Finance and Resourcing Dissertation Report: City Family Fitness Centre

VerifiedAdded on 2020/02/03

|13

|2039

|73

Report

AI Summary

This dissertation report focuses on the financial aspects of establishing a family fitness center. It includes projected sales and profit forecasts based on membership fees, expected cash flow statements, and a two-year profit and loss statement and balance sheet. The report identifies implementation strategies, assumptions behind the financial projections, and potential risks such as recession, inflation, and competition, along with strategies to mitigate these risks. The financial analysis is supported by various assumptions including wage rates, taxation rates, and customer behavior. The report includes references to relevant literature and appendices with detailed financial data, providing a comprehensive overview of the financial planning and risk management for the fitness center, with a focus on resourcing and sustainability. The report also analyzes the importance of adapting to customer needs and adopting new technologies to stay competitive.

DISSERTATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

FINANCE AND RESOURCING....................................................................................................3

35 Expected sales and profit.......................................................................................................3

36 Expected cash flow statements...............................................................................................3

37 Projected Profit and Loss and balance sheet for two years....................................................3

38 Identification of implementation strategies and assumptions for projected statements.........4

39 Identification of risks and strategy to manage these..............................................................4

REFERENCES................................................................................................................................6

APPENDICES.................................................................................................................................8

FINANCE AND RESOURCING....................................................................................................3

35 Expected sales and profit.......................................................................................................3

36 Expected cash flow statements...............................................................................................3

37 Projected Profit and Loss and balance sheet for two years....................................................3

38 Identification of implementation strategies and assumptions for projected statements.........4

39 Identification of risks and strategy to manage these..............................................................4

REFERENCES................................................................................................................................6

APPENDICES.................................................................................................................................8

