Diploma in Finance and Mortgage Broking: Assignment Solution Analysis

VerifiedAdded on 2021/04/17

|7

|1754

|35

Homework Assignment

AI Summary

This document provides a comprehensive solution to a Diploma in Finance and Mortgage Broking assignment. It begins with a detailed analysis of financial ratios, including current ratio, quick ratio, return on equity, debt-to-equity ratio, and interest cover ratio, with calculations and interpretations for 2016 and 2017. The assignment further explores different types of trusts (unit, discretionary, hybrid, and family trusts), company legal requirements, and financial statements such as balance sheets, profit and loss statements, and cash flow statements. It also defines key financial terms like depreciation, liquidity ratios, and assets and liabilities. The assignment also delves into various financing methods including commercial bank bills, invoice financing, chattel mortgages, and equipment finance. Finally, it outlines the principles of risk management and risk categorization for effective financial management.

Running Head: DIPLOMA IN FINANCE AND MORTGAGE BROKING

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Diploma in finance and mortgage broking 1

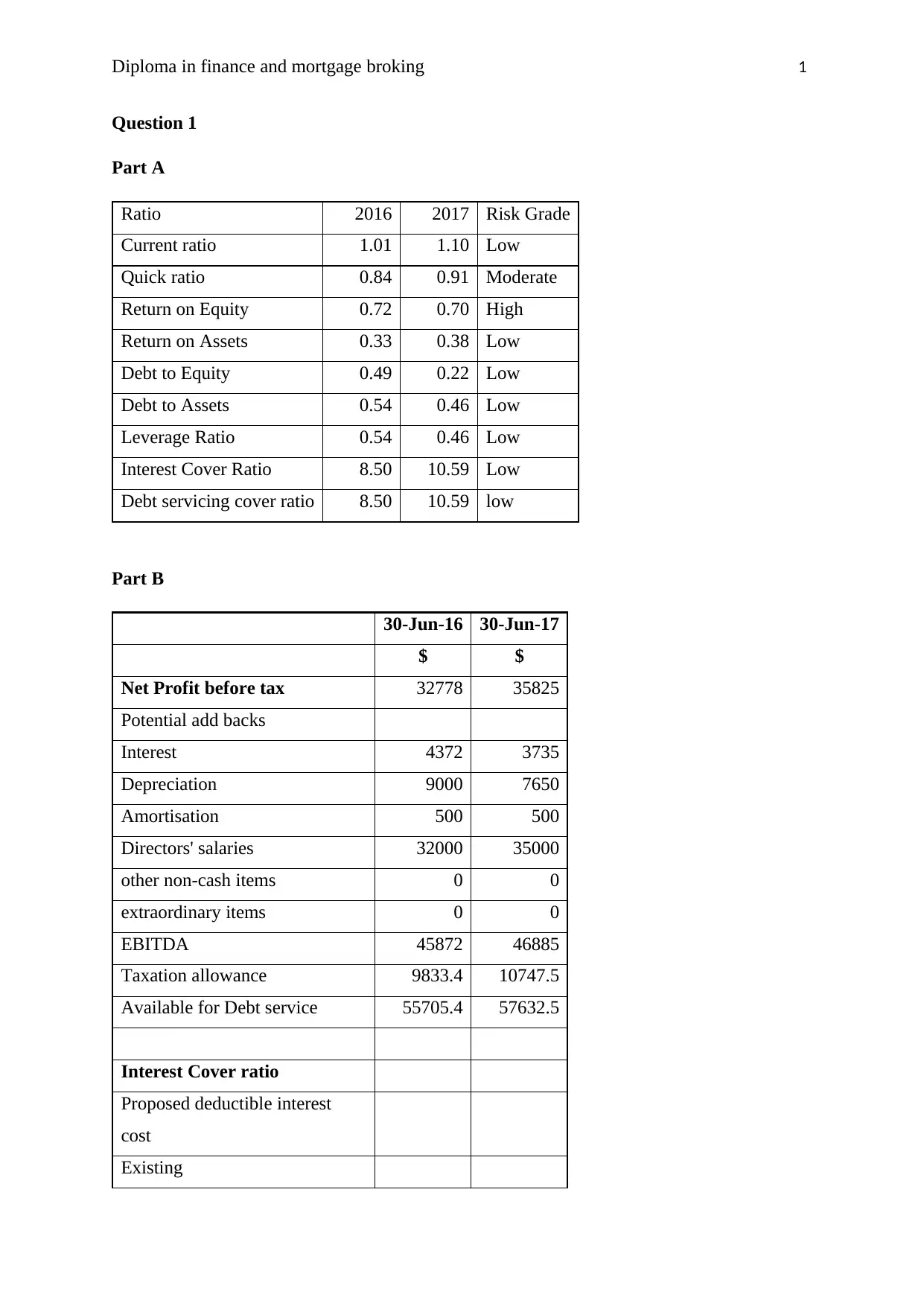

Question 1

Part A

Ratio 2016 2017 Risk Grade

Current ratio 1.01 1.10 Low

Quick ratio 0.84 0.91 Moderate

Return on Equity 0.72 0.70 High

Return on Assets 0.33 0.38 Low

Debt to Equity 0.49 0.22 Low

