DIPMB3_AS_v2 Business Management Skills: CCF & MB Case Study

VerifiedAdded on 2023/04/23

|35

|15450

|367

Report

AI Summary

This document presents a solved written assignment focusing on Business Management Skills, utilizing the Capital City Finance and Mortgage Brokers (CCF & MB) case study. The assignment addresses key areas such as developing client relationships, growing the business, identifying and managing risks, improving business processes, managing people performance, and demonstrating leadership. The solution provides insights into strategic alliances with real estate agents, accountants, and legal firms, as well as consolidating relationships with existing partners. It also covers the company's vision, mission, values, and the roles of its employees. The student's initial attempt is assessed, with feedback provided for improvement in specific tasks related to risk management, people performance, and leadership. Desklib offers this and other solved assignments to aid students in their studies.

Written Assignment

Business Management Skills

(DIPMB3_AS_v2)

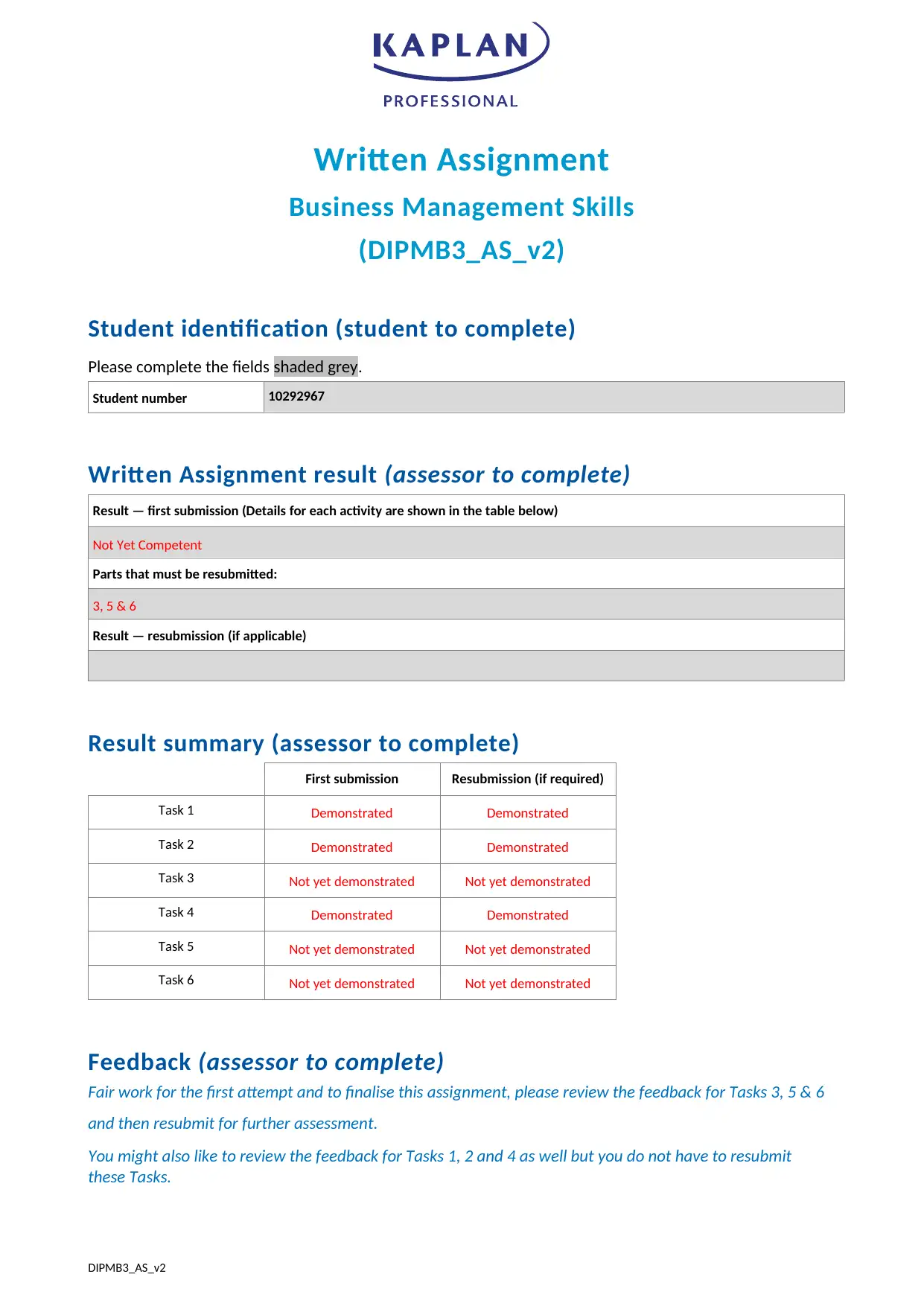

Student identification (student to complete)

Please complete the fields shaded grey.

Student number 10292967

Written Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Not Yet Competent

Parts that must be resubmitted:

3, 5 & 6

Result — resubmission (if applicable)

Result summary (assessor to complete)

First submission Resubmission (if required)

Task 1 Demonstrated Demonstrated

Task 2 Demonstrated Demonstrated

Task 3 Not yet demonstrated Not yet demonstrated

Task 4 Demonstrated Demonstrated

Task 5 Not yet demonstrated Not yet demonstrated

Task 6 Not yet demonstrated Not yet demonstrated

Feedback (assessor to complete)

Fair work for the first attempt and to finalise this assignment, please review the feedback for Tasks 3, 5 & 6

and then resubmit for further assessment.

You might also like to review the feedback for Tasks 1, 2 and 4 as well but you do not have to resubmit

these Tasks.

DIPMB3_AS_v2

Business Management Skills

(DIPMB3_AS_v2)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number 10292967

Written Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Not Yet Competent

Parts that must be resubmitted:

3, 5 & 6

Result — resubmission (if applicable)

Result summary (assessor to complete)

First submission Resubmission (if required)

Task 1 Demonstrated Demonstrated

Task 2 Demonstrated Demonstrated

Task 3 Not yet demonstrated Not yet demonstrated

Task 4 Demonstrated Demonstrated

Task 5 Not yet demonstrated Not yet demonstrated

Task 6 Not yet demonstrated Not yet demonstrated

Feedback (assessor to complete)

Fair work for the first attempt and to finalise this assignment, please review the feedback for Tasks 3, 5 & 6

and then resubmit for further assessment.

