AHIC Diploma of Accounting Assessment - FNSACC501 - Term 1, 2024

VerifiedAdded on 2020/04/13

|21

|5565

|172

Homework Assignment

AI Summary

This document contains solutions to an accounting assessment for the Diploma of Accounting course, focusing on the unit FNSACC501. The assessment covers various aspects of financial and business performance information. It includes discussions on business expenses and tax legislation, trust allowances, forecast returns, and adherence of NFP sector organizations to government financial policies. The assessment also involves a loan repayment calculation, identifying business performance objectives, defining GPFRU's, and discussing state and territory charges. Additionally, the assignment analyzes a client information form (CIF) to address client objectives and financial options for business performance information. It concludes with a forecast versus actual report for an operational project, and identifies stages of financial management and agreed criteria for return analysis. This assignment provides comprehensive insights into financial accounting principles and practical applications.

Assessment Details

Qualification Code/Title Diploma of Accounting

Assessment Type Assessment -2 Time allowed

Due Date Location AHIC Term / Year

Student Details

Student Name Student ID

Student Declaration: I declare that the work submitted is my own,

and has not been copied or plagiarised from any person or source.

Signature: ____________________________

Date: _____/______/__________

Assessor Details

Assessor’s Name

RESULTS (Please

Circle) SATISFACTORY NOT SATISFACTORY

Feedback to student:

.........................................................................................................................................................................................

.........................................................................................................................................................................................

.........................................................................................................................................................................................

.........................................................................................................................................................................................

Student Declaration: I declare that I have been

assessed in this unit, and I have been advised of my

result. I am also aware of my appeal rights.

Signature: _______________________________

Date: ______/_______/___________

Assessor Declaration: I declare that I have conducted a fair,

valid, reliable and flexible assessment with this student, and I

have provided appropriate feedback.

Signature: ________________________________________

Date: ______/_______/___________

Instructions to the Candidates

This assessment is to be completed in class supervised by assessor.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in knowledge. You will

be given another opportunity to demonstrate your knowledge and skills to be deemed competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-submission and re-sit policy for more information.

If you have questions and other concerns that may affect your performance in the examination please inform the assessor

immediately.

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 1 of 21

Unit of Competency

National Code/Title FNSACC501-Provide Financial and Business Performance Information

Qualification Code/Title Diploma of Accounting

Assessment Type Assessment -2 Time allowed

Due Date Location AHIC Term / Year

Student Details

Student Name Student ID

Student Declaration: I declare that the work submitted is my own,

and has not been copied or plagiarised from any person or source.

Signature: ____________________________

Date: _____/______/__________

Assessor Details

Assessor’s Name

RESULTS (Please

Circle) SATISFACTORY NOT SATISFACTORY

Feedback to student:

.........................................................................................................................................................................................

.........................................................................................................................................................................................

.........................................................................................................................................................................................

.........................................................................................................................................................................................

Student Declaration: I declare that I have been

assessed in this unit, and I have been advised of my

result. I am also aware of my appeal rights.

Signature: _______________________________

Date: ______/_______/___________

Assessor Declaration: I declare that I have conducted a fair,

valid, reliable and flexible assessment with this student, and I

have provided appropriate feedback.

Signature: ________________________________________

Date: ______/_______/___________

Instructions to the Candidates

This assessment is to be completed in class supervised by assessor.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in knowledge. You will

be given another opportunity to demonstrate your knowledge and skills to be deemed competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-submission and re-sit policy for more information.

If you have questions and other concerns that may affect your performance in the examination please inform the assessor

immediately.

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 1 of 21

Unit of Competency

National Code/Title FNSACC501-Provide Financial and Business Performance Information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Project 1

Part 1

1. How are business expenses treated in regard to tax legislation? Discuss in 30 to 50 words.

Answer: For the purpose of tax deductible expenditure expenses are generally considered to

be ordinary, necessary and reasonable expenses that assist in earning business income. therefore,

business expenses can be subtracted from the income of the company prior to considered for

taxation.

2. What allowance in tax legislation is there for businesses that are managed on behalf of a

trust? Discuss in 80 to 100 words.

Answer: A trust can be defined as the structure that where the trustee executes the business on

behalf of the trust members or beneficiaries. The benefits that are available to the trust are as

follows;

a. Reduction in the liability particularly if the corporate is the trustee

b. A benefit is provided for the protection of the assets

c. A benefit is provided relating to the flexibility of the asset and distribution of income

3. Describe forecast returns and set up and describe a simple table over several years for

similar amounts. Discuss in 50 to 80 words.

Answer: Forecast returns is the use of the historic information to determine the future

trends. The forecasting model is used to cope up with the uncertainty future. For a data that is

simple over the period of several years constructing portfolio should be adopted in choosing the best

available model to forecast the class of asset returns.

4. Describe (150 to 180 words) how NFP sector organisations adhere to government financial

policies where the preparation of statutory returns are required.

Answer: The NFP sector organizes and prepares the report in respect of the general

government sector financial reporting under the AASB 102 Inventories, AASB 116 property plant and

equipment’s AASB 138 intangible assets. Disclosure requirements in regard to the whole of the

government and GGS financial reporting are stated under the 1049. The non-for profit subsidiary is

anticipated to keep their information to facilitate the preparation for the disclosure of the financial

statements with the non-for profit entities are required to present their financial disclosure in the

non-for profit consolidated financial statements. The segment reporting by the Non-for-profit

governments must be addressed in the AASB 1049 and AASB 1052 instead of reporting in AASB 8. In

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 2 of 21

Part 1

1. How are business expenses treated in regard to tax legislation? Discuss in 30 to 50 words.

Answer: For the purpose of tax deductible expenditure expenses are generally considered to

be ordinary, necessary and reasonable expenses that assist in earning business income. therefore,

business expenses can be subtracted from the income of the company prior to considered for

taxation.

2. What allowance in tax legislation is there for businesses that are managed on behalf of a

trust? Discuss in 80 to 100 words.

