Financial Management: Dividend Policy, Investment Appraisal Techniques

VerifiedAdded on 2023/01/09

|18

|3909

|25

Report

AI Summary

This report delves into the core aspects of financial management, beginning with an examination of dividend policy. It explores the factors influencing dividend decisions, including legal requirements, liquidity, repayment needs, and expected rates of return. The report analyzes different dividend options, such as cash dividends, scrip dividends, and share repurchases, providing calculations and interpretations. Furthermore, the report critically evaluates how companies make decisions that affect investment opportunities, considering the impact on resources and return on investment. The second part of the report focuses on investment appraisal techniques, describing methods like the payback period, and critically evaluating their benefits and limitations, providing a comprehensive overview of financial management practices.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

MAIN BODY.................................................................................................................................................3

Question 2- Dividend Policy.........................................................................................................................3

1. Size of the annual dividend which return to its shareholders...............................................................3

2. Practical issues that need to consider at the time of deciding size of dividend payment......................5

3. Calculate the three options...................................................................................................................6

4. Critically evaluate how companies make their decisions which affects the investment opportunities. 8

QUESTION 3.................................................................................................................................................9

Description of all the investment appraisal techniques............................................................................9

Critical evaluation of benefits and limitations of all the investment appraisal techniques.....................13

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................16

INTRODUCTION...........................................................................................................................................3

MAIN BODY.................................................................................................................................................3

Question 2- Dividend Policy.........................................................................................................................3

1. Size of the annual dividend which return to its shareholders...............................................................3

2. Practical issues that need to consider at the time of deciding size of dividend payment......................5

3. Calculate the three options...................................................................................................................6

4. Critically evaluate how companies make their decisions which affects the investment opportunities. 8

QUESTION 3.................................................................................................................................................9

Description of all the investment appraisal techniques............................................................................9

Critical evaluation of benefits and limitations of all the investment appraisal techniques.....................13

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial management is defined as having to work with others and assessing funds as well

as financial affairs to promote or budget accordingly after a person or a firm. A aspect of

financial auditing is the component a finance manager does for a company. It requires

information and appropriate management, distribution and exposure to businesses' current

liabilities, and availability of business financing items along with investment, revenue, payable

accounts and accruals, working capital and profitability (Alkordi, Al-Nimer and Dabaghia,

2017). Financial management is described as communicating with and evaluating property and

money to further prepare financial reports for a individual or a company. The instance of cash

decisions is the things undertaken for a corporation by accounts payable. This analysis is focused

on different separate questions where the first concerns dividend policy that covers many aspects

such as the magnitude of the yearly payout returned to its stockholders or many practical

problems that had to be addressed while making informed decisions on retained earnings. It also

includes the estimation of three choices and objectively analyses the measures made by the

organization in the third. Second question focused on capital budgeting techniques that enables

the economy evaluate increasing idea is advantageous to them or they does or doesn't innovate in

it.

MAIN BODY

Question 2- Dividend Policy

1. Size of the annual dividend which return to its shareholders

Dividend is essentially the sum or fraction of the income of a company, the gain in the

valuation and promotion of participants of the council; it is reported and payable as both a

percentage of par company's securities. In essence, a dividend is a component of the bonus which

really occurs after sufficient allocation has now been made for different types of services and

revenues etc. after all expenditure has been withdrawn from the total sales. Supporters are so

responsible for having the profit, and could not consent to the delivery purposes. When the

company wants revenue so entity retains the full percentage of the profits with or without

providing any distribution (Baker and Dellaert, 2017). Thus no dividends are registered in the

Financial management is defined as having to work with others and assessing funds as well

as financial affairs to promote or budget accordingly after a person or a firm. A aspect of

financial auditing is the component a finance manager does for a company. It requires

information and appropriate management, distribution and exposure to businesses' current

liabilities, and availability of business financing items along with investment, revenue, payable

accounts and accruals, working capital and profitability (Alkordi, Al-Nimer and Dabaghia,

2017). Financial management is described as communicating with and evaluating property and

money to further prepare financial reports for a individual or a company. The instance of cash

decisions is the things undertaken for a corporation by accounts payable. This analysis is focused

on different separate questions where the first concerns dividend policy that covers many aspects

such as the magnitude of the yearly payout returned to its stockholders or many practical

problems that had to be addressed while making informed decisions on retained earnings. It also

includes the estimation of three choices and objectively analyses the measures made by the

organization in the third. Second question focused on capital budgeting techniques that enables

the economy evaluate increasing idea is advantageous to them or they does or doesn't innovate in

it.

MAIN BODY

Question 2- Dividend Policy

1. Size of the annual dividend which return to its shareholders

Dividend is essentially the sum or fraction of the income of a company, the gain in the

valuation and promotion of participants of the council; it is reported and payable as both a

percentage of par company's securities. In essence, a dividend is a component of the bonus which

really occurs after sufficient allocation has now been made for different types of services and

revenues etc. after all expenditure has been withdrawn from the total sales. Supporters are so

responsible for having the profit, and could not consent to the delivery purposes. When the

company wants revenue so entity retains the full percentage of the profits with or without

providing any distribution (Baker and Dellaert, 2017). Thus no dividends are registered in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

event that the net profit is supposed to still be in the context of a standard unit or shortfall.

Understand the two usual things listed below by you concentrate on interest earned.

