A Comprehensive Analysis: ST Engineering Dividend Policies Report

VerifiedAdded on 2023/01/11

|13

|3072

|99

Report

AI Summary

This report provides a detailed analysis of ST Engineering's dividend policies, focusing on the company's dividend payout strategies and their impact on shareholders. It examines the executive summary, which includes an overview of the company's dividend payout in relation to its shareholders, critical analysis of earnings per share, and revenue forecasts for 2019. The report delves into both financial and non-financial aspects influencing dividend payouts, such as innovation, firm size, and legal rules. It discusses key dividend theories like the MM approach, clientele effect, and signaling hypothesis, and provides a revenue forecast based on historical data. The report also offers advice on future dividend payouts, considering dividend yield, and concludes with a comprehensive overview of the company's dividend policies. The analysis includes tables and graphs illustrating sales, revenue, and earnings projections, along with dividend yield variations over the years. The report emphasizes the importance of dividend policies in conveying information about a company's performance and its impact on retained earnings and investor perception.

RUNNING HEAD: DIVIDEND POLICIES 1

UNIVERSITY NAME

STUDENT NAME

COURSE

DATE

UNIVERSITY NAME

STUDENT NAME

COURSE

DATE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DIVIDEND POLICIES 2

EXECUTIVE SUMMARY

The purpose of this report is to analyze the annual reports ST ENGINEERING CO. and examine

the dividends policies adopted by the company in relation to dividend payout to its shareholders.

Earnings per share distributed to shareholders are critically analyzed for previous years, current

year and future projection. The report also make revenue forecast for the company for the next

year that is 2019.critical discussion of its sales volume and net income levels are clearly

highlighted for the previous, current and future. Based on the projection, it is observed that the

sales volume of the company might be to 6.59B in 2019.the net income value also fluctuates

considerably.

Dividend payout does not necessarily indicate good performance of the company but instead

send a key information to the outside world on how the company is performing (Baker &

Jabbouri, 2016). For instance, high dividend payment level indicates that the company pays a

proportionately large amount of its income into dividends and reinvest less and vice versa (Abor

& Bokpin, 2010).

Dividend payout also affects the retained earnings of the company since they are paid out of

this.it is common knowledge that every company should pay dividends out of its earnings and

not out of its assets. This is to protect the interests of third parties like the creditors (Wei & Xiao,

2009).

EXECUTIVE SUMMARY

The purpose of this report is to analyze the annual reports ST ENGINEERING CO. and examine

the dividends policies adopted by the company in relation to dividend payout to its shareholders.

Earnings per share distributed to shareholders are critically analyzed for previous years, current

year and future projection. The report also make revenue forecast for the company for the next

year that is 2019.critical discussion of its sales volume and net income levels are clearly

highlighted for the previous, current and future. Based on the projection, it is observed that the

sales volume of the company might be to 6.59B in 2019.the net income value also fluctuates

considerably.

Dividend payout does not necessarily indicate good performance of the company but instead

send a key information to the outside world on how the company is performing (Baker &

Jabbouri, 2016). For instance, high dividend payment level indicates that the company pays a

proportionately large amount of its income into dividends and reinvest less and vice versa (Abor

& Bokpin, 2010).

Dividend payout also affects the retained earnings of the company since they are paid out of

this.it is common knowledge that every company should pay dividends out of its earnings and

not out of its assets. This is to protect the interests of third parties like the creditors (Wei & Xiao,

2009).

DIVIDEND POLICIES 3

Table of Contents

INTRODUCTION.......................................................................................................................................4

NON-FINANCIAL.....................................................................................................................................4

FINANCIAL...............................................................................................................................................4

HOW DIVIDEND PAYOUT AFFECTS FINANCIAL AND NON-FINANCIAL ASPECT,....................5

DISCUSSION OF DIVIDEND POLICIES.................................................................................................6

MM APPROACH....................................................................................................................................7

CLIENTELE EFFECT............................................................................................................................7

SIGNALING HYPOTHESIS..................................................................................................................8

FORECASTING COMPANY’S REVENUES............................................................................................8

ADVICE ON THE NEXT DIVIDEND PAYOUT OF ST ENGINEERING...............................................9

DIVIDEND YIELD.....................................................................................................................................9

CONCLUSION.........................................................................................................................................10

REFERENCES..........................................................................................................................................11

Table of Contents

INTRODUCTION.......................................................................................................................................4

NON-FINANCIAL.....................................................................................................................................4

FINANCIAL...............................................................................................................................................4

HOW DIVIDEND PAYOUT AFFECTS FINANCIAL AND NON-FINANCIAL ASPECT,....................5

DISCUSSION OF DIVIDEND POLICIES.................................................................................................6

MM APPROACH....................................................................................................................................7

CLIENTELE EFFECT............................................................................................................................7

SIGNALING HYPOTHESIS..................................................................................................................8