Answer: A trust can be defined as the structure that where the trustee executes the business on

behalf of the trust members or beneficiaries. The benefits that are available to the trust are as

follows;

a. Reduction in the liability particularly if the corporate is the trustee

b. A benefit is provided for the protection of the assets

c. A benefit is provided relating to the flexibility of the asset and distribution of income

3. Describe forecast returns and set up and describe a simple table over several years for

similar amounts. Discuss in 50 to 80 words.

Answer: Forecast returns is the use of the historic information to determine the future

trends. The forecasting model is used to cope up with the uncertainty future. For a data that is

simple over the period of several years constructing portfolio should be adopted in choosing the best

available model to forecast the class of asset returns.

4. Describe (150 to 180 words) how NFP sector organisations adhere to government financial

policies where the preparation of statutory returns are required.

Answer: The NFP sector organizes and prepares the report in respect of the general

government sector financial reporting under the AASB 102 Inventories, AASB 116 property plant and

equipment’s AASB 138 intangible assets. Disclosure requirements in regard to the whole of the

government and GGS financial reporting are stated under the 1049. The non-for profit subsidiary is

anticipated to keep their information to facilitate the preparation for the disclosure of the financial

statements with the non-for profit entities are required to present their financial disclosure in the

non-for profit consolidated financial statements. The segment reporting by the Non-for-profit

governments must be addressed in the AASB 1049 and AASB 1052 instead of reporting in AASB 8. In

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 2 of 21

respect of the government compliance the non-for-profit entities are primarily concerned with the

achievement of the objectives instead of generation of the profit. Disclosure needs concerning the

whole of the government and GGS financial reporting must adhere with the AASB 1049 for the

preparation of the statutory returns.

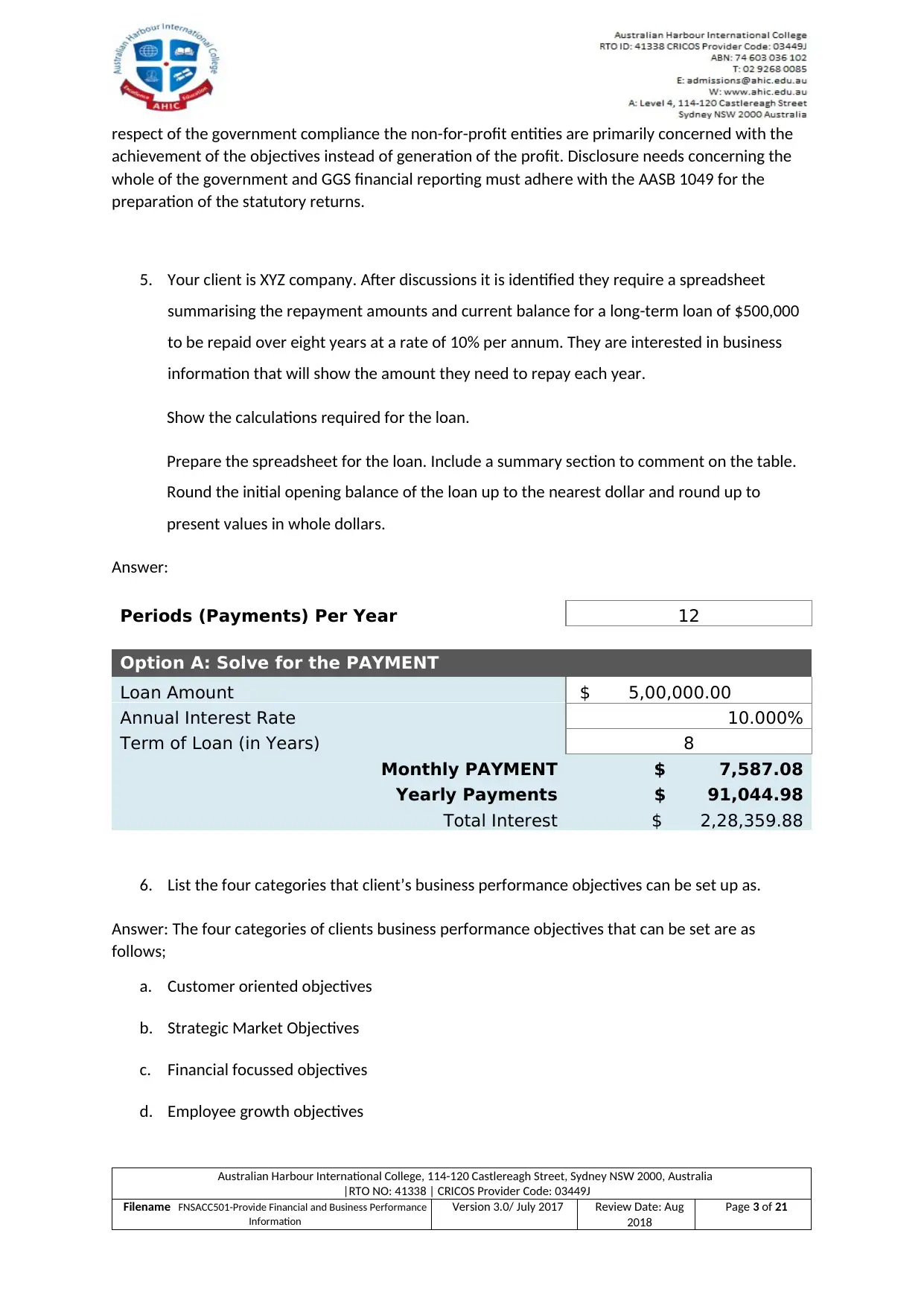

5. Your client is XYZ company. After discussions it is identified they require a spreadsheet

summarising the repayment amounts and current balance for a long-term loan of $500,000

to be repaid over eight years at a rate of 10% per annum. They are interested in business

information that will show the amount they need to repay each year.

Show the calculations required for the loan.

Prepare the spreadsheet for the loan. Include a summary section to comment on the table.