You might also like to review the feedback for Tasks 1, 2 and 4 as well but you do not have to resubmit

these Tasks.

DIPMB3_AS_v2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Before you begin

Read everything in this document before you start your written assignment for Business Management Skills

(DIPMB3_AS_v2).

About this document

This document includes the following parts:

• Instructions for completing and submitting this assignment

• CCF & MB case study and tasks covering Business Management Skills:

• Task 1 — Developing and nurturing relationships with clients, other professionals and third-party referrers

• Task 2 — Growing the business

• Task 3 — Identifying risk and applying risk management processes

• Task 4— Improving the business

• Task 5 —Managing people performance

• Task 6 — Showing leadership in the workplace

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearn Business Management

Skills (DIPMB3v2) subject room.

Page 2 of 35

Read everything in this document before you start your written assignment for Business Management Skills

(DIPMB3_AS_v2).

About this document

This document includes the following parts:

• Instructions for completing and submitting this assignment

• CCF & MB case study and tasks covering Business Management Skills:

• Task 1 — Developing and nurturing relationships with clients, other professionals and third-party referrers

• Task 2 — Growing the business

• Task 3 — Identifying risk and applying risk management processes

• Task 4— Improving the business

• Task 5 —Managing people performance

• Task 6 — Showing leadership in the workplace

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearn Business Management

Skills (DIPMB3v2) subject room.

Page 2 of 35

Instructions for completing and submitting this written

assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Assignment_versionnumber_Submissionnumber

(e.g. 12345678_DIPMB3_AS_v2_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Submitting the written assignment

Only Microsoft Office compatible written assignments submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The written assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete written assignments will be returned to you unmarked.

The maximum file size is 20MB for the Written and Oral Assignment. Once you submit your written

assignment for marking you will be unable to make any further changes to it.

You are able to submit your written assignment earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

Please refer to the Assignment submission/resubmission instructions (pdf) in the Assessment section of

KapLearn for details on how to submit your written assignment.

Your written assignment and oral assignment must be submitted together on or before your due date.

Please check KapLearn for the due date.

The written assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

If you reach the end of your initial enrolment period and have been deemed Not Yet Competent in one or

more assessment items, then an additional 4 weeks will be granted, provided you attempted all assessment

tasks during the initial enrolment period.

Your assessor will mark your written and oral assignment and return it to you in the Business Management

Skills (DIPMB3v2) subject room in KapLearn under the ‘Assessment’ tab.

Page 3 of 35

assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Assignment_versionnumber_Submissionnumber

(e.g. 12345678_DIPMB3_AS_v2_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Submitting the written assignment

Only Microsoft Office compatible written assignments submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The written assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete written assignments will be returned to you unmarked.

The maximum file size is 20MB for the Written and Oral Assignment. Once you submit your written

assignment for marking you will be unable to make any further changes to it.

You are able to submit your written assignment earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

Please refer to the Assignment submission/resubmission instructions (pdf) in the Assessment section of

KapLearn for details on how to submit your written assignment.

Your written assignment and oral assignment must be submitted together on or before your due date.

Please check KapLearn for the due date.

The written assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

If you reach the end of your initial enrolment period and have been deemed Not Yet Competent in one or

more assessment items, then an additional 4 weeks will be granted, provided you attempted all assessment

tasks during the initial enrolment period.

Your assessor will mark your written and oral assignment and return it to you in the Business Management

Skills (DIPMB3v2) subject room in KapLearn under the ‘Assessment’ tab.

Page 3 of 35

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding

the suggested word count. Please do not include additional information which is outside the scope of

the question.

Additional research

When completing this assignment, assumptions are permitted although they must not be in conflict with

the information provided in the Case Study.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your client’s requirements, or to calculate any service fees

that may be applicable.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed written and oral assignment.

How your written assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your written assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

You must be deemed competent in all assessment items in order to be awarded your qualification,

including demonstrating competency in:

• all of the exam questions

• the written and oral assignment.

Page 4 of 35

The word count shown with each question is indicative only. You will not be penalised for exceeding

the suggested word count. Please do not include additional information which is outside the scope of

the question.

Additional research

When completing this assignment, assumptions are permitted although they must not be in conflict with

the information provided in the Case Study.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your client’s requirements, or to calculate any service fees

that may be applicable.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed written and oral assignment.

How your written assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your written assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

You must be deemed competent in all assessment items in order to be awarded your qualification,

including demonstrating competency in:

• all of the exam questions

• the written and oral assignment.

Page 4 of 35

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This written assignment is your opportunity to demonstrate your competency against these units:

Unit code Unit name

BSBRSK401 Identify risk and apply risk management processes

FNSPRM603 Grow the practice

BSBMGT502 Manage people performance

BSBMGT401 Show leadership in the workplace

FNSRSK502 Assess risks

Note that the Written and Oral Assignment is one of two assessments required to meet the requirements

of the units of competency.

We are here to help

If you have any questions about this written assignment you can post your query at the ‘Ask your Tutor’

forum in your subject room. You can expect an answer within 24 hours of your posting from one of our

technical advisers or student support staff.

Page 5 of 35

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This written assignment is your opportunity to demonstrate your competency against these units:

Unit code Unit name

BSBRSK401 Identify risk and apply risk management processes

FNSPRM603 Grow the practice

BSBMGT502 Manage people performance

BSBMGT401 Show leadership in the workplace

FNSRSK502 Assess risks

Note that the Written and Oral Assignment is one of two assessments required to meet the requirements

of the units of competency.

We are here to help

If you have any questions about this written assignment you can post your query at the ‘Ask your Tutor’

forum in your subject room. You can expect an answer within 24 hours of your posting from one of our

technical advisers or student support staff.

