Financial Management Report: Dividend Policy and Appraisal

VerifiedAdded on 2023/01/09

|14

|3669

|31

Report

AI Summary

This report delves into the realm of financial management, focusing on two key areas: dividend policy and investment appraisal techniques. The first section examines dividend policy, exploring the size of annual dividends distributed to shareholders, practical considerations in dividend decisions, and the calculation and evaluation of different dividend options, including cash dividends, scrip dividends, and share repurchases. The second section concentrates on investment appraisal techniques, calculating and critically evaluating methods such as payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR). The report analyzes the benefits and limitations of each technique, providing a comprehensive understanding of financial decision-making processes. The assignment uses Lovewell Limited as a case study to apply these concepts, assessing the potential purchase of new machinery and making informed financial recommendations. The conclusion summarizes the findings, highlighting the importance of these techniques for sound financial management.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1 – Dividend Policy..........................................................................................................1

1. Size of annual dividend that distributed to shareholders.........................................................1

2. Practice issues..........................................................................................................................2

3. Calculate three options............................................................................................................3

4. Critically evaluate the company’s decisions............................................................................5

Question 3 – Investment Appraisal Techniques..............................................................................5

1. Calculate the following investment appraisal techniques........................................................5

2. Critically evaluate the benefits and limitation of several investment appraisal techniques....8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

MAIN BODY..................................................................................................................................1

Question 1 – Dividend Policy..........................................................................................................1

1. Size of annual dividend that distributed to shareholders.........................................................1

2. Practice issues..........................................................................................................................2

3. Calculate three options............................................................................................................3

4. Critically evaluate the company’s decisions............................................................................5

Question 3 – Investment Appraisal Techniques..............................................................................5

1. Calculate the following investment appraisal techniques........................................................5

2. Critically evaluate the benefits and limitation of several investment appraisal techniques....8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial management is described as working with and evaluating money and finances to

support or make financial decisions for an individual or a company. A definition of financial

reporting is the function done for a firm by an accounting team (Alkaraan, 2020). It includes

knowing and adequately managing, allocating and accessing the resources and liabilities of a

business and management of financial finance products such as spending, sales, payable and

receivables reports, cash balance, and productivity. This assessment based on two different

questions where first one is about dividend policy which includes several topics such as size of

annual dividend which return to its shareholders and some practice issues which required

considering before making dividend payment decisions. In addition, it covers calculation of three

options and in the last critically evaluate the company’s decisions. Second question based on

investment appraisal techniques which help the organization to identify that which proposal is

beneficial for them or they should invent in it or not.

MAIN BODY

Question 1 – Dividend Policy

1. Size of annual dividend that distributed to shareholders

Dividend is simply amount or proportion of a firm's profits, benefit throughout the

assessment and appointment of board members; it is declared and paid as a ratio of par shares or

per securities. In fact, dividend is a percentage of the surplus that exists after adequate allowance

for various forms of utilities and taxes etc. was already rendered after all investment has been

deducted in overall income (Anthony, 2019). Members have such responsibility to make that

benefit, but they cannot agree to the immediate sale. If the corporation needs income so the

organization will keep the full share of the sales even without paying any amount of dividend.

Therefore, in case the overall income is expected to have been in the form of common unit or

surplus, no dividend is recorded. Take into account the normal two items mentioned below when

focusing on dividends paid, owners will:

Fair consideration:

Managers need a realistic estimation of the degree at which shareholders plan to benefit

from capital and take chances in return. If this is not done, it will also be difficult to maintain the

1

Financial management is described as working with and evaluating money and finances to

support or make financial decisions for an individual or a company. A definition of financial

reporting is the function done for a firm by an accounting team (Alkaraan, 2020). It includes

knowing and adequately managing, allocating and accessing the resources and liabilities of a

business and management of financial finance products such as spending, sales, payable and

receivables reports, cash balance, and productivity. This assessment based on two different

questions where first one is about dividend policy which includes several topics such as size of

annual dividend which return to its shareholders and some practice issues which required

considering before making dividend payment decisions. In addition, it covers calculation of three

options and in the last critically evaluate the company’s decisions. Second question based on

investment appraisal techniques which help the organization to identify that which proposal is

beneficial for them or they should invent in it or not.

MAIN BODY

Question 1 – Dividend Policy

1. Size of annual dividend that distributed to shareholders

Dividend is simply amount or proportion of a firm's profits, benefit throughout the

assessment and appointment of board members; it is declared and paid as a ratio of par shares or

per securities. In fact, dividend is a percentage of the surplus that exists after adequate allowance

for various forms of utilities and taxes etc. was already rendered after all investment has been

deducted in overall income (Anthony, 2019). Members have such responsibility to make that

benefit, but they cannot agree to the immediate sale. If the corporation needs income so the

organization will keep the full share of the sales even without paying any amount of dividend.

Therefore, in case the overall income is expected to have been in the form of common unit or

surplus, no dividend is recorded. Take into account the normal two items mentioned below when

focusing on dividends paid, owners will:

Fair consideration:

Managers need a realistic estimation of the degree at which shareholders plan to benefit

from capital and take chances in return. If this is not done, it will also be difficult to maintain the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

investors completely happy as this can have a detrimental impact on the group's trading returns

in goodwill securities.

Requirement of company:

Managing the long term financial role is the key responsibility of managers, especially as

members are required to make other sacrifices to do so. Therefore, it is extremely important for

the investor to really be able to identify just how much extra financing the company requires

growing and succeeding.

Factors affecting dividend distribution decisions:

Legal requirement: A corporation has no moral obligation to pay dividends. There are,

however, other law-imposed provisions regarding how dividends are allocated. There are

essentially three laws pertaining to dividend payments. They are the law of net income,

the law of capital loss and the rule of insolvency.

