Management Accounting Report: Analysis of Divine Denim Case Study

VerifiedAdded on 2022/09/18

|13

|1850

|42

Report

AI Summary

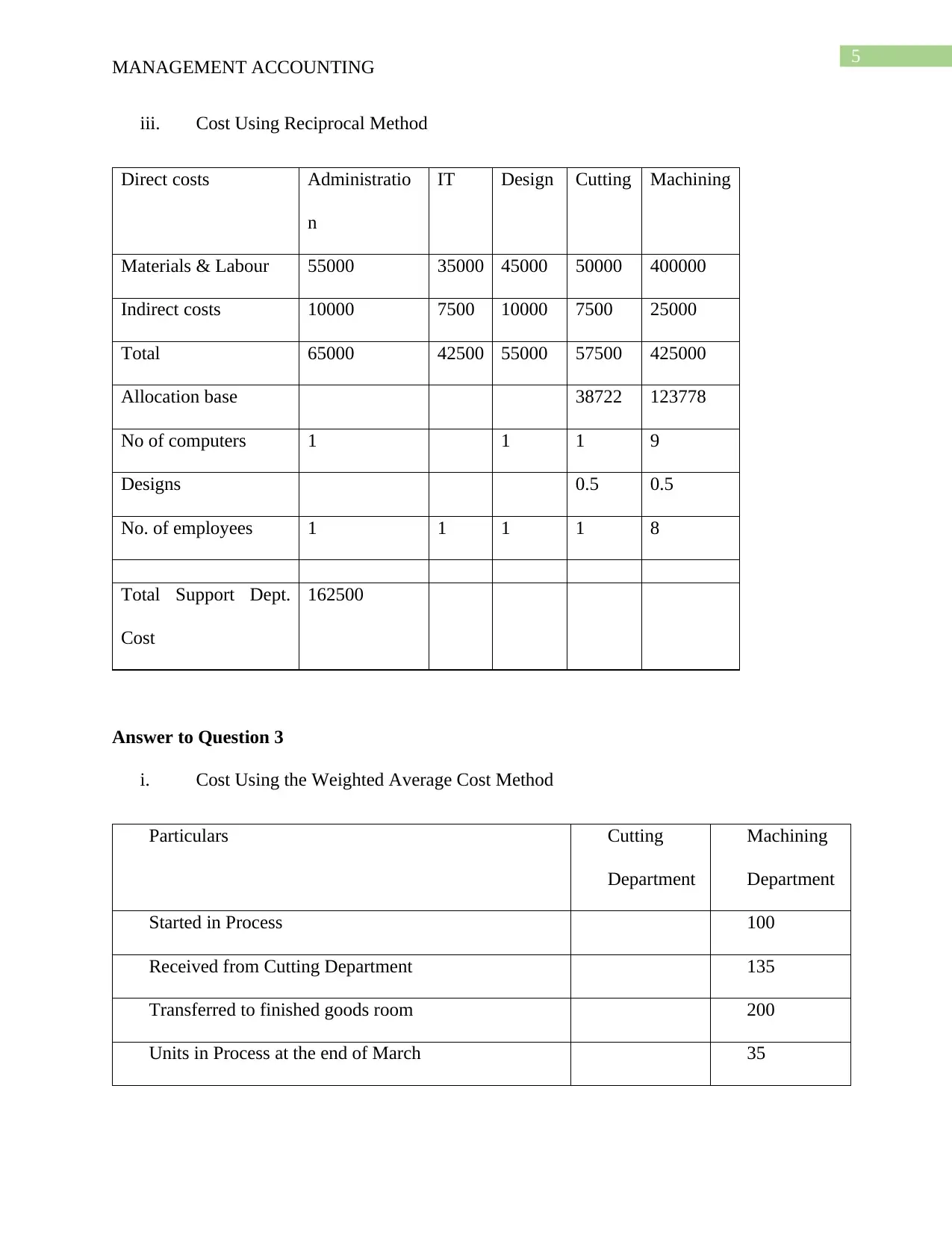

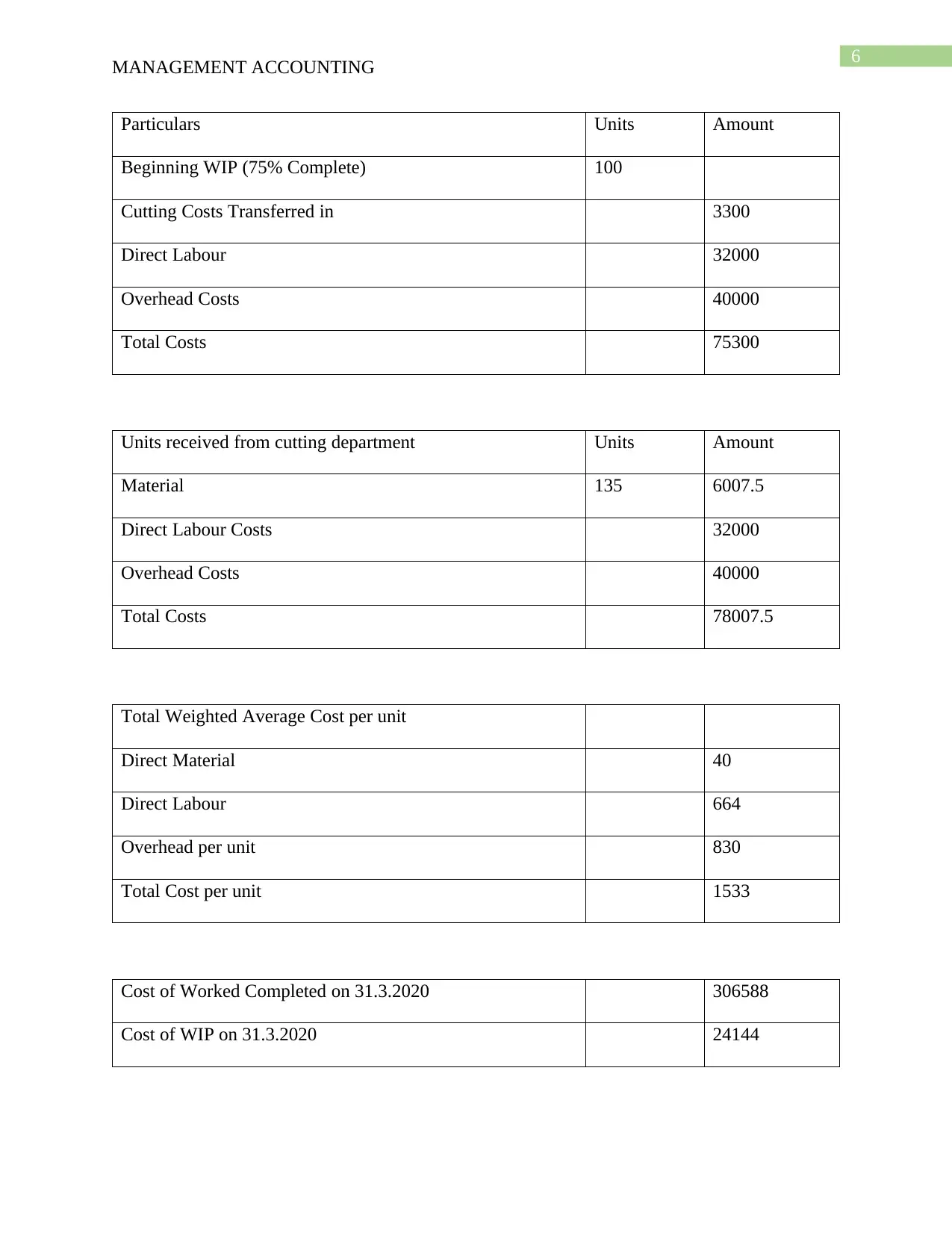

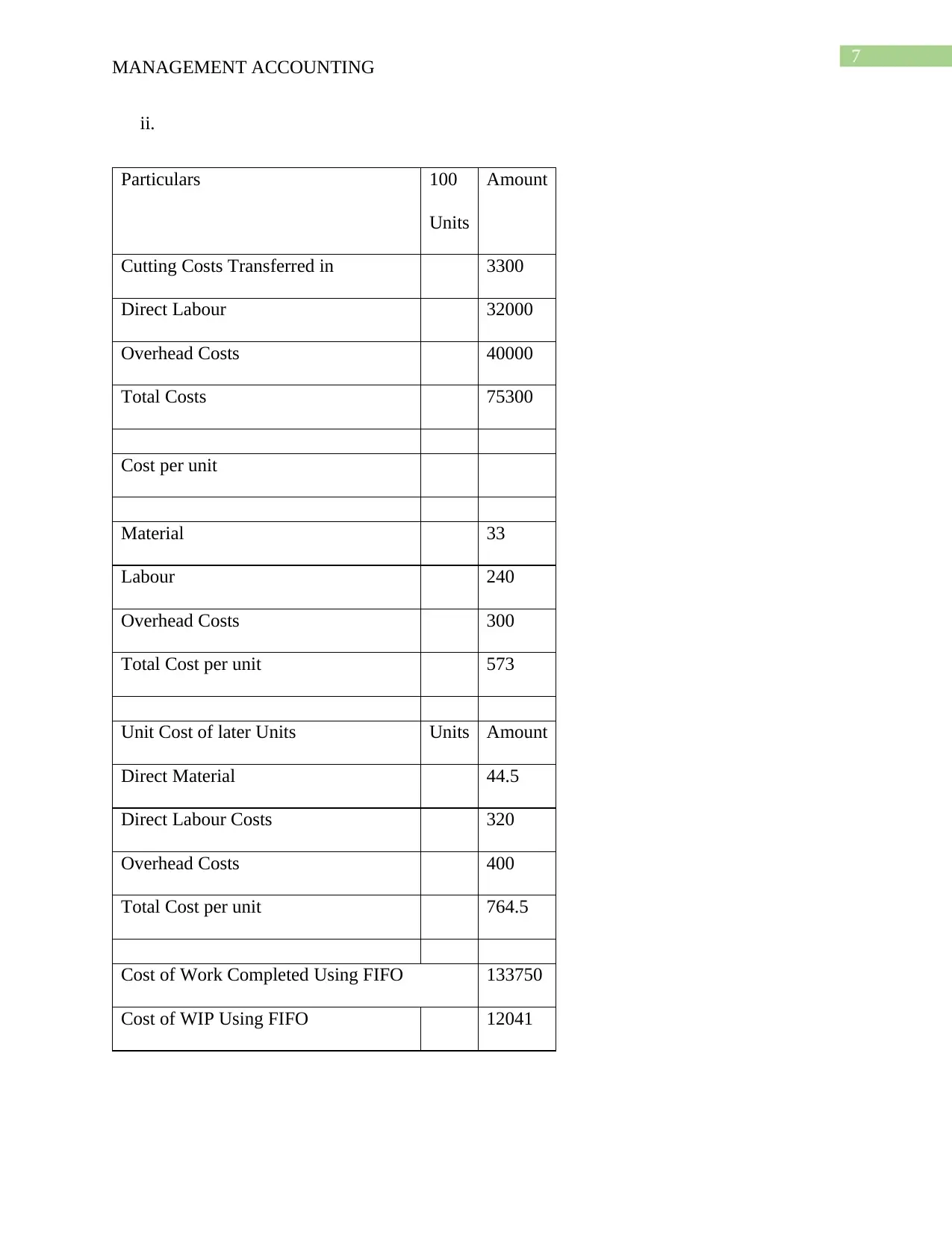