FINANCE AND RESOURCING

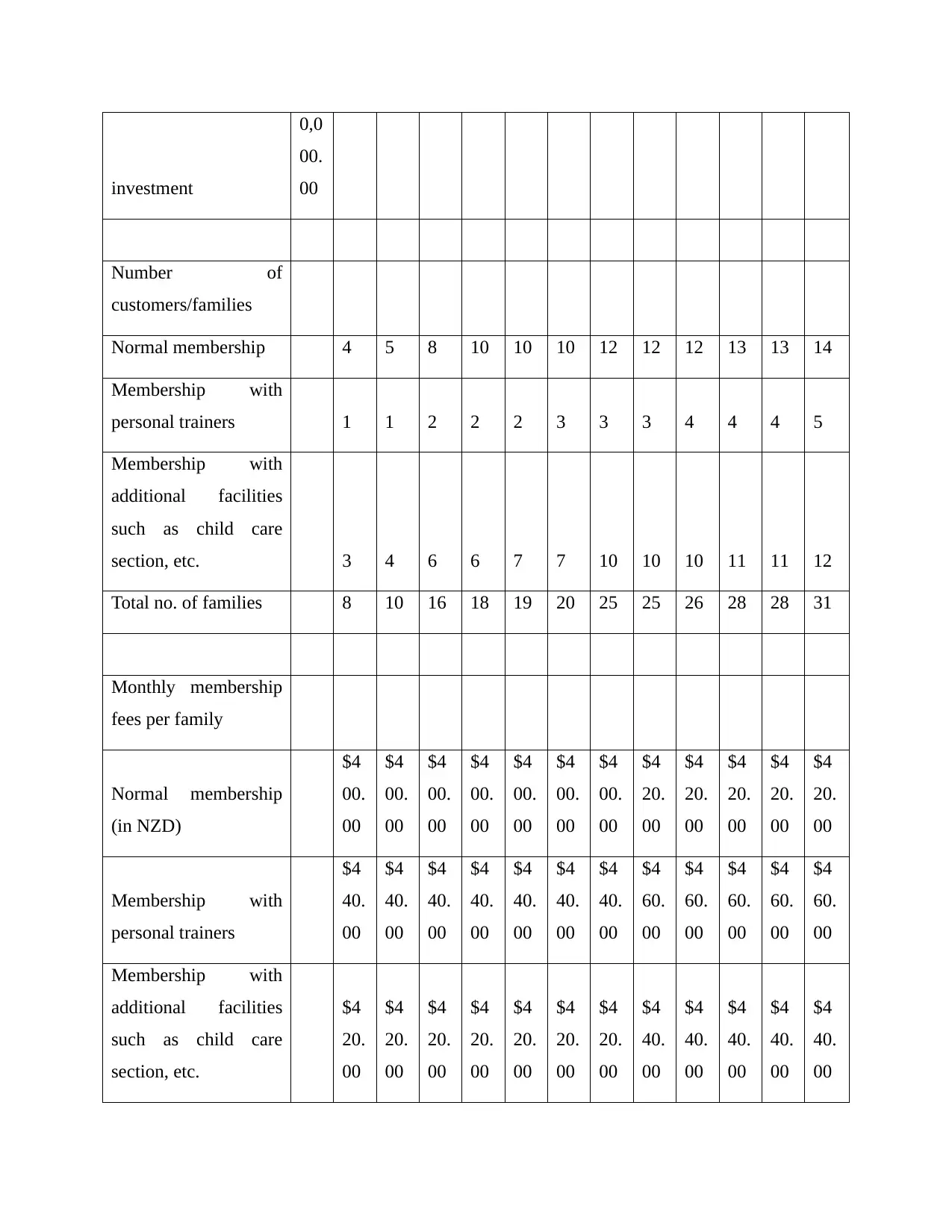

35 Expected sales and profit

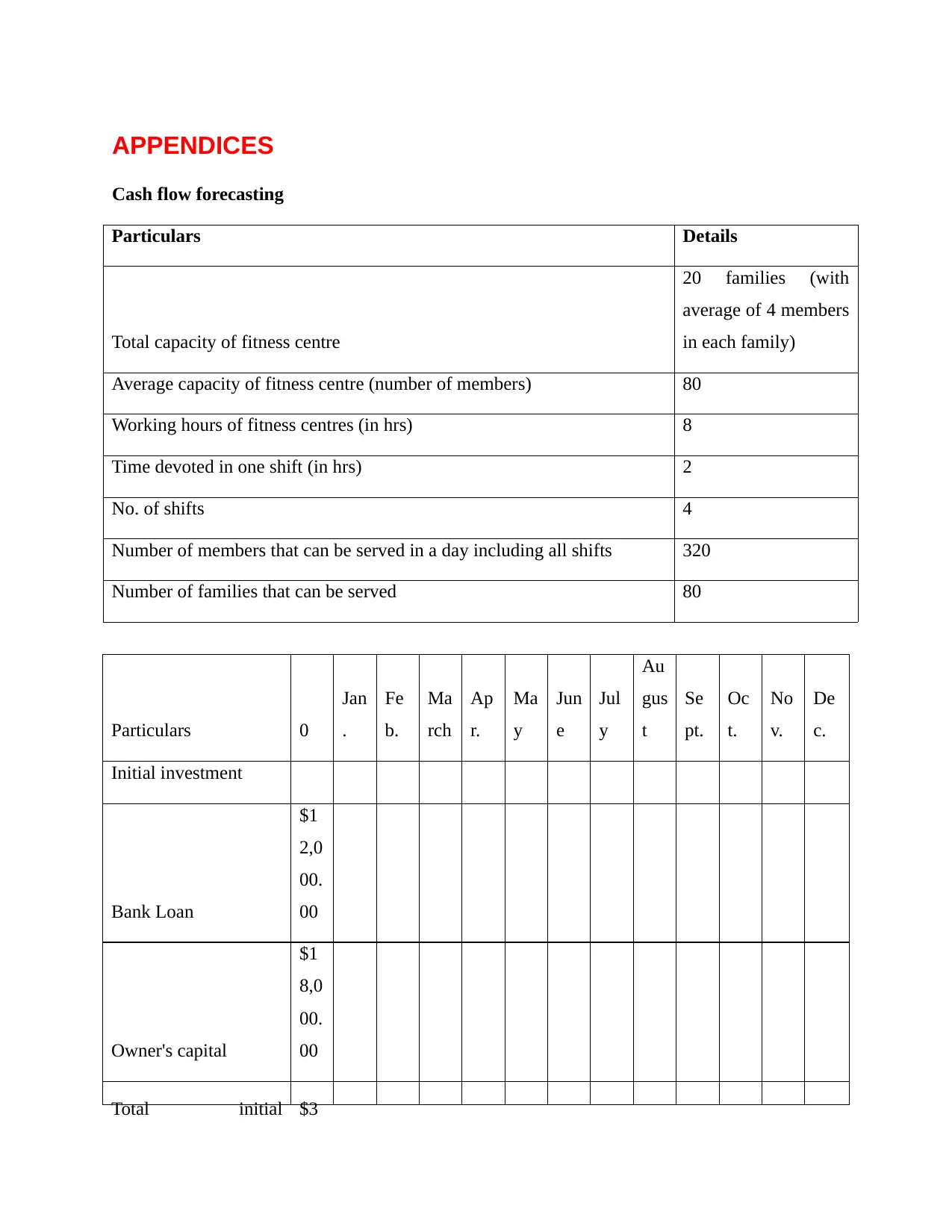

Revenue of this family fitness centre are fortecasted on teh basis of member ship fee

charges from the customers on montly basis (Bose, 2006). This centre runs for 8 hours and 54

days in a week in order to facilitate all theior custoimers with their oprecious services and

facilties. The average capacity of this place is taken as for 20 families of standard four member

per family. The sales are foreacted for this centre in a category of threesiuch as normal

membership which charge around $428, Membership witbpersonal trainers charges $471 and last

option is membership with additional facilties charges around$518 per families. The number of

familities in year one taken aas small ratio of 21 familoies whicxh graduuallt increases as per the

budget and capacity generated by the enterprise (Davies and Drexler, 2010). The additional

facilities provided by this enterprise is chid care services which allow a mother to take care about

their health as the child are takencare at teh bsame place.