Liquidity position of the firm: Payment of dividend is influenced by the liquidity status

of the company (Factors affecting dividend distribution strategy, 2019). Despite ample

retained profits, if the profits are not kept in cash the company cannot be capable of

paying cash dividend.

Need of repayment: A business is using multiple forms of debt funding to fulfill its

financing requirements (Ayodele, 2019). At maturity, the obligation must be repaid. If the

company needs to maintain its earnings for debt servicing purposes, the ability to pay

dividends reduces.

Expected rate of return: When the anticipated rate of return mostly on capital funding is

comparatively higher for a company, the firm tends to hold profits for reinvestment

instead of pay cash dividends.

Stability of earning: If a corporation has fairly predictable profits, it is much more

probable than a company with comparatively fluctuating profits to pay relatively larger

dividends.

2. Practice issues

It's not just the factors that affect directors' option regarding payment of dividend. The

company looks at market problems when pursuing benefit policy. A part of such common-sense

problems is mentioned below:

2

in goodwill securities.

Requirement of company:

Managing the long term financial role is the key responsibility of managers, especially as

members are required to make other sacrifices to do so. Therefore, it is extremely important for

the investor to really be able to identify just how much extra financing the company requires

growing and succeeding.

Factors affecting dividend distribution decisions:

Legal requirement: A corporation has no moral obligation to pay dividends. There are,

however, other law-imposed provisions regarding how dividends are allocated. There are

essentially three laws pertaining to dividend payments. They are the law of net income,

the law of capital loss and the rule of insolvency.

Liquidity position of the firm: Payment of dividend is influenced by the liquidity status

of the company (Factors affecting dividend distribution strategy, 2019). Despite ample

retained profits, if the profits are not kept in cash the company cannot be capable of

paying cash dividend.

Need of repayment: A business is using multiple forms of debt funding to fulfill its

financing requirements (Ayodele, 2019). At maturity, the obligation must be repaid. If the

company needs to maintain its earnings for debt servicing purposes, the ability to pay

dividends reduces.

Expected rate of return: When the anticipated rate of return mostly on capital funding is

comparatively higher for a company, the firm tends to hold profits for reinvestment

instead of pay cash dividends.

Stability of earning: If a corporation has fairly predictable profits, it is much more

probable than a company with comparatively fluctuating profits to pay relatively larger

dividends.

2. Practice issues

It's not just the factors that affect directors' option regarding payment of dividend. The

company looks at market problems when pursuing benefit policy. A part of such common-sense

problems is mentioned below:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Choice of inventors: The primary concern is investment choice or selection; because

every investor has different preferences and opinions. Often creditors don't worry about money,

they really need to invest these gained rewards to acquire new projects or to grow current

enterprise. As this evolution improves the cost of a proposal just as market cost which increases,

that will benefit the shareholders at the time of selling the proposals.

Alternatives: Fewer than two systems, corporate leaders will generate profits such as cash

income and benefit break. The organization's main issue is to choose which alternative to meet

investors should be picked to satisfying its choices between profit and profit from money.

Customer’s desire: it is impossible for a company to determine the expectations of

consumers for income esteem; shareholders will presume spending more than expected if the

entity does not focus on growth and will expect the expense of the bid to decrease later.

Guidelines Act: The regulatory body has agreed with a number of guidelines for the

entity, after which the corporation will have to spend. For example, it allows the company to

retain a certain amount of revenue for income.

