Fin 801, UIL: Dividend Theories and Policies Presentation

VerifiedAdded on 2021/10/27

|18

|6829

|483

Presentation

AI Summary

This presentation, prepared for a Corporate Finance course (Fin 801) at the University of Ilorin, delves into the critical area of dividend policy. It begins by introducing the core concept: the decision between distributing profits to shareholders versus reinvesting them in the business, emphasizing its impact on shareholder wealth maximization. The presentation explores various dividend types, including regular cash dividends, extra dividends, special dividends, and liquidating dividends, along with bonus shares and stock splits. It then outlines the standard methods of cash dividend payment and the establishment of dividend policies, including the residual dividend approach and the importance of dividend stability. The analysis considers the significance of dividend decisions in financial management and their influence on the overall valuation of a firm. The presentation also provides a detailed explanation of dividend policy objectives and the classification of dividends, alongside the procedures for dividend payments. This comprehensive overview offers a deep understanding of dividend policies and their implications for financial decision-making.

Page1

DIVIDEND THEORIES AND POLICIES

THE RELEVANCE OF THE POLICY ON THE

VALUE OF THE FIRM

COURSE TITLE: CORPORATE FINANCE

COURSE CODE: FIN 801

A PRESENTATION SUBMITTED TO THE DEPARTMENT OF ACCOUNTING AND

FINANCE, FACULTY OF MANAGEMENT SCIENCES, UNIVERSITY OF ILORIIN, KWARA

STATE, NIGERIA.

BY

NASIRUDEEN ABDULLAHI

UIL/PG2020/1432

LECTURER IN CHARGE: DR. I.B ABDULLAHI

OCTOBER, 2021

DIVIDEND THEORIES AND POLICIES

THE RELEVANCE OF THE POLICY ON THE

VALUE OF THE FIRM

COURSE TITLE: CORPORATE FINANCE

COURSE CODE: FIN 801

A PRESENTATION SUBMITTED TO THE DEPARTMENT OF ACCOUNTING AND

FINANCE, FACULTY OF MANAGEMENT SCIENCES, UNIVERSITY OF ILORIIN, KWARA

STATE, NIGERIA.

BY

NASIRUDEEN ABDULLAHI

UIL/PG2020/1432

LECTURER IN CHARGE: DR. I.B ABDULLAHI

OCTOBER, 2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page2

DIVIDEND THEORIES AND POLICIES

THE RELEVANCE OF THE POLICY ON THE VALUE OF THE FIRM

Introduction

The dividend policy decision involves the choice between distributing the profits belonging to

the shareholders and their retention by the firm. A major decision area of Financial

management is the dividend policy decision in the sense that the firm has to choose between

distributing the profits to the shareholders and ploughing them back into the business. The

selection would be influenced by the effect on the objective of Financial Management of

maximizing shareholder’s wealth. The firm should pay dividend if the payment will lead to the

maximisation of the wealth of the owners and if not then the firm should retain profits to

finance investment programmes.The relationship between dividends and value of the firm

should, therefore, be the decision criterion.There are conflicting opinions regarding the impact

of dividends on the valuation of a firm. Retained earnings are the most significant internal

sources of financing the growth of the firm. On the other hand, dividends may be considered

desirable from the shareholders’ point of view as they tend to increase their current return.

Dividends, however, constitute the use of the firm’s funds. Dividend policy involves the

balancing of the shareholders’ desire for current dividends and the firms’ needs for funds for

growth.

Objective of dividend policy

A firms’ dividend policy has the effect of dividing its net earnings into two parts:

retained earnings and dividends. The retained earnings provide funds to finance the firm’s long

– term growth. It is the most significant source of financing a firm’s investment in practice.

Dividends are paid in cash. Thus, the distribution of earnings uses the available cash of the

firm. A firm which intends to pay dividends and also needs funds to finance its investment

opportunities will have to use external sources of financing, such as the issue of debt or equity.

Dividends - Classification

The term dividend usually refers to cash paid out of earnings. If a payment is made

from sources other than current or accumulated retained earnings, the term distribution, rather

than dividend, is used. However, it is acceptable to refer to a distribution of earnings as a

dividend and a distribution from capital as a liquidating dividend. More generally, any direct

payment by the corporation to the shareholders may be considered a dividend or a part of

dividend policy.

DIVIDEND THEORIES AND POLICIES

THE RELEVANCE OF THE POLICY ON THE VALUE OF THE FIRM

Introduction

The dividend policy decision involves the choice between distributing the profits belonging to

the shareholders and their retention by the firm. A major decision area of Financial

management is the dividend policy decision in the sense that the firm has to choose between

distributing the profits to the shareholders and ploughing them back into the business. The

selection would be influenced by the effect on the objective of Financial Management of

maximizing shareholder’s wealth. The firm should pay dividend if the payment will lead to the

maximisation of the wealth of the owners and if not then the firm should retain profits to

finance investment programmes.The relationship between dividends and value of the firm

should, therefore, be the decision criterion.There are conflicting opinions regarding the impact

of dividends on the valuation of a firm. Retained earnings are the most significant internal

sources of financing the growth of the firm. On the other hand, dividends may be considered

desirable from the shareholders’ point of view as they tend to increase their current return.

Dividends, however, constitute the use of the firm’s funds. Dividend policy involves the

balancing of the shareholders’ desire for current dividends and the firms’ needs for funds for

growth.

Objective of dividend policy

A firms’ dividend policy has the effect of dividing its net earnings into two parts:

retained earnings and dividends. The retained earnings provide funds to finance the firm’s long

– term growth. It is the most significant source of financing a firm’s investment in practice.

Dividends are paid in cash. Thus, the distribution of earnings uses the available cash of the

firm. A firm which intends to pay dividends and also needs funds to finance its investment

opportunities will have to use external sources of financing, such as the issue of debt or equity.