FORECASTING COMPANY’S REVENUES............................................................................................8

ADVICE ON THE NEXT DIVIDEND PAYOUT OF ST ENGINEERING...............................................9

DIVIDEND YIELD.....................................................................................................................................9

CONCLUSION.........................................................................................................................................10

REFERENCES..........................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DIVIDEND POLICIES 4

INTRODUCTION

ST ENGINEERING CO is a listed company in the Singapore stock exchange which means they

float their shares publicly through prospectus issue.it is a company that is in technology industry

and specializes in defense, aerospace, electronics, land and marine technology. The company

does not have any predefined dividend policy regarding payment of its shares since it is argued

that dividends payouts is affected by many factors such as the need to hold cash and future cash

flows needs of the company so as to meet its obligations as and when they fall due.it is also

observed that the company payment of shares fluctuates from one year to another based on the

earnings of the company.

NON-FINANCIAL

Innovation-this refers to entity’s capability to bring a new product or service into the,

marketplace. This determine the success of that company and survival in the industry. This will

also create more value to its clients and therefore increase its revenue (Ozuomba, Anichebe &

Okoye, 2016).

Firm size (market share)-this refers to the size that a firm occupies in the marketplace. Increase

in the market share leads to increase in earnings of a company due to increased sales.

industry-this is the whole marketplace that the company operates in

Ownership structure-this refers to whether the company has a large level of promoter holding or

not.

Shareholders-this are owners of the company who have invested in the company with an

expectation to get return

Legal rules-this are laws and regulations put in place so as to protect shareholders and creditors

of the company

FINANCIAL.

Return on assets-this refers to the rate at which investments generates incomes to the

shareholders. Every shareholders expects an earning from every shilling that he/she invest into

the business and therefore return on assets is that part of revenue generated by the assets invested

(Al-Malkawi, Rafferty & Pillai, 2010).

INTRODUCTION

ST ENGINEERING CO is a listed company in the Singapore stock exchange which means they

float their shares publicly through prospectus issue.it is a company that is in technology industry

and specializes in defense, aerospace, electronics, land and marine technology. The company

does not have any predefined dividend policy regarding payment of its shares since it is argued

that dividends payouts is affected by many factors such as the need to hold cash and future cash

flows needs of the company so as to meet its obligations as and when they fall due.it is also

observed that the company payment of shares fluctuates from one year to another based on the

earnings of the company.

NON-FINANCIAL

Innovation-this refers to entity’s capability to bring a new product or service into the,

marketplace. This determine the success of that company and survival in the industry. This will

also create more value to its clients and therefore increase its revenue (Ozuomba, Anichebe &

Okoye, 2016).

Firm size (market share)-this refers to the size that a firm occupies in the marketplace. Increase

in the market share leads to increase in earnings of a company due to increased sales.

industry-this is the whole marketplace that the company operates in

Ownership structure-this refers to whether the company has a large level of promoter holding or

not.

Shareholders-this are owners of the company who have invested in the company with an

expectation to get return

Legal rules-this are laws and regulations put in place so as to protect shareholders and creditors

of the company

FINANCIAL.

Return on assets-this refers to the rate at which investments generates incomes to the

shareholders. Every shareholders expects an earning from every shilling that he/she invest into

the business and therefore return on assets is that part of revenue generated by the assets invested

(Al-Malkawi, Rafferty & Pillai, 2010).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DIVIDEND POLICIES 5

Retained earnings-this implies that portion of income that is left in the company after deducting

all the expenses for the year. This value represents re-investment. this will bring a lot of incomes

in the future.

Profitability-this are income generated from the normal operation of the company and is gross,

that is no deduction has been made or after making such other adjustments (Abor & Bokpin,

2010).

Leverage-this are loans brought in to finance the operations of the business

Tax policies-this refers to compulsory payment to the state and this affect dividend payout a

great deal.

Inflation-this is a situation where general prices of goods and services are rising uncontrollably.

Liquidity-this shows ability of the company to pay its obligations when they fall due

HOW DIVIDEND PAYOUT AFFECTS FINANCIAL AND NON-FINANCIAL ASPECT,

Dividend Payout refers to the amount out of net incomes of a company that is payable as

dividends and measured by dividend payout ratio;

PR=TOTAL DIVIDENDS/NET INCOME

A very high level of dividend payout ratio indicates that the company is not reinvesting a lot of

its incomes but instead pays a lot to the shareholders in form of dividends

A very low dividend payout show that the company reinvests a lot of its income into the business

and therefore it is projected that it will generate a lot of incomes going into the future.

Dividend payout of a certain company affects the financial aspect of any company since

dividends is dependent on the income of the company, that is, income made by a company will

influence the amount of dividends to be distributed to shareholders. Thus a company that

distributes large amount of its earning to shareholders will reduce its retained earnings thus

affecting its internal finance.