Fair consideration

Management teams could use a reliable estimate of the magnitude to which stakeholders

expect to take advantage of the resources and take incentives in return. When this is not

achieved, it would also be impossible to keep the creditors absolutely satisfied because this will

want a negative effect on the group's investment performance on shares of gratitude.

Company’s requirement:

Handling the lengthy-term financial position is the administrators' main purpose,

particularly when representatives are expected to make certain concessions to do so. This is

indeed absolutely crucial enough for entrepreneur to be able to visually determine exactly how

often additional capital the industry needs to expand and prosper (Chiappini, 2017).

Factors determined at the time making dividend decisions:

When an organisation takes decision in regard of dividend for the distribution of the

shareholders. This time manager can focus on different things in particular manner such as:

Legal requirements: A corporation has no lawful moral obligation to interest - bearing debt.

There are, however, other law-imposed requirements on how distribution is allocated. There are

essentially three rules pertaining to dividend payouts. They're the law of net income, the law of

negative return and the law of bankruptcy.

Firm’s liquidity position: Payment of dividends is also influenced by the leverage status of the

company. Given ample capital gains, if the profits are not kept in money the company would not

be able to buy outright dividends.

Repayment need: To fulfill their capital needs, a company uses many types of equity financing.

Upon completion, the obligation must be forgiven. If the company needs to maintain its earnings

for debt servicing purposes, the ability to pay dividends reduces.

Understand the two usual things listed below by you concentrate on interest earned.

Fair consideration

Management teams could use a reliable estimate of the magnitude to which stakeholders

expect to take advantage of the resources and take incentives in return. When this is not

achieved, it would also be impossible to keep the creditors absolutely satisfied because this will

want a negative effect on the group's investment performance on shares of gratitude.

Company’s requirement:

Handling the lengthy-term financial position is the administrators' main purpose,

particularly when representatives are expected to make certain concessions to do so. This is

indeed absolutely crucial enough for entrepreneur to be able to visually determine exactly how

often additional capital the industry needs to expand and prosper (Chiappini, 2017).

Factors determined at the time making dividend decisions:

When an organisation takes decision in regard of dividend for the distribution of the

shareholders. This time manager can focus on different things in particular manner such as:

Legal requirements: A corporation has no lawful moral obligation to interest - bearing debt.

There are, however, other law-imposed requirements on how distribution is allocated. There are

essentially three rules pertaining to dividend payouts. They're the law of net income, the law of

negative return and the law of bankruptcy.

Firm’s liquidity position: Payment of dividends is also influenced by the leverage status of the

company. Given ample capital gains, if the profits are not kept in money the company would not

be able to buy outright dividends.

Repayment need: To fulfill their capital needs, a company uses many types of equity financing.

Upon completion, the obligation must be forgiven. If the company needs to maintain its earnings

for debt servicing purposes, the ability to pay dividends reduces.

Expected rate of return: If the anticipated rate of interest on the capital funding is

comparatively higher for a company, the company tends to maintain profits for government

investment instead of just allocate cash dividends (Gaynor and et.al, 2016).

Stability of earnings: When a business has fairly predictable profits, it is much more probable

than with a company with fairly varying income to offer comparatively greater dividends.

2. Practical issues that need to consider at the time of deciding size of dividend payment

There a

Legal, contractual constraints and restrictions: It is among the most important measures

to be taken into consideration when evaluating a company's dividend strategy as it needs to grow

within the corporate framework and constraints. Declaring distributions is not legally enforceable

on the performance of the structure. Upon paying interest, distributions shall are only announced

or payable so out existing or previous income, though its Federal system allows any person to

pay distributions from out expected earnings for any fiscal years prior to spending billions.

Tax policy: The tax policy practiced as a company often influences a company's dividend

strategy. If it is easier to announce and pay dividends in money or by issuing reward securities,

relies on the taxation policy to some degree. Since dividend payments are not so beneficial to

buyers in higher income brackets, either (Gleasure and Feller, 2016).

Stability of dividends: For this reason it really should be given significant weight-age while the

same would vary through one company to the next. For example, the dividend payout should

have a level of consistency, i.e. income / revenue that vary significantly from week to week but

not really the distribution as stakeholders tend to consider predictable distributions rather than

varying ones. In many other terms, the companies consider a secure dividend in almost as often

as they do the annual dividend. Steady distributions relate to the continuity or absence of

variation in the income channel, payments shall be made on a consistent basis, i.e. a certain

specific number of payout.

Inflation: Inflation could also influence a company's payout strategy. Through can costs, the

finances created by deflation can fall well short to replacement outdated technology. The deficit

can be rendered from financing activities (as a funding source). This is really important because

comparatively higher for a company, the company tends to maintain profits for government

investment instead of just allocate cash dividends (Gaynor and et.al, 2016).

Stability of earnings: When a business has fairly predictable profits, it is much more probable

than with a company with fairly varying income to offer comparatively greater dividends.

2. Practical issues that need to consider at the time of deciding size of dividend payment

There a

Legal, contractual constraints and restrictions: It is among the most important measures

to be taken into consideration when evaluating a company's dividend strategy as it needs to grow

within the corporate framework and constraints. Declaring distributions is not legally enforceable

on the performance of the structure. Upon paying interest, distributions shall are only announced

or payable so out existing or previous income, though its Federal system allows any person to

pay distributions from out expected earnings for any fiscal years prior to spending billions.

