Comprehensive Audit Report: Financial Analysis of DIPL Ltd

VerifiedAdded on 2020/03/04

|9

|2492

|68

Report

AI Summary

This report provides a comprehensive audit analysis of DIPL Ltd, covering various aspects of its financial performance and risk assessment. The report begins with an overview of analytical processes, including trend and ratio analysis, used to evaluate the company's financial statements. It then delves into the identification of inherent risks, such as those associated with the adoption of a new IT system and inaccurate treatment of accounts receivable, and their potential impact on the financial statements. Furthermore, the report addresses fraud risks related to the new IT system and revenue recognition processes. The report highlights the importance of internal controls, proper reconciliation procedures, and the auditor's role in identifying and mitigating these risks. The report emphasizes the need for corrective actions to ensure the accuracy and reliability of financial reporting, including the importance of auditors being familiar with the new system and the potential impact of management's decisions on the audit opinion.

AUDIT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

Answer to 1

Several analytical processes are being conducted in DIPL Ltd and for such purpose; various

kinds of ideas must be implemented. One of such processes is substantive process wherein

businesses can easily analyze the market pattern so that future course of action can be

anticipated. Auditors can also seek assistance from such process by identifying relevant evidence

so that the truthfulness and completeness of financial statements can be ascertained. In simple

words, material misstatements from the financial statements can be easily recognized with the

help of this procedure, thereby proving of great help in decision-making. Auditors in their

capacity can easily bring professionalism and expertise in the form of such procedures so that a

direct influence on business can be established (Church et. al, 2008). This is the reason why the

auditors must know prior knowledge of analytical processes.

In relation to DIPL Ltd, such processes can be easily implemented to ascertain the differences in

books of accounts. Trend analysis is one of such analytical processes wherein auditors can

determine the change in patterns over the business of the company in order to make relevant

decisions. Further, ratio analysis can also be used in such situation so that assistance in relation

to financial execution can be gained (Knapp, 2013). Hence, enabling the decision-making

process within companies can be easily guided with the help of control, examination, and

forecasting. Nevertheless, ratio analysis has been conducted in relation to DIPL Ltd so that

effective decisions can be made regarding its financial statements. For the purpose of such

evaluation, the computation of various ratios has been done for the period of three years (2013-

2015). Besides, ratios like solvency ratio, liquidity ratio, and profitability ratio have been focused

upon in order to anticipate the patterns in company’s business.