Page 5 of 35

Capital City Finance and Mortgage Brokers (CCF & MB)

George and Mildred are very happy with the way you service your clients and are sure that you are a good

fit for the team. They now want you to turn your focus to your primary task, which is to assist in expanding

the business by building relationships with selected real estate agents, accountants and legal firms through

strategic alliances. They also want you to consider how CCF & MB can consolidate its relationships with its

existing strategic partners.

Let’s recap on what you already know about Capital City Finance and Mortgage Brokers (CCF & MB).

It’s a family owned business providing a range of mortgage and finance broking services to the business and

private sectors, with experience in all facets of finance and insurance, providing expert advice covering a

multitude of products and options existing within the market.

CCF & MB specialises in home loans, commercial lending, business lending, personal and motor vehicle

finance and insurance (life and general), and focuses on helping clients find the finance service suited to

their individual circumstances.

It provides its services through its association with the following partners:

• Australian Aggregators: a rising company within the aggregation business, with an extensive panel of

residential and commercial lenders, and asset finance.

• ABC General Insurance: a boutique insurance company specialising in a full range of general insurances.

• XYZ Life: a small family-owned insurance brokerage specialising in the full range of life insurance

products.

Based in the city, CCF & MB has the capacity to service clients from their office or anywhere at their clients’

convenience through its team of mobile brokers.

CCF & MB does not hold a credit license but operates as a credit representative of Australian Aggregators.

Since its inception 13 years ago, CCF & MB has built a loan book of almost $1.2 billion and averages over

$120 million in new loans annually.

CCF & MB’s vision is to be the mortgage and finance broker of choice in the greater metropolitan area.

CCF & MB’s mission statement is: ‘to operate professionally in accordance with legislation, our licence and

professional standards’.

CCF & MB’s values are as follows:

• to act with honesty and integrity at all times

• to provide unbiased advice and conduct business, free from any conflict of interest

• to maintain confidentiality in all dealings

• to meet all NCCP regulatory requirements

• to comply with all mortgage industry laws and regulations

• to ensure quality and efficiency in its loan processes.

Page 6 of 35

George and Mildred are very happy with the way you service your clients and are sure that you are a good

fit for the team. They now want you to turn your focus to your primary task, which is to assist in expanding

the business by building relationships with selected real estate agents, accountants and legal firms through

strategic alliances. They also want you to consider how CCF & MB can consolidate its relationships with its

existing strategic partners.

Let’s recap on what you already know about Capital City Finance and Mortgage Brokers (CCF & MB).

It’s a family owned business providing a range of mortgage and finance broking services to the business and

private sectors, with experience in all facets of finance and insurance, providing expert advice covering a

multitude of products and options existing within the market.

CCF & MB specialises in home loans, commercial lending, business lending, personal and motor vehicle

finance and insurance (life and general), and focuses on helping clients find the finance service suited to

their individual circumstances.

It provides its services through its association with the following partners:

• Australian Aggregators: a rising company within the aggregation business, with an extensive panel of

residential and commercial lenders, and asset finance.

• ABC General Insurance: a boutique insurance company specialising in a full range of general insurances.

• XYZ Life: a small family-owned insurance brokerage specialising in the full range of life insurance

products.

Based in the city, CCF & MB has the capacity to service clients from their office or anywhere at their clients’

convenience through its team of mobile brokers.

CCF & MB does not hold a credit license but operates as a credit representative of Australian Aggregators.

Since its inception 13 years ago, CCF & MB has built a loan book of almost $1.2 billion and averages over

$120 million in new loans annually.

CCF & MB’s vision is to be the mortgage and finance broker of choice in the greater metropolitan area.

CCF & MB’s mission statement is: ‘to operate professionally in accordance with legislation, our licence and

professional standards’.

CCF & MB’s values are as follows:

• to act with honesty and integrity at all times

• to provide unbiased advice and conduct business, free from any conflict of interest

• to maintain confidentiality in all dealings

• to meet all NCCP regulatory requirements

• to comply with all mortgage industry laws and regulations

• to ensure quality and efficiency in its loan processes.

Page 6 of 35

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CCF & MB’s people

CCF & MB is owned by husband and wife, George and Mildred Spencer.

With over 35 years experience in finance and business ownership, George established and built a successful

business dedicated to assisting clients with managing their finances effectively. Starting the business with

his wife Mildred 13 years ago, George gained immense satisfaction in seeing it expand, to service more and

more clients across the city and greater metropolitan area. Although in recent years he has stepped back

from dealing directly with clients, he still maintains a small select clientele. He also takes great pride in

training and mentoring his team to enhance their performance.

Mildred has over 22 years of lending experience and is qualified, not only to assist her clients with their

mortgage requirements, but also to assist them with their commercial finance requirements. She also holds

financial planning qualifications. She specialises in asset finance.

The company has a small team of five additional consultants and two administration staff members.

Profiles for the team are as follows:

• Jennifer Dee is recognised as one of the top female brokers in Australia. She has been in the broking

industry for over 10 years and has a passion and dedication to assist and accommodate all of her clients’

needs with their financial dreams. Jennifer is an Accredited Mortgage Consultant with the Mortgage and

Finance Association of Australia (MFAA).

• Louise Spencer (George and Mildred’s eldest daughter) is an Accredited Mortgage Consultant with the

Mortgage and Finance Association of Australia (MFAA) and has been working as a loan consultant for

almost two years. Louise started off in the lending industry in the office as an administrator to gain as

much experience and knowledge as possible before taking a broking role. Her passion for helping her

clients ensures that she is always available to her clients at a time and place convenient for them.

• Michael Spencer is George’s younger brother and is CCF & MB’s equipment finance specialist. He has

over 25 years working in the equipment finance industry. He has developed an in-depth understanding

of the transport and agricultural industries, and also provides finance for general equipment,

motor vehicles and computer equipment.

