Comprehensive Analysis of Financial Lease Disclosure under AASB 117

VerifiedAdded on 2023/06/05

|8

|1602

|354

Report

AI Summary

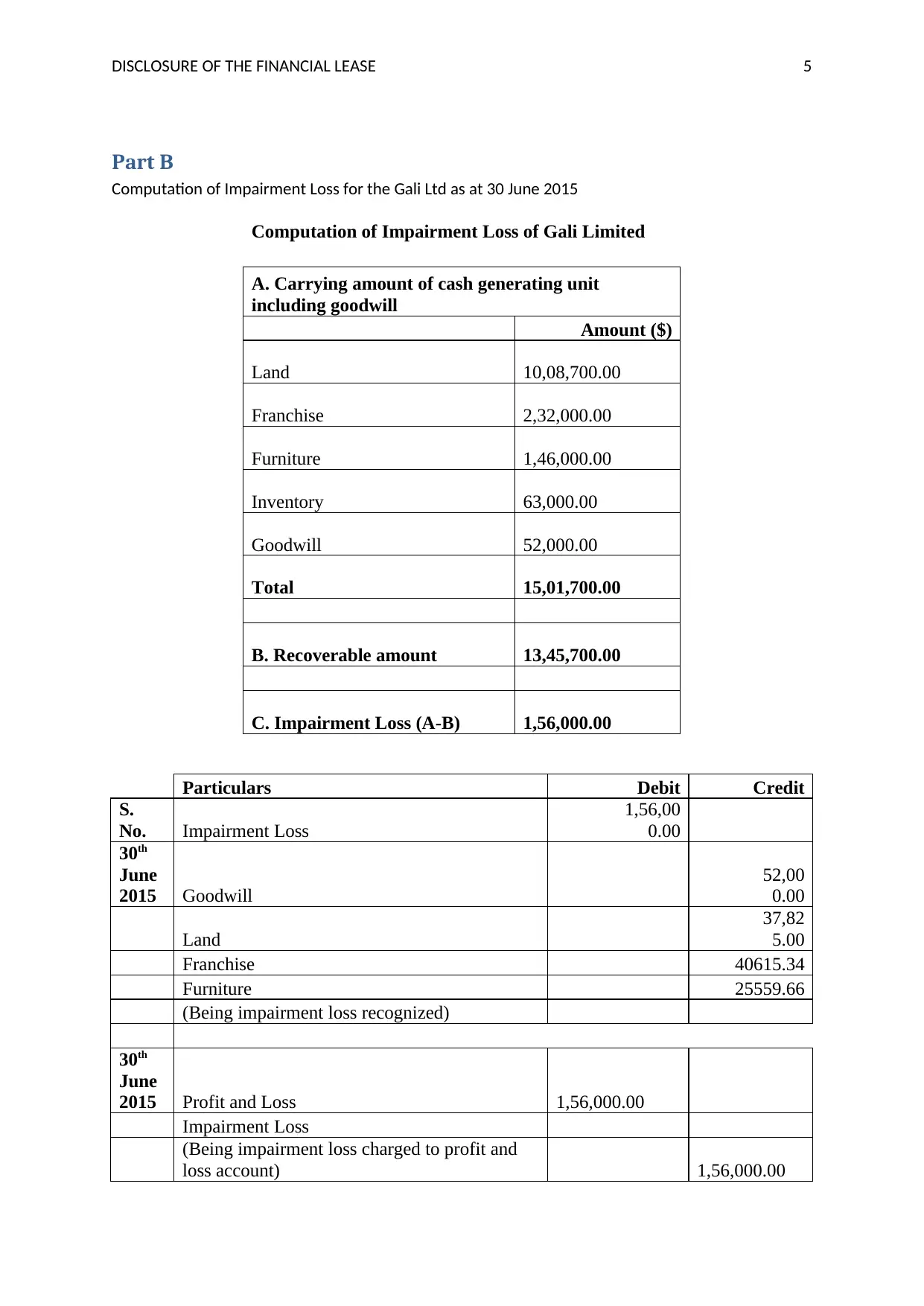

This report provides a comprehensive analysis of financial lease disclosure, focusing on the requirements outlined in AASB 117. It examines the roles and responsibilities of both lessors and lessees in financial lease arrangements, detailing the specific disclosure obligations for each party. The report delves into the accounting treatment of financial leases, including the calculation and presentation of carrying amounts, reconciliation of lease payments, and the disclosure of contingent rents and sub-lease arrangements. Furthermore, it addresses the requirements for lessors, such as the classification of investment amounts and the disclosure of unearned finance income and unguaranteed residual values. The report also includes a practical application, demonstrating the computation of an impairment loss for Gali Ltd, providing a real-world example of the concepts discussed. References to relevant literature and accounting standards are provided to support the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.