Taxation Law Report: Dividend Imputation System in Australia

VerifiedAdded on 2021/06/17

|12

|2789

|21

Report

AI Summary

This report provides a comprehensive overview of the dividend imputation system in Australia, a corporate tax system introduced in 1987. It details the system's operation, highlighting the double taxation issue it addressed and the subsequent reforms by the Howard Costello liberal government, including the introduction of franking credits and refundable tax credits. The report examines the rationale behind the system's introduction, focusing on the need to manage dual taxation and incentivize financing. It further analyzes Labour's proposed reforms, discussing their advantages, such as ensuring fair taxation and promoting economic growth, and disadvantages, including potential complexities. The report also answers specific questions related to tax calculations, corporate tax rates, and dividend eligibility, providing a clear understanding of the system's practical application. Finally, the report concludes with a discussion of generally accepted attributes of a good tax policy, such as equity, certainty, and convenience. This report is a valuable resource for students studying taxation and finance, offering a detailed analysis of the Australian dividend imputation system and its implications.

Running Head: TAXATION LAW 0

Taxation Law

Taxation Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW

1

Table of Contents

Part A.........................................................................................................................................2

Introduction............................................................................................................................2

How it operates.......................................................................................................................2

Reason for the introduction....................................................................................................3

Labour’s Proposed Reforms...................................................................................................3

Part B..........................................................................................................................................4

Part C..........................................................................................................................................5

Answer to Question-1.............................................................................................................5

Answer to Question -2............................................................................................................5

Answer to Question-3.............................................................................................................6

Answer to Quetsion-4.............................................................................................................7

Answer to Question-5.............................................................................................................7

References..................................................................................................................................9

1

Table of Contents

Part A.........................................................................................................................................2

Introduction............................................................................................................................2

How it operates.......................................................................................................................2

Reason for the introduction....................................................................................................3

Labour’s Proposed Reforms...................................................................................................3

Part B..........................................................................................................................................4

Part C..........................................................................................................................................5

Answer to Question-1.............................................................................................................5

Answer to Question -2............................................................................................................5

Answer to Question-3.............................................................................................................6

Answer to Quetsion-4.............................................................................................................7

Answer to Question-5.............................................................................................................7

References..................................................................................................................................9

TAXATION LAW

2

Part A

Introduction

Dividend system is a corporate tax system introduced in Australia in 1987 by the Hawke-

Keating labour government. Earlier the company was paying tax on its profits and if the

dividend is allocated than the dividend was taxed against income for shareholders, which

created the effect of the double taxation. In 1997, the rules of eligibility were implemented by

Howard Costello liberal government. The exemption to the shareholder was given of $2000.

After 1999 the exemption was raised by $4000. In 2000 the credits received for franking the

dividend were fully refundable. In 2002 the dividend streaming on preferential shares was

banned (Australian Government, 2018a).

How it operates

For example the company makes a profit of $200 and the tax paid @50% amounts to $100.

The tax amount of $100 is recorded in the franking account. Now the remaining amount left

is of $100 which can be paid either in the same year or in the upcoming years. When the

company operates this way a franking credit has been attached in the franking account in

proportion to the rate of tax (Inside Story 2017). If the $100 is paid as dividend, remaining

$100 can be attached to the franking credit account and the franking account is debited by

$100. The cash amount and the franked income received by an eligible shareholder are

credited as income, and are also credited with the franking credit against the overall tax bill

(McClure, et al 2018).

Thus the profits which are given to eligible shareholders are taxed just once. Either the profits

are retained by the company at the corporate tax rate or the amount is paid later in the form of

the dividends and taxed at the rate of the shareholder’s rate. Dividends can also be paid out

2

Part A

Introduction

Dividend system is a corporate tax system introduced in Australia in 1987 by the Hawke-

Keating labour government. Earlier the company was paying tax on its profits and if the

dividend is allocated than the dividend was taxed against income for shareholders, which

created the effect of the double taxation. In 1997, the rules of eligibility were implemented by

Howard Costello liberal government. The exemption to the shareholder was given of $2000.

After 1999 the exemption was raised by $4000. In 2000 the credits received for franking the

dividend were fully refundable. In 2002 the dividend streaming on preferential shares was

banned (Australian Government, 2018a).

How it operates

For example the company makes a profit of $200 and the tax paid @50% amounts to $100.

The tax amount of $100 is recorded in the franking account. Now the remaining amount left

is of $100 which can be paid either in the same year or in the upcoming years. When the

company operates this way a franking credit has been attached in the franking account in

proportion to the rate of tax (Inside Story 2017). If the $100 is paid as dividend, remaining

$100 can be attached to the franking credit account and the franking account is debited by

$100. The cash amount and the franked income received by an eligible shareholder are

credited as income, and are also credited with the franking credit against the overall tax bill

(McClure, et al 2018).

Thus the profits which are given to eligible shareholders are taxed just once. Either the profits

are retained by the company at the corporate tax rate or the amount is paid later in the form of

the dividends and taxed at the rate of the shareholder’s rate. Dividends can also be paid out

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION LAW

3

when the franking credits are not available. This is known as unfranked dividend, or the

payment of the partly franked dividend is also done.