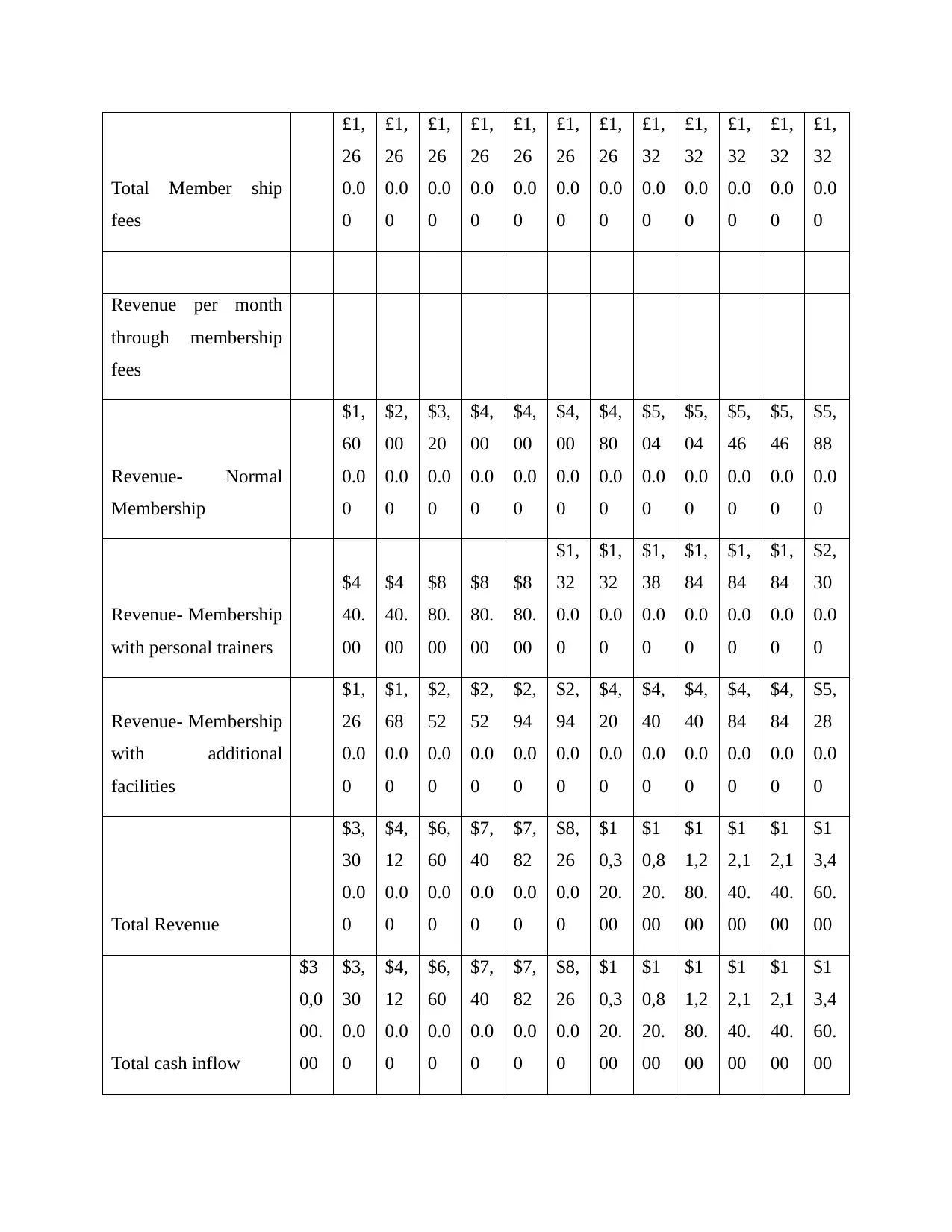

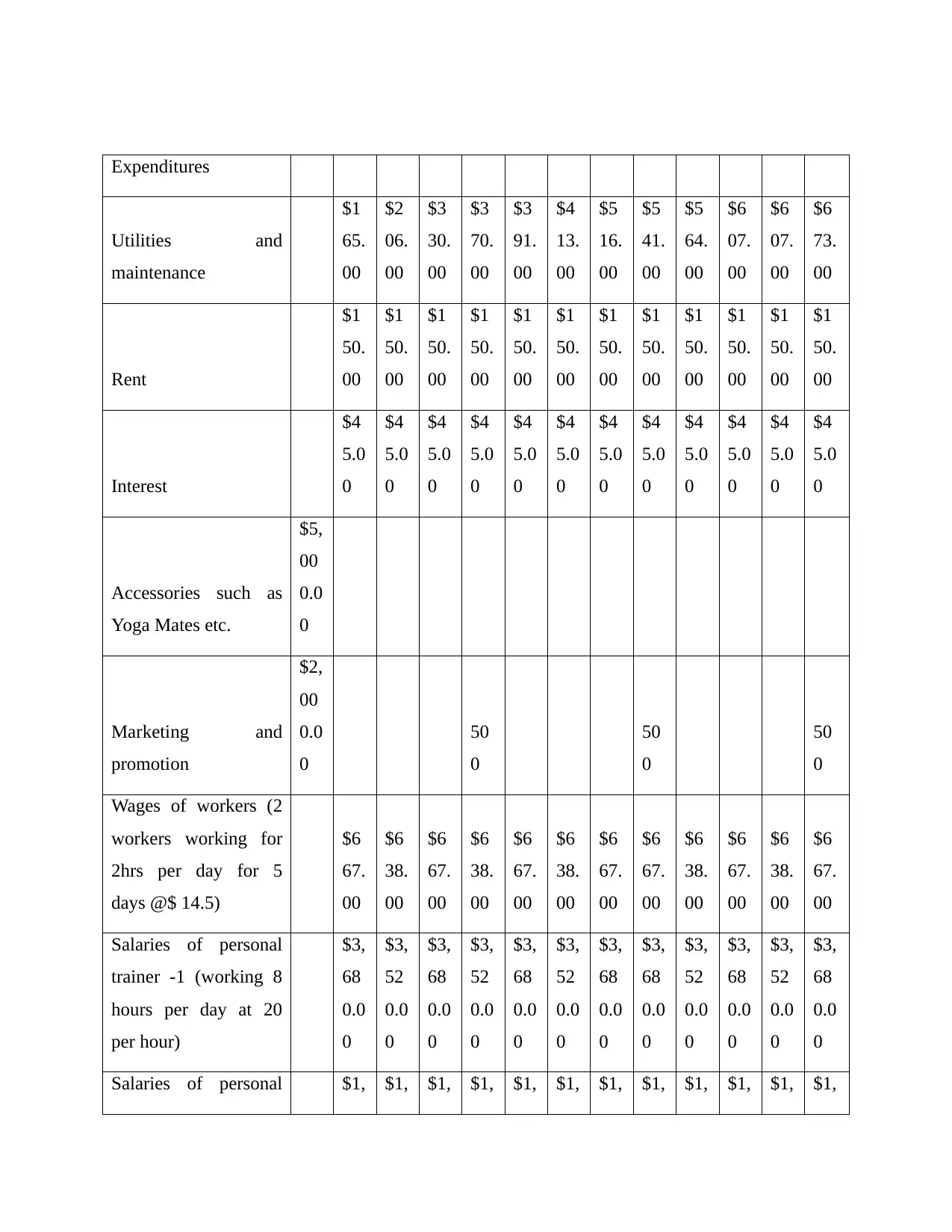

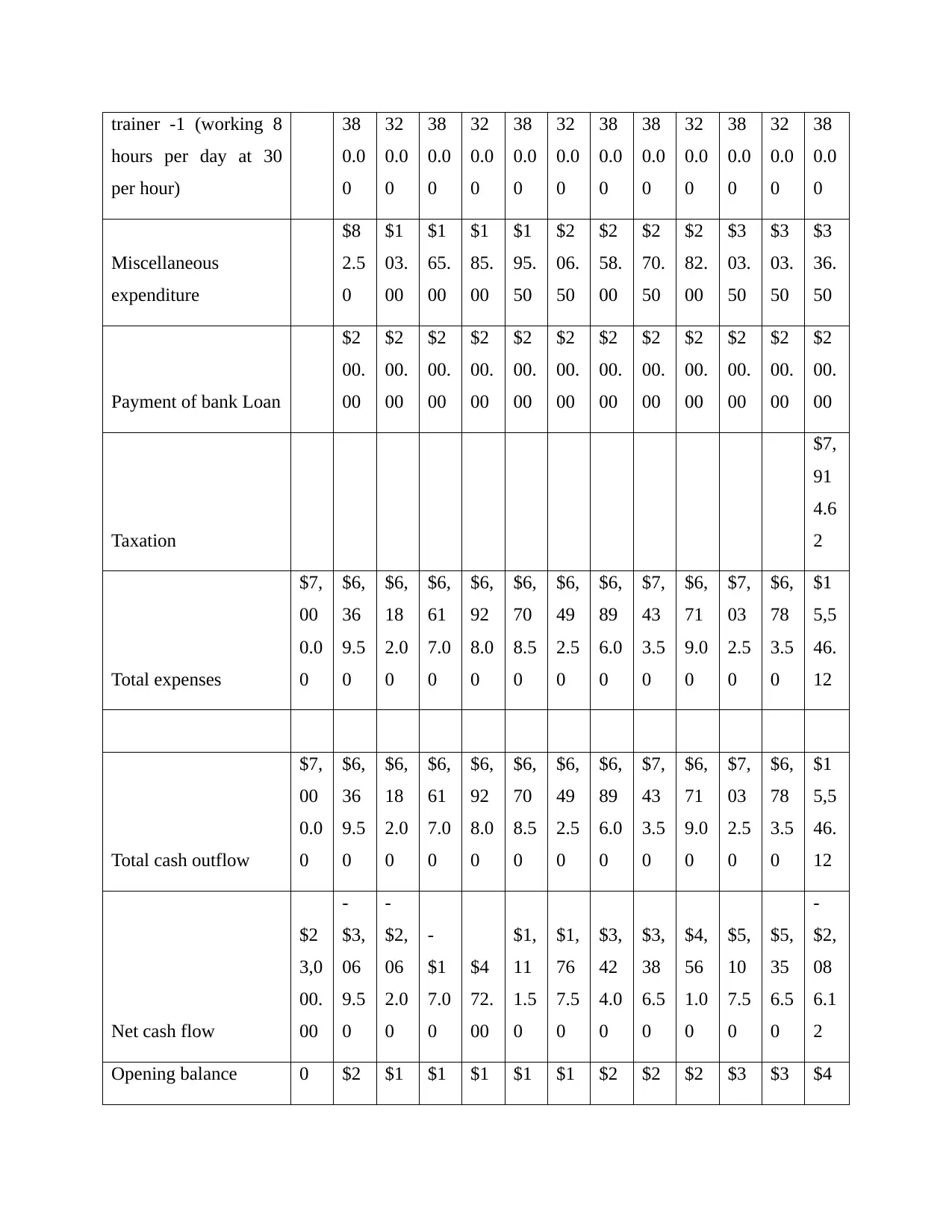

36 Expected cash flow statements

The cash flow statements are given below in appendices are prteaprerd by taking into

considerations all the reveneues and incomes generated by this enterprise and all expenses are

also form part of this cash flow forecast (Dayananda, 2002). The rates of utilities and

maintenance are taken asd per the standard rates of utilities bills in Newzealand. The rent opf the

place in which this centre is located are also taken into considerations as per the monthly. The

wages are taken as per the national standard wage rates of Newzealand that is $14.5 of hour rate.

It is charded to all the workrs for 2hrs in a week of 5 days (DaDalt and Coughlin, 2016). The

salarries of the personal trainers are taken as 20 per hour as per 8 hours in a day and for another

trainers the rate is 30 hour oper day as thehir capabilities experienxce are more than this trainer.

The expenses also included payment of bnbank loan taken to initiate the business proceedings.

37 Projected Profit and Loss and balance sheet for two years

The cash flow forecasting is used as a basis for preparing profit and loss statement in

order to ascertain the profitability of this small scale enterprise. It will consider the salers figure

generated from cash flow forecasting abnd all optyher operating expenses in form of salariers,

wages, marketing promotion expenses (Fletcher, 2016). It also considered taxation rate of the

35 Expected sales and profit

Revenue of this family fitness centre are fortecasted on teh basis of member ship fee

charges from the customers on montly basis (Bose, 2006). This centre runs for 8 hours and 54

days in a week in order to facilitate all theior custoimers with their oprecious services and

facilties. The average capacity of this place is taken as for 20 families of standard four member

per family. The sales are foreacted for this centre in a category of threesiuch as normal

membership which charge around $428, Membership witbpersonal trainers charges $471 and last