• Martin Long has specialised in equipment finance for the last three years, but prior to this he spent

five years operating his own retail food business. This practical experience allows him to see things from

his client’s point of view, including experience with equipment finance. He specialises in plant and

equipment in the machinery, woodworking and packaging industries. Examples of some of the

equipment he has financed are farm machinery, extrusion lines, plastic injection moulders,

commercial catering equipment, woodworking plant, packaging lines, forklifts, office fit-outs and many

different motor vehicles.

• Luis Ramirez migrated to Australia as a young boy; 25 years ago with his family. After completing

high school he graduated from university with an accounting degree and worked in ANZ in commercial

lending. He joined CCF & MB four years ago and specialises in vehicle and capital equipment financing.

He provides ITC and general equipment lease funding options for clients. By providing better outcomes,

both during and at the end of their equipment leases, Luis’ many clients have been able to reduce costs

and maximise the value of their available budgets.

CCF & MB is a member of the MFAA, as a broking business dealing directly with the public. Both George

and Mildred are fellows of the MFAA. CCF & MB is also a corporate member of the FBAA.

All staff members, including consultants, are paid an annual salary plus superannuation. Consultants also

receive a car allowance plus a percentage of trail commissions, which are paid quarterly based on their

performance targets.

Page 7 of 35

CCF & MB is owned by husband and wife, George and Mildred Spencer.

With over 35 years experience in finance and business ownership, George established and built a successful

business dedicated to assisting clients with managing their finances effectively. Starting the business with

his wife Mildred 13 years ago, George gained immense satisfaction in seeing it expand, to service more and

more clients across the city and greater metropolitan area. Although in recent years he has stepped back

from dealing directly with clients, he still maintains a small select clientele. He also takes great pride in

training and mentoring his team to enhance their performance.

Mildred has over 22 years of lending experience and is qualified, not only to assist her clients with their

mortgage requirements, but also to assist them with their commercial finance requirements. She also holds

financial planning qualifications. She specialises in asset finance.

The company has a small team of five additional consultants and two administration staff members.

Profiles for the team are as follows:

• Jennifer Dee is recognised as one of the top female brokers in Australia. She has been in the broking

industry for over 10 years and has a passion and dedication to assist and accommodate all of her clients’

needs with their financial dreams. Jennifer is an Accredited Mortgage Consultant with the Mortgage and

Finance Association of Australia (MFAA).

• Louise Spencer (George and Mildred’s eldest daughter) is an Accredited Mortgage Consultant with the

Mortgage and Finance Association of Australia (MFAA) and has been working as a loan consultant for

almost two years. Louise started off in the lending industry in the office as an administrator to gain as

much experience and knowledge as possible before taking a broking role. Her passion for helping her

clients ensures that she is always available to her clients at a time and place convenient for them.

• Michael Spencer is George’s younger brother and is CCF & MB’s equipment finance specialist. He has

over 25 years working in the equipment finance industry. He has developed an in-depth understanding

of the transport and agricultural industries, and also provides finance for general equipment,

motor vehicles and computer equipment.

• Martin Long has specialised in equipment finance for the last three years, but prior to this he spent

five years operating his own retail food business. This practical experience allows him to see things from

his client’s point of view, including experience with equipment finance. He specialises in plant and

equipment in the machinery, woodworking and packaging industries. Examples of some of the

equipment he has financed are farm machinery, extrusion lines, plastic injection moulders,

commercial catering equipment, woodworking plant, packaging lines, forklifts, office fit-outs and many

different motor vehicles.

• Luis Ramirez migrated to Australia as a young boy; 25 years ago with his family. After completing

high school he graduated from university with an accounting degree and worked in ANZ in commercial

lending. He joined CCF & MB four years ago and specialises in vehicle and capital equipment financing.

He provides ITC and general equipment lease funding options for clients. By providing better outcomes,

both during and at the end of their equipment leases, Luis’ many clients have been able to reduce costs

and maximise the value of their available budgets.

CCF & MB is a member of the MFAA, as a broking business dealing directly with the public. Both George

and Mildred are fellows of the MFAA. CCF & MB is also a corporate member of the FBAA.

All staff members, including consultants, are paid an annual salary plus superannuation. Consultants also

receive a car allowance plus a percentage of trail commissions, which are paid quarterly based on their

performance targets.