Tax policy: The tax policy practiced as a company often influences a company's dividend

strategy. If it is easier to announce and pay dividends in money or by issuing reward securities,

relies on the taxation policy to some degree. Since dividend payments are not so beneficial to

buyers in higher income brackets, either (Gleasure and Feller, 2016).

Stability of dividends: For this reason it really should be given significant weight-age while the

same would vary through one company to the next. For example, the dividend payout should

have a level of consistency, i.e. income / revenue that vary significantly from week to week but

not really the distribution as stakeholders tend to consider predictable distributions rather than

varying ones. In many other terms, the companies consider a secure dividend in almost as often

as they do the annual dividend. Steady distributions relate to the continuity or absence of

variation in the income channel, payments shall be made on a consistent basis, i.e. a certain

specific number of payout.

Inflation: Inflation could also influence a company's payout strategy. Through can costs, the

finances created by deflation can fall well short to replacement outdated technology. The deficit

can be rendered from financing activities (as a funding source). This is really important because

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in the foreseeable term the properties have to be substituted. As being such, the dividend yield

throughout times of inflation appears to be small (Halim and et.al, 2019).

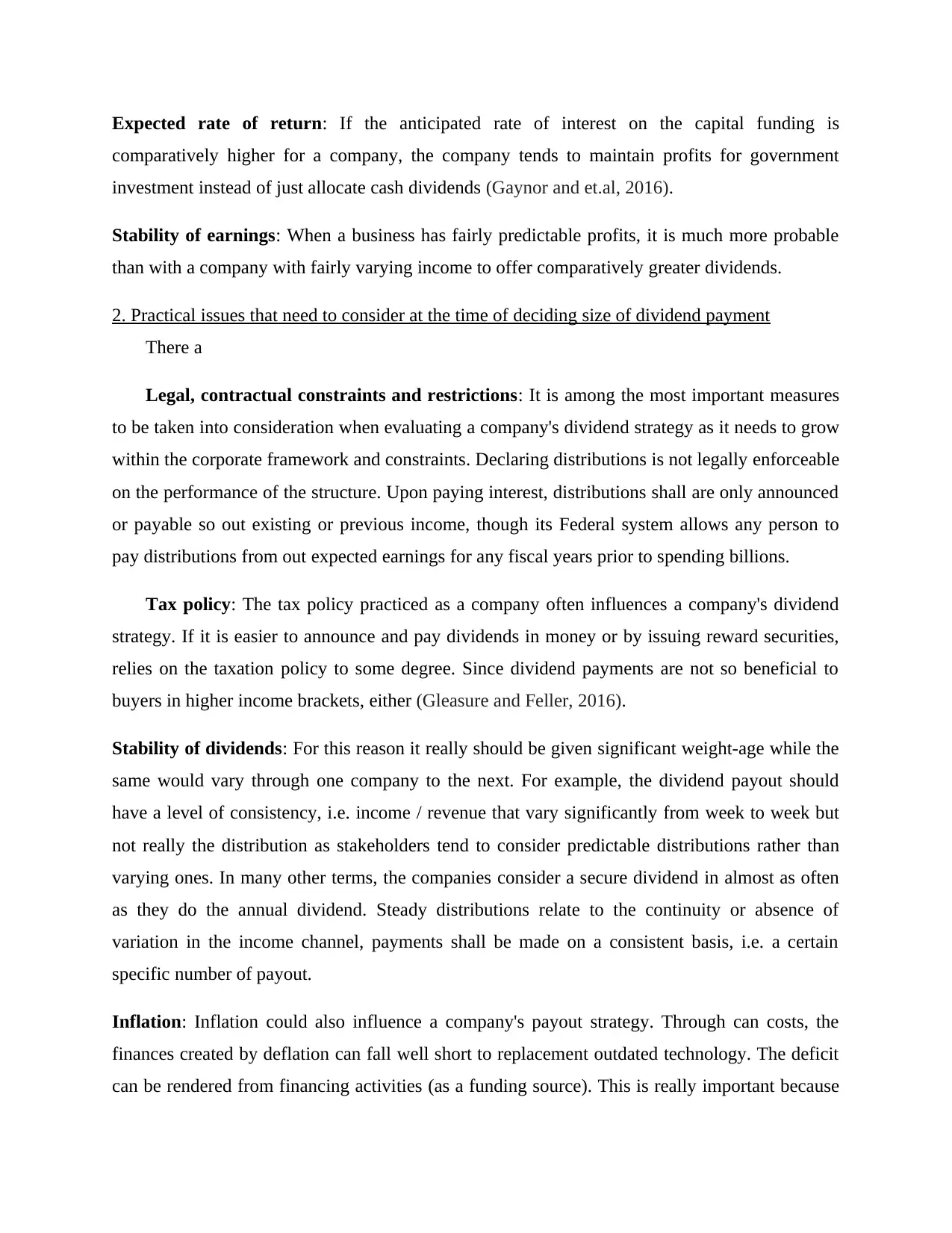

3. Calculate the three options

Cash dividend: Cash dividends reflect control of the distributed income to company ’s

shareholders and offer an opportunity for buyers to invest the stock of big businesses, even

though they're not growth-oriented. People paying cash dividends produce usually good working

capital for coming periods and thus are generally seen as economically viable. Yet most

dividend-paying businesses aren't growth-oriented. Rather, they look to enhance the investors'

interests and to create a stable revenue source for their investors. Companies are now looking to

develop into developing companies and are focused on potential prospects for growth. Many

dividend-paying firms preferably place their dividend payment at about fifty percent -55 percent,

and allocate the resulting remaining balance as a distribution to their stakeholders.