Round the initial opening balance of the loan up to the nearest dollar and round up to

present values in whole dollars.

Answer:

Periods (Payments) Per Year 12

Option A: Solve for the PAYMENT

Loan Amount $ 5,00,000.00

Annual Interest Rate 10.000%

Term of Loan (in Years) 8

Monthly PAYMENT $ 7,587.08

Yearly Payments $ 91,044.98

Total Interest $ 2,28,359.88

6. List the four categories that client’s business performance objectives can be set up as.

Answer: The four categories of clients business performance objectives that can be set are as

follows;

a. Customer oriented objectives

b. Strategic Market Objectives

c. Financial focussed objectives

d. Employee growth objectives

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 3 of 21

achievement of the objectives instead of generation of the profit. Disclosure needs concerning the

whole of the government and GGS financial reporting must adhere with the AASB 1049 for the

preparation of the statutory returns.

5. Your client is XYZ company. After discussions it is identified they require a spreadsheet

summarising the repayment amounts and current balance for a long-term loan of $500,000

to be repaid over eight years at a rate of 10% per annum. They are interested in business

information that will show the amount they need to repay each year.

Show the calculations required for the loan.

Prepare the spreadsheet for the loan. Include a summary section to comment on the table.

Round the initial opening balance of the loan up to the nearest dollar and round up to

present values in whole dollars.

Answer:

Periods (Payments) Per Year 12

Option A: Solve for the PAYMENT

Loan Amount $ 5,00,000.00

Annual Interest Rate 10.000%

Term of Loan (in Years) 8

Monthly PAYMENT $ 7,587.08

Yearly Payments $ 91,044.98

Total Interest $ 2,28,359.88

6. List the four categories that client’s business performance objectives can be set up as.

Answer: The four categories of clients business performance objectives that can be set are as

follows;

a. Customer oriented objectives

b. Strategic Market Objectives

c. Financial focussed objectives

d. Employee growth objectives

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 3 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7. What does GPFRU’s mean? List three potential users.

Answer: GPFRU’s represents general purpose of financial reporting which is issued all through the

year to assist the investors and creditors in the process of their decision making.

Three potential users of the GPFRU’s are as follows;

a. Current and potential investors

b. Lenders

c. Other creditors

8. What type of clients can expect state and territory charges? Discuss in 50 to 80 words.

Answer: Clients that are included in the state and territory taxes comprises of the following;

a. Not-for-profit companies

b. Employers that are held accountable for payroll tax whose total Australian wages goes past

the tax-free threshold limit.

c. Non-for-profit societies, clubs and religious institutions

9. How can the amount of taxes and charges on land be calculated? Discuss in 50 to 80 words.

Answer: Land tax is yearly amount of tax on land. It is based on the land that is owned from June 30

and it is computed on the unimproved value of the land that is determined by the valuer-general.

Land tax is computed based on the aggregated taxable value of the land held in the ownership at the

midnight of 30 June.

10. What practices should these businesses and those who pay Commonwealth taxes complete?

Discuss in 80 to 100 words.

Answer: Practices that businesses and those paying commonwealth taxes should complete are as

follows;

a. Ensuring that the adequacy of material is maintained

b. General and administrative practices must be considered to make sure that the statement of

tax return is based on the ground of non-applicability of the penalty.

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 4 of 21

Answer: GPFRU’s represents general purpose of financial reporting which is issued all through the

year to assist the investors and creditors in the process of their decision making.

Three potential users of the GPFRU’s are as follows;

a. Current and potential investors

b. Lenders

c. Other creditors

8. What type of clients can expect state and territory charges? Discuss in 50 to 80 words.

Answer: Clients that are included in the state and territory taxes comprises of the following;

a. Not-for-profit companies

b. Employers that are held accountable for payroll tax whose total Australian wages goes past

the tax-free threshold limit.

c. Non-for-profit societies, clubs and religious institutions

9. How can the amount of taxes and charges on land be calculated? Discuss in 50 to 80 words.

Answer: Land tax is yearly amount of tax on land. It is based on the land that is owned from June 30

and it is computed on the unimproved value of the land that is determined by the valuer-general.

Land tax is computed based on the aggregated taxable value of the land held in the ownership at the

midnight of 30 June.

10. What practices should these businesses and those who pay Commonwealth taxes complete?

Discuss in 80 to 100 words.

Answer: Practices that businesses and those paying commonwealth taxes should complete are as

follows;

a. Ensuring that the adequacy of material is maintained

b. General and administrative practices must be considered to make sure that the statement of

tax return is based on the ground of non-applicability of the penalty.

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 4 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c. General and administrative practices must be established by making appropriate

communications comprising of the wide range of the issues for the taxpayers

d. To improve the certainty of the taxpayers by making the advice of the tax office more

reliable and legally binding on the commissioner.

