Dividends and Share Repurchases: Forms, Payment, and Analysis

VerifiedAdded on 2021/10/04

|20

|1829

|62

Report

AI Summary

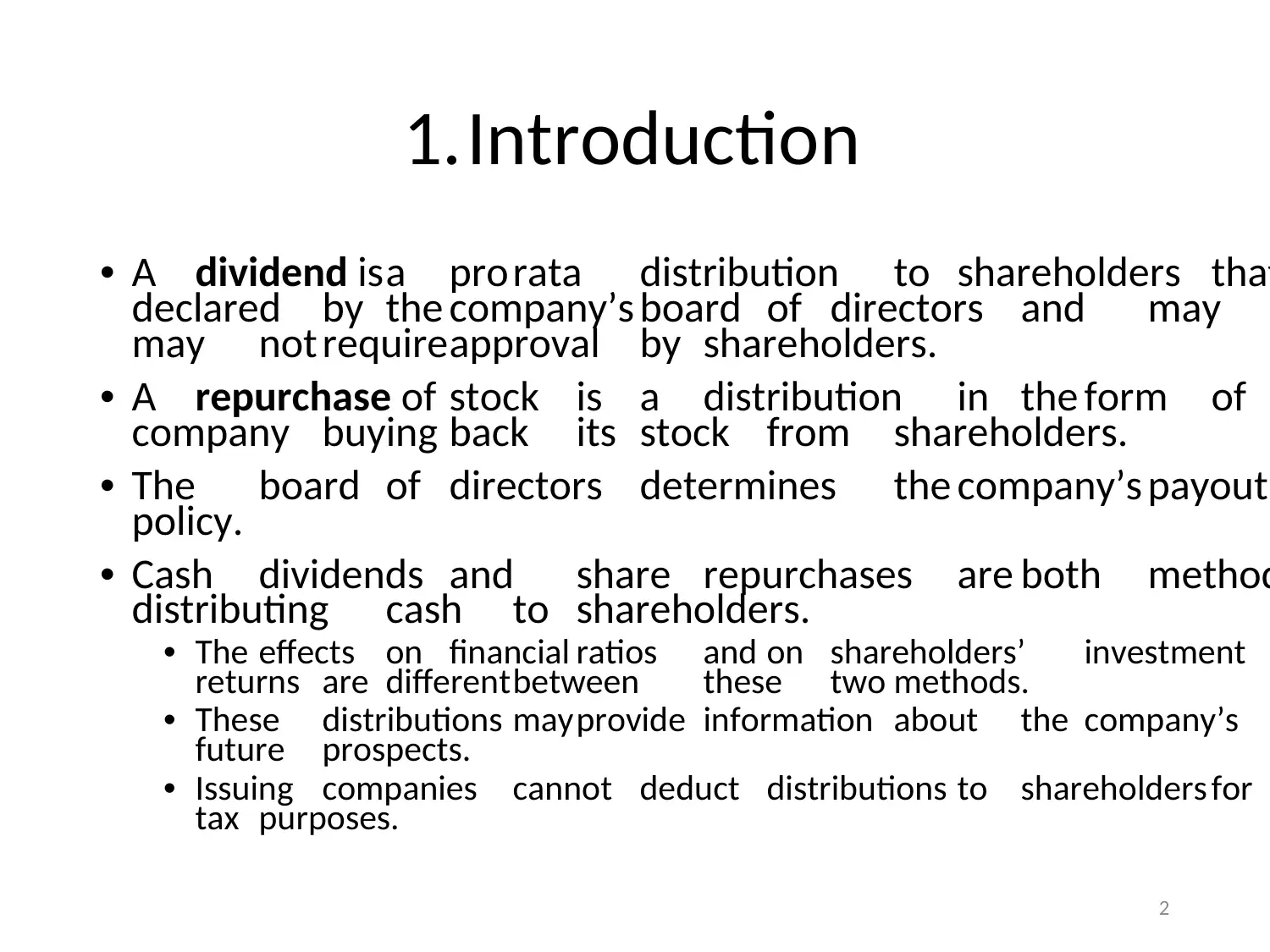

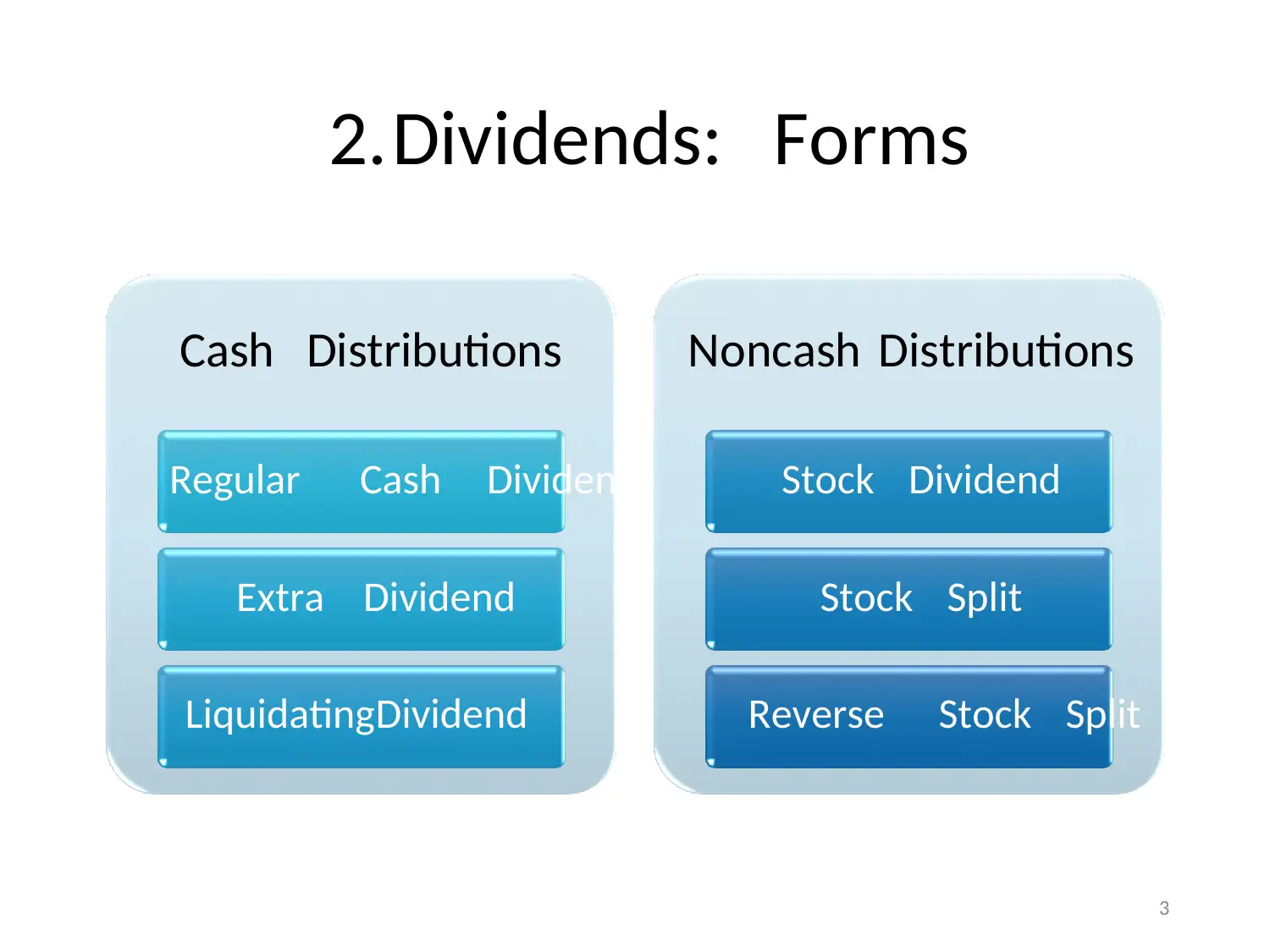