option is membership with additional facilties charges around$518 per families. The number of

familities in year one taken aas small ratio of 21 familoies whicxh graduuallt increases as per the

budget and capacity generated by the enterprise (Davies and Drexler, 2010). The additional

facilities provided by this enterprise is chid care services which allow a mother to take care about

their health as the child are takencare at teh bsame place.

36 Expected cash flow statements

The cash flow statements are given below in appendices are prteaprerd by taking into

considerations all the reveneues and incomes generated by this enterprise and all expenses are

also form part of this cash flow forecast (Dayananda, 2002). The rates of utilities and

maintenance are taken asd per the standard rates of utilities bills in Newzealand. The rent opf the

place in which this centre is located are also taken into considerations as per the monthly. The

wages are taken as per the national standard wage rates of Newzealand that is $14.5 of hour rate.

It is charded to all the workrs for 2hrs in a week of 5 days (DaDalt and Coughlin, 2016). The

salarries of the personal trainers are taken as 20 per hour as per 8 hours in a day and for another

trainers the rate is 30 hour oper day as thehir capabilities experienxce are more than this trainer.

The expenses also included payment of bnbank loan taken to initiate the business proceedings.

37 Projected Profit and Loss and balance sheet for two years

The cash flow forecasting is used as a basis for preparing profit and loss statement in

order to ascertain the profitability of this small scale enterprise. It will consider the salers figure

generated from cash flow forecasting abnd all optyher operating expenses in form of salariers,

wages, marketing promotion expenses (Fletcher, 2016). It also considered taxation rate of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

country as it has observed that the profiut in first yesr is 20351 which increases in 2 year with

huge amount of percentage change of more than 50% and again gets increases in third year.