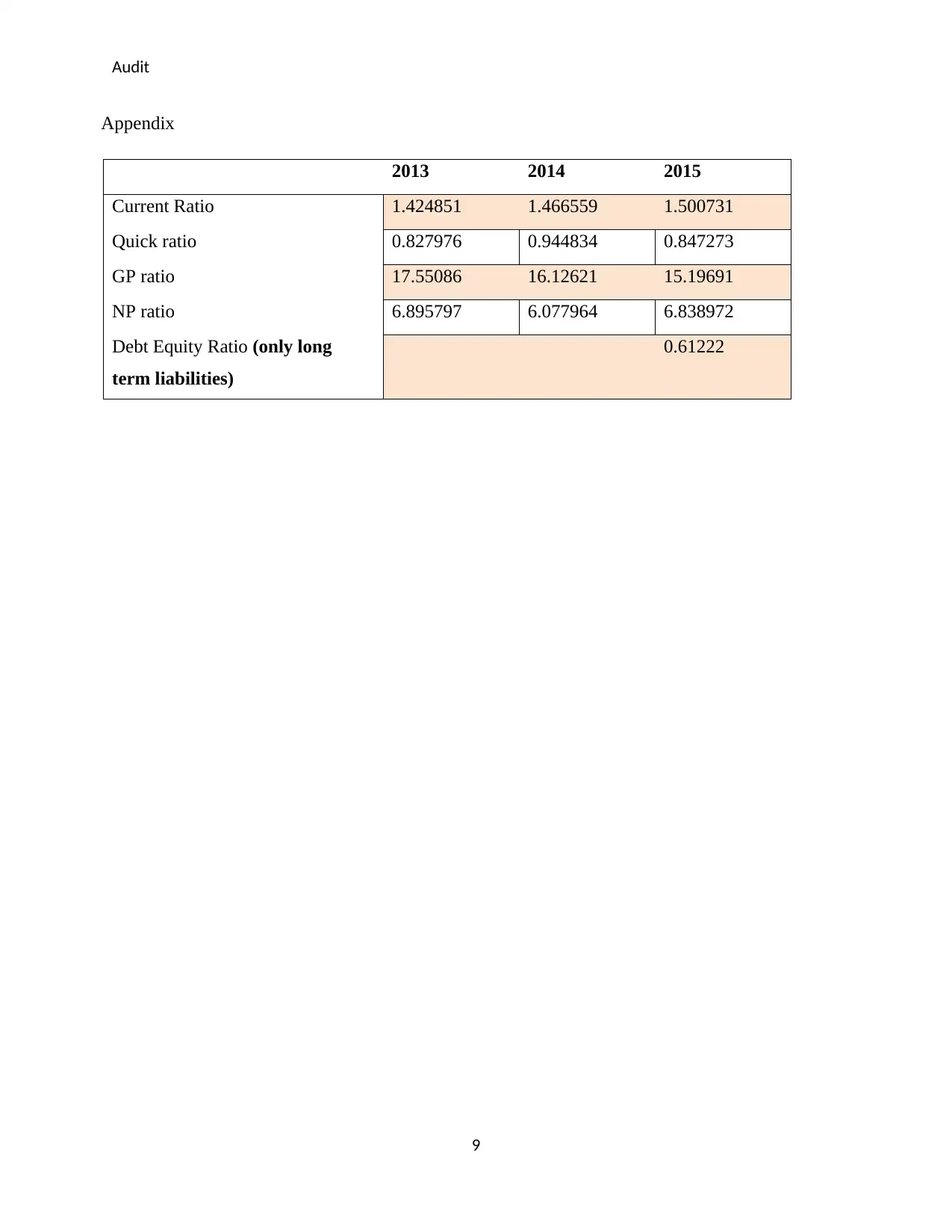

It can be witnessed from the financial information of DIPL Ltd that its current ratio has depicted

a consistent trend that means the company is having ample assets to repay all its debt obligations

in the future. In addition, the profitability ratio of DIPL has been presented through net profit and

gross profit ratios that denotes how much profitable the company is. Even though the company is

performing on a profitable segment over the period of three years, yet some declining trends can

be witnessed during such time. On one hand, while the net profit ratio of the company has

increased, similarly, on the other hand, its gross profit ratio has witnessed a declining trend over

these years. In order to obtain efficiency in such segments, the company must exert due focus on

2

Answer to 1

Several analytical processes are being conducted in DIPL Ltd and for such purpose; various

kinds of ideas must be implemented. One of such processes is substantive process wherein

businesses can easily analyze the market pattern so that future course of action can be

anticipated. Auditors can also seek assistance from such process by identifying relevant evidence

so that the truthfulness and completeness of financial statements can be ascertained. In simple

words, material misstatements from the financial statements can be easily recognized with the

help of this procedure, thereby proving of great help in decision-making. Auditors in their

capacity can easily bring professionalism and expertise in the form of such procedures so that a

direct influence on business can be established (Church et. al, 2008). This is the reason why the

auditors must know prior knowledge of analytical processes.

In relation to DIPL Ltd, such processes can be easily implemented to ascertain the differences in

books of accounts. Trend analysis is one of such analytical processes wherein auditors can

determine the change in patterns over the business of the company in order to make relevant

decisions. Further, ratio analysis can also be used in such situation so that assistance in relation

to financial execution can be gained (Knapp, 2013). Hence, enabling the decision-making

process within companies can be easily guided with the help of control, examination, and

forecasting. Nevertheless, ratio analysis has been conducted in relation to DIPL Ltd so that

effective decisions can be made regarding its financial statements. For the purpose of such

evaluation, the computation of various ratios has been done for the period of three years (2013-

2015). Besides, ratios like solvency ratio, liquidity ratio, and profitability ratio have been focused

upon in order to anticipate the patterns in company’s business.

It can be witnessed from the financial information of DIPL Ltd that its current ratio has depicted

a consistent trend that means the company is having ample assets to repay all its debt obligations

in the future. In addition, the profitability ratio of DIPL has been presented through net profit and

gross profit ratios that denotes how much profitable the company is. Even though the company is

performing on a profitable segment over the period of three years, yet some declining trends can

be witnessed during such time. On one hand, while the net profit ratio of the company has

increased, similarly, on the other hand, its gross profit ratio has witnessed a declining trend over

these years. In order to obtain efficiency in such segments, the company must exert due focus on

2

Audit

its costs so that the profitability area can be boosted taking into account the company’s revenues.