Dividends payout in a company has impacts on the perception of the investor and therefore care

must be undertaken by the company when designing its dividend payout.

Retained earnings-this implies that portion of income that is left in the company after deducting

all the expenses for the year. This value represents re-investment. this will bring a lot of incomes

in the future.

Profitability-this are income generated from the normal operation of the company and is gross,

that is no deduction has been made or after making such other adjustments (Abor & Bokpin,

2010).

Leverage-this are loans brought in to finance the operations of the business

Tax policies-this refers to compulsory payment to the state and this affect dividend payout a

great deal.

Inflation-this is a situation where general prices of goods and services are rising uncontrollably.

Liquidity-this shows ability of the company to pay its obligations when they fall due

HOW DIVIDEND PAYOUT AFFECTS FINANCIAL AND NON-FINANCIAL ASPECT,

Dividend Payout refers to the amount out of net incomes of a company that is payable as

dividends and measured by dividend payout ratio;

PR=TOTAL DIVIDENDS/NET INCOME

A very high level of dividend payout ratio indicates that the company is not reinvesting a lot of

its incomes but instead pays a lot to the shareholders in form of dividends

A very low dividend payout show that the company reinvests a lot of its income into the business

and therefore it is projected that it will generate a lot of incomes going into the future.

Dividend payout of a certain company affects the financial aspect of any company since

dividends is dependent on the income of the company, that is, income made by a company will

influence the amount of dividends to be distributed to shareholders. Thus a company that

distributes large amount of its earning to shareholders will reduce its retained earnings thus

affecting its internal finance.

Dividends payout in a company has impacts on the perception of the investor and therefore care

must be undertaken by the company when designing its dividend payout.

DIVIDEND POLICIES 6

An industry that a company operates in determine its dividend policy and therefore it affects its

dividend payout. For example, a company that operates in a more certain industry like Amara

holding limited will be able to make projections on how to pay its dividends. Leverage reduces

the amount of dividends paid so that the company can be able to make payments even on periods

of low incomes.

Dividend payout affect the expectation of different shareholders as their expectation differ a lot.

Some expect large dividends while some want large reinvestment.

Dividend payout affect taxes to the state. Tax reduces earnings after tax that can be distributed to

shareholders

Inflation will force the company to retain much and give out less in form of dividends.

Dividend payout affect the liquidity of the company and therefore high payment of dividends is

only possible when the company is highly liquid ((Harada & Nguyen, 2011).

Dividend payout is affected by the rules that states when dividends should be paid.it says

dividends should only be paid out of profits and not out of capital. This protects the interest of

the creditors. Payments of dividends should not contravene this law (Yarram, & Dollery, 2015).

Return on assets-dividends ca only be paid if the company is making profits. If the company is

not making profits, dividends cannot be paid (Baba, 2009).

Dividends payout reduces the amount re-invested in the business thus affecting the level of

innovation in the company due to less money to be re invested (Benavides, Berggrun & Perafan,

2016).

DISCUSSION OF DIVIDEND POLICIES

Dividends is that part of the profit that is distributed to the shareholders and can be Cash, stock,

bond or property dividends (Allen, Gottesman, Saunders, & Tang, 2012).

This discussion is based on the annual reports ST ENGINEERING. A critical analysis of

dividend policies based on the general theories of dividend policies.

An industry that a company operates in determine its dividend policy and therefore it affects its

dividend payout. For example, a company that operates in a more certain industry like Amara

holding limited will be able to make projections on how to pay its dividends. Leverage reduces

the amount of dividends paid so that the company can be able to make payments even on periods

of low incomes.

Dividend payout affect the expectation of different shareholders as their expectation differ a lot.

Some expect large dividends while some want large reinvestment.

Dividend payout affect taxes to the state. Tax reduces earnings after tax that can be distributed to

shareholders

Inflation will force the company to retain much and give out less in form of dividends.

Dividend payout affect the liquidity of the company and therefore high payment of dividends is

only possible when the company is highly liquid ((Harada & Nguyen, 2011).

Dividend payout is affected by the rules that states when dividends should be paid.it says

dividends should only be paid out of profits and not out of capital. This protects the interest of

the creditors. Payments of dividends should not contravene this law (Yarram, & Dollery, 2015).

Return on assets-dividends ca only be paid if the company is making profits. If the company is

not making profits, dividends cannot be paid (Baba, 2009).

Dividends payout reduces the amount re-invested in the business thus affecting the level of

innovation in the company due to less money to be re invested (Benavides, Berggrun & Perafan,

2016).

DISCUSSION OF DIVIDEND POLICIES

Dividends is that part of the profit that is distributed to the shareholders and can be Cash, stock,

bond or property dividends (Allen, Gottesman, Saunders, & Tang, 2012).