38 Identification of implementation strategies and assumptions for projected statements

There are several assumptions taken by an enterprise while pojecting their financial

outocomes generated by this firm in near future.The sales and revenues are taken on the

membership decided by the owbner as per their average families taken up by an enitity in their

fist year. The expenses are are also backed up by different assumptions on teh basis of wage rate

that is styandard wage rate of $14.5 per hour, hourly rate oif salaries for oersonal trainers are 20

and 30 (Hira, 2016). The taxation rate is taken as 28% as per the specific nature of teh business

and income produces by the business.

39 Identification of risks and strategy to manage these

Business plan is based on some specific assumptions about the future interest rates,

exchange rates, tax rates, market growth and behaviour of customers and competitors, etc. So,

small changes in these assumptions may affect the whole business performance in negative

manner (Hosain, 2016). So, business owner needs to use appropriate risk assessment and

management strategy for identifying and managing different types of risk in starting a new

fitness centre. The major risks that may affect the overall business in negative manner will be

recession, inflation, government rules and regulations, tax rates fluctuations, changes in customer

needs, technical risk, legal risks, financial risks, quality issues and competition risks, etc. All

these risks will have negative impact on overall sales and profitability of the fitness centre.

Recession and inflation have direct impact on purchasing price of customers or clients of

fitness centre so, business owner needs to forecast economic position of the country in advance

which will have help in making the appropriate strategy for managing such type of risk (Kostova

and Nell, 2016). Along with this, changes in government rules, regulation, tax rates and

legislation business owner of City Family Fitness Centre should develop organizational policies

with considerations of all rules and regulations because these will help in developing appropriate

strategies for managing business performance. Including this, due to the changes in life style

fitness center can face the problem of changes in customer’s needs also (Hiro and Sofat, 2010).

So, business owner needs to provide customize services for satisfying needs and

requirements of customers, it will help in managing such type of risks in effective manner. Along

huge amount of percentage change of more than 50% and again gets increases in third year.

38 Identification of implementation strategies and assumptions for projected statements

There are several assumptions taken by an enterprise while pojecting their financial

outocomes generated by this firm in near future.The sales and revenues are taken on the

membership decided by the owbner as per their average families taken up by an enitity in their

fist year. The expenses are are also backed up by different assumptions on teh basis of wage rate

that is styandard wage rate of $14.5 per hour, hourly rate oif salaries for oersonal trainers are 20

and 30 (Hira, 2016). The taxation rate is taken as 28% as per the specific nature of teh business

and income produces by the business.

39 Identification of risks and strategy to manage these

Business plan is based on some specific assumptions about the future interest rates,

exchange rates, tax rates, market growth and behaviour of customers and competitors, etc. So,

small changes in these assumptions may affect the whole business performance in negative

manner (Hosain, 2016). So, business owner needs to use appropriate risk assessment and

management strategy for identifying and managing different types of risk in starting a new

fitness centre. The major risks that may affect the overall business in negative manner will be

recession, inflation, government rules and regulations, tax rates fluctuations, changes in customer

needs, technical risk, legal risks, financial risks, quality issues and competition risks, etc. All

these risks will have negative impact on overall sales and profitability of the fitness centre.

Recession and inflation have direct impact on purchasing price of customers or clients of

fitness centre so, business owner needs to forecast economic position of the country in advance

which will have help in making the appropriate strategy for managing such type of risk (Kostova

and Nell, 2016). Along with this, changes in government rules, regulation, tax rates and

legislation business owner of City Family Fitness Centre should develop organizational policies

with considerations of all rules and regulations because these will help in developing appropriate

strategies for managing business performance. Including this, due to the changes in life style

fitness center can face the problem of changes in customer’s needs also (Hiro and Sofat, 2010).

So, business owner needs to provide customize services for satisfying needs and

requirements of customers, it will help in managing such type of risks in effective manner. Along

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with this, for managing technical risks City Family Fitness Centre should adopt the latest

technologies for exercise which will help in improving the quality of services as well as this

strategy will also attract customers. For managing financial business owner will use appropriate

financial tools such as budgeting, investment appraisal method, and activity based costing and

financial statements (Jorgensen and Rotter, 2016). These tools and techniques will help in

managing financial performance of the company in effective manner. Further, for reducing

competition and attaining competitive advantages City Family Fitness Centre will differentiate

its services from existing competitors. For example, new business will shed light on Yoga with

exercise which will help in making differentiation in services with existing competitors.

Therefore, these will play important role in managing competition risk in effective manner.

Overall, all the above discussion strategy will play significant role in managing risks and

improving performance of City Family Fitness Centre in effective manner (Hill and Clarke,

2013).

technologies for exercise which will help in improving the quality of services as well as this

strategy will also attract customers. For managing financial business owner will use appropriate

financial tools such as budgeting, investment appraisal method, and activity based costing and

financial statements (Jorgensen and Rotter, 2016). These tools and techniques will help in

managing financial performance of the company in effective manner. Further, for reducing

competition and attaining competitive advantages City Family Fitness Centre will differentiate

its services from existing competitors. For example, new business will shed light on Yoga with

exercise which will help in making differentiation in services with existing competitors.

Therefore, these will play important role in managing competition risk in effective manner.

Overall, all the above discussion strategy will play significant role in managing risks and

improving performance of City Family Fitness Centre in effective manner (Hill and Clarke,

2013).

REFERENCES

Books and journals

Bose, C., 2006. Fundamentals of Financial Management. PHI learning.

Coronel, C. and Morris, 2016. Database Systems: Design, Implementation, & Management.

Cengage Learning.

Correia, C. and Flynn, D., 2012. Financial Management. Business Enterprises.

DaDalt, O. and Coughlin, J. F., 2016. Managing Financial Well-Being in the Shadow of

Alzheimer’s Disease. Public Policy & Aging Report. 26(1). pp.36-38.

Davies, H. and Drexler, M., 2010. Financial Development, Capital Flows, and Capital Controls.

InThe Financial Development Report 2010. Geneva and New York: World Economic

Forum. Pp. 31–47.

Dayananda, D.,2002. Capital Budgeting: Financial Appraisal of Investment Projects. Cambridge

University Press.

Ehrhardt, M. and Brigham, E., 2016. Corporate finance: A focused approach. Cengage Learning.