Debt to Assets 0.54 0.46 Low

Leverage Ratio 0.54 0.46 Low

Interest Cover Ratio 8.50 10.59 Low

Debt servicing cover ratio 8.50 10.59 low

Part B

30-Jun-16 30-Jun-17

$ $

Net Profit before tax 32778 35825

Potential add backs

Interest 4372 3735

Depreciation 9000 7650

Amortisation 500 500

Directors' salaries 32000 35000

other non-cash items 0 0

extraordinary items 0 0

EBITDA 45872 46885

Taxation allowance 9833.4 10747.5

Available for Debt service 55705.4 57632.5

Interest Cover ratio

Proposed deductible interest

cost

Existing

Question 1

Part A

Ratio 2016 2017 Risk Grade

Current ratio 1.01 1.10 Low

Quick ratio 0.84 0.91 Moderate

Return on Equity 0.72 0.70 High

Return on Assets 0.33 0.38 Low

Debt to Equity 0.49 0.22 Low

Debt to Assets 0.54 0.46 Low

Leverage Ratio 0.54 0.46 Low

Interest Cover Ratio 8.50 10.59 Low

Debt servicing cover ratio 8.50 10.59 low

Part B

30-Jun-16 30-Jun-17

$ $

Net Profit before tax 32778 35825

Potential add backs

Interest 4372 3735

Depreciation 9000 7650

Amortisation 500 500

Directors' salaries 32000 35000

other non-cash items 0 0

extraordinary items 0 0

EBITDA 45872 46885

Taxation allowance 9833.4 10747.5

Available for Debt service 55705.4 57632.5

Interest Cover ratio

Proposed deductible interest

cost

Existing

Diploma in finance and mortgage broking 2

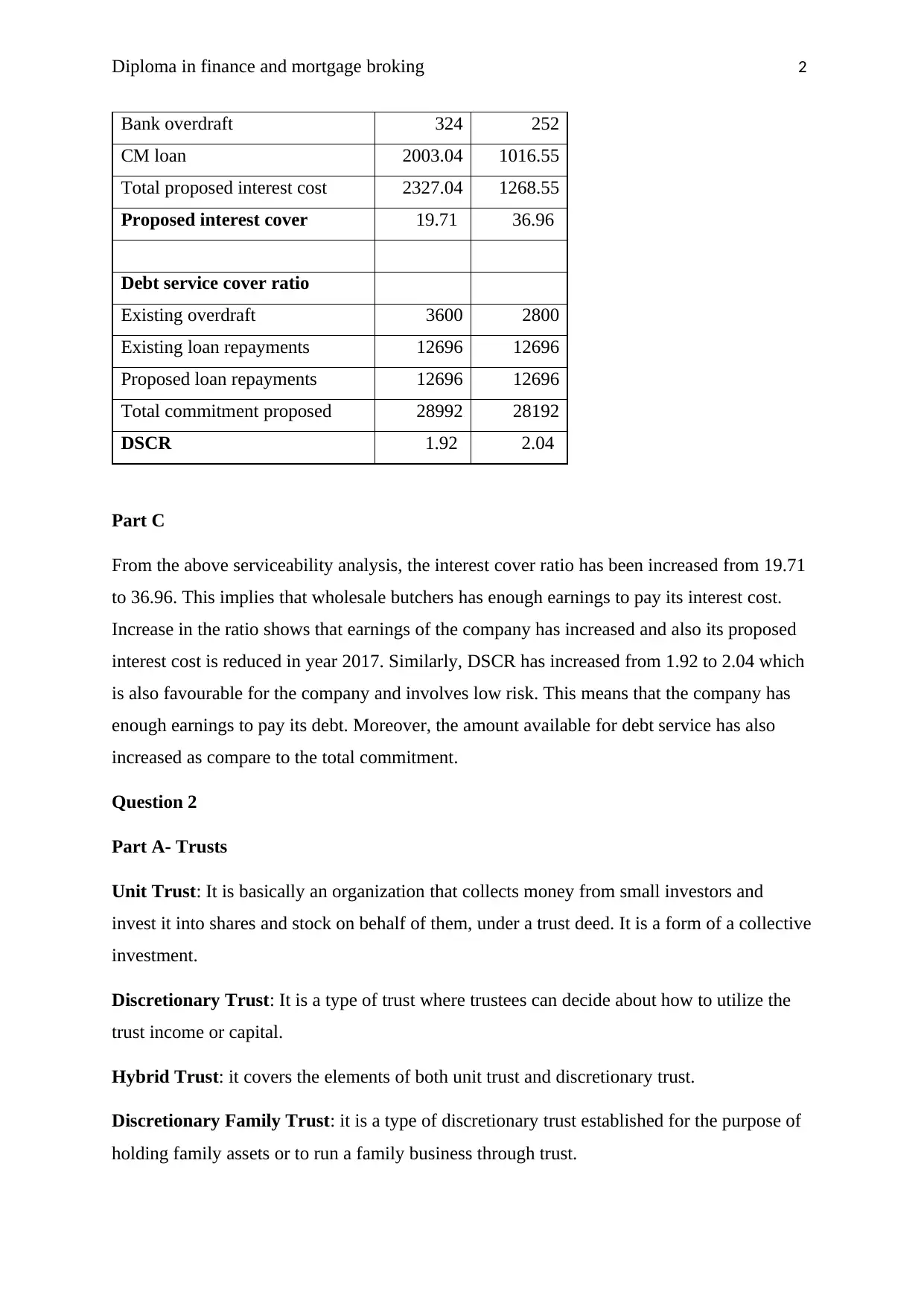

Bank overdraft 324 252

CM loan 2003.04 1016.55

Total proposed interest cost 2327.04 1268.55

Proposed interest cover 19.71 36.96

Debt service cover ratio

Existing overdraft 3600 2800

Existing loan repayments 12696 12696

Proposed loan repayments 12696 12696

Total commitment proposed 28992 28192

DSCR 1.92 2.04

Part C

From the above serviceability analysis, the interest cover ratio has been increased from 19.71

to 36.96. This implies that wholesale butchers has enough earnings to pay its interest cost.

Increase in the ratio shows that earnings of the company has increased and also its proposed

interest cost is reduced in year 2017. Similarly, DSCR has increased from 1.92 to 2.04 which

is also favourable for the company and involves low risk. This means that the company has

enough earnings to pay its debt. Moreover, the amount available for debt service has also

increased as compare to the total commitment.

Question 2

Part A- Trusts

Unit Trust: It is basically an organization that collects money from small investors and

invest it into shares and stock on behalf of them, under a trust deed. It is a form of a collective

investment.

Discretionary Trust: It is a type of trust where trustees can decide about how to utilize the

trust income or capital.

Hybrid Trust: it covers the elements of both unit trust and discretionary trust.

Discretionary Family Trust: it is a type of discretionary trust established for the purpose of

holding family assets or to run a family business through trust.