Dividends - Classification

The term dividend usually refers to cash paid out of earnings. If a payment is made

from sources other than current or accumulated retained earnings, the term distribution, rather

than dividend, is used. However, it is acceptable to refer to a distribution of earnings as a

dividend and a distribution from capital as a liquidating dividend. More generally, any direct

payment by the corporation to the shareholders may be considered a dividend or a part of

dividend policy.

Page3

Dividends come in several different forms. The basic types of cash dividends are:

Regular cash dividends

Extra dividends

Special dividends

Liquidating dividends

Cash Dividends

The most common type of dividend is a cash dividend. Commonly, public companies

pay regular cash dividends four times a year. As the name suggests, these are cash payments

made directly to shareholders, and they are made in the regular course of business. In other

words, management sees nothing unusual about the dividend and no reason why it won’t be

continued.

Sometimes firms will pay a regular cash dividend and an extra cash dividend. By

calling part of the payment “extra” management is indicating that the “extra” part may or may

not be repeated in the future. A special dividend is similar, but the name usually indicates that

this dividend is viewed as a truly unusual or one-time event and won’t be repeated. Finally, the

payment of a liquidating dividend usually means that some or all of the business has been

liquidated, that is, sold off. However it is labeled, a cash dividend payment reduces corporate

cash and retained earnings, except in the case of a liquidating dividend.

Bonus Shares (Stock dividend)

An issue of bonus shares is the distribution of shares free of cost to existing

shareholders. Bonus shares are issued in addition to the cash dividend and not in lieu of cash

dividends. Hence, companies may supplement cash dividend by bonus issues. Issuing bonus

shares increase the number of outstanding shares of the company. The bonus shares are

distributed proportionately to the existing shareholder. Hence there is no dilution of ownership.

For example, if a shareholder owns 100 shares at the time when a 10 per cent (ie., 1:10) bonus

issue made, he will receive 10 additional shares. The declaration of the bonus shares will

increase the paid-up share capital and reduce the reserve and surplus earnings of the company.

The total net worth is not affected by the bonus issue.

Stock Split

A stock split is essentially the same thing as a stock dividend, except that a split is

expressed as a ratio instead of a percentage. When a split is declared, each share is split up to

create additional shares. For example, in a three-for-one stock split, each old share is split into

three new shares.

Dividends come in several different forms. The basic types of cash dividends are:

Regular cash dividends

Extra dividends

Special dividends

Liquidating dividends

Cash Dividends

The most common type of dividend is a cash dividend. Commonly, public companies

pay regular cash dividends four times a year. As the name suggests, these are cash payments

made directly to shareholders, and they are made in the regular course of business. In other

words, management sees nothing unusual about the dividend and no reason why it won’t be

continued.

Sometimes firms will pay a regular cash dividend and an extra cash dividend. By

calling part of the payment “extra” management is indicating that the “extra” part may or may

not be repeated in the future. A special dividend is similar, but the name usually indicates that

this dividend is viewed as a truly unusual or one-time event and won’t be repeated. Finally, the

payment of a liquidating dividend usually means that some or all of the business has been

liquidated, that is, sold off. However it is labeled, a cash dividend payment reduces corporate

cash and retained earnings, except in the case of a liquidating dividend.

Bonus Shares (Stock dividend)

An issue of bonus shares is the distribution of shares free of cost to existing

shareholders. Bonus shares are issued in addition to the cash dividend and not in lieu of cash

dividends. Hence, companies may supplement cash dividend by bonus issues. Issuing bonus

shares increase the number of outstanding shares of the company. The bonus shares are

distributed proportionately to the existing shareholder. Hence there is no dilution of ownership.

For example, if a shareholder owns 100 shares at the time when a 10 per cent (ie., 1:10) bonus

issue made, he will receive 10 additional shares. The declaration of the bonus shares will

increase the paid-up share capital and reduce the reserve and surplus earnings of the company.

The total net worth is not affected by the bonus issue.

Stock Split

A stock split is essentially the same thing as a stock dividend, except that a split is

expressed as a ratio instead of a percentage. When a split is declared, each share is split up to

create additional shares. For example, in a three-for-one stock split, each old share is split into

three new shares.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page4

Standard Method of Cash Dividend Payment

The decision to pay a dividend rests in the hands of the board of directors of the

corporation. When a dividend has been declared, it becomes a debt of the firm and cannot be

rescinded easily. Sometime after it has been declared, a dividend is distributed to all

shareholders as of some specific date. Commonly, the amount of the cash dividend is

expressed in terms of dollars per share (dividends per share). As we have seen in other

chapters, it is also expressed as a percentage of the market price (the dividend yield) or as a

percentage of net income or earnings per share (the dividend payout).

Example of procedure for dividend payment

January 15 January 28 January 30 February 16

(Declaration date) (Ex-Dividend date) (Record date) (Payment date)

Establishing Dividend policies and Decisions

How do firms actually determine the level of dividends they will pay at a particular

time? As we have seen, there are good reasons for firms to pay high dividends and there are

good reasons to pay low dividends. There are three approaches for establishing dividend

policy. These are three types of the dividend policy, such as residual dividend approach,

dividend stability and a compromise dividend policy.

Residual Dividend Approach

Firms with higher dividend payouts will have to sell stock more often. Such sales are not

very common and they can be very expensive.

Consistent with this, we will assume that the firm wishes to minimize the need to sell new

equity. We will also assume that the firm wishes to maintain its current capital structure.

If a firm wishes to avoid new equity sales, then it will have to rely on internally generated

equity to finance new positive NPV projects. Dividends can only be paid out of what is

left over. This leftover is called the residual, and such a dividend policy is called a

residual dividend approach.

With a residual dividend policy, the firm’s objective is to meet its investment needs and

maintain its desired debt-equity ratio before paying dividends.