Page 7 of 35

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

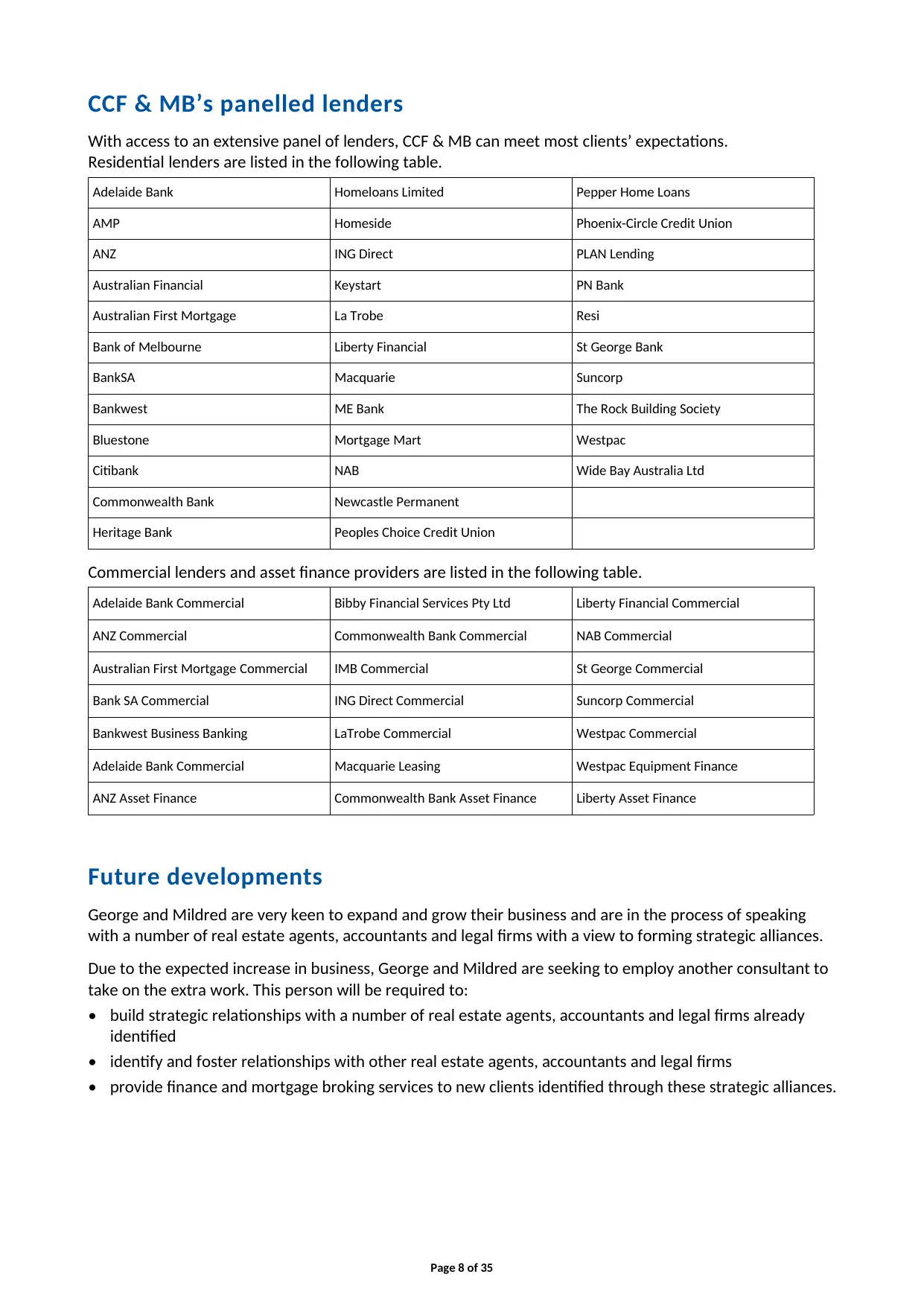

CCF & MB’s panelled lenders

With access to an extensive panel of lenders, CCF & MB can meet most clients’ expectations.

Residential lenders are listed in the following table.

Adelaide Bank Homeloans Limited Pepper Home Loans

AMP Homeside Phoenix-Circle Credit Union

ANZ ING Direct PLAN Lending

Australian Financial Keystart PN Bank

Australian First Mortgage La Trobe Resi

Bank of Melbourne Liberty Financial St George Bank

BankSA Macquarie Suncorp

Bankwest ME Bank The Rock Building Society

Bluestone Mortgage Mart Westpac

Citibank NAB Wide Bay Australia Ltd

Commonwealth Bank Newcastle Permanent

Heritage Bank Peoples Choice Credit Union

Commercial lenders and asset finance providers are listed in the following table.

Adelaide Bank Commercial Bibby Financial Services Pty Ltd Liberty Financial Commercial

ANZ Commercial Commonwealth Bank Commercial NAB Commercial

Australian First Mortgage Commercial IMB Commercial St George Commercial

Bank SA Commercial ING Direct Commercial Suncorp Commercial

Bankwest Business Banking LaTrobe Commercial Westpac Commercial

Adelaide Bank Commercial Macquarie Leasing Westpac Equipment Finance

ANZ Asset Finance Commonwealth Bank Asset Finance Liberty Asset Finance

Future developments

George and Mildred are very keen to expand and grow their business and are in the process of speaking

with a number of real estate agents, accountants and legal firms with a view to forming strategic alliances.

Due to the expected increase in business, George and Mildred are seeking to employ another consultant to

take on the extra work. This person will be required to:

• build strategic relationships with a number of real estate agents, accountants and legal firms already

identified

• identify and foster relationships with other real estate agents, accountants and legal firms

• provide finance and mortgage broking services to new clients identified through these strategic alliances.

Page 8 of 35

With access to an extensive panel of lenders, CCF & MB can meet most clients’ expectations.

Residential lenders are listed in the following table.

Adelaide Bank Homeloans Limited Pepper Home Loans

AMP Homeside Phoenix-Circle Credit Union

ANZ ING Direct PLAN Lending

Australian Financial Keystart PN Bank

Australian First Mortgage La Trobe Resi

Bank of Melbourne Liberty Financial St George Bank

BankSA Macquarie Suncorp

Bankwest ME Bank The Rock Building Society

Bluestone Mortgage Mart Westpac

Citibank NAB Wide Bay Australia Ltd

Commonwealth Bank Newcastle Permanent

Heritage Bank Peoples Choice Credit Union

Commercial lenders and asset finance providers are listed in the following table.

Adelaide Bank Commercial Bibby Financial Services Pty Ltd Liberty Financial Commercial

ANZ Commercial Commonwealth Bank Commercial NAB Commercial

Australian First Mortgage Commercial IMB Commercial St George Commercial

Bank SA Commercial ING Direct Commercial Suncorp Commercial

Bankwest Business Banking LaTrobe Commercial Westpac Commercial

Adelaide Bank Commercial Macquarie Leasing Westpac Equipment Finance

ANZ Asset Finance Commonwealth Bank Asset Finance Liberty Asset Finance

Future developments

George and Mildred are very keen to expand and grow their business and are in the process of speaking

with a number of real estate agents, accountants and legal firms with a view to forming strategic alliances.

Due to the expected increase in business, George and Mildred are seeking to employ another consultant to

take on the extra work. This person will be required to:

• build strategic relationships with a number of real estate agents, accountants and legal firms already

identified

• identify and foster relationships with other real estate agents, accountants and legal firms

• provide finance and mortgage broking services to new clients identified through these strategic alliances.

Page 8 of 35

Business management skills

Task 1 — Developing and nurturing relationships with clients,

other professionals and third-party referrers

George and Mildred now require you to write a plan to assist in developing and nurturing relationships

with clients, other professionals and third-party referrers.