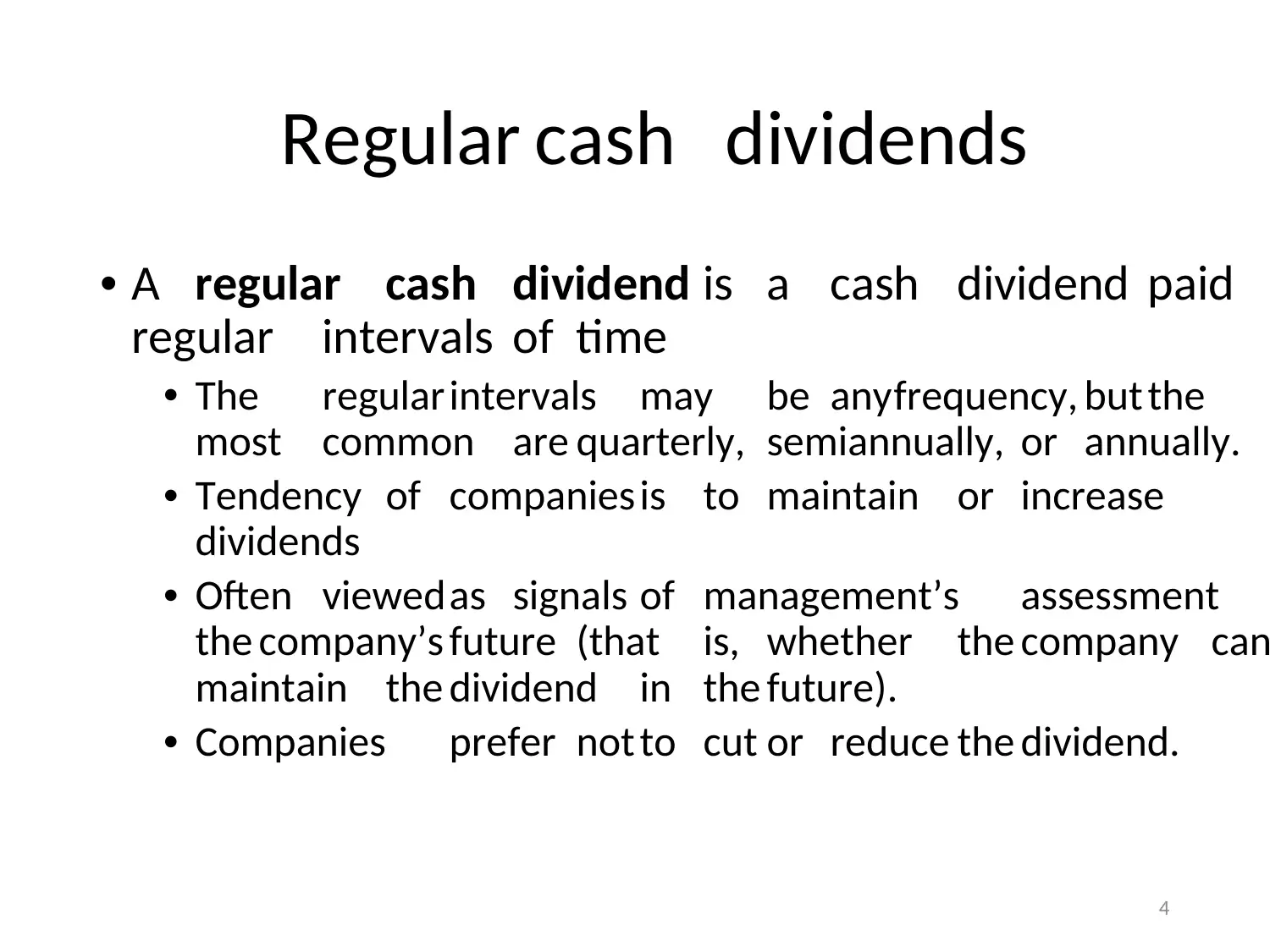

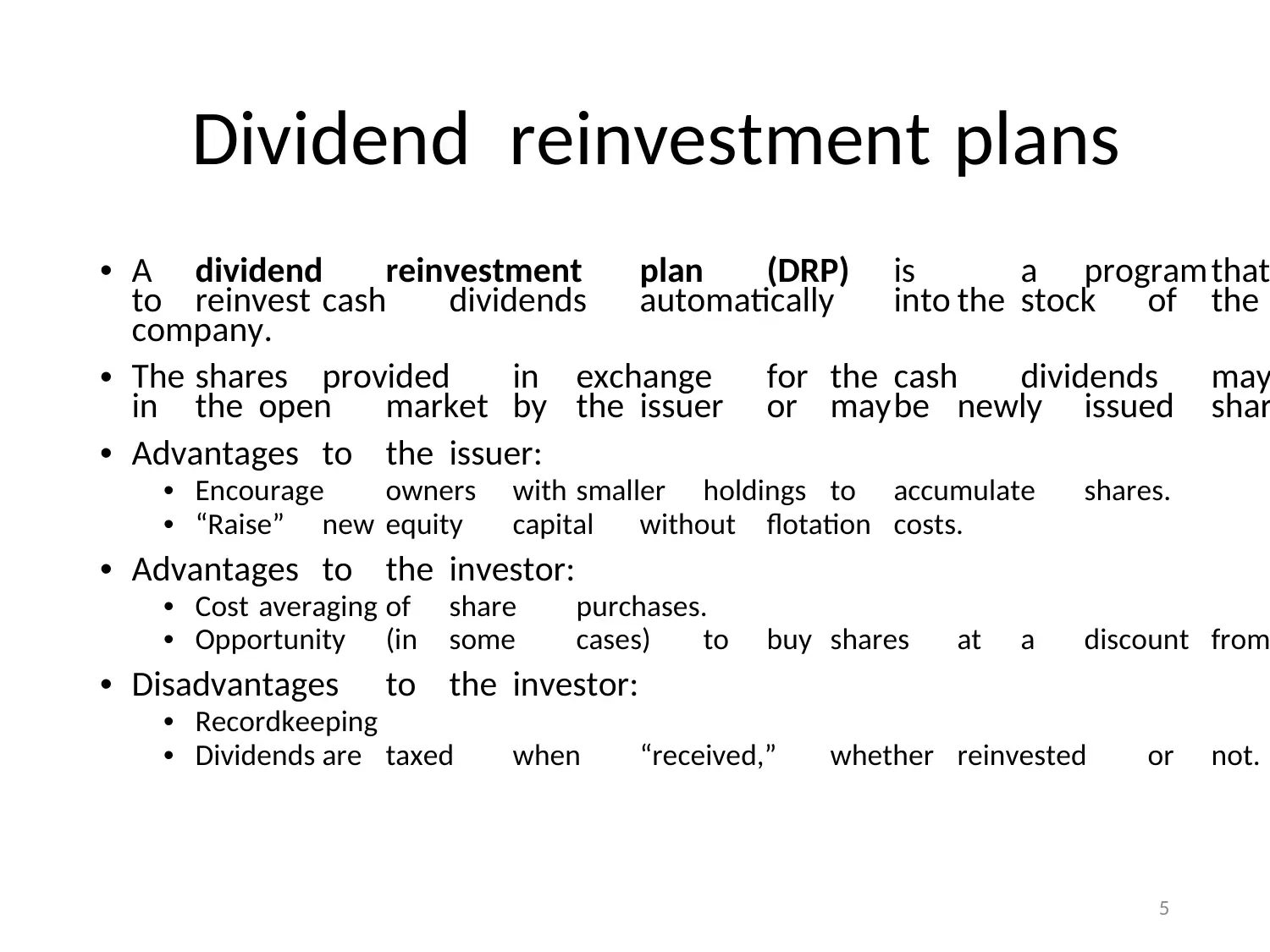

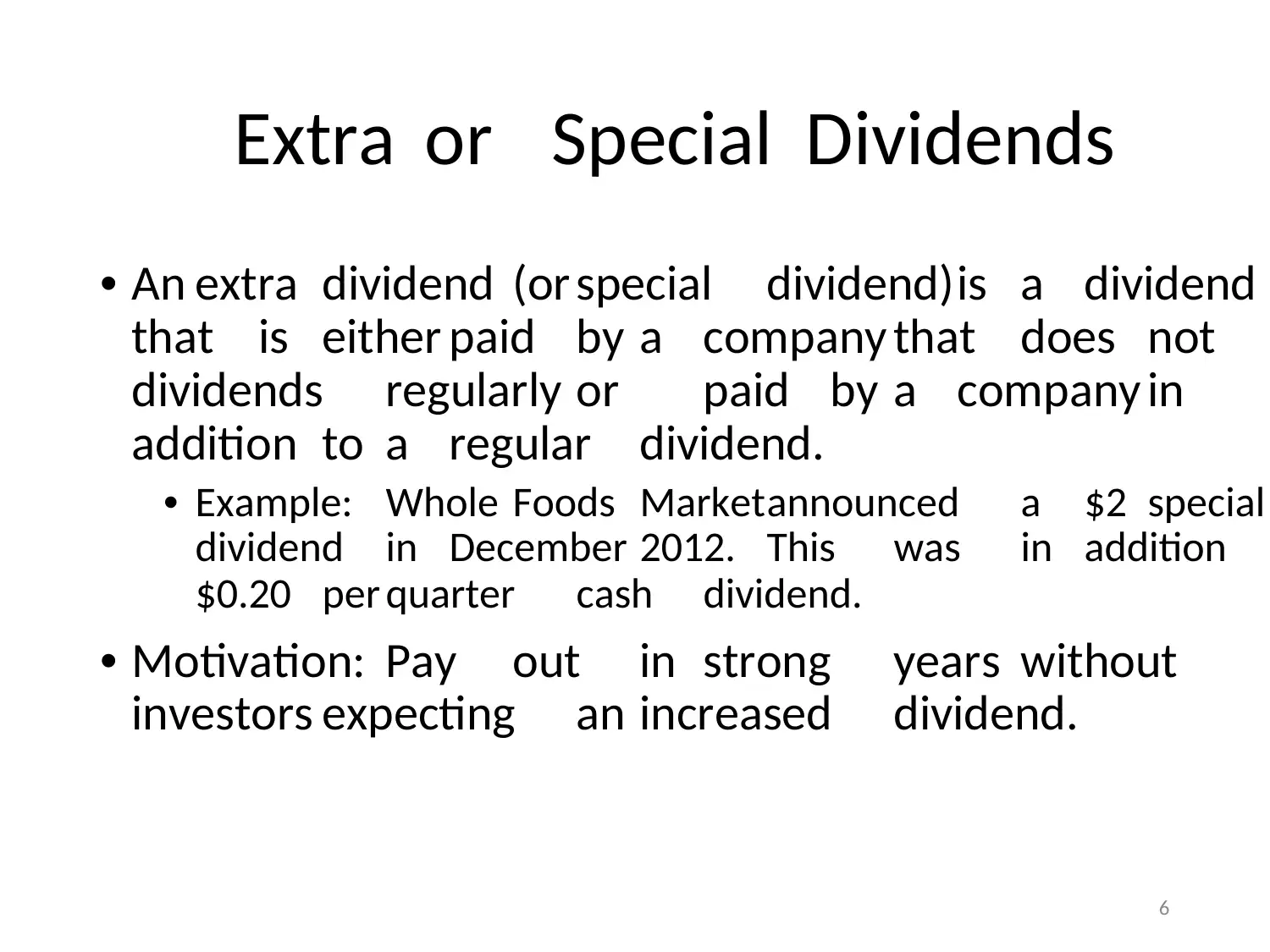

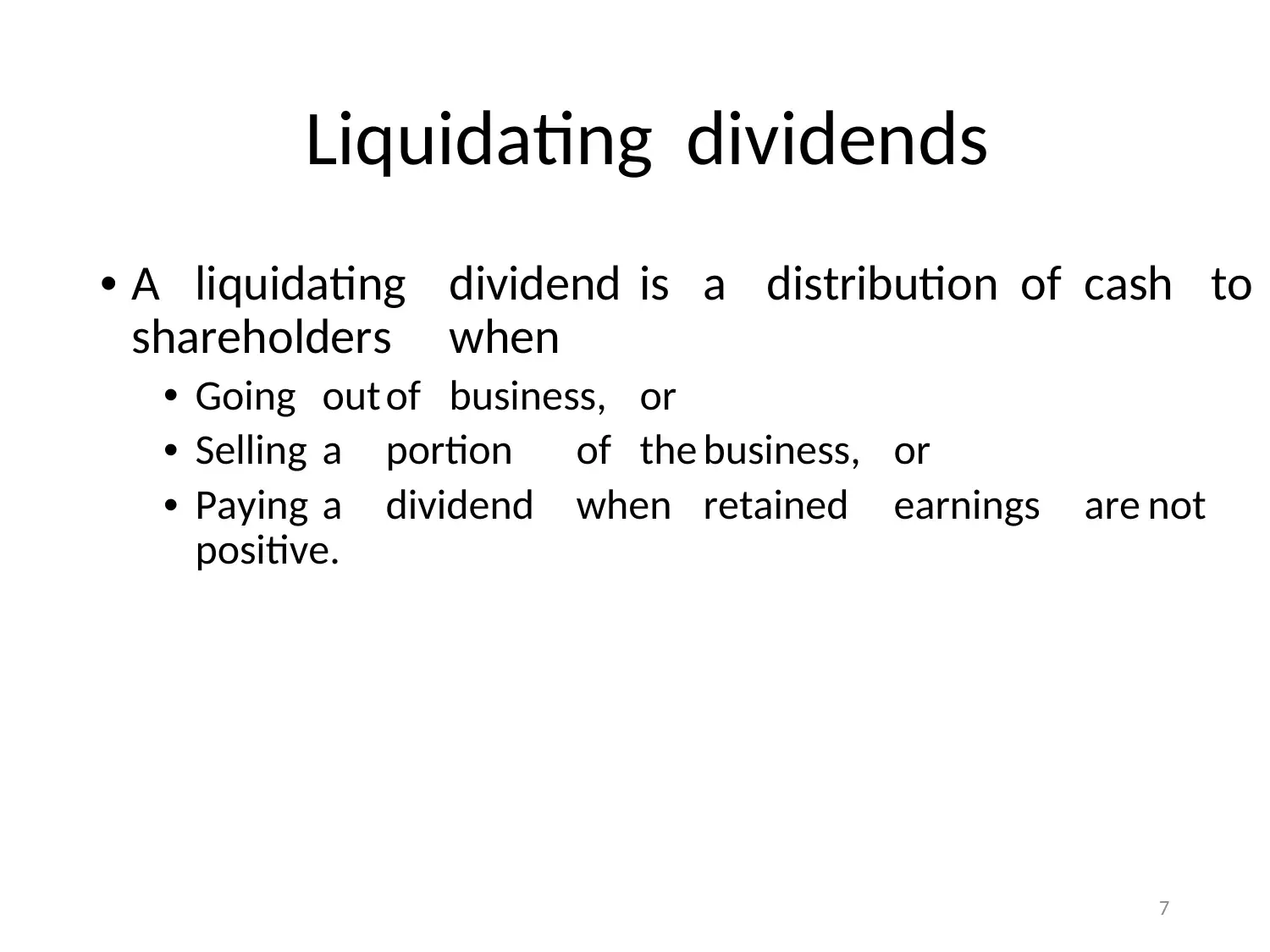

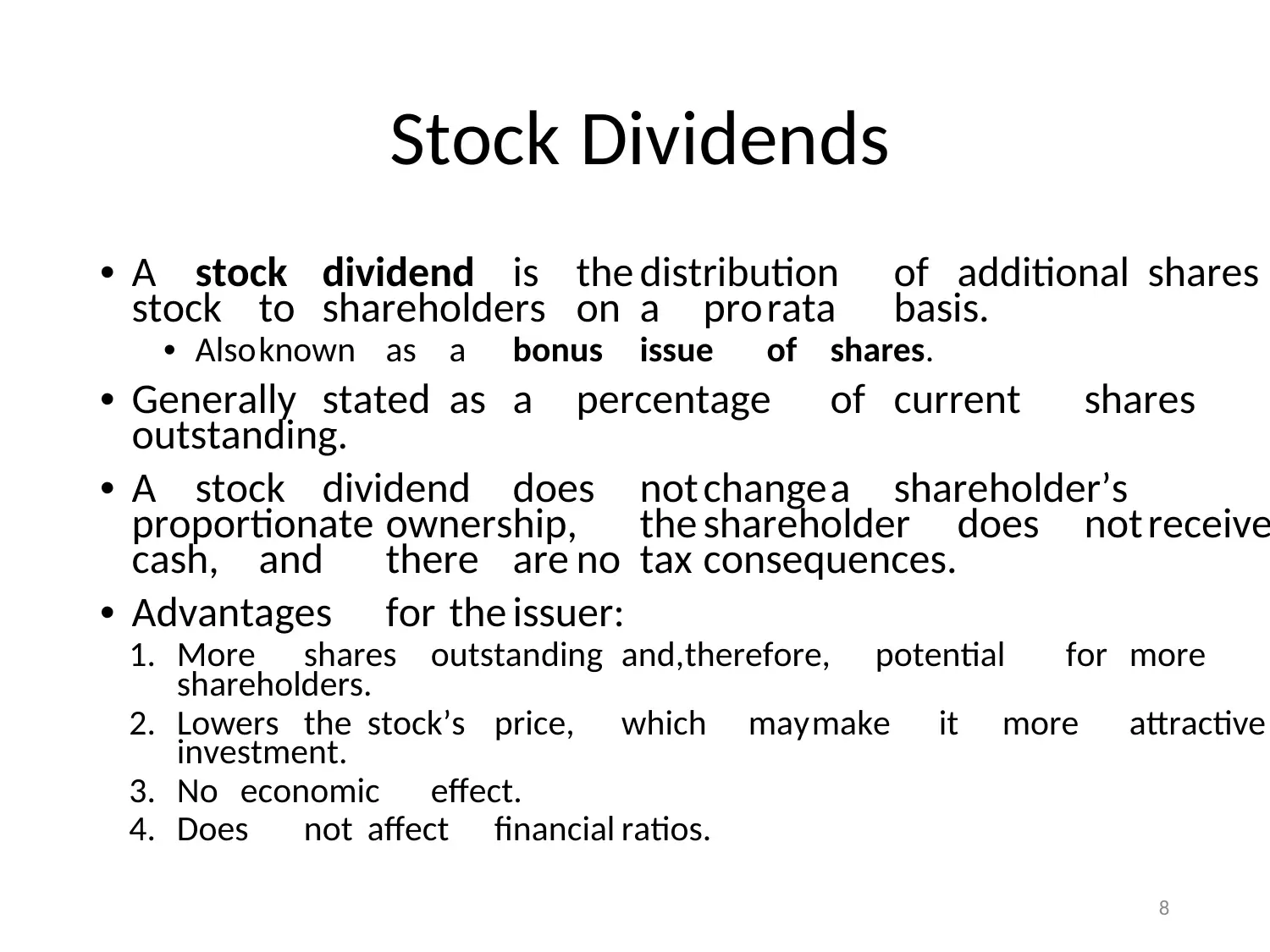