Illustrate, imagine that a firm has N1,000 in earnings and a debt-equity ratio of 0.50. Notice

that, because the debt-equity ratio is 0.50, the firm has 50 cents in debt for every N1.50 in total

value. The firm’s capital structure is thus debt and equity.

The first step in implementing a residual dividend policy is to determine the amount of

funds that can be generated without selling new equity. If the firm reinvests the entire N1,000

and pays no dividend, then equity will increase by N1,000. To keep the debt-equity ratio of

Standard Method of Cash Dividend Payment

The decision to pay a dividend rests in the hands of the board of directors of the

corporation. When a dividend has been declared, it becomes a debt of the firm and cannot be

rescinded easily. Sometime after it has been declared, a dividend is distributed to all

shareholders as of some specific date. Commonly, the amount of the cash dividend is

expressed in terms of dollars per share (dividends per share). As we have seen in other

chapters, it is also expressed as a percentage of the market price (the dividend yield) or as a

percentage of net income or earnings per share (the dividend payout).

Example of procedure for dividend payment

January 15 January 28 January 30 February 16

(Declaration date) (Ex-Dividend date) (Record date) (Payment date)

Establishing Dividend policies and Decisions

How do firms actually determine the level of dividends they will pay at a particular

time? As we have seen, there are good reasons for firms to pay high dividends and there are

good reasons to pay low dividends. There are three approaches for establishing dividend

policy. These are three types of the dividend policy, such as residual dividend approach,

dividend stability and a compromise dividend policy.

Residual Dividend Approach

Firms with higher dividend payouts will have to sell stock more often. Such sales are not

very common and they can be very expensive.

Consistent with this, we will assume that the firm wishes to minimize the need to sell new

equity. We will also assume that the firm wishes to maintain its current capital structure.

If a firm wishes to avoid new equity sales, then it will have to rely on internally generated

equity to finance new positive NPV projects. Dividends can only be paid out of what is

left over. This leftover is called the residual, and such a dividend policy is called a

residual dividend approach.

With a residual dividend policy, the firm’s objective is to meet its investment needs and

maintain its desired debt-equity ratio before paying dividends.

Illustrate, imagine that a firm has N1,000 in earnings and a debt-equity ratio of 0.50. Notice

that, because the debt-equity ratio is 0.50, the firm has 50 cents in debt for every N1.50 in total

value. The firm’s capital structure is thus debt and equity.

The first step in implementing a residual dividend policy is to determine the amount of

funds that can be generated without selling new equity. If the firm reinvests the entire N1,000

and pays no dividend, then equity will increase by N1,000. To keep the debt-equity ratio of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page5

0.50, the firm must borrow an additional N500. The total amount of funds that can be

generated without selling new equity is thus N1,000 + 500 = N1,500.

The second step is to decide whether or not a dividend will be paid. To do this, we

compare the total amount that can be generated without selling new equity (N1,500 in this

case) to planned capital spending.

If funds needed exceed funds available, then no dividend will be paid. In addition, the firm

will have to sell new equity to raise the needed financing or else postpone some planned

capital spending.

If funds needed are less than funds generated, then a dividend will be paid. The amount of

the dividend will be the residual, that is, that portion of the earnings that is not needed to

finance new projects.

For example,

Suppose we have N900 in planning capital spending. To maintain the firm’s capital

structure, this N900 must be financed by 2⁄3 equity and 1⁄3debt. So, the firm will actually

borrow 1⁄3 X N900 = N300. The firm will spend 2⁄3 X N900 = N600 of the N1,000 in equity

available. There is a N1,000 - 600 = N400 residual, so the dividend will be N400.

In sum, the firm has after tax earnings of N1,000. Dividends paid are N400. Retained

earnings are N600, and new borrowing totals N300. The firm’s debt-equity ratio is unchanged

at 0.50.

Stability of Dividend

It is considered a desirable policy by the management of most companies in practices.

Many surveys have shown that shareholders also seem generally to favor this policy and value

stable dividends higher than the fluctuating ones. All other things being the same, the stable

dividend policy may have a positive impact on the market price of the share.

It is also meant regularity in paying some dividend annually, even though the amount of

the dividend may fluctuate over the years, and may not relate to earnings. There are a number

of companies, which have records of paying dividend for a long, unbroken period. More

precisely, stability of dividend refers to the amounts paid out regularly. Three forms of such

stability may be distinguished:

a) Constant dividend per share or dividend rate

b) Constant pay out.

c) Constant dividend per share plus extra dividend.

0.50, the firm must borrow an additional N500. The total amount of funds that can be

generated without selling new equity is thus N1,000 + 500 = N1,500.

The second step is to decide whether or not a dividend will be paid. To do this, we

compare the total amount that can be generated without selling new equity (N1,500 in this

case) to planned capital spending.

If funds needed exceed funds available, then no dividend will be paid. In addition, the firm

will have to sell new equity to raise the needed financing or else postpone some planned

capital spending.

If funds needed are less than funds generated, then a dividend will be paid. The amount of

the dividend will be the residual, that is, that portion of the earnings that is not needed to

finance new projects.

For example,

Suppose we have N900 in planning capital spending. To maintain the firm’s capital

structure, this N900 must be financed by 2⁄3 equity and 1⁄3debt. So, the firm will actually

borrow 1⁄3 X N900 = N300. The firm will spend 2⁄3 X N900 = N600 of the N1,000 in equity

available. There is a N1,000 - 600 = N400 residual, so the dividend will be N400.

In sum, the firm has after tax earnings of N1,000. Dividends paid are N400. Retained

earnings are N600, and new borrowing totals N300. The firm’s debt-equity ratio is unchanged

at 0.50.

Stability of Dividend

It is considered a desirable policy by the management of most companies in practices.

