Corporate Finance Case Study: PepsiCo Stock Valuation and DDM Analysis

VerifiedAdded on 2022/09/18

|6

|2146

|28

Case Study

AI Summary

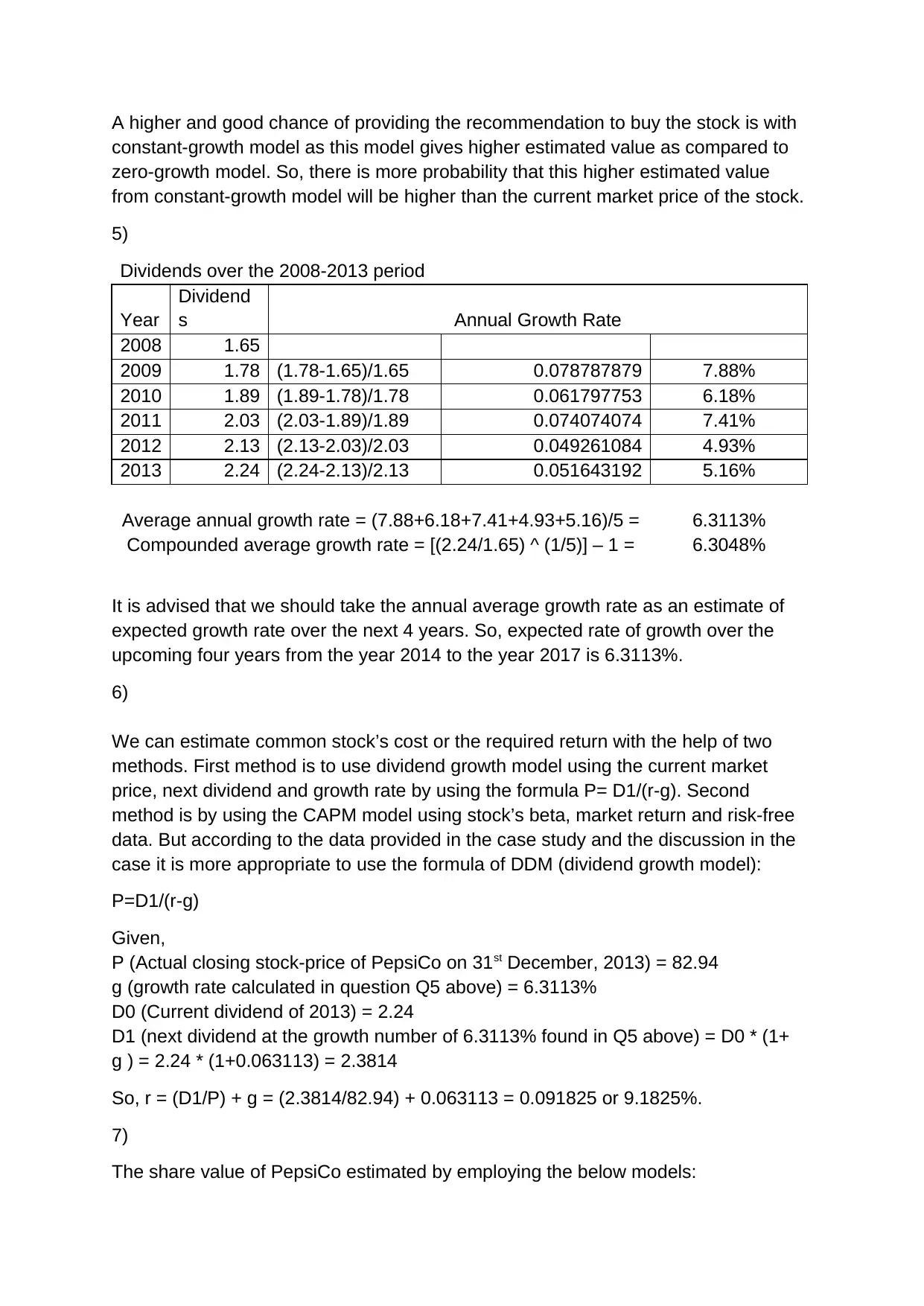

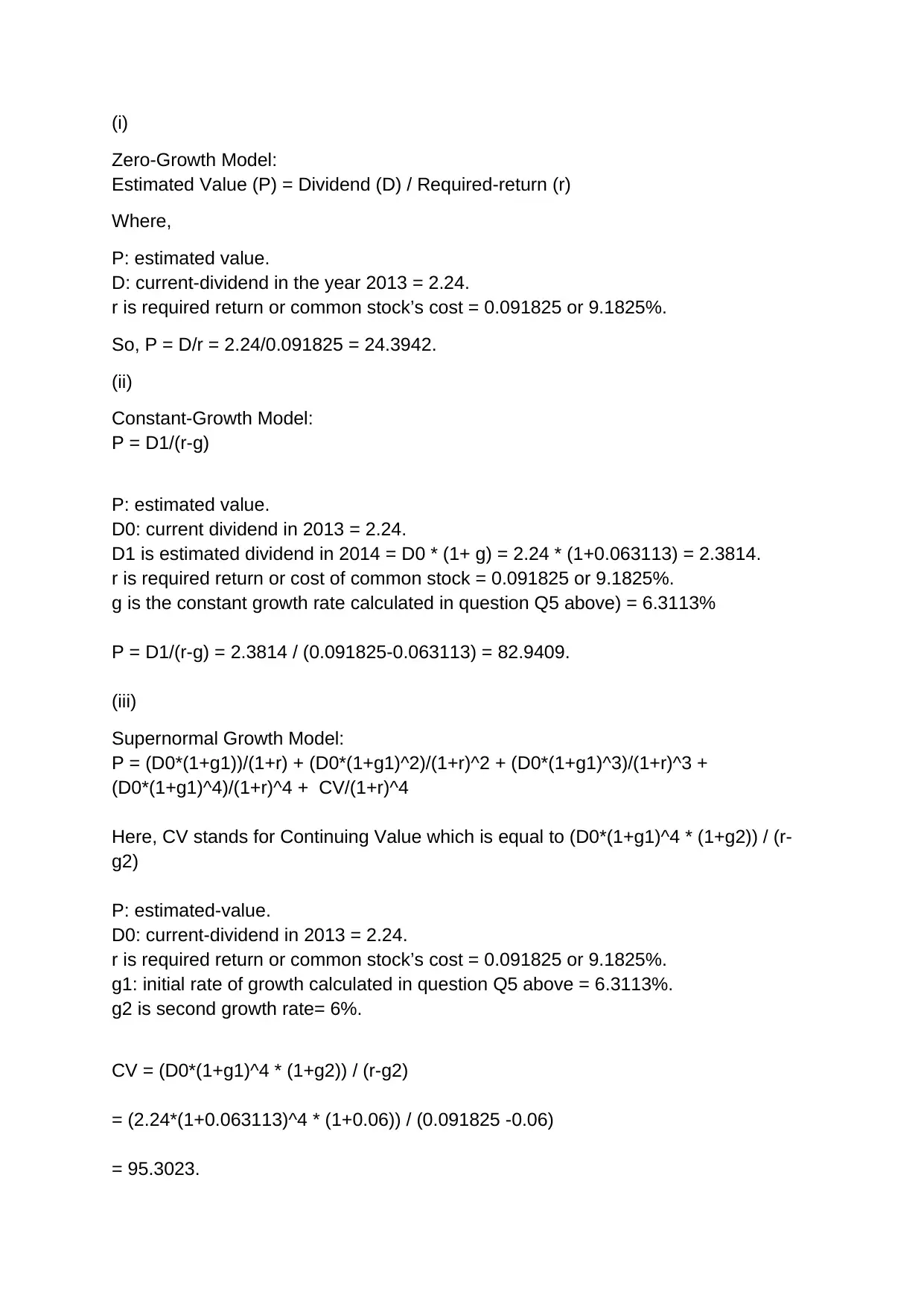

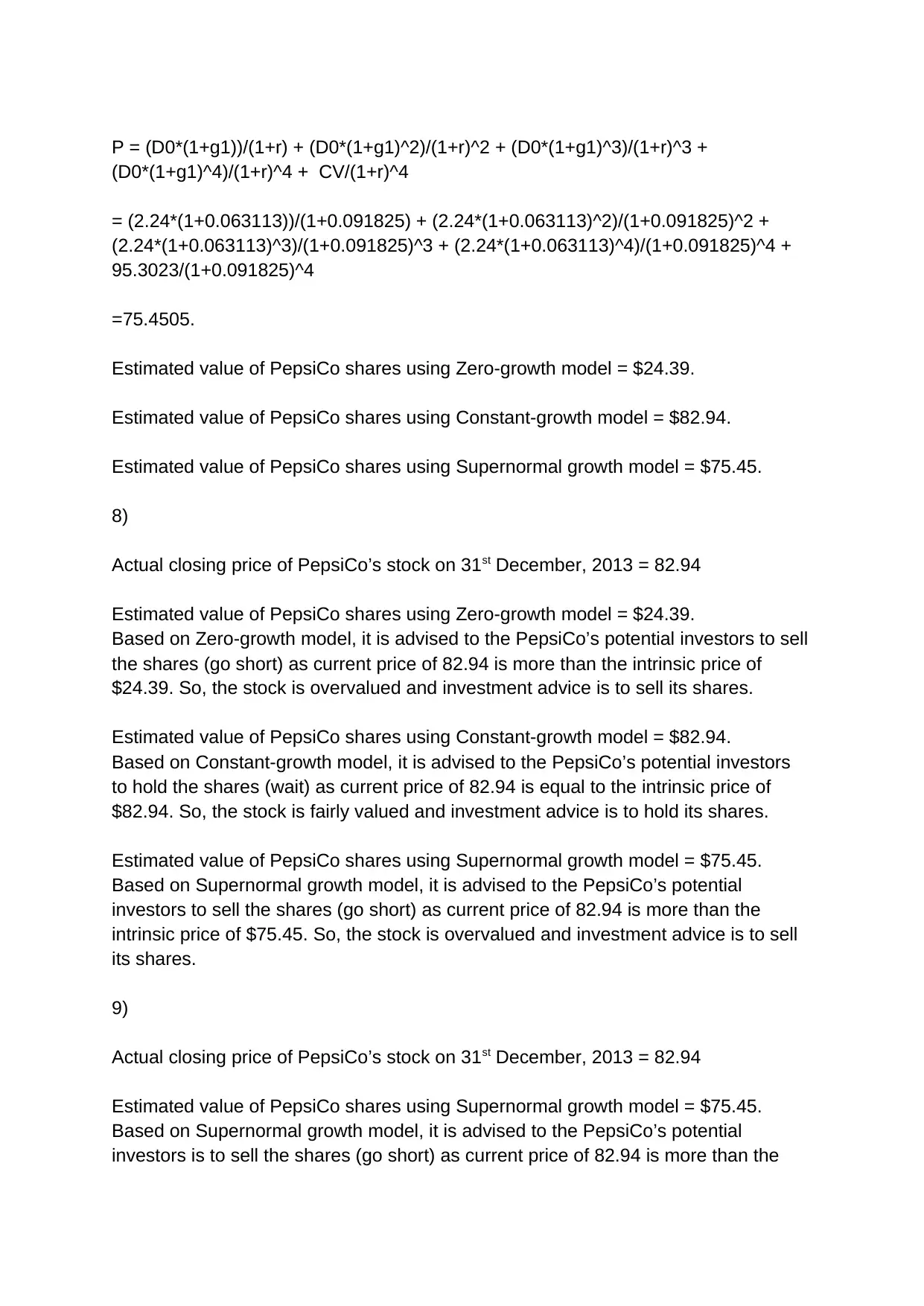

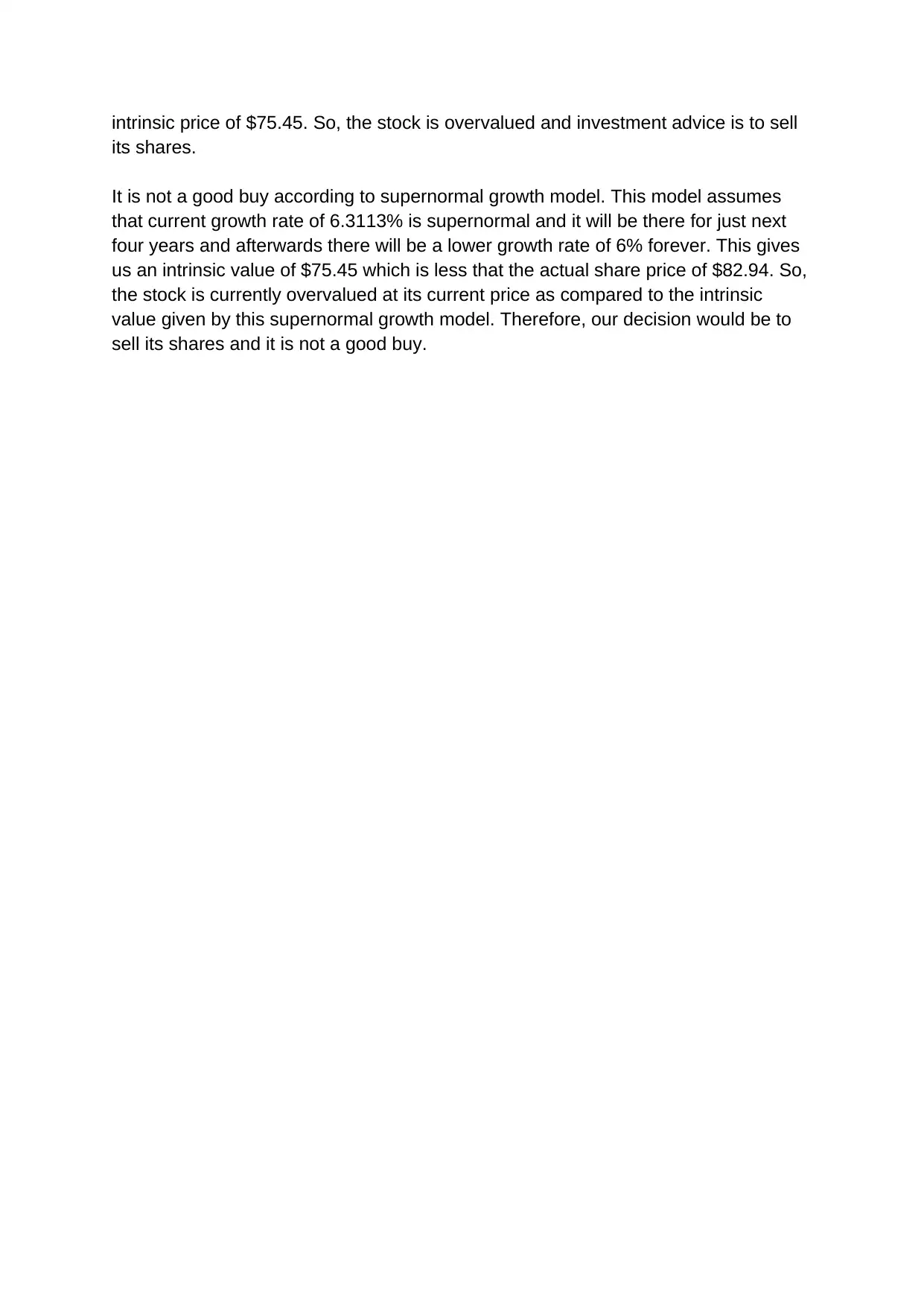

This case study focuses on valuing PepsiCo stock using the Dividend Discount Model (DDM). It begins by explaining the DDM and its advantages and disadvantages. The assignment then applies three DDM variations: zero-growth, constant-growth, and supernormal growth models, to estimate PepsiCo's intrinsic value. It calculates the average annual and compounded average dividend growth rates from 2008 to 2013. The cost of equity is determined using the dividend growth model. The study then calculates the estimated share values using each DDM variation. Finally, it compares the estimated values with the actual market price to provide investment recommendations (buy, sell, or hold). The analysis suggests selling shares based on the supernormal growth model and provides a detailed breakdown of the calculations and assumptions used in each model, offering valuable insights into stock valuation techniques.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.