This discussion is based on the annual reports ST ENGINEERING. A critical analysis of

dividend policies based on the general theories of dividend policies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DIVIDEND POLICIES 7

Economists argues that entity’s dividend policies have no effect on the prices of its stock. They

say that if a company has been operational for quite some time, then shareholders expect high

shares and not diversification (Adjaoud & Ben, 2010).

MM APPROACH

According to the arguments of dividends irrelevance theory, it emphasizes that investment

policies of the company is clear and known always and therefore more profits should not be

reinvested (Okafor & Chijoke, 2011). According to MM’s dividends irrelevance, therefore, it

reinforces the inclination of managers to keep dividends very low and use money to expand the

business. According to the MM approach, whether a company pays dividends or not, it has no

effect on the overall value of the company.it says that under perfect environment, dividend

policies of the co. is irrelevant and doesn’t affect the its value (Al-Kuwari, 2009).

The ST ENGINEERING doesn’t have any fixed dividend policies in relation to payment of

dividends since it is dependent on many factors such as current cash needs of the company and

future financial needs. Any changes regarding the payment of dividends ST ENGINEERING

will be communicated to the shareholders (DeAngelo, DeAngelo & Skinner, 2009).

Considering the income statement of ST ENGINEERING for the year 2016 and 2017,we found

out that the company is paying out dividends to its shareholders in proportionate amount i.e. in

2016 it paid out dividends at the rate of 15.60 per share while in 2017 it paid out dividends at the

rate of 16.43 and in 2015,it paid out dividends at the rate of 17.05 this indicates that, the MM

approach model hold in this case, whether ST ENGINEERING pays dividends or not, it will not

affect its share prices or value(Jeong, 2013).

CLIENTELE EFFECT

this theory focuses on the movement of share values in relation to demand and aims of the

investors.it comes in reaction to the taxation which might affect the share prices. This theory

assumes that shareholders are in the first place attracted to company rules and when this rules

and policies are changed, they will consequently change their shareholding and this leads to

consequent change in the share prices (Hussainey, Oscar & Chijoke 2011).

Economists argues that entity’s dividend policies have no effect on the prices of its stock. They

say that if a company has been operational for quite some time, then shareholders expect high

shares and not diversification (Adjaoud & Ben, 2010).

MM APPROACH

According to the arguments of dividends irrelevance theory, it emphasizes that investment

policies of the company is clear and known always and therefore more profits should not be

reinvested (Okafor & Chijoke, 2011). According to MM’s dividends irrelevance, therefore, it

reinforces the inclination of managers to keep dividends very low and use money to expand the

business. According to the MM approach, whether a company pays dividends or not, it has no

effect on the overall value of the company.it says that under perfect environment, dividend

policies of the co. is irrelevant and doesn’t affect the its value (Al-Kuwari, 2009).

The ST ENGINEERING doesn’t have any fixed dividend policies in relation to payment of

dividends since it is dependent on many factors such as current cash needs of the company and

future financial needs. Any changes regarding the payment of dividends ST ENGINEERING

will be communicated to the shareholders (DeAngelo, DeAngelo & Skinner, 2009).

Considering the income statement of ST ENGINEERING for the year 2016 and 2017,we found

out that the company is paying out dividends to its shareholders in proportionate amount i.e. in

2016 it paid out dividends at the rate of 15.60 per share while in 2017 it paid out dividends at the

rate of 16.43 and in 2015,it paid out dividends at the rate of 17.05 this indicates that, the MM

approach model hold in this case, whether ST ENGINEERING pays dividends or not, it will not

affect its share prices or value(Jeong, 2013).

CLIENTELE EFFECT

this theory focuses on the movement of share values in relation to demand and aims of the

investors.it comes in reaction to the taxation which might affect the share prices. This theory

assumes that shareholders are in the first place attracted to company rules and when this rules

and policies are changed, they will consequently change their shareholding and this leads to

consequent change in the share prices (Hussainey, Oscar & Chijoke 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DIVIDEND POLICIES 8

SIGNALING HYPOTHESIS

this particular theory argues that a company may offer a very generous dividend policy to its

shareholders not because they want to do so but they want to send out a positive signal outside

about the company and future opportunities of the company. this will assist the company look

good in the eyes of financial market. This is why ST ENGINEERING pays its dividends to

shareholders even if it is very low (Goncharov, & van, 2011).