Further, it can be seen that the company has borrowed interest-bearing liabilities in the year 2015

and this is the reason why its debt-equity ratio reported at 0.61. Besides, the normal debt-equity

ratio stands at 0.50, which shows that the company has to expend huge resources for payment of

interests on such borrowings. Nevertheless, in the computation of debt-equity ratio, only long-

term liabilities have been taken into account. The long term liabilities have been considered

because the consideration is mainly on the long term loans. Such loans are used for a long term

purpose while the short ones are paid off within a year (Northington, 2011).

In addition to the above, there are some other concerns that must be taken into account. Firstly,

the cash balances of the company have significantly decreased that is a very negative aspect on

the part of the company. In addition, it can also be seen that the recovery process of the company

is very imperfect, as major resources are being blocked in its accounts receivables and therefore,

this must be immediately looked after by the company (Northington, 2011). Besides, an

enormous pile of inventories can also be seen in the financials of the company that generates

doubts whether improper activities have been conducted within the company or not. On a whole,

all these areas must be given due consideration by the company so that proper corrective actions

can be implemented to have a better long-term survival. Therefore, the flaws in the methods to

record the financial transaction will create obstacles for the auditor as there will be a requirement

of an in-depth analysis by the auditor. The auditor generally makes a strong observation but

relies on the data provided by the management (Lapsley, 2012). If the management makes grave

mistakes it will create impact on the auditor’s decision. The faulty planning and data will

influence the auditor to provide a decision that is different.

3

its costs so that the profitability area can be boosted taking into account the company’s revenues.

Further, it can be seen that the company has borrowed interest-bearing liabilities in the year 2015

and this is the reason why its debt-equity ratio reported at 0.61. Besides, the normal debt-equity

ratio stands at 0.50, which shows that the company has to expend huge resources for payment of

interests on such borrowings. Nevertheless, in the computation of debt-equity ratio, only long-

term liabilities have been taken into account. The long term liabilities have been considered

because the consideration is mainly on the long term loans. Such loans are used for a long term

purpose while the short ones are paid off within a year (Northington, 2011).

In addition to the above, there are some other concerns that must be taken into account. Firstly,

the cash balances of the company have significantly decreased that is a very negative aspect on

the part of the company. In addition, it can also be seen that the recovery process of the company

is very imperfect, as major resources are being blocked in its accounts receivables and therefore,

this must be immediately looked after by the company (Northington, 2011). Besides, an

enormous pile of inventories can also be seen in the financials of the company that generates

doubts whether improper activities have been conducted within the company or not. On a whole,

all these areas must be given due consideration by the company so that proper corrective actions

can be implemented to have a better long-term survival. Therefore, the flaws in the methods to

record the financial transaction will create obstacles for the auditor as there will be a requirement

of an in-depth analysis by the auditor. The auditor generally makes a strong observation but

relies on the data provided by the management (Lapsley, 2012). If the management makes grave

mistakes it will create impact on the auditor’s decision. The faulty planning and data will

influence the auditor to provide a decision that is different.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

Answer to 2

Inherent risks are the risks prevalent in a business organization irrespective of internal control

measures or audit processes. Such a risk is present in the system and is not due to any omission

or negligence. This is because a business is vulnerable to various internal and external factors in

order to survive in the competing environment. Besides, the key reason for the generation of

inherent risk is the prevalence of material misstatements in the financial statements. The inherent

risks present in the financials of DIPL Ltd are as follows:

a. Firstly, the company has decided to adopt a new IT system in its operations that are a

good step but the major problem associated with such step is the lack of proper

evaluation and research. The main reason for the adoption of the new system was to

simplify the recording of transactions but there were inaccuracies in its testing and

research before its installation. Since the management did not conduct effective steps

before adopting the system, many transactions failed to be properly allocated to their

right period (Roach, 2010). Hence, this is of a major issue because the transactions will

be reflected in different period. As a result, the profit amounts of the company were

either exaggerated or downgraded. Hence, such inappropriateness in the accounting

system can result in manipulation of accounts on the part of company officials, thereby

posing a big risk for the entire organization as a whole. When the officials are aware of

the loopholes then it provides them with the opportunity of making profit or taking

advantage. This ultimately tends to disturb the overall accounts and will impact the profit

or loss of the company.

b. Secondly, the officials of the company have done the treatment of accounts receivable in

an inaccurate way. The cashier takes the receipts attained from the debtors into account

on a regular basis but the recognition of the same is done through mail wherein the

debtors enclose the cheques. In contrast to this, the actual encashment of such cheques is

not taken into due consideration during the elimination of such receipts. Hence, this poses

a huge risk to the company because the actual recording of receipts and realization of

amounts may be distinct and therefore, vulnerable to manipulation by the accountants.