Part 2

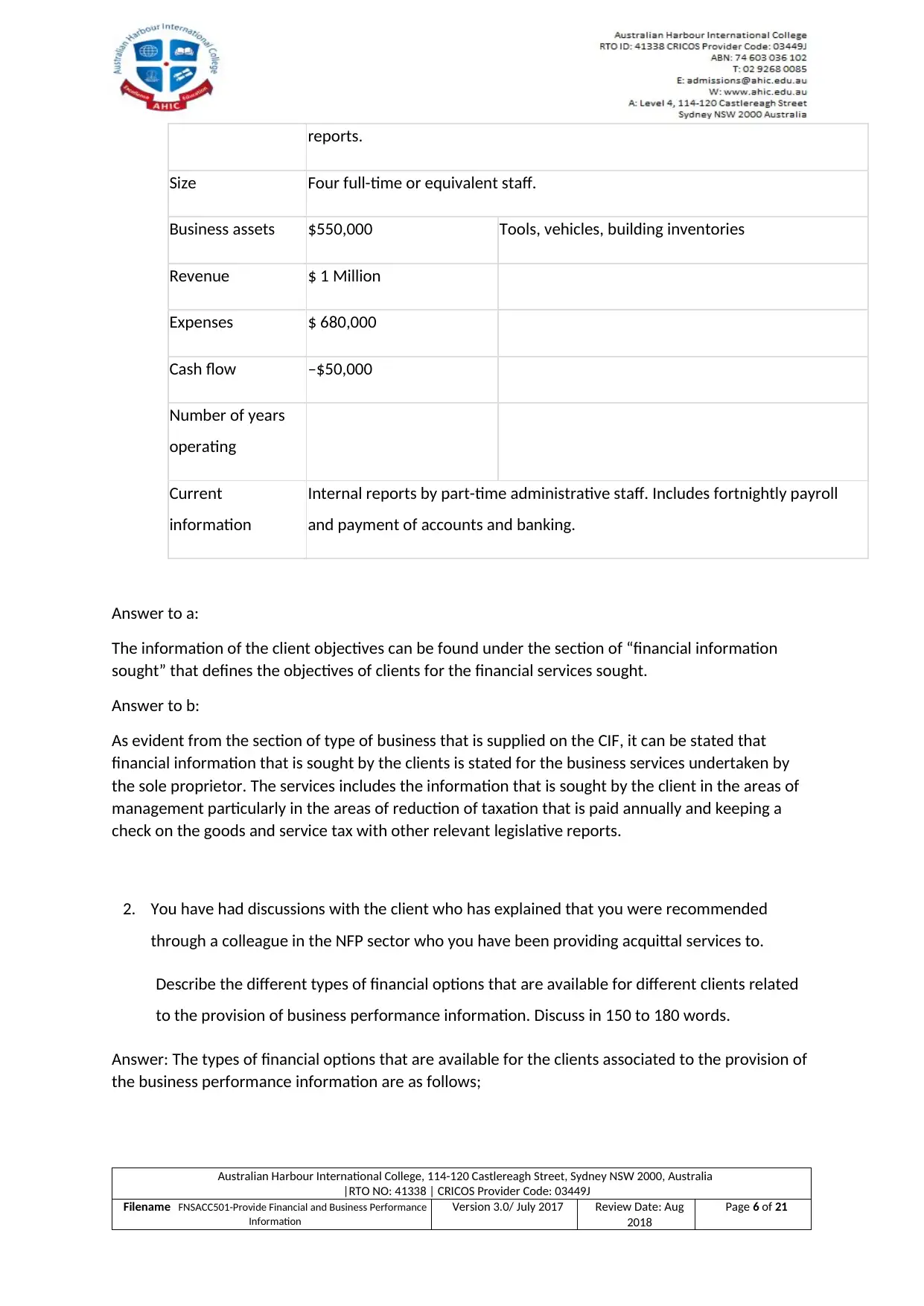

1. Use the supplied CIF to answer the questions listed.

a. Where can information about client objectives be found?

b. Describe (80 to 100 words) how the Type of business section on the supplied CIF is

relevant to the client’s legal and financial requirements, explain how this is important to

taxation.

ABC Financial Management

Client Information Form

Surname Citizen

First name John

Employment title Manager

Other key staff

Type of business Building services Sole proprietor

Financial

information sought

Provide ongoing financial management especially in the reduction of annual

income tax and checking goods and services tax (GST) and other legislative

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 5 of 21

communications comprising of the wide range of the issues for the taxpayers

d. To improve the certainty of the taxpayers by making the advice of the tax office more

reliable and legally binding on the commissioner.

Part 2

1. Use the supplied CIF to answer the questions listed.

a. Where can information about client objectives be found?

b. Describe (80 to 100 words) how the Type of business section on the supplied CIF is

relevant to the client’s legal and financial requirements, explain how this is important to

taxation.

ABC Financial Management

Client Information Form

Surname Citizen

First name John

Employment title Manager

Other key staff

Type of business Building services Sole proprietor

Financial

information sought

Provide ongoing financial management especially in the reduction of annual

income tax and checking goods and services tax (GST) and other legislative

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 5 of 21

reports.

Size Four full-time or equivalent staff.

Business assets $550,000 Tools, vehicles, building inventories

Revenue $ 1 Million

Expenses $ 680,000

Cash flow –$50,000

Number of years

operating

Current

information

Internal reports by part-time administrative staff. Includes fortnightly payroll

and payment of accounts and banking.

Answer to a:

The information of the client objectives can be found under the section of “financial information

sought” that defines the objectives of clients for the financial services sought.

Answer to b:

As evident from the section of type of business that is supplied on the CIF, it can be stated that

financial information that is sought by the clients is stated for the business services undertaken by

the sole proprietor. The services includes the information that is sought by the client in the areas of

management particularly in the areas of reduction of taxation that is paid annually and keeping a

check on the goods and service tax with other relevant legislative reports.

2. You have had discussions with the client who has explained that you were recommended

through a colleague in the NFP sector who you have been providing acquittal services to.

Describe the different types of financial options that are available for different clients related

to the provision of business performance information. Discuss in 150 to 180 words.

Answer: The types of financial options that are available for the clients associated to the provision of

the business performance information are as follows;

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 6 of 21

Size Four full-time or equivalent staff.

Business assets $550,000 Tools, vehicles, building inventories

Revenue $ 1 Million

Expenses $ 680,000

Cash flow –$50,000

Number of years

operating

Current

information

Internal reports by part-time administrative staff. Includes fortnightly payroll

and payment of accounts and banking.

Answer to a:

The information of the client objectives can be found under the section of “financial information

sought” that defines the objectives of clients for the financial services sought.

Answer to b:

As evident from the section of type of business that is supplied on the CIF, it can be stated that

financial information that is sought by the clients is stated for the business services undertaken by

the sole proprietor. The services includes the information that is sought by the client in the areas of

management particularly in the areas of reduction of taxation that is paid annually and keeping a

check on the goods and service tax with other relevant legislative reports.

2. You have had discussions with the client who has explained that you were recommended

through a colleague in the NFP sector who you have been providing acquittal services to.