Many surveys have shown that shareholders also seem generally to favor this policy and value

stable dividends higher than the fluctuating ones. All other things being the same, the stable

dividend policy may have a positive impact on the market price of the share.

It is also meant regularity in paying some dividend annually, even though the amount of

the dividend may fluctuate over the years, and may not relate to earnings. There are a number

of companies, which have records of paying dividend for a long, unbroken period. More

precisely, stability of dividend refers to the amounts paid out regularly. Three forms of such

stability may be distinguished:

a) Constant dividend per share or dividend rate

b) Constant pay out.

c) Constant dividend per share plus extra dividend.

Page6

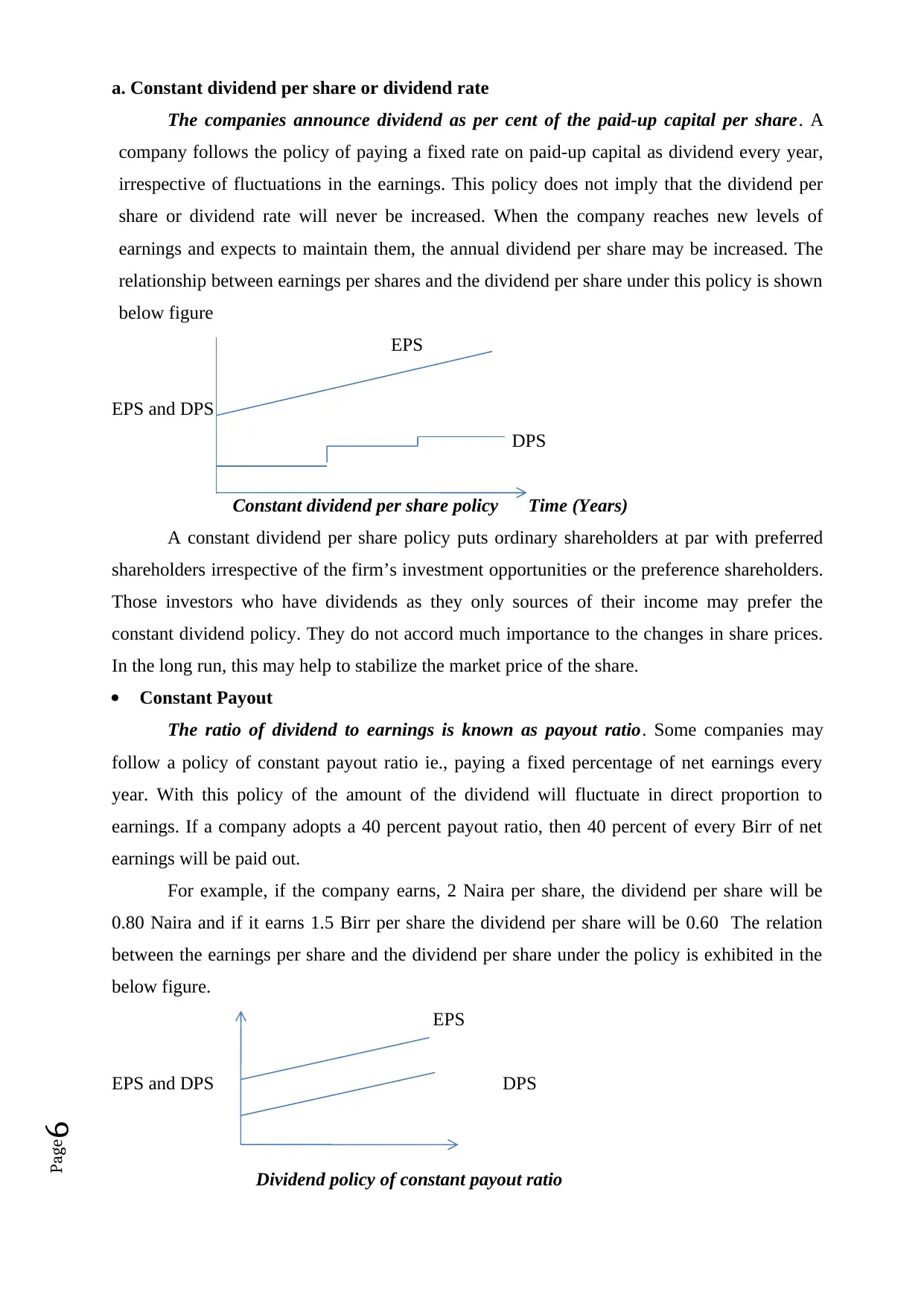

a. Constant dividend per share or dividend rate

The companies announce dividend as per cent of the paid-up capital per share. A

company follows the policy of paying a fixed rate on paid-up capital as dividend every year,

irrespective of fluctuations in the earnings. This policy does not imply that the dividend per

share or dividend rate will never be increased. When the company reaches new levels of

earnings and expects to maintain them, the annual dividend per share may be increased. The

relationship between earnings per shares and the dividend per share under this policy is shown

below figure

EPS

EPS and DPS

DPS

Constant dividend per share policy Time (Years)

A constant dividend per share policy puts ordinary shareholders at par with preferred

shareholders irrespective of the firm’s investment opportunities or the preference shareholders.

Those investors who have dividends as they only sources of their income may prefer the

constant dividend policy. They do not accord much importance to the changes in share prices.

In the long run, this may help to stabilize the market price of the share.

Constant Payout

The ratio of dividend to earnings is known as payout ratio. Some companies may

follow a policy of constant payout ratio ie., paying a fixed percentage of net earnings every

year. With this policy of the amount of the dividend will fluctuate in direct proportion to

earnings. If a company adopts a 40 percent payout ratio, then 40 percent of every Birr of net

earnings will be paid out.

For example, if the company earns, 2 Naira per share, the dividend per share will be

0.80 Naira and if it earns 1.5 Birr per share the dividend per share will be 0.60 The relation

between the earnings per share and the dividend per share under the policy is exhibited in the

below figure.