Thus, this gives rise to the fact that the system of reconciliation is not appropriate,

thereby posing a major risk for the company as a whole. Besides, such risk may play a

4

Answer to 2

Inherent risks are the risks prevalent in a business organization irrespective of internal control

measures or audit processes. Such a risk is present in the system and is not due to any omission

or negligence. This is because a business is vulnerable to various internal and external factors in

order to survive in the competing environment. Besides, the key reason for the generation of

inherent risk is the prevalence of material misstatements in the financial statements. The inherent

risks present in the financials of DIPL Ltd are as follows:

a. Firstly, the company has decided to adopt a new IT system in its operations that are a

good step but the major problem associated with such step is the lack of proper

evaluation and research. The main reason for the adoption of the new system was to

simplify the recording of transactions but there were inaccuracies in its testing and

research before its installation. Since the management did not conduct effective steps

before adopting the system, many transactions failed to be properly allocated to their

right period (Roach, 2010). Hence, this is of a major issue because the transactions will

be reflected in different period. As a result, the profit amounts of the company were

either exaggerated or downgraded. Hence, such inappropriateness in the accounting

system can result in manipulation of accounts on the part of company officials, thereby

posing a big risk for the entire organization as a whole. When the officials are aware of

the loopholes then it provides them with the opportunity of making profit or taking

advantage. This ultimately tends to disturb the overall accounts and will impact the profit

or loss of the company.

b. Secondly, the officials of the company have done the treatment of accounts receivable in

an inaccurate way. The cashier takes the receipts attained from the debtors into account

on a regular basis but the recognition of the same is done through mail wherein the

debtors enclose the cheques. In contrast to this, the actual encashment of such cheques is

not taken into due consideration during the elimination of such receipts. Hence, this poses

a huge risk to the company because the actual recording of receipts and realization of

amounts may be distinct and therefore, vulnerable to manipulation by the accountants.

Thus, this gives rise to the fact that the system of reconciliation is not appropriate,

thereby posing a major risk for the company as a whole. Besides, such risk may play a

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

key role in affecting the maintenance of accounts and the audit report as well, because the

auditor depends on the financials of a company to make their judgement. Therefore, if the

actual system has variations, then the auditor may also fail in his attempts in providing an

effective audit opinion.

Therefore, in relation to the financial information of DIPL Ltd, these two risks pose a huge threat

to the auditor and their decision-making process as a whole.

5

key role in affecting the maintenance of accounts and the audit report as well, because the

auditor depends on the financials of a company to make their judgement. Therefore, if the

actual system has variations, then the auditor may also fail in his attempts in providing an

effective audit opinion.

Therefore, in relation to the financial information of DIPL Ltd, these two risks pose a huge threat

to the auditor and their decision-making process as a whole.

5

Audit

Answer to 3

a. Fraud risks that are prevalent in the financial statement of DIPL Ltd are related to the

adoption of the new IT system and identification of receipts obtained from debtors. In

relation to the identification of revenue, it can be seen that the company has utilized

mailing technologies, which is not an effective measure as the receipts entries cannot be

tallied with the bank statements (Gay & Simnet, 2015). Mailing technology can be

beneficial in certain scenario where the records need to be sent in a flash. However,

recognition of any amount or cheque from the debtors will be a difficult task because

realization is important in accounts and realization takes time while mail arrives in a

fraction of a second. Hence, a difference persists and going by the overall situation it will

lead to serious issue for the auditor. In other words, the bank statements may portray a

distinct amount because the recording is not done effectively. Further, the strategy of

internal control is not appropriate because the company officials may engage in

fraudulent activities, thereby affecting the entire financial statements (Johnstone et. al,

2014). Besides, it is compulsory for the management to take steps for effective

reconciliation on a daily basis.

Secondly, there is a probability that the hardware and software accommodate few

alterations. The major fraud risk that can affect the financial statements is that full

information may not be incorporated into the system or may be ineffectively entered in

the system, thereby resulting in manipulated accounts payables or receivables.