In cases of the refunds, a franking credit which is received after 1st July 2000 are categorised

as refundable tax credits. It is such a kind of tax which can minimise the liability of the tax

payer’s and any excess amount is refunded back (Rankin, 2017).

Reason for the introduction

The problem of the dual taxation of profits of the company which are related to the

unincorporated enterprises is managed by the methodology of the dividend imputation. It

provides the benefit of the franking credit to the shareholders which is offsetting of the credit

against the income tax liabilities (Balachandran, et al 2017). If the process of the dividend

imputation is not followed the profits which are distributed to the shareholders are taxed

twice one at the level of the company and the other at the level of the shareholders personal

income. Due the dividend imputation process the underlying distortions were removed, which

used to provide incentives for financing through the debt component. The interest expense is

deducted from the corporate income and the therefore, tax is paid only once when received

against the personal income. In the year 1980 many corporations in Australia became highly

leveraged and the biasness is tax is observed which shifted more on the front of debt

financing (Morrison, 2017).

Labour’s Proposed Reforms

Paul Keating the architect of the dividend imputation system, has supported the Labour’s

proposed reforms to cease the refund of cash balances for excess imputation of the credit and

introduced this provision under the governmental supervision by Howard. The system was

proposed with the name as “unnecessary Largesse” (Shevlin, Shivakumar and Urcan, 2017).

The imputation system introduced was not incorporating the cash back for the tax payers who

3

when the franking credits are not available. This is known as unfranked dividend, or the

payment of the partly franked dividend is also done.

In cases of the refunds, a franking credit which is received after 1st July 2000 are categorised

as refundable tax credits. It is such a kind of tax which can minimise the liability of the tax

payer’s and any excess amount is refunded back (Rankin, 2017).

Reason for the introduction

The problem of the dual taxation of profits of the company which are related to the

unincorporated enterprises is managed by the methodology of the dividend imputation. It

provides the benefit of the franking credit to the shareholders which is offsetting of the credit

against the income tax liabilities (Balachandran, et al 2017). If the process of the dividend

imputation is not followed the profits which are distributed to the shareholders are taxed

twice one at the level of the company and the other at the level of the shareholders personal

income. Due the dividend imputation process the underlying distortions were removed, which

used to provide incentives for financing through the debt component. The interest expense is

deducted from the corporate income and the therefore, tax is paid only once when received

against the personal income. In the year 1980 many corporations in Australia became highly

leveraged and the biasness is tax is observed which shifted more on the front of debt

financing (Morrison, 2017).

Labour’s Proposed Reforms

Paul Keating the architect of the dividend imputation system, has supported the Labour’s

proposed reforms to cease the refund of cash balances for excess imputation of the credit and

introduced this provision under the governmental supervision by Howard. The system was

proposed with the name as “unnecessary Largesse” (Shevlin, Shivakumar and Urcan, 2017).

The imputation system introduced was not incorporating the cash back for the tax payers who

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW

4

did not the fall under the category of more than 30% corporate tax rate slab. This policy

created a hassle in the country. Australia’s dividend imputation system ensures that the dual

taxation ion shareholder’s income is not followed. Labour’s plan restores the pre 2001 system

where most tax payers were still allowed to use the credit of the imputation to offset the tax

liability to the Australian Tax Officer (Twite, 2013). There were certain people whose

income tax liability was nil mainly due to the self-managed superannuation funds and

retirees. They were no longer able to take the claim of the refunds in cash. The government

informed that 54% per cent of the people were affected by the Labour policy. Around 612000

individuals were under the category of the income taxable at $18200. They are either part-

pensioners or were non-receivers of the pension at all, and much of the income was drawn

from the superannuation fund. Further, 86% of the value of all franking credits was ultimately

received by those people who fall under the taxable income less than $87000. The policy was

an essential step to the dividend imputation system. The imputation system essentially turned

the entire tax system of the company into the withholding tax, which means a tax which is

withheld by the Commonwealth to be the part of the shareholders to staple the dividend.

Part B

Advantages of the Labour policy

There are certain advantages to the labour policy prevailing in Australia. The first

advantage is the economy and growth of the country. A sound policy generally

determines the tax structure of the country. A clear structure determines the efficiency

of the company to work (Cannavan and Gray, 2017).

After reformation it ensured that the shareholders are not taxed twice on the corporate

profits. The profits can be save d for the purpose of future investments.

4

did not the fall under the category of more than 30% corporate tax rate slab. This policy

created a hassle in the country. Australia’s dividend imputation system ensures that the dual

taxation ion shareholder’s income is not followed. Labour’s plan restores the pre 2001 system

where most tax payers were still allowed to use the credit of the imputation to offset the tax

liability to the Australian Tax Officer (Twite, 2013). There were certain people whose

income tax liability was nil mainly due to the self-managed superannuation funds and

retirees. They were no longer able to take the claim of the refunds in cash. The government

informed that 54% per cent of the people were affected by the Labour policy. Around 612000

individuals were under the category of the income taxable at $18200. They are either part-

pensioners or were non-receivers of the pension at all, and much of the income was drawn

from the superannuation fund. Further, 86% of the value of all franking credits was ultimately

received by those people who fall under the taxable income less than $87000. The policy was

an essential step to the dividend imputation system. The imputation system essentially turned

the entire tax system of the company into the withholding tax, which means a tax which is

withheld by the Commonwealth to be the part of the shareholders to staple the dividend.