EPS

EPS and DPS DPS

Dividend policy of constant payout ratio

a. Constant dividend per share or dividend rate

The companies announce dividend as per cent of the paid-up capital per share. A

company follows the policy of paying a fixed rate on paid-up capital as dividend every year,

irrespective of fluctuations in the earnings. This policy does not imply that the dividend per

share or dividend rate will never be increased. When the company reaches new levels of

earnings and expects to maintain them, the annual dividend per share may be increased. The

relationship between earnings per shares and the dividend per share under this policy is shown

below figure

EPS

EPS and DPS

DPS

Constant dividend per share policy Time (Years)

A constant dividend per share policy puts ordinary shareholders at par with preferred

shareholders irrespective of the firm’s investment opportunities or the preference shareholders.

Those investors who have dividends as they only sources of their income may prefer the

constant dividend policy. They do not accord much importance to the changes in share prices.

In the long run, this may help to stabilize the market price of the share.

Constant Payout

The ratio of dividend to earnings is known as payout ratio. Some companies may

follow a policy of constant payout ratio ie., paying a fixed percentage of net earnings every

year. With this policy of the amount of the dividend will fluctuate in direct proportion to

earnings. If a company adopts a 40 percent payout ratio, then 40 percent of every Birr of net

earnings will be paid out.

For example, if the company earns, 2 Naira per share, the dividend per share will be

0.80 Naira and if it earns 1.5 Birr per share the dividend per share will be 0.60 The relation

between the earnings per share and the dividend per share under the policy is exhibited in the

below figure.

EPS

EPS and DPS DPS

Dividend policy of constant payout ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page7

This policy is related to a company’s ability to pay dividends. If the company incurs

losses, no dividend shall be paid regardless of the desires of shareholders. Internal financing

with retained earnings is automatic when this policy is followed. At any given payout ratio, the

amount of dividends and the additions to retained earnings increase with increasing earnings

and decrease with decrease earnings. This policy does not put any pressure on a company’s

liquidity since dividends are distributed only when the company has profited.

Constant dividend per share plus Extra dividend

The smallest amount of dividend per share is fixed to reduce the possibility of every

missing a dividend payment. By paying extra dividend in periods of prosperity, an attempt is

made to prevent investors from expecting that the dividend represents an increase in the

established dividend amount. This type of policy enables a company to pay a constant amount

of dividend regularly without a default and allows a great deal of flexibility for supplementing

the income of shareholders only when the company earnings are higher than the usual, without

committing itself to make a larger payments as part of the future fixed dividend.

A Compromise Dividend Policy

In practice, many firms appear to follow a compromise dividend policy. Such a policy

is based on five main goals:

1. Avoid cutting back on positive NPV projects to pay a dividend.

2. Avoid dividend cuts.

3. Avoid the need to sell equity.

4. Maintain a target debt-equity ratio.

5. Maintain a target dividend payout ratio.

These goals are ranked more or less in order of their importance. In our strict residual

approach, we assume that the firm maintains a fixed debt-equity ratio. Under the compromise

approach, the debt-equity ratio is viewed as a long-range goal. It is allowed to vary in the short

run if necessary to avoid a dividend cut or the need to sell new equity.

In addition to having a strong reluctance to cut dividends, financial managers tend to

think of dividend payments in terms of a proportion of income, and they also tend to think

investors are entitled to a “fair” share of corporate income. This share is the long-run target

payout ratio, and it is the fraction of the earnings the firm expects to pay as dividends under

ordinary circumstances. Again, this ratio is viewed as a long-range goal, so it might vary in the

short run if this is necessary. As a result, in the long run, earnings growth is followed by

dividend increases, but only with a lag.

This policy is related to a company’s ability to pay dividends. If the company incurs

losses, no dividend shall be paid regardless of the desires of shareholders. Internal financing

with retained earnings is automatic when this policy is followed. At any given payout ratio, the

amount of dividends and the additions to retained earnings increase with increasing earnings

and decrease with decrease earnings. This policy does not put any pressure on a company’s

liquidity since dividends are distributed only when the company has profited.

Constant dividend per share plus Extra dividend

The smallest amount of dividend per share is fixed to reduce the possibility of every

missing a dividend payment. By paying extra dividend in periods of prosperity, an attempt is

made to prevent investors from expecting that the dividend represents an increase in the

established dividend amount. This type of policy enables a company to pay a constant amount

of dividend regularly without a default and allows a great deal of flexibility for supplementing

the income of shareholders only when the company earnings are higher than the usual, without

committing itself to make a larger payments as part of the future fixed dividend.

A Compromise Dividend Policy

In practice, many firms appear to follow a compromise dividend policy. Such a policy

is based on five main goals:

1. Avoid cutting back on positive NPV projects to pay a dividend.

2. Avoid dividend cuts.

3. Avoid the need to sell equity.

4. Maintain a target debt-equity ratio.

5. Maintain a target dividend payout ratio.

These goals are ranked more or less in order of their importance. In our strict residual

approach, we assume that the firm maintains a fixed debt-equity ratio. Under the compromise

approach, the debt-equity ratio is viewed as a long-range goal. It is allowed to vary in the short

run if necessary to avoid a dividend cut or the need to sell new equity.

In addition to having a strong reluctance to cut dividends, financial managers tend to

think of dividend payments in terms of a proportion of income, and they also tend to think

investors are entitled to a “fair” share of corporate income. This share is the long-run target

payout ratio, and it is the fraction of the earnings the firm expects to pay as dividends under

ordinary circumstances. Again, this ratio is viewed as a long-range goal, so it might vary in the

short run if this is necessary. As a result, in the long run, earnings growth is followed by

dividend increases, but only with a lag.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page8

Factors Determination of Dividend Policies

1. Bond Indentures. Debt contracts often limit dividend payments to earnings generated

after the loan was granted. Also, debt contracts often stipulate that no dividends can be

paid unless the current ratio, times-interest earned ratio, and other safety ratios exceed

stated minimums.