Your plan should address the following:

1. How CCF & MB’s policies and procedures and legislative, regulatory and professional codes of practice

impact on developing and nurturing relationships.

2. How you would use CCF & MB’s social, business and ethical standards to develop and maintain positive

relationships.

3. The importance of confidentiality and how you would maintain it in your dealings with colleagues,

clients and other parties.

4. How you would adjust your interpersonal style to the needs and situation of other parties.

5. How you would go about developing and maintaining business and professional networks and other

relationships to benefit the organisation; and how you would use them to identify and cultivate

relationships in order to promote and market the organisation.

6. How you could use and cooperate with other professionals and third parties to expand and enhance the

reputation of the organisation, and to identify new and improved business practices.

7. How you would build referral business through appropriate communication channels, to find and secure

new business relationships.

8. How you would identify referral needs and provide information about CCF & MB’s relevant products

and services.

9. How you would secure interviews with referral business so that the needs of clients can be met.

(1,000 words)

You may use any format for your plan but you are not permitted to simply answer the points above. If you

are unsure as to how to write a plan, you can refer to the Business Growth and Marketing topic and use the

suggested SMEAC format outlined in Part 6, Section 13. Remember also the SMART principles.

When completing this task, assumptions are permitted although they must not be in conflict with the

information provided in the background information.

Student response to Task 1

The CCF&MB needs to adhere to social, legislative and regulatory framework so that appropriate

relationship can be nurtured and maintained with the clients. The are certain legislative code and

regulations which are applicable to CCF&MB and if the same are properly followed by CCF&MB than the

same would lead to better development of relations in the business. Some of the legislations and

regulations are listed below:

National Credit Code

As per section 9A of National Credit Code (NCC), the company needs to maintain a register of referrers with

the company is in agreement and it also needs to get the referral agreement signed when they are trying to

set up the referral agreement. This agreement is crucial as the same would be including discussion about

fess and benefits and all other commercial details which is related to the referrer. The referral register

needs to depict the name and contact details of the referrer, date and method of setting up an agreement.

In addition to this, the referral source and the first referral are also presented in the referral register.

Page 9 of 35

Task 1 — Developing and nurturing relationships with clients,

other professionals and third-party referrers

George and Mildred now require you to write a plan to assist in developing and nurturing relationships

with clients, other professionals and third-party referrers.

Your plan should address the following:

1. How CCF & MB’s policies and procedures and legislative, regulatory and professional codes of practice

impact on developing and nurturing relationships.

2. How you would use CCF & MB’s social, business and ethical standards to develop and maintain positive

relationships.

3. The importance of confidentiality and how you would maintain it in your dealings with colleagues,

clients and other parties.

4. How you would adjust your interpersonal style to the needs and situation of other parties.

5. How you would go about developing and maintaining business and professional networks and other

relationships to benefit the organisation; and how you would use them to identify and cultivate

relationships in order to promote and market the organisation.

6. How you could use and cooperate with other professionals and third parties to expand and enhance the

reputation of the organisation, and to identify new and improved business practices.

7. How you would build referral business through appropriate communication channels, to find and secure

new business relationships.

8. How you would identify referral needs and provide information about CCF & MB’s relevant products

and services.

9. How you would secure interviews with referral business so that the needs of clients can be met.

(1,000 words)

You may use any format for your plan but you are not permitted to simply answer the points above. If you

are unsure as to how to write a plan, you can refer to the Business Growth and Marketing topic and use the

suggested SMEAC format outlined in Part 6, Section 13. Remember also the SMART principles.

When completing this task, assumptions are permitted although they must not be in conflict with the

information provided in the background information.

Student response to Task 1

The CCF&MB needs to adhere to social, legislative and regulatory framework so that appropriate

relationship can be nurtured and maintained with the clients. The are certain legislative code and

regulations which are applicable to CCF&MB and if the same are properly followed by CCF&MB than the

same would lead to better development of relations in the business. Some of the legislations and

regulations are listed below:

National Credit Code

As per section 9A of National Credit Code (NCC), the company needs to maintain a register of referrers with

the company is in agreement and it also needs to get the referral agreement signed when they are trying to

set up the referral agreement. This agreement is crucial as the same would be including discussion about

fess and benefits and all other commercial details which is related to the referrer. The referral register

needs to depict the name and contact details of the referrer, date and method of setting up an agreement.

In addition to this, the referral source and the first referral are also presented in the referral register.

Page 9 of 35

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The rules which are set out by NCC also states that contact needs to be made with the referred customer

within a period of 10 business days. These referrals made to CCF&MB are important processes for

maintaining and nurturing relations with clients.

Australian Consumer Law

The main purpose of establishing the Australian Consumer law is to ensure that there is a fair and ethical

competition in the market is maintained and consumers are protected from malpractices of businesses. The

law applies to CCF&MB which implies that that the business should not engage in any activity which might

be unethical or misleading or deceptive. The Australia Consumer law clearly states the consumers should

not be harassed in any manner and effective sprit of competition needs to be maintained. The business of

CCF&MB needs to adhere to this code and thereby ensure that the needs of the consumers are met.

Code of Conduct and Practice

The management of CCF&MB needs to follow an established set of practices and conduct for developing

relations with the clients. The CCF&MB need to have a minimum standard and efficient training for the

employees so that the business can efficiently meet the standards of the clients and maintain an healthy

working environment.

The Anti Money Laundering and Counter Terrorism Financing

AML/CTF Act is an important act for businesses which are operating within the financial sector and

therefore appropriate adherence needs to be placed on such provisions by CCF&MB. These regulations

protect the clients from illegal practices. The obligations which are applicable on the business of CCF&MB

are listed below in point form:

Conducting due diligence in conducting the activities of the business.

Any suspicious activities or transactions needs to be checked carefully and if situation requires the

same is to be reported as well.

Adequate records are to be maintained by CCF&MB so that proper scrutiny of the same can be

done at regular intervals.