Part B

Advantages of the Labour policy

There are certain advantages to the labour policy prevailing in Australia. The first

advantage is the economy and growth of the country. A sound policy generally

determines the tax structure of the country. A clear structure determines the efficiency

of the company to work (Cannavan and Gray, 2017).

After reformation it ensured that the shareholders are not taxed twice on the corporate

profits. The profits can be save d for the purpose of future investments.

TAXATION LAW

5

Franking credits were attached to the dividends which have been distributed to the

shareholders. This eventually led to taking the shareholders in confidence (Bellamy,

2015).

The tax was utilised to offset any personal tax underlying and to be paid to the

Australian tax office. This helped in reduction of the overall liability.

Refunds for unused credit were also made available after the reformation.

The claims are not misleading and a proper tax calculation has been introduced to

avoid the cascading effect (Murphy, 2018).

Disadvantages of Labour Policy

Dual Taxation: The biggest disadvantage of the labour policy earlier was the

imposition of dual taxation on the income of the shareholders. The credit was not

given back then.

Labour policy planned to abolish refunds of the credits of imputations which are

unused. The claim was not allowed to be taken.

Earlier the retirees who were having enough wealth were not ready to pay the fair tax

of share and the lower class people suffered due to this. The fact that what they own is

different from they pay in the form of tax (Nguyen and Balachandran, 2017).

Superannuation pay-outs have been made tax free since 2006. They were not even

supposed to be declared on personal income tax returns. Apart from these shares,

investment property, bank deposits were also not formed under the category of the

taxable income (Rankin, 2017).

Australian Bureau of Statistics also does not provide the clear picture of the people

and the number of shares they own, whether they receive imputation tax credit and

lastly how much income they pay.

5

Franking credits were attached to the dividends which have been distributed to the

shareholders. This eventually led to taking the shareholders in confidence (Bellamy,

2015).

The tax was utilised to offset any personal tax underlying and to be paid to the

Australian tax office. This helped in reduction of the overall liability.

Refunds for unused credit were also made available after the reformation.

The claims are not misleading and a proper tax calculation has been introduced to

avoid the cascading effect (Murphy, 2018).

Disadvantages of Labour Policy

Dual Taxation: The biggest disadvantage of the labour policy earlier was the

imposition of dual taxation on the income of the shareholders. The credit was not

given back then.

Labour policy planned to abolish refunds of the credits of imputations which are

unused. The claim was not allowed to be taken.

Earlier the retirees who were having enough wealth were not ready to pay the fair tax

of share and the lower class people suffered due to this. The fact that what they own is

different from they pay in the form of tax (Nguyen and Balachandran, 2017).

Superannuation pay-outs have been made tax free since 2006. They were not even

supposed to be declared on personal income tax returns. Apart from these shares,

investment property, bank deposits were also not formed under the category of the

taxable income (Rankin, 2017).

Australian Bureau of Statistics also does not provide the clear picture of the people

and the number of shares they own, whether they receive imputation tax credit and

lastly how much income they pay.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION LAW

6

The policy was complex and people were not able to understand the mechanism and

operation of the same (Ingles and Stewart, 2018).

There was lack of certainty in the policy earlier. The tax portion was not calculated

correctly and there was no transparency about the income of the individuals.

Generally accepted attributes of a good tax policy

For a policy to be considered as the good tax policy there are certain principles which have

been followed accordingly.

Equity and fairness: The situated tax payers shall be taxed similarly. This includes the

horizontal level of equity which determines the liability of each individual of a

particular category to be the same. Vertical equity on the other hand attribute to fact

that the tax payers with the greater liability shall be pooled under one category and

shall pay more taxes.

Certainty: tax rules shall be of lucid nature and it shall describe the payment methods

and the limit and extent for each group accordingly. The rules shall also pertain to the

fact that the tax is calculated correctly or not (Tran and Zhu, 2017).

Convenience of payment: A tax payer if made due shall be in capacity and

convenience to the tax payer. The convenience at times also leads to follow up of

compliances by the tax payers. To determine whether the payment mechanism is

appropriate or not will ultimately depend upon the liability’s amount and how the

collection can be made in an easy manner (Shaw, 2017)

Economy of calculation: the cost shall be kept in such a manner which is feasible for

both the government as well as the tax payer.

6

The policy was complex and people were not able to understand the mechanism and

operation of the same (Ingles and Stewart, 2018).

There was lack of certainty in the policy earlier. The tax portion was not calculated

correctly and there was no transparency about the income of the individuals.

Generally accepted attributes of a good tax policy

For a policy to be considered as the good tax policy there are certain principles which have

been followed accordingly.