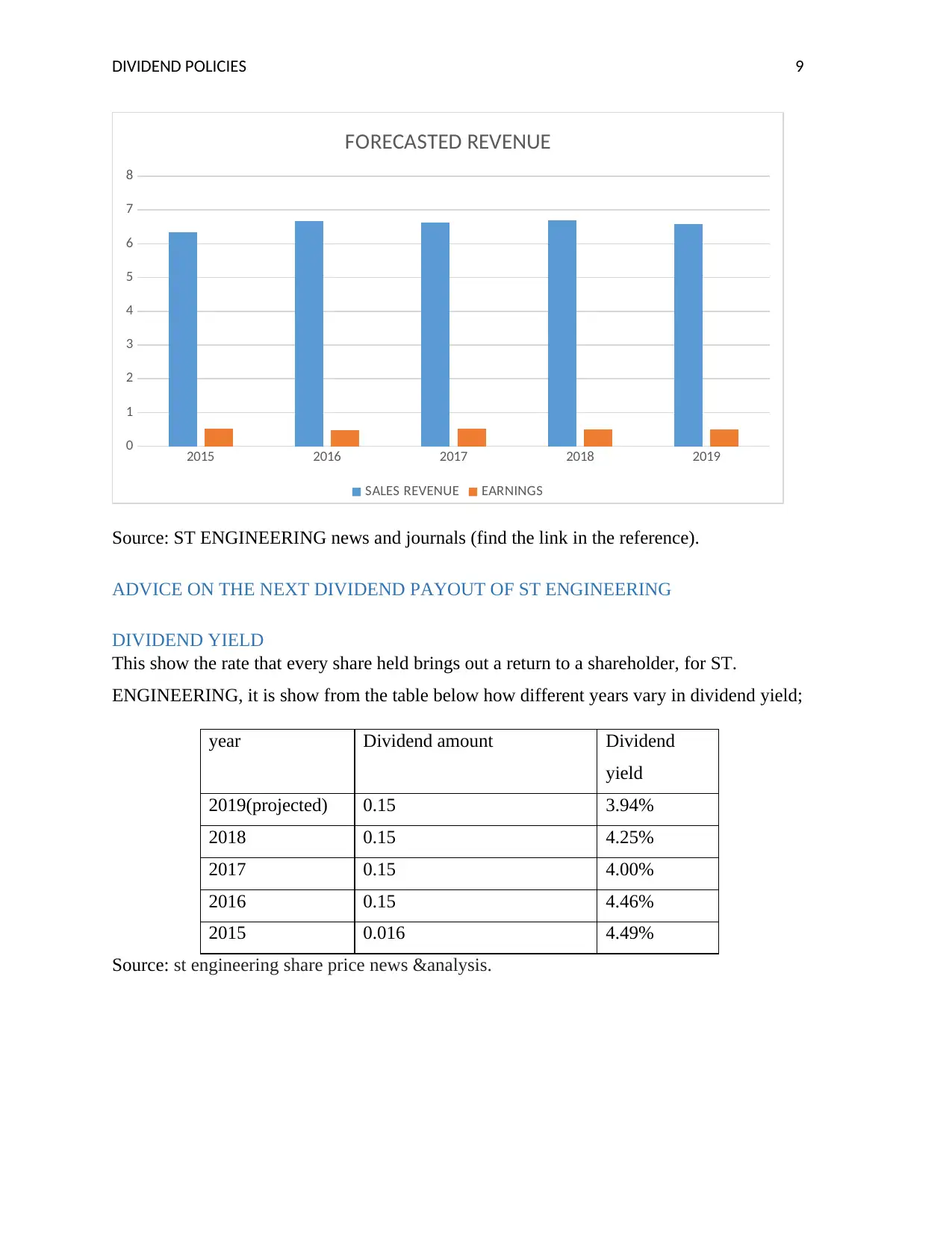

FORECASTING COMPANY’S REVENUES

Revenue forecasting involves extrapolating the current revenues of the company to the future so

as to determine the possible range of the revenues of that company in future. this is done

basically by analyzing current years’ revenue and extrapolating it to the future. Based on the

company’s previous revenues, I have prepared the bar graph below to ease my projection for the

next year based on the current revenues (Mirza & Azfa, 2010). this is in the form of

extrapolation and determination of future incomes and earnings of the ST. ENGINEERING

based on the financial information given for 2015,2016 and 2017 and 2018 basing on this years, I

have projected the same for 2019 as shown in the table below.

YEAR 2015 2016 2017 2018 2019(PROJECTED)

SALES

REVENUE

6.34B 6.68B 6.62B 6.70B 6.59B

EARNINGS 529.04M 484.51M 511.88M 494.24M 504.92M

SIGNALING HYPOTHESIS

this particular theory argues that a company may offer a very generous dividend policy to its

shareholders not because they want to do so but they want to send out a positive signal outside

about the company and future opportunities of the company. this will assist the company look

good in the eyes of financial market. This is why ST ENGINEERING pays its dividends to

shareholders even if it is very low (Goncharov, & van, 2011).

FORECASTING COMPANY’S REVENUES

Revenue forecasting involves extrapolating the current revenues of the company to the future so

as to determine the possible range of the revenues of that company in future. this is done

basically by analyzing current years’ revenue and extrapolating it to the future. Based on the

company’s previous revenues, I have prepared the bar graph below to ease my projection for the

next year based on the current revenues (Mirza & Azfa, 2010). this is in the form of

extrapolation and determination of future incomes and earnings of the ST. ENGINEERING

based on the financial information given for 2015,2016 and 2017 and 2018 basing on this years, I

have projected the same for 2019 as shown in the table below.