If the business of CCF&MB follows such regulations, it would be able to build strong personal relations

Anti-discrimination legislation

The above legislation is specifically imposed for the purpose of prohibiting any kind of discrimination which

is based on race, caste, creed, gender, colour, sexual preference, age, religion and belief. This legislation

states that CCF&MB needs to build relations with members of groups and clients. These are important to

be followed for building relations.

Privacy Legislations

The privacy and confidentiality of the referral partners needs to be protected which is regulated by privacy

act 1988. The act specially states businesses to maintain, collect and store information of the client

securely. CFF & MB can develop a referral process which includes a confirmation from the referral partner

to say that the client’s approval being obtained. The client files needs to protected with the help of

passwords so that appropriate data can be stored by the business.

In order to adjust to interpersonal style to the needs to situation of the other parties the following steps

can be followed by personnel:

The business needs to develop a rapport with the clients. In order to achieve this, the business should be

communicating and build relations with the client in such a manner that they are influenced. The last stage

is the stage where I can put emphasis on work collaboration.

At CCF&MB, the business is quite diverse as we have residential lending, commercial lending, motor finance

and insurance scheme. We are continuously engaged in our activities and also ensure that we can get some

referrals for building up our business. In internal network plan, cross training programs are efficient ways to

gather information and option appropriate knowledge regarding the product and help different employees

of different sections to identify referral options. In case of external network plan, we will be developing

Page 10 of 35

within a period of 10 business days. These referrals made to CCF&MB are important processes for

maintaining and nurturing relations with clients.

Australian Consumer Law

The main purpose of establishing the Australian Consumer law is to ensure that there is a fair and ethical

competition in the market is maintained and consumers are protected from malpractices of businesses. The

law applies to CCF&MB which implies that that the business should not engage in any activity which might

be unethical or misleading or deceptive. The Australia Consumer law clearly states the consumers should

not be harassed in any manner and effective sprit of competition needs to be maintained. The business of

CCF&MB needs to adhere to this code and thereby ensure that the needs of the consumers are met.

Code of Conduct and Practice

The management of CCF&MB needs to follow an established set of practices and conduct for developing

relations with the clients. The CCF&MB need to have a minimum standard and efficient training for the

employees so that the business can efficiently meet the standards of the clients and maintain an healthy

working environment.

The Anti Money Laundering and Counter Terrorism Financing

AML/CTF Act is an important act for businesses which are operating within the financial sector and

therefore appropriate adherence needs to be placed on such provisions by CCF&MB. These regulations

protect the clients from illegal practices. The obligations which are applicable on the business of CCF&MB

are listed below in point form:

Conducting due diligence in conducting the activities of the business.

Any suspicious activities or transactions needs to be checked carefully and if situation requires the

same is to be reported as well.

Adequate records are to be maintained by CCF&MB so that proper scrutiny of the same can be

done at regular intervals.

If the business of CCF&MB follows such regulations, it would be able to build strong personal relations

Anti-discrimination legislation

The above legislation is specifically imposed for the purpose of prohibiting any kind of discrimination which

is based on race, caste, creed, gender, colour, sexual preference, age, religion and belief. This legislation

states that CCF&MB needs to build relations with members of groups and clients. These are important to

be followed for building relations.

Privacy Legislations

The privacy and confidentiality of the referral partners needs to be protected which is regulated by privacy

act 1988. The act specially states businesses to maintain, collect and store information of the client

securely. CFF & MB can develop a referral process which includes a confirmation from the referral partner

to say that the client’s approval being obtained. The client files needs to protected with the help of

passwords so that appropriate data can be stored by the business.

In order to adjust to interpersonal style to the needs to situation of the other parties the following steps

can be followed by personnel:

The business needs to develop a rapport with the clients. In order to achieve this, the business should be

communicating and build relations with the client in such a manner that they are influenced. The last stage

is the stage where I can put emphasis on work collaboration.

At CCF&MB, the business is quite diverse as we have residential lending, commercial lending, motor finance

and insurance scheme. We are continuously engaged in our activities and also ensure that we can get some

referrals for building up our business. In internal network plan, cross training programs are efficient ways to

gather information and option appropriate knowledge regarding the product and help different employees

of different sections to identify referral options. In case of external network plan, we will be developing

Page 10 of 35

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

relations with professional organizations with whom we will be working closely. We will be involving local

schools, corporate houses so that the message is passed that CCF&MB can help in fulfilling objectives of

clients seeking financial advisers.

CCF&MB would be relying on quality services for enhancing the reputation of the business. Quality services

would also bring about more referrals. The business can also enter into agreements with professionals for

proper promotion of the business. I would be also recommending that CCF&MB need to create its own

linkedin account so that information regarding the professional services can be shared from such a source.

This can also turn out to be an efficient method for enhancing the reputation and client base of CCF&MB.

I believe that the people needs to know that at CCF&MB what services we provide and therefore

communication needs to made appropriately. The clients who are currently be handled by the company are

important sources as they spread the news more effective regarding the nature of the business and then

they also refer to family members. The moves which CCF&MB needs to engage in is to send text messages,

emails to past clients, new clients, potential clients for communicating the services which is provided by

CCF&MB. An opinion of a person is the best form of referral and the same can only be done by a present

client.

The identification of the referral needs of referral partners and updating them is an important aspect of the

business. For establishing this, regular contact with the partners need to be established. This will ensure

our referral partners are aware about what is happening in lending market.

Assessor feedback for Task 1: Resubmission required?

A simple structured, relatively well thought out Plan and you have

demonstrated that you are competent regarding this Task. You just spent to

much time on the legislative and regulatory requirements.

No

Page 11 of 35

schools, corporate houses so that the message is passed that CCF&MB can help in fulfilling objectives of

clients seeking financial advisers.

CCF&MB would be relying on quality services for enhancing the reputation of the business. Quality services

would also bring about more referrals. The business can also enter into agreements with professionals for

proper promotion of the business. I would be also recommending that CCF&MB need to create its own

linkedin account so that information regarding the professional services can be shared from such a source.

This can also turn out to be an efficient method for enhancing the reputation and client base of CCF&MB.