Equity and fairness: The situated tax payers shall be taxed similarly. This includes the

horizontal level of equity which determines the liability of each individual of a

particular category to be the same. Vertical equity on the other hand attribute to fact

that the tax payers with the greater liability shall be pooled under one category and

shall pay more taxes.

Certainty: tax rules shall be of lucid nature and it shall describe the payment methods

and the limit and extent for each group accordingly. The rules shall also pertain to the

fact that the tax is calculated correctly or not (Tran and Zhu, 2017).

Convenience of payment: A tax payer if made due shall be in capacity and

convenience to the tax payer. The convenience at times also leads to follow up of

compliances by the tax payers. To determine whether the payment mechanism is

appropriate or not will ultimately depend upon the liability’s amount and how the

collection can be made in an easy manner (Shaw, 2017)

Economy of calculation: the cost shall be kept in such a manner which is feasible for

both the government as well as the tax payer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW

7

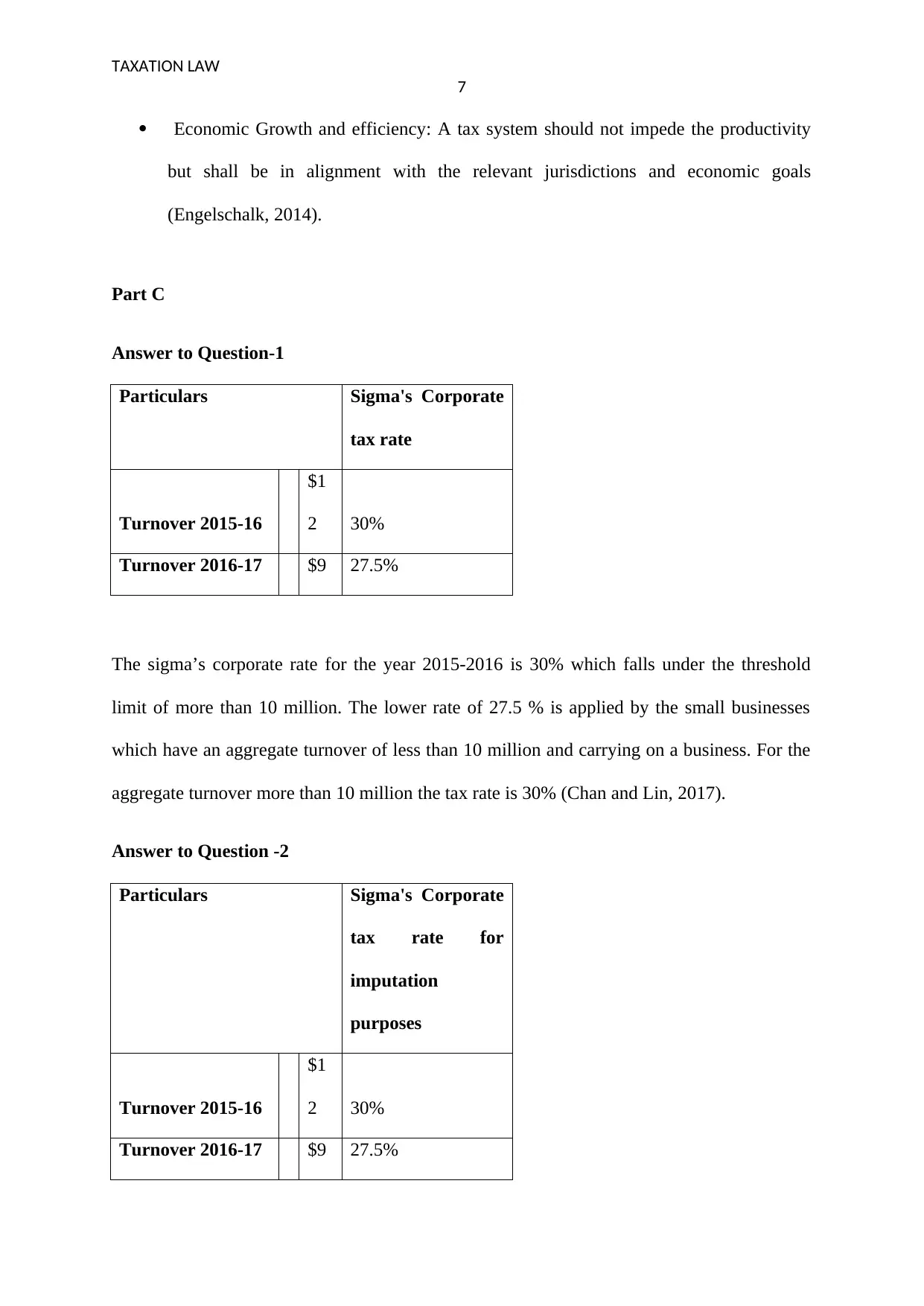

Economic Growth and efficiency: A tax system should not impede the productivity

but shall be in alignment with the relevant jurisdictions and economic goals

(Engelschalk, 2014).