YEAR 2015 2016 2017 2018 2019(PROJECTED)

SALES

REVENUE

6.34B 6.68B 6.62B 6.70B 6.59B

EARNINGS 529.04M 484.51M 511.88M 494.24M 504.92M

DIVIDEND POLICIES 9

2015 2016 2017 2018 2019

0

1

2

3

4

5

6

7

8

FORECASTED REVENUE

SALES REVENUE EARNINGS

Source: ST ENGINEERING news and journals (find the link in the reference).

ADVICE ON THE NEXT DIVIDEND PAYOUT OF ST ENGINEERING

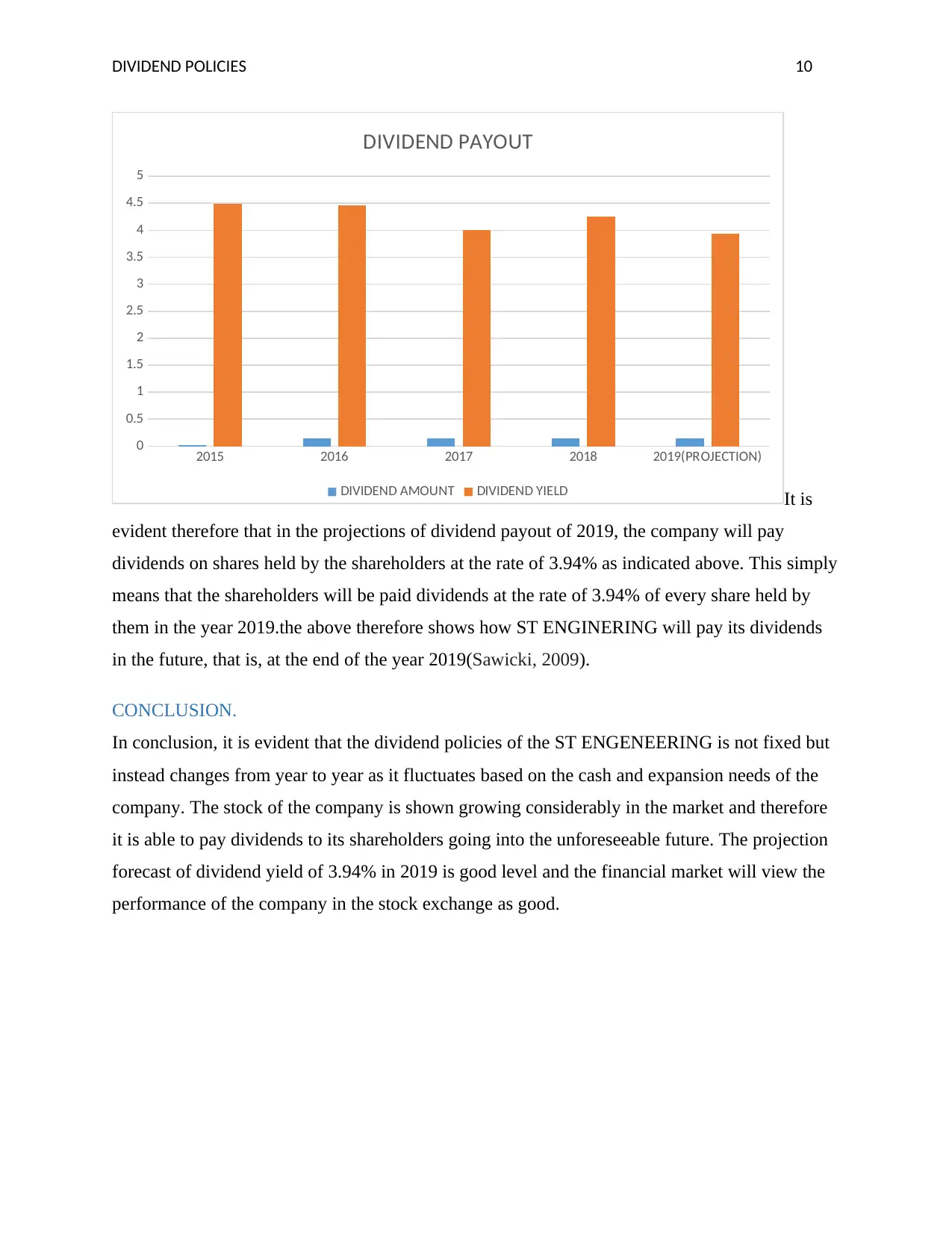

DIVIDEND YIELD

This show the rate that every share held brings out a return to a shareholder, for ST.