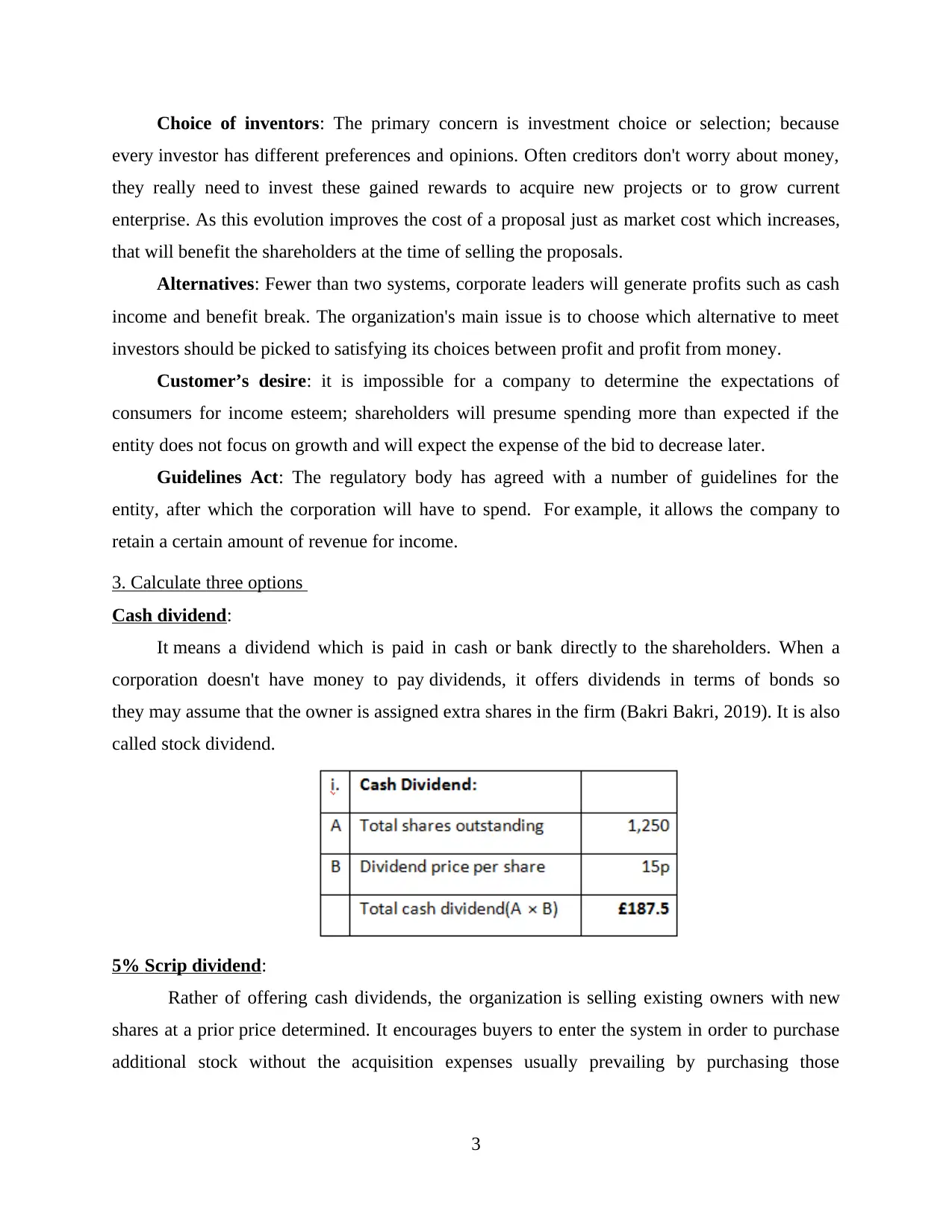

3. Calculate three options

Cash dividend:

It means a dividend which is paid in cash or bank directly to the shareholders. When a

corporation doesn't have money to pay dividends, it offers dividends in terms of bonds so

they may assume that the owner is assigned extra shares in the firm (Bakri Bakri, 2019). It is also

called stock dividend.

5% Scrip dividend:

Rather of offering cash dividends, the organization is selling existing owners with new

shares at a prior price determined. It encourages buyers to enter the system in order to purchase

additional stock without the acquisition expenses usually prevailing by purchasing those

3

every investor has different preferences and opinions. Often creditors don't worry about money,

they really need to invest these gained rewards to acquire new projects or to grow current

enterprise. As this evolution improves the cost of a proposal just as market cost which increases,

that will benefit the shareholders at the time of selling the proposals.

Alternatives: Fewer than two systems, corporate leaders will generate profits such as cash

income and benefit break. The organization's main issue is to choose which alternative to meet

investors should be picked to satisfying its choices between profit and profit from money.

Customer’s desire: it is impossible for a company to determine the expectations of

consumers for income esteem; shareholders will presume spending more than expected if the

entity does not focus on growth and will expect the expense of the bid to decrease later.

Guidelines Act: The regulatory body has agreed with a number of guidelines for the

entity, after which the corporation will have to spend. For example, it allows the company to

retain a certain amount of revenue for income.

3. Calculate three options

Cash dividend:

It means a dividend which is paid in cash or bank directly to the shareholders. When a

corporation doesn't have money to pay dividends, it offers dividends in terms of bonds so

they may assume that the owner is assigned extra shares in the firm (Bakri Bakri, 2019). It is also

called stock dividend.

5% Scrip dividend:

Rather of offering cash dividends, the organization is selling existing owners with new

shares at a prior price determined. It encourages buyers to enter the system in order to purchase

additional stock without the acquisition expenses usually prevailing by purchasing those

3

securities on the market. Money savings are the main reason for the firm's payment of scrip

dividends. It is one of the effective strategy which should be used by the organizations.