Part C

Answer to Question-1

Particulars Sigma's Corporate

tax rate

Turnover 2015-16

$1

2 30%

Turnover 2016-17 $9 27.5%

The sigma’s corporate rate for the year 2015-2016 is 30% which falls under the threshold

limit of more than 10 million. The lower rate of 27.5 % is applied by the small businesses

which have an aggregate turnover of less than 10 million and carrying on a business. For the

aggregate turnover more than 10 million the tax rate is 30% (Chan and Lin, 2017).

Answer to Question -2

Particulars Sigma's Corporate

tax rate for

imputation

purposes

Turnover 2015-16

$1

2 30%

Turnover 2016-17 $9 27.5%

7

Economic Growth and efficiency: A tax system should not impede the productivity

but shall be in alignment with the relevant jurisdictions and economic goals

(Engelschalk, 2014).

Part C

Answer to Question-1

Particulars Sigma's Corporate

tax rate

Turnover 2015-16

$1

2 30%

Turnover 2016-17 $9 27.5%

The sigma’s corporate rate for the year 2015-2016 is 30% which falls under the threshold

limit of more than 10 million. The lower rate of 27.5 % is applied by the small businesses

which have an aggregate turnover of less than 10 million and carrying on a business. For the

aggregate turnover more than 10 million the tax rate is 30% (Chan and Lin, 2017).

Answer to Question -2

Particulars Sigma's Corporate

tax rate for

imputation

purposes

Turnover 2015-16

$1

2 30%

Turnover 2016-17 $9 27.5%

TAXATION LAW

8

The corporate tax rate for the purpose of the dividend imputation has not changed for the year

2015-16 and 2016-17 (Australian Government 2018a).