Elearn, 2013. Financial Management Revised Edition. Routledge publication.

Evans, M. and Porter, R., 2010. Real estate financial reporting and accounting. Journal of

Property Investment & Finance. 28(5). Pp. 105-111.

Fletcher, F., 2016. Solutions: Business Problem Solving. Routledge.

Hill, V. R., and Clarke, J. D., 2013. Cost-Benefit Analysis of the African Risk Capacity Facility.

Intl Food Policy Res Inst.

Hira, T. K., 2016. Financial Sustainability and Personal Finance Education. Springer

International Publishing.

Hiro, P. and Sofat, R., 2010. Basic Accounting. Delhi: PHI Learning Pvt Ltd.

Hosain, M. S., 2016. Impact of Best HRM Practices on Retaining the Best Employees: A Study

on Selected Bangladeshi Firms. Asian Journal of Social Sciences and Management

Studies. 3(2). pp.108-114.

Books and journals

Bose, C., 2006. Fundamentals of Financial Management. PHI learning.

Coronel, C. and Morris, 2016. Database Systems: Design, Implementation, & Management.

Cengage Learning.

Correia, C. and Flynn, D., 2012. Financial Management. Business Enterprises.

DaDalt, O. and Coughlin, J. F., 2016. Managing Financial Well-Being in the Shadow of

Alzheimer’s Disease. Public Policy & Aging Report. 26(1). pp.36-38.

Davies, H. and Drexler, M., 2010. Financial Development, Capital Flows, and Capital Controls.

InThe Financial Development Report 2010. Geneva and New York: World Economic

Forum. Pp. 31–47.

Dayananda, D.,2002. Capital Budgeting: Financial Appraisal of Investment Projects. Cambridge

University Press.

Ehrhardt, M. and Brigham, E., 2016. Corporate finance: A focused approach. Cengage Learning.

Elearn, 2013. Financial Management Revised Edition. Routledge publication.

Evans, M. and Porter, R., 2010. Real estate financial reporting and accounting. Journal of

Property Investment & Finance. 28(5). Pp. 105-111.

Fletcher, F., 2016. Solutions: Business Problem Solving. Routledge.

Hill, V. R., and Clarke, J. D., 2013. Cost-Benefit Analysis of the African Risk Capacity Facility.

Intl Food Policy Res Inst.

Hira, T. K., 2016. Financial Sustainability and Personal Finance Education. Springer

International Publishing.

Hiro, P. and Sofat, R., 2010. Basic Accounting. Delhi: PHI Learning Pvt Ltd.

Hosain, M. S., 2016. Impact of Best HRM Practices on Retaining the Best Employees: A Study

on Selected Bangladeshi Firms. Asian Journal of Social Sciences and Management

Studies. 3(2). pp.108-114.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Jorgensen, P. W. and Rotter, 2016. Ecosystem services assessments in local municipal decision

making in South Africa: justification for the use of a business-based approach. Journal of

Environmental Planning and Management. 59(2). pp.263-279.

Kostova, T., Nell, 2016. Understanding Agency Problems in Headquarters-Subsidiary

Relationships in Multinational Corporations A Contextualized Model. Journal of

Management. 26(1). pp.36-38.

Online

Advantages and Limitations of Ratio Analysis, 2014. [Online]. Available through: <

http://accountingexplained.com/financial/ratios/advantages-limitations>. [Accessed on 26

October 2016].

A profile of the New Zealand Fitness Industry, 2015 [Online]. Available through: <

http://www.nzihf.co.nz/media-resources-1/articles/a-profile-of-the-new-zealand-fitness-

industry>. [Accessed on 26 Oct 2016].

making in South Africa: justification for the use of a business-based approach. Journal of

Environmental Planning and Management. 59(2). pp.263-279.

Kostova, T., Nell, 2016. Understanding Agency Problems in Headquarters-Subsidiary

Relationships in Multinational Corporations A Contextualized Model. Journal of

Management. 26(1). pp.36-38.

Online

Advantages and Limitations of Ratio Analysis, 2014. [Online]. Available through: <

http://accountingexplained.com/financial/ratios/advantages-limitations>. [Accessed on 26

October 2016].

A profile of the New Zealand Fitness Industry, 2015 [Online]. Available through: <

http://www.nzihf.co.nz/media-resources-1/articles/a-profile-of-the-new-zealand-fitness-

industry>. [Accessed on 26 Oct 2016].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDICES

Cash flow forecasting

Particulars Details

Total capacity of fitness centre

20 families (with

average of 4 members

in each family)

Average capacity of fitness centre (number of members) 80

Working hours of fitness centres (in hrs) 8

Time devoted in one shift (in hrs) 2

No. of shifts 4

Number of members that can be served in a day including all shifts 320

Number of families that can be served 80

Particulars 0

Jan

.

Fe

b.

Ma

rch

Ap

r.

Ma

y

Jun

e

Jul

y

Au

gus

t

Se

pt.

Oc

t.

No

v.

De

c.

Initial investment

Bank Loan

$1

2,0

00.

00

Owner's capital

$1

8,0

00.

00

Total initial $3

Cash flow forecasting

Particulars Details

Total capacity of fitness centre

20 families (with

average of 4 members

in each family)

Average capacity of fitness centre (number of members) 80

Working hours of fitness centres (in hrs) 8

Time devoted in one shift (in hrs) 2

No. of shifts 4

Number of members that can be served in a day including all shifts 320

Number of families that can be served 80

Particulars 0

Jan

.

Fe

b.

Ma

rch

Ap

r.

Ma

y

Jun

e

Jul

y

Au

gus

t

Se

pt.

Oc

t.

No

v.

De

c.

Initial investment

Bank Loan

$1

2,0

00.

00

Owner's capital

$1

8,0

00.

00

Total initial $3

investment

0,0

00.

00

Number of

customers/families

Normal membership 4 5 8 10 10 10 12 12 12 13 13 14

Membership with

personal trainers 1 1 2 2 2 3 3 3 4 4 4 5

Membership with

additional facilities

such as child care

section, etc. 3 4 6 6 7 7 10 10 10 11 11 12

Total no. of families 8 10 16 18 19 20 25 25 26 28 28 31

Monthly membership

fees per family

Normal membership

(in NZD)

$4

00.