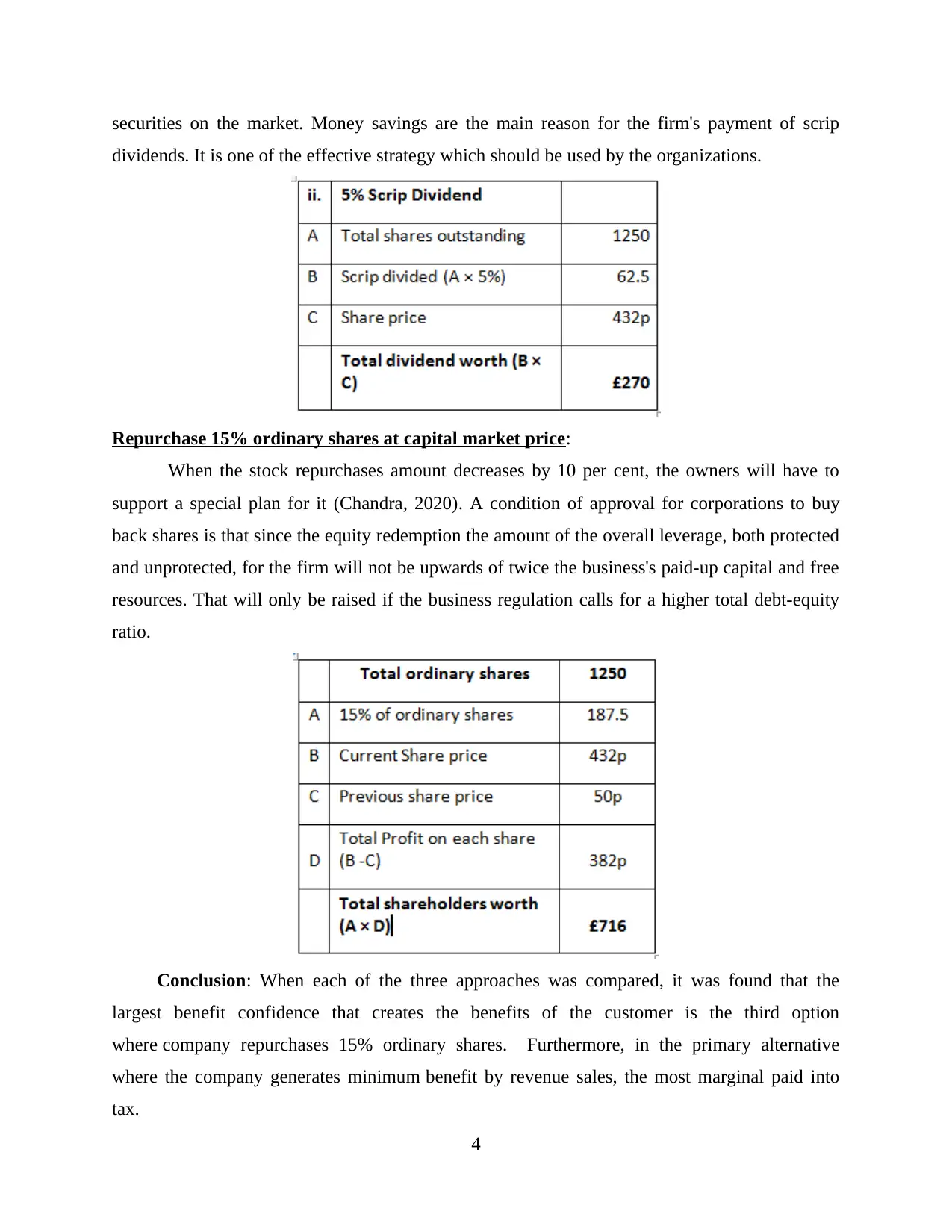

Repurchase 15% ordinary shares at capital market price:

When the stock repurchases amount decreases by 10 per cent, the owners will have to

support a special plan for it (Chandra, 2020). A condition of approval for corporations to buy

back shares is that since the equity redemption the amount of the overall leverage, both protected

and unprotected, for the firm will not be upwards of twice the business's paid-up capital and free

resources. That will only be raised if the business regulation calls for a higher total debt-equity

ratio.

Conclusion: When each of the three approaches was compared, it was found that the

largest benefit confidence that creates the benefits of the customer is the third option

where company repurchases 15% ordinary shares. Furthermore, in the primary alternative

where the company generates minimum benefit by revenue sales, the most marginal paid into

tax.

4

dividends. It is one of the effective strategy which should be used by the organizations.

Repurchase 15% ordinary shares at capital market price:

When the stock repurchases amount decreases by 10 per cent, the owners will have to

support a special plan for it (Chandra, 2020). A condition of approval for corporations to buy

back shares is that since the equity redemption the amount of the overall leverage, both protected

and unprotected, for the firm will not be upwards of twice the business's paid-up capital and free

resources. That will only be raised if the business regulation calls for a higher total debt-equity

ratio.

Conclusion: When each of the three approaches was compared, it was found that the

largest benefit confidence that creates the benefits of the customer is the third option

where company repurchases 15% ordinary shares. Furthermore, in the primary alternative

where the company generates minimum benefit by revenue sales, the most marginal paid into

tax.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Critically evaluate the company’s decisions

The biggest influence on the decision would be to make a option to collect investment funds

with an investment of £70million (Laitinen, 2019). For the owner of the company, three options

are available; funding by contract, expanding properties by utilizing stores and surplus through

issue of interest shares. All three options have the massive disservice and points of concern.

Using a combination of each of such strategies or it can be predicted. For example; the company

should split the requirement of the business into three amounts, e.g. 30 percent through duty, 60

percent through issue of interest shares and 10 percent through store keeping. If a problem of

deals should appear, the company has three options available:

Right distribution of shares to equity owners.

Grant preferred shares with fixed dividend payout rate and;

To sell ordinary shares at a cheaper selling level.

Question 3 – Investment Appraisal Techniques

This segment is focused on applying various methodologies of investment appraisal to

decide the utility of new machinery that Lovewell Limited should purchase or not. Further

calculation mentioned below:

1. Calculate the following investment appraisal techniques

Payback Period:

Formula:

Payback period = Initial investment / cash flows

Given information:

Initial investment = £275000

Cash inflow = £85000

Less: Cash outflow = £12500

Cash flow = £72500

Calculate:

Payback period = 275000 / 72500

= 3.79 years

5

The biggest influence on the decision would be to make a option to collect investment funds

with an investment of £70million (Laitinen, 2019). For the owner of the company, three options

are available; funding by contract, expanding properties by utilizing stores and surplus through

issue of interest shares. All three options have the massive disservice and points of concern.

Using a combination of each of such strategies or it can be predicted. For example; the company

should split the requirement of the business into three amounts, e.g. 30 percent through duty, 60

percent through issue of interest shares and 10 percent through store keeping. If a problem of

deals should appear, the company has three options available:

Right distribution of shares to equity owners.

Grant preferred shares with fixed dividend payout rate and;

To sell ordinary shares at a cheaper selling level.

Question 3 – Investment Appraisal Techniques

This segment is focused on applying various methodologies of investment appraisal to

decide the utility of new machinery that Lovewell Limited should purchase or not. Further

calculation mentioned below:

1. Calculate the following investment appraisal techniques

Payback Period:

Formula:

Payback period = Initial investment / cash flows

Given information:

Initial investment = £275000

Cash inflow = £85000

Less: Cash outflow = £12500

Cash flow = £72500

Calculate:

Payback period = 275000 / 72500

= 3.79 years

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

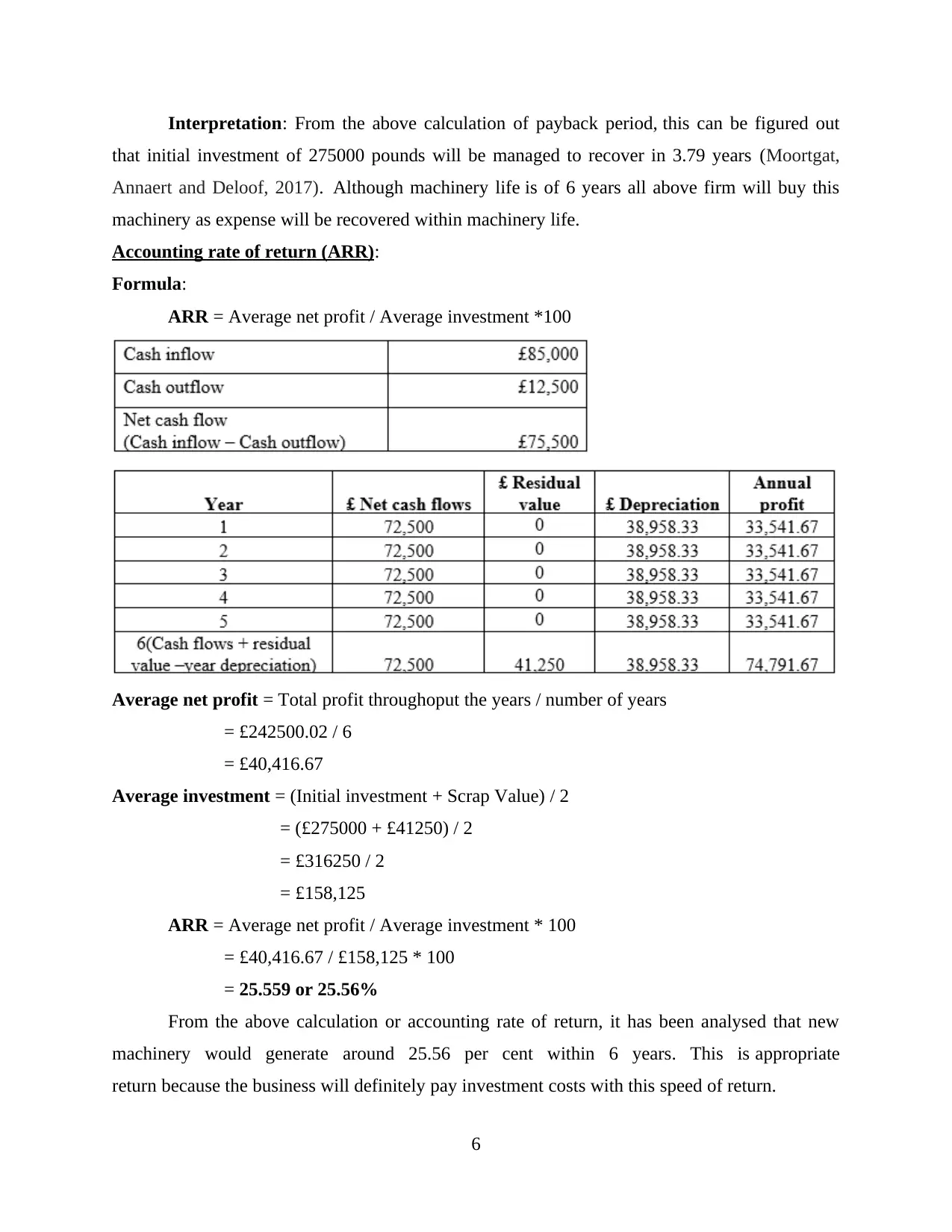

Interpretation: From the above calculation of payback period, this can be figured out

that initial investment of 275000 pounds will be managed to recover in 3.79 years (Moortgat,

Annaert and Deloof, 2017). Although machinery life is of 6 years all above firm will buy this

machinery as expense will be recovered within machinery life.

Accounting rate of return (ARR):

Formula:

ARR = Average net profit / Average investment *100

Average net profit = Total profit throughoput the years / number of years

= £242500.02 / 6

= £40,416.67

Average investment = (Initial investment + Scrap Value) / 2

= (£275000 + £41250) / 2

= £316250 / 2

= £158,125

ARR = Average net profit / Average investment * 100

= £40,416.67 / £158,125 * 100

= 25.559 or 25.56%

From the above calculation or accounting rate of return, it has been analysed that new

machinery would generate around 25.56 per cent within 6 years. This is appropriate

return because the business will definitely pay investment costs with this speed of return.

6

that initial investment of 275000 pounds will be managed to recover in 3.79 years (Moortgat,

Annaert and Deloof, 2017). Although machinery life is of 6 years all above firm will buy this

machinery as expense will be recovered within machinery life.

Accounting rate of return (ARR):

Formula:

ARR = Average net profit / Average investment *100

Average net profit = Total profit throughoput the years / number of years

= £242500.02 / 6

= £40,416.67

Average investment = (Initial investment + Scrap Value) / 2

= (£275000 + £41250) / 2

= £316250 / 2

= £158,125

ARR = Average net profit / Average investment * 100

= £40,416.67 / £158,125 * 100

= 25.559 or 25.56%

From the above calculation or accounting rate of return, it has been analysed that new

machinery would generate around 25.56 per cent within 6 years. This is appropriate

return because the business will definitely pay investment costs with this speed of return.