ENGINEERING, it is show from the table below how different years vary in dividend yield;

year Dividend amount Dividend

yield

2019(projected) 0.15 3.94%

2018 0.15 4.25%

2017 0.15 4.00%

2016 0.15 4.46%

2015 0.016 4.49%

Source: st engineering share price news &analysis.

2015 2016 2017 2018 2019

0

1

2

3

4

5

6

7

8

FORECASTED REVENUE

SALES REVENUE EARNINGS

Source: ST ENGINEERING news and journals (find the link in the reference).

ADVICE ON THE NEXT DIVIDEND PAYOUT OF ST ENGINEERING

DIVIDEND YIELD

This show the rate that every share held brings out a return to a shareholder, for ST.

ENGINEERING, it is show from the table below how different years vary in dividend yield;

year Dividend amount Dividend

yield

2019(projected) 0.15 3.94%

2018 0.15 4.25%

2017 0.15 4.00%

2016 0.15 4.46%

2015 0.016 4.49%

Source: st engineering share price news &analysis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DIVIDEND POLICIES 10

It is

evident therefore that in the projections of dividend payout of 2019, the company will pay

dividends on shares held by the shareholders at the rate of 3.94% as indicated above. This simply

means that the shareholders will be paid dividends at the rate of 3.94% of every share held by

them in the year 2019.the above therefore shows how ST ENGINERING will pay its dividends

in the future, that is, at the end of the year 2019(Sawicki, 2009).

CONCLUSION.

In conclusion, it is evident that the dividend policies of the ST ENGENEERING is not fixed but

instead changes from year to year as it fluctuates based on the cash and expansion needs of the

company. The stock of the company is shown growing considerably in the market and therefore

it is able to pay dividends to its shareholders going into the unforeseeable future. The projection

forecast of dividend yield of 3.94% in 2019 is good level and the financial market will view the

performance of the company in the stock exchange as good.

2015 2016 2017 2018 2019(PROJECTION)

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

DIVIDEND PAYOUT

DIVIDEND AMOUNT DIVIDEND YIELD

It is

evident therefore that in the projections of dividend payout of 2019, the company will pay

dividends on shares held by the shareholders at the rate of 3.94% as indicated above. This simply

means that the shareholders will be paid dividends at the rate of 3.94% of every share held by

them in the year 2019.the above therefore shows how ST ENGINERING will pay its dividends

in the future, that is, at the end of the year 2019(Sawicki, 2009).

CONCLUSION.

In conclusion, it is evident that the dividend policies of the ST ENGENEERING is not fixed but

instead changes from year to year as it fluctuates based on the cash and expansion needs of the

company. The stock of the company is shown growing considerably in the market and therefore

it is able to pay dividends to its shareholders going into the unforeseeable future. The projection

forecast of dividend yield of 3.94% in 2019 is good level and the financial market will view the

performance of the company in the stock exchange as good.

2015 2016 2017 2018 2019(PROJECTION)

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

DIVIDEND PAYOUT

DIVIDEND AMOUNT DIVIDEND YIELD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DIVIDEND POLICIES 11

REFERENCES.

Abor, J., & Bokpin, G. A. (2010). Investment opportunities, corporate finance, and dividend payout

policy: Evidence from emerging markets. Studies in Economics and Finance, 27(3), 180-

194.

Al-Kuwari, D. (2009). Determinants of the dividend policy of companies listed on emerging

stock exchanges: the case of the Gulf Cooperation Council (GCC) countries.

Allen, L., Gottesman, A., Saunders, A., & Tang, Y. (2012). The role of banks in dividend

policy. Financial Management, 41(3), 591-613.

Al-Malkawi, H. A. N., Rafferty, M., & Pillai, R. (2010). Dividend policy: A review of theories

and empirical evidence. International Bulletin of Business Administration, 9(1),

171-200.

Baker, H. K., & Jabbouri, I. (2016). How Moroccan managers view dividend policy. Managerial

Finance, 42(3), 270-288.

Benavides, J., Berggrun, L., & Perafan, H. (2016). Dividend payout policies: evidence from

Latin America. Finance Research, 17, 197-210.

DeAngelo, H., DeAngelo, L., & Skinner, D. J. (2009). Corporate payout policy. Foundations

and Trends® in Finance, 3(2–3), 95-287.

Goncharov, I., & van Triest, S. (2011). Do fair value adjustments influence dividend

policy?. Accounting and Business Research, 41(1), 51-68.

Harada, K., & Nguyen, P. (2011). Ownership concentration and dividend policy in

Japan. Managerial Finance, 37(4), 362-379.

<https://sg.finance.yahoo.com/quote/S63.SI/key-statistics/>

<https://stocks.cafe/stock/dividend/S63/singapore%2Btech%2Bengineering%2Bltd?

type=xsummary&exchange=XSES>

Hussainey, K., Oscar Mgbame, C., & Chijoke-Mgbame, A. M. (2011). Dividend policy and

share price volatility: UK evidence. The Journal of risk finance, 12(1), 57-68.