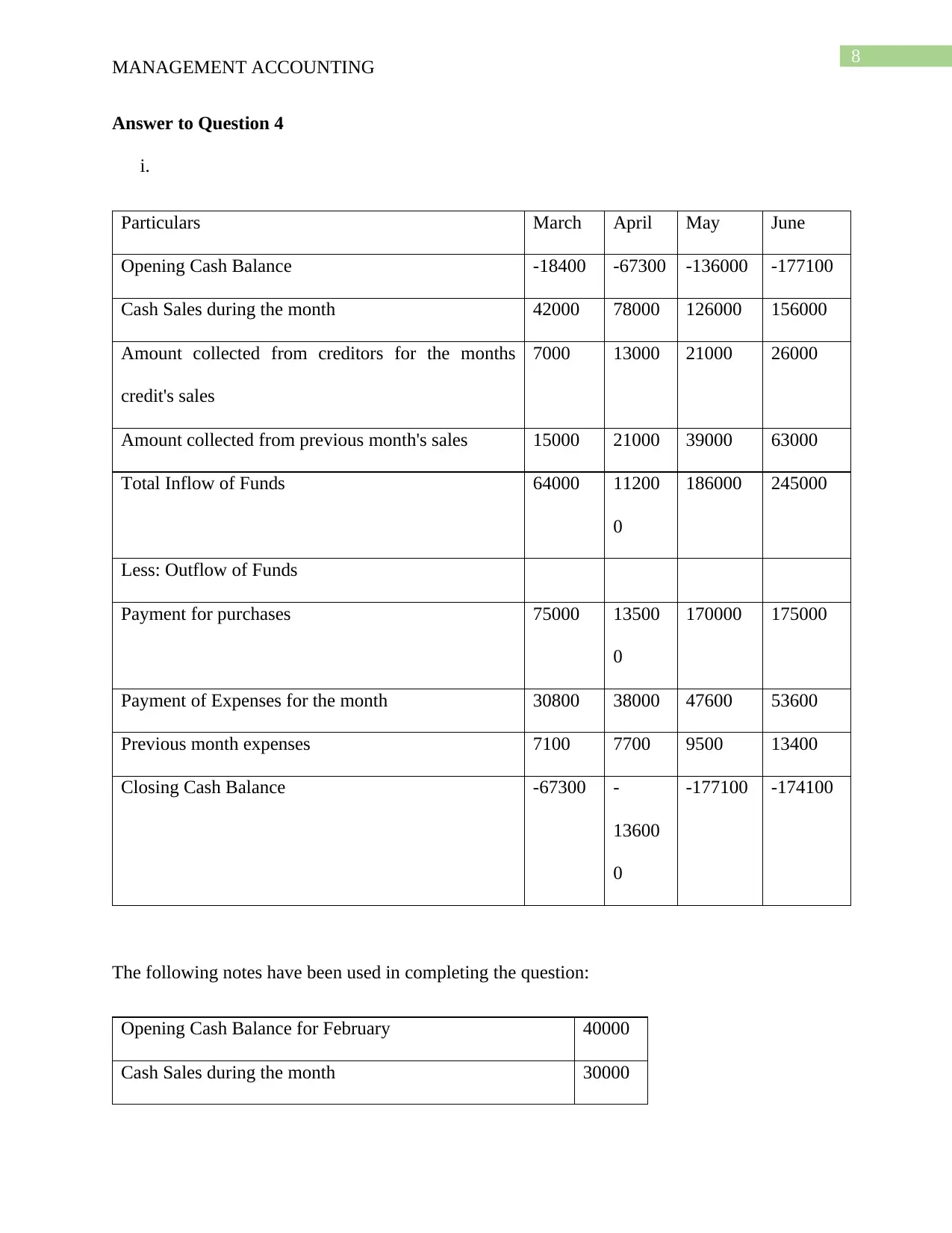

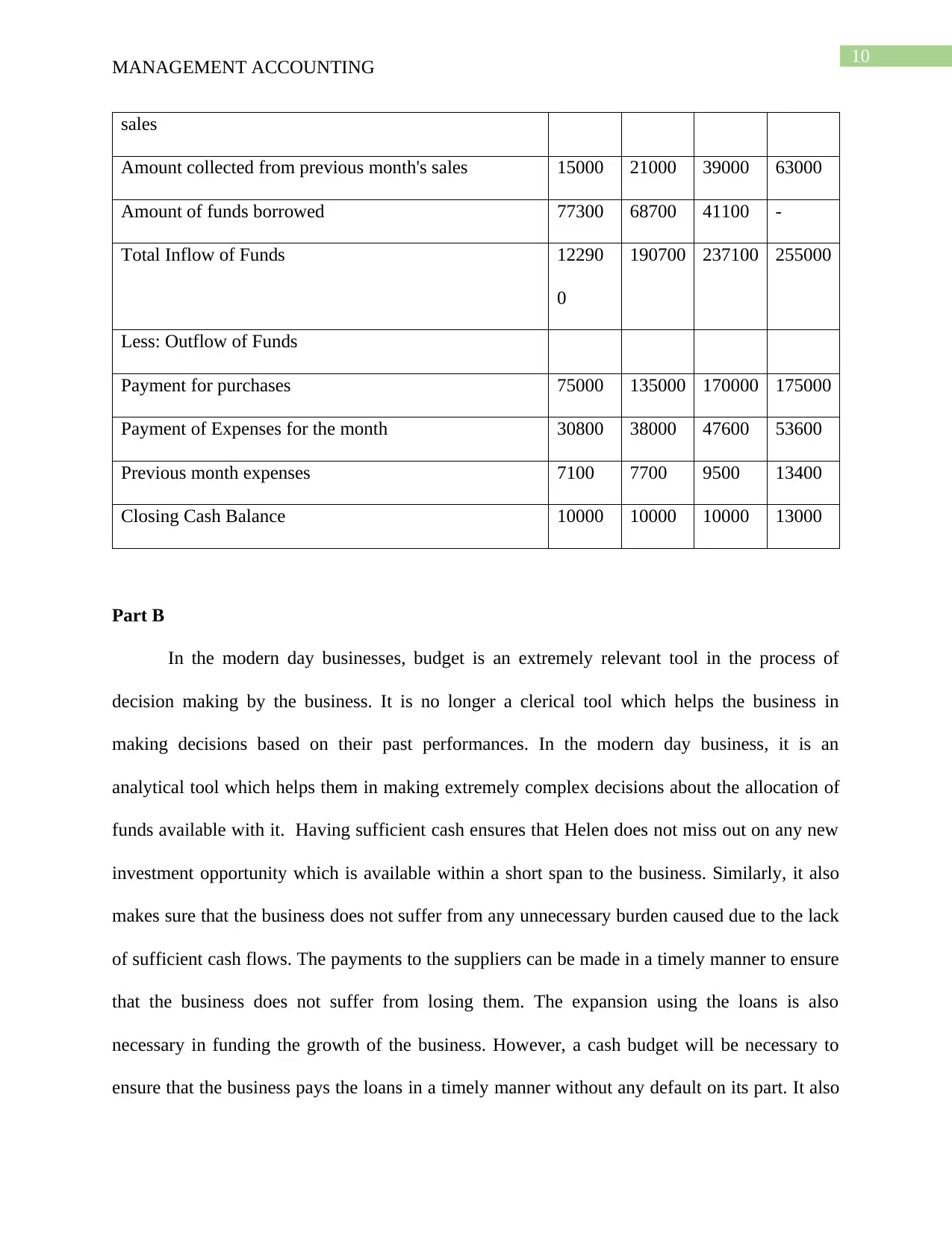

This report presents a comprehensive analysis of the Divine Denim case study, a growing company specializing in made-to-measure and ready-to-wear denim clothing. The report begins with an application of Porter's Five Forces to assess the competitive landscape, differentiating between the made-to-measure and ready-to-wear segments. It then delves into cost allocation methods, including direct, step-down, and reciprocal methods, to determine departmental costs. The report further examines cost accounting using the weighted average cost method to calculate unit costs and work-in-progress valuation. Finally, it analyzes cash flow projections, identifies potential financial challenges, and recommends strategies to improve cash management through borrowing and budgeting, highlighting the importance of budgets in business decision-making. The analysis aims to provide insights into the financial and strategic challenges faced by Divine Denim and propose solutions for sustainable growth.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.