Bank overdraft 324 252

CM loan 2003.04 1016.55

Total proposed interest cost 2327.04 1268.55

Proposed interest cover 19.71 36.96

Debt service cover ratio

Existing overdraft 3600 2800

Existing loan repayments 12696 12696

Proposed loan repayments 12696 12696

Total commitment proposed 28992 28192

DSCR 1.92 2.04

Part C

From the above serviceability analysis, the interest cover ratio has been increased from 19.71

to 36.96. This implies that wholesale butchers has enough earnings to pay its interest cost.

Increase in the ratio shows that earnings of the company has increased and also its proposed

interest cost is reduced in year 2017. Similarly, DSCR has increased from 1.92 to 2.04 which

is also favourable for the company and involves low risk. This means that the company has

enough earnings to pay its debt. Moreover, the amount available for debt service has also

increased as compare to the total commitment.

Question 2

Part A- Trusts

Unit Trust: It is basically an organization that collects money from small investors and

invest it into shares and stock on behalf of them, under a trust deed. It is a form of a collective

investment.

Discretionary Trust: It is a type of trust where trustees can decide about how to utilize the

trust income or capital.

Hybrid Trust: it covers the elements of both unit trust and discretionary trust.

Discretionary Family Trust: it is a type of discretionary trust established for the purpose of

holding family assets or to run a family business through trust.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Diploma in finance and mortgage broking 3