00

$4

00.

00

$4

00.

00

$4

00.

00

$4

00.

00

$4

00.

00

$4

00.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

Membership with

personal trainers

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

60.

00

$4

60.

00

$4

60.

00

$4

60.

00

$4

60.

00

Membership with

additional facilities

such as child care

section, etc.

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

0,0

00.

00

Number of

customers/families

Normal membership 4 5 8 10 10 10 12 12 12 13 13 14

Membership with

personal trainers 1 1 2 2 2 3 3 3 4 4 4 5

Membership with

additional facilities

such as child care

section, etc. 3 4 6 6 7 7 10 10 10 11 11 12

Total no. of families 8 10 16 18 19 20 25 25 26 28 28 31

Monthly membership

fees per family

Normal membership

(in NZD)

$4

00.

00

$4

00.

00

$4

00.

00

$4

00.

00

$4

00.

00

$4

00.

00

$4

00.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

Membership with

personal trainers

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

60.

00

$4

60.

00

$4

60.

00

$4

60.

00

$4

60.

00

Membership with

additional facilities

such as child care

section, etc.

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

20.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

$4

40.

00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Member ship

fees

£1,

26

0.0

0

£1,

26

0.0

0

£1,

26

0.0

0

£1,

26

0.0

0

£1,

26

0.0

0

£1,

26

0.0

0

£1,

26

0.0

0

£1,

32

0.0

0

£1,

32

0.0

0

£1,

32

0.0

0

£1,

32

0.0

0

£1,

32

0.0

0

Revenue per month

through membership

fees

Revenue- Normal

Membership

$1,

60

0.0

0

$2,

00

0.0

0

$3,

20

0.0

0

$4,

00

0.0

0

$4,

00

0.0

0

$4,

00

0.0

0

$4,

80

0.0

0

$5,

04

0.0

0

$5,

04

0.0

0

$5,

46

0.0

0

$5,

46

0.0

0

$5,

88

0.0

0

Revenue- Membership

with personal trainers

$4

40.

00

$4

40.

00

$8

80.

00

$8

80.

00

$8

80.

00

$1,

32

0.0

0

$1,

32

0.0

0

$1,

38

0.0

0

$1,

84

0.0

0

$1,

84

0.0

0

$1,

84

0.0

0

$2,

30

0.0

0

Revenue- Membership

with additional

facilities

$1,

26

0.0

0

$1,

68

0.0

0

$2,

52

0.0

0

$2,

52

0.0

0

$2,

94

0.0

0

$2,

94

0.0

0

$4,

20

0.0

0

$4,

40

0.0

0

$4,

40

0.0

0

$4,

84

0.0

0

$4,

84

0.0

0

$5,

28

0.0

0

Total Revenue

$3,

30

0.0

0

$4,

12

0.0

0

$6,

60

0.0

0

$7,

40

0.0

0

$7,

82

0.0

0

$8,

26

0.0

0

$1

0,3

20.

00

$1

0,8

20.

00

$1

1,2

80.

00

$1

2,1

40.

00

$1

2,1

40.

00

$1

3,4

60.

00

Total cash inflow

$3

0,0

00.

00

$3,

30

0.0

0

$4,

12

0.0

0

$6,

60

0.0

0

$7,

40

0.0

0

$7,

82

0.0

0

$8,

26

0.0

0

$1

0,3

20.

00

$1

0,8

20.

00

$1

1,2

80.

00

$1

2,1

40.

00

$1

2,1

40.

00

$1

3,4

60.

00

fees

£1,

26

0.0

0

£1,

26

0.0

0

£1,

26

0.0

0

£1,

26

0.0

0

£1,

26

0.0

0

£1,

26

0.0

0

£1,

26

0.0

0

£1,

32

0.0

0

£1,

32

0.0

0

£1,

32

0.0

0

£1,

32

0.0

0

£1,

32

0.0

0

Revenue per month

through membership

fees

Revenue- Normal

Membership

$1,

60

0.0

0

$2,

00

0.0

0

$3,

20

0.0

0

$4,

00

0.0

0

$4,

00

0.0

0

$4,

00

0.0

0

$4,

80

0.0

0

$5,

04

0.0

0

$5,

04

0.0

0

$5,

46

0.0

0

$5,

46

0.0

0

$5,

88

0.0

0

Revenue- Membership

with personal trainers

$4

40.

00

$4

40.

00

$8

80.

00

$8

80.

00

$8

80.

00

$1,

32

0.0

0

$1,

32

0.0

0

$1,

38

0.0

0

$1,

84

0.0

0

$1,

84

0.0

0

$1,

84

0.0

0

$2,

30

0.0

0

Revenue- Membership

with additional

facilities

$1,

26

0.0

0

$1,

68

0.0

0

$2,

52

0.0

0

$2,

52

0.0

0

$2,

94

0.0

0

$2,

94

0.0

0

$4,

20

0.0

0

$4,

40

0.0

0

$4,

40

0.0

0

$4,

84

0.0

0

$4,

84

0.0

0

$5,

28

0.0

0

Total Revenue

$3,

30

0.0

0

$4,

12

0.0

0

$6,

60

0.0

0

$7,

40

0.0

0

$7,

82

0.0

0

$8,

26

0.0

0

$1

0,3

20.

00

$1

0,8

20.

00

$1

1,2

80.

00

$1

2,1

40.

00

$1

2,1

40.

00

$1

3,4

60.

00

Total cash inflow

$3

0,0

00.

00

$3,

30

0.0

0

$4,

12

0.0

0

$6,

60

0.0

0

$7,

40

0.0

0

$7,

82

0.0

0

$8,

26

0.0

0

$1

0,3

20.

00

$1

0,8

20.

00

$1

1,2

80.

00

$1

2,1

40.

00

$1

2,1

40.

00

$1

3,4

60.

00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Expenditures

Utilities and

maintenance

$1

65.

00

$2

06.

00

$3

30.

00

$3

70.

00

$3

91.

00

$4

13.

00

$5

16.

00

$5

41.

00

$5

64.

00

$6

07.

00

$6

07.

00

$6

73.

00

Rent

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

Interest

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

Accessories such as

Yoga Mates etc.