6

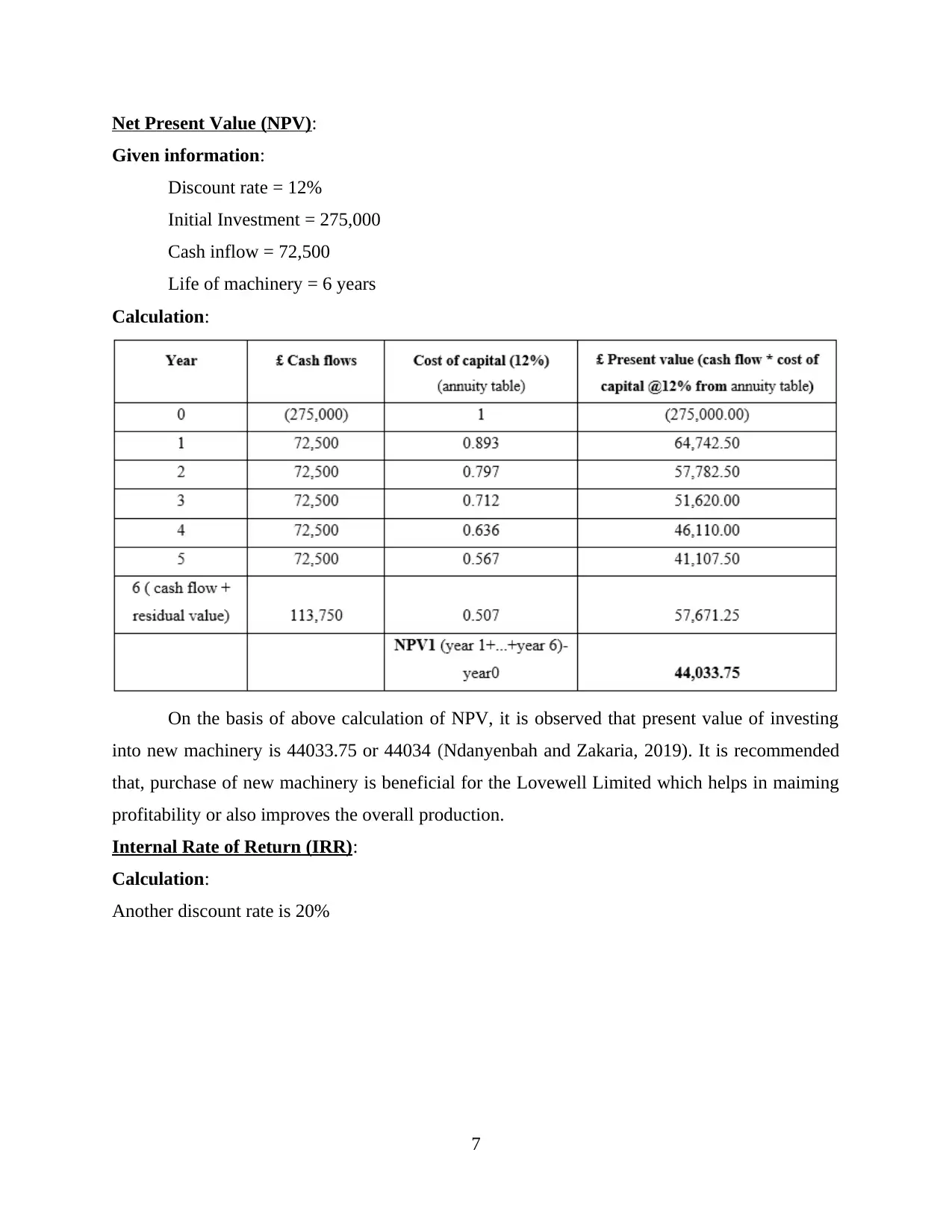

Net Present Value (NPV):

Given information:

Discount rate = 12%

Initial Investment = 275,000

Cash inflow = 72,500

Life of machinery = 6 years

Calculation:

On the basis of above calculation of NPV, it is observed that present value of investing

into new machinery is 44033.75 or 44034 (Ndanyenbah and Zakaria, 2019). It is recommended

that, purchase of new machinery is beneficial for the Lovewell Limited which helps in maiming

profitability or also improves the overall production.

Internal Rate of Return (IRR):