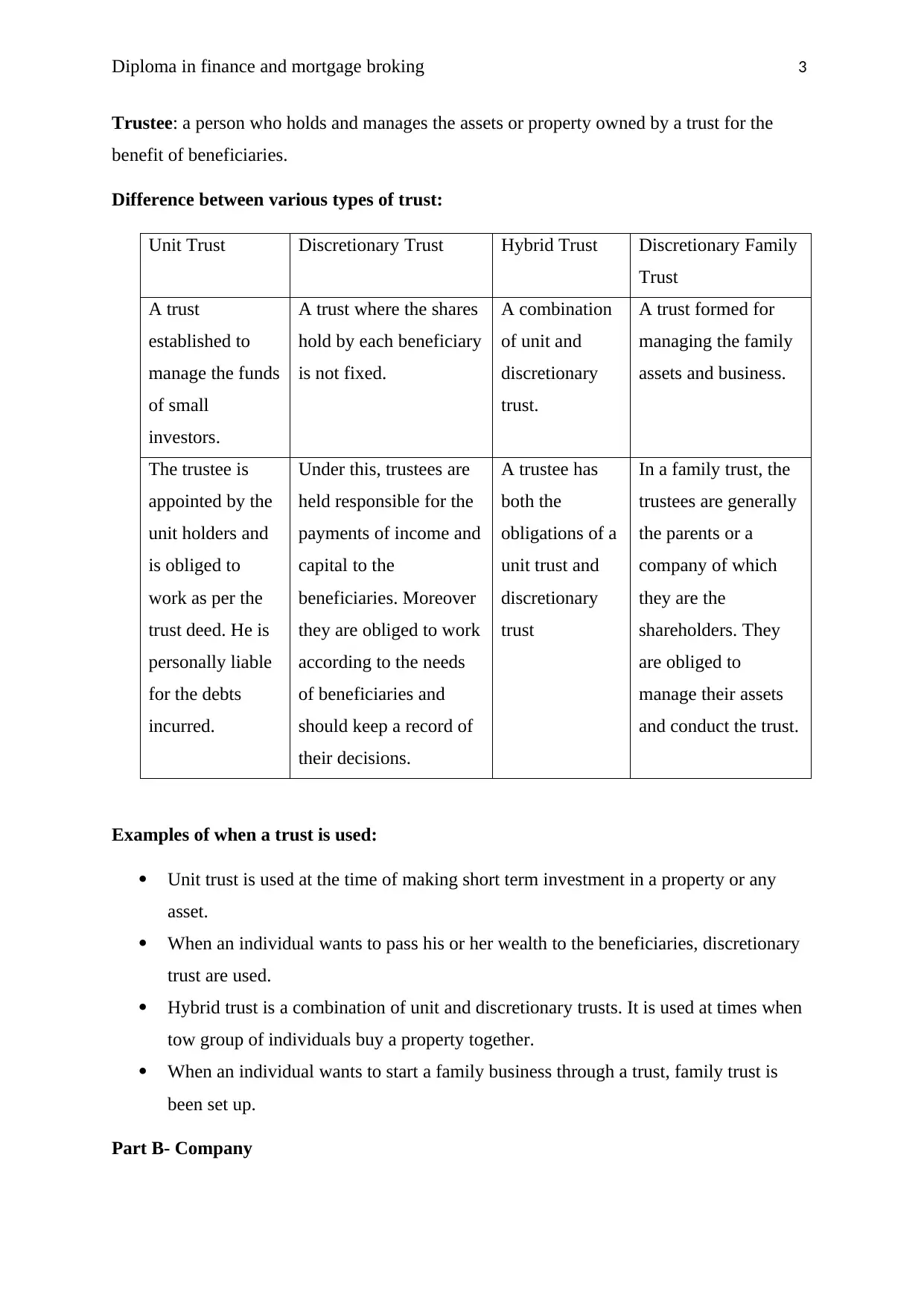

Trustee: a person who holds and manages the assets or property owned by a trust for the

benefit of beneficiaries.

Difference between various types of trust:

Unit Trust Discretionary Trust Hybrid Trust Discretionary Family

Trust

A trust

established to

manage the funds

of small

investors.

A trust where the shares

hold by each beneficiary

is not fixed.

A combination

of unit and

discretionary

trust.

A trust formed for

managing the family

assets and business.

The trustee is

appointed by the

unit holders and

is obliged to

work as per the

trust deed. He is

personally liable

for the debts

incurred.

Under this, trustees are

held responsible for the

payments of income and

capital to the

beneficiaries. Moreover

they are obliged to work

according to the needs

of beneficiaries and

should keep a record of

their decisions.

A trustee has

both the

obligations of a

unit trust and

discretionary

trust

In a family trust, the

trustees are generally

the parents or a

company of which

they are the

shareholders. They

are obliged to

manage their assets

and conduct the trust.

Examples of when a trust is used:

Unit trust is used at the time of making short term investment in a property or any

asset.

When an individual wants to pass his or her wealth to the beneficiaries, discretionary

trust are used.

Hybrid trust is a combination of unit and discretionary trusts. It is used at times when

tow group of individuals buy a property together.

When an individual wants to start a family business through a trust, family trust is

been set up.

Part B- Company

Trustee: a person who holds and manages the assets or property owned by a trust for the

benefit of beneficiaries.

Difference between various types of trust:

Unit Trust Discretionary Trust Hybrid Trust Discretionary Family

Trust

A trust

established to

manage the funds

of small

investors.

A trust where the shares

hold by each beneficiary

is not fixed.

A combination

of unit and

discretionary

trust.

A trust formed for

managing the family

assets and business.

The trustee is

appointed by the

unit holders and

is obliged to

work as per the

trust deed. He is

personally liable

for the debts

incurred.

Under this, trustees are

held responsible for the

payments of income and

capital to the

beneficiaries. Moreover

they are obliged to work

according to the needs

of beneficiaries and

should keep a record of

their decisions.

A trustee has

both the

obligations of a

unit trust and

discretionary

trust

In a family trust, the

trustees are generally

the parents or a

company of which

they are the

shareholders. They

are obliged to

manage their assets

and conduct the trust.

Examples of when a trust is used:

Unit trust is used at the time of making short term investment in a property or any

asset.

When an individual wants to pass his or her wealth to the beneficiaries, discretionary

trust are used.

Hybrid trust is a combination of unit and discretionary trusts. It is used at times when

tow group of individuals buy a property together.

When an individual wants to start a family business through a trust, family trust is

been set up.

Part B- Company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Diploma in finance and mortgage broking 4

Legal requirements:

Must have a registered office should inform to ASIC about its location.

Personal details of all the directors should be provided to ASIC

Keeping up to date, the financial records.

At time of registration, company is required to pay a certain fees to ASIC.

Inform ASIC about the changes in the business and also checking the accuracy

of annual statements.

