Fraud” lead to Recurrent, Intensifying Bubbles

and Crises. Working paper, University of Missouri-Kansas City.

Cappelleto, G. (2010) Challenges Facing Accounting Education in Australia. AFAANZ,

Carcello, J. (2012). What do investors want from the standard audit report?. CPA Journal,

82(1), 7-12. http://dx.doi.org/10.2139/ssrn.2930375

Coram, P., Mock, T. J., Turner, J., and Gray, G. (2011). The communicative value of the

auditor’s report. Australian Accounting Review, 21(3), 235-252.

https://doi.org/10.1111/j.1835-2561.2011.00140.x

Elder, J. R., Beasley S. M., and Arens A. A. (2010). Auditing and Assurance Services. Person

Education, New Jersey: USA

Gay, G., and Simnet, R. (2015). Auditing and Assurance Services. McGraw Hill

Geoffrey D. B., Joleen K., K. K.S., and David A. W. (2016). Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors.

Accounting Horizons, 30(1), 143-156. https://doi.org/10.2308/acch-51309

Heeler, D. (2009). Audit Principles, Risk Assessment & Effective Reporting. Pearson Press

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Holland., K. & Lane, J. (2012). Perceived auditor independence and audit firm fees.

Accounting and Business Research, 42(2), 115-141. https://doi.org/10.2308/accr-10217

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383.

https://doi.org/10.2308/accr.00000031

Livne, G. (2015, May 12). Threats to Auditor Independence and Possible Remedies. Retrieved

from: http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Livne, G. (2015, May 12). Threats to Auditor Independence and Possible Remedies.

Retrieved from: http://www.financepractitioner.com/auditing-best-practice/threats-to-

auditor-independence-and-possible-remedies?full

8

References

Black, W. K. (2010). Epidemics of “Control Fraud” lead to Recurrent, Intensifying Bubbles

and Crises. Working paper, University of Missouri-Kansas City.

Cappelleto, G. (2010) Challenges Facing Accounting Education in Australia. AFAANZ,

Carcello, J. (2012). What do investors want from the standard audit report?. CPA Journal,

82(1), 7-12. http://dx.doi.org/10.2139/ssrn.2930375

Coram, P., Mock, T. J., Turner, J., and Gray, G. (2011). The communicative value of the

auditor’s report. Australian Accounting Review, 21(3), 235-252.

https://doi.org/10.1111/j.1835-2561.2011.00140.x

Elder, J. R., Beasley S. M., and Arens A. A. (2010). Auditing and Assurance Services. Person

Education, New Jersey: USA

Gay, G., and Simnet, R. (2015). Auditing and Assurance Services. McGraw Hill

Geoffrey D. B., Joleen K., K. K.S., and David A. W. (2016). Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors.

Accounting Horizons, 30(1), 143-156. https://doi.org/10.2308/acch-51309

Heeler, D. (2009). Audit Principles, Risk Assessment & Effective Reporting. Pearson Press

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Holland., K. & Lane, J. (2012). Perceived auditor independence and audit firm fees.

Accounting and Business Research, 42(2), 115-141. https://doi.org/10.2308/accr-10217

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383.

https://doi.org/10.2308/accr.00000031

Livne, G. (2015, May 12). Threats to Auditor Independence and Possible Remedies. Retrieved

from: http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Livne, G. (2015, May 12). Threats to Auditor Independence and Possible Remedies.

Retrieved from: http://www.financepractitioner.com/auditing-best-practice/threats-to-

auditor-independence-and-possible-remedies?full

8

Audit DIPL

Manoharan, T.N. (2011). Financial Statement Fraud and Corporate Governance. The

George Washington University.

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. https://doi.org/10.1108/01140581211283904

Niemi, L., and Sundgren, S. (2012). Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review, 21(4), 767-796.

https://doi.org/10.1080/09638180.2012.671465

Roach, L. (2010). Auditor Liability: Liability Limitation Agreements. Pearson.

Ruhnke, K., and Schmidt, M. (2014). The audit expectation gap: existence, causes, and the

impact of changes. Accounting and Business Research 44(5), 572-601.

https://doi.org/10.1080/00014788.2014.929519

9

Manoharan, T.N. (2011). Financial Statement Fraud and Corporate Governance. The

George Washington University.

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. https://doi.org/10.1108/01140581211283904

Niemi, L., and Sundgren, S. (2012). Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review, 21(4), 767-796.

https://doi.org/10.1080/09638180.2012.671465

Roach, L. (2010). Auditor Liability: Liability Limitation Agreements. Pearson.

Ruhnke, K., and Schmidt, M. (2014). The audit expectation gap: existence, causes, and the

impact of changes. Accounting and Business Research 44(5), 572-601.

https://doi.org/10.1080/00014788.2014.929519

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.