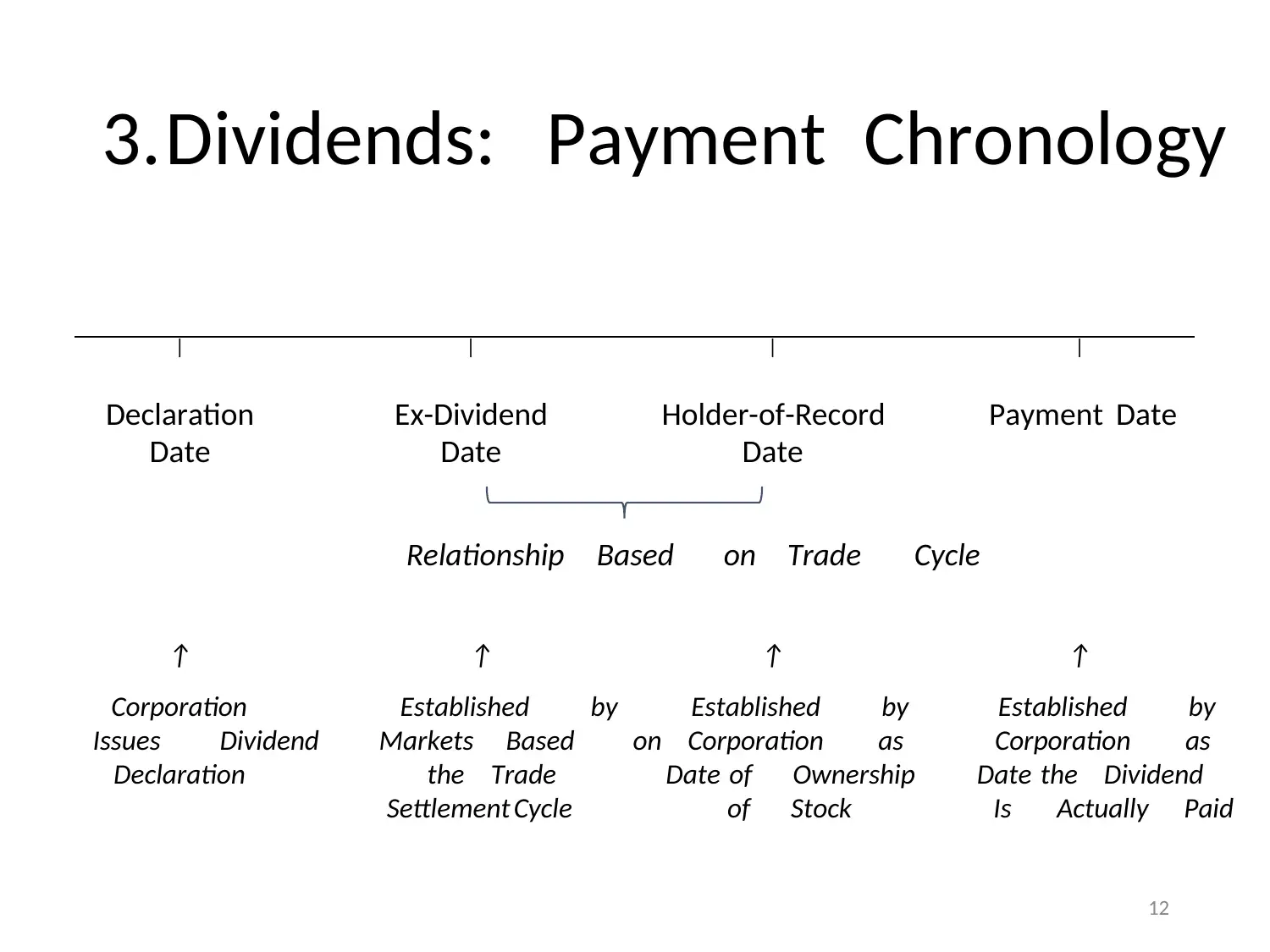

This report provides a comprehensive overview of dividends and share repurchases, crucial financial strategies for distributing value to shareholders. It begins by defining dividends, which can be cash or noncash distributions, including regular, extra, and liquidating dividends, as well as stock dividends and stock splits. The report then explores dividend reinvestment plans and the payment chronology, including declaration, ex-dividend, holder-of-record, and payment dates. The report also details share repurchases, or buybacks, including methods such as open market purchases, tender offers, and direct negotiations, and analyzes their impact on earnings per share and book value per share. The report concludes by comparing share repurchases and cash dividends, highlighting that they provide the same cash flow to investors. The report emphasizes that announcements of share repurchases and dividend initiations often signal positive market sentiment, and the key takeaway is that both dividends and share repurchases are essential tools for financial management, each with its own implications for shareholder value and company strategy.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.