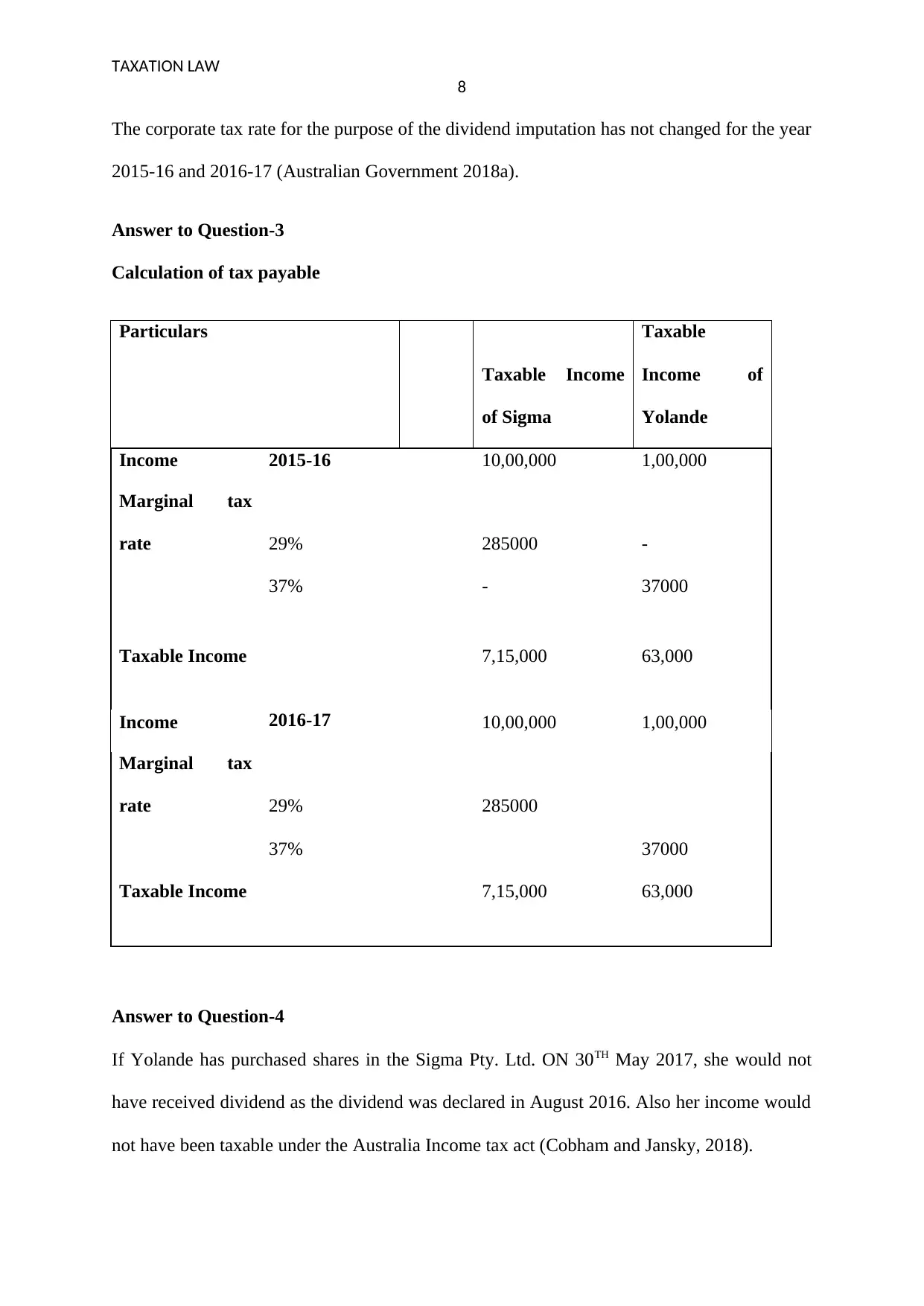

Answer to Question-3

Calculation of tax payable

Particulars

Taxable Income

of Sigma

Taxable

Income of

Yolande

Income 2015-16 10,00,000 1,00,000

Marginal tax

rate 29% 285000 -

37% - 37000

Taxable Income 7,15,000 63,000

Income 2016-17 10,00,000 1,00,000

Marginal tax

rate 29% 285000

37% 37000

Taxable Income 7,15,000 63,000

Answer to Question-4

If Yolande has purchased shares in the Sigma Pty. Ltd. ON 30TH May 2017, she would not

have received dividend as the dividend was declared in August 2016. Also her income would

not have been taxable under the Australia Income tax act (Cobham and Jansky, 2018).

8

The corporate tax rate for the purpose of the dividend imputation has not changed for the year

2015-16 and 2016-17 (Australian Government 2018a).

Answer to Question-3

Calculation of tax payable

Particulars

Taxable Income

of Sigma

Taxable

Income of

Yolande

Income 2015-16 10,00,000 1,00,000

Marginal tax

rate 29% 285000 -

37% - 37000

Taxable Income 7,15,000 63,000

Income 2016-17 10,00,000 1,00,000

Marginal tax

rate 29% 285000

37% 37000

Taxable Income 7,15,000 63,000

Answer to Question-4

If Yolande has purchased shares in the Sigma Pty. Ltd. ON 30TH May 2017, she would not

have received dividend as the dividend was declared in August 2016. Also her income would

not have been taxable under the Australia Income tax act (Cobham and Jansky, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION LAW