Personal obligations of a director as per law is that he or she has to act in the best interest

of the company, avoid conflicts between personal interest and company’s interest, to protect

the company from being insolvent and to perform the duties with due care and diligence.

A person who is 18 years old and above and also ready to undertake the roles and

responsibility of a director.

In a proprietary company, at least one director is required and in public company, at least

three are required.

Question 3

Balance sheet: It reflects the balances of all the accounts prepared by the company during a

fiscal year. It represents the true and fair view of company’s profitability and financial

stability.

Profit and loss statement: The account shows all the incomes earned and expenses incurred

by a company. The net difference between these income and expenses is reported as a profit

or loss in the income statement.

Depreciation: it is a kind of expense charged on the life of an asset. It reduces the value of an

asset over the time and also known as a method of reallocating the cost of a tangible asset

over its life.

Liquidity Ratio: it is a ratio calculated for measuring the liquidity of the company. It shows

the ability of a company to pay its short term financial obligations with its current assets.

Current Ratio: it measures the portion of company’s Current assets against its current

liabilities. The ideal CR is 2:1 which implies that the value of business’s current assets should

be double of its current liabilities (Weil, Schipper & Francis, 2013).

Legal requirements:

Must have a registered office should inform to ASIC about its location.

Personal details of all the directors should be provided to ASIC

Keeping up to date, the financial records.

At time of registration, company is required to pay a certain fees to ASIC.

Inform ASIC about the changes in the business and also checking the accuracy

of annual statements.

Personal obligations of a director as per law is that he or she has to act in the best interest

of the company, avoid conflicts between personal interest and company’s interest, to protect

the company from being insolvent and to perform the duties with due care and diligence.

A person who is 18 years old and above and also ready to undertake the roles and

responsibility of a director.

In a proprietary company, at least one director is required and in public company, at least

three are required.

Question 3

Balance sheet: It reflects the balances of all the accounts prepared by the company during a

fiscal year. It represents the true and fair view of company’s profitability and financial

stability.

Profit and loss statement: The account shows all the incomes earned and expenses incurred

by a company. The net difference between these income and expenses is reported as a profit

or loss in the income statement.

Depreciation: it is a kind of expense charged on the life of an asset. It reduces the value of an

asset over the time and also known as a method of reallocating the cost of a tangible asset

over its life.

Liquidity Ratio: it is a ratio calculated for measuring the liquidity of the company. It shows

the ability of a company to pay its short term financial obligations with its current assets.

Current Ratio: it measures the portion of company’s Current assets against its current

liabilities. The ideal CR is 2:1 which implies that the value of business’s current assets should

be double of its current liabilities (Weil, Schipper & Francis, 2013).

Diploma in finance and mortgage broking 5

Debt to Equity Ratio: it is one of the financial leverage ratio which shows that how much of

the company’s assets are been financed through debt and how much are financed through

equity.

Cash flow Statement: A statement which shows the outflow and inflow of cash from

operating. Investing and financing activities.

Asset: an item owned by a business which has its own value and is used for paying debts or

legacies.

Liability: A financial debt or an obligation for a company, arises during the course of its

operations.

Net profit: The figure is determined by deducting all the operating expenses from the total

revenue earned by the business.

Equity: it is simply means ownership in the business. It is an accounting difference between

total liabilities and total assets.

As per Australian taxation, allowable expenses are travel expenses, gifts and donations,

interest, dividend, investment income, clothing expenses, home office expenses, tools and

equipment and other deductions for specific industries

Question 4

Commercial bank bill: a bill of exchange issued by a commercial bank for helping in raising

finance for the purpose of investment. For example, for purpose of financing the working

capital requirements, company borrows through bank bills.

Invoice or Factoring finance: it is a method for raising finance, used by the companies, in

which accounts receivables of the business are sold to a third party known as factor.

Chattel mortgage: It is a loan provided to the individual on a moveable property. For

example, business can raise finance for purchasing a heavy machinery by giving a security

interest in machinery to the seller. So in case of default, the seller can sell the machine to

recover the loss.