$5,

00

0.0

0

Marketing and

promotion

$2,

00

0.0

0

50

0

50

0

50

0

Wages of workers (2

workers working for

2hrs per day for 5

days @$ 14.5)

$6

67.

00

$6

38.

00

$6

67.

00

$6

38.

00

$6

67.

00

$6

38.

00

$6

67.

00

$6

67.

00

$6

38.

00

$6

67.

00

$6

38.

00

$6

67.

00

Salaries of personal

trainer -1 (working 8

hours per day at 20

per hour)

$3,

68

0.0

0

$3,

52

0.0

0

$3,

68

0.0

0

$3,

52

0.0

0

$3,

68

0.0

0

$3,

52

0.0

0

$3,

68

0.0

0

$3,

68

0.0

0

$3,

52

0.0

0

$3,

68

0.0

0

$3,

52

0.0

0

$3,

68

0.0

0

Salaries of personal $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1,

Utilities and

maintenance

$1

65.

00

$2

06.

00

$3

30.

00

$3

70.

00

$3

91.

00

$4

13.

00

$5

16.

00

$5

41.

00

$5

64.

00

$6

07.

00

$6

07.

00

$6

73.

00

Rent

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

$1

50.

00

Interest

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

$4

5.0

0

Accessories such as

Yoga Mates etc.

$5,

00

0.0

0

Marketing and

promotion

$2,

00

0.0

0

50

0

50

0

50

0

Wages of workers (2

workers working for

2hrs per day for 5

days @$ 14.5)

$6

67.

00

$6

38.

00

$6

67.

00

$6

38.

00

$6

67.

00

$6

38.

00

$6

67.

00

$6

67.

00

$6

38.

00

$6

67.

00

$6

38.

00

$6

67.

00

Salaries of personal

trainer -1 (working 8

hours per day at 20

per hour)

$3,

68

0.0

0

$3,

52

0.0

0

$3,

68

0.0

0

$3,

52

0.0

0

$3,

68

0.0

0

$3,

52

0.0

0

$3,

68

0.0

0

$3,

68

0.0

0

$3,

52

0.0

0

$3,

68

0.0

0

$3,

52

0.0

0

$3,

68

0.0

0

Salaries of personal $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1,

trainer -1 (working 8

hours per day at 30

per hour)

38

0.0

0

32

0.0

0

38

0.0

0

32

0.0

0

38

0.0

0

32

0.0

0

38

0.0

0

38

0.0

0

32

0.0

0

38

0.0

0

32

0.0

0

38

0.0

0

Miscellaneous

expenditure

$8

2.5

0

$1

03.

00

$1

65.

00

$1

85.

00

$1

95.

50

$2

06.

50

$2

58.

00

$2

70.

50

$2

82.

00

$3

03.

50

$3

03.

50

$3

36.

50

Payment of bank Loan

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

Taxation

$7,

91

4.6

2

Total expenses

$7,

00

0.0

0

$6,

36

9.5

0

$6,

18

2.0

0

$6,

61

7.0

0

$6,

92

8.0

0

$6,

70

8.5

0

$6,

49

2.5

0

$6,

89

6.0

0

$7,

43

3.5

0

$6,

71

9.0

0

$7,

03

2.5

0

$6,

78

3.5

0

$1

5,5

46.

12

Total cash outflow

$7,

00

0.0

0

$6,

36

9.5

0

$6,

18

2.0

0

$6,

61

7.0

0

$6,

92

8.0

0

$6,

70

8.5

0

$6,

49

2.5

0

$6,

89

6.0

0

$7,

43

3.5

0

$6,

71

9.0

0

$7,

03

2.5

0

$6,

78

3.5

0

$1

5,5

46.

12

Net cash flow

$2

3,0

00.

00

-

$3,

06

9.5

0

-

$2,

06

2.0

0

-

$1

7.0

0

$4

72.

00

$1,

11

1.5

0

$1,

76

7.5

0

$3,

42

4.0

0

$3,

38

6.5

0

$4,

56

1.0

0

$5,

10

7.5

0

$5,

35

6.5

0

-

$2,

08

6.1

2

Opening balance 0 $2 $1 $1 $1 $1 $1 $2 $2 $2 $3 $3 $4

hours per day at 30

per hour)

38

0.0

0

32

0.0

0

38

0.0

0

32

0.0

0

38

0.0

0

32

0.0

0

38

0.0

0

38

0.0

0

32

0.0

0

38

0.0

0

32

0.0

0

38

0.0

0

Miscellaneous

expenditure

$8

2.5

0

$1

03.

00

$1

65.

00

$1

85.

00

$1

95.

50

$2

06.

50

$2

58.

00

$2

70.

50

$2

82.

00

$3

03.

50

$3

03.

50

$3

36.

50

Payment of bank Loan

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

$2

00.

00

Taxation

$7,

91

4.6

2

Total expenses

$7,

00

0.0

0

$6,

36

9.5

0

$6,

18

2.0

0

$6,

61

7.0

0

$6,

92

8.0

0

$6,

70

8.5

0

$6,

49

2.5

0

$6,

89

6.0

0

$7,

43

3.5

0

$6,

71

9.0

0

$7,

03

2.5

0

$6,

78

3.5

0

$1

5,5

46.

12

Total cash outflow

$7,

00

0.0

0

$6,

36

9.5

0

$6,

18

2.0

0

$6,

61

7.0

0

$6,

92

8.0

0

$6,

70

8.5

0

$6,

49

2.5

0

$6,

89

6.0

0

$7,

43

3.5

0

$6,

71

9.0

0

$7,

03

2.5

0

$6,

78

3.5

0

$1

5,5

46.

12

Net cash flow

$2

3,0

00.

00

-

$3,

06

9.5

0

-

$2,

06

2.0

0

-

$1

7.0

0

$4

72.

00

$1,

11

1.5

0

$1,

76

7.5

0

$3,

42

4.0

0

$3,

38

6.5

0

$4,

56

1.0

0

$5,

10

7.5

0

$5,

35

6.5

0

-

$2,

08

6.1

2

Opening balance 0 $2 $1 $1 $1 $1 $1 $2 $2 $2 $3 $3 $4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.