I believe that the people needs to know that at CCF&MB what services we provide and therefore

communication needs to made appropriately. The clients who are currently be handled by the company are

important sources as they spread the news more effective regarding the nature of the business and then

they also refer to family members. The moves which CCF&MB needs to engage in is to send text messages,

emails to past clients, new clients, potential clients for communicating the services which is provided by

CCF&MB. An opinion of a person is the best form of referral and the same can only be done by a present

client.

The identification of the referral needs of referral partners and updating them is an important aspect of the

business. For establishing this, regular contact with the partners need to be established. This will ensure

our referral partners are aware about what is happening in lending market.

Assessor feedback for Task 1: Resubmission required?

A simple structured, relatively well thought out Plan and you have

demonstrated that you are competent regarding this Task. You just spent to

much time on the legislative and regulatory requirements.

No

Page 11 of 35

Task 2 — Growing the business

Having considered how you would go about building and nurturing relationships, George and Mildred now

require you to turn your attention to marketing and promoting CCF & MB’s business. This requires you to

develop a marketing plan for the business.

In developing your marketing plan you should consider the following:

1. Your plan should be developed in line with CCF & MB’s vision statement.

2. The identification of target markets, using a combination of research and your own personal experience.

3. The identification of your major competitors (at least two) with a competitor analysis developed for

each competitor.

4. The identification of CCF & MB’s market position, based on your research findings and analysis.

5. How you would promote CCF & MB’s brand and the tools you would use to achieve this.

6. The provision of options for increasing yield per existing client.

7. How you would implement your plan and monitor it to ensure objectives/goals/performance indicators

are being met.

8. How you would adjust your plan if required.

(1,000 words)

You may use any format for your plan but you are not permitted to simply answer the points above. If you

are unsure as to how to write a plan, you can refer to the Business Growth and Marketing topic and use the

suggested SMEAC format outlined in Part 6, Section 13. Remember also the SMART principles.

When completing this task, assumptions are permitted although they must not be in conflict with the

information provided in the background information.

Student response to Task 2

The business of CCF&MB had started around 13 years ago and has grown to build of a loan book of

appropriately $ 1.2 billion with new loans averaging $ 120 million yearly. The marketing plan which I would

be developing are structured and shown below in details:

Vision Statement: The vision of the company is to be the preferred choice in mortgage and finance

brokering in the greater metropolitan areas and attract more and more clients in the area.

Mission Statement: The mission for the company is to operate efficiently and professional in accordance

with legislations, license for operating and professional standards.

The goals which are considered by the organization are listed below:

To offer the best services and affordable mortgage and finance broker services in the area.

To attract more clients to the business and attract over 500 clients through the referral programs.

The business aims to attain a client base of 2000 clients annually.

The business wants to partner with 15 more lenders in the next four-year period to create a better

borrowing capacity for the company.

The mortgage and brokering marketing has grown significantly and this is the main reason due to which

businesses and individuals can access loans more freely for the purpose of acquiring properties and

premises with the help of mortgages. There are many deals which are available in the market and some of

the same are not appropriate. The business of CFF & MB has been growing significantly over the years and

is determined to acquire shares in the mortgage industry. Mortgages are currently available for residential

loans, commercial property loans, and investment loans.

The client base which is constituted in CFF & MB are under three classifications which are the clients wants

to purchase their own houses, clients who wants to purchase rental property and clients who are looking

for expansion of their business. In most cases, the clients are after mortgages for purchasing houses which

Page 12 of 35

Having considered how you would go about building and nurturing relationships, George and Mildred now

require you to turn your attention to marketing and promoting CCF & MB’s business. This requires you to

develop a marketing plan for the business.

In developing your marketing plan you should consider the following:

1. Your plan should be developed in line with CCF & MB’s vision statement.

2. The identification of target markets, using a combination of research and your own personal experience.

3. The identification of your major competitors (at least two) with a competitor analysis developed for

each competitor.

4. The identification of CCF & MB’s market position, based on your research findings and analysis.

5. How you would promote CCF & MB’s brand and the tools you would use to achieve this.

6. The provision of options for increasing yield per existing client.

7. How you would implement your plan and monitor it to ensure objectives/goals/performance indicators

are being met.

8. How you would adjust your plan if required.

(1,000 words)

You may use any format for your plan but you are not permitted to simply answer the points above. If you

are unsure as to how to write a plan, you can refer to the Business Growth and Marketing topic and use the

suggested SMEAC format outlined in Part 6, Section 13. Remember also the SMART principles.

When completing this task, assumptions are permitted although they must not be in conflict with the

information provided in the background information.

Student response to Task 2

The business of CCF&MB had started around 13 years ago and has grown to build of a loan book of

appropriately $ 1.2 billion with new loans averaging $ 120 million yearly. The marketing plan which I would

be developing are structured and shown below in details:

Vision Statement: The vision of the company is to be the preferred choice in mortgage and finance

brokering in the greater metropolitan areas and attract more and more clients in the area.

Mission Statement: The mission for the company is to operate efficiently and professional in accordance

with legislations, license for operating and professional standards.

The goals which are considered by the organization are listed below:

To offer the best services and affordable mortgage and finance broker services in the area.

To attract more clients to the business and attract over 500 clients through the referral programs.

The business aims to attain a client base of 2000 clients annually.

The business wants to partner with 15 more lenders in the next four-year period to create a better

borrowing capacity for the company.

The mortgage and brokering marketing has grown significantly and this is the main reason due to which

businesses and individuals can access loans more freely for the purpose of acquiring properties and

premises with the help of mortgages. There are many deals which are available in the market and some of

the same are not appropriate. The business of CFF & MB has been growing significantly over the years and

is determined to acquire shares in the mortgage industry. Mortgages are currently available for residential

loans, commercial property loans, and investment loans.

The client base which is constituted in CFF & MB are under three classifications which are the clients wants

to purchase their own houses, clients who wants to purchase rental property and clients who are looking

for expansion of their business. In most cases, the clients are after mortgages for purchasing houses which

Page 12 of 35

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 35

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.