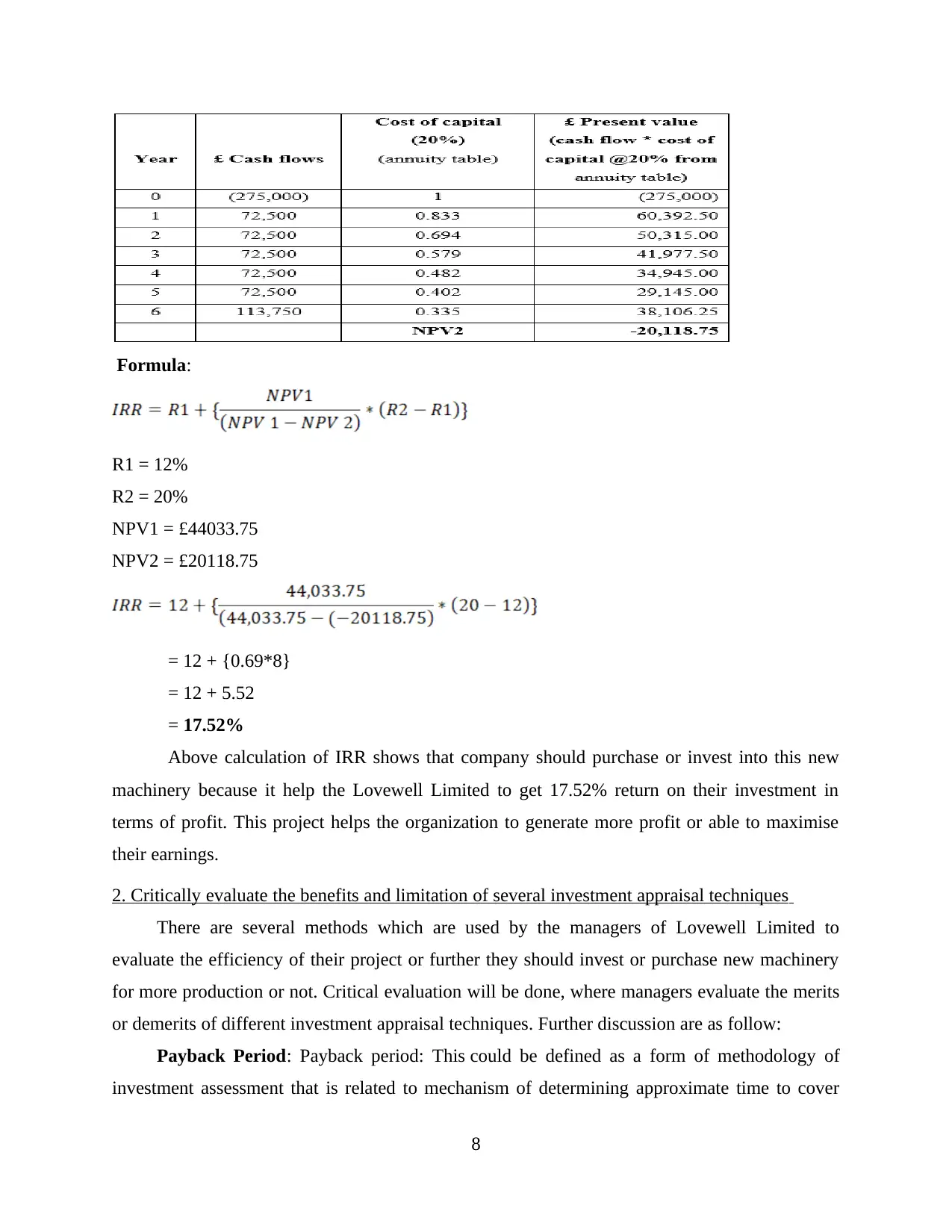

Calculation:

Another discount rate is 20%

7

Given information:

Discount rate = 12%

Initial Investment = 275,000

Cash inflow = 72,500

Life of machinery = 6 years

Calculation:

On the basis of above calculation of NPV, it is observed that present value of investing

into new machinery is 44033.75 or 44034 (Ndanyenbah and Zakaria, 2019). It is recommended

that, purchase of new machinery is beneficial for the Lovewell Limited which helps in maiming

profitability or also improves the overall production.

Internal Rate of Return (IRR):

Calculation:

Another discount rate is 20%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Formula:

R1 = 12%

R2 = 20%

NPV1 = £44033.75

NPV2 = £20118.75

= 12 + {0.69*8}

= 12 + 5.52

= 17.52%

Above calculation of IRR shows that company should purchase or invest into this new

machinery because it help the Lovewell Limited to get 17.52% return on their investment in

terms of profit. This project helps the organization to generate more profit or able to maximise

their earnings.

2. Critically evaluate the benefits and limitation of several investment appraisal techniques

There are several methods which are used by the managers of Lovewell Limited to

evaluate the efficiency of their project or further they should invest or purchase new machinery

for more production or not. Critical evaluation will be done, where managers evaluate the merits

or demerits of different investment appraisal techniques. Further discussion are as follow:

Payback Period: Payback period: This could be defined as a form of methodology of

investment assessment that is related to mechanism of determining approximate time to cover

8

R1 = 12%

R2 = 20%

NPV1 = £44033.75

NPV2 = £20118.75

= 12 + {0.69*8}

= 12 + 5.52

= 17.52%

Above calculation of IRR shows that company should purchase or invest into this new

machinery because it help the Lovewell Limited to get 17.52% return on their investment in

terms of profit. This project helps the organization to generate more profit or able to maximise

their earnings.

2. Critically evaluate the benefits and limitation of several investment appraisal techniques

There are several methods which are used by the managers of Lovewell Limited to

evaluate the efficiency of their project or further they should invest or purchase new machinery

for more production or not. Critical evaluation will be done, where managers evaluate the merits

or demerits of different investment appraisal techniques. Further discussion are as follow:

Payback Period: Payback period: This could be defined as a form of methodology of

investment assessment that is related to mechanism of determining approximate time to cover

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

their total cost of initial investment (Setiawan, Bandi, Phua and Trinugroho, 2016). This

function facilitates the implementation of some project in the organization. As for Lovewell

limited, this method was applied that also claims that total project costs will be recovered in 3.79

years. With the help of evaluating some benefits or limitations, manage is able to get idea that

they should invest in new machinery or not. There are certain advantages and drawbacks which

are discussed below:

Benefits: As stated according to the above discussion, it is simpler to apply this approach

which makes it great for all types of businesses, either small or large. As well as within this

approach, project effectiveness evaluation can be performed in less time and expense. Moreover,

it is used by any employer in an organisation, since this does not required any special experience

and skills in accounting.

Limitation: It has certain demerits that make results less accurate, as factors such as time

value of money are overlooked under this system. Despite of this, depending on generated result

is challenging for users, because time worth of money is among the key considerations to

remember when assessing a project. In this process, cash flows of every years is not included as

cash flows of the remaining years following recovery of investment costs are overlooked.

Accounting rate of return (ARR): It is just another method of investment appraisal

technique. By implementing this strategy, the rate of return company calculated and made their

decision accordingly. Under this process, businesses take appropriate action to purchase or

invest into any project on the basis of determined result. Compared to the approach above, this

also needs little more information to give the final result (Shapiro and Hanouna, 2019). As for

Lovewell Limited, this technique was used to estimate the approximate return that is 25.56

percent. This accounting rate of return effectively contributes to executives in deciding whether

or not they will consider a plan. It has some benefits and limitations which are as follow:

Benefits: This strategy has a variety of benefits which it more effective to use as

accounting profits that are used underneath it while total profit for proposed project are regarded

in several other methods. This factor allows applicability more accurate and convenient. This

approach is very simple to use because this is based on method and it will be calculated by

everyone inside the organization without any specialised information.