Interpretation: Shown above list illustrates that for housing benefits, a requirement of 1250

shares issued are deemed necessary; bribe money is the decision being made to make profits.

And the maximum tax deduction is £187.5 per transaction, at 15 pesa.

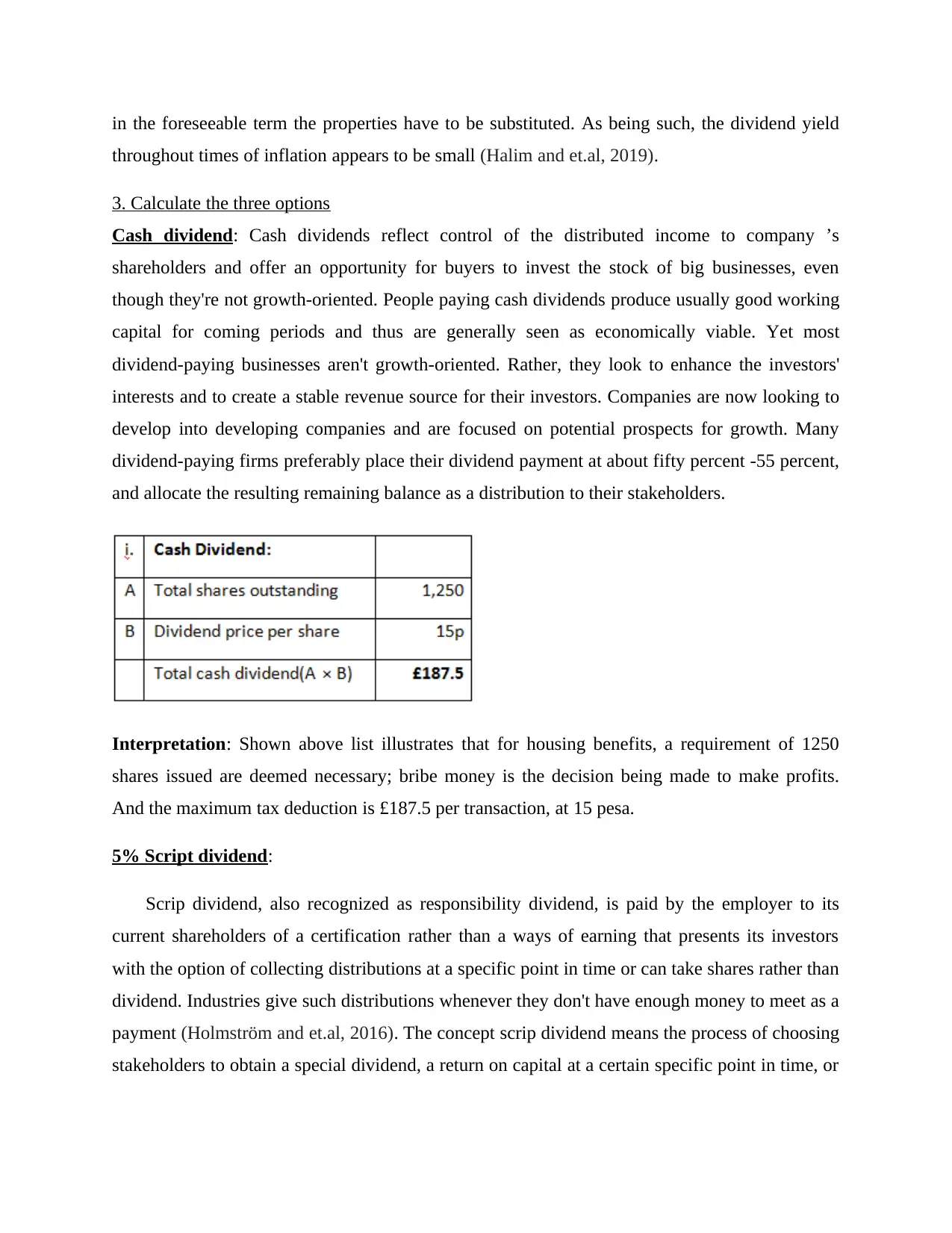

5% Script dividend:

Scrip dividend, also recognized as responsibility dividend, is paid by the employer to its

current shareholders of a certification rather than a ways of earning that presents its investors

with the option of collecting distributions at a specific point in time or can take shares rather than

dividend. Industries give such distributions whenever they don't have enough money to meet as a

payment (Holmström and et.al, 2016). The concept scrip dividend means the process of choosing

stakeholders to obtain a special dividend, a return on capital at a certain specific point in time, or

throughout times of inflation appears to be small (Halim and et.al, 2019).

3. Calculate the three options

Cash dividend: Cash dividends reflect control of the distributed income to company ’s

shareholders and offer an opportunity for buyers to invest the stock of big businesses, even

though they're not growth-oriented. People paying cash dividends produce usually good working

capital for coming periods and thus are generally seen as economically viable. Yet most

dividend-paying businesses aren't growth-oriented. Rather, they look to enhance the investors'

interests and to create a stable revenue source for their investors. Companies are now looking to

develop into developing companies and are focused on potential prospects for growth. Many

dividend-paying firms preferably place their dividend payment at about fifty percent -55 percent,

and allocate the resulting remaining balance as a distribution to their stakeholders.