Equipment Finance: it is a loan used for purchasing or borrowing a physical asset for the

business. Method of financing are Equipment loan and equipment leasing.

Question 5

Debt to Equity Ratio: it is one of the financial leverage ratio which shows that how much of

the company’s assets are been financed through debt and how much are financed through

equity.

Cash flow Statement: A statement which shows the outflow and inflow of cash from

operating. Investing and financing activities.

Asset: an item owned by a business which has its own value and is used for paying debts or

legacies.

Liability: A financial debt or an obligation for a company, arises during the course of its

operations.

Net profit: The figure is determined by deducting all the operating expenses from the total

revenue earned by the business.

Equity: it is simply means ownership in the business. It is an accounting difference between

total liabilities and total assets.

As per Australian taxation, allowable expenses are travel expenses, gifts and donations,

interest, dividend, investment income, clothing expenses, home office expenses, tools and

equipment and other deductions for specific industries

Question 4

Commercial bank bill: a bill of exchange issued by a commercial bank for helping in raising

finance for the purpose of investment. For example, for purpose of financing the working

capital requirements, company borrows through bank bills.

Invoice or Factoring finance: it is a method for raising finance, used by the companies, in

which accounts receivables of the business are sold to a third party known as factor.

Chattel mortgage: It is a loan provided to the individual on a moveable property. For

example, business can raise finance for purchasing a heavy machinery by giving a security

interest in machinery to the seller. So in case of default, the seller can sell the machine to

recover the loss.

Equipment Finance: it is a loan used for purchasing or borrowing a physical asset for the

business. Method of financing are Equipment loan and equipment leasing.

Question 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Diploma in finance and mortgage broking 6

Principle Outline of principle

Creates and protect

value

Through continuous review of risk management process and

system, agency’s objective can be easily achieved.

Integral part of

organization

processes.

This principle says that, risk management must integrate with the

framework of government and be a part of its planning process.

A part of decision

making

Risk management help the decision makers in selecting appropriate

option and also in identifying the priorities.

Addressing

uncertainty

Identification of potential risk, helps the agencies to implement

controls and treatment for minimising the chances of loss.

Systematic,

structured and

timely process

Risk management process should remain consistent across the

agency for ensuring efficiency and reliability of the results.

Transparent and

inclusive.

Stakeholder’s engagement in the risk management process implies

that proper communication and transparency is there in course of

identifying and analysing the risk (Australian Government. 2010).

Question 6

In the process of risk management, it is very necessary to categorize the various risks

into a common area, as this will facilitate a structured and systematic approach in

identification of the risks.

Risk categorization enables the management to enhance their focus on the wider

range of risks. Moreover, the managers can identify all the risk in a very systematic

and consistent manner.

It makes the risk assessment easier as the categories enable the meeting and

interviews with the people who are familiar with a specific risk category.

Categorization of the risk helps in greater controlling and monitoring the identified

risk classified under same area.

Principle Outline of principle

Creates and protect

value

Through continuous review of risk management process and

system, agency’s objective can be easily achieved.

Integral part of

organization

processes.

This principle says that, risk management must integrate with the

framework of government and be a part of its planning process.

A part of decision

making

Risk management help the decision makers in selecting appropriate

option and also in identifying the priorities.

Addressing

uncertainty

Identification of potential risk, helps the agencies to implement

controls and treatment for minimising the chances of loss.

Systematic,

structured and

timely process

Risk management process should remain consistent across the

agency for ensuring efficiency and reliability of the results.

Transparent and

inclusive.

Stakeholder’s engagement in the risk management process implies

that proper communication and transparency is there in course of

identifying and analysing the risk (Australian Government. 2010).

Question 6

In the process of risk management, it is very necessary to categorize the various risks

into a common area, as this will facilitate a structured and systematic approach in

identification of the risks.

Risk categorization enables the management to enhance their focus on the wider

range of risks. Moreover, the managers can identify all the risk in a very systematic

and consistent manner.

It makes the risk assessment easier as the categories enable the meeting and

interviews with the people who are familiar with a specific risk category.

Categorization of the risk helps in greater controlling and monitoring the identified

risk classified under same area.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.