Nevertheless, accountants can easily access the system and influence the accountants for

their own benefits (Carcello, 2012). When the accountants are aware of the loopholes

then personal benefit can be derived from the system that will hamper the overall system.

This can pose a big threat to the overall financial statements of the company.

b. An auditor highly depends on the financial statements offered by the company but if the

management engages in fraudulent practices, his decision may not prove efficient in

nature. This is because the auditor will rely on the financial data provided by the

management but if the data is tampered or the origin of the data is altered then it is bound

to impact the decision of the auditor. Further, tracing every relevant detail in the financial

statements may become problematic for the auditor since the management can easily

manipulate their accounts to make significant information untraceable (Carcello, 2012).

6

Answer to 3

a. Fraud risks that are prevalent in the financial statement of DIPL Ltd are related to the

adoption of the new IT system and identification of receipts obtained from debtors. In

relation to the identification of revenue, it can be seen that the company has utilized

mailing technologies, which is not an effective measure as the receipts entries cannot be

tallied with the bank statements (Gay & Simnet, 2015). Mailing technology can be

beneficial in certain scenario where the records need to be sent in a flash. However,

recognition of any amount or cheque from the debtors will be a difficult task because

realization is important in accounts and realization takes time while mail arrives in a

fraction of a second. Hence, a difference persists and going by the overall situation it will

lead to serious issue for the auditor. In other words, the bank statements may portray a

distinct amount because the recording is not done effectively. Further, the strategy of

internal control is not appropriate because the company officials may engage in

fraudulent activities, thereby affecting the entire financial statements (Johnstone et. al,

2014). Besides, it is compulsory for the management to take steps for effective

reconciliation on a daily basis.

Secondly, there is a probability that the hardware and software accommodate few

alterations. The major fraud risk that can affect the financial statements is that full

information may not be incorporated into the system or may be ineffectively entered in

the system, thereby resulting in manipulated accounts payables or receivables.

Nevertheless, accountants can easily access the system and influence the accountants for

their own benefits (Carcello, 2012). When the accountants are aware of the loopholes

then personal benefit can be derived from the system that will hamper the overall system.

This can pose a big threat to the overall financial statements of the company.

b. An auditor highly depends on the financial statements offered by the company but if the

management engages in fraudulent practices, his decision may not prove efficient in

nature. This is because the auditor will rely on the financial data provided by the

management but if the data is tampered or the origin of the data is altered then it is bound

to impact the decision of the auditor. Further, tracing every relevant detail in the financial

statements may become problematic for the auditor since the management can easily

manipulate their accounts to make significant information untraceable (Carcello, 2012).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

Therefore, documents like ledgers must be taken into account in order to verify the

effectiveness of information accommodated in the financial statements. Hence, it is

imperative for the auditor to cross check all the available information present with the

company so that any shortfalls can be highlighted and the same can be brought to the

management’s view. Moreover, the problem of recording receipts is also a big concern

for the company because the auditor may consume immense time to verify the bank

statements and it may happen that some details are overlooked by him (Johnstone et. al,

2014). In short, the data of the company and the one reflected at the bank must reconcile

otherwise will create a problem while auditing. In addition, during the adoption of the

new accounting system, the auditor must take relevant steps to be habituated with the

system so that decision-making is not influenced (Elder et. al, 2010). In relation to this,

the biggest risk here is the inaccuracies in recording the entries based on their time. As a

result, auditor’s decision may be influenced, thereby affecting the entire financial

statements. Moreover, since the testing of the system was not adequate, problems like a

breach of information, piracy, etc may also happen, thereby resulting in a wrong audit

opinion on the part of auditors. Further, it may also happen that the auditor relies on such

new automated information technology system and hamper the entire decision-making

process. Automated system contains shortfalls at times because the same is not controlled

by human. Hence, in this scenario, the auditor will face serious problem because the

entire system needs to be evaluated by him that might be cumbersome in nature. On a

whole, the audit process may be entirely affected because of such issues and therefore,

corrective actions are the need of the hour (Matthew, 2015). Further, the auditor process

will take time because the auditor needs to have a complete grasp of the new system.