2. Preferred stock restrictions. Typically, common dividends cannot be paid if the

company has omitted its preferred dividend. The preferred average must be satisfied

before common dividends can be resumed.

3. Impairment of capital rule. Dividend payments cannot exceed the balance sheet item

“retained earnings.” This legal restriction, known as the impairment of capital rule, is

designed to protect creditors. Without the rule, a company that is in trouble might

distribute most of its assets to stockholders and leave its debt holders out in the cold.

(Liquidating dividends can be paid out of capital, but they must be indicated as such, and

they must not reduce capital below the limits stated in debt contracts.)

4. Availability of cash. Cash dividends can be paid only with cash. Thus, a shortage of cash

in the bank can restrict dividend payments. However, the ability to borrow can offset this

factor.

5. Penalty tax on improperly accumulated earnings. To prevent wealthy individuals from

using corporations to avoid personal taxes, the Tax Code provides for a special surtax on

improperly accumulated income. Thus, if the IRS can demonstrate that a firm’s dividend

payout ratio is being deliberately held down to help its stockholders avoid personal taxes,

the firm is subject to heavy penalties. This factor is generally relevant only to privately

owned firms.

6. Number of profitable investment opportunities. If a firm typically has a large number

of profitable investment opportunities, this will tend to produce a low target payout ratio,

and vice versa if the firm’s profitable investment opportunities are few in number.

7. Possibility of accelerating or delaying projects. The ability to accelerate or postpone

projects will permit a firm to adhere more closely to a stable dividend policy.

8. Cost of selling new stock. If a firm needs to finance a given level of investment, it can

obtain equity by retaining earnings or by issuing new common stock. If flotation costs

(including any negative signaling effects of a stock offering) are high, ke will be well

above Ks, making it better to set a low payout ratio and to finance through retention rather

than through sales of new common stock. On the other hand, a high dividend payout ratio

is more feasible for a firm whose flotation costs are low.

Factors Determination of Dividend Policies

1. Bond Indentures. Debt contracts often limit dividend payments to earnings generated

after the loan was granted. Also, debt contracts often stipulate that no dividends can be

paid unless the current ratio, times-interest earned ratio, and other safety ratios exceed

stated minimums.

2. Preferred stock restrictions. Typically, common dividends cannot be paid if the

company has omitted its preferred dividend. The preferred average must be satisfied

before common dividends can be resumed.

3. Impairment of capital rule. Dividend payments cannot exceed the balance sheet item

“retained earnings.” This legal restriction, known as the impairment of capital rule, is

designed to protect creditors. Without the rule, a company that is in trouble might

distribute most of its assets to stockholders and leave its debt holders out in the cold.

(Liquidating dividends can be paid out of capital, but they must be indicated as such, and

they must not reduce capital below the limits stated in debt contracts.)

4. Availability of cash. Cash dividends can be paid only with cash. Thus, a shortage of cash

in the bank can restrict dividend payments. However, the ability to borrow can offset this

factor.

5. Penalty tax on improperly accumulated earnings. To prevent wealthy individuals from

using corporations to avoid personal taxes, the Tax Code provides for a special surtax on

improperly accumulated income. Thus, if the IRS can demonstrate that a firm’s dividend

payout ratio is being deliberately held down to help its stockholders avoid personal taxes,

the firm is subject to heavy penalties. This factor is generally relevant only to privately

owned firms.

6. Number of profitable investment opportunities. If a firm typically has a large number

of profitable investment opportunities, this will tend to produce a low target payout ratio,

and vice versa if the firm’s profitable investment opportunities are few in number.

7. Possibility of accelerating or delaying projects. The ability to accelerate or postpone

projects will permit a firm to adhere more closely to a stable dividend policy.

8. Cost of selling new stock. If a firm needs to finance a given level of investment, it can

obtain equity by retaining earnings or by issuing new common stock. If flotation costs

(including any negative signaling effects of a stock offering) are high, ke will be well

above Ks, making it better to set a low payout ratio and to finance through retention rather

than through sales of new common stock. On the other hand, a high dividend payout ratio

is more feasible for a firm whose flotation costs are low.

Page9

9. Flotation costs differ among firm For example, the flotation percentage is generally

higher for small firms, so they tend to set low payout ratios.

10. Ability to substitute debt for equity. A firm can finance a given level of investment

with either debt or equity. As noted above, low stock flotation costs permit a more flexible

dividend policy because equity can be raised either by retaining earnings or by selling new

stock. A similar situation holds for debt policy: If the firm can adjust its debt ratio without

raising costs sharply, it can pay the expected dividend, even if earnings fluctuate, by

increasing its debt ratio.

DETERMINANTS OF DIVIDEND POLICY

The factors determining the dividend policy of a firm are as follows:

(1) Dividend payout (D/P) ratio

(2) Stability of dividends

(3) Legal, contractual and internal constraints and restrictions

(4) Owner’s considerations

(5) Capital market considerations

(6) Inflation

(1) Dividend Payout (D/P) ratio:

The D/P ratio indicates the percentage share of the net earnings distributed to the shareholders

as dividend. Given the objective of wealth maximisation, the D/p ratio should be such can

maximise the wealth of its owners in the long run. In practice, investors, in general, have a

clear cut preference for dividends because of uncertainty and imperfect capital markets.

Therefore, a low D/P ratio may cause a decline in share prices, while a high ratio may lead to a

rise in the market price of the shares.