Describe the different types of financial options that are available for different clients related

to the provision of business performance information. Discuss in 150 to 180 words.

Answer: The types of financial options that are available for the clients associated to the provision of

the business performance information are as follows;

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 6 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a. Assessing the needs of the clients: Financial options and procedures must be discussed with

the clients in order to develop appropriate plans for the provision of the information and the

attainment of the client’s goals. Additionally, the progress of the plans must be reviewed

constantly against the agree criteria and results should be clearly communicated to the

client.

b. Analysing the data: Analysis must be undertaken to make sure that the consistency of the

analysis is present with the business of clients and personal objectives. Advice relating to

the reliability and accuracy of the data must be sought from appropriate authorities and

sources in compliance with the organizational procedures. Additionally, advising the clients

to assess the financial potential of the business and its future funding requirements.

c. Preparation of the advice: Advising the clients with the realistic view of the business financial

performance and compliance along with the issues of the taxation and comparisons of the

options.

3. Prepare an example of a forecast versus actual for XYZ company for an operational project.

Include columns to show forecast returns versus actual on a multi period report. Include a

summary section.

Answer:

INCOME Actual Budget Difference

Operating Income

Category 1 25,000 20,000 5,000

Total Operating Income 25,000 20,000 5,000

Non-Operating Income

Interest Income 2,500 2,250 250

Rental Income 3,500 3,150 350

Gifts Received 1,250 1,125 125

Donations 750 675 75

Total Non-Operating Income 8,000 7,200 800

Total INCOME 33,000 27,200 5,800

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 7 of 21

the clients in order to develop appropriate plans for the provision of the information and the

attainment of the client’s goals. Additionally, the progress of the plans must be reviewed

constantly against the agree criteria and results should be clearly communicated to the

client.

b. Analysing the data: Analysis must be undertaken to make sure that the consistency of the

analysis is present with the business of clients and personal objectives. Advice relating to

the reliability and accuracy of the data must be sought from appropriate authorities and

sources in compliance with the organizational procedures. Additionally, advising the clients

to assess the financial potential of the business and its future funding requirements.

c. Preparation of the advice: Advising the clients with the realistic view of the business financial

performance and compliance along with the issues of the taxation and comparisons of the

options.

3. Prepare an example of a forecast versus actual for XYZ company for an operational project.

Include columns to show forecast returns versus actual on a multi period report. Include a

summary section.

Answer:

INCOME Actual Budget Difference

Operating Income

Category 1 25,000 20,000 5,000

Total Operating Income 25,000 20,000 5,000

Non-Operating Income

Interest Income 2,500 2,250 250

Rental Income 3,500 3,150 350

Gifts Received 1,250 1,125 125

Donations 750 675 75

Total Non-Operating Income 8,000 7,200 800

Total INCOME 33,000 27,200 5,800

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 7 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