7

Therefore, documents like ledgers must be taken into account in order to verify the

effectiveness of information accommodated in the financial statements. Hence, it is

imperative for the auditor to cross check all the available information present with the

company so that any shortfalls can be highlighted and the same can be brought to the

management’s view. Moreover, the problem of recording receipts is also a big concern

for the company because the auditor may consume immense time to verify the bank

statements and it may happen that some details are overlooked by him (Johnstone et. al,

2014). In short, the data of the company and the one reflected at the bank must reconcile

otherwise will create a problem while auditing. In addition, during the adoption of the

new accounting system, the auditor must take relevant steps to be habituated with the

system so that decision-making is not influenced (Elder et. al, 2010). In relation to this,

the biggest risk here is the inaccuracies in recording the entries based on their time. As a

result, auditor’s decision may be influenced, thereby affecting the entire financial

statements. Moreover, since the testing of the system was not adequate, problems like a

breach of information, piracy, etc may also happen, thereby resulting in a wrong audit

opinion on the part of auditors. Further, it may also happen that the auditor relies on such

new automated information technology system and hamper the entire decision-making

process. Automated system contains shortfalls at times because the same is not controlled

by human. Hence, in this scenario, the auditor will face serious problem because the

entire system needs to be evaluated by him that might be cumbersome in nature. On a

whole, the audit process may be entirely affected because of such issues and therefore,

corrective actions are the need of the hour (Matthew, 2015). Further, the auditor process

will take time because the auditor needs to have a complete grasp of the new system.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

References

Carcello, J 2012, ‘What do investors want from the standard audit report?’, CPA Journal vol. 82,

no. 2, pp. 7-12

Church, B., Davis, S & McCracken, S 2008, ‘The auditor’s reporting model: A literature overview

and research synthesis’, Accounting Horizons vol. 22, no. 1, pp. 69-90.

Elder, J. R, Beasley S. M.& Arens A. A 2010, Auditing and Assurance Services, Person

Gay, G & Simnet, R 2015, Auditing and Assurance Services, McGraw Hill

Johnstone, K, Gramling, A & Rittenberg, L.E 2014, Auditing: A Risk Based-Approach to

Conducting a Quality Audit, 10th Edition, Cengage Learning

Knapp, M.C 2013, Contemporary Accounting, Cengage Learning

Lapsley, I., 2012, Commentary: Financial Accountability & Management. Qualitative Research in

Accounting & Management, 9(3), pp. 291-292.

Matthew S. E 2015, ‘ Does Internal Audit Function Quality Deter Management Misconduct?’, The

Accounting Review, vol. 90, no. 2, pp. 495-527

Northington, S 2011, Finance, New York, NY: Ferguson's, pp. 52-55

Roach, L 2010, Auditor Liability: Liability Limitation Agreements, Pearson

8

References

Carcello, J 2012, ‘What do investors want from the standard audit report?’, CPA Journal vol. 82,

no. 2, pp. 7-12

Church, B., Davis, S & McCracken, S 2008, ‘The auditor’s reporting model: A literature overview

and research synthesis’, Accounting Horizons vol. 22, no. 1, pp. 69-90.

Elder, J. R, Beasley S. M.& Arens A. A 2010, Auditing and Assurance Services, Person

Gay, G & Simnet, R 2015, Auditing and Assurance Services, McGraw Hill

Johnstone, K, Gramling, A & Rittenberg, L.E 2014, Auditing: A Risk Based-Approach to

Conducting a Quality Audit, 10th Edition, Cengage Learning

Knapp, M.C 2013, Contemporary Accounting, Cengage Learning

Lapsley, I., 2012, Commentary: Financial Accountability & Management. Qualitative Research in

Accounting & Management, 9(3), pp. 291-292.

Matthew S. E 2015, ‘ Does Internal Audit Function Quality Deter Management Misconduct?’, The

Accounting Review, vol. 90, no. 2, pp. 495-527

Northington, S 2011, Finance, New York, NY: Ferguson's, pp. 52-55

Roach, L 2010, Auditor Liability: Liability Limitation Agreements, Pearson

8

Audit

Appendix

2013 2014 2015

Current Ratio 1.424851 1.466559 1.500731

Quick ratio 0.827976 0.944834 0.847273

GP ratio 17.55086 16.12621 15.19691

NP ratio 6.895797 6.077964 6.838972

Debt Equity Ratio (only long

term liabilities)

0.61222

9

Appendix

2013 2014 2015

Current Ratio 1.424851 1.466559 1.500731

Quick ratio 0.827976 0.944834 0.847273

GP ratio 17.55086 16.12621 15.19691

NP ratio 6.895797 6.077964 6.838972

Debt Equity Ratio (only long

term liabilities)

0.61222

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.