9

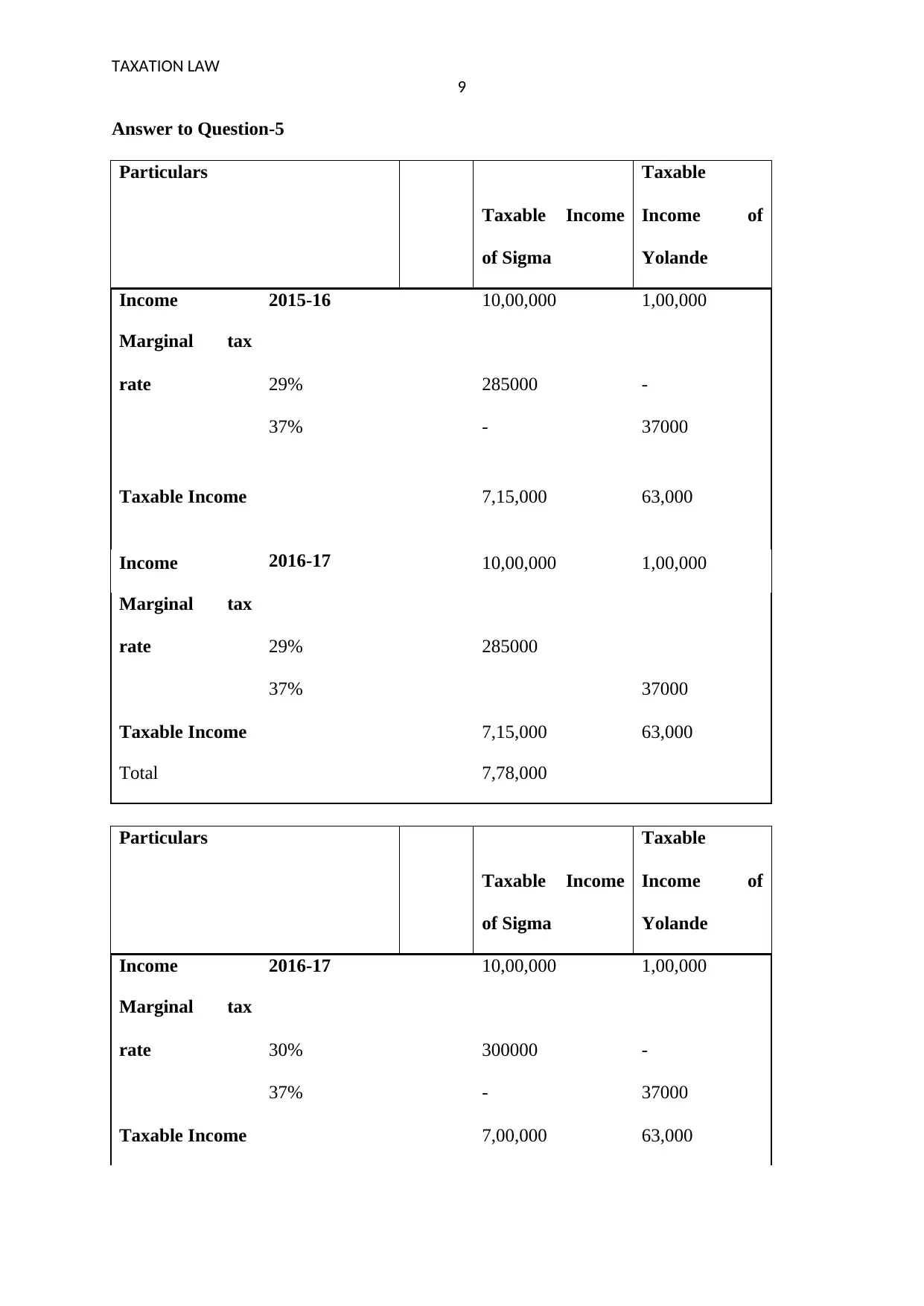

Answer to Question-5

Particulars

Taxable Income

of Sigma

Taxable

Income of

Yolande

Income 2015-16 10,00,000 1,00,000

Marginal tax

rate 29% 285000 -

37% - 37000

Taxable Income 7,15,000 63,000

Income 2016-17 10,00,000 1,00,000

Marginal tax

rate 29% 285000

37% 37000

Taxable Income 7,15,000 63,000

Total 7,78,000

Particulars

Taxable Income

of Sigma

Taxable

Income of

Yolande

Income 2016-17 10,00,000 1,00,000

Marginal tax

rate 30% 300000 -

37% - 37000

Taxable Income 7,00,000 63,000

9

Answer to Question-5

Particulars

Taxable Income

of Sigma

Taxable

Income of

Yolande

Income 2015-16 10,00,000 1,00,000

Marginal tax

rate 29% 285000 -

37% - 37000

Taxable Income 7,15,000 63,000

Income 2016-17 10,00,000 1,00,000

Marginal tax

rate 29% 285000

37% 37000

Taxable Income 7,15,000 63,000

Total 7,78,000

Particulars

Taxable Income

of Sigma

Taxable

Income of

Yolande

Income 2016-17 10,00,000 1,00,000

Marginal tax

rate 30% 300000 -

37% - 37000

Taxable Income 7,00,000 63,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW

10

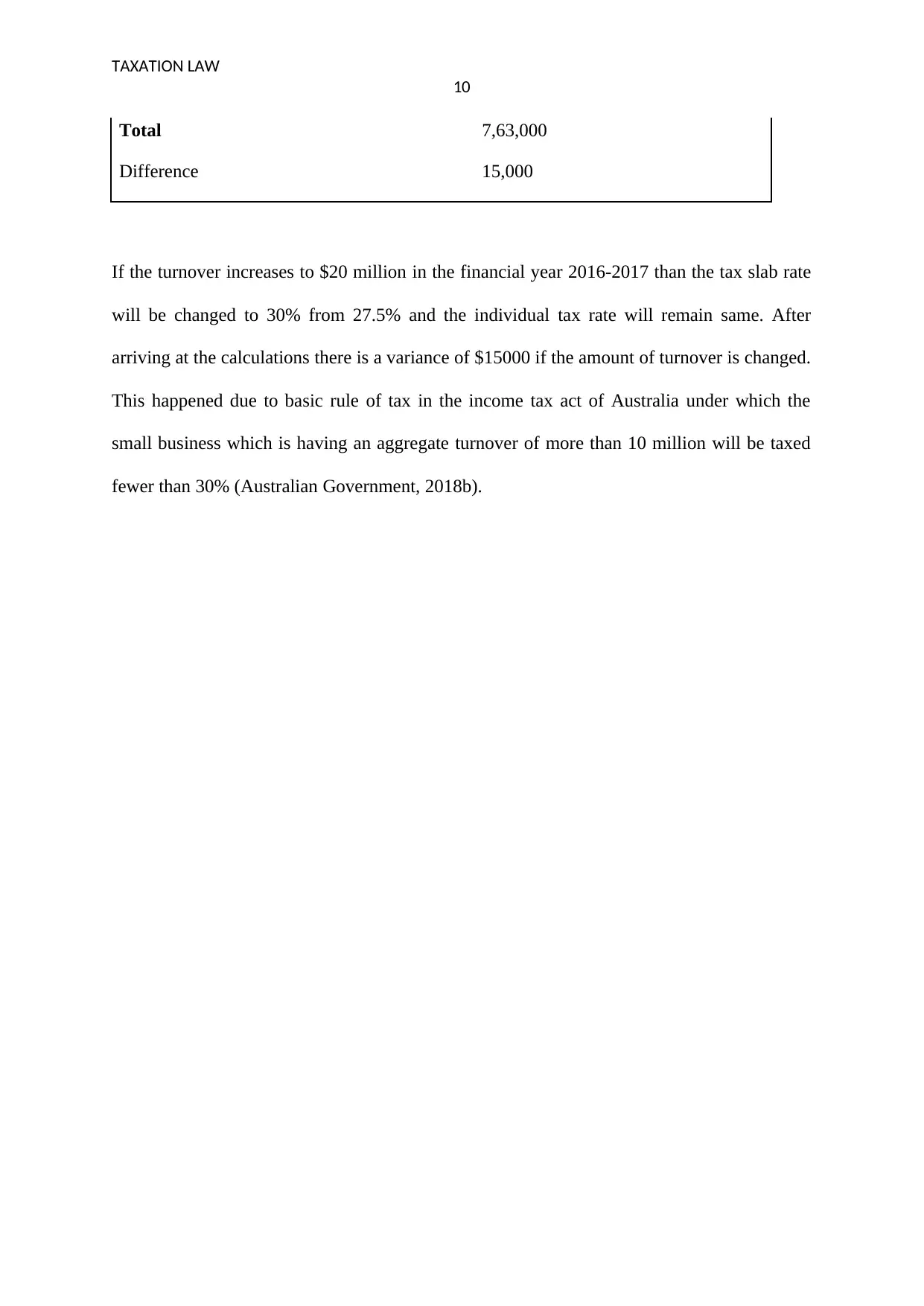

Total 7,63,000

Difference 15,000

If the turnover increases to $20 million in the financial year 2016-2017 than the tax slab rate

will be changed to 30% from 27.5% and the individual tax rate will remain same. After

arriving at the calculations there is a variance of $15000 if the amount of turnover is changed.

This happened due to basic rule of tax in the income tax act of Australia under which the

small business which is having an aggregate turnover of more than 10 million will be taxed

fewer than 30% (Australian Government, 2018b).

10

Total 7,63,000

Difference 15,000

If the turnover increases to $20 million in the financial year 2016-2017 than the tax slab rate

will be changed to 30% from 27.5% and the individual tax rate will remain same. After

arriving at the calculations there is a variance of $15000 if the amount of turnover is changed.

This happened due to basic rule of tax in the income tax act of Australia under which the

small business which is having an aggregate turnover of more than 10 million will be taxed

fewer than 30% (Australian Government, 2018b).

TAXATION LAW

11

References

Australian Government (2018a) Changes to company tax rates, [online] Available from

https://www.ato.gov.au/Rates/Changes-to-company-tax-rates/ [Accessed on 18th May 2018].

Australian Government (2018b) Reducing company tax rates, [online] Available from

https://www.ato.gov.au/General/New-legislation/In-detail/Direct-taxes/Income-tax-for-

businesses/Reducing-the-corporate-tax-rate/ [Accessed on 17th May 2018].

Balachandran, B., et al. (2017) Insider ownership and dividend policy in an imputation tax

environment. Journal of Corporate Finance, 12(9), pp. 15-19.

Bellamy, D. E. (2015) Evidence of imputation clienteles in the Australian equity market. Asia

Pacific Journal of Management, 11(2), pp. 275-287.

Cannavan, D., and Gray, S. (2017) Dividend drop-off estimates of the value of dividend

imputation tax credits. Pacific-Basin Finance Journal, 46, pp. 213-226.

Chan, C. H., and Lin, M. H. (2017) Imputation tax system, dividend pay-out, and investor

behavior: Evidence from the Taiwan stock exchange. Asia Pacific Management

Review, 22(3), pp. 146-158.

Cobham, A., and Janský, P. (2018) Global distribution of revenue loss from corporate tax

avoidance: re‐estimation and country results. Journal of International Development, 30(2),

pp. 206-232.

Engelschalk, M. (2014) Creating a favourable tax environment for small

business. Contributions to Economic Analysis, 268(1), pp. 275-311.

11

References

Australian Government (2018a) Changes to company tax rates, [online] Available from

https://www.ato.gov.au/Rates/Changes-to-company-tax-rates/ [Accessed on 18th May 2018].

Australian Government (2018b) Reducing company tax rates, [online] Available from

https://www.ato.gov.au/General/New-legislation/In-detail/Direct-taxes/Income-tax-for-

businesses/Reducing-the-corporate-tax-rate/ [Accessed on 17th May 2018].

Balachandran, B., et al. (2017) Insider ownership and dividend policy in an imputation tax

environment. Journal of Corporate Finance, 12(9), pp. 15-19.

Bellamy, D. E. (2015) Evidence of imputation clienteles in the Australian equity market. Asia

Pacific Journal of Management, 11(2), pp. 275-287.

Cannavan, D., and Gray, S. (2017) Dividend drop-off estimates of the value of dividend

imputation tax credits. Pacific-Basin Finance Journal, 46, pp. 213-226.

Chan, C. H., and Lin, M. H. (2017) Imputation tax system, dividend pay-out, and investor

behavior: Evidence from the Taiwan stock exchange. Asia Pacific Management

Review, 22(3), pp. 146-158.

Cobham, A., and Janský, P. (2018) Global distribution of revenue loss from corporate tax

avoidance: re‐estimation and country results. Journal of International Development, 30(2),

pp. 206-232.

Engelschalk, M. (2014) Creating a favourable tax environment for small

business. Contributions to Economic Analysis, 268(1), pp. 275-311.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.