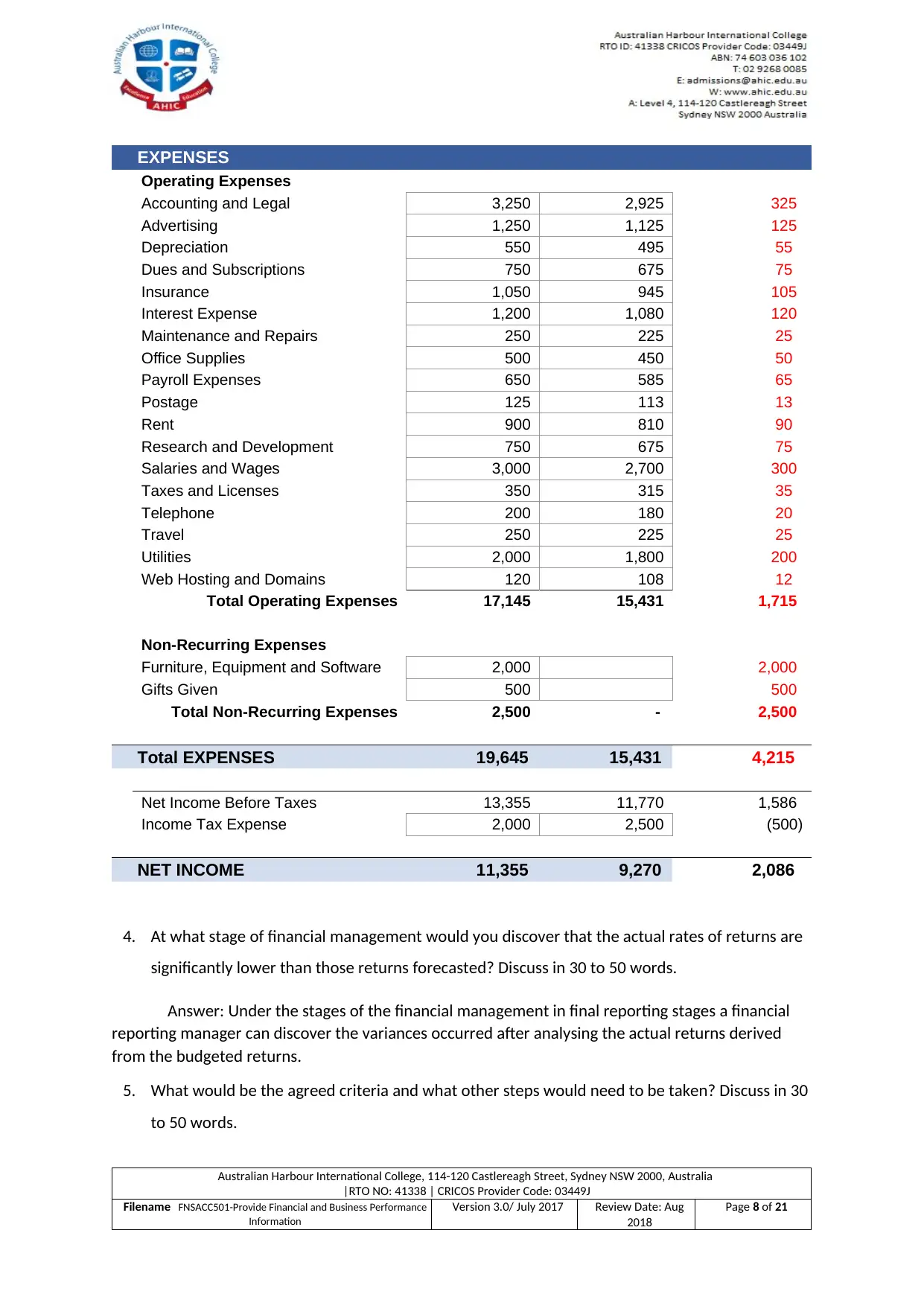

EXPENSES

Operating Expenses

Accounting and Legal 3,250 2,925 325

Advertising 1,250 1,125 125

Depreciation 550 495 55

Dues and Subscriptions 750 675 75

Insurance 1,050 945 105

Interest Expense 1,200 1,080 120

Maintenance and Repairs 250 225 25

Office Supplies 500 450 50

Payroll Expenses 650 585 65

Postage 125 113 13

Rent 900 810 90

Research and Development 750 675 75

Salaries and Wages 3,000 2,700 300

Taxes and Licenses 350 315 35

Telephone 200 180 20

Travel 250 225 25

Utilities 2,000 1,800 200

Web Hosting and Domains 120 108 12

Total Operating Expenses 17,145 15,431 1,715

Non-Recurring Expenses

Furniture, Equipment and Software 2,000 2,000

Gifts Given 500 500

Total Non-Recurring Expenses 2,500 - 2,500

Total EXPENSES 19,645 15,431 4,215

Net Income Before Taxes 13,355 11,770 1,586

Income Tax Expense 2,000 2,500 (500)

NET INCOME 11,355 9,270 2,086

4. At what stage of financial management would you discover that the actual rates of returns are

significantly lower than those returns forecasted? Discuss in 30 to 50 words.

Answer: Under the stages of the financial management in final reporting stages a financial

reporting manager can discover the variances occurred after analysing the actual returns derived

from the budgeted returns.

5. What would be the agreed criteria and what other steps would need to be taken? Discuss in 30

to 50 words.

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 8 of 21

Operating Expenses

Accounting and Legal 3,250 2,925 325

Advertising 1,250 1,125 125

Depreciation 550 495 55

Dues and Subscriptions 750 675 75

Insurance 1,050 945 105

Interest Expense 1,200 1,080 120

Maintenance and Repairs 250 225 25

Office Supplies 500 450 50

Payroll Expenses 650 585 65

Postage 125 113 13

Rent 900 810 90

Research and Development 750 675 75

Salaries and Wages 3,000 2,700 300

Taxes and Licenses 350 315 35

Telephone 200 180 20

Travel 250 225 25

Utilities 2,000 1,800 200

Web Hosting and Domains 120 108 12

Total Operating Expenses 17,145 15,431 1,715

Non-Recurring Expenses

Furniture, Equipment and Software 2,000 2,000

Gifts Given 500 500

Total Non-Recurring Expenses 2,500 - 2,500

Total EXPENSES 19,645 15,431 4,215

Net Income Before Taxes 13,355 11,770 1,586

Income Tax Expense 2,000 2,500 (500)

NET INCOME 11,355 9,270 2,086

4. At what stage of financial management would you discover that the actual rates of returns are

significantly lower than those returns forecasted? Discuss in 30 to 50 words.

Answer: Under the stages of the financial management in final reporting stages a financial

reporting manager can discover the variances occurred after analysing the actual returns derived

from the budgeted returns.

5. What would be the agreed criteria and what other steps would need to be taken? Discuss in 30

to 50 words.

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 8 of 21

Answer: The agree criteria and other steps that is required to be taken for significant fall in the

return includes the following;

a. Using the high impact marketing to improve the business returns

b. Monitoring the events that could change the landscape of the business

c. Setting appropriate planning tools to ensure sufficient returns is generated.

6. You work for ABC financial management. Your client is XYZ company. The CEO contacts you

directly on the 1st July, thanking you for the satisfaction of current objectives in line with the

financial plan. Current objectives are reporting annual financial reports including preparing the

BAS.

The client asks that this now ceases as the finance officer will take over the duties. The client

asks that you prepare a manual to assist the finance officer in their new duties. The client also

asks that you now assist with preparing for and recording monthly governance board meetings.

a. Prepare a quarterly financial management questionnaire for the current quarter to

show the current and proposed new objectives as if they had been discovered as a

result of the quarterly questionnaire process.

b. Prepare a file note to properly record the main points of your phone call with the

CEO.

Answer: Answer A:

Questionnaire:

a. Discussion of organizational strategies following the completion of BAS in order to enhance

the governance board meetings.

b. Discussion relating to the development of the organizational strategies in order to

contribute to the financial and accounting information to establish the functional objectives

in accordance with the organizational objectives.

Answer to B:

File Note:

Dear Client,

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 9 of 21

return includes the following;

a. Using the high impact marketing to improve the business returns

b. Monitoring the events that could change the landscape of the business

c. Setting appropriate planning tools to ensure sufficient returns is generated.

6. You work for ABC financial management. Your client is XYZ company. The CEO contacts you

directly on the 1st July, thanking you for the satisfaction of current objectives in line with the

financial plan. Current objectives are reporting annual financial reports including preparing the

BAS.

The client asks that this now ceases as the finance officer will take over the duties. The client

asks that you prepare a manual to assist the finance officer in their new duties. The client also

asks that you now assist with preparing for and recording monthly governance board meetings.

a. Prepare a quarterly financial management questionnaire for the current quarter to

show the current and proposed new objectives as if they had been discovered as a

result of the quarterly questionnaire process.

b. Prepare a file note to properly record the main points of your phone call with the

CEO.