(2) Stability of dividends:

The second major aspect of the dividend policy of a firm is the stability of dividends. The

investors favour a stable dividend as much as they favour the payment of dividends. Dividend

stability refers to the consistency or lack of variability in the stream of dividends which means

that a certain minimum amount of dividend is paid regularly. The stability of dividends can

take any of the following three forms:

(1) Constant dividend per share

(2) Constant payout ratio

(3) Constant dividend per share plus extra dividend

(3) Legal, Contractual and Internal constraints and restrictions:

9. Flotation costs differ among firm For example, the flotation percentage is generally

higher for small firms, so they tend to set low payout ratios.

10. Ability to substitute debt for equity. A firm can finance a given level of investment

with either debt or equity. As noted above, low stock flotation costs permit a more flexible

dividend policy because equity can be raised either by retaining earnings or by selling new

stock. A similar situation holds for debt policy: If the firm can adjust its debt ratio without

raising costs sharply, it can pay the expected dividend, even if earnings fluctuate, by

increasing its debt ratio.

DETERMINANTS OF DIVIDEND POLICY

The factors determining the dividend policy of a firm are as follows:

(1) Dividend payout (D/P) ratio

(2) Stability of dividends

(3) Legal, contractual and internal constraints and restrictions

(4) Owner’s considerations

(5) Capital market considerations

(6) Inflation

(1) Dividend Payout (D/P) ratio:

The D/P ratio indicates the percentage share of the net earnings distributed to the shareholders

as dividend. Given the objective of wealth maximisation, the D/p ratio should be such can

maximise the wealth of its owners in the long run. In practice, investors, in general, have a

clear cut preference for dividends because of uncertainty and imperfect capital markets.

Therefore, a low D/P ratio may cause a decline in share prices, while a high ratio may lead to a

rise in the market price of the shares.

(2) Stability of dividends:

The second major aspect of the dividend policy of a firm is the stability of dividends. The

investors favour a stable dividend as much as they favour the payment of dividends. Dividend

stability refers to the consistency or lack of variability in the stream of dividends which means

that a certain minimum amount of dividend is paid regularly. The stability of dividends can

take any of the following three forms:

(1) Constant dividend per share

(2) Constant payout ratio

(3) Constant dividend per share plus extra dividend

(3) Legal, Contractual and Internal constraints and restrictions:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page10

The dividend decision is also affected by certain legal, contractual and internal constraints.

The legal factor stem from certain statutory requirements, the contractual restrictions arise

from certain loan covenants and the internal constraints are the result of the firm’s liquidity

positions.

(4) Owner’s considerations:

The dividend policy is also likely to be affected by the owner’s considerations of

(a) the tax status of the shareholders, (b) their opportunities of investment, and (c) the dilution

of ownership. It is impossible to establish a policy that will maximise each owner’s wealth.

The firm must aim at a dividend policy which has a beneficial effect on the wealth of the

majority of shareholders.

(5) Capital Market Considerations:

Another set of factors that can strongly affect dividend policy is the extent to which the firm

has access to the capital markets. A firm which has easy access to the capital market can follow

a liberal dividend policy, whereas a firm having only limited access to the capital markets is

likely to adopt low dividend payout ratio as they are likely to rely, to a greater extent, on

retained earnings as a source of financing their investments.

(6) Inflation:

Inflation is another factor which affects the firm’s dividend decisions. With rising prices, funds

generated from depreciation may be inadequate to replace obsolete equipments. As a result D/P

ratio tends to be low during period of inflation.

Dividend Theories and Behaviour

a) Irrelevance of Dividend

MM Approach

b) Relevance of Dividend

Walter’s Model

Gordon’s Model

(A) RELEVANCE OF DIVIDENDS

In sharp contrast to the MM hypothesis, there are some theories that consider dividend

decisions to be an active variable in determining the value of the firm. The dividend decision is

therefore relevant. According to this concept, dividend policy is considered to affect the value

of the firm. Dividend relevance implies that shareholders prefer current dividend and there is

no direct relationship between dividend policy and the value of the firm. There are two theories

which support the relevance of dividends namely:

The dividend decision is also affected by certain legal, contractual and internal constraints.

The legal factor stem from certain statutory requirements, the contractual restrictions arise

from certain loan covenants and the internal constraints are the result of the firm’s liquidity

positions.

(4) Owner’s considerations:

The dividend policy is also likely to be affected by the owner’s considerations of

(a) the tax status of the shareholders, (b) their opportunities of investment, and (c) the dilution

of ownership. It is impossible to establish a policy that will maximise each owner’s wealth.

The firm must aim at a dividend policy which has a beneficial effect on the wealth of the

majority of shareholders.

(5) Capital Market Considerations:

Another set of factors that can strongly affect dividend policy is the extent to which the firm

has access to the capital markets. A firm which has easy access to the capital market can follow

a liberal dividend policy, whereas a firm having only limited access to the capital markets is

likely to adopt low dividend payout ratio as they are likely to rely, to a greater extent, on

retained earnings as a source of financing their investments.

(6) Inflation:

Inflation is another factor which affects the firm’s dividend decisions. With rising prices, funds

generated from depreciation may be inadequate to replace obsolete equipments. As a result D/P

ratio tends to be low during period of inflation.

Dividend Theories and Behaviour

a) Irrelevance of Dividend

MM Approach

b) Relevance of Dividend

Walter’s Model

Gordon’s Model

(A) RELEVANCE OF DIVIDENDS

In sharp contrast to the MM hypothesis, there are some theories that consider dividend

decisions to be an active variable in determining the value of the firm. The dividend decision is

therefore relevant. According to this concept, dividend policy is considered to affect the value

of the firm. Dividend relevance implies that shareholders prefer current dividend and there is

no direct relationship between dividend policy and the value of the firm. There are two theories

which support the relevance of dividends namely:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page11

(i) WALTER’S MODEL

(ii) GORDON’S MODEL

(i) WALTER’S MODEL

Prof. James E. Walter argues that the dividend policy almost always affects the value

of the firm. This model supports the doctrine that dividends are relevant. The investment policy

of a firm cannot be separated from its dividend policy and both are interlinked. The key

argument in support of the relevance of Walter’s model is the relationship between the return

on a firm’s investment (r) and its cost of capital/ required rate of return (k).