Interpretation: Shown above list illustrates that for housing benefits, a requirement of 1250

shares issued are deemed necessary; bribe money is the decision being made to make profits.

And the maximum tax deduction is £187.5 per transaction, at 15 pesa.

5% Script dividend:

Scrip dividend, also recognized as responsibility dividend, is paid by the employer to its

current shareholders of a certification rather than a ways of earning that presents its investors

with the option of collecting distributions at a specific point in time or can take shares rather than

dividend. Industries give such distributions whenever they don't have enough money to meet as a

payment (Holmström and et.al, 2016). The concept scrip dividend means the process of choosing

stakeholders to obtain a special dividend, a return on capital at a certain specific point in time, or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

common shares. These help investors to change the amount of their assets while risking any

charges whenever a government announces cash bonuses.

Interpretation: Premised on the said calculation, actual shares of the company are estimated to

be 1250 while 5 per cent are derived from other new deposits as were often pending revenue, and

this would be 62.5. The expenditure per unit is assessed at £270 and the maximum value of the

owner of the business being received new offers is £270.

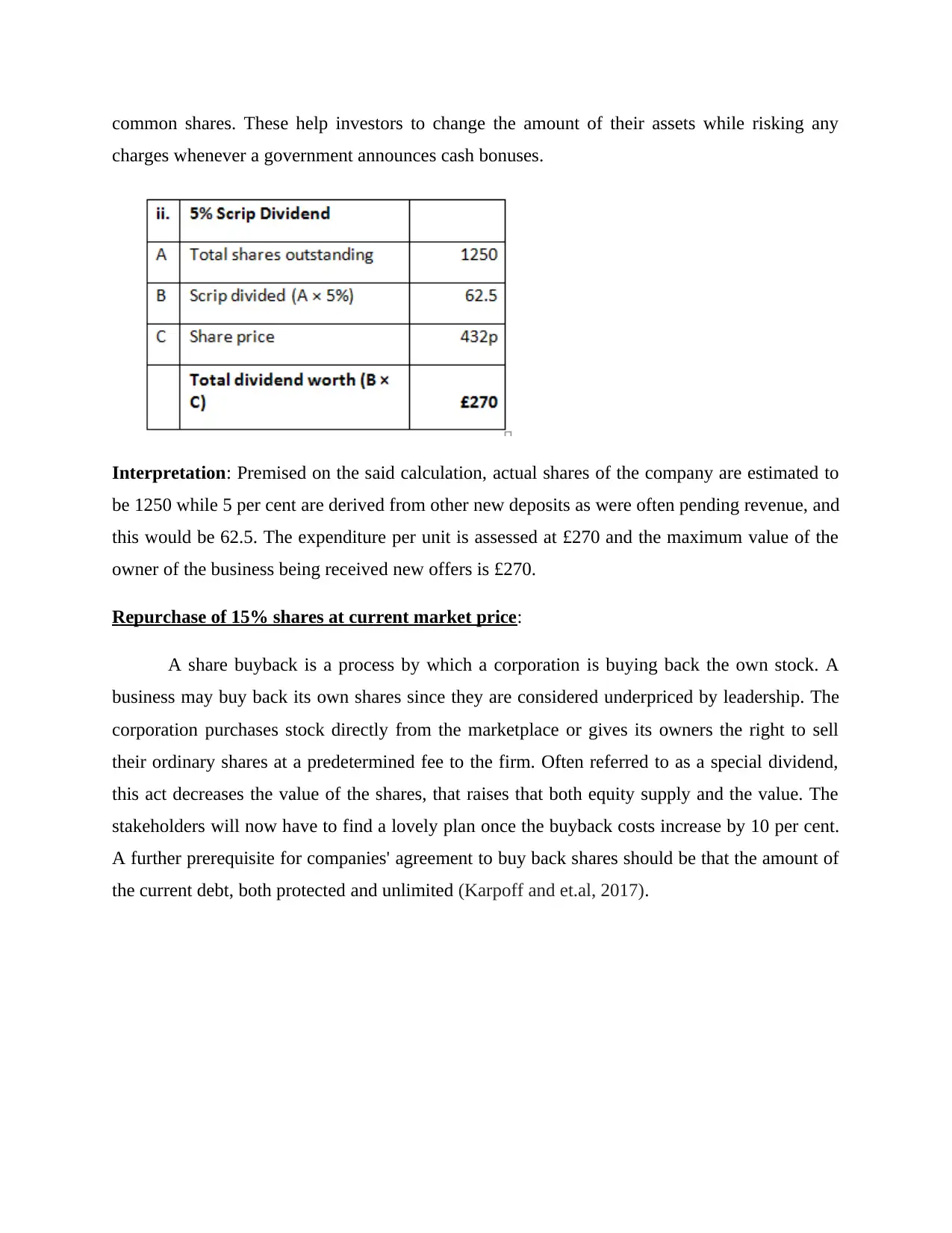

Repurchase of 15% shares at current market price:

A share buyback is a process by which a corporation is buying back the own stock. A

business may buy back its own shares since they are considered underpriced by leadership. The

corporation purchases stock directly from the marketplace or gives its owners the right to sell

their ordinary shares at a predetermined fee to the firm. Often referred to as a special dividend,

this act decreases the value of the shares, that raises that both equity supply and the value. The

stakeholders will now have to find a lovely plan once the buyback costs increase by 10 per cent.