Jeong, J. (2013). Determinants of dividend smoothing in emerging market: The case of

Korea. Emerging markets finance book, 17, 76-88.

REFERENCES.

Abor, J., & Bokpin, G. A. (2010). Investment opportunities, corporate finance, and dividend payout

policy: Evidence from emerging markets. Studies in Economics and Finance, 27(3), 180-

194.

Al-Kuwari, D. (2009). Determinants of the dividend policy of companies listed on emerging

stock exchanges: the case of the Gulf Cooperation Council (GCC) countries.

Allen, L., Gottesman, A., Saunders, A., & Tang, Y. (2012). The role of banks in dividend

policy. Financial Management, 41(3), 591-613.

Al-Malkawi, H. A. N., Rafferty, M., & Pillai, R. (2010). Dividend policy: A review of theories

and empirical evidence. International Bulletin of Business Administration, 9(1),

171-200.

Baker, H. K., & Jabbouri, I. (2016). How Moroccan managers view dividend policy. Managerial

Finance, 42(3), 270-288.

Benavides, J., Berggrun, L., & Perafan, H. (2016). Dividend payout policies: evidence from

Latin America. Finance Research, 17, 197-210.

DeAngelo, H., DeAngelo, L., & Skinner, D. J. (2009). Corporate payout policy. Foundations

and Trends® in Finance, 3(2–3), 95-287.

Goncharov, I., & van Triest, S. (2011). Do fair value adjustments influence dividend

policy?. Accounting and Business Research, 41(1), 51-68.

Harada, K., & Nguyen, P. (2011). Ownership concentration and dividend policy in

Japan. Managerial Finance, 37(4), 362-379.

<https://sg.finance.yahoo.com/quote/S63.SI/key-statistics/>

<https://stocks.cafe/stock/dividend/S63/singapore%2Btech%2Bengineering%2Bltd?

type=xsummary&exchange=XSES>

Hussainey, K., Oscar Mgbame, C., & Chijoke-Mgbame, A. M. (2011). Dividend policy and

share price volatility: UK evidence. The Journal of risk finance, 12(1), 57-68.

Jeong, J. (2013). Determinants of dividend smoothing in emerging market: The case of

Korea. Emerging markets finance book, 17, 76-88.

DIVIDEND POLICIES 12

Mirza, H. H., & Azfa, T. (2010). Ownership structure and cash flows as determinants of

corporate dividend policy in Pakistan. International Business Research, 3(3), 210-

221.

Okafor, C. A., & Chijoke-Mgbame, A. M. (2011). Dividend policy and share price volatility in

Nigeria. Jorind, 9(1), 202-210.

Ozuomba, C. N., Anichebe, A. S., & Okoye, P. V. C. (2016). The effect of dividend policies on

wealth maximization–a study of some selected plcs. Cogent Business &

Management, 3(1), 1226457.

Ramli, N. M. (2010). Ownership structure and dividend policy: Evidence from Malaysian

companies. International Review of Business Research Papers, 6(1), 170-180.

Sawicki, J. (2009). Corporate governance and dividend policy in Southeast Asia pre-and post-

crisis. The European Journal of Finance, 15(2), 211-230.

Wei, G., & Xiao, J. Z. (2009). Equity ownership segregation, shareholder preferences, and

dividend policy in China. The British accounting review, 41(3), 169-183.

Yarram, S. R., & Dollery, B. (2015). Corporate governance and financial policies: Influence of

board characteristics on the dividend policy of Australian firms. Managerial

Finance, 41(3), 267-285.

Mirza, H. H., & Azfa, T. (2010). Ownership structure and cash flows as determinants of

corporate dividend policy in Pakistan. International Business Research, 3(3), 210-

221.

Okafor, C. A., & Chijoke-Mgbame, A. M. (2011). Dividend policy and share price volatility in

Nigeria. Jorind, 9(1), 202-210.

Ozuomba, C. N., Anichebe, A. S., & Okoye, P. V. C. (2016). The effect of dividend policies on

wealth maximization–a study of some selected plcs. Cogent Business &

Management, 3(1), 1226457.

Ramli, N. M. (2010). Ownership structure and dividend policy: Evidence from Malaysian

companies. International Review of Business Research Papers, 6(1), 170-180.

Sawicki, J. (2009). Corporate governance and dividend policy in Southeast Asia pre-and post-

crisis. The European Journal of Finance, 15(2), 211-230.

Wei, G., & Xiao, J. Z. (2009). Equity ownership segregation, shareholder preferences, and

dividend policy in China. The British accounting review, 41(3), 169-183.

Yarram, S. R., & Dollery, B. (2015). Corporate governance and financial policies: Influence of

board characteristics on the dividend policy of Australian firms. Managerial

Finance, 41(3), 267-285.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.