If r > k ( growth firms) the firm should retain the earnings or D/P ratio should be zero as it is

able to earn higher than what the shareholders could by investing on their own.

In case r < k (declining firms) it implies that shareholders can earn a higher return by

investing elsewhere. Therefore, the entire earnings (D/P ratio should be 100 percent) should be

distributed to them.

Finally, when r = k (normal firms), it is a matter of indifference whether earnings are

retained or distributed. This is so because for all D/P ratios (ranging between zero and 100) the

market price of shares will remain constant. For such firms, there is no optimum dividend

policy (D/P ratio). By following such a policy in all the three cases, the market price of shares

will be maximised.Walter model is based on the relationship between the following important

factors:

Rate of return I

Cost of capital (k)

According to the Walter’s model, if r > k, the firm is able to earn more than what the

shareholders could by reinvesting, if the earnings are paid to them. The implication of r > k is

that the shareholders can earn a higher return by investing elsewhere. If the firm has r = k, it is

a matter of indifference whether earnings are retained or distributed.

Assumptions

Walters model is based on the following important assumptions:

The firm uses only internal finance.

The firm does not use debt or equity finance.

The firm has constant return and cost of capital.

The firm has 100 recent payout.

The firm has constant EPS and dividend.

The firm has a very long life.

Walter has evolved a mathematical formula for determining the value of market share.

(i) WALTER’S MODEL

(ii) GORDON’S MODEL

(i) WALTER’S MODEL

Prof. James E. Walter argues that the dividend policy almost always affects the value

of the firm. This model supports the doctrine that dividends are relevant. The investment policy

of a firm cannot be separated from its dividend policy and both are interlinked. The key

argument in support of the relevance of Walter’s model is the relationship between the return

on a firm’s investment (r) and its cost of capital/ required rate of return (k).

If r > k ( growth firms) the firm should retain the earnings or D/P ratio should be zero as it is

able to earn higher than what the shareholders could by investing on their own.

In case r < k (declining firms) it implies that shareholders can earn a higher return by

investing elsewhere. Therefore, the entire earnings (D/P ratio should be 100 percent) should be

distributed to them.

Finally, when r = k (normal firms), it is a matter of indifference whether earnings are

retained or distributed. This is so because for all D/P ratios (ranging between zero and 100) the

market price of shares will remain constant. For such firms, there is no optimum dividend

policy (D/P ratio). By following such a policy in all the three cases, the market price of shares

will be maximised.Walter model is based on the relationship between the following important

factors:

Rate of return I

Cost of capital (k)

According to the Walter’s model, if r > k, the firm is able to earn more than what the

shareholders could by reinvesting, if the earnings are paid to them. The implication of r > k is

that the shareholders can earn a higher return by investing elsewhere. If the firm has r = k, it is

a matter of indifference whether earnings are retained or distributed.

Assumptions

Walters model is based on the following important assumptions:

The firm uses only internal finance.

The firm does not use debt or equity finance.

The firm has constant return and cost of capital.

The firm has 100 recent payout.

The firm has constant EPS and dividend.

The firm has a very long life.

Walter has evolved a mathematical formula for determining the value of market share.

Page12

P = (D + (r /Ke) (E-D))

Ke

Where,

P = Market price of an equity share;

D = Dividend per share;

r = Internal rate of return

E = Earning per share;

Ke = Cost of equity capital

Exercise 2

From the following information supplied to you, ascertain whether the firm is following

an optional dividend policy as per Walter’s Model?

Total Earnings 2,00,000

No. of equity shares (of 100 each 20,000)

Dividend paid 1,00,000

P/E Ratio 10

Return Investment 15%

The firm is expected to maintain its rate of return on fresh investments. Also find out

what should be the E/P ratio at which the dividend policy will have no effect on the value of

the share? Will your decision change if the P/E ratio is 7.25 and interest of 10%?

Solution

EPS = Earnings

No.of shares

= 200, 000

20,000 = 10.

PE ratio = 10

Ke = 1

PE ratio = 1 / 10 = 0.10

DPS = Total dividend paid / no of shares

= 100,000 / 20,000 = 5.

The value of the share as per Walter’s Model is

P = (D + (r /Ke) (E-D)) / Ke

= (5 + 0.15 / 0.10 (10 – 5)) / 0.10

= 5 + 7.5 / 0.10 = 12.5

P = (D + (r /Ke) (E-D))

Ke

Where,

P = Market price of an equity share;

D = Dividend per share;

r = Internal rate of return

E = Earning per share;

Ke = Cost of equity capital

Exercise 2

From the following information supplied to you, ascertain whether the firm is following

an optional dividend policy as per Walter’s Model?

Total Earnings 2,00,000

No. of equity shares (of 100 each 20,000)

Dividend paid 1,00,000

P/E Ratio 10

Return Investment 15%

The firm is expected to maintain its rate of return on fresh investments. Also find out

what should be the E/P ratio at which the dividend policy will have no effect on the value of

the share? Will your decision change if the P/E ratio is 7.25 and interest of 10%?

Solution

EPS = Earnings

No.of shares

= 200, 000

20,000 = 10.

PE ratio = 10

Ke = 1

PE ratio = 1 / 10 = 0.10

DPS = Total dividend paid / no of shares

= 100,000 / 20,000 = 5.

The value of the share as per Walter’s Model is

P = (D + (r /Ke) (E-D)) / Ke

= (5 + 0.15 / 0.10 (10 – 5)) / 0.10

= 5 + 7.5 / 0.10 = 12.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.