Answer: Answer A:

Questionnaire:

a. Discussion of organizational strategies following the completion of BAS in order to enhance

the governance board meetings.

b. Discussion relating to the development of the organizational strategies in order to

contribute to the financial and accounting information to establish the functional objectives

in accordance with the organizational objectives.

Answer to B:

File Note:

Dear Client,

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 9 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Thank you for allowing our company to represent you in this matter. We are enclosing the main

point that was made during the phone call with the CEO which are as follows;

a. Analysis and recommendations relating to the strategic thinking

b. Creation of financial for strategic thinking and objectives.

c. Keeping record of the gross income

d. Preparation and presentation of the financial report of the organization associated semi-

annually.

7. Your client contact is the finance officer of XYZ company. They phone you briefly on 1.10.20xx

and say that the financial position detail report contains too much detail. They also state that

there is no explanation for the changes in financial position even though they know that

several new desks were purchased in the previous quarter because they recorded them on the

asset register. Prepare a file note to show how the feedback will be incorporated into services

to the client.

Answer:

File Note:

Dear Client,

I would like express my gratitude for allowing our company to represent you in this matter. I would

like to bring this into your notice that I appreciate your time to discuss this position in further detail.

We are giving you a brief summary of the report regarding the purchase of the new asset that was

incorporated in the purchase register of the earlier quarter. Additionally, I would also like to draw

your kind attention towards my application that your feedback has been considered and we would

be incorporating the asset purchased in the in the purchase register for better understanding of the

financial reports.

Thanking You

8. Your client is XYZ company. They phone you on 15.11.20xx and question what has caused them

to pay higher than normal GST. Your investigation shows that the income amount included the

previous year’s income. Record a file note to implement improved customer services.

Answer: File Note:

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 10 of 21

point that was made during the phone call with the CEO which are as follows;

a. Analysis and recommendations relating to the strategic thinking

b. Creation of financial for strategic thinking and objectives.

c. Keeping record of the gross income

d. Preparation and presentation of the financial report of the organization associated semi-

annually.

7. Your client contact is the finance officer of XYZ company. They phone you briefly on 1.10.20xx

and say that the financial position detail report contains too much detail. They also state that

there is no explanation for the changes in financial position even though they know that

several new desks were purchased in the previous quarter because they recorded them on the

asset register. Prepare a file note to show how the feedback will be incorporated into services

to the client.

Answer:

File Note:

Dear Client,

I would like express my gratitude for allowing our company to represent you in this matter. I would

like to bring this into your notice that I appreciate your time to discuss this position in further detail.

We are giving you a brief summary of the report regarding the purchase of the new asset that was

incorporated in the purchase register of the earlier quarter. Additionally, I would also like to draw

your kind attention towards my application that your feedback has been considered and we would

be incorporating the asset purchased in the in the purchase register for better understanding of the

financial reports.

Thanking You

8. Your client is XYZ company. They phone you on 15.11.20xx and question what has caused them

to pay higher than normal GST. Your investigation shows that the income amount included the

previous year’s income. Record a file note to implement improved customer services.

Answer: File Note:

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 10 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Dear Client,

We are grateful for choosing our company in order to allow us to present in the matter relating to

the payment of higher amount of GST than the normal amount paid by you. According to our

investigations of the books of accounts we found that the figure of sales that was reported by you

also included the income of the previous year. As a result this led to the income being overstated

with higher amount of GST.

We advise you to reconcile the figures of sales before lodging for GST returns. We hope that your

concern has been addressed relating to the higher payment of GST.