A further prerequisite for companies' agreement to buy back shares should be that the amount of

the current debt, both protected and unlimited (Karpoff and et.al, 2017).

charges whenever a government announces cash bonuses.

Interpretation: Premised on the said calculation, actual shares of the company are estimated to

be 1250 while 5 per cent are derived from other new deposits as were often pending revenue, and

this would be 62.5. The expenditure per unit is assessed at £270 and the maximum value of the

owner of the business being received new offers is £270.

Repurchase of 15% shares at current market price:

A share buyback is a process by which a corporation is buying back the own stock. A

business may buy back its own shares since they are considered underpriced by leadership. The

corporation purchases stock directly from the marketplace or gives its owners the right to sell

their ordinary shares at a predetermined fee to the firm. Often referred to as a special dividend,

this act decreases the value of the shares, that raises that both equity supply and the value. The

stakeholders will now have to find a lovely plan once the buyback costs increase by 10 per cent.

A further prerequisite for companies' agreement to buy back shares should be that the amount of

the current debt, both protected and unlimited (Karpoff and et.al, 2017).

Interpretation: There are 1250 existing options where only the prevailing purchase price pays a

fixed at a rate of 15 per cent, which are 187.5. The deal cost for the agency is 50p, and the

biggest cost for the enterprise is 432p. Then the relationship between the two might effectively

be 382p and is appealing to creditors. Squizeco buys back the deal and reveals that it would be

established as inventory, a measure made by the directors to communicate.

4. Critically evaluate how companies make their decisions which affects the investment

opportunities

Return on investment: The consequence on sustainability is one of the apparent factors

influencing purchasing decisions. Developers can quantify this in a variety of different ways but

sometimes the easiest method is to calculate a financial return. The value of the land is the

percentage gain and everything to lose by doing an operation

Effect on resources: Remember also the cumulative impact on staff in advertising, human

resources, accounting, development and systems engineering when measuring income from a

sound effect. When producing a specific device prevents employees from other operations, they

might be missing other opportunities for investors. If overburdened workers will start to lose top

personnel for making and selling products (Li and et.al, 2016).

fixed at a rate of 15 per cent, which are 187.5. The deal cost for the agency is 50p, and the

biggest cost for the enterprise is 432p. Then the relationship between the two might effectively

be 382p and is appealing to creditors. Squizeco buys back the deal and reveals that it would be

established as inventory, a measure made by the directors to communicate.

4. Critically evaluate how companies make their decisions which affects the investment

opportunities

Return on investment: The consequence on sustainability is one of the apparent factors

influencing purchasing decisions. Developers can quantify this in a variety of different ways but

sometimes the easiest method is to calculate a financial return. The value of the land is the

percentage gain and everything to lose by doing an operation

Effect on resources: Remember also the cumulative impact on staff in advertising, human

resources, accounting, development and systems engineering when measuring income from a

sound effect. When producing a specific device prevents employees from other operations, they

might be missing other opportunities for investors. If overburdened workers will start to lose top

personnel for making and selling products (Li and et.al, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 3

Description of all the investment appraisal techniques

The payback period: Whenever a company is able to fund the venture or choose the best

options for organization improvement, and can be used to assess the time that the task will take

to reclaim the initial wealth. In other phrases, it could still be described as the period of time an

undertaking could needed to complete the threshold of breaking quite that is no benefit and no

expense. It is one of the successful budgeting methods which allow all the companies'

administrators identify the best approach for the company. The organizations will determine,

with both the aid of it, whether to consider investing in the venture or otherwise. If the timeframe

is large, the alternative should not be specified and when it is low, it really should be chosen

since this entire construction value can be restored in a short amount of time (Nollet, Filis and

Mitrokostas, 2016).