Limitations: The ARR approach does not require time value element that is an essential

aspect to consider. This renders decisions less efficient and reliable. Besides this, cash flows

9

function facilitates the implementation of some project in the organization. As for Lovewell

limited, this method was applied that also claims that total project costs will be recovered in 3.79

years. With the help of evaluating some benefits or limitations, manage is able to get idea that

they should invest in new machinery or not. There are certain advantages and drawbacks which

are discussed below:

Benefits: As stated according to the above discussion, it is simpler to apply this approach

which makes it great for all types of businesses, either small or large. As well as within this

approach, project effectiveness evaluation can be performed in less time and expense. Moreover,

it is used by any employer in an organisation, since this does not required any special experience

and skills in accounting.

Limitation: It has certain demerits that make results less accurate, as factors such as time

value of money are overlooked under this system. Despite of this, depending on generated result

is challenging for users, because time worth of money is among the key considerations to

remember when assessing a project. In this process, cash flows of every years is not included as

cash flows of the remaining years following recovery of investment costs are overlooked.

Accounting rate of return (ARR): It is just another method of investment appraisal

technique. By implementing this strategy, the rate of return company calculated and made their

decision accordingly. Under this process, businesses take appropriate action to purchase or

invest into any project on the basis of determined result. Compared to the approach above, this

also needs little more information to give the final result (Shapiro and Hanouna, 2019). As for

Lovewell Limited, this technique was used to estimate the approximate return that is 25.56

percent. This accounting rate of return effectively contributes to executives in deciding whether

or not they will consider a plan. It has some benefits and limitations which are as follow:

Benefits: This strategy has a variety of benefits which it more effective to use as

accounting profits that are used underneath it while total profit for proposed project are regarded

in several other methods. This factor allows applicability more accurate and convenient. This

approach is very simple to use because this is based on method and it will be calculated by

everyone inside the organization without any specialised information.

Limitations: The ARR approach does not require time value element that is an essential

aspect to consider. This renders decisions less efficient and reliable. Besides this, cash flows

9

underneath it is totally neglected which is really not that helpful in terms of a proposal's

computational performance.

Net Present Value (NPV): This type of appraisal technique used to calculate recent value

of a project. Under it, net present value of any proposal is determined by subtracting amount of

initial investment from cash flows of the different time periods. Under it, the net discounted cash

flow valuation is calculated using the expected Present Value (PV) element. The process is

commonly known as NPV (Sinha and Datta, 2020). This approach has been extended in the

sense of the aforementioned business to figure out the net present value of their planned

equipment. Under this approach, higher the NPV project is selected and the lower one rejected

because higher one profit more benefits or profitability to the organization. Many of the benefits

and demerits of this approach are explained in this way below:

Benefits: The main advantage of using this approach is that, it is the method of monitoring

project's current valuation it includes time value of money aspect. It makes it more efficient and

appropriate approach relative to the methods described above, as this aspect has been overlooked

in the above methods. Another major aspect of this approach is that calculating the present value

of the project requires cash flows among all years.

Limitation: It is a difficult to implement making assumptions relating to capital costs. As

well as this presumption, the result makes long-term judgments less accurate and successful. In

relation to this, fixed costs for estimating current project value are not included under it.

Internal Rate of Return (IRR): It could be defined as a form of approach that applies to

the evaluation process of a proposal's rate of return. This technique is found a method that is too

complicated to use because strong accounting information is required. As well as just those

individuals who have adequate knowledge regarding finance will apply this process. With regard

to the above-mentioned business, accountants have applied this approach to learn for the future

about the productivity of new machinery (Zietlow and et.al., 2018). This approach has some

benefits and demerit points which clarified below:

Benefits: The key advantage of this analysis is that it allows accurate outcomes that make it

easy for administrators to take effective action. In particular, all those variables that are

mandatory to move in before assessing a project's success will be included under this method to

evaluate whether project is beneficial or not.

10

computational performance.

Net Present Value (NPV): This type of appraisal technique used to calculate recent value

of a project. Under it, net present value of any proposal is determined by subtracting amount of

initial investment from cash flows of the different time periods. Under it, the net discounted cash

flow valuation is calculated using the expected Present Value (PV) element. The process is

commonly known as NPV (Sinha and Datta, 2020). This approach has been extended in the

sense of the aforementioned business to figure out the net present value of their planned

equipment. Under this approach, higher the NPV project is selected and the lower one rejected

because higher one profit more benefits or profitability to the organization. Many of the benefits

and demerits of this approach are explained in this way below:

Benefits: The main advantage of using this approach is that, it is the method of monitoring

project's current valuation it includes time value of money aspect. It makes it more efficient and

appropriate approach relative to the methods described above, as this aspect has been overlooked

in the above methods. Another major aspect of this approach is that calculating the present value

of the project requires cash flows among all years.

Limitation: It is a difficult to implement making assumptions relating to capital costs. As

well as this presumption, the result makes long-term judgments less accurate and successful. In

relation to this, fixed costs for estimating current project value are not included under it.

Internal Rate of Return (IRR): It could be defined as a form of approach that applies to

the evaluation process of a proposal's rate of return. This technique is found a method that is too

complicated to use because strong accounting information is required. As well as just those

individuals who have adequate knowledge regarding finance will apply this process. With regard

to the above-mentioned business, accountants have applied this approach to learn for the future

about the productivity of new machinery (Zietlow and et.al., 2018). This approach has some

benefits and demerit points which clarified below:

Benefits: The key advantage of this analysis is that it allows accurate outcomes that make it

easy for administrators to take effective action. In particular, all those variables that are

mandatory to move in before assessing a project's success will be included under this method to

evaluate whether project is beneficial or not.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.