Thank You

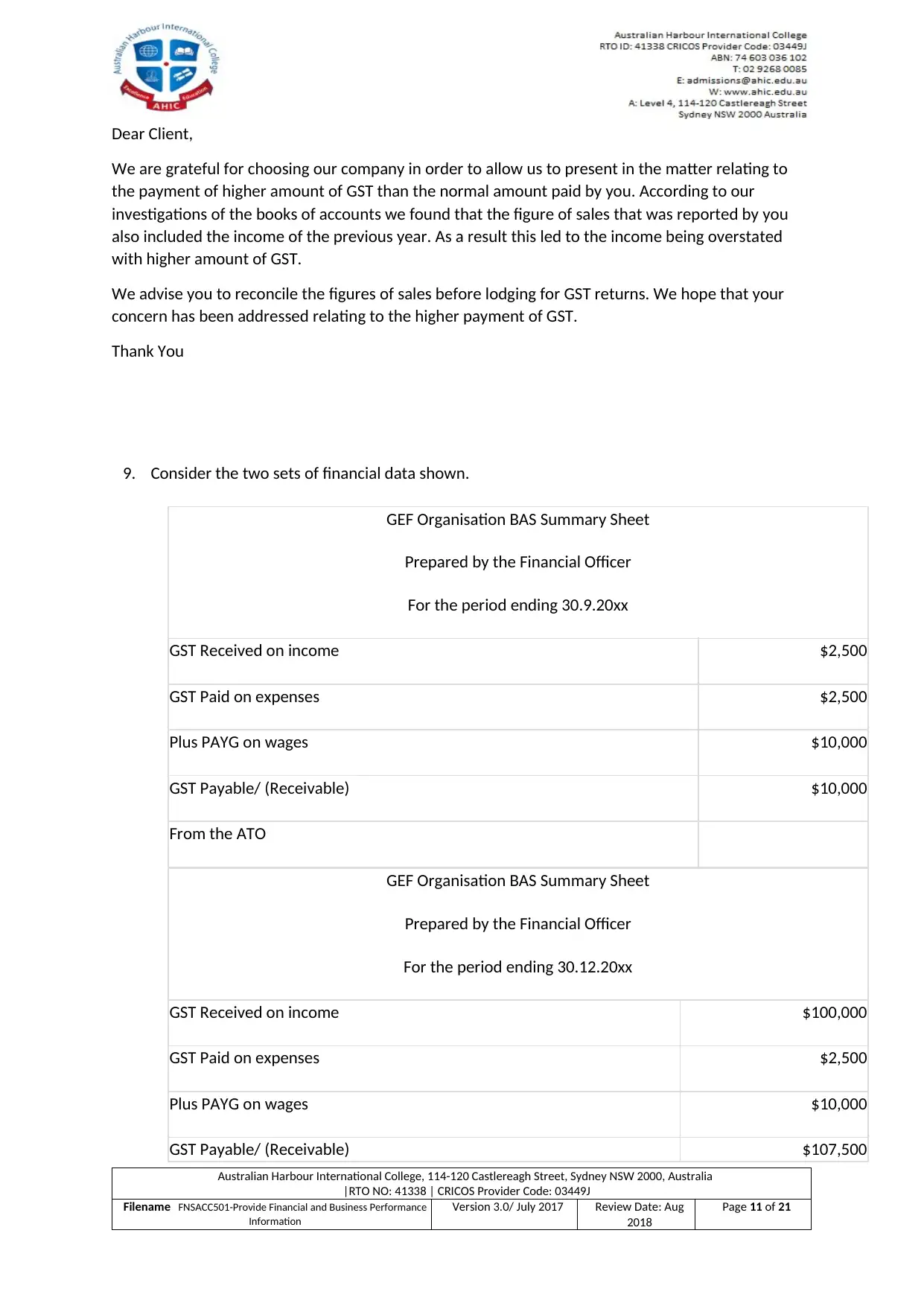

9. Consider the two sets of financial data shown.

GEF Organisation BAS Summary Sheet

Prepared by the Financial Officer

For the period ending 30.9.20xx

GST Received on income $2,500

GST Paid on expenses $2,500

Plus PAYG on wages $10,000

GST Payable/ (Receivable) $10,000

From the ATO

GEF Organisation BAS Summary Sheet

Prepared by the Financial Officer

For the period ending 30.12.20xx

GST Received on income $100,000

GST Paid on expenses $2,500

Plus PAYG on wages $10,000

GST Payable/ (Receivable) $107,500

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 11 of 21

We are grateful for choosing our company in order to allow us to present in the matter relating to

the payment of higher amount of GST than the normal amount paid by you. According to our

investigations of the books of accounts we found that the figure of sales that was reported by you

also included the income of the previous year. As a result this led to the income being overstated

with higher amount of GST.

We advise you to reconcile the figures of sales before lodging for GST returns. We hope that your

concern has been addressed relating to the higher payment of GST.

Thank You

9. Consider the two sets of financial data shown.

GEF Organisation BAS Summary Sheet

Prepared by the Financial Officer

For the period ending 30.9.20xx

GST Received on income $2,500

GST Paid on expenses $2,500

Plus PAYG on wages $10,000

GST Payable/ (Receivable) $10,000

From the ATO

GEF Organisation BAS Summary Sheet

Prepared by the Financial Officer

For the period ending 30.12.20xx

GST Received on income $100,000

GST Paid on expenses $2,500

Plus PAYG on wages $10,000

GST Payable/ (Receivable) $107,500

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 11 of 21

From the ATO

a. What would be of interest to the financial manager responsible for preparing the BAS

based on the reports? Discuss in 30 to 50 words.

b. For what reason would this be of interest? Discuss in 30 to 50 words.

c. What steps should the financial manager take in this scenario? Discuss in 50 to 80

words.

Answer: Answer a:

The interest of the financial manager that is responsible in the preparation of the BAS is that it would

help the business in timely lodgement of the tax requirements. The activity statement would help in

meeting the tax obligations of the business depending upon the frequencies and dependencies.

Answer b:

The reasons for interest of the financial manager in the preparation of the BAS would help in

meeting goods and service tax obligations. Additionally, it will help the business in goods and service

tax GST. Additionally, it helps in meeting the obligations of the pay as you go instalment together

with PAYG withholding and other tax matters.

Answer c:

Concerning the steps that are involved with the financial manager includes the lodging of the BAS

either with the help of electronically or with the help of the nil lodgement on the phone.

Additionally, the financial managers can pay electronically either with the help of mail or in person

that are at the Australian post.

10.Use the following information to prepare a bank reconciliation for KLM company.

Closing account balance 30.6.20xx, $68,000

Unpresented cheques:

Number 100 $5,000

Number 101 $5,000

Number 102 $3,000

Number 103 $4,000

KLM Bank Statement extract

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 12 of 21

a. What would be of interest to the financial manager responsible for preparing the BAS

based on the reports? Discuss in 30 to 50 words.

b. For what reason would this be of interest? Discuss in 30 to 50 words.

c. What steps should the financial manager take in this scenario? Discuss in 50 to 80

words.

Answer: Answer a:

The interest of the financial manager that is responsible in the preparation of the BAS is that it would

help the business in timely lodgement of the tax requirements. The activity statement would help in

meeting the tax obligations of the business depending upon the frequencies and dependencies.

Answer b:

The reasons for interest of the financial manager in the preparation of the BAS would help in

meeting goods and service tax obligations. Additionally, it will help the business in goods and service

tax GST. Additionally, it helps in meeting the obligations of the pay as you go instalment together

with PAYG withholding and other tax matters.

Answer c:

Concerning the steps that are involved with the financial manager includes the lodging of the BAS

either with the help of electronically or with the help of the nil lodgement on the phone.

Additionally, the financial managers can pay electronically either with the help of mail or in person

that are at the Australian post.

10.Use the following information to prepare a bank reconciliation for KLM company.

Closing account balance 30.6.20xx, $68,000

Unpresented cheques:

Number 100 $5,000

Number 101 $5,000

Number 102 $3,000

Number 103 $4,000

KLM Bank Statement extract

Australian Harbour International College, 114-120 Castlereagh Street, Sydney NSW 2000, Australia

|RTO NO: 41338 | CRICOS Provider Code: 03449J

Filename FNSACC501-Provide Financial and Business Performance

Information

Version 3.0/ July 2017 Review Date: Aug

2018

Page 12 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.