Payback period = Initial Investment / Cash Inflow

= £ 275,000 / £ 85,000

= 3.79 years

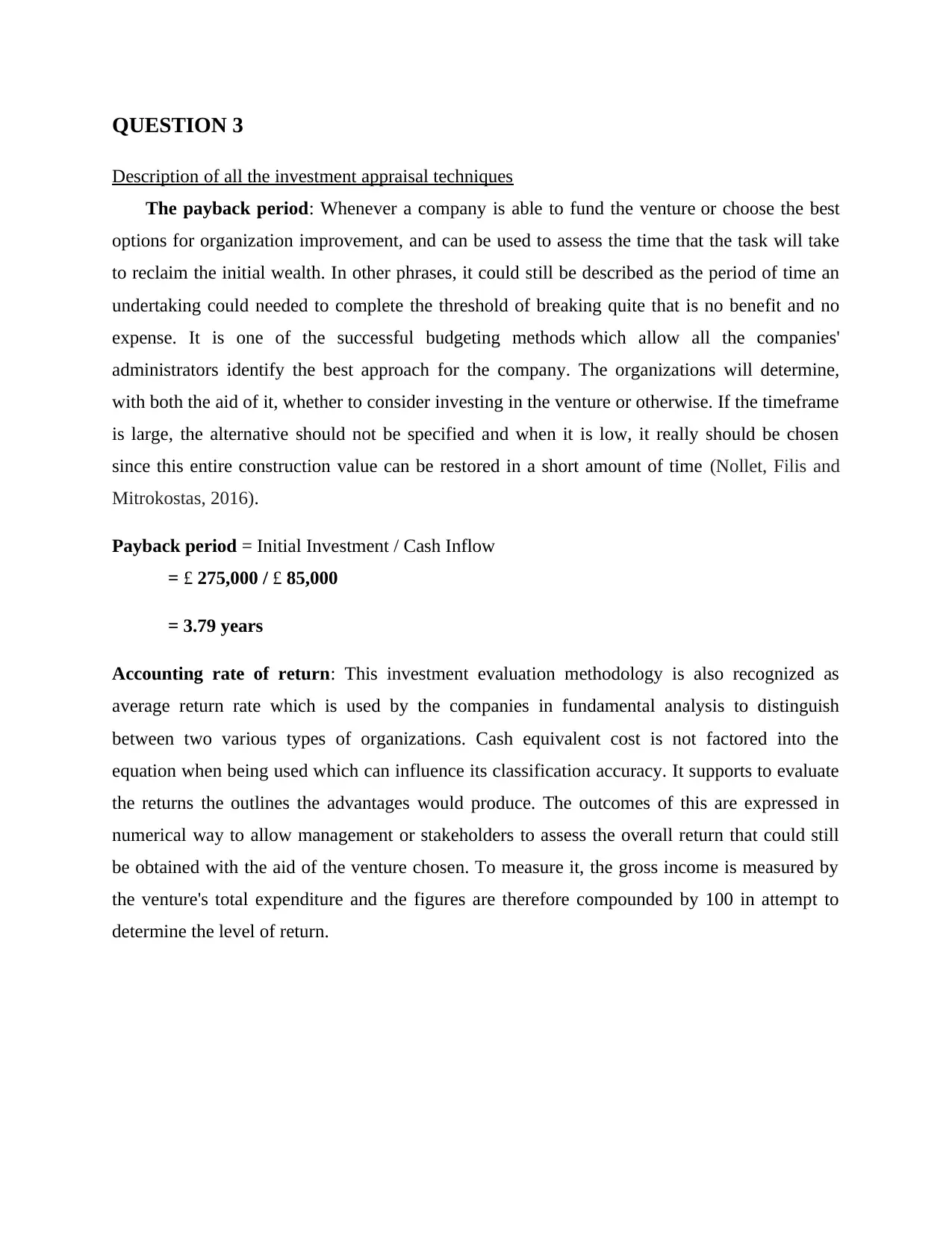

Accounting rate of return: This investment evaluation methodology is also recognized as

average return rate which is used by the companies in fundamental analysis to distinguish

between two various types of organizations. Cash equivalent cost is not factored into the

equation when being used which can influence its classification accuracy. It supports to evaluate

the returns the outlines the advantages would produce. The outcomes of this are expressed in

numerical way to allow management or stakeholders to assess the overall return that could still

be obtained with the aid of the venture chosen. To measure it, the gross income is measured by

the venture's total expenditure and the figures are therefore compounded by 100 in attempt to

determine the level of return.

Description of all the investment appraisal techniques

The payback period: Whenever a company is able to fund the venture or choose the best

options for organization improvement, and can be used to assess the time that the task will take

to reclaim the initial wealth. In other phrases, it could still be described as the period of time an

undertaking could needed to complete the threshold of breaking quite that is no benefit and no

expense. It is one of the successful budgeting methods which allow all the companies'

administrators identify the best approach for the company. The organizations will determine,

with both the aid of it, whether to consider investing in the venture or otherwise. If the timeframe

is large, the alternative should not be specified and when it is low, it really should be chosen

since this entire construction value can be restored in a short amount of time (Nollet, Filis and

Mitrokostas, 2016).

Payback period = Initial Investment / Cash Inflow

= £ 275,000 / £ 85,000

= 3.79 years

Accounting rate of return: This investment evaluation methodology is also recognized as

average return rate which is used by the companies in fundamental analysis to distinguish

between two various types of organizations. Cash equivalent cost is not factored into the

equation when being used which can influence its classification accuracy. It supports to evaluate

the returns the outlines the advantages would produce. The outcomes of this are expressed in

numerical way to allow management or stakeholders to assess the overall return that could still

be obtained with the aid of the venture chosen. To measure it, the gross income is measured by

the venture's total expenditure and the figures are therefore compounded by 100 in attempt to

determine the level of return.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Rate of Return = £ 33,541.67 / £ 275,000 * 100

= 12.19 %

Working Notes:

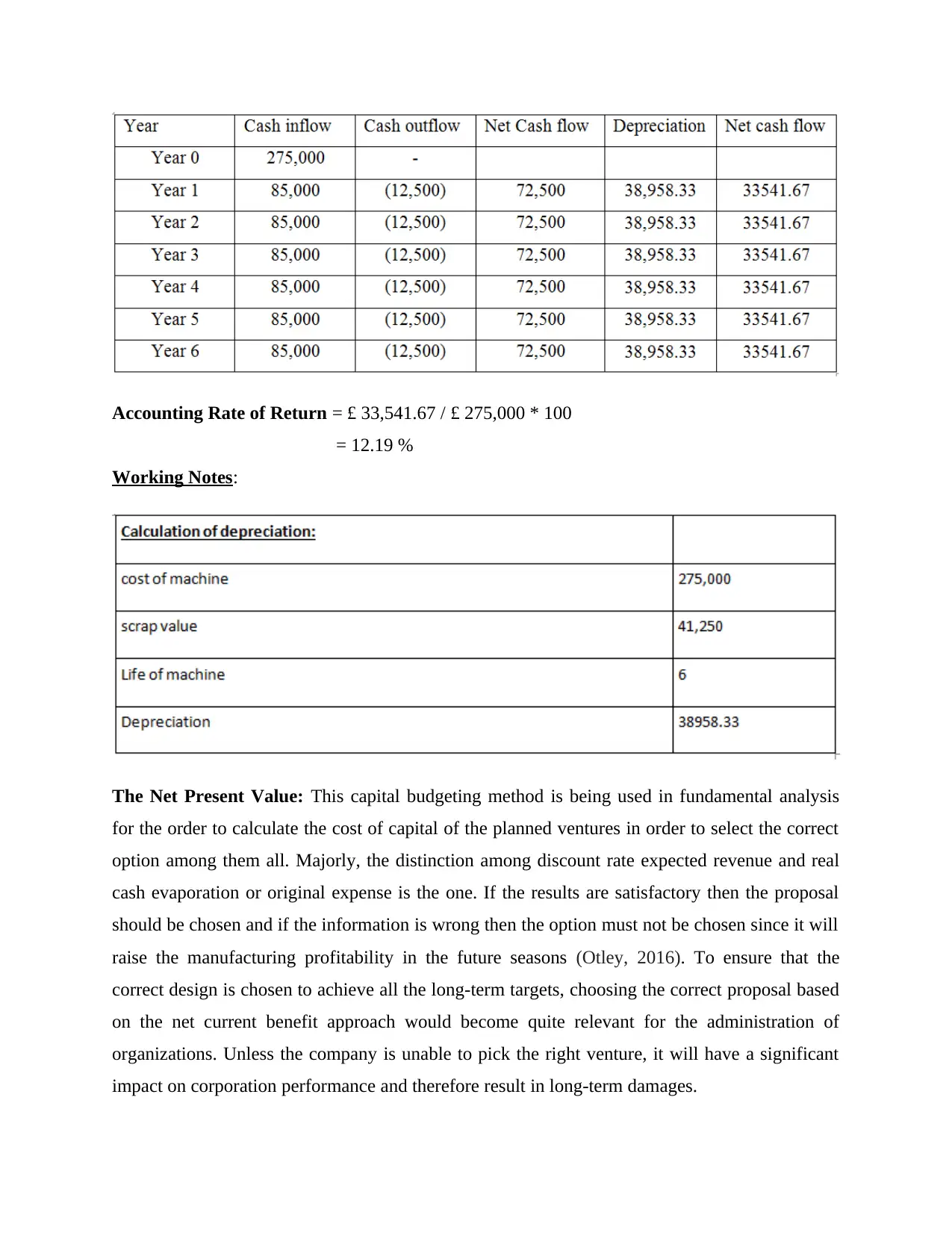

The Net Present Value: This capital budgeting method is being used in fundamental analysis

for the order to calculate the cost of capital of the planned ventures in order to select the correct

option among them all. Majorly, the distinction among discount rate expected revenue and real

cash evaporation or original expense is the one. If the results are satisfactory then the proposal

should be chosen and if the information is wrong then the option must not be chosen since it will

raise the manufacturing profitability in the future seasons (Otley, 2016). To ensure that the

correct design is chosen to achieve all the long-term targets, choosing the correct proposal based

on the net current benefit approach would become quite relevant for the administration of

organizations. Unless the company is unable to pick the right venture, it will have a significant

impact on corporation performance and therefore result in long-term damages.

= 12.19 %

Working Notes:

The Net Present Value: This capital budgeting method is being used in fundamental analysis

for the order to calculate the cost of capital of the planned ventures in order to select the correct

option among them all. Majorly, the distinction among discount rate expected revenue and real

cash evaporation or original expense is the one. If the results are satisfactory then the proposal

should be chosen and if the information is wrong then the option must not be chosen since it will

raise the manufacturing profitability in the future seasons (Otley, 2016). To ensure that the

correct design is chosen to achieve all the long-term targets, choosing the correct proposal based

on the net current benefit approach would become quite relevant for the administration of

organizations. Unless the company is unable to pick the right venture, it will have a significant

impact on corporation performance and therefore result in long-term damages.

The internal rate of return: This is primarily related to the sustainability of the projects in order

to make the best plans for the future that also affect the economy. In the use of net present value

it is densely packed because then reliable results can be produced. It is a form of present value

that is used to allow the total value of the cash receipts equal to 0 from either a particular

variation or ultimately pay. In other words, this methodology of investment evaluation is a

calculation of an investment portfolio anticipated rate of return. This is the calculation of the

potential annualized average that could be created as additional income on the venture chosen by

the client.

PV @ 12 %

to make the best plans for the future that also affect the economy. In the use of net present value

it is densely packed because then reliable results can be produced. It is a form of present value

that is used to allow the total value of the cash receipts equal to 0 from either a particular

variation or ultimately pay. In other words, this methodology of investment evaluation is a

calculation of an investment portfolio anticipated rate of return. This is the calculation of the

potential annualized average that could be created as additional income on the venture chosen by

the client.

PV @ 12 %

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.